University Assignment: Credit Analysis and Lending Management Report

VerifiedAdded on 2022/11/23

|26

|4439

|93

Report

AI Summary

This report provides a detailed credit analysis and lending management evaluation of Maxis Communications, a Malaysian communication service provider seeking a RM50.0 million loan for infrastructure expansion. The analysis includes both quantitative and qualitative assessments. The quantitative analysis examines the company's financial performance over a five-year period, utilizing income statements and profitability ratios like net profit ratio, asset turnover, and interest coverage ratio to determine its ability to generate revenue and repay the loan. The financial position is evaluated using balance sheets and liquidity and solvency ratios such as the current ratio, quick ratio, and debt-to-equity ratio. Qualitative aspects are also considered, although they are not extensively detailed in the provided text. The report aims to assess Maxis's capacity to borrow and repay the loan, providing insights into its financial health and suitability for the loan approval.

Running head: CREDIT ANALYSIS AND LENDING MANAGEMENT

Credit Analysis and Lending Management

Name of the Student:

Name of the University:

Authors Note:

Credit Analysis and Lending Management

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CREDIT ANALYSIS AND LENDING MANAGEMENT

Executive summary:

Globalization has created number of opportunities for large entities across the globe to expand

their business operations including expansion of infrastructure and other facilities in different

parts of the globe. As a result companies are continuously looking to enter new markets or

expand its facilities in existing markets. However, expansion is very costly for any organization

and requires huge amount of fund. Often the huge requirement of fund becomes a constraint for

an entity and a barrier in its way of expansion. Generally an entity has two broad sources to

generate necessary funds required for expansion; these are internal sources and external sources.

Internal sources include use of retained earnings, i.e. the accumulated profit of the company over

the years. External sources on other hand include issue of share capital or borrowing from banks

and financial institutions. Borrowing is relatively easier option if an entity fulfills the required

criterions needed by the banks and financial institutions for approving loans to companies. A

detailed discussion in this document shows the important aspects that the banks consider before

deciding on the eligibility of an entity to get loan. Both quantitative and qualitative aspects have

been discussed here in relation to the loan requirement of Maxis Communications in this

document.

CREDIT ANALYSIS AND LENDING MANAGEMENT

Executive summary:

Globalization has created number of opportunities for large entities across the globe to expand

their business operations including expansion of infrastructure and other facilities in different

parts of the globe. As a result companies are continuously looking to enter new markets or

expand its facilities in existing markets. However, expansion is very costly for any organization

and requires huge amount of fund. Often the huge requirement of fund becomes a constraint for

an entity and a barrier in its way of expansion. Generally an entity has two broad sources to

generate necessary funds required for expansion; these are internal sources and external sources.

Internal sources include use of retained earnings, i.e. the accumulated profit of the company over

the years. External sources on other hand include issue of share capital or borrowing from banks

and financial institutions. Borrowing is relatively easier option if an entity fulfills the required

criterions needed by the banks and financial institutions for approving loans to companies. A

detailed discussion in this document shows the important aspects that the banks consider before

deciding on the eligibility of an entity to get loan. Both quantitative and qualitative aspects have

been discussed here in relation to the loan requirement of Maxis Communications in this

document.

2

CREDIT ANALYSIS AND LENDING MANAGEMENT

Contents

Executive summary:........................................................................................................................1

Introduction:....................................................................................................................................3

About the company:.........................................................................................................................3

Loan requirement and the objective of application for loan:...........................................................4

Evaluation of company’s capacity to borrow the required funds:...................................................4

Quantitative analysis:...................................................................................................................4

The financial performance of the company:................................................................................5

Financial position analysis of the company:................................................................................9

Cash flow position of the company:..........................................................................................15

Qualitative analysis:...................................................................................................................19

Observation:...................................................................................................................................22

Conclusion.....................................................................................................................................23

References:....................................................................................................................................24

CREDIT ANALYSIS AND LENDING MANAGEMENT

Contents

Executive summary:........................................................................................................................1

Introduction:....................................................................................................................................3

About the company:.........................................................................................................................3

Loan requirement and the objective of application for loan:...........................................................4

Evaluation of company’s capacity to borrow the required funds:...................................................4

Quantitative analysis:...................................................................................................................4

The financial performance of the company:................................................................................5

Financial position analysis of the company:................................................................................9

Cash flow position of the company:..........................................................................................15

Qualitative analysis:...................................................................................................................19

Observation:...................................................................................................................................22

Conclusion.....................................................................................................................................23

References:....................................................................................................................................24

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CREDIT ANALYSIS AND LENDING MANAGEMENT

Introduction:

Maxis Communications is a communication service provider in Malaysia is looking to expand its

business operations by expanding its infrastructure and facilities. As per the initial estimate the

management expects that approximately RM50.0 million funds will be necessary to materialize

the expansion plan of the company. The expansion strategy of the company includes expanding

its infrastructure and facilities in different parts of Malaysia including Kuala Lumpur. A closer

look at its financial statements over the years shall be helpful in assessing its financial

performance and position to assess the capacity of the company to borrow the required amount

of RM50.0 million from banks or any other financial institutions. A bank or a financial

institution would firstly conduct a thorough investigation on the affairs of the company to assess

and evaluate its financial position to determine whether the company fulfills the qualitative and

quantitative criterions to determine eligibility of the bank to get the loan (Bijak, Thomas &

Mues, 2018). A detailed discussion on the financial performance and position of the company

with the help of financial statements shall help us to determine whether the company is eligible

for the required amount of loan to materialize its expansion strategy.

About the company:

Maxis Communications also known as Maxis Berhad is one of the largest communication

service providers in the Malaysia. Headquarter of the company is situated in Kuala Lumpur. The

company provides different types of services and products related to communication and

information technology to the consumers in the country. It also serves large, medium and small

business enterprises to help them conduct their communication affairs in orderly manner

(Buckley, 2018).

CREDIT ANALYSIS AND LENDING MANAGEMENT

Introduction:

Maxis Communications is a communication service provider in Malaysia is looking to expand its

business operations by expanding its infrastructure and facilities. As per the initial estimate the

management expects that approximately RM50.0 million funds will be necessary to materialize

the expansion plan of the company. The expansion strategy of the company includes expanding

its infrastructure and facilities in different parts of Malaysia including Kuala Lumpur. A closer

look at its financial statements over the years shall be helpful in assessing its financial

performance and position to assess the capacity of the company to borrow the required amount

of RM50.0 million from banks or any other financial institutions. A bank or a financial

institution would firstly conduct a thorough investigation on the affairs of the company to assess

and evaluate its financial position to determine whether the company fulfills the qualitative and

quantitative criterions to determine eligibility of the bank to get the loan (Bijak, Thomas &

Mues, 2018). A detailed discussion on the financial performance and position of the company

with the help of financial statements shall help us to determine whether the company is eligible

for the required amount of loan to materialize its expansion strategy.

About the company:

Maxis Communications also known as Maxis Berhad is one of the largest communication

service providers in the Malaysia. Headquarter of the company is situated in Kuala Lumpur. The

company provides different types of services and products related to communication and

information technology to the consumers in the country. It also serves large, medium and small

business enterprises to help them conduct their communication affairs in orderly manner

(Buckley, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CREDIT ANALYSIS AND LENDING MANAGEMENT

Loan requirement and the objective of application for loan:

As already discussed that the company is looking to expand its facilities and infrastructure and

thus, requires RM50.0 million to finance the expansion strategy. The objective of the company is

to improve its standing in the market further and emerge as one of the large communication

service providers in Asia (Travaglini, 2018).

Evaluation of company’s capacity to borrow the required funds:

As already pointed out at the beginning of the document that an entity primarily has two sources,

i.e. internal and external sources to generate required amount of fund necessary to finance an

expansion of strategy. As the internal sources is out of question and the company has decided to

apply for a loan of RM50.0 million it is up-to the bank to decide whether to approve the

application for the loan of RM50.0 million or not. In order to decide on the fate of the loan

application of Maxis Communications the bank would evaluate the capacity of the company to

borrow and repay the installments for such loan amount on or before the due time. Accordingly,

let us proceed towards evaluating the capacity of the applicant to borrow necessary funds for its

expansion (Doorasamy, 2016).

Quantitative analysis:

Quantitate analysis include evaluating the financial performance and position of the company

over the last five or more years to determine whether the company has the capacity to generate

necessary revenue to repay the loan installments without any failure. Only after quantitative

analysis of the company any bank can decide whether to accept or reject the loan application of

the company. Accordingly, let us proceed towards evaluation of financial performance and

position of the company by using its financial statements (GEORGIEV, 2017).

CREDIT ANALYSIS AND LENDING MANAGEMENT

Loan requirement and the objective of application for loan:

As already discussed that the company is looking to expand its facilities and infrastructure and

thus, requires RM50.0 million to finance the expansion strategy. The objective of the company is

to improve its standing in the market further and emerge as one of the large communication

service providers in Asia (Travaglini, 2018).

Evaluation of company’s capacity to borrow the required funds:

As already pointed out at the beginning of the document that an entity primarily has two sources,

i.e. internal and external sources to generate required amount of fund necessary to finance an

expansion of strategy. As the internal sources is out of question and the company has decided to

apply for a loan of RM50.0 million it is up-to the bank to decide whether to approve the

application for the loan of RM50.0 million or not. In order to decide on the fate of the loan

application of Maxis Communications the bank would evaluate the capacity of the company to

borrow and repay the installments for such loan amount on or before the due time. Accordingly,

let us proceed towards evaluating the capacity of the applicant to borrow necessary funds for its

expansion (Doorasamy, 2016).

