University Costing Methods Assignment: Financial Accounting Analysis

VerifiedAdded on 2023/03/20

|11

|2028

|60

Homework Assignment

AI Summary

This assignment solution delves into various costing methods, providing a comprehensive analysis of financial accounting principles. The document covers key concepts such as variable costing, absorption costing, standard costing, and flexible budgeting. It explores overhead cost allocation, the impact of different costing techniques on profit and loss statements, and the importance of choosing appropriate costing methods for decision-making. The solution includes calculations, memos, and letters demonstrating practical application of these concepts. The assignment addresses scenarios involving hiring decisions, outsourcing, and the development of chemical products, offering a practical perspective on cost management within different business contexts. The student's work provides a detailed overview of how costing methods are applied in real-world business situations, highlighting the financial implications of each method.

Running Head: COSTING METHOD 1

COSTING METHODS

COSTING METHODS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: COSTING METHOD

Table of Contents

Question 1........................................................................................................................................3

Part 3............................................................................................................................................3

Part 4............................................................................................................................................3

Question 2........................................................................................................................................3

Part 2............................................................................................................................................3

Part 4............................................................................................................................................3

Question 3........................................................................................................................................4

PART 5........................................................................................................................................4

Question 4........................................................................................................................................5

Part 1............................................................................................................................................5

Question 5........................................................................................................................................5

Part 2............................................................................................................................................5

Part 4............................................................................................................................................5

References........................................................................................................................................6

Table of Contents

Question 1........................................................................................................................................3

Part 3............................................................................................................................................3

Part 4............................................................................................................................................3

Question 2........................................................................................................................................3

Part 2............................................................................................................................................3

Part 4............................................................................................................................................3

Question 3........................................................................................................................................4

PART 5........................................................................................................................................4

Question 4........................................................................................................................................5

Part 1............................................................................................................................................5

Question 5........................................................................................................................................5

Part 2............................................................................................................................................5

Part 4............................................................................................................................................5

References........................................................................................................................................6

Running Head: COSTING METHOD

Question 1

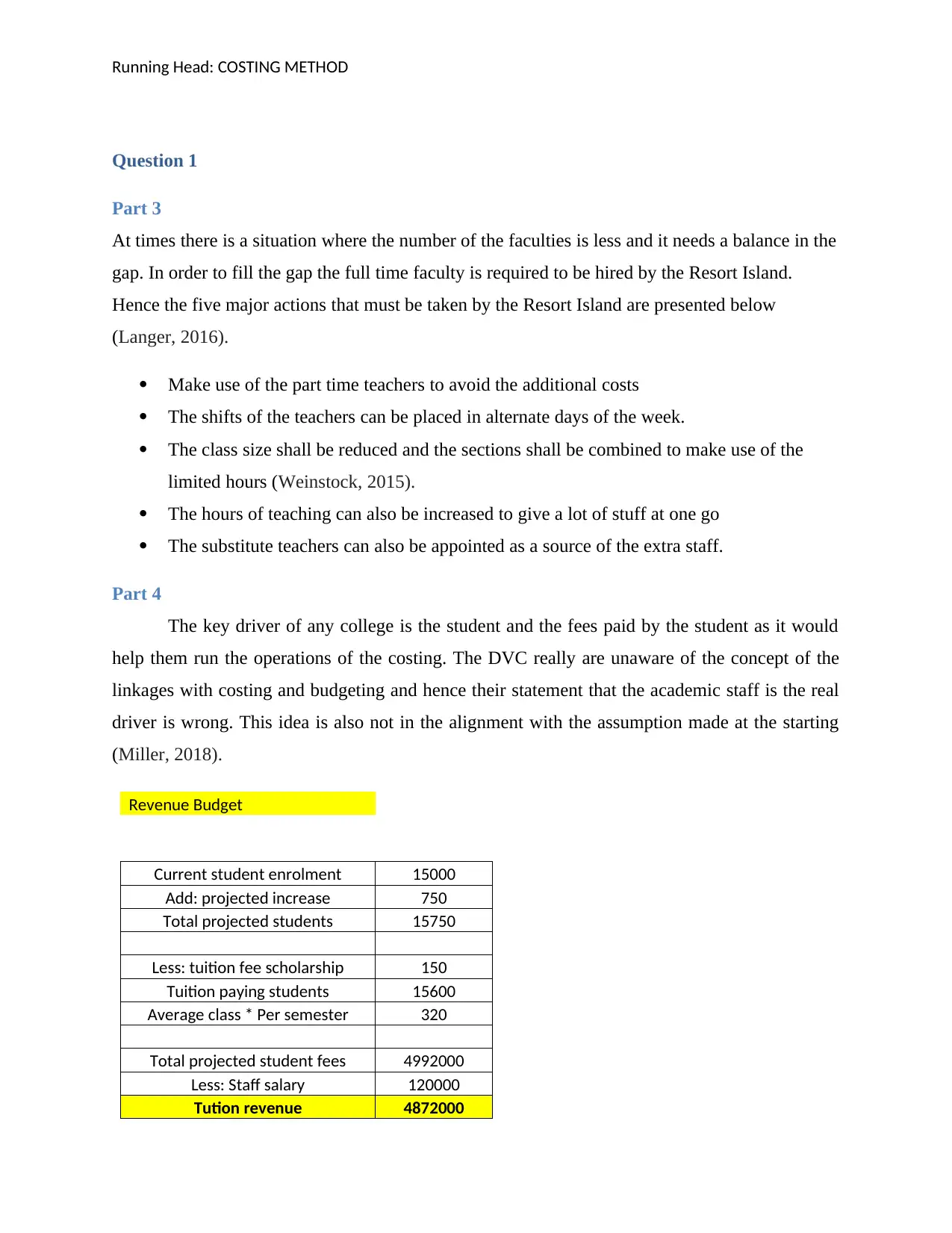

Part 3

At times there is a situation where the number of the faculties is less and it needs a balance in the

gap. In order to fill the gap the full time faculty is required to be hired by the Resort Island.

Hence the five major actions that must be taken by the Resort Island are presented below

(Langer, 2016).

Make use of the part time teachers to avoid the additional costs

The shifts of the teachers can be placed in alternate days of the week.

The class size shall be reduced and the sections shall be combined to make use of the

limited hours (Weinstock, 2015).

The hours of teaching can also be increased to give a lot of stuff at one go

The substitute teachers can also be appointed as a source of the extra staff.

