Costs and Revenues: Analyzing Costs, Reporting, and Activity Levels

VerifiedAdded on 2020/11/12

|21

|4061

|378

Report

AI Summary

This report provides a detailed analysis of costs and revenues within an organization, covering various aspects of financial management. It begins by outlining the purpose of internal reporting and its importance in providing accurate information to management, as well as examining the relationships between different costing systems like absorption and marginal costing. The report then delves into the identification of responsibility centers, including cost centers, profit centers, and investment centers, and explores different cost classification types and their applications in costing. Furthermore, it differentiates between marginal and absorption costing, highlighting their respective uses. The report also includes the recording and analysis of cost information for labor, materials, and expenses, along with an examination of inventory stages and valuation methods, like FIFO. Additionally, the report covers the behavior of different costs and the application of various costing systems. The report also covers attributing overhead costs, calculating absorption rates, adjusting for under or over-recovered overhead, and reviewing allocation methods. Finally, it discusses the preparation of management reports and the impact of changing activity levels on unit costs.

Costs and Revenues

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

TASK 1............................................................................................................................................1

1. Purpose of internal reporting as well as providing accurate information to management......1

2. Relationship between different costing system within organisation.......................................1

3. Determine responsibility centres, cost centres, profit centres and investment centres within

company......................................................................................................................................2

4. Characteristics of several types of cost classification as well as their use in costing.............2

5. Difference between marginal and absorption costing.............................................................3

TASK 2............................................................................................................................................3

1. Recording cost information for labour material and expenses................................................3

2. Analysing the cost of information for labour, material and expenses according to the

process of organisation. ..............................................................................................................4

3. Different Stages of Inventory..................................................................................................4

4. Inventory Valuation using different methods.........................................................................5

5. Behaviour of Different cost.....................................................................................................7

6. Recording cost information by using different costing systems.............................................8

TASK 3............................................................................................................................................8

3.1.Attributing overhead costs ...................................................................................................8

3.2 Calculating overhead absorption rates according to the suitable bases of absorption..........9

3.3 Adjustments for under or over recovered overhead costs in accordance with established

procedure...................................................................................................................................11

3.4 Reviewing method of allocation apportionment and absorption at regular intervals,

implementing agreed changes to methods................................................................................12

TASK 4..........................................................................................................................................13

4.4 Prepaing management report in an appropriate format.......................................................14

TASK 5..........................................................................................................................................14

5.3 Calculating the effect of changing activity level on unit costs...........................................16

REFERENCES..............................................................................................................................17

TASK 1............................................................................................................................................1

1. Purpose of internal reporting as well as providing accurate information to management......1

2. Relationship between different costing system within organisation.......................................1

3. Determine responsibility centres, cost centres, profit centres and investment centres within

company......................................................................................................................................2

4. Characteristics of several types of cost classification as well as their use in costing.............2

5. Difference between marginal and absorption costing.............................................................3

TASK 2............................................................................................................................................3

1. Recording cost information for labour material and expenses................................................3

2. Analysing the cost of information for labour, material and expenses according to the

process of organisation. ..............................................................................................................4

3. Different Stages of Inventory..................................................................................................4

4. Inventory Valuation using different methods.........................................................................5

5. Behaviour of Different cost.....................................................................................................7

6. Recording cost information by using different costing systems.............................................8

TASK 3............................................................................................................................................8

3.1.Attributing overhead costs ...................................................................................................8

3.2 Calculating overhead absorption rates according to the suitable bases of absorption..........9

3.3 Adjustments for under or over recovered overhead costs in accordance with established

procedure...................................................................................................................................11

3.4 Reviewing method of allocation apportionment and absorption at regular intervals,

implementing agreed changes to methods................................................................................12

TASK 4..........................................................................................................................................13

4.4 Prepaing management report in an appropriate format.......................................................14

TASK 5..........................................................................................................................................14

5.3 Calculating the effect of changing activity level on unit costs...........................................16

REFERENCES..............................................................................................................................17

TASK 1

1. Purpose of internal reporting as well as providing accurate information to management.

Internal reporting system is the system that provides information related to the business at

all levels to management (Ghiyasi, 2017). With the help of internal reporting system, it becomes

easy to detect the performance as well as responsibilities of various centres.

The main purpose of internal reporting system are as follows-

It allows manager to take decision for the businesses.

It aids transparency in the work of management.

Stakeholders which have higher interest with the company are informed about the

performance of organisation.

It also aids in identifying the financial performance of the company with some

analysis tools such as cash flow.

It also facilitates in improving the efficiency of senior manager of the

organisation.

2. Relationship between different costing system within organisation.

Absorption, marginal, standard and historical are some types of costing system that are

usually adopted by the organisation in order to allocate various expenditure overheads. These all

types of cost are interlinked and as marginal costing and absorption costing are used by the

organisation to check the profitability of the company as profit per unit and cost per unit. Both

these types of costing helps the management of organisation in decision making like in preparing

budget and other expenses or resources. In addition to this, with the help of these costing,

management make sure that there should be proper allocation of the cost to several overheads. It

results in accurate identification cost of each input which is used in the process of production.

Moreover, in standard and historical costing are also used by the management in order to make

effective decisions for the businesses regarding the allocation of cost (Shepherd, 2015).

On the other hand, the difference among these two costing (marginal and absorption) is

that marginal costing considers variable cost whereas absorption costing used both variable and

fixed cost.

1

1. Purpose of internal reporting as well as providing accurate information to management.

Internal reporting system is the system that provides information related to the business at

all levels to management (Ghiyasi, 2017). With the help of internal reporting system, it becomes

easy to detect the performance as well as responsibilities of various centres.

The main purpose of internal reporting system are as follows-

It allows manager to take decision for the businesses.

It aids transparency in the work of management.

Stakeholders which have higher interest with the company are informed about the

performance of organisation.

It also aids in identifying the financial performance of the company with some

analysis tools such as cash flow.

It also facilitates in improving the efficiency of senior manager of the

organisation.

2. Relationship between different costing system within organisation.

Absorption, marginal, standard and historical are some types of costing system that are

usually adopted by the organisation in order to allocate various expenditure overheads. These all

types of cost are interlinked and as marginal costing and absorption costing are used by the

organisation to check the profitability of the company as profit per unit and cost per unit. Both

these types of costing helps the management of organisation in decision making like in preparing

budget and other expenses or resources. In addition to this, with the help of these costing,

management make sure that there should be proper allocation of the cost to several overheads. It

results in accurate identification cost of each input which is used in the process of production.

Moreover, in standard and historical costing are also used by the management in order to make

effective decisions for the businesses regarding the allocation of cost (Shepherd, 2015).

On the other hand, the difference among these two costing (marginal and absorption) is

that marginal costing considers variable cost whereas absorption costing used both variable and

fixed cost.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3. Determine responsibility centres, cost centres, profit centres and investment centres within

company.

Responsibility centres is the part of the organisation for which manager has responsibility

as well as authority. All the responsibilities and authorities are assigned to all the manager.

Departments are the most common responsibility centre within organisation.

