MBA Project: Determinants of SME Credit Access in Ga East Municipality

VerifiedAdded on 2023/06/12

ACCOUNTING DEPARTMENT IN PARTIAL FULFILMENT OF THE AWARD FOR

THE REQUIREMENT OF A MASTER OF BUSINESS ADMINISTRATION IN

ACCOUNTING AND FINANCE.

APRIL 2022

TABLE OF CONTENTS

CHAPTER ONE..........................................................................................................................3

INTRODUCTION.......................................................................................................................3

1.1 Background of the Study...........................................................................................................3

Project Questions.............................................................................................................................6

1.4 Objectives of the Study..............................................................................................................6

1.4.1 Main Project Objective...........................................................................................................6

1.4.2 Specific Project Objectives.....................................................................................................6

1.5 Scope of the Study.....................................................................................................................7

1.6 Significance of the Study...........................................................................................................7

1.7 Project Outline...........................................................................................................................7

CHAPTER TWO.........................................................................................................................9

LITERATURE REVIEW............................................................................................................9

2.1 Overview....................................................................................................................................9

2.2 Definition of SMEs..................................................................................................................12

Paraphrase This Document

2.3.1 Reliance on few employees..................................................................................................16

2.3.2 Simplicity..............................................................................................................................17

2.3.3 Market Area..........................................................................................................................17

2.3.4 Locations...............................................................................................................................18

2.4 Historical development of credit in Ghana..............................................................................18

2.5 Credit reforms and regulatory framework in Ghana................................................................20

2.6 Importance of SMEs to the economic development in Ghana................................................21

2.8 The Determinants of access to funding by SMEs in Ga East municipality.............................26

2.8.1 Firm’s Age............................................................................................................................26

2.8.2 Industry/Sector of the Firm...................................................................................................27

2.8.3 Firm’s Performance..............................................................................................................27

2.8.4 Firm’s Innovation..................................................................................................................27

2.8.5 Firm’s Size............................................................................................................................27

2.8.6 Level of Education................................................................................................................28

2.8.7 Collateral security.................................................................................................................28

CHAPTER THREE...................................................................................................................30

PROJECT IMPLEMENTATION..............................................................................................30

Overview....................................................................................................................................30

Methods......................................................................................................................................30

Materials/Data............................................................................................................................33

Analytical Tools.........................................................................................................................34

Ethical Issues Addressed............................................................................................................35

Summary....................................................................................................................................35

Questionnaire.............................................................................................................................36

REFERENCES..............................................................................................................................38

INTRODUCTION

1.1 Background of the Study

Universally, the impact of Small and Medium Enterprises (SMEs) on the development of general

(national) economies is substantial. In the advanced markets, minor businesses are

acknowledged as the central mechanisms or engines for development as well as growth. Truly,

research undertaken recently in urbanized markets, including the Freedman studies done in the

United Kingdom, established the fact that small (minor) businesses account for the uppermost

total of listed companies and result in substantial involvement in prosperity and the growth of the

economy. In Ghana, statistics gathered from the Registrar General’s Department advocate that,

92 percent of companies registered are micro, small, and medium scale enterprises. SMEs in

Ghana have also been well-known to offer about 85 percent of manufacturing employment,

which contributes to about 70 percent of Ghana’s GDP, and therefore has a catalytic influence on

employment, income as well as economic growth.

Nevertheless, funding of small and medium-sized enterprises (SMEs) has been a matter of

massive attention to both legislators and researchers as a result of the importance of SMEs in the

private sectors worldwide and the insight or fact that these firms are monetarily inhibited.

According to (Ayyagari, 2007) on average, SMEs account for the majority percentage of

manufacturing employment. More significantly, SMEs not only perceive access to finance and

the cost of credit is not only perceived by SMEs to be grand barriers or hindrances or obstacles

than large firms, but these dynamics coerce SMEs (that is, there is an effect or impact on their

performance) far greater than huge businesses.

The subject of what entails a small or medium enterprise remains a key issue in the collected

works. Diverse writers have regularly given dissimilar accounts to this group or class of

business. SMEs have certainly not been left out of the definition problem that is commonly

linked with notions or thoughts or theories associated with a lot of components. Firms described

by their size differ among researchers. Some endeavor to use the capital assets whereas others

use the skill of labor and revenue level. Others describe SMEs in terms of their legal status and

routine of production. In Ghana, Small enterprises are described as enterprises that are worth up

to $100,000 of fixed assets whiles they employ between 6 and 29 employees whereas Medium

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

between 30 and 99 employees. These enterprises offer substantial prominence to the economy by

engaging the majority of the working populace, increasing GDP, and serving as an engine of the

economy for economic growth.

Notwithstanding their significant standing of SMEs in economic growth, SMEs worldwide, and

Ghana (Ga East municipality) to be precise, are still confronted with several obstacles that

impede entrepreneurial development. Besides poor management skills which is a consequence of

the absence of satisfactory training and education, SMEs financing and access to financial

sustenance (which is the focus of this study), is one of the challenges affecting the growth of

SMEs in Ghana (Ga East municipality). Financial institutions have conventionally fixated on the

large multi-corporate businesses due to the high risks and high transactional budgets involved

when dealing with SMEs. A gap is formed owing to the disregard; this is what the IFC and

others denote as the SME Financial Gap. According to Price Water House Cooper

(PWC)banking survey conducted in 2013, SMEs are often referred to as the Missing Middle in

the context of financial inclusion or access to financial (including banking) services. Financial

inclusion can be described as the state in which every person has the opportunity or chance to

suitable, preferred financial services and products, in other to use or manage their money

commendably. This is attained by financial competence as well as financial literacy on the part

of the consumer and access on the part of financial products, services, and advice suppliers. This

means that SMEs are chiefly ignored when it comes to banking services and other financial

institutions. In other instances, SMEs are neglected when it comes to financial support such as

loans, grants, among others.

– Profile of the Organization (or Business Sector/Industry)

The organization profile primarily revolves around small and medium-sized enterprises which

can be referred to as those organizations where the number of workforces associated with the

company or revenue generation is limited to a certain extent. In addition to that, the asset under

the management of this organization is also limited within a certain threshold. One of the

Paraphrase This Document

entities that are independently owned. Following a recent study conducted by Deloitte in 2017, it

is observed that almost all of the small and medium-sized enterprises operating across Ghana are

having a workforce of fewer than 250 employees. On top of that, throughout the African nations,

small and medium-sized enterprises act as the backbone of the national economy; which

represents the significance as well as the gravity of contribution conducted by small and

medium-sized enterprises in terms of regulating the Ghana economy. On January 1st, 2005, a

new legislative principle was brought forward by the Ministry of finance in Ghana in terms of

revitalizing the national economy; with the help of consolidating SMEs that are operational

across Ghana. The main objective of this legislative principle is to undertake certain initiatives

through which funding programs can reinforce the facilitation of business aids in higher intensity

to small and medium enterprises. Additionally, the financial ceilings of aid acquisition are also

increased vehemently in this new legislation.