Part 4

The key driver of any college is the student and the fees paid by the student as it would

help them run the operations of the costing. The DVC really are unaware of the concept of the

linkages with costing and budgeting and hence their statement that the academic staff is the real

driver is wrong. This idea is also not in the alignment with the assumption made at the starting

(Miller, 2018).

Revenue Budget

Current student enrolment 15000

Add: projected increase 750

Total projected students 15750

Less: tuition fee scholarship 150

Tuition paying students 15600

Average class * Per semester 320

Total projected student fees 4992000

Less: Staff salary 120000

Tution revenue 4872000

Question 1

Part 3

At times there is a situation where the number of the faculties is less and it needs a balance in the

gap. In order to fill the gap the full time faculty is required to be hired by the Resort Island.

Hence the five major actions that must be taken by the Resort Island are presented below

(Langer, 2016).

Make use of the part time teachers to avoid the additional costs

The shifts of the teachers can be placed in alternate days of the week.

The class size shall be reduced and the sections shall be combined to make use of the

limited hours (Weinstock, 2015).

The hours of teaching can also be increased to give a lot of stuff at one go

The substitute teachers can also be appointed as a source of the extra staff.

Part 4

The key driver of any college is the student and the fees paid by the student as it would

help them run the operations of the costing. The DVC really are unaware of the concept of the

linkages with costing and budgeting and hence their statement that the academic staff is the real

driver is wrong. This idea is also not in the alignment with the assumption made at the starting

(Miller, 2018).

Revenue Budget

Current student enrolment 15000

Add: projected increase 750

Total projected students 15750

Less: tuition fee scholarship 150

Tuition paying students 15600

Average class * Per semester 320

Total projected student fees 4992000

Less: Staff salary 120000

Tution revenue 4872000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: COSTING METHOD

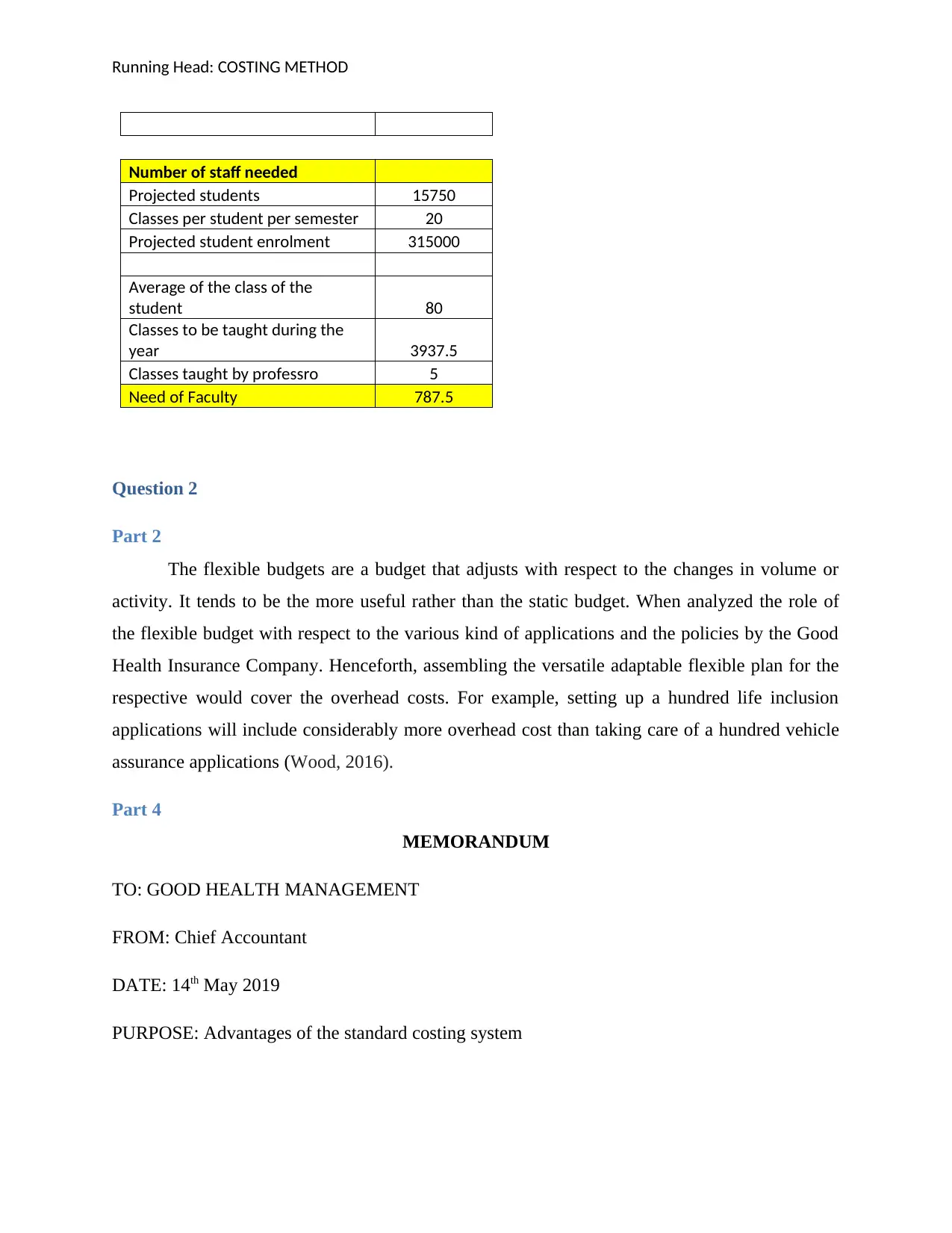

Number of staff needed

Projected students 15750

Classes per student per semester 20

Projected student enrolment 315000

Average of the class of the

student 80

Classes to be taught during the

year 3937.5

Classes taught by professro 5

Need of Faculty 787.5

Question 2

Part 2

The flexible budgets are a budget that adjusts with respect to the changes in volume or

activity. It tends to be the more useful rather than the static budget. When analyzed the role of

the flexible budget with respect to the various kind of applications and the policies by the Good

Health Insurance Company. Henceforth, assembling the versatile adaptable flexible plan for the

respective would cover the overhead costs. For example, setting up a hundred life inclusion

applications will include considerably more overhead cost than taking care of a hundred vehicle

assurance applications (Wood, 2016).