Cost Centres are is also one of the most important department within organisation as it is

concerned with the allocation of cost but they are not responsible for the revenues or investment

decision. They are not responsible for the profitability of the company (Nguyen, 2018).

Profit Centres are is the part of company with assigned revenues as well as cost and

hence ascertainable profitability. Profit and losses of this department are evaluated separately.

Manager at profit centres are responsible for managing all the activities of sales which leads to

more revenues than the cost of those activities. This centres is very beneficial for the company as

by creating separate profit centres, management can measures the profitability of each activities

of business.

Investment Centre is also one of the essential unit of the business organisation. The

managers in the investment centres are responsible for measuring the performance of all the

departments of the organisation (Weisbach, Hemel and Nou, 2018). Cost, capital expenditure,

revenue are considered by the investment centre in the form of asserts which are used in the

process of production. They contribute profitability of the company.

4. Characteristics of several types of cost classification as well as their use in costing.

There are several types of costing that company incurs in buying and selling of goods and

services which are as follows-

Variable Cost- These are type of cost that changes in proportionate with the level of

output. This is the type of cost that varies depending on the number of good a company

manufactures.

Fixed Cost- These are the types of cost which do not vary with the respect to changes in

output and would occur when no output was manufactures. For example- payment of interest,

rent, taxes, salary and wages etc.

Total Cost- This is total of fixed and variable cost (Yang and Chen, 2018).

Semi-variable Cost- Mixture of both variable and fixed cost are called as semi-variable

cost as to some extent it remains fixed but after passing the limit it becomes variable cost.

2

company.

Responsibility centres is the part of the organisation for which manager has responsibility

as well as authority. All the responsibilities and authorities are assigned to all the manager.

Departments are the most common responsibility centre within organisation.

Cost Centres are is also one of the most important department within organisation as it is

concerned with the allocation of cost but they are not responsible for the revenues or investment

decision. They are not responsible for the profitability of the company (Nguyen, 2018).

Profit Centres are is the part of company with assigned revenues as well as cost and

hence ascertainable profitability. Profit and losses of this department are evaluated separately.

Manager at profit centres are responsible for managing all the activities of sales which leads to

more revenues than the cost of those activities. This centres is very beneficial for the company as

by creating separate profit centres, management can measures the profitability of each activities

of business.

Investment Centre is also one of the essential unit of the business organisation. The

managers in the investment centres are responsible for measuring the performance of all the

departments of the organisation (Weisbach, Hemel and Nou, 2018). Cost, capital expenditure,

revenue are considered by the investment centre in the form of asserts which are used in the

process of production. They contribute profitability of the company.

4. Characteristics of several types of cost classification as well as their use in costing.

There are several types of costing that company incurs in buying and selling of goods and

services which are as follows-

Variable Cost- These are type of cost that changes in proportionate with the level of

output. This is the type of cost that varies depending on the number of good a company

manufactures.

Fixed Cost- These are the types of cost which do not vary with the respect to changes in

output and would occur when no output was manufactures. For example- payment of interest,

rent, taxes, salary and wages etc.

Total Cost- This is total of fixed and variable cost (Yang and Chen, 2018).

Semi-variable Cost- Mixture of both variable and fixed cost are called as semi-variable

cost as to some extent it remains fixed but after passing the limit it becomes variable cost.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

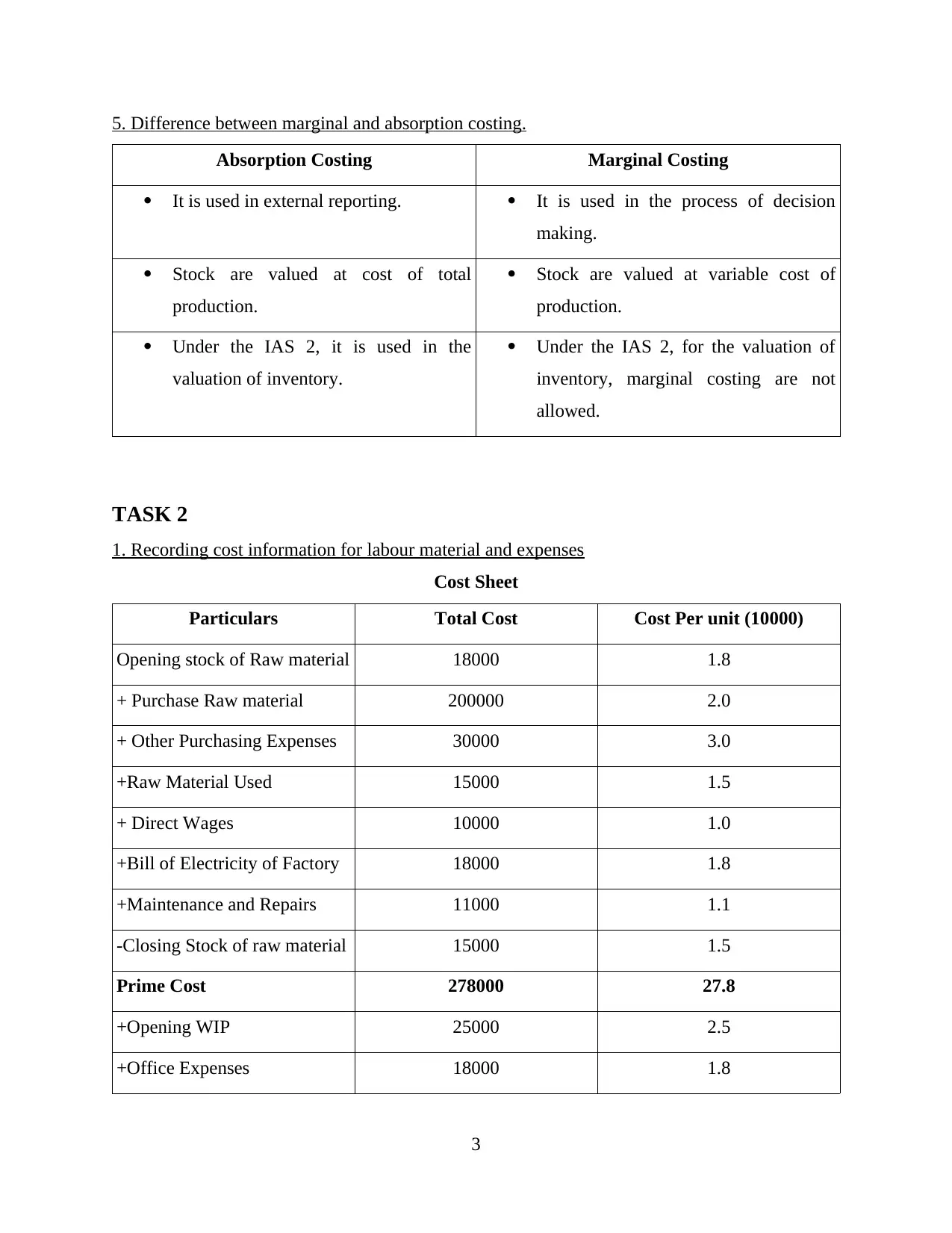

5. Difference between marginal and absorption costing.

Absorption Costing Marginal Costing

It is used in external reporting. It is used in the process of decision

making.

