Tesco PLC: Internal Reporting, Costing Systems, and Decision Making

VerifiedAdded on 2020/10/23

|17

|4287

|104

Report

AI Summary

This report analyzes the costs and revenues of Tesco PLC, a major British multinational retailer. It explores the purpose of internal reporting, various costing systems (job, process, direct), and responsibility centers within an organization. The report details different cost classifications (direct, indirect, fixed, variable) and contrasts marginal and absorption costing methods. It covers recording and analyzing cost information for materials, labor, and expenses, including inventory valuation using FIFO, LIFO, and weighted average methods. The behavior of costs (fixed, variable, semi-variable, stepped) is examined, along with the application of different costing systems (job, batch, unit, process, service). Furthermore, the report discusses overhead cost allocation, absorption rates, variance analysis, and management reporting. Finally, it addresses the preparation of future income and cost estimates for decision-making, considering the effect of changing activity levels and factors influencing short-term and long-term decisions.

COSTS

AND

REVENUES

AND

REVENUES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 The purpose of internal reporting and providing accurate information to management.......1

1.2 The relationship between the various costing systems with in Tesco plc.............................1

1.3 The responsibility centres, cost centres, profit centres and investment centres with in an

organisation.................................................................................................................................2

1.4 The characteristics of different types of cost classifications and their use in costing...........2

1.5 The difference between marginal and absorption costing.....................................................3

TASK 2............................................................................................................................................3

2.1 Record cost information for material, labour and expenses in accordance with the

organisation's costing procedures................................................................................................3

2.2 Analyse cost information for material, labour and expenses in accordance with the

organisation's costing procedures................................................................................................3

2.3 Various stages of inventory...................................................................................................4

2.4 Value inventory using these methods...................................................................................4

2.5 The behaviour of costs..........................................................................................................6

2.6 Record cost information in costing system...........................................................................7

TASK 3............................................................................................................................................8

3.1 Attribute overhead costs to production and services cost centres in accordance with agreed

bases of allocation and apportionment........................................................................................8

3.2 Calculate overhead absorption rates in accordance with suitable bases of absorption.........8

3.3 Make adjustments for under or over recovered overhead costs in accordance with

established procedures................................................................................................................8

Overhead rate per machine hours: -............................................................................................8

Over and under absorption: -.......................................................................................................9

3.4 Review methods of allocation, apportionment and absorption at regular intervals,

implementing agreed changes to methods..................................................................................9

3.5 Communicate with relevant staff to resolve any queries in overhead cost data.................10

TASK 4..........................................................................................................................................10

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 The purpose of internal reporting and providing accurate information to management.......1

1.2 The relationship between the various costing systems with in Tesco plc.............................1

1.3 The responsibility centres, cost centres, profit centres and investment centres with in an

organisation.................................................................................................................................2

1.4 The characteristics of different types of cost classifications and their use in costing...........2

1.5 The difference between marginal and absorption costing.....................................................3

TASK 2............................................................................................................................................3

2.1 Record cost information for material, labour and expenses in accordance with the

organisation's costing procedures................................................................................................3

2.2 Analyse cost information for material, labour and expenses in accordance with the

organisation's costing procedures................................................................................................3

2.3 Various stages of inventory...................................................................................................4

2.4 Value inventory using these methods...................................................................................4

2.5 The behaviour of costs..........................................................................................................6

2.6 Record cost information in costing system...........................................................................7

TASK 3............................................................................................................................................8

3.1 Attribute overhead costs to production and services cost centres in accordance with agreed

bases of allocation and apportionment........................................................................................8

3.2 Calculate overhead absorption rates in accordance with suitable bases of absorption.........8

3.3 Make adjustments for under or over recovered overhead costs in accordance with

established procedures................................................................................................................8

Overhead rate per machine hours: -............................................................................................8

Over and under absorption: -.......................................................................................................9