Part 4

MEMORANDUM

TO: GOOD HEALTH MANAGEMENT

FROM: Chief Accountant

DATE: 14th May 2019

PURPOSE: Advantages of the standard costing system

Number of staff needed

Projected students 15750

Classes per student per semester 20

Projected student enrolment 315000

Average of the class of the

student 80

Classes to be taught during the

year 3937.5

Classes taught by professro 5

Need of Faculty 787.5

Question 2

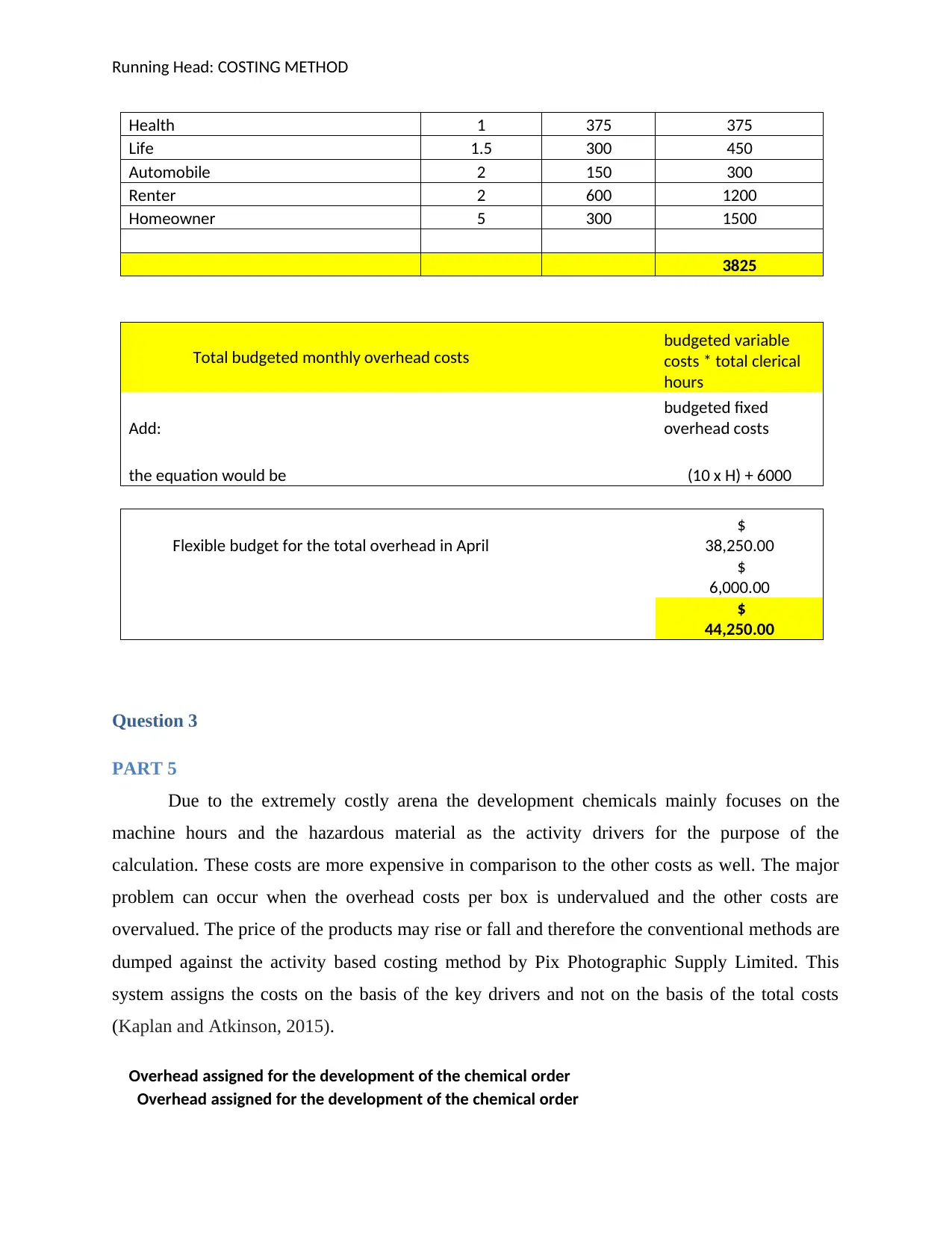

Part 2

The flexible budgets are a budget that adjusts with respect to the changes in volume or

activity. It tends to be the more useful rather than the static budget. When analyzed the role of

the flexible budget with respect to the various kind of applications and the policies by the Good

Health Insurance Company. Henceforth, assembling the versatile adaptable flexible plan for the

respective would cover the overhead costs. For example, setting up a hundred life inclusion

applications will include considerably more overhead cost than taking care of a hundred vehicle

assurance applications (Wood, 2016).