Quantitative analysis:

Quantitate analysis include evaluating the financial performance and position of the company

over the last five or more years to determine whether the company has the capacity to generate

necessary revenue to repay the loan installments without any failure. Only after quantitative

analysis of the company any bank can decide whether to accept or reject the loan application of

the company. Accordingly, let us proceed towards evaluation of financial performance and

position of the company by using its financial statements (GEORGIEV, 2017).

5

CREDIT ANALYSIS AND LENDING MANAGEMENT

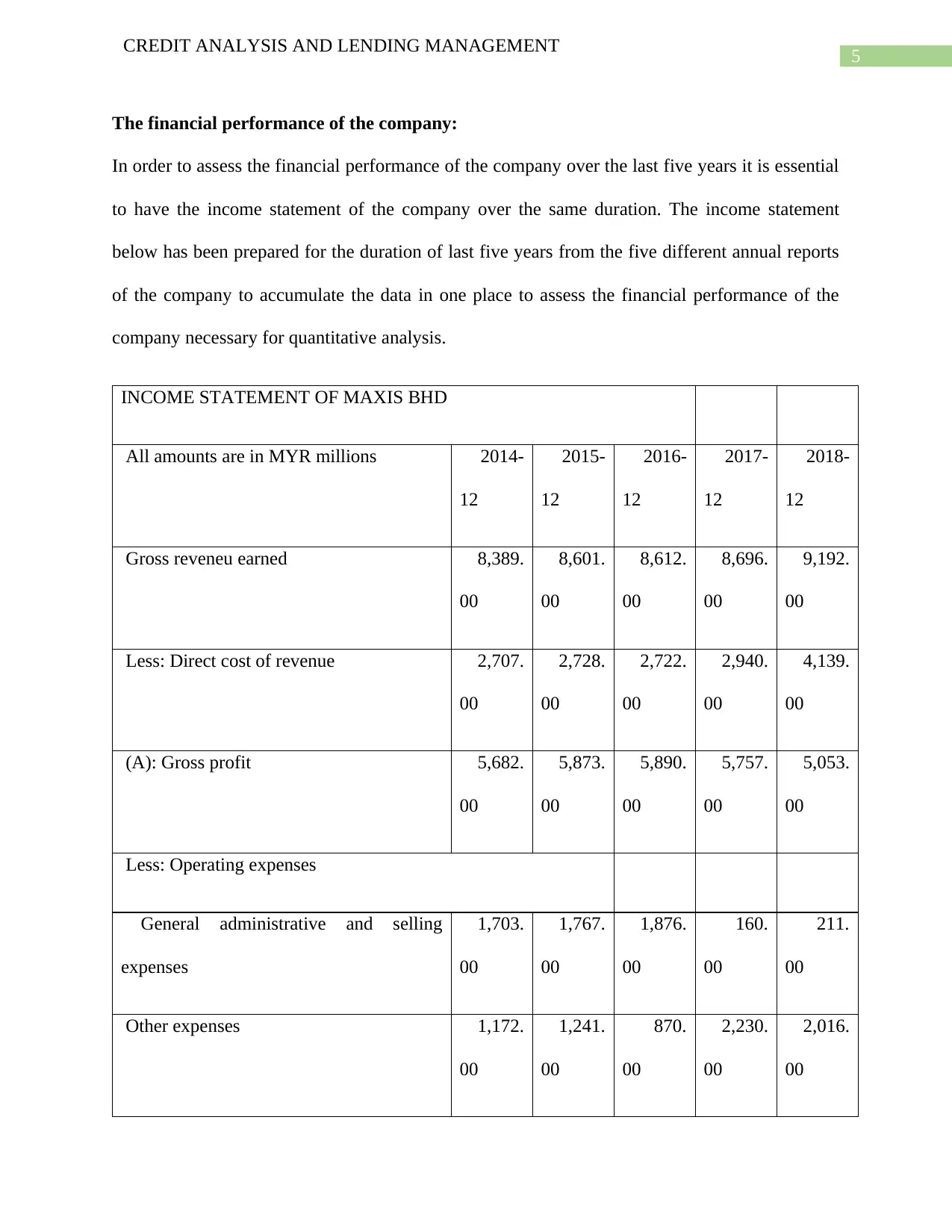

The financial performance of the company:

In order to assess the financial performance of the company over the last five years it is essential

to have the income statement of the company over the same duration. The income statement

below has been prepared for the duration of last five years from the five different annual reports

of the company to accumulate the data in one place to assess the financial performance of the

company necessary for quantitative analysis.

INCOME STATEMENT OF MAXIS BHD

All amounts are in MYR millions 2014-

12

2015-

12

2016-

12

2017-

12

2018-

12

Gross reveneu earned 8,389.