3.4 Review methods of allocation, apportionment and absorption at regular intervals,

implementing agreed changes to methods..................................................................................9

3.5 Communicate with relevant staff to resolve any queries in overhead cost data.................10

TASK 4..........................................................................................................................................10

4.1 Compare budgets costs with actual costs, noting any variances.........................................10

4.2 Analyse variances for management reports........................................................................11

4.3 Provide information for budget holders of any significant variances, making valid

suggestions for remedial action.................................................................................................11

4.4 Prepare management reports in an appropriate format, presenting these within the required

timescales..................................................................................................................................11

TASK 5..........................................................................................................................................12

5.1 Prepare estimates of future income and costs for decision making....................................12

5.2 The effect of changing activity levels on unit costs............................................................12

5.3 Calculate the effect of changing activity level on units costs.............................................12

5.4 Identify factors affecting short term and long term decision making.................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

4.2 Analyse variances for management reports........................................................................11

4.3 Provide information for budget holders of any significant variances, making valid

suggestions for remedial action.................................................................................................11

4.4 Prepare management reports in an appropriate format, presenting these within the required

timescales..................................................................................................................................11

TASK 5..........................................................................................................................................12

5.1 Prepare estimates of future income and costs for decision making....................................12

5.2 The effect of changing activity levels on unit costs............................................................12

5.3 Calculate the effect of changing activity level on units costs.............................................12

5.4 Identify factors affecting short term and long term decision making.................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

The terms costs and revenues are likely two of the most important concepts in business

and management. No business can survive without profit and it depends on cost control and sales

revenues. Cost and revenues are helping to improve and maintain profitability (Burchell and

Listokin, 2012). Revenue is the total amount of money received which are acquired by sold of

goods or services. Costs of goods sold are included in direct costs referable to the production of

the goods sold by a company. In other terms, every business wants to make more revenues for

cover its costs. In the present report selecting company Tesco plc, is a British multinational

groceries and general merchandise retailer. It was founded in 1919 by Jack Cohen as a group of

market stalls. The report focused on nature and role of costing system in the context of tesco plc.

Record and analyse cost information and absorption cost according to organisational

requirements. Analyse deviations from budget and report of management and use information to

gather from costing systems to assist decision making.

TASK 1

1.1 The purpose of internal reporting and providing accurate information to management

Internal reporting plays an important role in current business environment and it provides

a clear picture to executive teams about the financial health of Tesco plc. But it does not provide

accurate and over all information that helps to understand hoe the business is performing at an

operational level. In internal reports including forecast report, cash reports, financial reports and

budget books etc. There is mention purpose of internal reporting that are provided accurate

information to management of tesco plc -

The internal report measure and monitor specific performance of KPIs and metrics.

It is determine benchmarks to know minimum expected result.

The purpose of this report to provide status report, board report and packages to

management for decision making (Terpstra and Verbeeten, 2014).

1.2 The relationship between the various costing systems with in Tesco plc

In Tesco plc applies various costing system like job costing system, process costing and

direct costing. Each of these methods apply by company to different production and decision

environments.

1

The terms costs and revenues are likely two of the most important concepts in business

and management. No business can survive without profit and it depends on cost control and sales

revenues. Cost and revenues are helping to improve and maintain profitability (Burchell and

Listokin, 2012). Revenue is the total amount of money received which are acquired by sold of

goods or services. Costs of goods sold are included in direct costs referable to the production of

the goods sold by a company. In other terms, every business wants to make more revenues for

cover its costs. In the present report selecting company Tesco plc, is a British multinational

groceries and general merchandise retailer. It was founded in 1919 by Jack Cohen as a group of

market stalls. The report focused on nature and role of costing system in the context of tesco plc.

Record and analyse cost information and absorption cost according to organisational

requirements. Analyse deviations from budget and report of management and use information to

gather from costing systems to assist decision making.