– Business Issue (or opportunity) Statement

The significance of SMEs in economic improvement is well recognized, SMEs in many

countries, developing countries in particular are not performing well (kessy & Temu, 2010). One

of the factors for poor performance is the lack of adequate finance to finance the operations and

expansion (Rweyemamu and Venter 2004). The funding of small and medium-sized enterprises

(SMEs) has been an issue of boundless concern to both legislators as well as investigators due to

the impact of SMEs in private sectors worldwide and the opinion that financially these firms are

inhibited. According to Ayyagari, et al (2007) on average, SMEs account for the majority

percentage of manufacturing employment. Since approximately 33% of the Ghana national

income is derived from businesses of small and medium-sized enterprises. Additionally, more

than 50% of the employment is only projected by medium and small-sized enterprises in

emerging economies such as Ga East municipality in Ghana. More essentially,

superior impediments as compared to big firms, on the other hand, but these features also coerce

SMEs (that is, disturb their performance) further, about huge firms.

Many SMEs do not have sufficient finance because they are unable to access bank loans (Nasser

et al 2003). Even those who can get access to bank finance, are unable to sufficient funds as they

request. While some SMEs get a small sum of the loan and some do not get at all, numerous

authors such as (Kessy and Temu, 2010; Kuzilwa, 2005; Rweyemamu and Venter, 2004; and

Nasser et al, 2003) argues that the inability to access finance is a challenge which impede the

performance of SMEs and in particular growth of SMEs. For example, Kessy and Temu (2010)

claim that “SMEs have very limited access to financial services from formal financial institutions

in particular credits to meet their working and investment capital needs”. While it is

consequently obvious, that access to finance is one of the elements that hamper the performance

and development of SMEs in the Ga East municipality; determinants of credit access have not

been researched. This study thus pursues to scrutinize the dynamics which determine access to

credit for SMEs in the Ga East municipality.

Project Questions

What are the sources of credit to SMEs in Ga East municipality?

Which factors influence SMEs ' access to credits in the Ga East municipality?

1.4 Objectives of the Study

1.4.1 Main Project Objective

To investigate the factors that influence SMEs ’ access to credits within Ga East

municipality.

1.4.2 Specific Project Objectives

To identify the sources of credits available to SMEs in the Ga East ………

To assess the factors that influence credit that can be accessed by SMEs in Ga East

municipality.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Ga East

To investigate the influence of interest rate on credit accessibility of SME's in Ga East

To recognise the outcome of electronic banking on accessibility of credit for SME's in Ga

East

1.5 Scope of the Study

The study concentrated predominantly on the determinants of credit accessed by small-scale

enterprises in Ga East municipality and advanced to designate the accessibility levels of the

diverse source of credit and assess the elements that affect the possibility of small Scale

Enterprises requesting funding. This study was conducted mainly within the boundaries of Ga

East municipality.

1.6 Significance of the Study

Access to credit is seen to be vital to the development and sustainability of small-scale

enterprises in Ghana and Ga East municipality to be precise. The result of this research will offer

complete evidence on the determinants of access to credit as well as their impacts on access to

credit by small and medium scale enterprises in the Ga East municipality. This research will also

make available detailed and laborious examination (analysis) of the components that influence

the probability of small-scale enterprises requesting funds.

Supplementary, this study will enlighten government, FIs, SMEs, and all engrossed interested

parties (that is stakeholders) about the elements or components that confine FI's delivery of credit

to SMEs. To end with, this research will add to the literature in this region of study that can

generate by future research.

1.7 Project Outline

This research is structured into five episodes which are arranged in the following manner; First

and foremost is chapter one which entails the background and viewpoint of the problem in the

study area. It encompasses predominantly the problem statement, objectives of the study,

significance of the study, the scope of the study the methodology used in this study. Chapter two,

on the other hand, captures a review of literature on the research topic. Chapter three also deals

with the Methodology. Chapter four depicts data analysis and presentation of findings.

Paraphrase This Document

analysis in chapter four of this study.

Summary

To summarize, it can be inferred that both medium and small-scale enterprises operating in Ga

East municipality across Ghana can enhance their business operation; provided they have

substantial access to credit facilities from the financial institutions and also help them to broaden

the scope of the business. Factors relevant to accessing credit are also evident throughout the

study with proper evidence so that organizations can operate fluently. Strategies that are

pertinent with credit accessing regulation in organizations are also discussed in the due course of

the study. Criteria of loan eligibility and how the organization can be able to fulfill the eligibility

criteria are also encompassed in the study. It is an important aspect of the research because, for

non-banking financial institutions, the strategies of determining the eligibility criteria are

completely distinct from banking financial institutions.

LITERATURE REVIEW

2.1 Overview

This section presents an evaluation of significant literature about this topic. This chapter also

aims to lay a theoretical foundation for the appraisal of the importance of the small and medium

enterprises (SMEs) sector to the Ga East municipality.

Firstly, the definition of SMEs is deliberated on, and the characteristics of the SMEs. It discusses

the historical development of credit in Ghana in general as well as the access to credit and

finance in Ghana by small and medium scale enterprises.

Additionally, it assesses the credit restructurings as well as the supervisory structure in Ghana

and a momentary performance of the credit and FIs in Ghana and some vitally interested parties

of the credit and finance sub-sector in Ghana. It further discusses the role and prominence of the

SME sector in economic development. The limitations faced by SMEs are also discussed.

Lastly, the determinants of access to funding by the SMEs within GA East municipality are also

discussed.

Theoretical Literature

Theory of Credit Rationing Hypothesis by Stiglitz and Weiss’ (1981)

Theoretically, the problem of lack of access to credit among small firms can be explained

through the theory of credit rationing propounded by Stiglitz and Weiss (1981). In their

exposition, Stiglitz and Weiss (1981) explain that lack of access to credit is due to imperfections

in the financial market, resulting in credit rationing-a situation where either some applicants’

loan applications are honoured and some rejected even though they possess similar

characteristics and are willing to pay higher interest rate or their applications for credit are

rejected because of the limited supply of credit.

Stiglitz and Weiss (1981) show that in equilibrium, the loan market can be characterized by

credit rationing. This is due to information asymmetry in the loan market, which results in

adverse selection-the sorting out of good borrowers from bad ones and moral hazard which

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Adverse selection results from the unequal probabilities of repayment by different borrowers.

Hence, banks use the interest rate as a means to distinguish good and bad risk borrowers. Stiglitz

and

Weiss (1981, p. 393) posit that “the interest rate which an individual is willing to pay may act as

one such device; those willing to pay higher interest rate may on average be worse risks; they are

willing to borrow at higher interest rate because they perceive their probabilities of repaying the

loan to be low”

They also note that moral hazard refers to the situation where the behavior of borrowers may

change after the loan contract has been made because borrowers may engage in undesirable

actions that may lower the probability of paying back the loan. In their view, borrowers may

undertake “projects with lower probability of success but higher payoffs when successful”

(Stiglitz and Weiss, 1981, p. 393).

Using demand and supply analysis, Stiglitz and Weiss (1981) explains the determination of

equilibrium interest rate. The supply of loans is influenced by the bank’s expected returns at the

‘optimal bank rate’ defined as “the interest rate at which the expected return to the bank is

maximized”. When there is excess demand for loans over supply, the interest rate rises.

However, banks would not lend above the optimal rate because it is riskier to do so, and

the expected returns of banks would be lower.

The supply of loans is also influenced by the amount of loan, the amount of collateral or equity

demanded by banks; however, increasing collateral beyond an optimal value may reduce the

returns of banks because of a reduction in average risk aversion of borrowers or result in the

undertaking of riskier projects. This is because there would be a reduction in the

equity of borrowers who could undertake smaller projects with a higher rate of failure. Banks

would therefore choose to deny loan applications because they are unable to distinguish between

bad risks applicants from those successful applicants, resulting in credit rationing.

