Dysonica Plc: Financial Cost Analysis, Reduction Methods & Budgeting

VerifiedAdded on 2023/06/10

|16

|4897

|440

Report

AI Summary

This report provides a comprehensive analysis of Dysonica Plc's financial situation, focusing on cost determination, reduction strategies, and budget forecasting. It begins by classifying costs into fixed, variable, and semi-variable categories, further exploring marginal, absorption, and activity-based costing methods. Recommendations for cost reduction are provided, alongside a 12-month budget forecast up to April 2023. The report concludes with an analysis of Dysonica's performance against the forecasted budget, offering insights into the company's operational efficiency and financial stability. Desklib provides a platform for students to access this and other solved assignments.

Time constrained

project Business

Finance

project Business

Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

Task 1...............................................................................................................................................3

Determine the cost of Dysonica according to their nature..........................................................3

TASK 2............................................................................................................................................7

Provide Recommendation & Method of Cost Reductions..........................................................7

TASK 3..........................................................................................................................................10

Preparation of a budget forecast of 12 moths for organisation up to 30 April 2023.................10

TASK 4..........................................................................................................................................14

Analysing the performance of Dysonica with the help of Forecasted budget.........................14

CONCLUSION .............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION ..........................................................................................................................3

Task 1...............................................................................................................................................3

Determine the cost of Dysonica according to their nature..........................................................3

TASK 2............................................................................................................................................7

Provide Recommendation & Method of Cost Reductions..........................................................7

TASK 3..........................................................................................................................................10

Preparation of a budget forecast of 12 moths for organisation up to 30 April 2023.................10

TASK 4..........................................................................................................................................14

Analysing the performance of Dysonica with the help of Forecasted budget.........................14

CONCLUSION .............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION

This report basically discuss about the two terms that is finance and credit these terms are come

from the concept business finance. The firm's financial base is very important. Basically this is

necessary to combine assets, goods and services and raw materials also with another economic

projected activities. In general, the money invested by the businessman into the business to start

the business is not enough to satisfy the organization's financial necessities. On the basis of

above performance, the proprietor must look for a direction to create sales revenue. A brief

examining the financial needs and expectations for gathering those requirements must be

executed for the purpose of showing accomplishment of better financial management in order to

maintain the stability of the business. This case is mainly discuss about the company Dysonica

Plc. This report is categorized into four sections. First task is describe about the separate cost of

the company and how the firm discriminate these costs into sections such as fixed cost, variable

cost and semi-variable cost(Baker and Nofsinger, 2012). It also explain about the case of

marginal, absorption and activity-based costing. In task two it also discuss about the various of

suggestions to the company in the case and how they can decline the cost and maintain the

efficiency of the project. In third task it describe about the predicted cash flow of the company

for the past 12 months up to 30th April 2023 of the Dysonica Plc. In last task it provides a

performance measurement of the company and how the business is operative in the industry with

the assist of these predicted figures in the cash flow it estimate the cash Flow Dysonica plc (Wu

and Wang, 2000).

Task 1

Determine the cost of Dysonica according to their nature

Cost: The term cost refers to expenditure on manufacturing and supplying of products and

services. In simple words, the cost arises when any type of production or selling activity takes

place. On behalf of cost accounting, the term is used as a form of managerial accounting that

main intent is to acquire a company's total cost of creation or production by analysing its variable

cost and fixed cost. Variable and fixed costs are expenses incurred during the company's

production (Bozec, 2005). These expenses are as follows:

Variable cost: The cost which is depending on company production and sales is known as

a variable cost. Variable cost fluctuation takes place when any type of change occurs in the

This report basically discuss about the two terms that is finance and credit these terms are come

from the concept business finance. The firm's financial base is very important. Basically this is

necessary to combine assets, goods and services and raw materials also with another economic

projected activities. In general, the money invested by the businessman into the business to start

the business is not enough to satisfy the organization's financial necessities. On the basis of

above performance, the proprietor must look for a direction to create sales revenue. A brief

examining the financial needs and expectations for gathering those requirements must be

executed for the purpose of showing accomplishment of better financial management in order to

maintain the stability of the business. This case is mainly discuss about the company Dysonica

Plc. This report is categorized into four sections. First task is describe about the separate cost of

the company and how the firm discriminate these costs into sections such as fixed cost, variable

cost and semi-variable cost(Baker and Nofsinger, 2012). It also explain about the case of

marginal, absorption and activity-based costing. In task two it also discuss about the various of

suggestions to the company in the case and how they can decline the cost and maintain the

efficiency of the project. In third task it describe about the predicted cash flow of the company

for the past 12 months up to 30th April 2023 of the Dysonica Plc. In last task it provides a

performance measurement of the company and how the business is operative in the industry with

the assist of these predicted figures in the cash flow it estimate the cash Flow Dysonica plc (Wu

and Wang, 2000).

Task 1

Determine the cost of Dysonica according to their nature

Cost: The term cost refers to expenditure on manufacturing and supplying of products and

services. In simple words, the cost arises when any type of production or selling activity takes

place. On behalf of cost accounting, the term is used as a form of managerial accounting that

main intent is to acquire a company's total cost of creation or production by analysing its variable

cost and fixed cost. Variable and fixed costs are expenses incurred during the company's

production (Bozec, 2005). These expenses are as follows:

Variable cost: The cost which is depending on company production and sales is known as

a variable cost. Variable cost fluctuation takes place when any type of change occurs in the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company during the formation and sales of its goods and services. In other words, variable cost is

increased or decreased in proportion to company creation and trade. Variable costs are calculated

by adding all marginal costs over the total number of units produced. It includes Raw material, a

charge of delivery and packaging and labour.