TASK 1

1.1 The purpose of internal reporting and providing accurate information to management

Internal reporting plays an important role in current business environment and it provides

a clear picture to executive teams about the financial health of Tesco plc. But it does not provide

accurate and over all information that helps to understand hoe the business is performing at an

operational level. In internal reports including forecast report, cash reports, financial reports and

budget books etc. There is mention purpose of internal reporting that are provided accurate

information to management of tesco plc -

The internal report measure and monitor specific performance of KPIs and metrics.

It is determine benchmarks to know minimum expected result.

The purpose of this report to provide status report, board report and packages to

management for decision making (Terpstra and Verbeeten, 2014).

1.2 The relationship between the various costing systems with in Tesco plc

In Tesco plc applies various costing system like job costing system, process costing and

direct costing. Each of these methods apply by company to different production and decision

environments.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.3 The responsibility centres, cost centres, profit centres and investment centres with in an

organisation

Responsibility centres is a functional unit of Tesco plc and it is headed by a manager

who is responsible for the activities of particular unit. In this centre manager is responsible for

the carry out the tasks in set unit. It is divided organizational task into sub task which are present

by various departments. In this sense, all sections in a business are responsibility centres.

Cost centres is a portion of Tesco plc in which the managers are held accountable for the

cost obtain in the portion but it is not for revenues. In the centre purpose of planning related to

budget estimation related to cost estimation and for control purposes evaluate of performance

that is guided by cost variance. It is a difference between the actual and budgeted costs for a

specific time period (Graham, 2013).

Profit centres is a section of Tesco plc where manager responsible for costs and

revenues. In the particular centre the manager take responsibility and authority of making

decision and it is affect to cost and revenues in certain division. There is main aim of this centre

to earn more profit.

Investment centres is a part of responsibility centre in whose manager is responsible for

earning a rate of return on the assets used in responsibility centre. In this centre control the

system for measure the monetary value of inputs and outputs.

1.4 The characteristics of different types of cost classifications and their use in costing Direct cost – It is related to producing a good or services. With the help of direct cost

easily track to a product, section and project of company. A direct cost using in costing to

calculate cost of materials, labours cost and overhead expenses. Indirect cost – It is not related to products and services and it will not traced to particular

object of costing. Indirect costs consist of operating costs, factory overhead and benefits

of one product, department of branch. It is using in costing to measure cost of each

product. Fixed cost – It is contain the number of goods and services in fixed way. It is using in

costing for fixed expenses that are not changeable in year to year. The characteristic of

this cost that it is easy to traced in particular year and remain same (Cruz, Simões, and

Marques, 2012).

2

organisation

Responsibility centres is a functional unit of Tesco plc and it is headed by a manager

who is responsible for the activities of particular unit. In this centre manager is responsible for

the carry out the tasks in set unit. It is divided organizational task into sub task which are present

by various departments. In this sense, all sections in a business are responsibility centres.

Cost centres is a portion of Tesco plc in which the managers are held accountable for the

cost obtain in the portion but it is not for revenues. In the centre purpose of planning related to

budget estimation related to cost estimation and for control purposes evaluate of performance

that is guided by cost variance. It is a difference between the actual and budgeted costs for a

specific time period (Graham, 2013).

Profit centres is a section of Tesco plc where manager responsible for costs and

revenues. In the particular centre the manager take responsibility and authority of making

decision and it is affect to cost and revenues in certain division. There is main aim of this centre

to earn more profit.

Investment centres is a part of responsibility centre in whose manager is responsible for

earning a rate of return on the assets used in responsibility centre. In this centre control the

system for measure the monetary value of inputs and outputs.

1.4 The characteristics of different types of cost classifications and their use in costing Direct cost – It is related to producing a good or services. With the help of direct cost

easily track to a product, section and project of company. A direct cost using in costing to

calculate cost of materials, labours cost and overhead expenses. Indirect cost – It is not related to products and services and it will not traced to particular

object of costing. Indirect costs consist of operating costs, factory overhead and benefits

of one product, department of branch. It is using in costing to measure cost of each

product. Fixed cost – It is contain the number of goods and services in fixed way. It is using in

costing for fixed expenses that are not changeable in year to year. The characteristic of

this cost that it is easy to traced in particular year and remain same (Cruz, Simões, and

Marques, 2012).

