Comparison of Managerial Accounting Techniques

VerifiedAdded on 2022/12/30

|9

|1561

|1

AI Summary

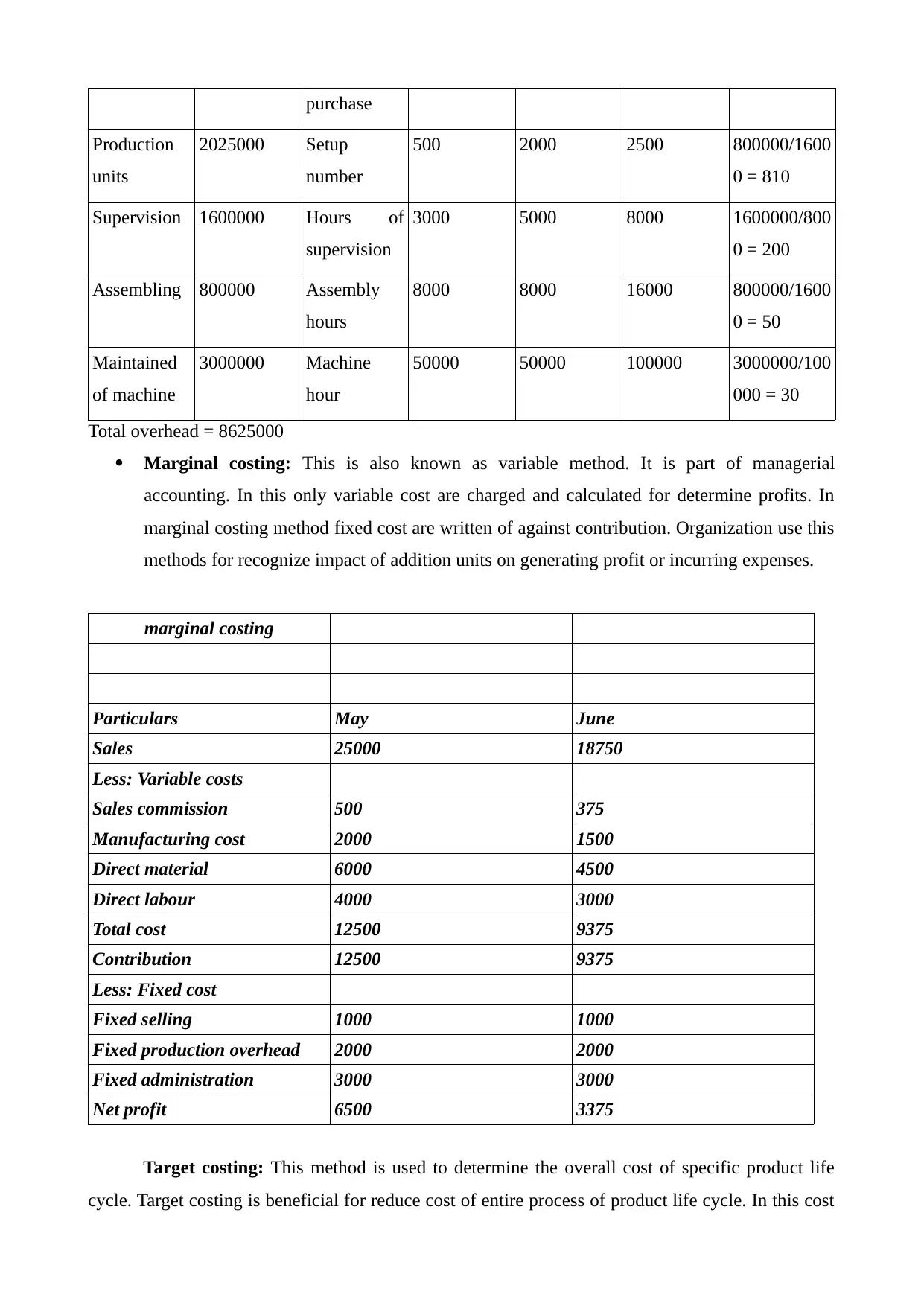

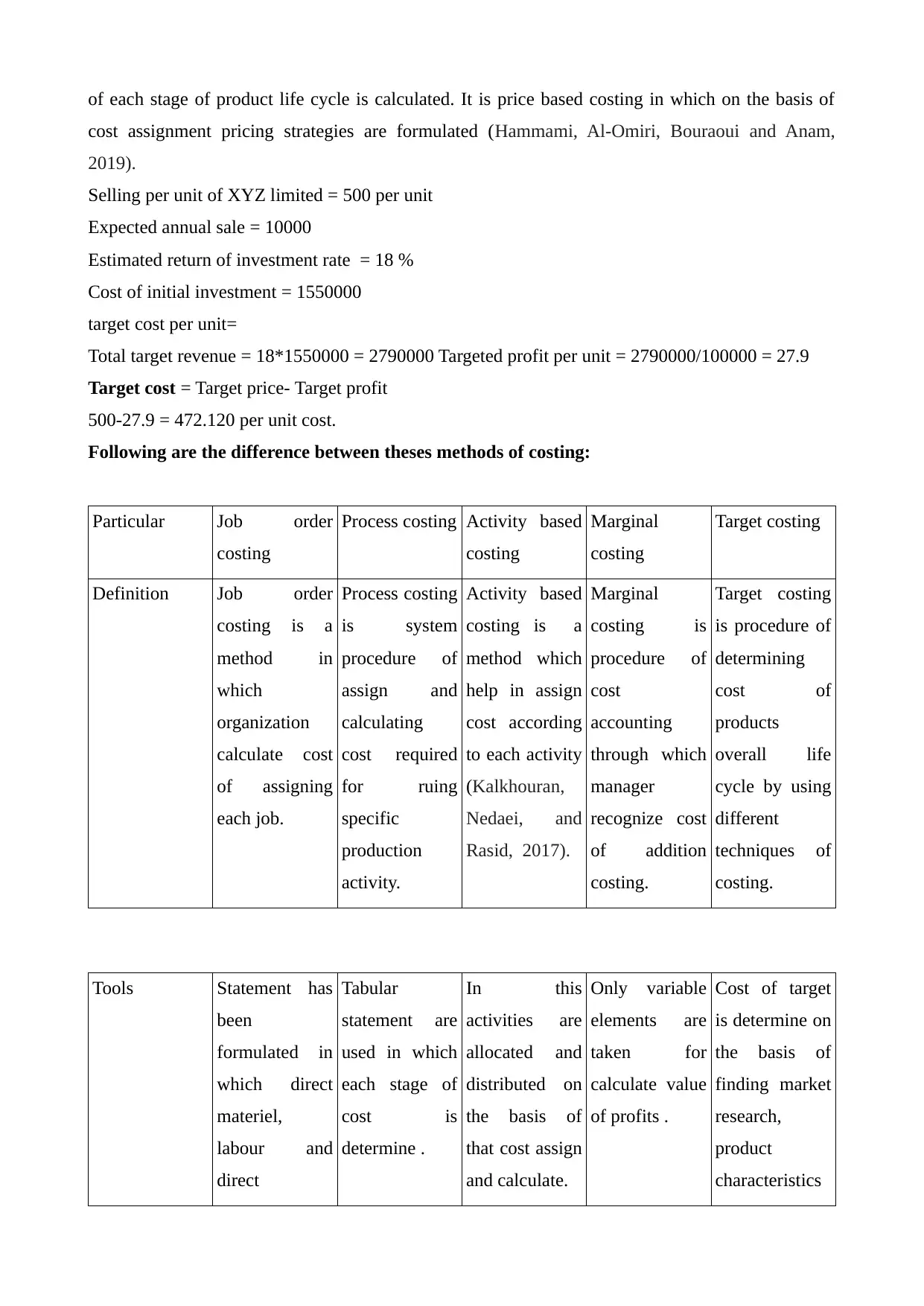

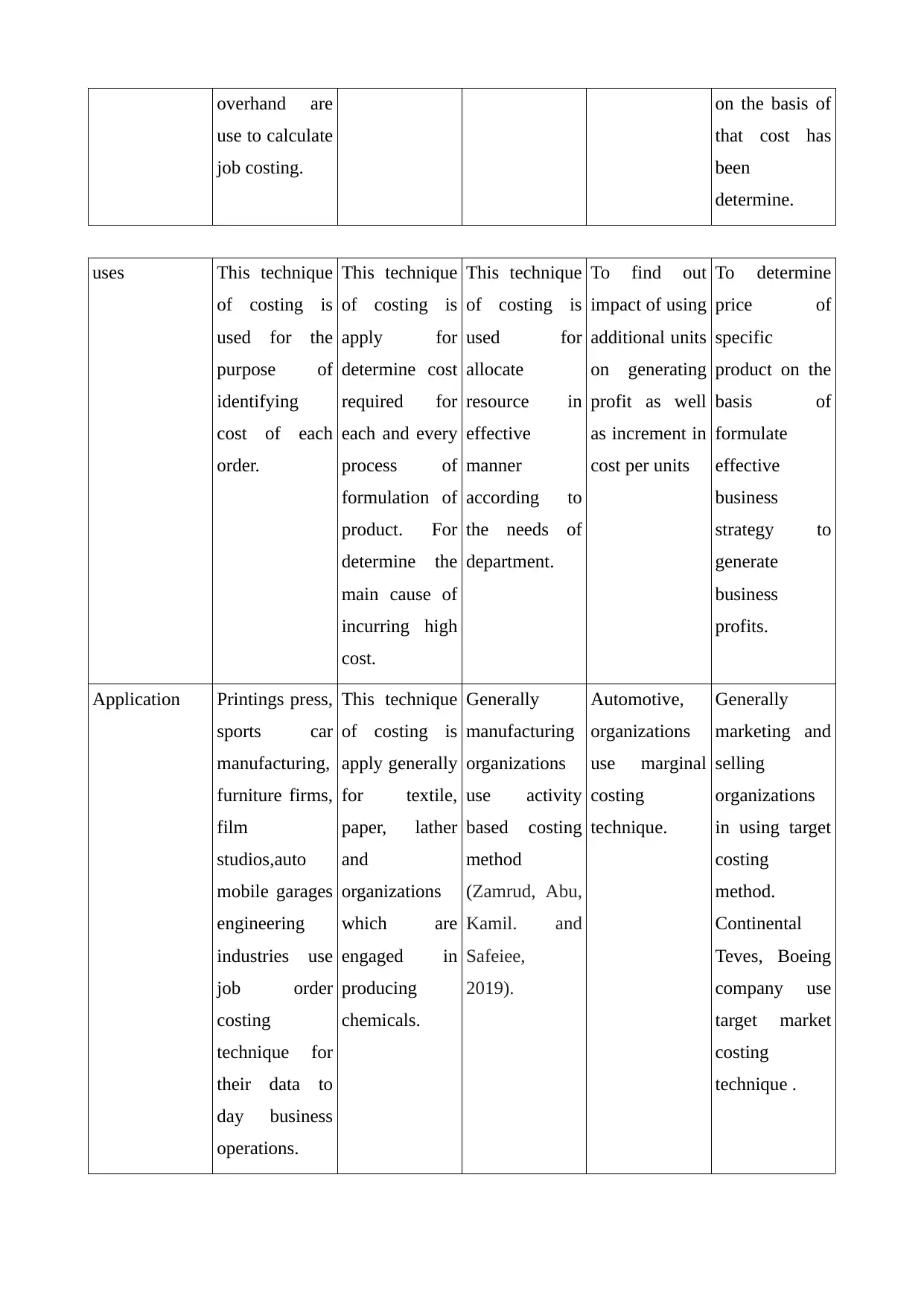