Paraphrase This Document

by many banks and borrowers, both of whom are risk-neutral and aim at maximizing their

profits.

On the one hand, banks seek to maximize profit by the interest rate charge and the collateral they

request from borrowers. On the other hand, borrowers also choose projects that maximize profit,

while at the same time increasing the probability of repaying the loan. The costs of these

projects.

are assumed to be fixed and indivisible.

The life cycle theory and SME financing

Businesses are thought of as living organisms and as such go through a life cycle. From startups,

they go through several growth phases. The literature regarding the number of SME growth

stages has been mixed. There is therefore no consensus on the number of growth stages for

SMEs. For instance, whilst Steinmetz (1969) proposes three stages of SME growth, Lewis

(1987) and D’Amboise and Muldowney (1988) suggest five growth stages. Nonetheless, the

growth stage an SME finds itself determines the type of financing it requires. According to

Berger & Udell’s (1998) financing life cycle theory, financing preferences of SMEs change as

they move along the trail of growth. SMEs that find themselves at the startup and nascent stage

are usually associated with a high incidence of information asymmetry (Huyghebaert & Van de

Gucht, 2007; Hyytinen & Pajarinen, 2008). As a result, they depend mostly on personal and

informal sources of credit, since formal lenders tend to relegate them to the background. This is

because they usually lack a good track record (Huyghebaert & Van de Gucht, 2007) and do not

have enough assets to meet the collateral requirements of formal lenders.

However, as SMEs advance along the growth path, their desire for informal credit wanes, and

their quest for formal credit increases. This is because as they grow, they come to a point where

they can meet major requirements of formal lenders such as collateral (Domeher et al., 2017) and

evidence of a good track record (Bhaird & Lucey, 2010). Hence, they tend to seek credit from

formal sources. The above discourse reflects the fact that business age and size do matter in the

choice of financing source. Even though the financing life cycle encompasses equity finance

go public, debt finance is emphasized since this is the focus of the paper.

2.2 Definition of SMEs

A firm can be classified in terms of two groups of characteristics (Bolton, 1971): quantity

characteristics, such as employment, assets, turnover; and quality characteristics, such as

innovations and organizational structure.

Nonetheless, it can be noted that the latter is much more problematic to measure. Consequently,

the most common benchmarks for disparity amongst small, medium, and large firms are the

number of properties, of which the magnitude of employment and capacity of yearly revenue is

the most recurrently used.

Correspondingly, the world bank (2013) categorizes an enterprise as SME on the basis that any

of the subsequent standards or benchmarks namely, size of assets, annual sales, or several

employees are met, as follows: microenterprises are enterprises that have total assets or year

sales up to $10,000 and also employ up to 10 personnel in addition; small enterprises are

enterprises that have total assets or annual sales to be up to $3 million as well as employing up to

50 personnel, and medium-sized enterprises are described as enterprises that are worth total

assets or annual turnover to be up to $15 million as well as employing up to 300 employees.

As noted by Kushnir (2010), the decision to choose a particular SMEs definition relies on many

components among which include the country’s business culture; the population of that

particular country; industry; among others.

She mentions the lack of data on SMEs as a major challenge because of the circumstance that

numerous SMEs function in the informal sector, expressly in unindustrialized countries.

Additionally, the absence of a constant characterization of SMEs is because countries have

dissimilar structural,

From the abovementioned, there is no widespread meaning of SMEs, which relates to all

countries.

This is owing to the datum that SMEs are not identical; they diverge from one country to the

other and from industry to industry. On the other hand, SMEs are generally privately-owned

firms that have relatively a small number of personnel and a low volume of sales and fixed assets

(Nkuah et al., 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

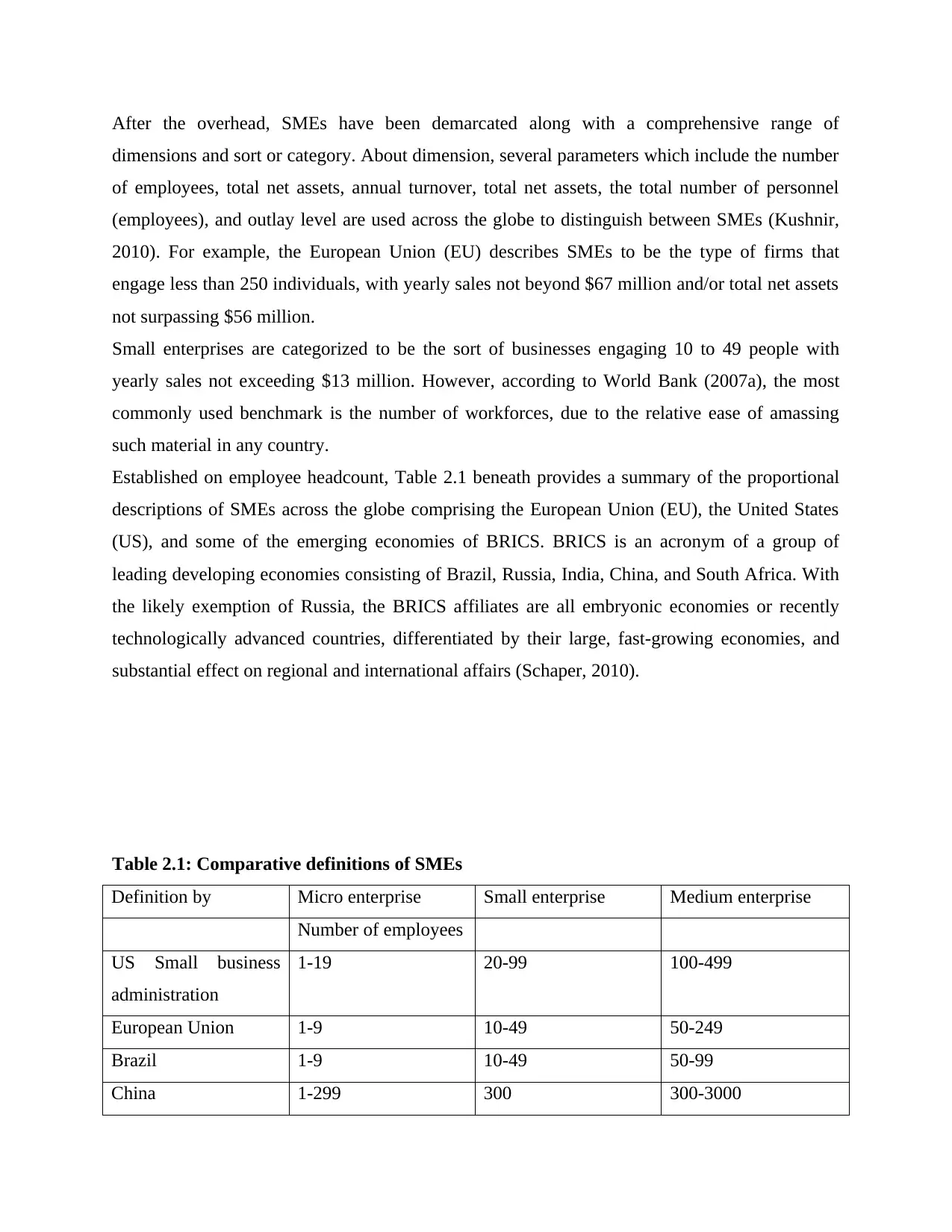

dimensions and sort or category. About dimension, several parameters which include the number

of employees, total net assets, annual turnover, total net assets, the total number of personnel

(employees), and outlay level are used across the globe to distinguish between SMEs (Kushnir,

2010). For example, the European Union (EU) describes SMEs to be the type of firms that

engage less than 250 individuals, with yearly sales not beyond $67 million and/or total net assets

not surpassing $56 million.