Stock are valued at cost of total

production.

Stock are valued at variable cost of

production.

Under the IAS 2, it is used in the

valuation of inventory.

Under the IAS 2, for the valuation of

inventory, marginal costing are not

allowed.

TASK 2

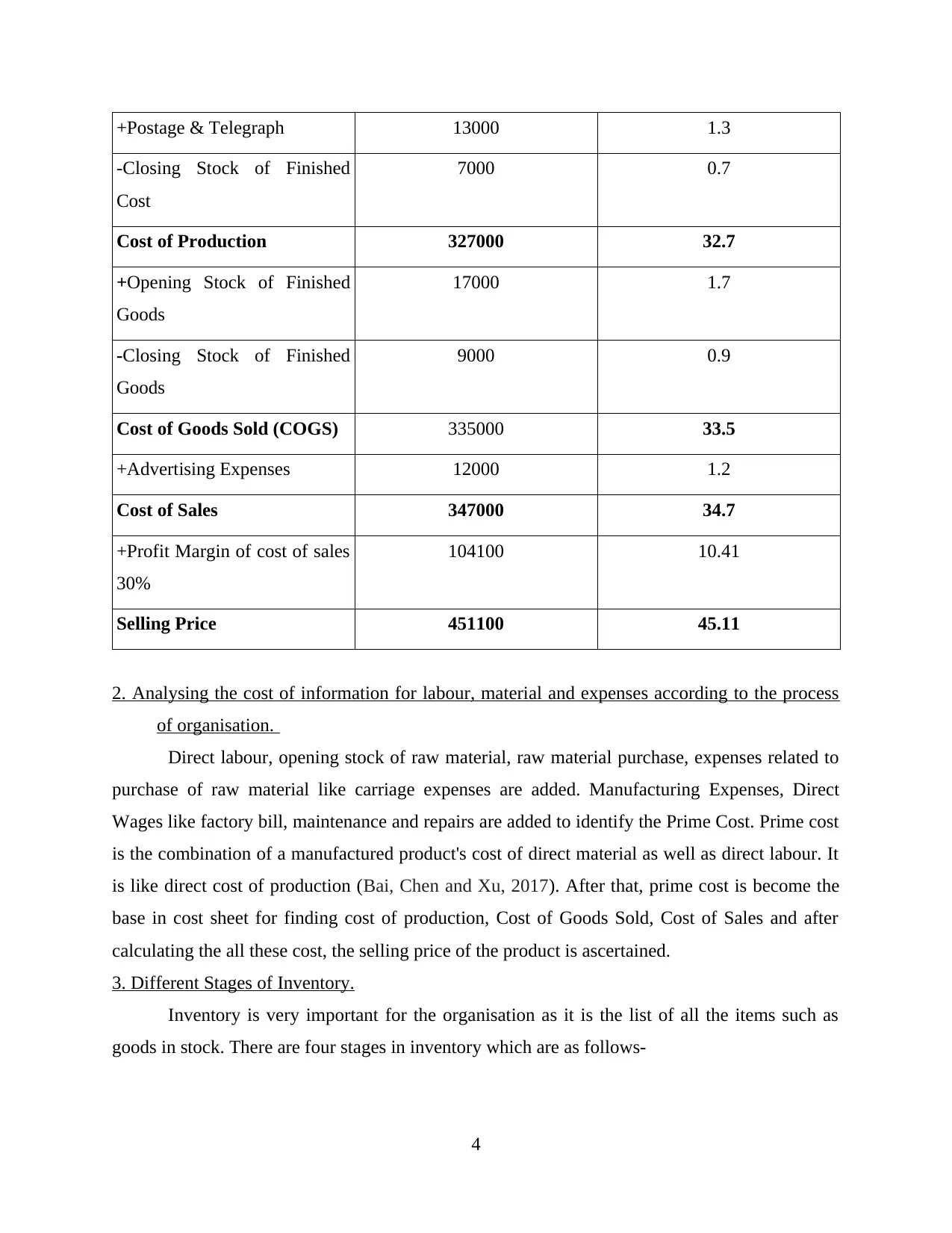

1. Recording cost information for labour material and expenses

Cost Sheet

Particulars Total Cost Cost Per unit (10000)

Opening stock of Raw material 18000 1.8

+ Purchase Raw material 200000 2.0

+ Other Purchasing Expenses 30000 3.0

+Raw Material Used 15000 1.5

+ Direct Wages 10000 1.0

+Bill of Electricity of Factory 18000 1.8

+Maintenance and Repairs 11000 1.1

-Closing Stock of raw material 15000 1.5

Prime Cost 278000 27.8

+Opening WIP 25000 2.5

+Office Expenses 18000 1.8

3

Absorption Costing Marginal Costing

It is used in external reporting. It is used in the process of decision

making.

Stock are valued at cost of total

production.

Stock are valued at variable cost of

production.

Under the IAS 2, it is used in the

valuation of inventory.

Under the IAS 2, for the valuation of

inventory, marginal costing are not

allowed.

TASK 2

1. Recording cost information for labour material and expenses

Cost Sheet

Particulars Total Cost Cost Per unit (10000)

Opening stock of Raw material 18000 1.8

+ Purchase Raw material 200000 2.0

+ Other Purchasing Expenses 30000 3.0

+Raw Material Used 15000 1.5

+ Direct Wages 10000 1.0

+Bill of Electricity of Factory 18000 1.8

+Maintenance and Repairs 11000 1.1

-Closing Stock of raw material 15000 1.5

Prime Cost 278000 27.8

+Opening WIP 25000 2.5

+Office Expenses 18000 1.8

3

+Postage & Telegraph 13000 1.3

-Closing Stock of Finished

Cost

7000 0.7

Cost of Production 327000 32.7

+Opening Stock of Finished

Goods

17000 1.7

-Closing Stock of Finished

Goods

9000 0.9

Cost of Goods Sold (COGS) 335000 33.5

+Advertising Expenses 12000 1.2

Cost of Sales 347000 34.7

+Profit Margin of cost of sales

30%

104100 10.41

Selling Price 451100 45.11

2. Analysing the cost of information for labour, material and expenses according to the process

of organisation.

Direct labour, opening stock of raw material, raw material purchase, expenses related to

purchase of raw material like carriage expenses are added. Manufacturing Expenses, Direct

Wages like factory bill, maintenance and repairs are added to identify the Prime Cost. Prime cost

is the combination of a manufactured product's cost of direct material as well as direct labour. It

is like direct cost of production (Bai, Chen and Xu, 2017). After that, prime cost is become the

base in cost sheet for finding cost of production, Cost of Goods Sold, Cost of Sales and after

calculating the all these cost, the selling price of the product is ascertained.