2

Variable cost – It is fluctuate the level of production to change output and it was

depended on the number products. It is helping to increases of volume production and

using in costing to calculate cost of products on various stages.

1.5 The difference between marginal and absorption costing

Basis Marginal costing Absorption costing

Meaning Marginal costing is a technique that

estimate of variable cost as product

cost.

Absorption costing is a technique

that anticipate of fixed and variable

cost as a product cost.

Nature of

overhead

In this method included fixed cost

and variable cost.

In the case of absorption costing

have different selling &

administration, production and

distribution.

Profit calculation In this method profit calculated by

using profit volume ratio (p/v ratio)

In absorption costing method fixed

cost are reasoned in product cost so

profit gets decreased.

TASK 2

2.1 Record cost information for material, labour and expenses in accordance with the

organisation's costing procedures

Costing procedure is the activity of recording cost in appropriate accounts and expenses

determined in manufacturing process. There are various types of costs these are -

Material – It is divided in two parts direct and indirect materials.

Labour – They are working in an organisation to manufacture products.

Expenses – It is related to revenues generation process and non operating business execution

process (Raisman, 2013).

2.2 Analyse cost information for material, labour and expenses in accordance with the

organisation's costing procedures

Material cost is a variable expenses that are changes according to demand in the market.

It is depended on market activities because in the market demand is high so need of material

3

depended on the number products. It is helping to increases of volume production and

using in costing to calculate cost of products on various stages.

1.5 The difference between marginal and absorption costing

Basis Marginal costing Absorption costing

Meaning Marginal costing is a technique that

estimate of variable cost as product

cost.

Absorption costing is a technique

that anticipate of fixed and variable

cost as a product cost.

Nature of

overhead

In this method included fixed cost

and variable cost.

In the case of absorption costing

have different selling &

administration, production and

distribution.

Profit calculation In this method profit calculated by

using profit volume ratio (p/v ratio)

In absorption costing method fixed

cost are reasoned in product cost so

profit gets decreased.

TASK 2

2.1 Record cost information for material, labour and expenses in accordance with the

organisation's costing procedures

Costing procedure is the activity of recording cost in appropriate accounts and expenses

determined in manufacturing process. There are various types of costs these are -

Material – It is divided in two parts direct and indirect materials.

Labour – They are working in an organisation to manufacture products.

Expenses – It is related to revenues generation process and non operating business execution

process (Raisman, 2013).

2.2 Analyse cost information for material, labour and expenses in accordance with the

organisation's costing procedures

Material cost is a variable expenses that are changes according to demand in the market.

It is depended on market activities because in the market demand is high so need of material

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

increases and it also affect to labour and overhead of the company. It depends on total items that

faced by all business entities.

2.3 Various stages of inventory

There are three different stages of inventory, all of them are as follows -

Raw Material – In the process on inventory it is first stage and used in production. In this

process includes all those starting products which are used in starting process and it is also

known as feed stock and unprocessed material.

Work in progress – It is mention as a mid process of inventory in which stocks are

partially manufactured. It is also called process inventory and in this stage waiting for

completion of goods.

Finished goods – In this stages process is finished and product are prepared because it is

last stage of production. After production it will sale out in market (Gensler, Leeflang and

Skiera, 2012).

2.4 Value inventory using these methods

First in first out (FIFO)

Date Particulars Purchase Sales Balance

Qty. Rate

Amo

unt Qty. Rate

Amo

unt Qty. Rate

Amo

unt

March, 1

Opening Inventory (68

units @15.00 per unit) 68 15 1020 68 15 1020

68 1020

March, 5

Purchase (140 units @

£15.50 per unit) 140 15.5 2170 140 15.5 2170

68 15 1020

208 3190

March, 9 Sale (94 units) 68 15 1020 114 15.5 1767

26 15.5 403 114 1767

4

faced by all business entities.