Part 4

MEMORANDUM

TO: GOOD HEALTH MANAGEMENT

FROM: Chief Accountant

DATE: 14th May 2019

PURPOSE: Advantages of the standard costing system

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: COSTING METHOD

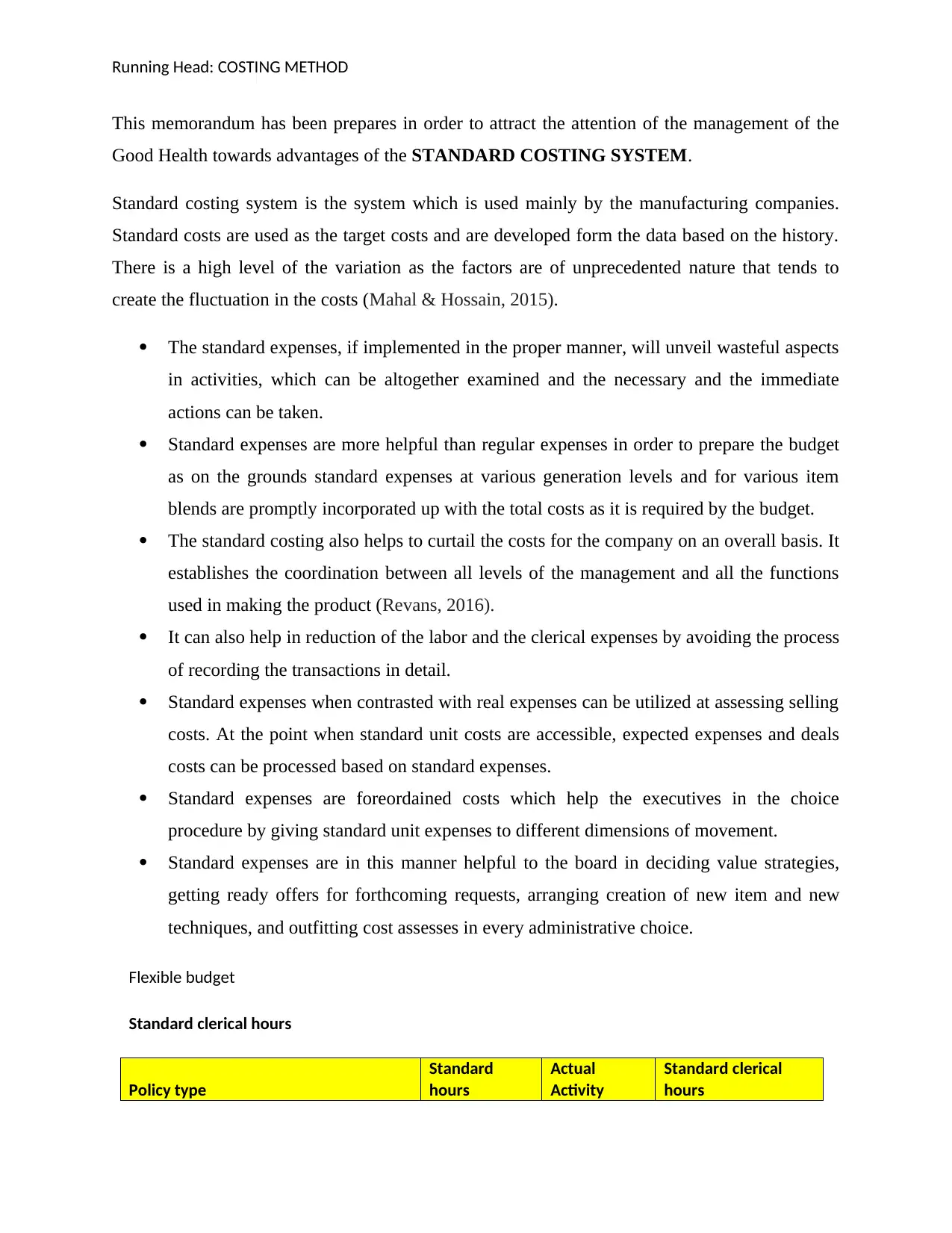

This memorandum has been prepares in order to attract the attention of the management of the

Good Health towards advantages of the STANDARD COSTING SYSTEM.

Standard costing system is the system which is used mainly by the manufacturing companies.

Standard costs are used as the target costs and are developed form the data based on the history.

There is a high level of the variation as the factors are of unprecedented nature that tends to

create the fluctuation in the costs (Mahal & Hossain, 2015).

The standard expenses, if implemented in the proper manner, will unveil wasteful aspects

in activities, which can be altogether examined and the necessary and the immediate

actions can be taken.

Standard expenses are more helpful than regular expenses in order to prepare the budget

as on the grounds standard expenses at various generation levels and for various item

blends are promptly incorporated up with the total costs as it is required by the budget.

The standard costing also helps to curtail the costs for the company on an overall basis. It

establishes the coordination between all levels of the management and all the functions

used in making the product (Revans, 2016).

It can also help in reduction of the labor and the clerical expenses by avoiding the process

of recording the transactions in detail.

Standard expenses when contrasted with real expenses can be utilized at assessing selling

costs. At the point when standard unit costs are accessible, expected expenses and deals

costs can be processed based on standard expenses.

Standard expenses are foreordained costs which help the executives in the choice

procedure by giving standard unit expenses to different dimensions of movement.

Standard expenses are in this manner helpful to the board in deciding value strategies,

getting ready offers for forthcoming requests, arranging creation of new item and new

techniques, and outfitting cost assesses in every administrative choice.

Flexible budget

Standard clerical hours

Policy type

Standard

hours

Actual

Activity

Standard clerical

hours

This memorandum has been prepares in order to attract the attention of the management of the

Good Health towards advantages of the STANDARD COSTING SYSTEM.

Standard costing system is the system which is used mainly by the manufacturing companies.

Standard costs are used as the target costs and are developed form the data based on the history.

There is a high level of the variation as the factors are of unprecedented nature that tends to

create the fluctuation in the costs (Mahal & Hossain, 2015).

The standard expenses, if implemented in the proper manner, will unveil wasteful aspects

in activities, which can be altogether examined and the necessary and the immediate

actions can be taken.

Standard expenses are more helpful than regular expenses in order to prepare the budget

as on the grounds standard expenses at various generation levels and for various item

blends are promptly incorporated up with the total costs as it is required by the budget.

The standard costing also helps to curtail the costs for the company on an overall basis. It

establishes the coordination between all levels of the management and all the functions

used in making the product (Revans, 2016).

It can also help in reduction of the labor and the clerical expenses by avoiding the process

of recording the transactions in detail.

Standard expenses when contrasted with real expenses can be utilized at assessing selling

costs. At the point when standard unit costs are accessible, expected expenses and deals

costs can be processed based on standard expenses.

Standard expenses are foreordained costs which help the executives in the choice

procedure by giving standard unit expenses to different dimensions of movement.

Standard expenses are in this manner helpful to the board in deciding value strategies,

getting ready offers for forthcoming requests, arranging creation of new item and new

techniques, and outfitting cost assesses in every administrative choice.

Flexible budget

Standard clerical hours

Policy type

Standard

hours

Actual

Activity

Standard clerical

hours

Running Head: COSTING METHOD

Health 1 375 375

Life 1.5 300 450

Automobile 2 150 300

Renter 2 600 1200

Homeowner 5 300 1500

3825

Total budgeted monthly overhead costs

budgeted variable

costs * total clerical

hours

Add:

budgeted fixed

overhead costs

the equation would be (10 x H) + 6000

Flexible budget for the total overhead in April

$

38,250.00

$

6,000.00

$

44,250.00

Question 3

PART 5

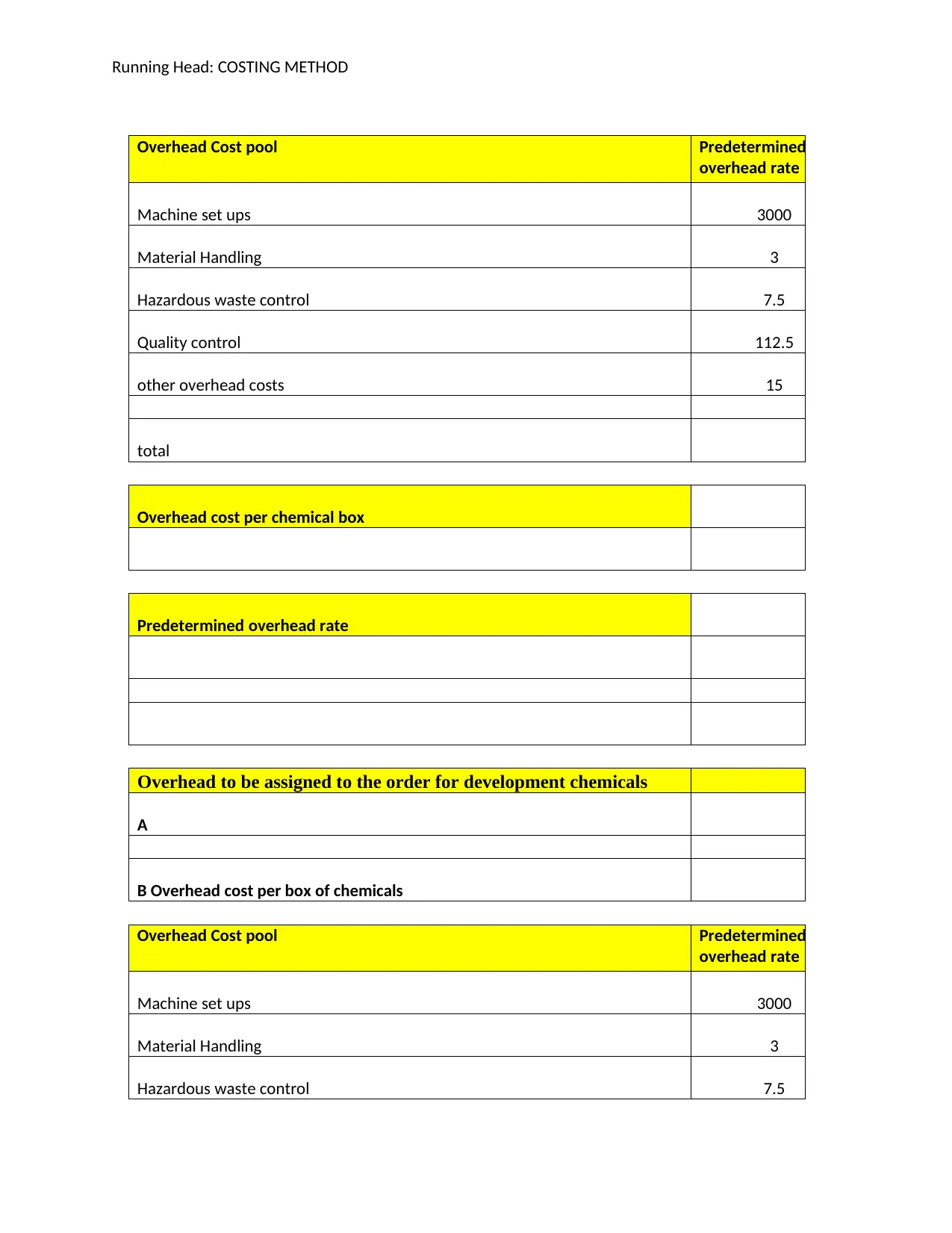

Due to the extremely costly arena the development chemicals mainly focuses on the

machine hours and the hazardous material as the activity drivers for the purpose of the

calculation. These costs are more expensive in comparison to the other costs as well. The major

problem can occur when the overhead costs per box is undervalued and the other costs are

overvalued. The price of the products may rise or fall and therefore the conventional methods are

dumped against the activity based costing method by Pix Photographic Supply Limited. This

system assigns the costs on the basis of the key drivers and not on the basis of the total costs

(Kaplan and Atkinson, 2015).

Overhead assigned for the development of the chemical order

Overhead assigned for the development of the chemical order

Health 1 375 375

Life 1.5 300 450

Automobile 2 150 300

Renter 2 600 1200

Homeowner 5 300 1500

3825

Total budgeted monthly overhead costs

budgeted variable

costs * total clerical

hours

Add:

budgeted fixed

overhead costs

the equation would be (10 x H) + 6000

Flexible budget for the total overhead in April

$

38,250.00

$

6,000.00

$

44,250.00

Question 3

PART 5

Due to the extremely costly arena the development chemicals mainly focuses on the

machine hours and the hazardous material as the activity drivers for the purpose of the

calculation. These costs are more expensive in comparison to the other costs as well. The major

problem can occur when the overhead costs per box is undervalued and the other costs are

overvalued. The price of the products may rise or fall and therefore the conventional methods are

dumped against the activity based costing method by Pix Photographic Supply Limited. This

system assigns the costs on the basis of the key drivers and not on the basis of the total costs

(Kaplan and Atkinson, 2015).

Overhead assigned for the development of the chemical order

Overhead assigned for the development of the chemical order

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: COSTING METHOD

Overhead Cost pool Predetermined

overhead rate

Machine set ups 3000

Material Handling 3

Hazardous waste control 7.5

Quality control 112.5

other overhead costs 15

total

Overhead cost per chemical box

Predetermined overhead rate

Overhead to be assigned to the order for development chemicals

A

B Overhead cost per box of chemicals

Overhead Cost pool Predetermined

overhead rate

Machine set ups 3000

Material Handling 3

Hazardous waste control 7.5

Overhead Cost pool Predetermined

overhead rate

Machine set ups 3000

Material Handling 3

Hazardous waste control 7.5

Quality control 112.5

other overhead costs 15

total

Overhead cost per chemical box

Predetermined overhead rate

Overhead to be assigned to the order for development chemicals

A

B Overhead cost per box of chemicals

Overhead Cost pool Predetermined

overhead rate

Machine set ups 3000

Material Handling 3

Hazardous waste control 7.5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: COSTING METHOD