3. Different Stages of Inventory.

Inventory is very important for the organisation as it is the list of all the items such as

goods in stock. There are four stages in inventory which are as follows-

4

-Closing Stock of Finished

Cost

7000 0.7

Cost of Production 327000 32.7

+Opening Stock of Finished

Goods

17000 1.7

-Closing Stock of Finished

Goods

9000 0.9

Cost of Goods Sold (COGS) 335000 33.5

+Advertising Expenses 12000 1.2

Cost of Sales 347000 34.7

+Profit Margin of cost of sales

30%

104100 10.41

Selling Price 451100 45.11

2. Analysing the cost of information for labour, material and expenses according to the process

of organisation.

Direct labour, opening stock of raw material, raw material purchase, expenses related to

purchase of raw material like carriage expenses are added. Manufacturing Expenses, Direct

Wages like factory bill, maintenance and repairs are added to identify the Prime Cost. Prime cost

is the combination of a manufactured product's cost of direct material as well as direct labour. It

is like direct cost of production (Bai, Chen and Xu, 2017). After that, prime cost is become the

base in cost sheet for finding cost of production, Cost of Goods Sold, Cost of Sales and after

calculating the all these cost, the selling price of the product is ascertained.

3. Different Stages of Inventory.

Inventory is very important for the organisation as it is the list of all the items such as

goods in stock. There are four stages in inventory which are as follows-

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

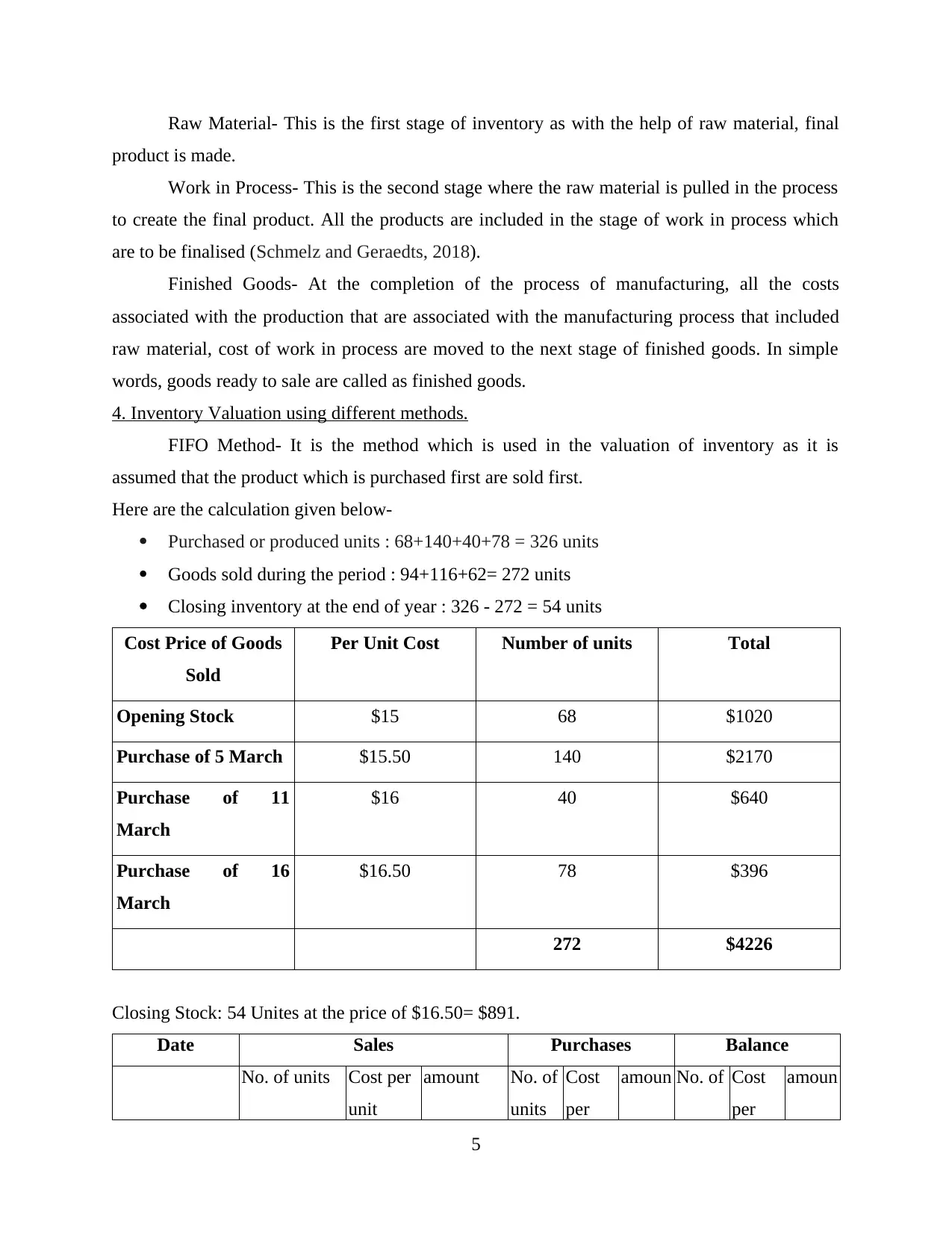

Raw Material- This is the first stage of inventory as with the help of raw material, final

product is made.

Work in Process- This is the second stage where the raw material is pulled in the process

to create the final product. All the products are included in the stage of work in process which

are to be finalised (Schmelz and Geraedts, 2018).

Finished Goods- At the completion of the process of manufacturing, all the costs

associated with the production that are associated with the manufacturing process that included

raw material, cost of work in process are moved to the next stage of finished goods. In simple

words, goods ready to sale are called as finished goods.

4. Inventory Valuation using different methods.

FIFO Method- It is the method which is used in the valuation of inventory as it is

assumed that the product which is purchased first are sold first.

Here are the calculation given below-

Purchased or produced units : 68+140+40+78 = 326 units

Goods sold during the period : 94+116+62= 272 units

Closing inventory at the end of year : 326 - 272 = 54 units

Cost Price of Goods

Sold

Per Unit Cost Number of units Total

Opening Stock $15 68 $1020

Purchase of 5 March $15.50 140 $2170

Purchase of 11

March

$16 40 $640

Purchase of 16

March

$16.50 78 $396

272 $4226

Closing Stock: 54 Unites at the price of $16.50= $891.

Date Sales Purchases Balance

No. of units Cost per

unit

amount No. of

units

Cost

per

amoun No. of Cost

per

amoun

5

product is made.

Work in Process- This is the second stage where the raw material is pulled in the process

to create the final product. All the products are included in the stage of work in process which

are to be finalised (Schmelz and Geraedts, 2018).

Finished Goods- At the completion of the process of manufacturing, all the costs

associated with the production that are associated with the manufacturing process that included

raw material, cost of work in process are moved to the next stage of finished goods. In simple

words, goods ready to sale are called as finished goods.

4. Inventory Valuation using different methods.

FIFO Method- It is the method which is used in the valuation of inventory as it is

assumed that the product which is purchased first are sold first.