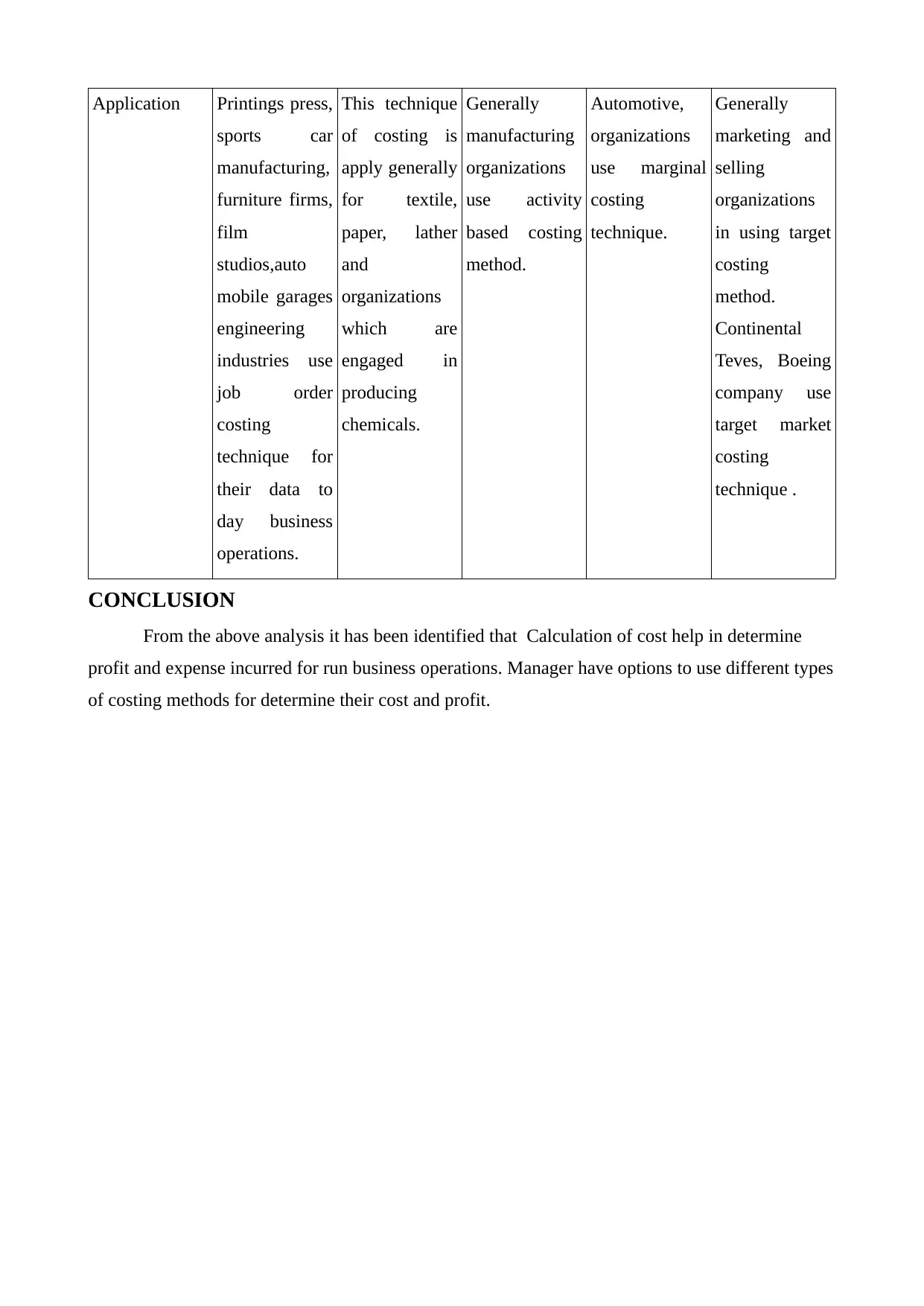

This report compares and contrasts different types of managerial accounting techniques such as job order costing, process costing, activity-based costing, marginal costing, and target costing. It discusses the definition, application, and characteristics of each method, as well as their advantages and disadvantages. The report also provides examples and calculations to illustrate how each method is used in practice. Overall, it highlights the importance of cost calculation in determining profits and expenses for businesses.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.