2.3 Various stages of inventory

There are three different stages of inventory, all of them are as follows -

Raw Material – In the process on inventory it is first stage and used in production. In this

process includes all those starting products which are used in starting process and it is also

known as feed stock and unprocessed material.

Work in progress – It is mention as a mid process of inventory in which stocks are

partially manufactured. It is also called process inventory and in this stage waiting for

completion of goods.

Finished goods – In this stages process is finished and product are prepared because it is

last stage of production. After production it will sale out in market (Gensler, Leeflang and

Skiera, 2012).

2.4 Value inventory using these methods

First in first out (FIFO)

Date Particulars Purchase Sales Balance

Qty. Rate

Amo

unt Qty. Rate

Amo

unt Qty. Rate

Amo

unt

March, 1

Opening Inventory (68

units @15.00 per unit) 68 15 1020 68 15 1020

68 1020

March, 5

Purchase (140 units @

£15.50 per unit) 140 15.5 2170 140 15.5 2170

68 15 1020

208 3190

March, 9 Sale (94 units) 68 15 1020 114 15.5 1767

26 15.5 403 114 1767

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

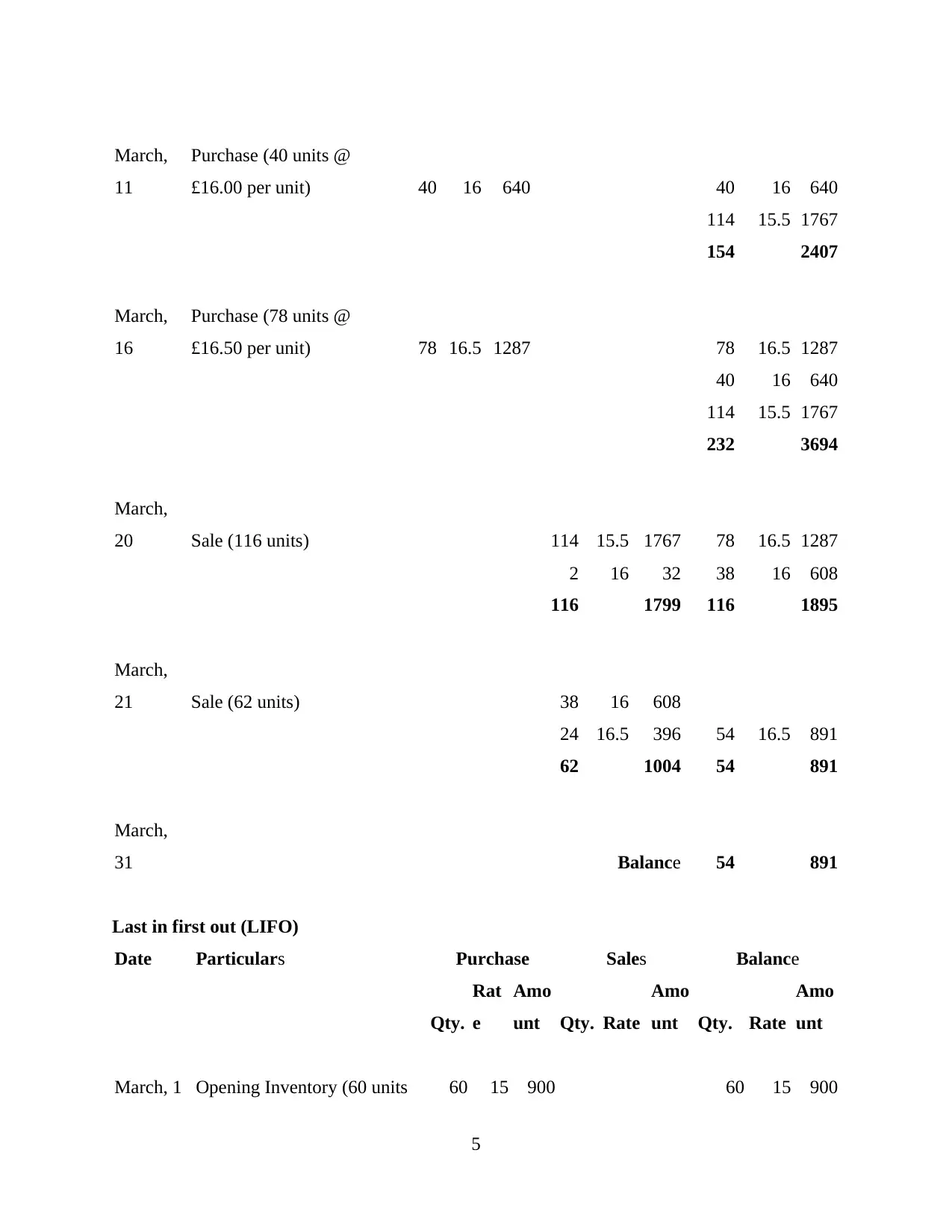

March,

11

Purchase (40 units @

£16.00 per unit) 40 16 640 40 16 640

114 15.5 1767

154 2407

March,

16

Purchase (78 units @

£16.50 per unit) 78 16.5 1287 78 16.5 1287

40 16 640

114 15.5 1767

232 3694

March,

20 Sale (116 units) 114 15.5 1767 78 16.5 1287

2 16 32 38 16 608

116 1799 116 1895

March,

21 Sale (62 units) 38 16 608

24 16.5 396 54 16.5 891

62 1004 54 891

March,

31 Balance 54 891

Last in first out (LIFO)

Date Particulars Purchase Sales Balance

Qty.

Rat

e

Amo

unt Qty. Rate

Amo

unt Qty. Rate

Amo

unt

March, 1 Opening Inventory (60 units 60 15 900 60 15 900

5

11

Purchase (40 units @

£16.00 per unit) 40 16 640 40 16 640

114 15.5 1767

154 2407

March,

16

Purchase (78 units @

£16.50 per unit) 78 16.5 1287 78 16.5 1287

40 16 640

114 15.5 1767

232 3694

March,

20 Sale (116 units) 114 15.5 1767 78 16.5 1287

2 16 32 38 16 608

116 1799 116 1895

March,

21 Sale (62 units) 38 16 608

24 16.5 396 54 16.5 891

62 1004 54 891

March,

31 Balance 54 891

Last in first out (LIFO)

Date Particulars Purchase Sales Balance

Qty.

Rat

e

Amo

unt Qty. Rate

Amo

unt Qty. Rate

Amo

unt

March, 1 Opening Inventory (60 units 60 15 900 60 15 900

5

@15.00 per unit)