00

8,601.

00

8,612.

00

8,696.

00

9,192.

00

Less: Direct cost of revenue 2,707.

00

2,728.

00

2,722.

00

2,940.

00

4,139.

00

(A): Gross profit 5,682.

00

5,873.

00

5,890.

00

5,757.

00

5,053.

00

Less: Operating expenses

General administrative and selling

expenses

1,703.

00

1,767.

00

1,876.

00

160.

00

211.

00

Other expenses 1,172.

00

1,241.

00

870.

00

2,230.

00

2,016.

00

CREDIT ANALYSIS AND LENDING MANAGEMENT

The financial performance of the company:

In order to assess the financial performance of the company over the last five years it is essential

to have the income statement of the company over the same duration. The income statement

below has been prepared for the duration of last five years from the five different annual reports

of the company to accumulate the data in one place to assess the financial performance of the

company necessary for quantitative analysis.

INCOME STATEMENT OF MAXIS BHD

All amounts are in MYR millions 2014-

12

2015-

12

2016-

12

2017-

12

2018-

12

Gross reveneu earned 8,389.

00

8,601.

00

8,612.

00

8,696.

00

9,192.

00

Less: Direct cost of revenue 2,707.

00

2,728.

00

2,722.

00

2,940.

00

4,139.

00

(A): Gross profit 5,682.

00

5,873.

00

5,890.

00

5,757.

00

5,053.

00

Less: Operating expenses

General administrative and selling

expenses

1,703.

00

1,767.

00

1,876.

00

160.

00

211.

00

Other expenses 1,172.

00

1,241.

00

870.

00

2,230.

00

2,016.