Quality control 112.5

other overhead costs 15

total

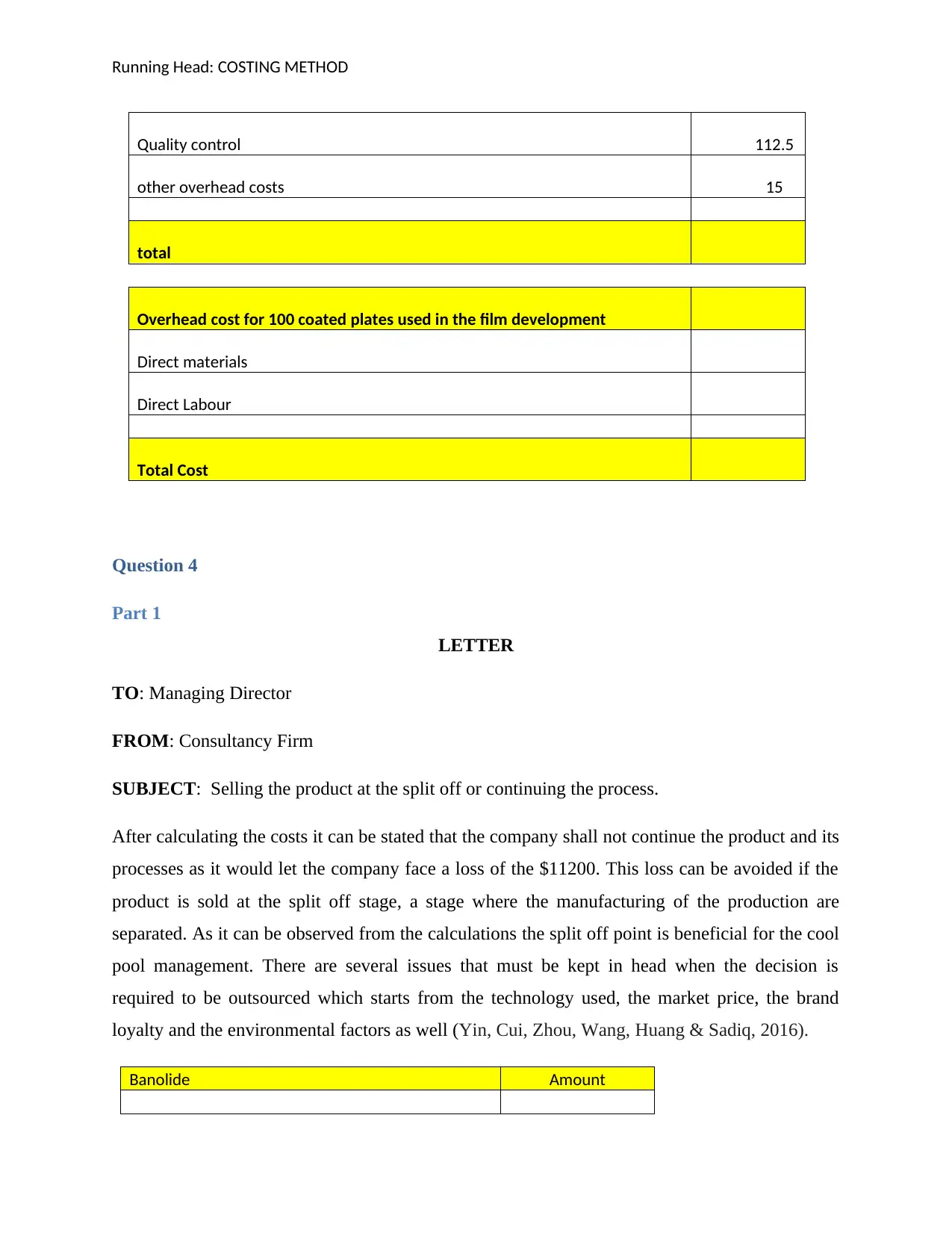

Overhead cost for 100 coated plates used in the film development

Direct materials

Direct Labour

Total Cost

Question 4

Part 1

LETTER

TO: Managing Director

FROM: Consultancy Firm

SUBJECT: Selling the product at the split off or continuing the process.

After calculating the costs it can be stated that the company shall not continue the product and its

processes as it would let the company face a loss of the $11200. This loss can be avoided if the

product is sold at the split off stage, a stage where the manufacturing of the production are

separated. As it can be observed from the calculations the split off point is beneficial for the cool

pool management. There are several issues that must be kept in head when the decision is

required to be outsourced which starts from the technology used, the market price, the brand

loyalty and the environmental factors as well (Yin, Cui, Zhou, Wang, Huang & Sadiq, 2016).

Banolide Amount

Quality control 112.5

other overhead costs 15

total

Overhead cost for 100 coated plates used in the film development

Direct materials

Direct Labour

Total Cost

Question 4

Part 1

LETTER

TO: Managing Director

FROM: Consultancy Firm

SUBJECT: Selling the product at the split off or continuing the process.

After calculating the costs it can be stated that the company shall not continue the product and its

processes as it would let the company face a loss of the $11200. This loss can be avoided if the

product is sold at the split off stage, a stage where the manufacturing of the production are

separated. As it can be observed from the calculations the split off point is beneficial for the cool

pool management. There are several issues that must be kept in head when the decision is

required to be outsourced which starts from the technology used, the market price, the brand

loyalty and the environmental factors as well (Yin, Cui, Zhou, Wang, Huang & Sadiq, 2016).

Banolide Amount

Running Head: COSTING METHOD

Allocation of Joint Cost

$

12,000.00

Sale value at split off Point

$

5,000.00

Sale value after processing further

$

20,000.00

Additional processing costs

$

26,200.00

Incremental Profit or Loss if processed further

Sales value incremental-Additional processing cost

$

(11,200.00)