Small enterprises are categorized to be the sort of businesses engaging 10 to 49 people with

yearly sales not exceeding $13 million. However, according to World Bank (2007a), the most

commonly used benchmark is the number of workforces, due to the relative ease of amassing

such material in any country.

Established on employee headcount, Table 2.1 beneath provides a summary of the proportional

descriptions of SMEs across the globe comprising the European Union (EU), the United States

(US), and some of the emerging economies of BRICS. BRICS is an acronym of a group of

leading developing economies consisting of Brazil, Russia, India, China, and South Africa. With

the likely exemption of Russia, the BRICS affiliates are all embryonic economies or recently

technologically advanced countries, differentiated by their large, fast-growing economies, and

substantial effect on regional and international affairs (Schaper, 2010).

Table 2.1: Comparative definitions of SMEs

Definition by Micro enterprise Small enterprise Medium enterprise

Number of employees

US Small business

administration

1-19 20-99 100-499

European Union 1-9 10-49 50-249

Brazil 1-9 10-49 50-99

China 1-299 300 300-3000

Paraphrase This Document

South Africa 1-5 20-49 50-200

Source; (Schaper, 2010).

As reflected in Table 2.1, a small business in Ghana is an enterprise with 6 to 29 employees

while a medium-sized enterprise engages the services of between 30 and 99 persons. Though the

same medium enterprise would be categorized as a small business in the US; a business is

regarded as medium-sized if it employs less than 500 people whiles SMEs are defined as a

business with 19 or lesser personnel in New Zealand (Ministry of Economic Development,

2011). The EU and Brazil use the same perimeter to classify micro and small enterprises but

dissimilar cut-offs for the medium enterprise limit. Hence, many businesses in America and

Europe viewed as medium enterprises with 250 to 500 employees may be considered to be big

enterprises in South Africa where firms with up to 200 employees are classified as large.

However, given China’s huge inhabitants and the labor-intensive features of its SME sector, a

small business can employ up to 3000 employees depending on the industry (Kongolo, 2010).

Hence it is virtually difficult to associate SMEs globally since they vary basically over the

threshold heights for the difference between small, medium, and large firms.

From the above dialogue, it is evident that there is no widespread meaning of what establishes an

SME. It can be inferred that SME cataloging standards differ in several nations. Although SMEs

function practically in all industries, they diverge greatly in their nature and significance from

industry to industry and from nation to nation.

Gaining a substantial amount of access to credit from the perspective of business is

quintessential. Because for a business to revitalize its working function and maintain the bottom

line, it is necessary to have constant access to credit. In the recent economy of Ghana, without

having appropriate credit access, it is not available for small and medium enterprises to maintain

their workflow. From an apparent vision, it would seem that access to credit is only a means to

make purchases. However, in reality, it is not only limited to that extent; but also extends to

fulfilling obligations of everyday business operation in small and medium enterprises in Ga East

municipality in Ghana. To put it in statistical perspective, 27% of small and medium enterprises

in Ga East municipality in Ghana are completely functional because of their indomitable access

to credit. In a different perspective, it can be stated that three of the four businesses operating in

accessed. They have encountered several impediments in terms of managing the working

function, but on a similar note, these enterprises have also encountered hindrances that impeded

the seamless growth of the micro economy of Ga East municipality in Ghana extensively.

Several important aspects should be taken into consideration in terms of projecting whether a

business should be able to get credit access or not; depending on how the financial management

of the organization takes place. The financial institutions which are in charge of extending the

line of credit determine whether the organization is eligible for the credit or not. A survey carried

out by MasterCard in Ghana in 2018, it is revealed that 46% of businesses operating in Ghana

are experiencing credit impediments because inappropriate financial management strategies are

incorporated in terms of segregating personal expenses with business expenses. If appropriate

financial management strategies are incorporated in terms of managing the company's financial

perspective; then not only the business should be able to determine the ongoing trend associated

with the industry; but at the same time, the small and medium enterprises would also be able to

undertake better financial decisions about their business operation. Hence an inference can be

drawn that as far as business credit is concerned concerning small and medium enterprises

operation, a business which has an exemplary financial management track record can get suitable

access to credit from the financial institution so that the organization’s working function In other

words, small and medium enterprises that are still functioning as of now in Ga East municipality

in Ghana is capable of expanding their business horizon, provided they have convenient access

to credit. This is the motivation as to why the research is conducted in this particular concept.

From the argument above, it can be established that there is no harmony in the characterization

of SMEs, as businesses vary in their heights of employment, revenue as well as capitalization.

Hence, descriptions centered on size, once employed to one subdivision might result in all

enterprises categorized as small, while similar dimension description employed to a dissimilar

segment would bring about the enterprises demarcated as huge (NCR 2012). The nonexistence of

a distinct explanation of SME contrasts bank lending practices somewhat inconsistent (Calice,

Chando, and Sekioua, 2012:9).

Conversely, concerning our research, we looked at all the registered SMEs in the Ga East

municipality which has their records with the national accreditation board for small and medium-

sized enterprises in the Ga East municipal assembly.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

financing gap theory that was advanced by Stiglitz and Weiss (1981) who in their instigation,

maintained that agency complications (a conflict of interest amongst administration

(management or agents) as well as stockholders (owners) of the entity) and information

irregularities were the foremost cause why SMEs had inhibited access to funding. They reasoned

that only SMEs knew their actual financial framework, the genuine power of the outlay project,

and the effective purpose to pay off the liability, that is, firms had greater private information

(asymmetric information). Therefore, the bank manager made judgments under distorted

information, also operated under a moral threat as well as adverse selection risk.

Notwithstanding the discrepancy in the relative designations of SMEs, the enterprises have some

shared features. Firstly, the position of management, as well as ownership, are conferred on a

single person or family, bringing about subjective decision-making. Furthermore, SMEs need

small capital start-ups in common, irrespective of the country in which they are founded or the

type of industry. But, SMEs encounter complications in drawing exterior funds for growth;

hereafter they depend greatly on investment from friends and relations.

Additionally, there is no dissimilarity amongst business and private funds in this manner

resulting in in-efficiency and non-performance of many SMEs. The subsequent segment

addresses the distinguishing features of SMEs which effects their access to finance.

2.3 Characteristics of SMEs

The word SME is used in the European Union and other international organizations to label

small to medium enterprises-companies that have a restricted, quantified number of personnel.

The United States characteristically uses the SMB, for small to medium businesses. Cataloging

as an SME is established on the number of employees, mostly between 10 and 250 to 500, reliant

on the country in which the business is situated. The Small Business Administration (SBA) of

the US describes a small business as “one which is independently owned and operated for-profit

and is not dominate in its field” (Hughes 2011). All SMEs share identical mutual features

irrespective of the industry and indigenous markets which comprise the following;

2.3.1 Reliance on few employees

Numerous SME firms are fairly small and have only limited employees. This inadequate staff is

expected to carry out all essential tasks comprising accounting, marketing, innovation,

Paraphrase This Document

the administrator who supervises all aspects of the entity. This may be a hindrance where the

personnel is not equipped with the prerequisite set of skills to execute compound tasks well;

though, this sort of business edifice stimulates long-term firmness rather than concentrating on

short-term results. Since the number of employees working in small and medium scale

organizations is extremely limited in nature, managing this employee can be a very convenient

responsibility for the concerned authority; which means delegating responsibilities to individuals

and ensuring that the task is completed within a predetermined time frame is highly probable

concerning logical companies. In addition to that, addressing the queries for resolving grievances

that are registered by the target market in which the small-scale company operates is also

feasible in nature.