60 0

March, 5

Purchase (140 units @ £15.50

per unit) 140 15.5 2170 140 15.5 2170

60 15 900

200 3070

March,

14 Sale (190 units) 140 15.5 2170 190 2920

50 15 750 10 150

March,

27

Purchase (70 units @ £16.00

per unit) 70 16 1120 70 16 1120

80 1270

March,

29 Sale (30 units) 30 16 480 30 480

March,

31 Balance 50 790

Weighted average

Date Particulars Purchase Sales Balance

Qty. Rate

Amo

unt Qty. Rate

Amou

nt Qty. Rate

Amou

nt

March, 1

Opening Inventory (60

units @15.00 per unit) 60 15 900

6

60 0

March, 5

Purchase (140 units @ £15.50

per unit) 140 15.5 2170 140 15.5 2170

60 15 900

200 3070

March,

14 Sale (190 units) 140 15.5 2170 190 2920

50 15 750 10 150

March,

27

Purchase (70 units @ £16.00

per unit) 70 16 1120 70 16 1120

80 1270

March,

29 Sale (30 units) 30 16 480 30 480

March,

31 Balance 50 790

Weighted average

Date Particulars Purchase Sales Balance

Qty. Rate

Amo

unt Qty. Rate

Amou

nt Qty. Rate

Amou

nt

March, 1

Opening Inventory (60

units @15.00 per unit) 60 15 900

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

March, 5

Purchase (140 units @

£15.50 per unit) 140 15.5 2170 200 15.35 3070

March,

14 Sale (190 units) 190 15.35 2916.5 10 15.35 153.5

March,

27

Purchase (70 units @

£16.00 per unit) 70 16 1120 80 15.92 1273.5

March,

29 Sale (30 units) 30 15.92 477.6 50 15.92 796

March,

31 Balance 50 15.92 796

2.5 The behaviour of costs

Fixed - It is that cost which is remain constant in the whole production period and it is

not matter that how much unit produce. For example: - amount of rent is to be fixed to pay no

matter how much unit produced or sold.

Variable - Variable cost are those which is change according to production level and it is

depend upon no of units produced in the organisation. For example: - company have to purchase

raw material according to production. If production is not happen than there is no need to buy

raw material so variable cost can vary.

Semi variable - It is also known as mixed cost which includes fixed as well as variable

cost. In this case, fixed cost is set up to one level after that if production is exceed from the set

standard than cost become variable.

Stepped - It also include step fixed or step variable cost, step fixed cost not changed at a

certain level of activities and it will changed after crossing that level. Step variable cost is vary

according to change in activities (Kirkham, 2014).

7

Purchase (140 units @

£15.50 per unit) 140 15.5 2170 200 15.35 3070

March,

14 Sale (190 units) 190 15.35 2916.5 10 15.35 153.5

March,

27

Purchase (70 units @

£16.00 per unit) 70 16 1120 80 15.92 1273.5

March,

29 Sale (30 units) 30 15.92 477.6 50 15.92 796

March,

31 Balance 50 15.92 796

2.5 The behaviour of costs

Fixed - It is that cost which is remain constant in the whole production period and it is

not matter that how much unit produce. For example: - amount of rent is to be fixed to pay no

matter how much unit produced or sold.

Variable - Variable cost are those which is change according to production level and it is

depend upon no of units produced in the organisation. For example: - company have to purchase

raw material according to production. If production is not happen than there is no need to buy

raw material so variable cost can vary.

Semi variable - It is also known as mixed cost which includes fixed as well as variable

cost. In this case, fixed cost is set up to one level after that if production is exceed from the set

standard than cost become variable.

Stepped - It also include step fixed or step variable cost, step fixed cost not changed at a

certain level of activities and it will changed after crossing that level. Step variable cost is vary

according to change in activities (Kirkham, 2014).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.6 Record cost information in costing system Job costing system - In the job costing system direct material, labour and overheads of

the company included at the time of preparing costing sheet. Batch costing system - It is used when organisation make different batches and than start

costing of each batch. Cost of one batch is divided by the each unit available in this batch

and after that organisation find the cost of each unit. It involves the material, labour and

overheads to prepare batch costing sheet. Unit costing system - This costing system find out the each product cost and repeat this

activity in the whole manufacturing period. It is known as single costing system and it is

calculated by dividing total manufacturing cost to total no of unit produced. Process costing system - It is also called operation costing because it identify the cost of

each product at every level of production. It is helpful to keep checking cost price at

every manufacturing stage.

Service costing system - This costing is applicable on those organisation who deals in

service market instead of manufacturing goods. It includes all the relevant expenses

which is spend by the company to produce services. In service costing system they

involve the maintenance, operation or fixed cost of the service (Tallon, 2013).