Question 5

Part 2

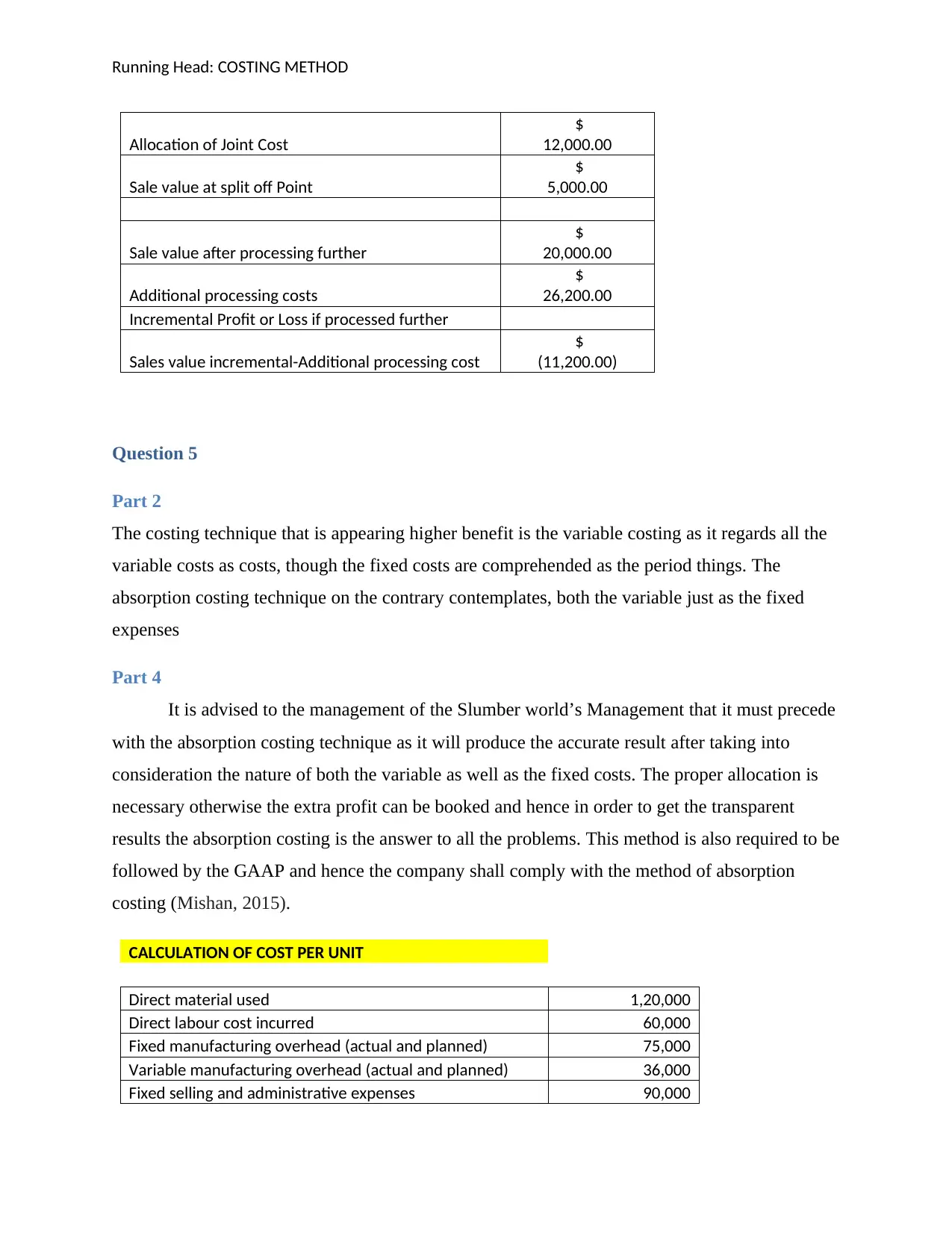

The costing technique that is appearing higher benefit is the variable costing as it regards all the

variable costs as costs, though the fixed costs are comprehended as the period things. The

absorption costing technique on the contrary contemplates, both the variable just as the fixed

expenses

Part 4

It is advised to the management of the Slumber world’s Management that it must precede

with the absorption costing technique as it will produce the accurate result after taking into

consideration the nature of both the variable as well as the fixed costs. The proper allocation is

necessary otherwise the extra profit can be booked and hence in order to get the transparent

results the absorption costing is the answer to all the problems. This method is also required to be

followed by the GAAP and hence the company shall comply with the method of absorption

costing (Mishan, 2015).

CALCULATION OF COST PER UNIT

Direct material used 1,20,000

Direct labour cost incurred 60,000

Fixed manufacturing overhead (actual and planned) 75,000

Variable manufacturing overhead (actual and planned) 36,000

Fixed selling and administrative expenses 90,000

Allocation of Joint Cost

$

12,000.00

Sale value at split off Point

$

5,000.00

Sale value after processing further

$

20,000.00

Additional processing costs

$

26,200.00

Incremental Profit or Loss if processed further

Sales value incremental-Additional processing cost

$

(11,200.00)

Question 5

Part 2

The costing technique that is appearing higher benefit is the variable costing as it regards all the

variable costs as costs, though the fixed costs are comprehended as the period things. The

absorption costing technique on the contrary contemplates, both the variable just as the fixed

expenses

Part 4

It is advised to the management of the Slumber world’s Management that it must precede

with the absorption costing technique as it will produce the accurate result after taking into

consideration the nature of both the variable as well as the fixed costs. The proper allocation is

necessary otherwise the extra profit can be booked and hence in order to get the transparent

results the absorption costing is the answer to all the problems. This method is also required to be

followed by the GAAP and hence the company shall comply with the method of absorption

costing (Mishan, 2015).

CALCULATION OF COST PER UNIT

Direct material used 1,20,000

Direct labour cost incurred 60,000

Fixed manufacturing overhead (actual and planned) 75,000

Variable manufacturing overhead (actual and planned) 36,000

Fixed selling and administrative expenses 90,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: COSTING METHOD