Here are the calculation given below-

Purchased or produced units : 68+140+40+78 = 326 units

Goods sold during the period : 94+116+62= 272 units

Closing inventory at the end of year : 326 - 272 = 54 units

Cost Price of Goods

Sold

Per Unit Cost Number of units Total

Opening Stock $15 68 $1020

Purchase of 5 March $15.50 140 $2170

Purchase of 11

March

$16 40 $640

Purchase of 16

March

$16.50 78 $396

272 $4226

Closing Stock: 54 Unites at the price of $16.50= $891.

Date Sales Purchases Balance

No. of units Cost per

unit

amount No. of

units

Cost

per

amoun No. of Cost

per

amoun

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

unit t units unit t

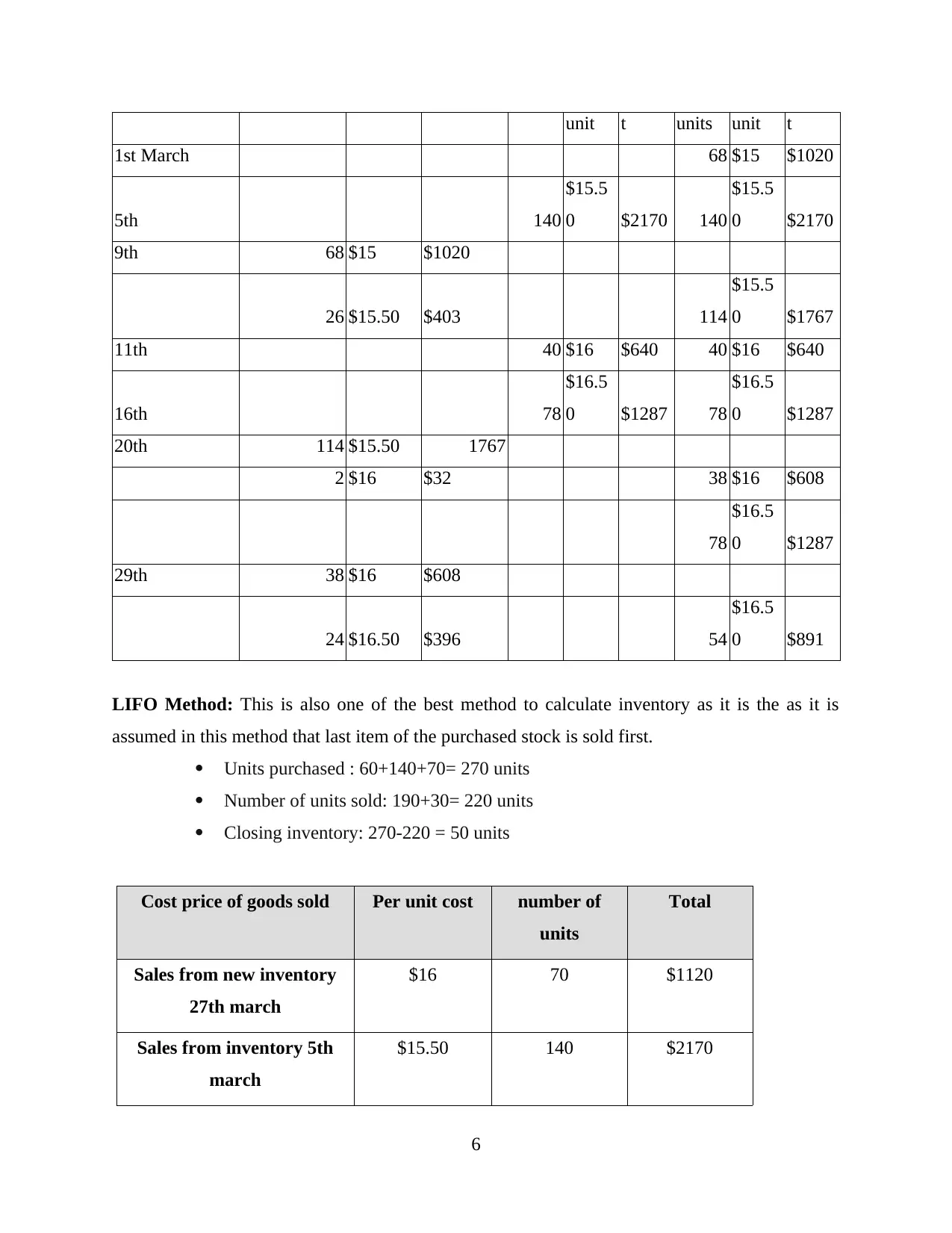

1st March 68 $15 $1020

5th 140

$15.5

0 $2170 140

$15.5

0 $2170

9th 68 $15 $1020

26 $15.50 $403 114

$15.5

0 $1767

11th 40 $16 $640 40 $16 $640

16th 78

$16.5

0 $1287 78

$16.5

0 $1287

20th 114 $15.50 1767

2 $16 $32 38 $16 $608

78

$16.5

0 $1287

29th 38 $16 $608

24 $16.50 $396 54

$16.5

0 $891

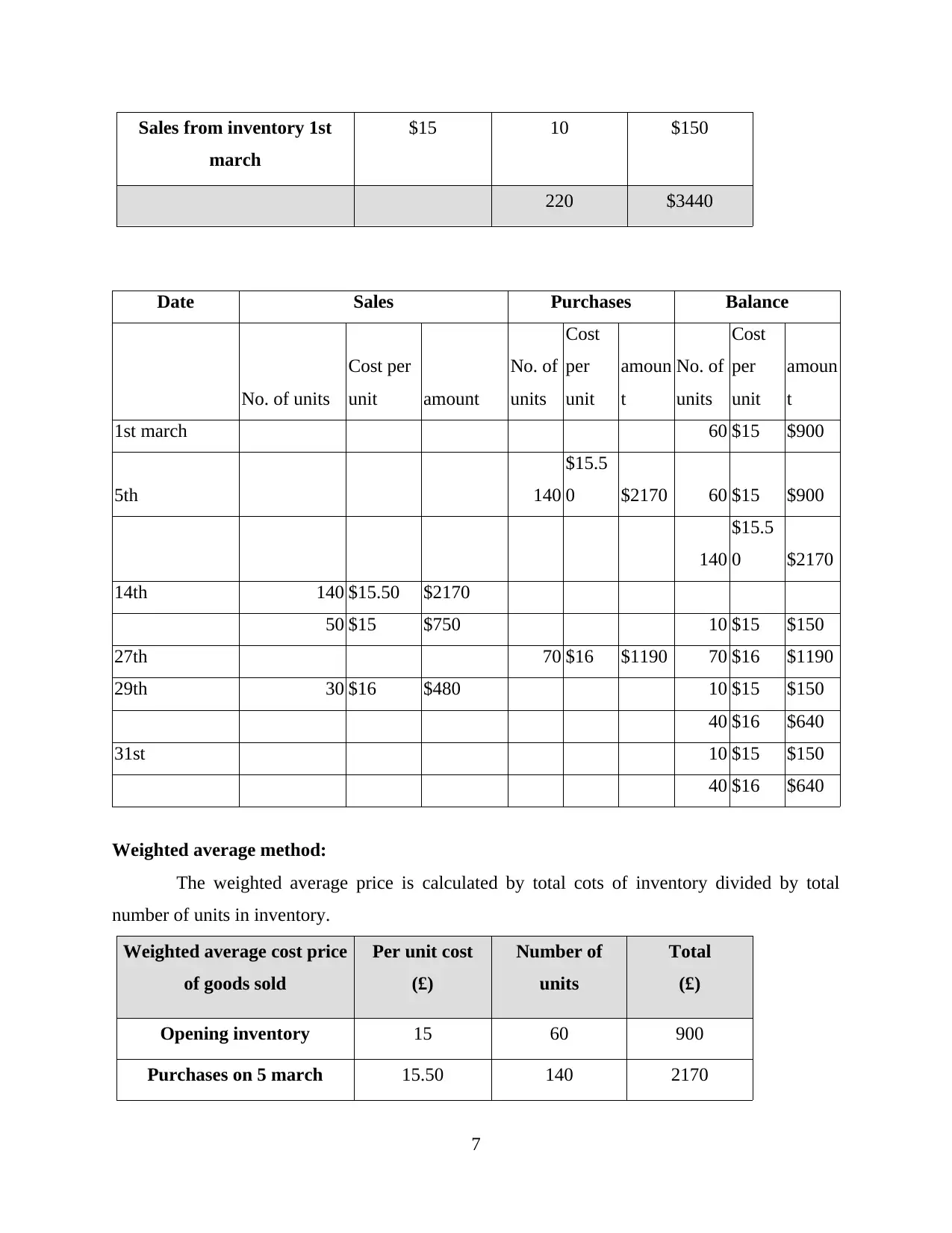

LIFO Method: This is also one of the best method to calculate inventory as it is the as it is

assumed in this method that last item of the purchased stock is sold first.

Units purchased : 60+140+70= 270 units

Number of units sold: 190+30= 220 units

Closing inventory: 270-220 = 50 units

Cost price of goods sold Per unit cost number of

units

Total

Sales from new inventory

27th march

$16 70 $1120

Sales from inventory 5th

march

$15.50 140 $2170

6

1st March 68 $15 $1020

5th 140

$15.5

0 $2170 140

$15.5

0 $2170

9th 68 $15 $1020

26 $15.50 $403 114

$15.5

0 $1767

11th 40 $16 $640 40 $16 $640

16th 78

$16.5

0 $1287 78

$16.5

0 $1287

20th 114 $15.50 1767

2 $16 $32 38 $16 $608

78

$16.5

0 $1287

29th 38 $16 $608

24 $16.50 $396 54

$16.5

0 $891