00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

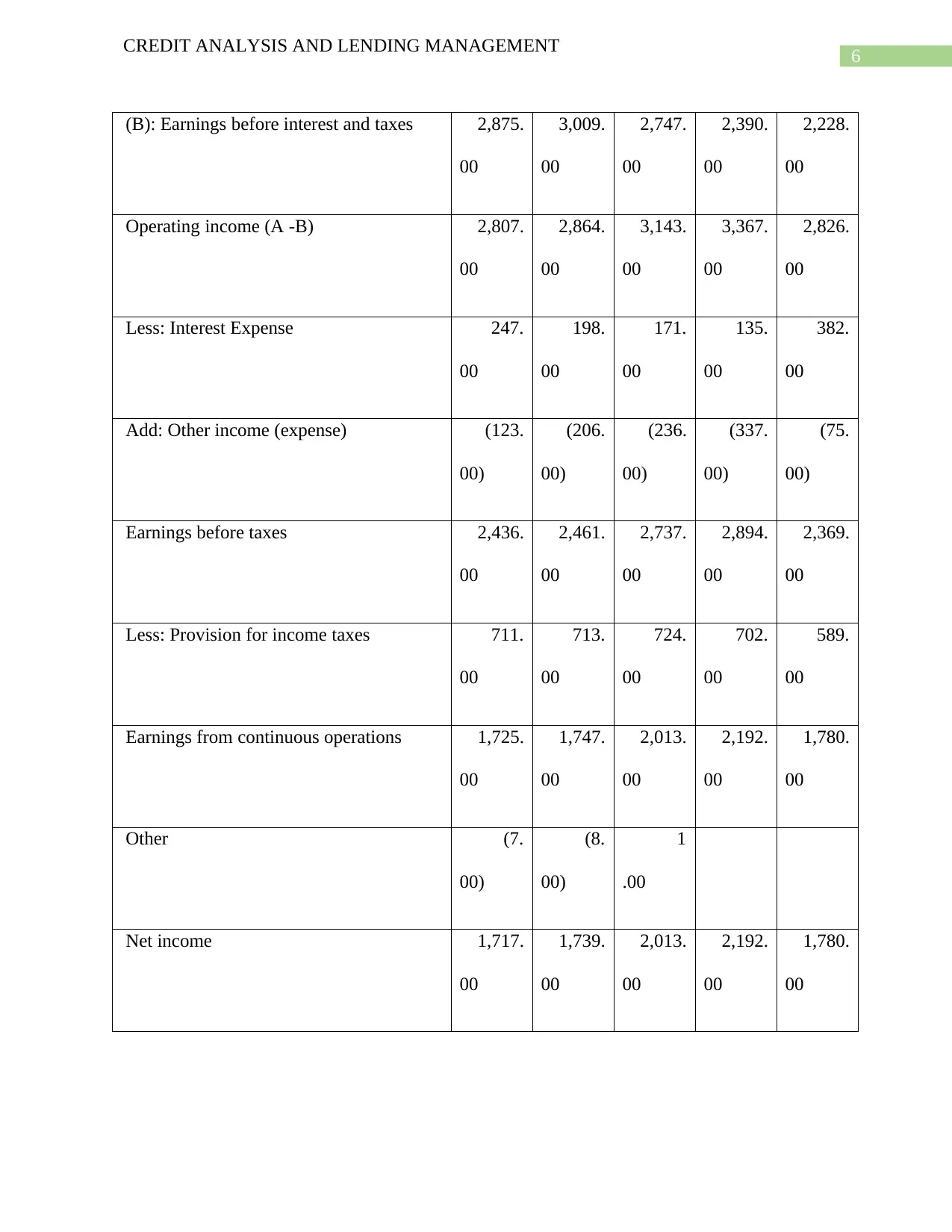

CREDIT ANALYSIS AND LENDING MANAGEMENT

(B): Earnings before interest and taxes 2,875.

00

3,009.

00

2,747.

00

2,390.

00

2,228.

00

Operating income (A -B) 2,807.

00

2,864.

00

3,143.

00

3,367.

00

2,826.

00

Less: Interest Expense 247.

00

198.

00

171.

00

135.

00

382.

00

Add: Other income (expense) (123.

00)

(206.

00)

(236.

00)

(337.

00)

(75.

00)

Earnings before taxes 2,436.

00

2,461.

00

2,737.

00

2,894.

00

2,369.

00

Less: Provision for income taxes 711.

00

713.

00

724.

00

702.

00

589.

00

Earnings from continuous operations 1,725.

00

1,747.

00

2,013.

00

2,192.

00

1,780.

00

Other (7.

00)

(8.

00)

1

.00

Net income 1,717.

00

1,739.

00

2,013.

00

2,192.

00

1,780.

00

CREDIT ANALYSIS AND LENDING MANAGEMENT

(B): Earnings before interest and taxes 2,875.

00

3,009.

00

2,747.

00

2,390.

00

2,228.

00

Operating income (A -B) 2,807.

00

2,864.

00

3,143.

00

3,367.

00

2,826.

00

Less: Interest Expense 247.

00

198.

00

171.

00

135.

00

382.

00

Add: Other income (expense) (123.

00)

(206.

00)

(236.

00)

(337.

00)

(75.

00)

Earnings before taxes 2,436.

00

2,461.

00

2,737.

00

2,894.

00

2,369.

00

Less: Provision for income taxes 711.

00

713.

00

724.

00

702.

00

589.

00

Earnings from continuous operations 1,725.

00

1,747.

00

2,013.

00

2,192.

00

1,780.

00

Other (7.

00)

(8.

00)

1

.00

Net income 1,717.

00

1,739.

00

2,013.

00

2,192.

00

1,780.