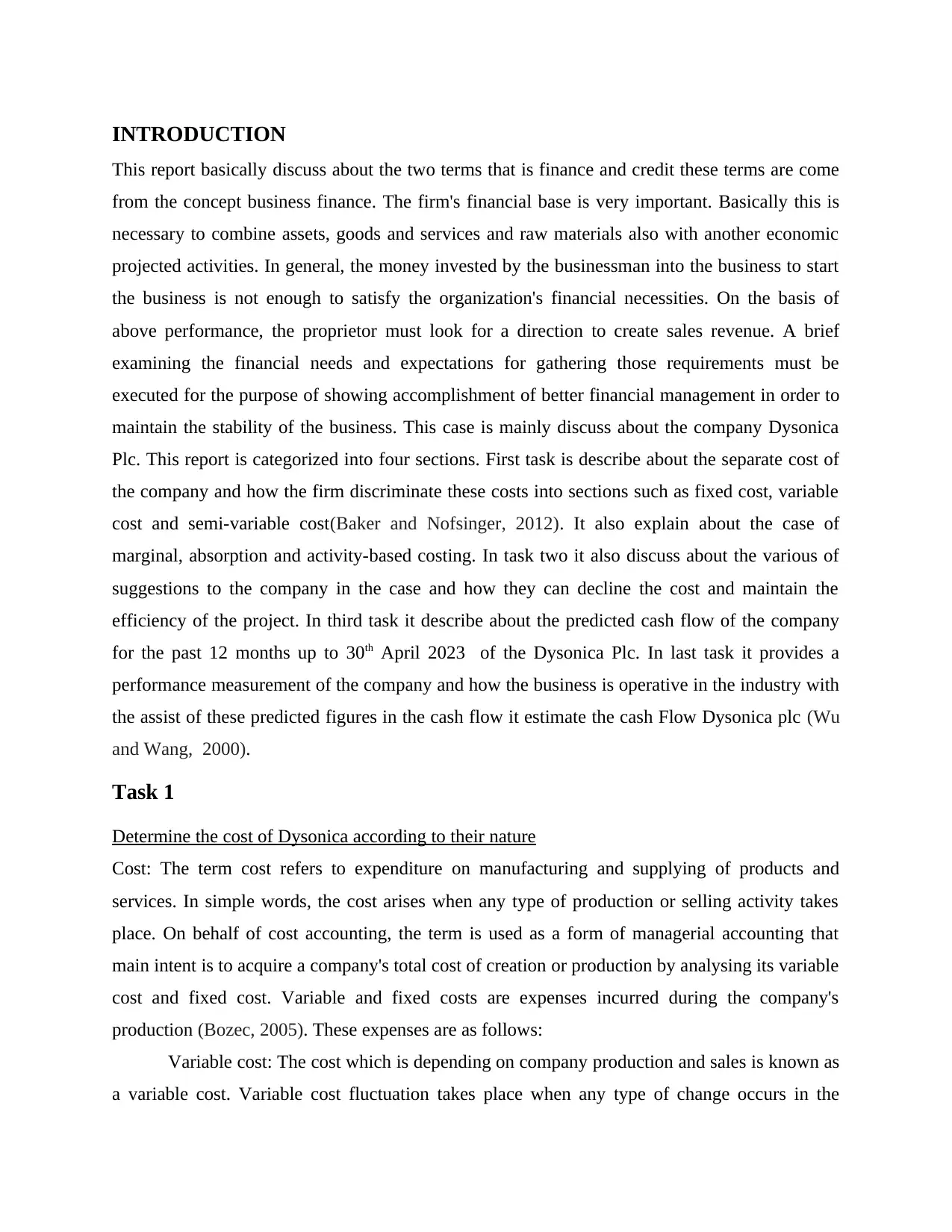

Fixed Cost: The cost which never fluctuates neither in increase nor in the decrease of

products and services is called fixed cost. Fixed cost are independent cost which do not depend

upon any production or sales of the company. Therefore, fixed cost are considered to be indirect

costs. Such costs are insurance and utility bill payment, rent payment and employees salaries.

Semi – variable costs: Semi variable cost are generated from the combination of two

costs, variable cost and fixed cost. It is also known as semi – fixed costs or a mixed cost. This

cost are fixed at a particular level of production or utilization, and turn into a variable cost after

level of production is exceeded (Brinn, Jones and Pendlebury, 2001).

Fixed Costs £ Variable

Costs

£ Semi-variable

Costs

£

Machinery 1500 Raw materials 15000 Office and

sales staff

9000

Factory and

storage rent

18000 Direct labour 17500 Logistics 3000

Utilities 500

Insurance 500

Total: 20500 32500 12000

Unit costing is the method which is used to determine the total number of expenditure

incurred by an organization to manufacture, preserve and sell per unit of a individual goods or

services. It is also named as “output” or single “output”.This costing manufacture a individual or

single product on huge altitude on a regular basis. The units of all individual are same in respects

of size, quality and shape. Process costing is the activity where products are not produce on a

continuous basis.

increased or decreased in proportion to company creation and trade. Variable costs are calculated

by adding all marginal costs over the total number of units produced. It includes Raw material, a

charge of delivery and packaging and labour.

Fixed Cost: The cost which never fluctuates neither in increase nor in the decrease of

products and services is called fixed cost. Fixed cost are independent cost which do not depend

upon any production or sales of the company. Therefore, fixed cost are considered to be indirect

costs. Such costs are insurance and utility bill payment, rent payment and employees salaries.

Semi – variable costs: Semi variable cost are generated from the combination of two

costs, variable cost and fixed cost. It is also known as semi – fixed costs or a mixed cost. This

cost are fixed at a particular level of production or utilization, and turn into a variable cost after

level of production is exceeded (Brinn, Jones and Pendlebury, 2001).

Fixed Costs £ Variable

Costs

£ Semi-variable

Costs

£

Machinery 1500 Raw materials 15000 Office and

sales staff

9000

Factory and

storage rent

18000 Direct labour 17500 Logistics 3000

Utilities 500

Insurance 500

Total: 20500 32500 12000

Unit costing is the method which is used to determine the total number of expenditure

incurred by an organization to manufacture, preserve and sell per unit of a individual goods or

services. It is also named as “output” or single “output”.This costing manufacture a individual or

single product on huge altitude on a regular basis. The units of all individual are same in respects

of size, quality and shape. Process costing is the activity where products are not produce on a

continuous basis.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

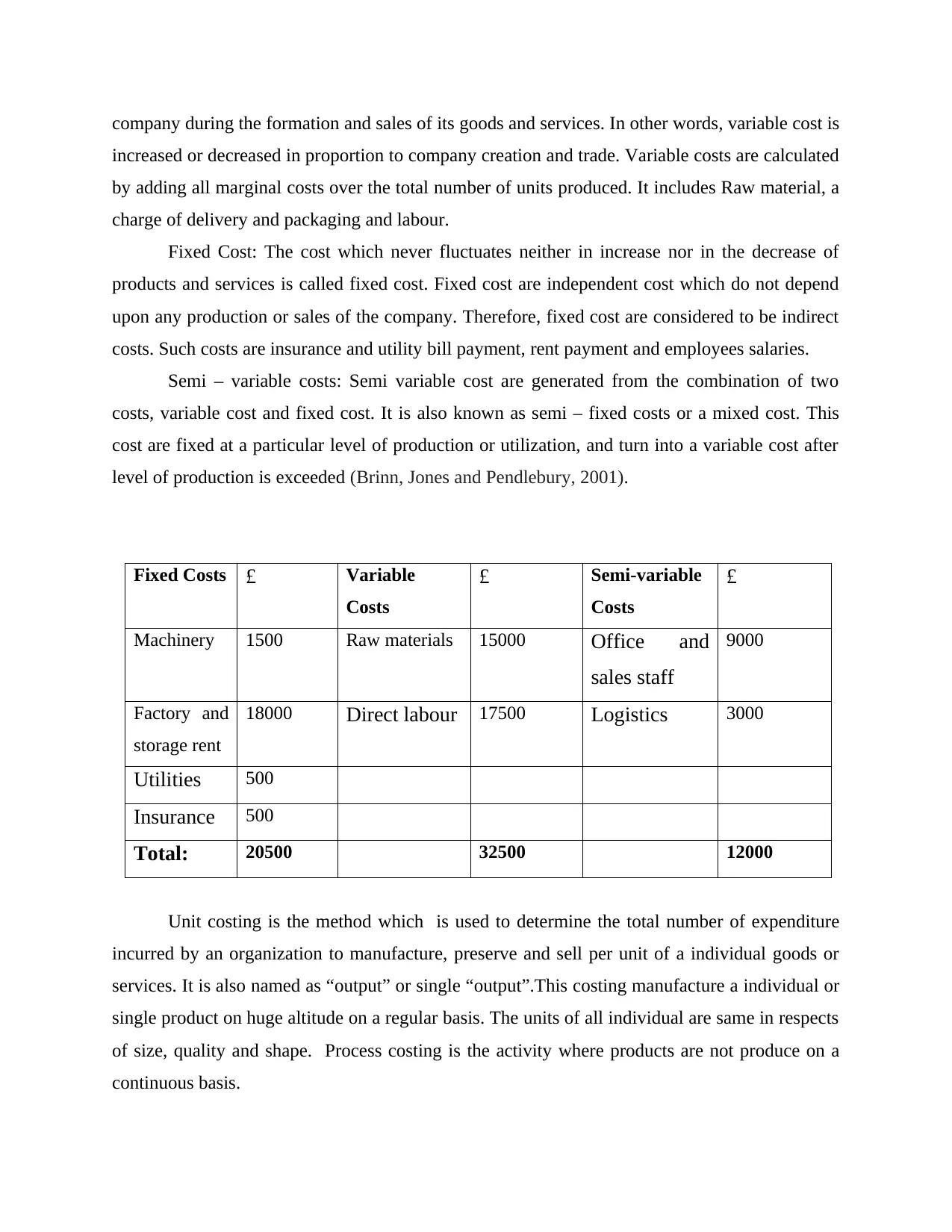

Absorption Costing: Absorption costing the process which is used to determine the total

cost incurred during the production of a single goods by the method of managerial accounting.