2.3.2 Simplicity

The SME is a modest corporate framework that permits the firm to be very elastic as well as

creates the essential variations swiftly deprived of such necessities as addressing board members

or shareholders for endorsement. The elasticity, conversely, does not certainly ensure the

organization is recognizing domestic or nationwide code of practice which a panel or legal team

of a huge entity would analyze preceding to setting such alterations into place. The simplicity

associated with the working function of small and medium scale enterprises is one of the greatest

advantages that can be capitalized on by these industries as well as management authorities in

terms of banking on new opportunities that are completely unexplored by large scale

organizations in Ga East municipality in Ghana. Since the approach of managing a working

function is quite distinct from large-scale companies; the probability of this organization

experiencing hindrances would also be reduced. However, if appropriate financial

management strategies are not incorporated at the initial phase; then the probability of this

organization experiencing an impediment down the line is inevitable. That is why this category

of the organization is in dire requirement of financial support from the government.

Small-scale businesses aid a quite reduced or less significant zone as compared to organizations

or large private entities. The smallest-scale businesses aid distinct populations, for instance, a

handiness shop in a rural settlement. The actual description of small-scale precludes these

enterprises from attending to regions far grander than a limited location, because developing

further than that will upsurge the measure of a small business’s maneuvers as well as drive it into

a different category. The market area upon which the small and medium scale enterprise operates

also crucially determines how the financial performance of the small and medium scale would

play out. In other words, if an appropriate market location is selected; then the feasibility of the

small-scale organization to experience profitability within a short span of operation is highly

probable; concerning other locations which are not at all suitable for appropriate market

conditions.

2.3.4 Locations

A small–scale business, by description, could be discovered only in limited areas. These entities

are not probable to owe new sales openings in numerous nations or states, for example. A

countless quantity of small-scale companies works from a retail shop service outlet or solitary

office. Deprived of any company convenience, it is possible to manage a small enterprise straight

from the comfort or convenience of your home.

2.4 Historical development of credit in Ghana

Giving money to individuals, anticipating that the money would be paid back plus interest is an

ancient occupation. It can be noble business, but it is also a very precarious business.

Undeniably, the notion of credit is not new in Ghana (Kwaku. P, 2010).

There always has been the practice of people saving and/or taking minor advances from

individuals and groups within the framework of self-help to commence businesses or farming

endeavors. For instance, existing evidence proposes that the paramount credit union in Africa

was established in Northern Ghana (Upper West-Jirapa) in 1955 by Canadian Catholic

Missionaries (Johnson P.A, 2007).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

thanks to numerous financial segment plans as well as packages embarked on since

independence by diverse regimes. Included are enumerated below:

Delivery of bankrolled (subsidized) funds in the 1950s

Addressing the financial need of the agricultural and fisheries sector by establishing the

Agricultural Development Bank in 1965.Establishment of the Agricultural Development

Bank in 1965.

Rules and regulations such as the requirement that commercial banks set aside 20% of

their total portfolio, as well as the establishment of Rural Community Banks (RCBs) in

the 1970s and the early 1980s to encourage or stimulate lending to agriculture and small

scale enterprises.

Moving from a restraining financial subdivision administration to ease up administration

in 1986

Allowing the establishment of dissimilar or diverse classifications or sort of non- bank

financial institutions, encompassing credit unions as well as savings and loans companies

through the declaration or decree of the PNDC Law 328 in 1991.

The programs have resulted in the development of three broad classifications of credit as well as

FIs which are enumerated below:

Formal suppliers such as savings and loans companies, rural and community banks, as well

as some development and commercial banks.

Semi-formal suppliers such as credit unions, financial non-governmental organizations

(NGOs), and cooperatives.

Informal suppliers such as “susu” collectors and clubs, rotating and accumulating savings

and credit associations (ROSCAs and ASCAP), traders, moneylenders, and other

individuals.

About the regulatory outline, Savings and Loans Companies are controlled under the Non-

Banking Financial Institutions (NBFI) Law 1993 (PNDC Law 328), whereas Rural and

Community Banks are controlled or structured under the Banking Act 2004 (Act 673).

However, the controlling or supervisory structure for credit unions is now being established, and

this would identify their dual nature as cooperatives as well as FIS. The remaindered of the

Paraphrase This Document

frameworks.

Agricultural Services Investment Project (ASIP), the United Nations Development Programme

(UNDP) Microfinance Project, the Community Based Rural Development Programme

(CBRDP), Rural Enterprise Project (REP), the Social Investment Fund (SIF), Financial Sector

Strategic Plan (FINSSP), the Rural Financial Services Project (RFSP), as well as the Financial

Sector Improvement Project (FINSIP) are all programs currently encompassed in addressing the

sub-sector in Ghana. (Johnson P.A, 2007)

2.5 Credit reforms and regulatory framework in Ghana

With the introduction of SAP (Structural Adjustment Programme), lending and deposit charges,

as well as credit regulators were meaningfully abridged. Obstacles to admission into the financial

division and money were also eradicated. The Reserve Bank Act was reviewed to eradicate

separation as well as to enhance rivalry. Limitations on the employment of excess reserves and

the interest cap on them were jettisoned, releasing such resources for outlay in the market at the

sovereign market tariffs.

The accomplishment of these as well as further changes in the financial subdivision can be

witnessed in the enhancements towards the gathering of reserves. This region is one of the very

uncommon that encountered progress under SAP’s Millennium Economic Recovery Programme

(MERP). The sector was flooded with lots of new competitors. Rivalry as a consequence of fresh

participants also added to the upgrading of the variety of services and products delivered to

consumers. Lending by the financial segment amplified in 1991. Though investigations designate

that rural and underprivileged urban societies did not profit from these restructurings.

Extraordinary interest charges that described credit from banks and other finance houses trickled

over into the informal sector, with money lenders charging even higher interest rates than banks

(Moyo, 2001).

In Ghana, the power assigned by the law to overseas well as police the permitting or accrediting

and set-ups of credit agencies is the Bank of Ghana. The Bank of Ghana (BoG) would certify

that credit agencies act in a way that is expected of them, and desist from the activities in which

they are expected to undertake.

This supervision or controlling of credit establishments is cited in the Credit Reporting Act,

2007(Act 279). According to the credit agencies, if you acquire a loan from a FI and are not able

can locate you or not, would furnish the credit bureaus with this information. If you can service

the loan too, this information is given to the credit bureaus. This is done to ensure the credit

worthiness of the borrower from the credit bureaus by asking them for information concerning

you when next you endeavor to request for financial assistance from any FI or attempt to acquire

any service on credit. The way this credit reporting is done in a different place, your data is

captured into the databank of credit agencies, even if your application for a loan or credit is

repudiated. Or, even where you are unable to pay your utility bills over a lengthy period, credit

agencies can also capture such information.

The worthy thing however is that; you can request a copy of all the data held about you in

writing to any credit agency at a fee. (Kwaku P, 2010).