00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

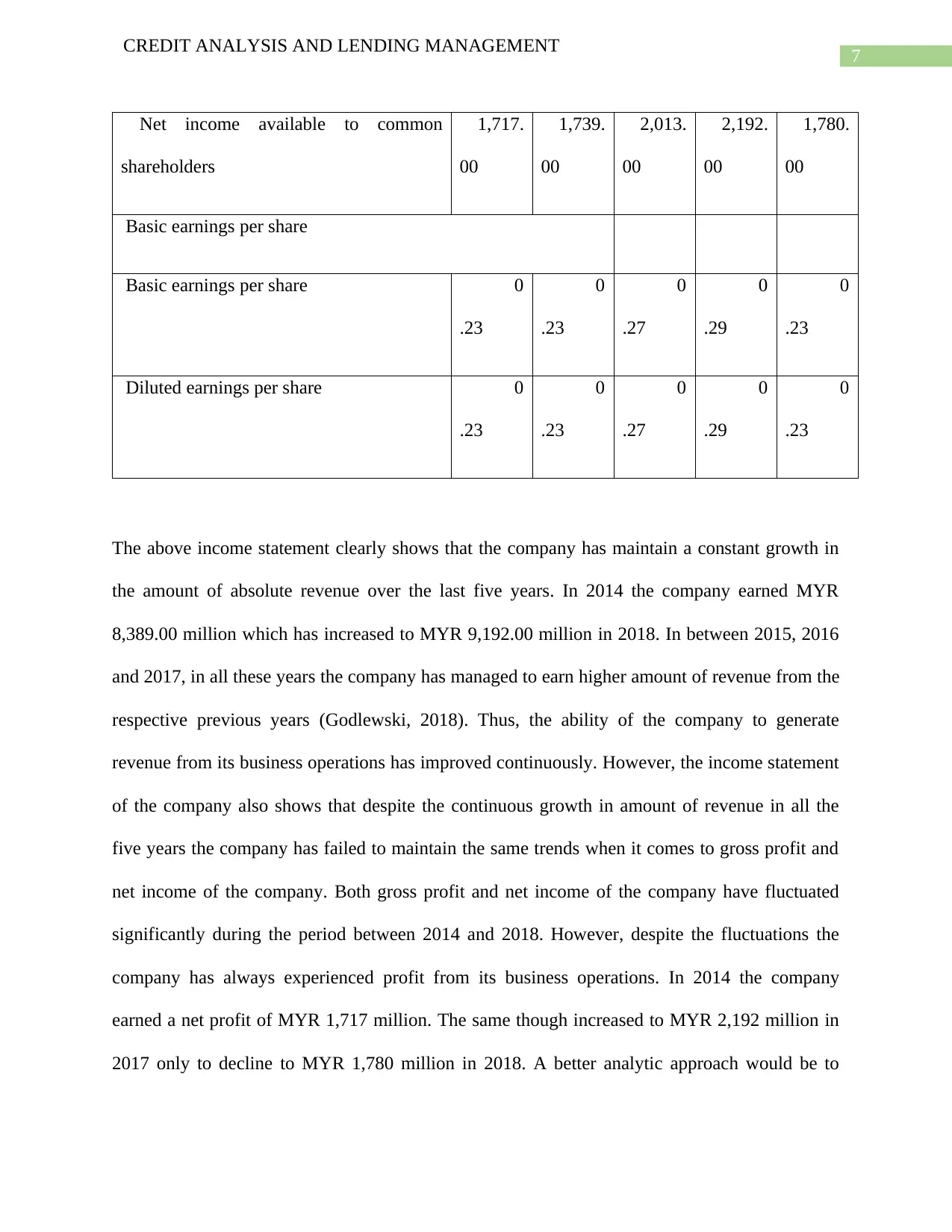

CREDIT ANALYSIS AND LENDING MANAGEMENT

Net income available to common

shareholders

1,717.

00

1,739.

00

2,013.

00

2,192.

00

1,780.

00

Basic earnings per share

Basic earnings per share 0

.23

0

.23

0

.27

0

.29

0

.23

Diluted earnings per share 0

.23

0

.23

0

.27

0

.29

0

.23

The above income statement clearly shows that the company has maintain a constant growth in

the amount of absolute revenue over the last five years. In 2014 the company earned MYR

8,389.00 million which has increased to MYR 9,192.00 million in 2018. In between 2015, 2016

and 2017, in all these years the company has managed to earn higher amount of revenue from the

respective previous years (Godlewski, 2018). Thus, the ability of the company to generate

revenue from its business operations has improved continuously. However, the income statement

of the company also shows that despite the continuous growth in amount of revenue in all the

five years the company has failed to maintain the same trends when it comes to gross profit and

net income of the company. Both gross profit and net income of the company have fluctuated

significantly during the period between 2014 and 2018. However, despite the fluctuations the

company has always experienced profit from its business operations. In 2014 the company

earned a net profit of MYR 1,717 million. The same though increased to MYR 2,192 million in

2017 only to decline to MYR 1,780 million in 2018. A better analytic approach would be to

CREDIT ANALYSIS AND LENDING MANAGEMENT

Net income available to common

shareholders

1,717.

00

1,739.

00

2,013.

00

2,192.

00

1,780.

00

Basic earnings per share

Basic earnings per share 0

.23

0

.23

0

.27

0

.29

0

.23

Diluted earnings per share 0

.23

0

.23

0

.27

0

.29

0

.23

The above income statement clearly shows that the company has maintain a constant growth in

the amount of absolute revenue over the last five years. In 2014 the company earned MYR

8,389.00 million which has increased to MYR 9,192.00 million in 2018. In between 2015, 2016

and 2017, in all these years the company has managed to earn higher amount of revenue from the

respective previous years (Godlewski, 2018). Thus, the ability of the company to generate

revenue from its business operations has improved continuously. However, the income statement

of the company also shows that despite the continuous growth in amount of revenue in all the

five years the company has failed to maintain the same trends when it comes to gross profit and

net income of the company. Both gross profit and net income of the company have fluctuated

significantly during the period between 2014 and 2018. However, despite the fluctuations the

company has always experienced profit from its business operations. In 2014 the company

earned a net profit of MYR 1,717 million. The same though increased to MYR 2,192 million in

2017 only to decline to MYR 1,780 million in 2018. A better analytic approach would be to