This type of method adopt by the management of the company to consume the product cost. Full

costing is also use as a place of absorption costing. It is not a continuous expenses but it is

capitalized cost that is captured on the balance sheet. In simple words, the absorption costing is

the key to analyse the cost showing accurate details of manufacturing goods and services. AC

also included the direct cost and indirect cost (Firth, 1997). Indirect cost examples are rent of

factory, administration fees and insurance. Direct cost calculate the number of raw materials and

labour are useful in producing the goods (Wong and Selvi, 1998).

Formula of absorption costing are as follows:

Absorption cost = (Direct labour cost + Direct material cost + Variable manufacturing

overhead cost + Fixed manufacturing overhead) / No. of units produced

Illustration of absorption costing:

Let, the company XYZ is a producer and supplier of led bulb. The following data is provided by

the company for single manufacturing face. Use absorption costing method for calculating the

profit of the company.

The total number of unit produced by the company is 20000 and 18000 units are sold

over the period is equal to $ 100 unit price.

Direct Labour is equal to $ 10 and Direct material = $ 40

variable costs is equal to $ 10

Overheads Fixed = $ 10

Fixed cost = $ 60,000

Marginal Costing: Marginal costing is a type of costing where the company perform

activity of allocating variable production to products. It is also say that, this cost which is useful

in measuring the effect of variable cost on the level of production. The major and important part

of marginal cost is break even analysis (Kahya, 1997). There are two types of cost belongs to a

product are variable cost and fixed cost. Variable cost are always changed in accordance of

change in production and sales and fixed cost always remain same or constant. Marginal costing

is the foundation of valuation of finished goods or products and ongoing process of raw material

where fixed cost is recovered from contribution price and variable cost is charged to production.

cost incurred during the production of a single goods by the method of managerial accounting.

This type of method adopt by the management of the company to consume the product cost. Full

costing is also use as a place of absorption costing. It is not a continuous expenses but it is

capitalized cost that is captured on the balance sheet. In simple words, the absorption costing is

the key to analyse the cost showing accurate details of manufacturing goods and services. AC

also included the direct cost and indirect cost (Firth, 1997). Indirect cost examples are rent of

factory, administration fees and insurance. Direct cost calculate the number of raw materials and

labour are useful in producing the goods (Wong and Selvi, 1998).

Formula of absorption costing are as follows:

Absorption cost = (Direct labour cost + Direct material cost + Variable manufacturing

overhead cost + Fixed manufacturing overhead) / No. of units produced

Illustration of absorption costing:

Let, the company XYZ is a producer and supplier of led bulb. The following data is provided by

the company for single manufacturing face. Use absorption costing method for calculating the

profit of the company.

The total number of unit produced by the company is 20000 and 18000 units are sold

over the period is equal to $ 100 unit price.

Direct Labour is equal to $ 10 and Direct material = $ 40

variable costs is equal to $ 10

Overheads Fixed = $ 10

Fixed cost = $ 60,000

Marginal Costing: Marginal costing is a type of costing where the company perform

activity of allocating variable production to products. It is also say that, this cost which is useful

in measuring the effect of variable cost on the level of production. The major and important part

of marginal cost is break even analysis (Kahya, 1997). There are two types of cost belongs to a

product are variable cost and fixed cost. Variable cost are always changed in accordance of

change in production and sales and fixed cost always remain same or constant. Marginal costing

is the foundation of valuation of finished goods or products and ongoing process of raw material

where fixed cost is recovered from contribution price and variable cost is charged to production.

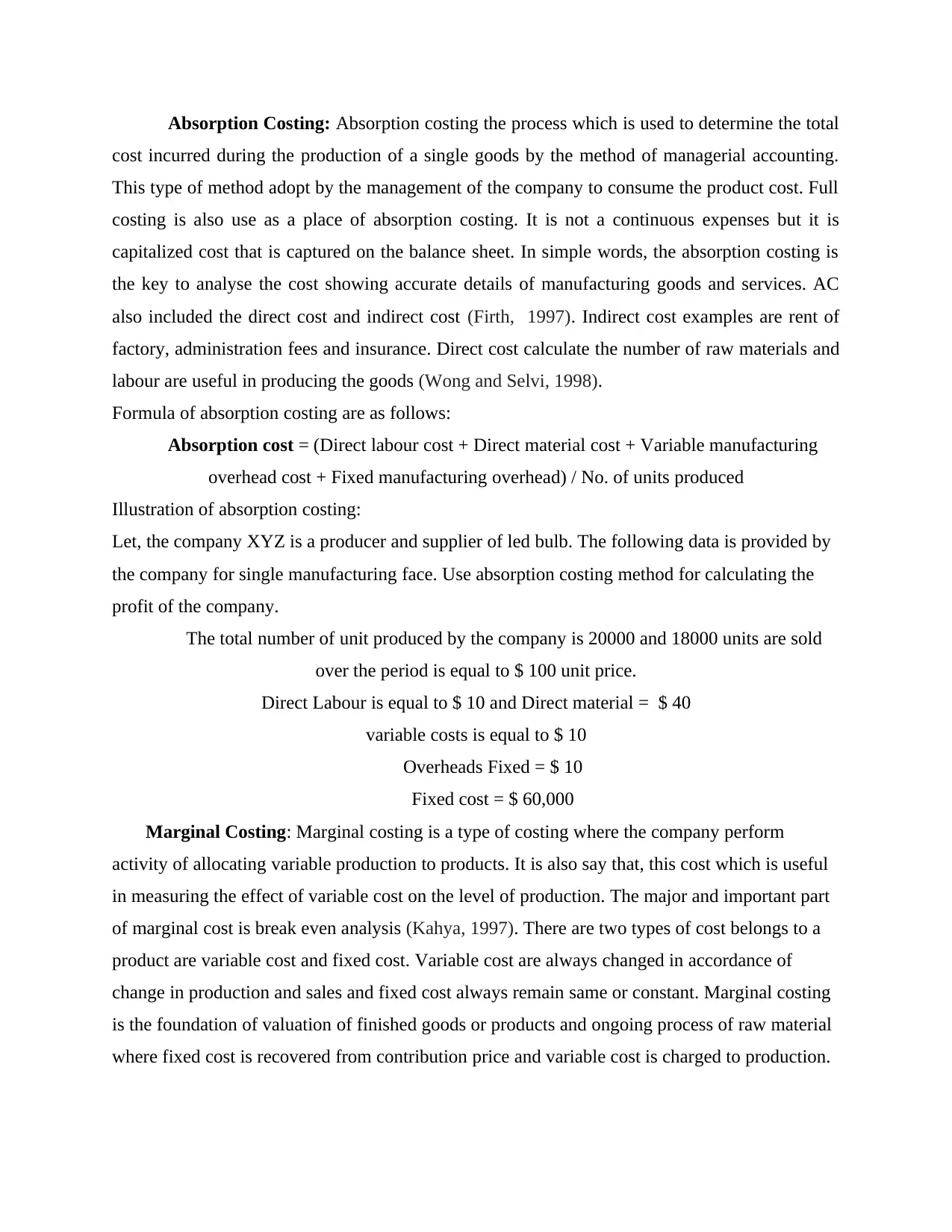

There are some examples of variable production costs are Direct material, direct labour and

direct equipments and few overheads.