In a nutshell, a credit agency (according to the current regulation) has been given the mandate to

possess information that would assist creditors and FIs to evaluate threats as well as take the

correct resolutions on credit as well as loan submissions from the public in general.

2.6 Importance of SMEs to the economic development in Ghana

There is a universal accord that SMEs contribute confidently to the economic as well as social

development of developed and developing countries. Economically, SMEs are known as engines

through which development purposes of developing nations can be attained. As such, SMEs

perform a substantial role in creating employment and revenue for both the rural as well as the

urban population and tend to engage more labor demanding (intensive) technology as compared

to huge firms (Newman, 2010).

The role played by medium and small-scale enterprises in terms of rejuvenating the national

economy of Ghana is crucial. For the reason that the characteristic features which are associated

with SMEs revolve around increasing production of a nation, which would require a workforce

to substantiate their respective business operations. This can necessarily be translated into the

fact that the rate of unemployment would reduce the nation as soon as the number of SMEs

increases. Apart from employment generation, the scope of economic contribution in export

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

consolidate the backbone of the national economy in Ghana.

The SMEs that are operating in Ghana can be broadly categorized into traditional SMEs as well

as modern SMEs. However, the number of modern SMEs is increasing day by day as per the

report published by MasterCard. The characteristic difference between the traditional SME and

the modern SME is that the workforce, as well as technological advancement, is substantially

distinct in the modern SME concerning the traditional SME. The regulation of modern SMEs in

Ghana is also bringing certain legislations which can further assist the Macro economy of Ghana

extensively. The scope of investment associated with SMEs also increases the number of chain

operations which can further give employment scope and opportunities for return on investment

which can captivate willing investors to get a line with SMEs.

The current political regime in Ghana has brought forth varieties of legislation to encourage and

support entrepreneurs. The main cause behind extending this assistance from the government by

furnishing legislation lies behind the consequences of SMEs' operation. For emerging

economies, small and medium enterprises can not only change the entire dynamics of the macro

economy but also assist the nation to get ahead of its competitive curve eventually. As far as

technical support is concerned, SMEs can bring forth the necessary change and make

amendments in infrastructure development across the nation; which can seamlessly give

hundreds and thousands of job opportunities for skilled labor in Ghana. Some of the noticeable

legislations would not only extend preferential access of credit to the businesses but at the same

time, preferential policy support is also extended to small and medium-sized enterprises in Ga

East municipality in Ghana.

Paraphrase This Document

Ghana are spearheaded by small and medium-sized organizations. To put it in simple perspective

it can be stated that the contribution of small and medium organizations in the manufacturing

sector in Ghana is simply paramount. Not only are they incorporating new technologies which

are recently developed, but at the same time, there are also generating employment opportunities

in the thousands. The manufacturing sector alone contributes 18% of the gross domestic product

in Ghana. Consequently, it can be inferred that small enterprises are the backbone of the national

economy. It is a value-added measure that is incorporated by the government by subjecting

preferential policy treatment towards the medium-sized enterprises in the small scale

organization in Ghana.

Of late, a recent trend is also taking place in Ga East municipality which is oriented towards

export promotion. It would address the current importance of the manufacturing sector. In 2019,

it is pointed out that one of the crucial shortcomings of the manufacturing sector which is

spearheaded by these small-scale organizations in Ghana is imbalances in terms of regulating

payments accounts. Export promotion would permanently mitigate the shortcoming extensively.

Unlike the large scale organization where the accumulation of wealth is primarily emphasized;

small-scale organization solely believes in equal distribution of income and opportunities

through which the operation of small scale business enterprises can be multiplied within a short

period. This is a strategic action undertaken by the small-scale organization in terms of

revitalizing the national economy of a country, especially in the emerging ones like Ghana.

These opportunities can be capitalized on by skilled labor that is already available in Ghana. The

concentration of wealth is not emphasized necessarily in medium-scale enterprises. However,

widespread equal distribution of wealth is prioritized as well as practiced by the medium-scale

national economy is significant. However, large companies cannot substantiate the ambiance

where the growth of entrepreneurs can take place in Ghana. Consequently, small-scale

organizations have given opportunities for entrepreneurs to explore areas where untapped

resources have potential. As a consequence of that, the probability of these entrepreneurs starting

their small-scale industry or even growing up to medium-scale organizations within a few years

would be a beneficial factor for the Ga East municipality’s micro-economy. Moreover, the

growing entrepreneurship culture would give rise to a plethora of startup cultures which can

further alleviate the economic condition associated with Ga East municipality. Small-scale

organization maintenance is a challenging responsibility that entrepreneurs cannot always

resolve. As a result of that, the preferential support policies are forwarded by the government

authorities; so that financial aid can be provided by municipalities' concerned government

agencies which can resolve crises in small-scale organizations. Accumulation of financial

support from government agencies can forward the SMEs extensively which in turn can bolster

the municipality's economics faculties extensively. Individuals who are deprived of accessing

opportunities can also be aided by the growth of small-scale companies. The notion of lean

production and optimal utilization of resources can be effectively practiced by small-scale

organizations which is a challenging responsibility for large-scale companies. Additionally,

medium-scale enterprises can effectively utilize the resources available to fulfill the preferences

of the target market. Therefore, excess products can be oriented for export promotion which

would open up new horizons for business opportunities to be capitalized on by small and

medium scale enterprises.

The significance of SMEs to economic growth has made them focal points in policy making in

both developed and developing economies (Eikebrokk and Olsen, 2007; Maredza and Ikhide,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

developing and emerging countries (Beck et al, 2006). For example, in India and China, SMEs

dominate the industrial and commercial infrastructure (Ebrahim et al, 2011).

SMEs also have advantages over large established firms as they are capable of adapting much

easier to market conditions because of their agile state (Abor and Quartey, 2010). Typically, they

are more flexible as a result of their flat hierarchical structures and are consequently capable to

react quickly to variations in the outer economic surroundings. Therefore, the turnaround period

for the development of a new product tends to be quicker for SMEs than for larger firms.

Furthermore, SMEs are more labor demanding about bigger firms and consequently are

associated with lower capital costs about job creation (Musara and Fatoki, 2012). Less capital per

worker is used in small businesses and can use capital more effectively and efficiently as

compared to larger firms. Where they are situated in the urban zones, SMEs stimulate

unexploited resources and talents, adding to a more unbiased spreading of income, which plays a

vital role in sectoral balance and regional development and therefore helps fortify political

steadiness in the economy.

2.7 The Constraints Faced by SMEs

Credit is an indispensable need for enterprises, predominantly SMEs which however minute

(small) can mutate into bigger firms when given the chance. Nonetheless, these same enterprises

lack the desirable exterior finance. In addition, Fatoki&Odeyemi, (2010) observed that about

75% of SMEs in Ghana failed within the first two years of operation due to several challenges

that impede their survival. Fundamental amid these encompass imperfectly sophisticated

workforce, crime, and corruption, inefficient legal systems, restricting labor code of practice, the

nonexistence of administrative and entrepreneurial skills, an unproductive government

bureaucracy, inhibited access to financing, and insufficient provision of infrastructure.