LIFO Method: This is also one of the best method to calculate inventory as it is the as it is

assumed in this method that last item of the purchased stock is sold first.

Units purchased : 60+140+70= 270 units

Number of units sold: 190+30= 220 units

Closing inventory: 270-220 = 50 units

Cost price of goods sold Per unit cost number of

units

Total

Sales from new inventory

27th march

$16 70 $1120

Sales from inventory 5th

march

$15.50 140 $2170

6

Sales from inventory 1st

march

$15 10 $150

220 $3440

Date Sales Purchases Balance

No. of units

Cost per

unit amount

No. of

units

Cost

per

unit

amoun

t

No. of

units

Cost

per

unit

amoun

t

1st march 60 $15 $900

5th 140

$15.5

0 $2170 60 $15 $900

140

$15.5

0 $2170

14th 140 $15.50 $2170

50 $15 $750 10 $15 $150

27th 70 $16 $1190 70 $16 $1190

29th 30 $16 $480 10 $15 $150

40 $16 $640

31st 10 $15 $150

40 $16 $640

Weighted average method:

The weighted average price is calculated by total cots of inventory divided by total

number of units in inventory.

Weighted average cost price

of goods sold

Per unit cost

(£)

Number of

units

Total

(£)

Opening inventory 15 60 900

Purchases on 5 march 15.50 140 2170

7

march

$15 10 $150

220 $3440

Date Sales Purchases Balance

No. of units

Cost per

unit amount

No. of

units

Cost

per

unit

amoun

t

No. of

units

Cost

per

unit

amoun

t

1st march 60 $15 $900

5th 140

$15.5

0 $2170 60 $15 $900

140

$15.5

0 $2170

14th 140 $15.50 $2170

50 $15 $750 10 $15 $150

27th 70 $16 $1190 70 $16 $1190

29th 30 $16 $480 10 $15 $150

40 $16 $640

31st 10 $15 $150

40 $16 $640

Weighted average method:

The weighted average price is calculated by total cots of inventory divided by total

number of units in inventory.

Weighted average cost price

of goods sold

Per unit cost

(£)

Number of

units

Total

(£)