Formula of Marginal cost are as follows:

Marginal Cost = Change in Cost/Change in Quantity

here, change in cost refers to rate of fluctuation of variable cost and change in quantity refers to

number of units will increase or decrease at a certain level of production.

Illustration of marginal cost:

Assume that XYZ is a company that produces led bulbs. For calculating the marginal cost

the company uses manufacturing data of products from the following information:

In 1 Month the company produces = 20000 units and second Month it Produced = 30000

Variable Costs of one month = $ 100000 and Variable Costs in Month 2 = $ 160000

Marginal Cost = Change in cost/change in quantity

(160000 – 100000) / (30000 – 20,000) = Marginal Cost

As a result, the marginal cost per unit is equal to $ 6 (60000/10000).

Activity Based costing: It is the method of costing which is useful in analysing practices in an

organization and fixing the cost of activity to products and services on behalf of the real and

accurate consumption by each. It is cost which is very helpful at the time of business

manufacturing large number of overheads. In result, it shows the true and fair value of the

company expenditure (Klusek and Bornstein, 2006). The activity based costing is also gives

knowledge of a particular goods production cost breakdown and also helpful in finding a

individual product which is profitable of an organization. There are some measures of activity

based costing:

It consider both the costs, direct cost and overhead costs of manufacturing each and every

product.

Activity based costing is useful in remembering different indirect expenses required in

different type of products.

The prices are very accurate and exact straight about spending and price your products.

Keeping in mind how the cost can be deducted or lower.

The ABC organization determines the path of distribution are used by the seller to sell

their product or services to consumers, such as wholesaler, social networking site,

advertisement and door to door services.

direct equipments and few overheads.

Formula of Marginal cost are as follows:

Marginal Cost = Change in Cost/Change in Quantity

here, change in cost refers to rate of fluctuation of variable cost and change in quantity refers to

number of units will increase or decrease at a certain level of production.

Illustration of marginal cost:

Assume that XYZ is a company that produces led bulbs. For calculating the marginal cost

the company uses manufacturing data of products from the following information:

In 1 Month the company produces = 20000 units and second Month it Produced = 30000

Variable Costs of one month = $ 100000 and Variable Costs in Month 2 = $ 160000

Marginal Cost = Change in cost/change in quantity

(160000 – 100000) / (30000 – 20,000) = Marginal Cost

As a result, the marginal cost per unit is equal to $ 6 (60000/10000).

Activity Based costing: It is the method of costing which is useful in analysing practices in an

organization and fixing the cost of activity to products and services on behalf of the real and

accurate consumption by each. It is cost which is very helpful at the time of business

manufacturing large number of overheads. In result, it shows the true and fair value of the

company expenditure (Klusek and Bornstein, 2006). The activity based costing is also gives

knowledge of a particular goods production cost breakdown and also helpful in finding a

individual product which is profitable of an organization. There are some measures of activity

based costing:

It consider both the costs, direct cost and overhead costs of manufacturing each and every

product.

Activity based costing is useful in remembering different indirect expenses required in

different type of products.

The prices are very accurate and exact straight about spending and price your products.

Keeping in mind how the cost can be deducted or lower.

The ABC organization determines the path of distribution are used by the seller to sell

their product or services to consumers, such as wholesaler, social networking site,

advertisement and door to door services.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

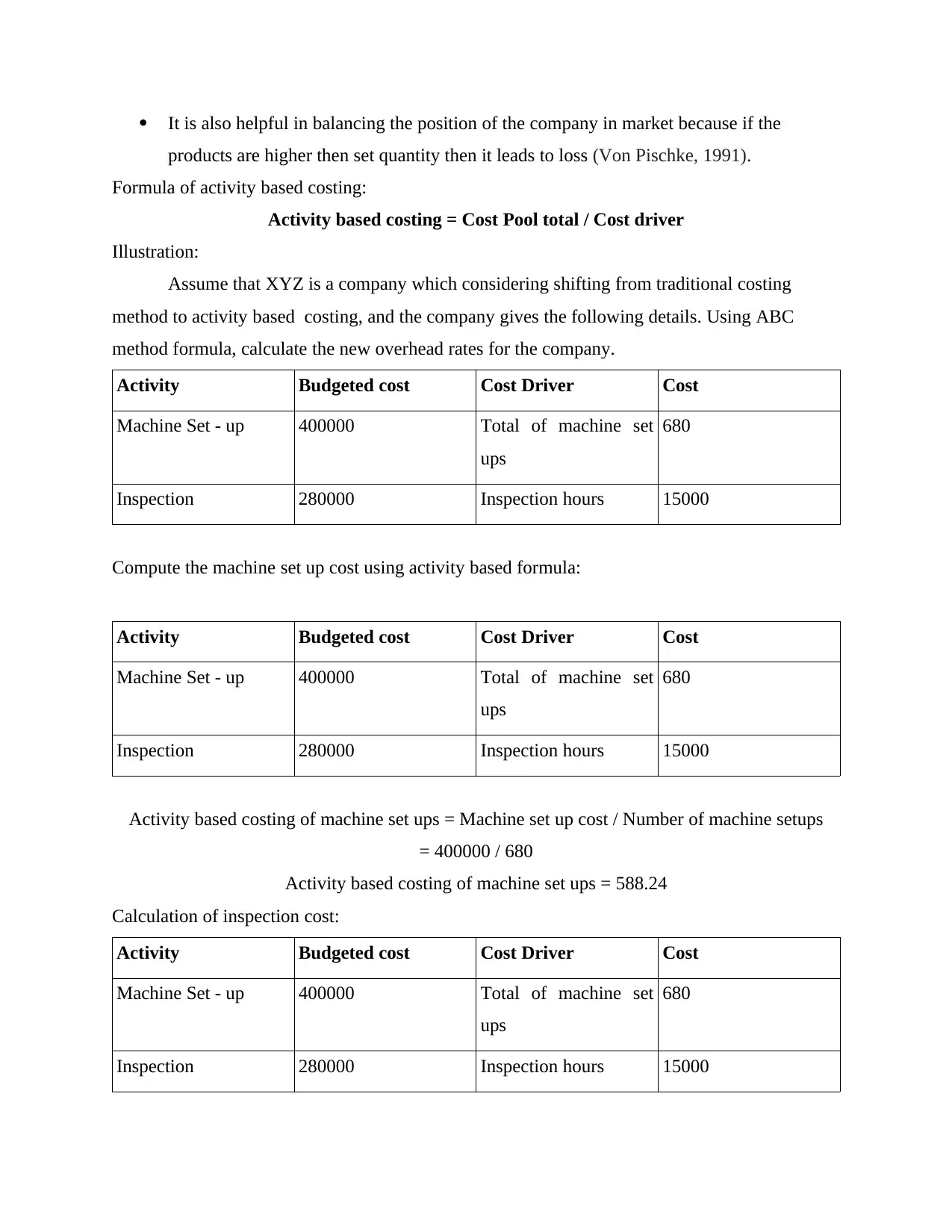

It is also helpful in balancing the position of the company in market because if the

products are higher then set quantity then it leads to loss (Von Pischke, 1991).