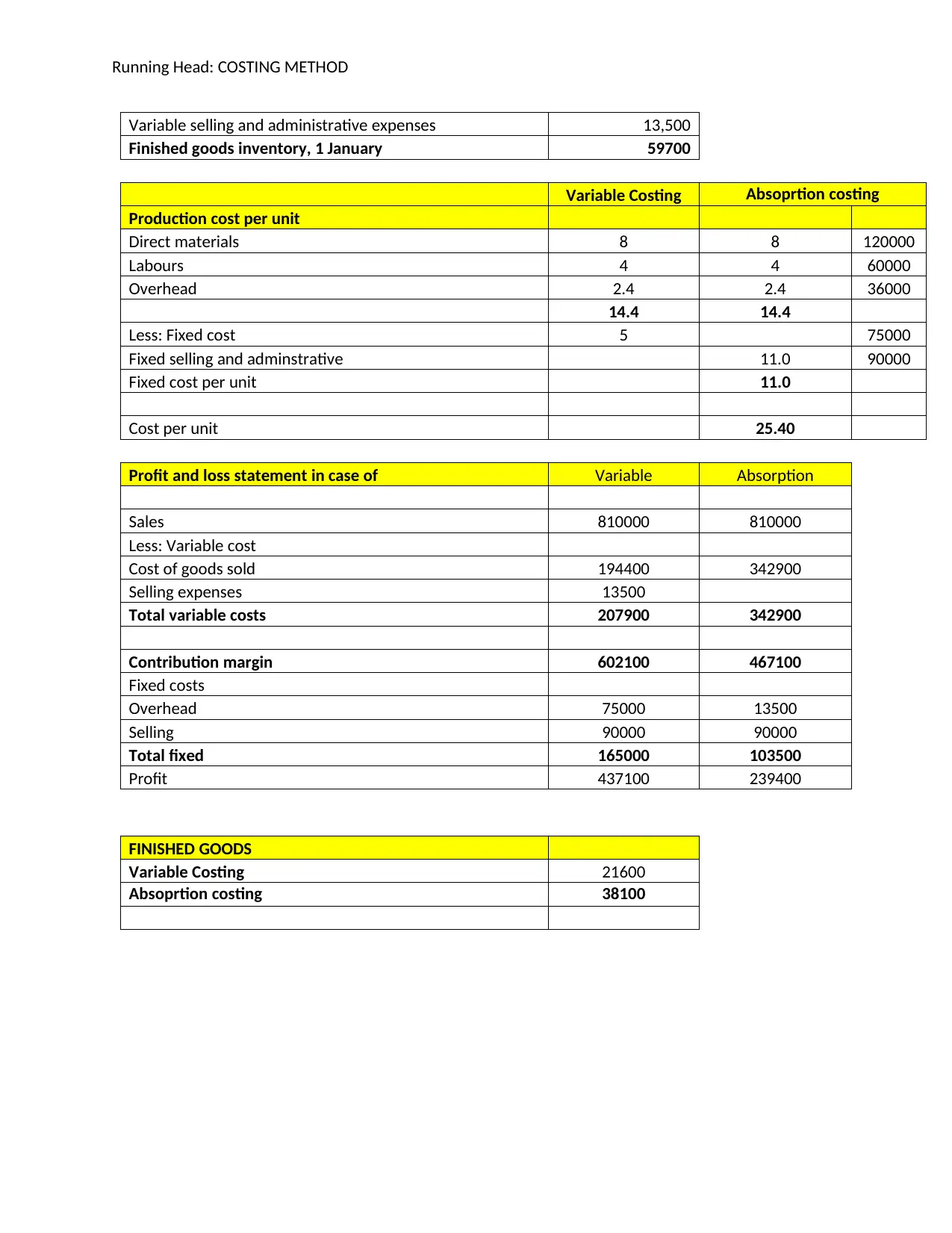

Variable selling and administrative expenses 13,500

Finished goods inventory, 1 January 59700

Variable Costing Absoprtion costing

Production cost per unit

Direct materials 8 8 120000

Labours 4 4 60000

Overhead 2.4 2.4 36000

14.4 14.4

Less: Fixed cost 5 75000

Fixed selling and adminstrative 11.0 90000

Fixed cost per unit 11.0

Cost per unit 25.40

Profit and loss statement in case of Variable Absorption

Sales 810000 810000

Less: Variable cost

Cost of goods sold 194400 342900

Selling expenses 13500

Total variable costs 207900 342900

Contribution margin 602100 467100

Fixed costs

Overhead 75000 13500

Selling 90000 90000

Total fixed 165000 103500

Profit 437100 239400

FINISHED GOODS

Variable Costing 21600

Absoprtion costing 38100

Variable selling and administrative expenses 13,500

Finished goods inventory, 1 January 59700

Variable Costing Absoprtion costing

Production cost per unit

Direct materials 8 8 120000

Labours 4 4 60000

Overhead 2.4 2.4 36000

14.4 14.4

Less: Fixed cost 5 75000

Fixed selling and adminstrative 11.0 90000

Fixed cost per unit 11.0

Cost per unit 25.40

Profit and loss statement in case of Variable Absorption

Sales 810000 810000

Less: Variable cost

Cost of goods sold 194400 342900

Selling expenses 13500

Total variable costs 207900 342900

Contribution margin 602100 467100

Fixed costs

Overhead 75000 13500

Selling 90000 90000

Total fixed 165000 103500

Profit 437100 239400

FINISHED GOODS

Variable Costing 21600

Absoprtion costing 38100

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: COSTING METHOD

References

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Langer, E. S. (2016). Hiring Difficulties Compound Downstream Processing Woes: Process

Development Jobs Still the Most Difficult to Fill. Genetic Engineering & Biotechnology

News, 36(16), 33-33.

Mahal, I., & Hossain, A. (2015). Activity-Based Costing (ABC)–An Effective Tool for Better

Management. Research Journal of Finance and Accounting, 6(4), 66-74.

Miller, G. (2018). Performance based budgeting. Routledge.

Mishan, E.J., 2015. Elements of Cost-Benefit Analysis (Routledge Revivals). Routledge.

Revans, R. (2016). The enterprise as a learning system. In Action learning in practice (pp. 43-

48). Routledge.

Weinstock, D. (2015). Hiring new staff? Aim for success by onboarding. The Journal of medical

practice management: MPM, 31(2), 96.

Wood, A. J. (2016). Flexible scheduling, degradation of job quality and barriers to collective

voice. Human Relations, 69(10), 1989-2010.

Yin, H., Cui, B., Zhou, X., Wang, W., Huang, Z., & Sadiq, S. (2016). Joint modeling of user

check-in behaviors for real-time point-of-interest recommendation. ACM Transactions

on Information Systems (TOIS), 35(2), 11.

References

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Langer, E. S. (2016). Hiring Difficulties Compound Downstream Processing Woes: Process

Development Jobs Still the Most Difficult to Fill. Genetic Engineering & Biotechnology

News, 36(16), 33-33.

Mahal, I., & Hossain, A. (2015). Activity-Based Costing (ABC)–An Effective Tool for Better

Management. Research Journal of Finance and Accounting, 6(4), 66-74.

Miller, G. (2018). Performance based budgeting. Routledge.

Mishan, E.J., 2015. Elements of Cost-Benefit Analysis (Routledge Revivals). Routledge.

Revans, R. (2016). The enterprise as a learning system. In Action learning in practice (pp. 43-

48). Routledge.

Weinstock, D. (2015). Hiring new staff? Aim for success by onboarding. The Journal of medical

practice management: MPM, 31(2), 96.

Wood, A. J. (2016). Flexible scheduling, degradation of job quality and barriers to collective

voice. Human Relations, 69(10), 1989-2010.

Yin, H., Cui, B., Zhou, X., Wang, W., Huang, Z., & Sadiq, S. (2016). Joint modeling of user

check-in behaviors for real-time point-of-interest recommendation. ACM Transactions

on Information Systems (TOIS), 35(2), 11.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.