Opening inventory 15 60 900

Purchases on 5 march 15.50 140 2170

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

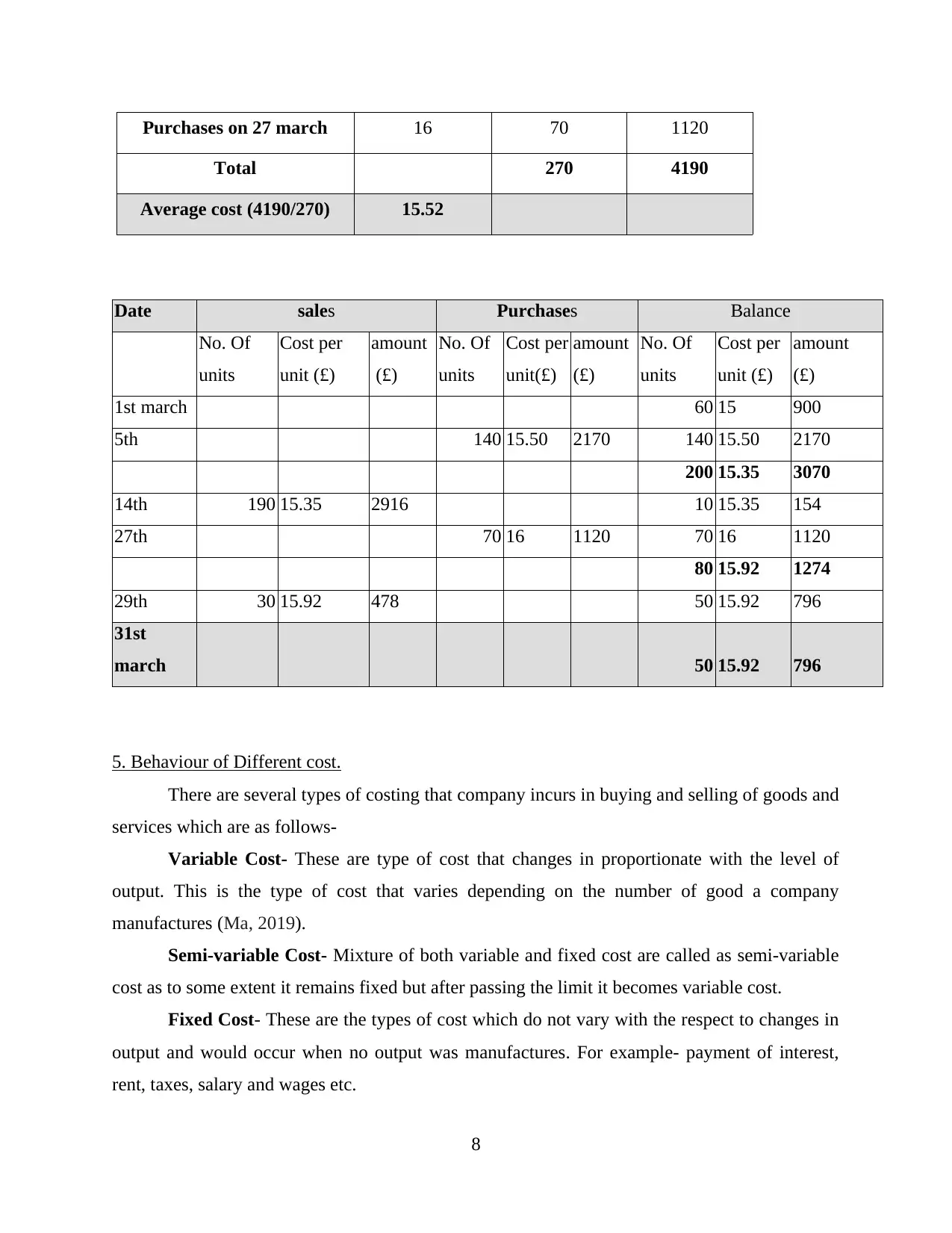

Purchases on 27 march 16 70 1120

Total 270 4190

Average cost (4190/270) 15.52

Date sales Purchases Balance

No. Of

units

Cost per

unit (£)

amount

(£)

No. Of

units

Cost per

unit(£)

amount

(£)

No. Of

units

Cost per

unit (£)

amount

(£)

1st march 60 15 900

5th 140 15.50 2170 140 15.50 2170

200 15.35 3070

14th 190 15.35 2916 10 15.35 154

27th 70 16 1120 70 16 1120

80 15.92 1274

29th 30 15.92 478 50 15.92 796

31st

march 50 15.92 796

5. Behaviour of Different cost.

There are several types of costing that company incurs in buying and selling of goods and

services which are as follows-

Variable Cost- These are type of cost that changes in proportionate with the level of

output. This is the type of cost that varies depending on the number of good a company

manufactures (Ma, 2019).

Semi-variable Cost- Mixture of both variable and fixed cost are called as semi-variable

cost as to some extent it remains fixed but after passing the limit it becomes variable cost.

Fixed Cost- These are the types of cost which do not vary with the respect to changes in

output and would occur when no output was manufactures. For example- payment of interest,

rent, taxes, salary and wages etc.

8

Total 270 4190

Average cost (4190/270) 15.52

Date sales Purchases Balance

No. Of

units

Cost per

unit (£)

amount

(£)

No. Of

units

Cost per

unit(£)

amount

(£)

No. Of

units

Cost per

unit (£)

amount

(£)

1st march 60 15 900

5th 140 15.50 2170 140 15.50 2170

200 15.35 3070

14th 190 15.35 2916 10 15.35 154

27th 70 16 1120 70 16 1120

80 15.92 1274

29th 30 15.92 478 50 15.92 796

31st

march 50 15.92 796

5. Behaviour of Different cost.

There are several types of costing that company incurs in buying and selling of goods and

services which are as follows-

Variable Cost- These are type of cost that changes in proportionate with the level of

output. This is the type of cost that varies depending on the number of good a company

manufactures (Ma, 2019).

Semi-variable Cost- Mixture of both variable and fixed cost are called as semi-variable

cost as to some extent it remains fixed but after passing the limit it becomes variable cost.

Fixed Cost- These are the types of cost which do not vary with the respect to changes in

output and would occur when no output was manufactures. For example- payment of interest,

rent, taxes, salary and wages etc.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

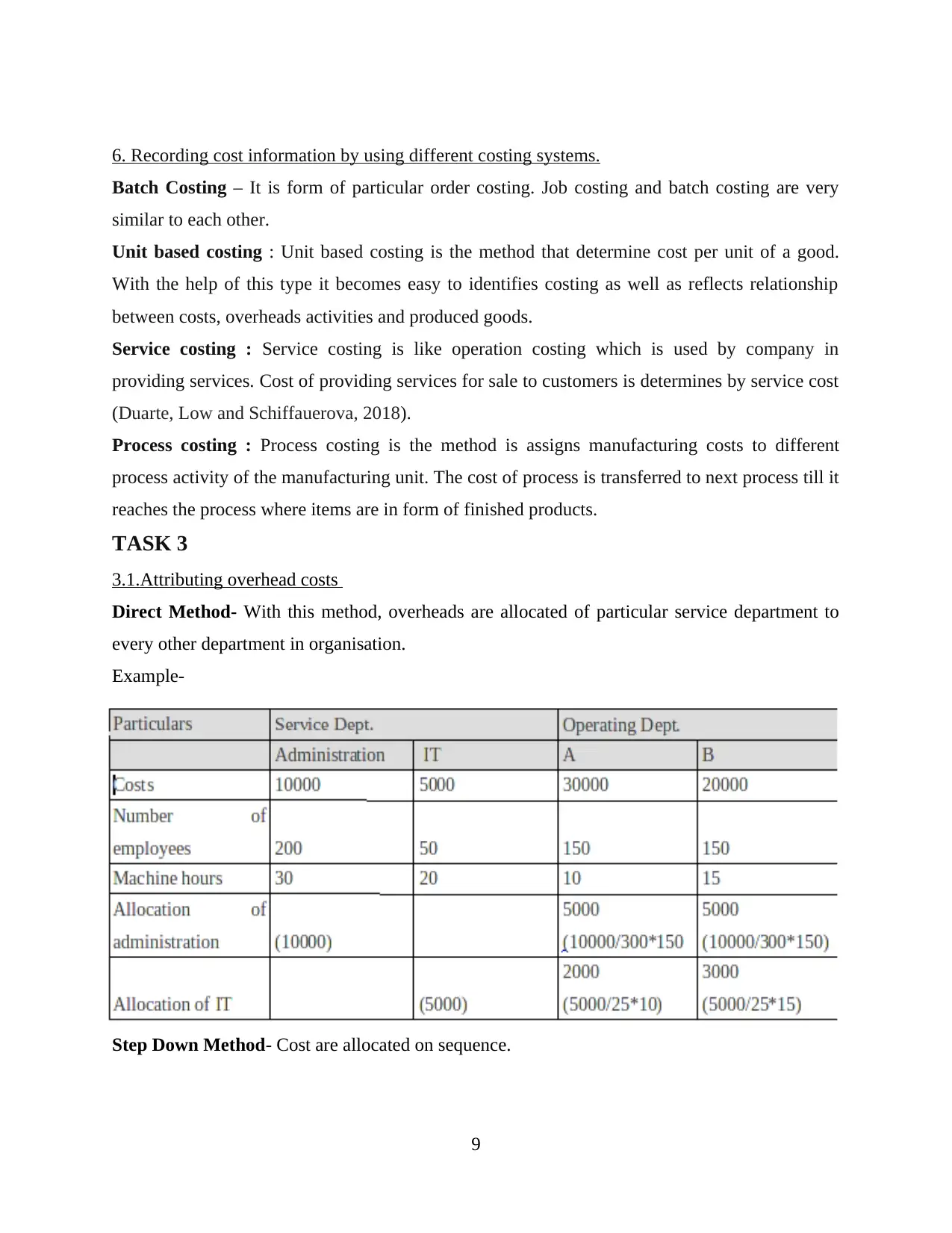

6. Recording cost information by using different costing systems.

Batch Costing – It is form of particular order costing. Job costing and batch costing are very

similar to each other.