Formula of activity based costing:

Activity based costing = Cost Pool total / Cost driver

Illustration:

Assume that XYZ is a company which considering shifting from traditional costing

method to activity based costing, and the company gives the following details. Using ABC

method formula, calculate the new overhead rates for the company.

Activity Budgeted cost Cost Driver Cost

Machine Set - up 400000 Total of machine set

ups

680

Inspection 280000 Inspection hours 15000

Compute the machine set up cost using activity based formula:

Activity Budgeted cost Cost Driver Cost

Machine Set - up 400000 Total of machine set

ups

680

Inspection 280000 Inspection hours 15000

Activity based costing of machine set ups = Machine set up cost / Number of machine setups

= 400000 / 680

Activity based costing of machine set ups = 588.24

Calculation of inspection cost:

Activity Budgeted cost Cost Driver Cost

Machine Set - up 400000 Total of machine set

ups

680

Inspection 280000 Inspection hours 15000

products are higher then set quantity then it leads to loss (Von Pischke, 1991).

Formula of activity based costing:

Activity based costing = Cost Pool total / Cost driver

Illustration:

Assume that XYZ is a company which considering shifting from traditional costing

method to activity based costing, and the company gives the following details. Using ABC

method formula, calculate the new overhead rates for the company.

Activity Budgeted cost Cost Driver Cost

Machine Set - up 400000 Total of machine set

ups

680

Inspection 280000 Inspection hours 15000

Compute the machine set up cost using activity based formula:

Activity Budgeted cost Cost Driver Cost

Machine Set - up 400000 Total of machine set

ups

680

Inspection 280000 Inspection hours 15000

Activity based costing of machine set ups = Machine set up cost / Number of machine setups

= 400000 / 680

Activity based costing of machine set ups = 588.24

Calculation of inspection cost:

Activity Budgeted cost Cost Driver Cost

Machine Set - up 400000 Total of machine set

ups

680

Inspection 280000 Inspection hours 15000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity based costing of inspection cost = Inspection cost / Inspection hours

= 280000 / 15000

Activity based costing of inspection cost = 18.67

TASK 2

Provide Recommendation & Method of Cost Reductions

Cost reduction is a method of maximising profitability of the company. This method help in

reducing expenses and also help in reducing wastage of resources. Cost reduction is result

oriented process which help in achieving higher profits and higher performance. This method

improve the cash flows of a company. It is a very challenging process performed by the

management (Lerner, 1998).

A. Absorption costing : This method help in controlling the cost incurred in a product

life cycle with the help of planning and controlling. In this process the cost of product life cycle

is pre determined by management. This help in making quality product within lower cost.

Dysonica plc has to adopt such technique to improve profitability of its company.

Advantage of Absorption Costing:

This is the important method of evaluating stock in the income statement.

Generally accepted accounting principle (GAAP) and international financial reporting

standards also suggest this method to evaluate inventories.

This includes all expenses incurred in the manufacturing a product and its results are

more realistic and accurate.

It is also used for external reporting and it improve accountability of financial statements.

Disadvantage of Absorption Costing:

This method does not consider fix overhead accurately

Due to considering inaccurate fix overhead, the whole report is gone wrong.

Absorption costing is not used for managerial decision-makings.

This method is not used for calculating profitability of a product because of inaccurate fix

overheads in the valuation of stock (Summers and Wilson, 2000).

Absorption costing is not effective for cost control Because total cost is merger of all

costs where fix cost is also included which is not accurately included.

= 280000 / 15000

Activity based costing of inspection cost = 18.67

TASK 2

Provide Recommendation & Method of Cost Reductions

Cost reduction is a method of maximising profitability of the company. This method help in

reducing expenses and also help in reducing wastage of resources. Cost reduction is result

oriented process which help in achieving higher profits and higher performance. This method

improve the cash flows of a company. It is a very challenging process performed by the

management (Lerner, 1998).

A. Absorption costing : This method help in controlling the cost incurred in a product

life cycle with the help of planning and controlling. In this process the cost of product life cycle

is pre determined by management. This help in making quality product within lower cost.

Dysonica plc has to adopt such technique to improve profitability of its company.

Advantage of Absorption Costing:

This is the important method of evaluating stock in the income statement.

Generally accepted accounting principle (GAAP) and international financial reporting

standards also suggest this method to evaluate inventories.

This includes all expenses incurred in the manufacturing a product and its results are

more realistic and accurate.

It is also used for external reporting and it improve accountability of financial statements.

Disadvantage of Absorption Costing:

This method does not consider fix overhead accurately

Due to considering inaccurate fix overhead, the whole report is gone wrong.

Absorption costing is not used for managerial decision-makings.

This method is not used for calculating profitability of a product because of inaccurate fix

overheads in the valuation of stock (Summers and Wilson, 2000).

Absorption costing is not effective for cost control Because total cost is merger of all

costs where fix cost is also included which is not accurately included.

B. Marginal Costing: it refers to the change in the total cost of production due to

increase and decrease in the quantity of pre-determined output. This cost is depend upon the

desired output or additional unit of product (Mason and Harrison, 1992).

Advantage of Marginal Costing:

Marginal cost remain same in long term but the variable cost change time to time.

It exclude the fix cost so that management can easily handle marginal costing.

It divide cost into two parts one is Fixed and another is Variable cost. The valuation of

work-in-process and finish goods is more accurate.

It give proper vision to the company that what is beneficial for company to manufacture

or to purchase product.

Disadvantage of Marginal Costing:

It creates difficulties when cost separated into fixed and variable costs. Semi fixed and

semi variable cost not included in marginal costing.

Marginal costing ignored time element. Both the cost perform different in short term bu

in long term both cost are variable. In the long run cost change according to the

operations.

Forecast Sale price at all levels are same which may or may not be realised and give

unrealistic results.

This method not elaborate change in the production and sales.

In the marginal costing sale price is fixed according to contribution so it is difficult to fix.

Marginal cost only consider variable cost so it lose its importance in Capital industries.

C. Activity Based Costing: This techniques help in controlling future cost which

incurred in events and activities involved in the process of providing product or promoting

product (Mason and Harrison, 2004). The main purpose of this method is to reducing overhead

costs (Schmölders, 1959).

Advantage of Activity based Costing:

It provide actual cost of manufacturing products.

It provide better allocation for manufacturing expenditure for a product.

It help in identifying insufficient or inaccurate process and help to improve it,

More accurately maximise product profits.

Activity based costing stops unnecessary and wasted costs.

increase and decrease in the quantity of pre-determined output. This cost is depend upon the

desired output or additional unit of product (Mason and Harrison, 1992).

Advantage of Marginal Costing:

Marginal cost remain same in long term but the variable cost change time to time.

It exclude the fix cost so that management can easily handle marginal costing.

It divide cost into two parts one is Fixed and another is Variable cost. The valuation of

work-in-process and finish goods is more accurate.

It give proper vision to the company that what is beneficial for company to manufacture

or to purchase product.

Disadvantage of Marginal Costing:

It creates difficulties when cost separated into fixed and variable costs. Semi fixed and

semi variable cost not included in marginal costing.

Marginal costing ignored time element. Both the cost perform different in short term bu

in long term both cost are variable. In the long run cost change according to the

operations.

Forecast Sale price at all levels are same which may or may not be realised and give

unrealistic results.

This method not elaborate change in the production and sales.