8

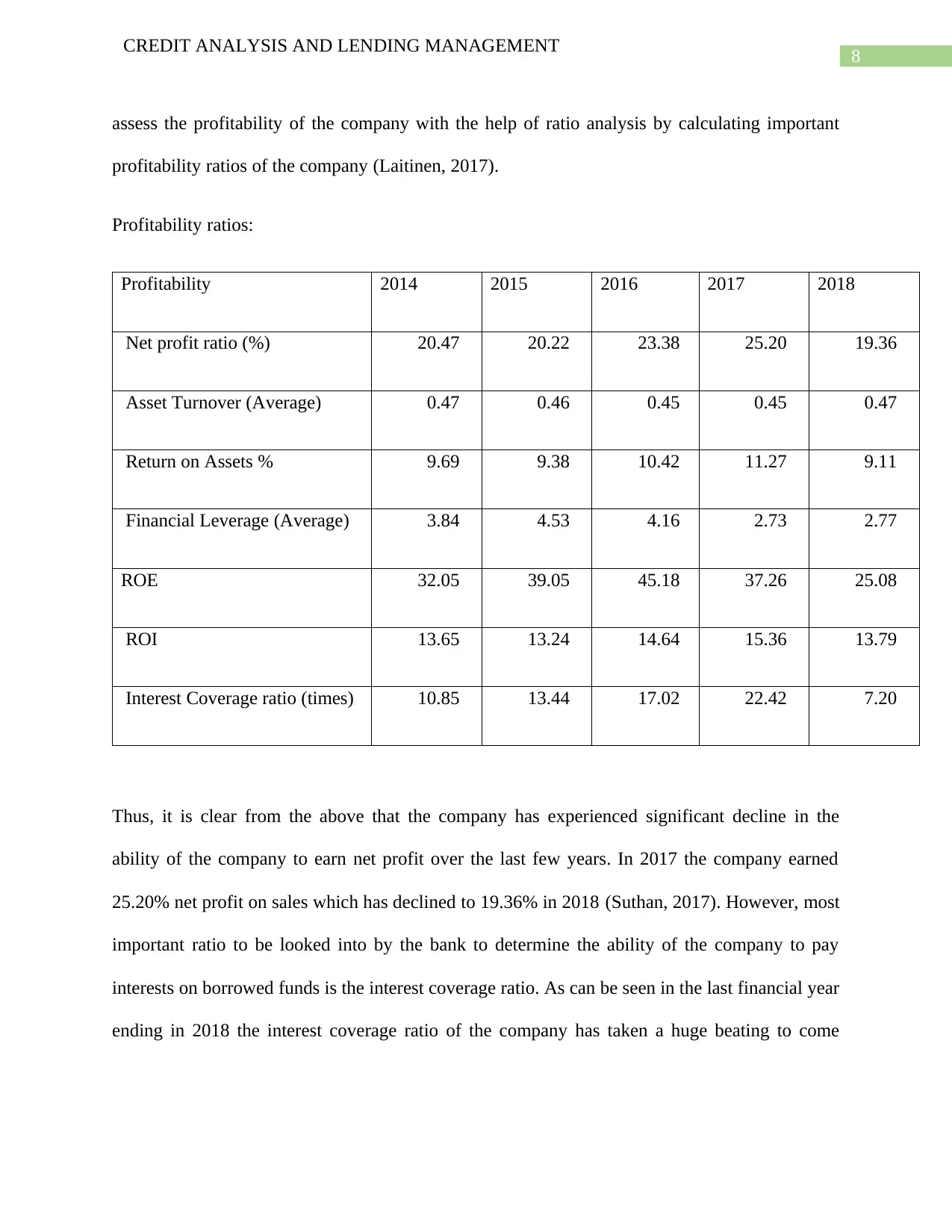

CREDIT ANALYSIS AND LENDING MANAGEMENT

assess the profitability of the company with the help of ratio analysis by calculating important

profitability ratios of the company (Laitinen, 2017).

Profitability ratios:

Profitability 2014 2015 2016 2017 2018

Net profit ratio (%) 20.47 20.22 23.38 25.20 19.36

Asset Turnover (Average) 0.47 0.46 0.45 0.45 0.47

Return on Assets % 9.69 9.38 10.42 11.27 9.11

Financial Leverage (Average) 3.84 4.53 4.16 2.73 2.77

ROE 32.05 39.05 45.18 37.26 25.08

ROI 13.65 13.24 14.64 15.36 13.79

Interest Coverage ratio (times) 10.85 13.44 17.02 22.42 7.20

Thus, it is clear from the above that the company has experienced significant decline in the

ability of the company to earn net profit over the last few years. In 2017 the company earned

25.20% net profit on sales which has declined to 19.36% in 2018 (Suthan, 2017). However, most

important ratio to be looked into by the bank to determine the ability of the company to pay

interests on borrowed funds is the interest coverage ratio. As can be seen in the last financial year

ending in 2018 the interest coverage ratio of the company has taken a huge beating to come

CREDIT ANALYSIS AND LENDING MANAGEMENT

assess the profitability of the company with the help of ratio analysis by calculating important

profitability ratios of the company (Laitinen, 2017).