According to Fatoki (2012), there is evidence that regulatory constraints resulting from

government bureaucracy place a proportionally high burden on SMEs, especially those in

developing economies such as Ghana. As such, SMEs repeatedly find it problematic to obtain

regulatory authority to conduct business undertakings. Regulatory barriers prevent SMEs from

operating in sectors of the economy in which local governments have a vested interest in

protecting state-owned enterprises (Newman, 2010). Also, the restrictions encountered by SMEs

Paraphrase This Document

whereas the supply flank elements relate to the creditor (financial intermediaries). comprising in

the demand-side factors are deficiency of information concerning bank products and services and

the solicitation procedure, being ‘discouraged’ by the perception that low-income earning clients

are denied loans by financial institutions, the nonexistence of collateral, and absence of

repayment capacity due to lack of secure income.

The supply-side factors are deficiency of tailor-made products, the resolution of either to a loan

or not, and in what quantum (Chen and Chivakul, 2008) among others. The existence of credit

constraints or the credit access difficulty is a result of the demand and supply-side factors. By the

principle of demand and supply, a credit constraint arises if the demand for credit exceeds what

financial intermediaries can offer (Ruiz-Tagle, 2005). From an alternative viewpoint, Banerjee

and Duflo (2004) assert that a credit constraint firm is unable to borrow as much as it would like

to at the going market rate.

Empirical Literature

2.8 The Determinants of access to funding by SMEs in Ga East municipality

Credit access in this framework refers to the likelihood that individuals or enterprises can secure

or access credit or loans from financial institutions (commercial banks) as well as Non- financial

institutions. Alhassan and Sakara (2014) find that the number of firm characteristics such as

fixed assets possessed, the size and form of business as well as and the sector of business in the

economy are important success factors in accessing bank finance in Ghana. Osei-Assibey (2014)

finds that a firm’s age, asset structure, and ownership of bank accounts increase the likelihood of

having access to finance among rural non-financial enterprises in Ghana.

2.8.1 Firm’s Age

Numerous studies have reasoned that older firms encounter little limitations in accessing credit

as compared to fresher firms. For instance, Beck and Cull (2014), this is that older firms tend to

have a greater reputation which increases the chances of accessing credit (Osei-Assibey, 2014).

This is as a result of the deficiency of sufficient information on the financial performance of

young as well as new firms makes it challenging for financiers to authorize their demand for

spell of offering financial assistance may be restricted for newer firms as a result of a lack of

conventional track record making the engagement charges correlated with loaning to fresher

firms moderately higher (Pandula, 2011). Moreover, younger, as well as fresh businesses or

enterprises, are less likely to meet the security requests of the banks as a result of the fact they

have not amassed ample fixed assets (Pandula, 2011; Adomako-Ansah, 2012).

2.8.2 Industry/Sector of the Firm

Pragmatic studies designate that firms in the services segment are more likely to acquire credit as

likened to their counterparts in the agricultural region as a result of the low level of threat and

reasonably increasing level of sales and turnover connected with the former (Kumah, 2011).

Furthermore, Deakins et al. (2010) find that manufacturing SMEs have less access to credit

because there is more information is required of them, especially in circumstances relating to

new technology, new products, in addition to divergence.

2.8.3 Firm’s Performance

The performance of SMEs is one of the standards or criteria for evaluating or assessing the credit

worthiness of the firm. This is occurring because well-to-do firms are more likely to be able to

service their loans. Pandula (2011) uses the average twelve-monthly sales growth for the

previous three years as measured by firm performance since it provides an enhanced indication

of financing requirements compared to that of only a particular year. One of the major reasons

why firms or businesses are unable to have access to credit is as a result of underprivileged

(poor) business performance. Baah-Nuakoh (2003) finds that credit is the utmost severe

limitation amid deteriorating or diminishing as well as stationary (stagnant) firms.

2.8.4 Firm’s Innovation

An empirical study by Ahmed and Hamid (2011) designates that innovation of the firm also

significantly influences the firm’s access to credit. This is because of the lender's perception of

threats and uncertainties linked with, principally product innovation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

in terms of how innovation is evaluated. Ahmed and Hamid (2011) define innovative firms as

those which have introduced a new process only over the last three years.

2.8.5 Firm’s Size

Another criterion for assessing the credit worthiness of a firm by financial institutions is by its

size. (Pandula, 2011; Kumah, 2011). Experimental studies by Pandula (2011) point out that small

entities are more credit inhibited as compared to huge entities about their incapability to deliver

financial data demanded by the FIs for selection and in numerous instances, they lack reviewed

financial reports or accounts (statements). Furthermore, minor firms have less fixed assets to

serve as collateral or security; and additionally, they have an increased risk of failure rate as

likened to huge firms.

2.8.6 Level of Education.

Researchers do not have a common agreement on the effect of the entrepreneur’s level of

education on access to credit (Kimuyu and Omiti 2000). Some have reasoned that education

hampers the realization of entrepreneurial outcomes by decreasing interest, vision, and the

preparedness to take risks. Formal education is said to formulate the issue to emphasize more on

white-collar jobs than the improvement of entrepreneurial skills and self-employment. However,

others have debated that education helps to differentiate entrepreneurs who access credit as well

as those who do not (Lore, 2007). In this instance, education enhances a person’s capability to

access or acquire information and skills which end up helping in formulating projects that can

entice credit from financial institutions. Enterprises with more or supplementary educated

proprietors can be anticipated to have more access or link to institutional credit as compared to

those enterprises with less-educated owners. This comes about since less educated owners are

inclined to have struggled with application processes and are expected to be rejected. Also, well-

educated managers are more probable to conceive managerial skills in finance, marketing

production, and international business that would result in the growth of the firm (Kumar 2005).

2.8.7 Collateral security

In advancing(lending) contracts or arrangements, collateral is a borrower's promise of precise or

explicit property to a lender, to secure repayment of a loan (Joan 1995). The surety or guarantee

Paraphrase This Document

borrower to service or repay the primary loan amount as well as the interest under the terms of a

loan obligation. If a borrower does default on a loan (due to insolvency or another event), that

borrower forfeits (gives up) the property pledged as collateral - and the lender then becomes the

owner of the collateral.

The research undertaken by Wanjiru (2000), revealed that one of the major determinants of

access to credit by SMEs from the FIs in Ga East municipality is collateral. This is about the fact

that mainstream of the respondents found the necessities of qualifying for credit in terms of

collateral as being unachievable.

2.8.8 Ownership type

Entrepreneurs select proprietorship frameworks in huge measure to guarantee sufficient funding

and as a result of the choice consequences, where funding is granted to entities that have

favorable ownership framework (Pandula, 2011). The ability of enterprises to have access to

finance can be influenced by the ownership structure. For example, the earlier study discovered

that registered firms and alien-owned enterprises encounter minimal financial restrictions (Beck

et al, 2006). Storey (1994), discovered that xxvii legal standing affects bank lending. He

additionally states that corporate status at start-up appears to be associated with a greater

likelihood of bank lending.

2.8.9 Audited accounts

Bass &Schrooten (2005) established that the nonexistence of dependable data brings about

comparably high-interest charges irrespective of the fact that there exists a long-term relationship

between the banks about the borrower. In such circumstances, the availability of appraised

financial reports plays a key part. In acquiring or obtaining credit from FIs, it is advantageous to

possess audited financial statements. Frequently, it has been discovered that, for banks to be able

to provide or offer credit, audited financial statements are required. For instance, Berry et al

(1993) revealed that lenders in the UK show a lot of interest in accounting data to treat the loan

submissions of small enterprises. Nonetheless, the majority of the SMEs in Ghana have

challenges when it comes to obtaining financial assistance from recognized FIs since they do not

have appropriate financial records. The majority of the businesses often keep various sets of

principles. These enterprises, in the long run, acquire loans at very high-interest charges or tariffs

on the hand, since banks consider them as high-risk borrowers as compared to those with a well

audited financial statement prepared under reliable accounting principles or standards.