In the marginal costing sale price is fixed according to contribution so it is difficult to fix.

Marginal cost only consider variable cost so it lose its importance in Capital industries.

C. Activity Based Costing: This techniques help in controlling future cost which

incurred in events and activities involved in the process of providing product or promoting

product (Mason and Harrison, 2004). The main purpose of this method is to reducing overhead

costs (Schmölders, 1959).

Advantage of Activity based Costing:

It provide actual cost of manufacturing products.

It provide better allocation for manufacturing expenditure for a product.

It help in identifying insufficient or inaccurate process and help to improve it,

More accurately maximise product profits.

Activity based costing stops unnecessary and wasted costs.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Disadvantage of Activity based Costing:

Activity based costing is a very time consuming process.

Collection of data and information is increase the cost of operation.

Data and information source is not easily available from accounting reports.

It is not useful in small expense management and the report of such costing is not used

for external reporting.

According to the above cost techniques. Dysonica plc is recommended to implement Activity

based costing and marginal costing in their planning an controlling process to achieve their

organisational goal. These techniques helps Dysonica plc in the management of the cost. They

are also help in reducing cost and maximising the profits. Marginal costing help to decrease cost

according to the predetermined outputs (Poon and Firth, 2005).

TASK 3

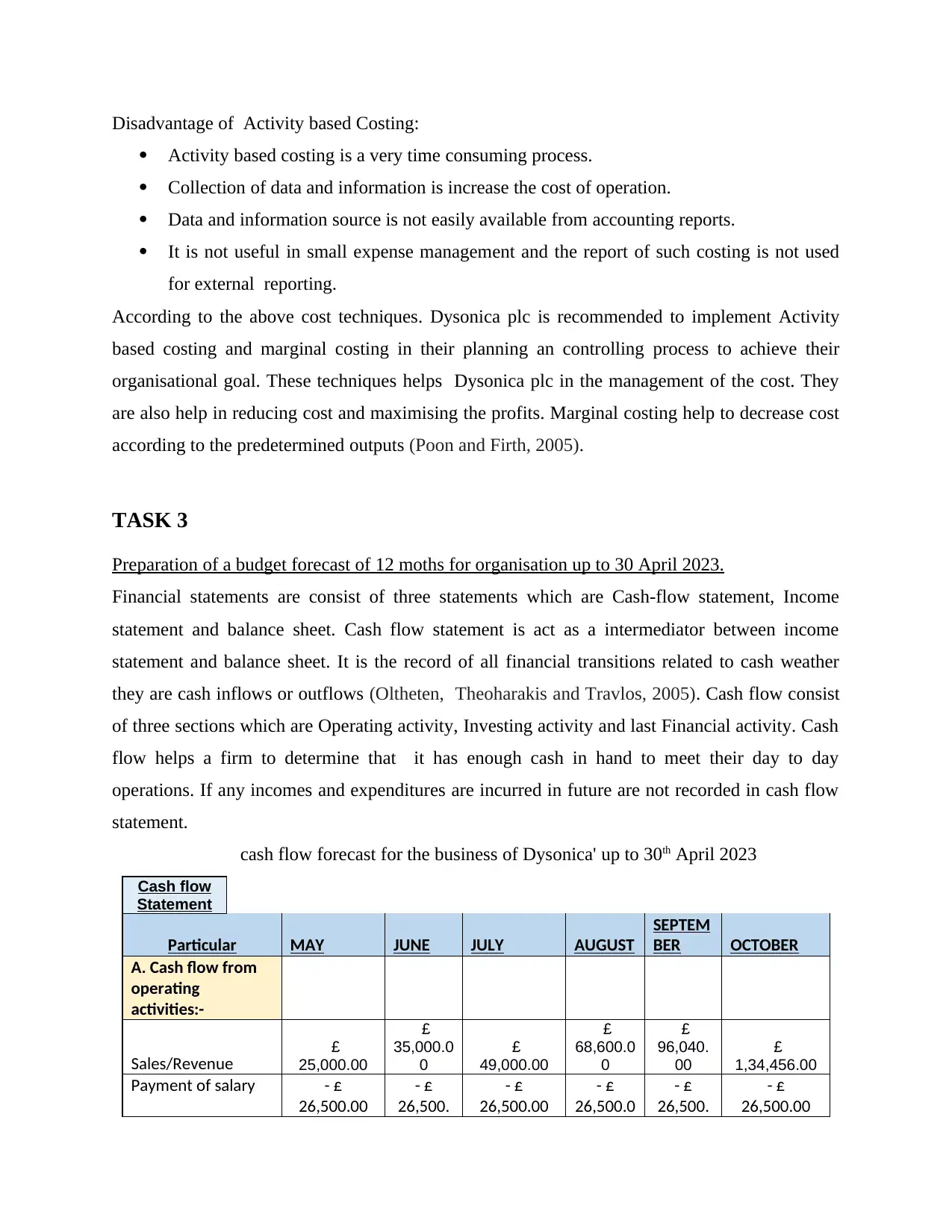

Preparation of a budget forecast of 12 moths for organisation up to 30 April 2023.

Financial statements are consist of three statements which are Cash-flow statement, Income

statement and balance sheet. Cash flow statement is act as a intermediator between income

statement and balance sheet. It is the record of all financial transitions related to cash weather

they are cash inflows or outflows (Oltheten, Theoharakis and Travlos, 2005). Cash flow consist

of three sections which are Operating activity, Investing activity and last Financial activity. Cash

flow helps a firm to determine that it has enough cash in hand to meet their day to day

operations. If any incomes and expenditures are incurred in future are not recorded in cash flow

statement.