Unit based costing : Unit based costing is the method that determine cost per unit of a good.

With the help of this type it becomes easy to identifies costing as well as reflects relationship

between costs, overheads activities and produced goods.

Service costing : Service costing is like operation costing which is used by company in

providing services. Cost of providing services for sale to customers is determines by service cost

(Duarte, Low and Schiffauerova, 2018).

Process costing : Process costing is the method is assigns manufacturing costs to different

process activity of the manufacturing unit. The cost of process is transferred to next process till it

reaches the process where items are in form of finished products.

TASK 3

3.1.Attributing overhead costs

Direct Method- With this method, overheads are allocated of particular service department to

every other department in organisation.

Example-

Step Down Method- Cost are allocated on sequence.

9

Batch Costing – It is form of particular order costing. Job costing and batch costing are very

similar to each other.

Unit based costing : Unit based costing is the method that determine cost per unit of a good.

With the help of this type it becomes easy to identifies costing as well as reflects relationship

between costs, overheads activities and produced goods.

Service costing : Service costing is like operation costing which is used by company in

providing services. Cost of providing services for sale to customers is determines by service cost

(Duarte, Low and Schiffauerova, 2018).

Process costing : Process costing is the method is assigns manufacturing costs to different

process activity of the manufacturing unit. The cost of process is transferred to next process till it

reaches the process where items are in form of finished products.

TASK 3

3.1.Attributing overhead costs

Direct Method- With this method, overheads are allocated of particular service department to

every other department in organisation.

Example-

Step Down Method- Cost are allocated on sequence.

9

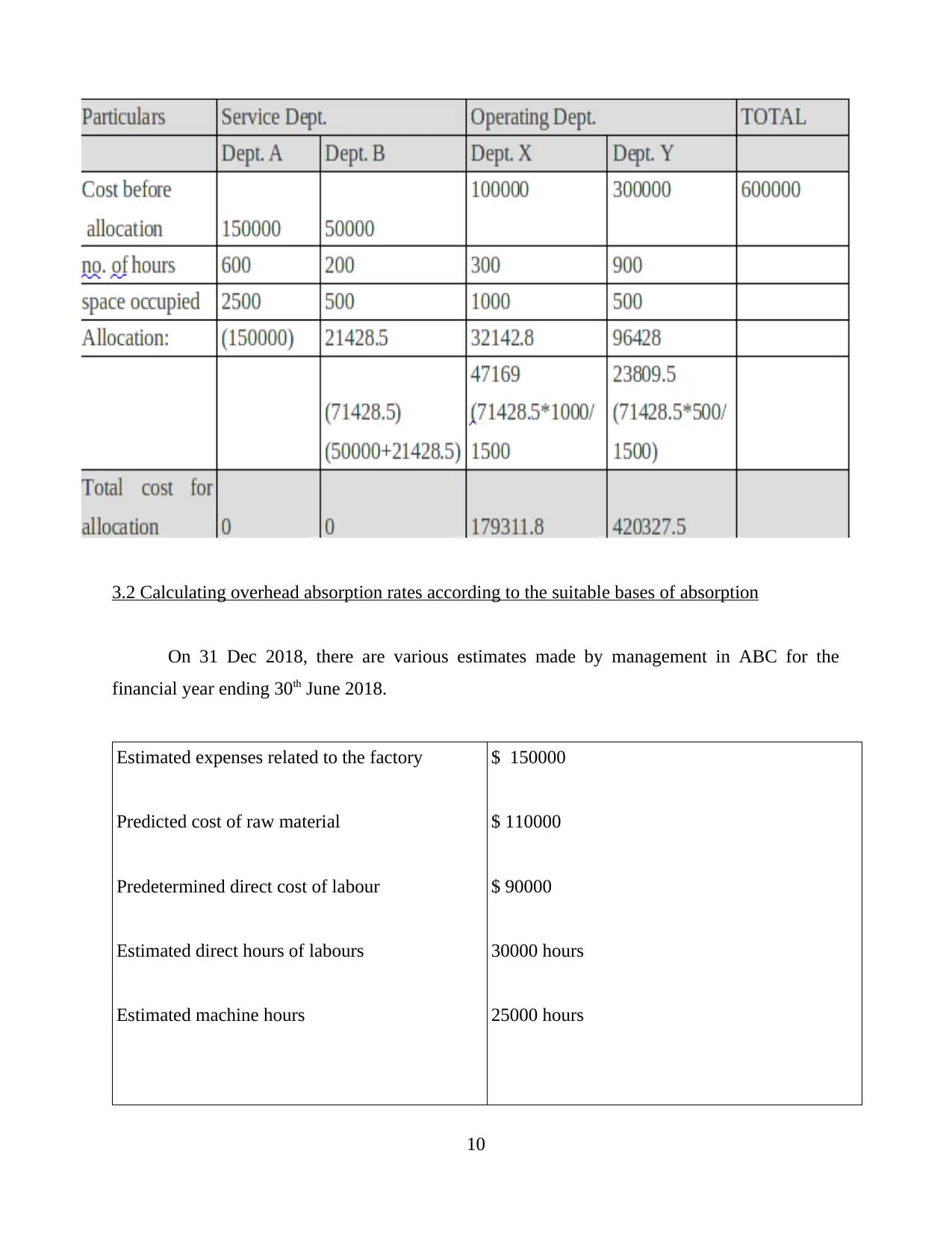

3.2 Calculating overhead absorption rates according to the suitable bases of absorption

On 31 Dec 2018, there are various estimates made by management in ABC for the

financial year ending 30th June 2018.

Estimated expenses related to the factory

Predicted cost of raw material

Predetermined direct cost of labour

Estimated direct hours of labours

Estimated machine hours

$ 150000

$ 110000

$ 90000

30000 hours

25000 hours

10

On 31 Dec 2018, there are various estimates made by management in ABC for the

financial year ending 30th June 2018.

Estimated expenses related to the factory

Predicted cost of raw material

Predetermined direct cost of labour

Estimated direct hours of labours

Estimated machine hours

$ 150000

$ 110000

$ 90000

30000 hours

25000 hours

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.