CHAPTER THREE

PROJECT IMPLEMENTATION

Overview

Chapter three entails the processes or ways, methods or approaches, tools and techniques used in

the study to facilitate in assessing or evaluating the key or most important contributing factors

(determinants) of financial assistance (credit) acquired (accessed) by Small and Medium Scale

Enterprises in Ga East Municipality. The major factors that lead to credit access by small and

medium scale enterprises, Research Design, Study Population, Sample Size, and instruments

used for Data collection as well as Data analysis techniques are all discussed in this chapter.

Methods

The study was conducted in Ga East Municipal. Ga East Municipal District is bordered on the

north by the Akuapim South District in the Eastern Region of Ghana. It is bordered on its other

three sides by other districts in the Greater Accra Region of Ghana. To the west is the Ga West

District, to the south Accra Metropolis District, and in the east the Tema Metropolis District.

Ga East Municipality has its capital as Abokobi.

Research Design

The collection and analysis of data in a logical or systematic and well-ordered or organized

approach in an attempt to make or get significant information from it is referred to as research

design. (Zikmund, 2003: Jankowice, 2005). It can be said to be the plan or blueprints and

framework or edifice of examination or exploitation considered to attain answers to the research

problem. This study is premeditated to deliver an in-death or detailed process of surveillance,

collecting or amassing, analyzing or scrutinizing, and interpreting data using quantitative and

qualitative research approaches. This research was undertaken to define the significant factors or

dynamics of credit access by small and medium scale enterprises in Ga East municipality.

Quantitative as well as Descriptive research designs or schemes were used for our study. Due to

the voluminous nature of the case study, a Descriptive research method or technique was adopted

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

research design or approach was also used to give a statistical, mathematical, or computational

view of the data that was gathered or collected out from the descriptive research. Quantitative

research is referred to as the systematic or organized empirical investigation or probe of social

occurrences or phenomena through computational or mathematical, or statistical methods. The

quantitative research method is to develop and use mathematical models, concepts, or postulates

relating to the occurrences and also employed to deal with variables that were congregated from

the survey research via well-thought-out or structured questionnaires.

Study Population

The population is an entire collection of all observations of interest (people object or

event) as defined by Burns and Burns (2008). SMEs registered to operate within Ga East

Municipality, financial institutions operating within Ga East Municipality, as well as non-

financial institution operating in the area, constituted the study population. The

population of the study encompassed eight (8) Commercial Banks and four (4) Non-Bank

Financial Institutions (NBFIs) in Ga East Municipality. More explicitly, the study

focused on NBFIs as well as commercial banks in Ga East Municipality. As a result of

the existence of an ample number of FIs providing each institution with an equal

opportunity of being represented, Ga East was selected for this study and also considering

the limited amount of time and available resources for this study. Principally, the number

of financial and non- financial institutions comprised the following Banks (Access Bank,

Ghana Commercial Bank, Absa Bank, Ecobank, Agricultural Development Bank, Stanbic

Bank, Consolidated Bank, Fidelity Bank). Non-Financial Bank (Done well insurance,

Loyalty insurance, Star assurance, Traders credit union). Small and Medium Enterprises

(Nyame one hene Enterprise, Queen’s Secret skin care).

Sample Size Determination

Sampling is the process of choosing a unit (for example organization or individuals) from a

definite populace of importance therefore, by observing the unit (sample), the specific populace

from which they were picked or selected can be generalized (Neuman 2011). Sampling

techniques are described as the systematic or organized steps the researcher implements or

employs in selecting objects amongst the sample. It also makes emphasis or stresses on the

number or quantity of objects to be taken into consideration in the sample in other to make

Paraphrase This Document

banks and SMEs in the Ga East Municipality and since the population of staff was relatively

small, non-probability sampling was used to obtain the data. Non-probability sampling

techniques suggest that the chances of an element being chosen are unknown. Furthermore,

purposive sampling was used for the interview guide. Sample size identification is the process of

indicating the amount or quantity of elements to be encompassed in a numerical sample. The

sample size is a significant characteristic of any pragmatic research within which the objective is

interpreted about a populace from a sample. All Banks and Non-Bank financial institutions in the

Ga East Municipality were demarcated for the Study, based on a population of eight (8) banks

and four (4) Non-Bank Financial Institutions in the Ga East municipality (making a total of

twelve). However, in this case, where all the institutions in the study are used there was no need

to use a sampling technique. In the case of identifying the determinants of Small-Scale

Enterprise financing in Ga, 100 questionnaire were administered based on a simple random

sampling of small-scale entrepreneurs within the Ga East Municipality.

Sampling Procedure

Research techniques are referred to as the systematic measures that can be followed to a mass

facts, as well as scrutinize or examine them to acquire or obtain the information which they

possess (Jankowicz, 2000). Credit Officers, Credit Managers in addition to Relationship

Managers within various financial institutions were presented by the management of the various

financial institutions to assist us in obtaining information. We received suitable replies for the

questions that were thrown to the respondents after the objective of our study or research was

disclosed to them. They were guaranteed of the concealment of the facts being divulged to us by

them and we again guaranteed them that, this would have no impact on their employment status

in the organization as well as the operations of the organization in any form. Furthermore, they

were given the assurance that during the analysis their response was to be treated as a unit, and

also the information provided by them was not to be disclosed to any third party without seeking

their consent first as well as the information they furnished us with was to be used for purposes

of research only. The study also collected primary data from SME owners using questionnaires.

Source of Data

Two major forms of data were collected in this study, that is;

via uninterrupted or straight hard work and understanding or skill, explicitly for the tenacity or

reason of tackling his study problem. Raw data or first-hand information or data is another name

conferred to this type of data. The data gathering or accumulation is under undeviating or strict

regulations under the management or administration of the researcher.

Case study, personal interviews, mailed questionnaires, physical testing, and questionnaires filled

and sent by enumerators, observations, surveys, as well as focused group discussions, among

others, are all approaches or means via which data can be collected. Structured interviews,

questionnaires, and surveys were the approaches employed in collecting primary data in this

study.

Secondary data: On the other hand, infers or suggests second-hand data or evidence which is

previously or before now assembled as well as documented by anybody apart from or accept the

user of the information for a resolution, not connecting to the present study problem. It is the

readily sort or type of data amassed or accumulated from countless bases or fonts such as

websites, internal records of the entity, reports, government publications, censuses, books, as

well as journal articles, among others. It provides quite a lot of benefits as it is effortlessly

obtainable or available, and also saves the researcher a lot of cost and time. Secondary data for

this study was collected or acquired from the Ga East Municipal Assembly which included

information on community profile and the number of registered Small-Scale Enterprises as well

as FIs in Ga East Municipality.

Materials/Data

Data gathering or collection apparatuses are the tools or equipment that are used in the amassing

or generation of data for the study. Enumerated below are some of the data collection

instruments that are commonly used by researchers to collect data for their study;

Questionnaires

A questionnaire is a data gathering or accumulating apparatus which consists of a sequence of

questions and other prompts for the determination of assembling facts (information) from

respondents. Sir Francis Galton was the inventor of questionnaires.

Interview Guide

⊘ This is a preview!⊘

Do you want full access?