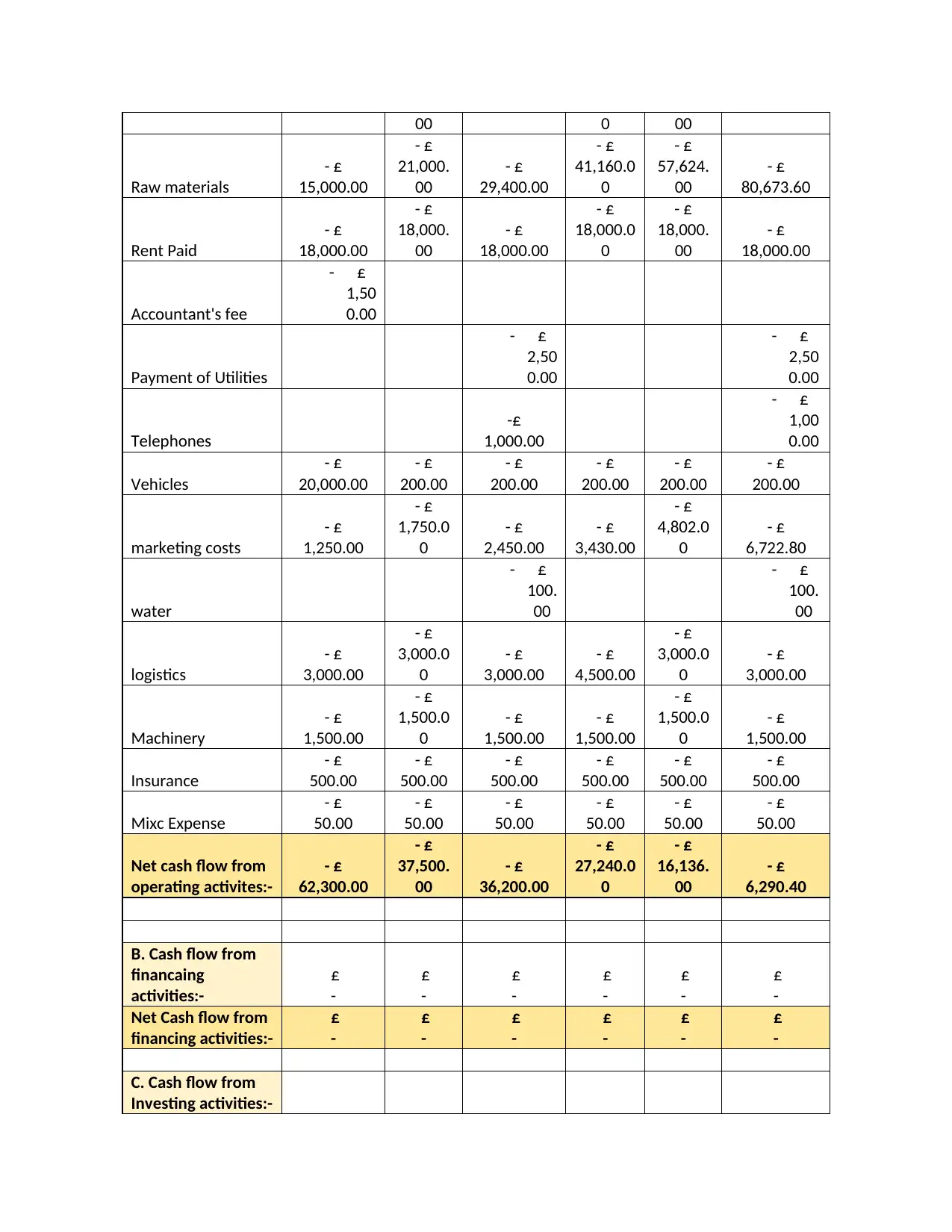

cash flow forecast for the business of Dysonica' up to 30th April 2023

Cash flow

Statement

Particular MAY JUNE JULY AUGUST

SEPTEM

BER OCTOBER

A. Cash flow from

operating

activities:-

Sales/Revenue £

25,000.00

£

35,000.0

0

£

49,000.00

£

68,600.0

0

£

96,040.

00

£

1,34,456.00

Payment of salary - £

26,500.00

- £

26,500.

- £

26,500.00

- £

26,500.0

- £

26,500.

- £

26,500.00

Activity based costing is a very time consuming process.

Collection of data and information is increase the cost of operation.

Data and information source is not easily available from accounting reports.

It is not useful in small expense management and the report of such costing is not used

for external reporting.

According to the above cost techniques. Dysonica plc is recommended to implement Activity

based costing and marginal costing in their planning an controlling process to achieve their

organisational goal. These techniques helps Dysonica plc in the management of the cost. They

are also help in reducing cost and maximising the profits. Marginal costing help to decrease cost

according to the predetermined outputs (Poon and Firth, 2005).

TASK 3

Preparation of a budget forecast of 12 moths for organisation up to 30 April 2023.

Financial statements are consist of three statements which are Cash-flow statement, Income

statement and balance sheet. Cash flow statement is act as a intermediator between income

statement and balance sheet. It is the record of all financial transitions related to cash weather

they are cash inflows or outflows (Oltheten, Theoharakis and Travlos, 2005). Cash flow consist

of three sections which are Operating activity, Investing activity and last Financial activity. Cash

flow helps a firm to determine that it has enough cash in hand to meet their day to day

operations. If any incomes and expenditures are incurred in future are not recorded in cash flow

statement.

cash flow forecast for the business of Dysonica' up to 30th April 2023

Cash flow

Statement

Particular MAY JUNE JULY AUGUST

SEPTEM

BER OCTOBER

A. Cash flow from

operating

activities:-

Sales/Revenue £

25,000.00

£

35,000.0

0

£

49,000.00

£

68,600.0

0

£

96,040.

00

£

1,34,456.00

Payment of salary - £

26,500.00

- £

26,500.

- £

26,500.00

- £

26,500.0

- £

26,500.

- £

26,500.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

00 0 00

Raw materials

- £

15,000.00

- £

21,000.

00

- £

29,400.00

- £

41,160.0

0

- £

57,624.

00

- £

80,673.60

Rent Paid

- £

18,000.00

- £

18,000.

00

- £

18,000.00

- £

18,000.0

0

- £

18,000.

00

- £

18,000.00

Accountant's fee

- £

1,50

0.00

Payment of Utilities

- £

2,50

0.00

- £

2,50

0.00

Telephones

-£

1,000.00

- £

1,00

0.00

Vehicles

- £

20,000.00

- £

200.00

- £

200.00

- £

200.00

- £

200.00

- £

200.00

marketing costs

- £

1,250.00

- £

1,750.0

0

- £

2,450.00

- £

3,430.00

- £

4,802.0

0

- £

6,722.80

water

- £

100.

00

- £

100.

00

logistics

- £

3,000.00

- £

3,000.0

0

- £

3,000.00

- £

4,500.00

- £

3,000.0

0

- £

3,000.00

Machinery

- £

1,500.00

- £

1,500.0

0

- £

1,500.00

- £

1,500.00

- £

1,500.0

0

- £

1,500.00

Insurance

- £

500.00

- £

500.00

- £

500.00

- £

500.00

- £

500.00

- £

500.00

Mixc Expense

- £

50.00

- £

50.00

- £

50.00

- £

50.00

- £

50.00

- £

50.00

Net cash flow from

operating activites:-

- £

62,300.00

- £

37,500.

00

- £

36,200.00

- £

27,240.0

0

- £

16,136.

00

- £

6,290.40

B. Cash flow from

financaing

activities:-

£

-

£

-

£

-

£

-

£

-

£

-

Net Cash flow from

financing activities:-

£

-

£

-

£

-

£

-

£

-

£

-

C. Cash flow from

Investing activities:-

Raw materials

- £

15,000.00

- £

21,000.

00

- £

29,400.00

- £

41,160.0

0

- £

57,624.

00

- £

80,673.60

Rent Paid

- £

18,000.00

- £

18,000.

00

- £

18,000.00

- £

18,000.0

0

- £

18,000.

00

- £

18,000.00

Accountant's fee

- £

1,50

0.00

Payment of Utilities

- £

2,50

0.00

- £

2,50

0.00

Telephones

-£

1,000.00

- £

1,00

0.00

Vehicles

- £

20,000.00

- £

200.00

- £

200.00

- £

200.00

- £

200.00

- £

200.00

marketing costs

- £

1,250.00

- £

1,750.0

0

- £

2,450.00

- £

3,430.00

- £

4,802.0

0

- £

6,722.80

water

- £

100.

00

- £

100.

00

logistics

- £

3,000.00

- £

3,000.0

0

- £

3,000.00

- £

4,500.00

- £

3,000.0

0

- £

3,000.00

Machinery

- £

1,500.00

- £

1,500.0

0

- £

1,500.00

- £

1,500.00

- £

1,500.0

0

- £

1,500.00

Insurance

- £

500.00

- £

500.00

- £

500.00

- £

500.00

- £

500.00

- £

500.00

Mixc Expense

- £

50.00

- £

50.00

- £

50.00

- £

50.00

- £

50.00

- £

50.00

Net cash flow from

operating activites:-

- £

62,300.00

- £

37,500.

00

- £

36,200.00

- £

27,240.0

0

- £

16,136.