TASK 3

3.1 Attribute overhead costs to production and services cost centres in accordance with agreed

bases of allocation and apportionment

Direct - Direct method identify the cost of each services department and allocated to

different department. This cost allocation method is applicable only service sector.

Step down - This method allocate the cost of services of department by another service

department. Step down method include the some limited costs like those expenses incurred by

the humans and the maintenance expenses which is required in the service department.

3.2 Calculate overhead absorption rates in accordance with suitable bases of absorption

Machine hours -

Overhead absorption rate = Estimated Factory Overheads / Estimated machine hours * 100

= $150000 / 25000 * 100

= 600%

8

the company included at the time of preparing costing sheet. Batch costing system - It is used when organisation make different batches and than start

costing of each batch. Cost of one batch is divided by the each unit available in this batch

and after that organisation find the cost of each unit. It involves the material, labour and

overheads to prepare batch costing sheet. Unit costing system - This costing system find out the each product cost and repeat this

activity in the whole manufacturing period. It is known as single costing system and it is

calculated by dividing total manufacturing cost to total no of unit produced. Process costing system - It is also called operation costing because it identify the cost of

each product at every level of production. It is helpful to keep checking cost price at

every manufacturing stage.

Service costing system - This costing is applicable on those organisation who deals in

service market instead of manufacturing goods. It includes all the relevant expenses

which is spend by the company to produce services. In service costing system they

involve the maintenance, operation or fixed cost of the service (Tallon, 2013).

TASK 3

3.1 Attribute overhead costs to production and services cost centres in accordance with agreed

bases of allocation and apportionment

Direct - Direct method identify the cost of each services department and allocated to

different department. This cost allocation method is applicable only service sector.

Step down - This method allocate the cost of services of department by another service

department. Step down method include the some limited costs like those expenses incurred by

the humans and the maintenance expenses which is required in the service department.

3.2 Calculate overhead absorption rates in accordance with suitable bases of absorption

Machine hours -

Overhead absorption rate = Estimated Factory Overheads / Estimated machine hours * 100

= $150000 / 25000 * 100

= 600%

8

Total absorption overheads = $600 * 44

= $26400

Labour hours -

Overhead absorption rate = Estimated Factory Overheads / Estimated labour hours * 100

= $150000 / 30000 * 100

= 500%

Total absorption overheads = $500 * 63

= $31500

3.3 Make adjustments for under or over recovered overhead costs in accordance with established

procedures

Overhead rate per machine hours: -

Normal working hours = No of machines*No of working hour per week*No of work per week

= 28*42*48

= 56448

Loss of hours on maintenance = No of machines*No of hour loss on maintenance per week*No

of work per week

= 28*5*48

= 6720

Annual effective working hours = Normal working hours - Loss of hours on maintenance

= 56448 - 6720

= 49728

Machine hours = Estimated annual overhead / Estimated working hours

= 124320/49728

= £2.5 per hours.

Over and under absorption: -

Over absorption = Machine hours produce – Overhead incurred

= (4200*2.5) – £10200

= £10500-£10200

= £300

9

= $26400

Labour hours -

Overhead absorption rate = Estimated Factory Overheads / Estimated labour hours * 100

= $150000 / 30000 * 100

= 500%

Total absorption overheads = $500 * 63

= $31500

3.3 Make adjustments for under or over recovered overhead costs in accordance with established

procedures

Overhead rate per machine hours: -

Normal working hours = No of machines*No of working hour per week*No of work per week

= 28*42*48

= 56448

Loss of hours on maintenance = No of machines*No of hour loss on maintenance per week*No

of work per week

= 28*5*48

= 6720

Annual effective working hours = Normal working hours - Loss of hours on maintenance

= 56448 - 6720

= 49728

Machine hours = Estimated annual overhead / Estimated working hours

= 124320/49728

= £2.5 per hours.

Over and under absorption: -

Over absorption = Machine hours produce – Overhead incurred

= (4200*2.5) – £10200

= £10500-£10200

= £300

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.