00

- £

6,290.40

B. Cash flow from

financaing

activities:-

£

-

£

-

£

-

£

-

£

-

£

-

Net Cash flow from

financing activities:-

£

-

£

-

£

-

£

-

£

-

£

-

C. Cash flow from

Investing activities:-

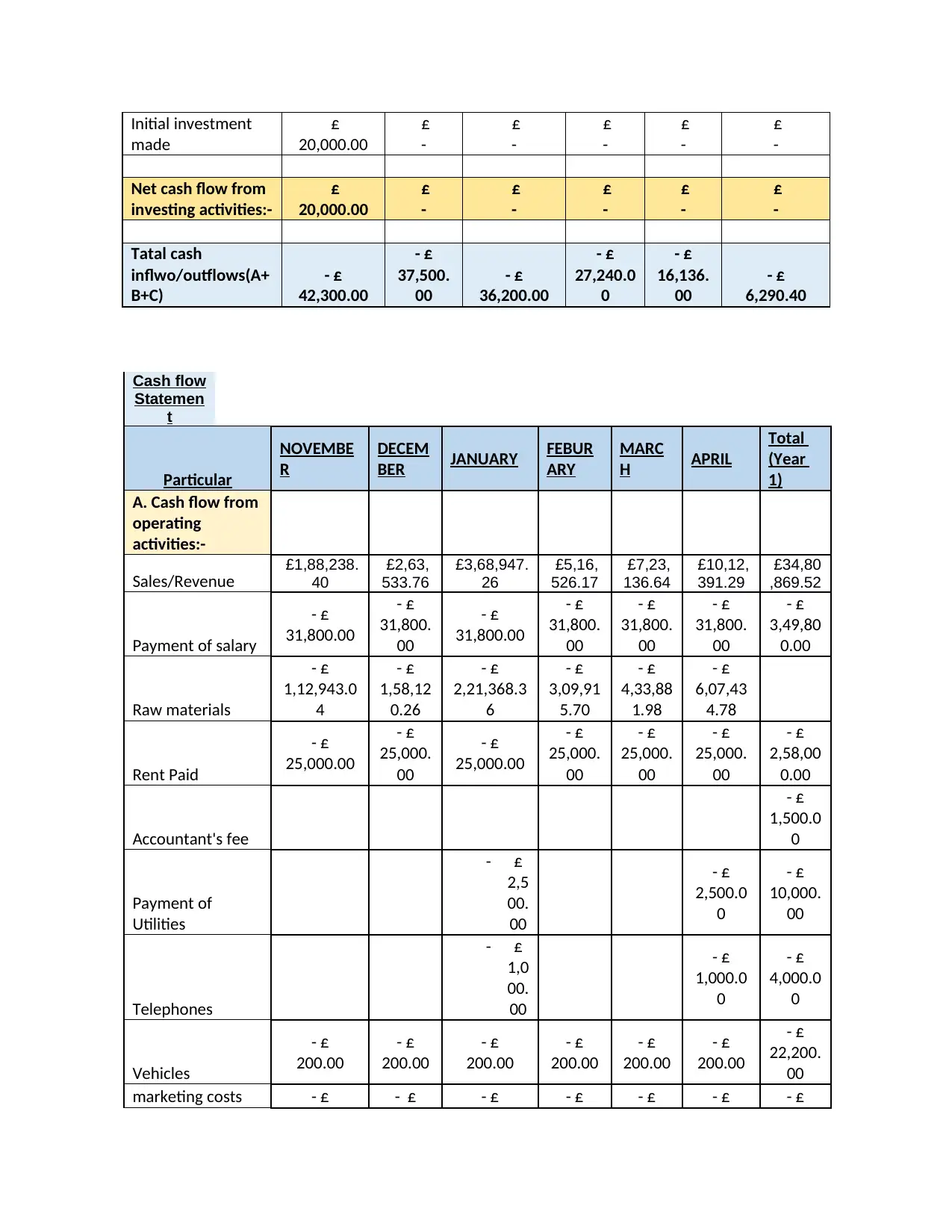

Initial investment

made

£

20,000.00

£

-

£

-

£

-

£

-

£

-

Net cash flow from

investing activities:-

£

20,000.00

£

-

£

-

£

-

£

-

£

-

Tatal cash

inflwo/outflows(A+

B+C)

- £

42,300.00

- £

37,500.

00

- £

36,200.00

- £

27,240.0

0

- £

16,136.

00

- £

6,290.40

Cash flow

Statemen

t

Particular

NOVEMBE

R

DECEM

BER JANUARY FEBUR

ARY

MARC

H APRIL

Total

(Year

1)

A. Cash flow from

operating

activities:-

Sales/Revenue £1,88,238.

40

£2,63,

533.76

£3,68,947.

26

£5,16,

526.17

£7,23,

136.64

£10,12,

391.29

£34,80

,869.52

Payment of salary

- £

31,800.00

- £

31,800.

00

- £

31,800.00

- £

31,800.

00

- £

31,800.

00

- £

31,800.

00

- £

3,49,80

0.00

Raw materials

- £

1,12,943.0

4

- £

1,58,12

0.26

- £

2,21,368.3

6

- £

3,09,91

5.70

- £

4,33,88

1.98

- £

6,07,43

4.78

Rent Paid

- £

25,000.00

- £

25,000.

00

- £

25,000.00

- £

25,000.

00

- £

25,000.

00

- £

25,000.

00

- £

2,58,00

0.00

Accountant's fee

- £

1,500.0

0

Payment of

Utilities

- £

2,5

00.

00

- £

2,500.0

0

- £

10,000.

00

Telephones

- £

1,0

00.

00

- £

1,000.0

0

- £

4,000.0

0

Vehicles

- £

200.00

- £

200.00

- £

200.00

- £

200.00

- £

200.00

- £

200.00

- £

22,200.

00

marketing costs - £ - £ - £ - £ - £ - £ - £

made

£

20,000.00

£

-

£

-

£

-

£

-

£

-

Net cash flow from

investing activities:-

£

20,000.00

£

-

£

-

£

-

£

-

£

-

Tatal cash

inflwo/outflows(A+

B+C)

- £

42,300.00

- £

37,500.

00

- £

36,200.00

- £

27,240.0

0

- £

16,136.

00

- £

6,290.40

Cash flow

Statemen

t

Particular

NOVEMBE

R

DECEM

BER JANUARY FEBUR

ARY

MARC

H APRIL

Total

(Year

1)

A. Cash flow from

operating

activities:-

Sales/Revenue £1,88,238.

40

£2,63,

533.76

£3,68,947.

26

£5,16,

526.17

£7,23,

136.64

£10,12,

391.29

£34,80

,869.52

Payment of salary

- £

31,800.00

- £

31,800.

00

- £

31,800.00

- £

31,800.

00

- £

31,800.

00

- £

31,800.

00

- £

3,49,80

0.00

Raw materials

- £

1,12,943.0

4

- £

1,58,12

0.26

- £

2,21,368.3

6

- £

3,09,91

5.70

- £

4,33,88

1.98

- £

6,07,43

4.78

Rent Paid

- £

25,000.00

- £

25,000.

00

- £

25,000.00

- £

25,000.

00

- £

25,000.

00

- £

25,000.

00

- £

2,58,00

0.00

Accountant's fee

- £

1,500.0

0

Payment of

Utilities

- £

2,5

00.

00

- £

2,500.0

0

- £

10,000.

00

Telephones

- £

1,0

00.

00

- £

1,000.0

0

- £

4,000.0

0

Vehicles

- £

200.00

- £

200.00

- £

200.00

- £

200.00

- £

200.00

- £

200.00

- £

22,200.

00

marketing costs - £ - £ - £ - £ - £ - £ - £

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.