Profitability ratios:

Profitability 2014 2015 2016 2017 2018

Net profit ratio (%) 20.47 20.22 23.38 25.20 19.36

Asset Turnover (Average) 0.47 0.46 0.45 0.45 0.47

Return on Assets % 9.69 9.38 10.42 11.27 9.11

Financial Leverage (Average) 3.84 4.53 4.16 2.73 2.77

ROE 32.05 39.05 45.18 37.26 25.08

ROI 13.65 13.24 14.64 15.36 13.79

Interest Coverage ratio (times) 10.85 13.44 17.02 22.42 7.20

Thus, it is clear from the above that the company has experienced significant decline in the

ability of the company to earn net profit over the last few years. In 2017 the company earned

25.20% net profit on sales which has declined to 19.36% in 2018 (Suthan, 2017). However, most

important ratio to be looked into by the bank to determine the ability of the company to pay

interests on borrowed funds is the interest coverage ratio. As can be seen in the last financial year

ending in 2018 the interest coverage ratio of the company has taken a huge beating to come

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CREDIT ANALYSIS AND LENDING MANAGEMENT

down to 7.20 times from 22.42 in 2017. Thus, it is clear that the company’s ability to pay interest

on borrowed funds have declined significantly (LANGREHR & LANGREHR, 2018).

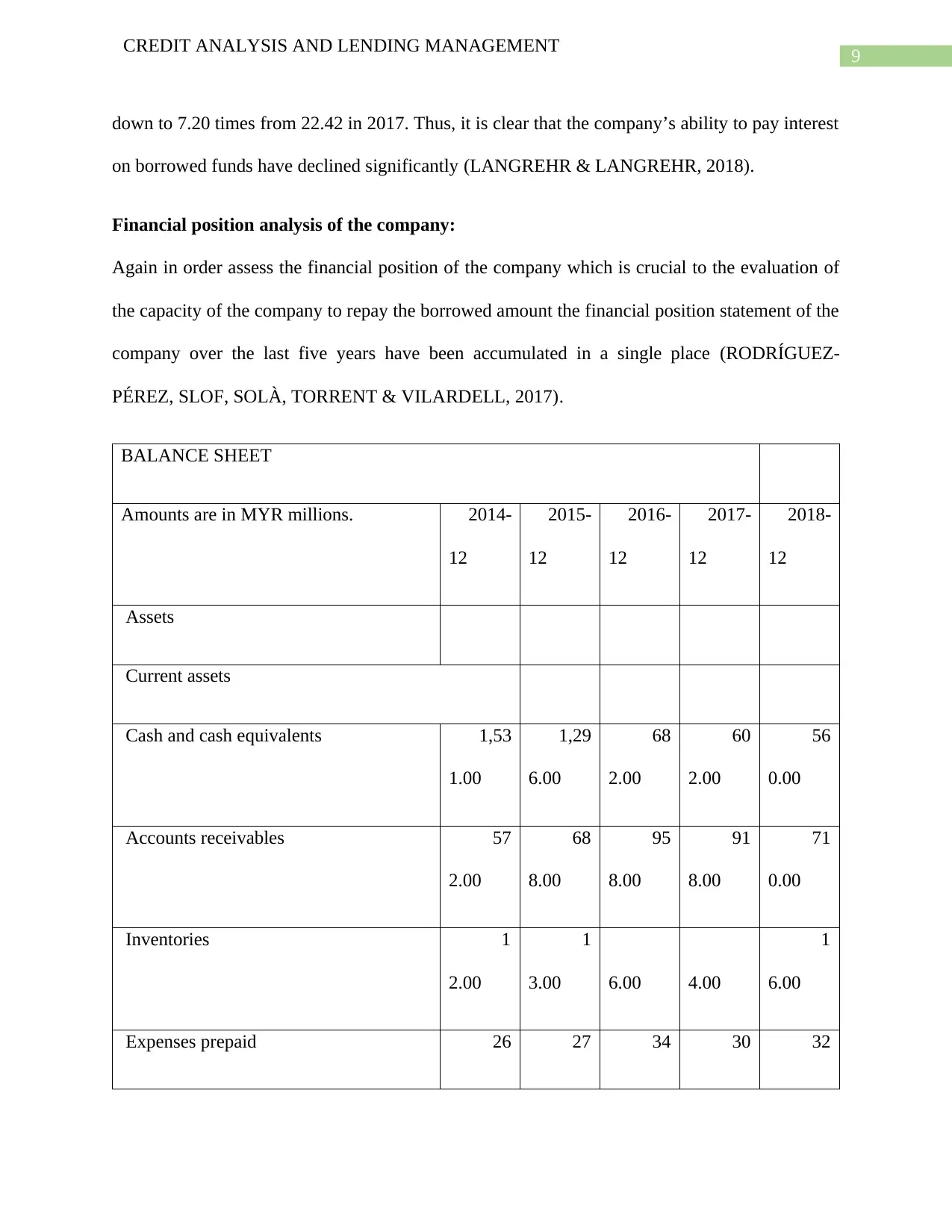

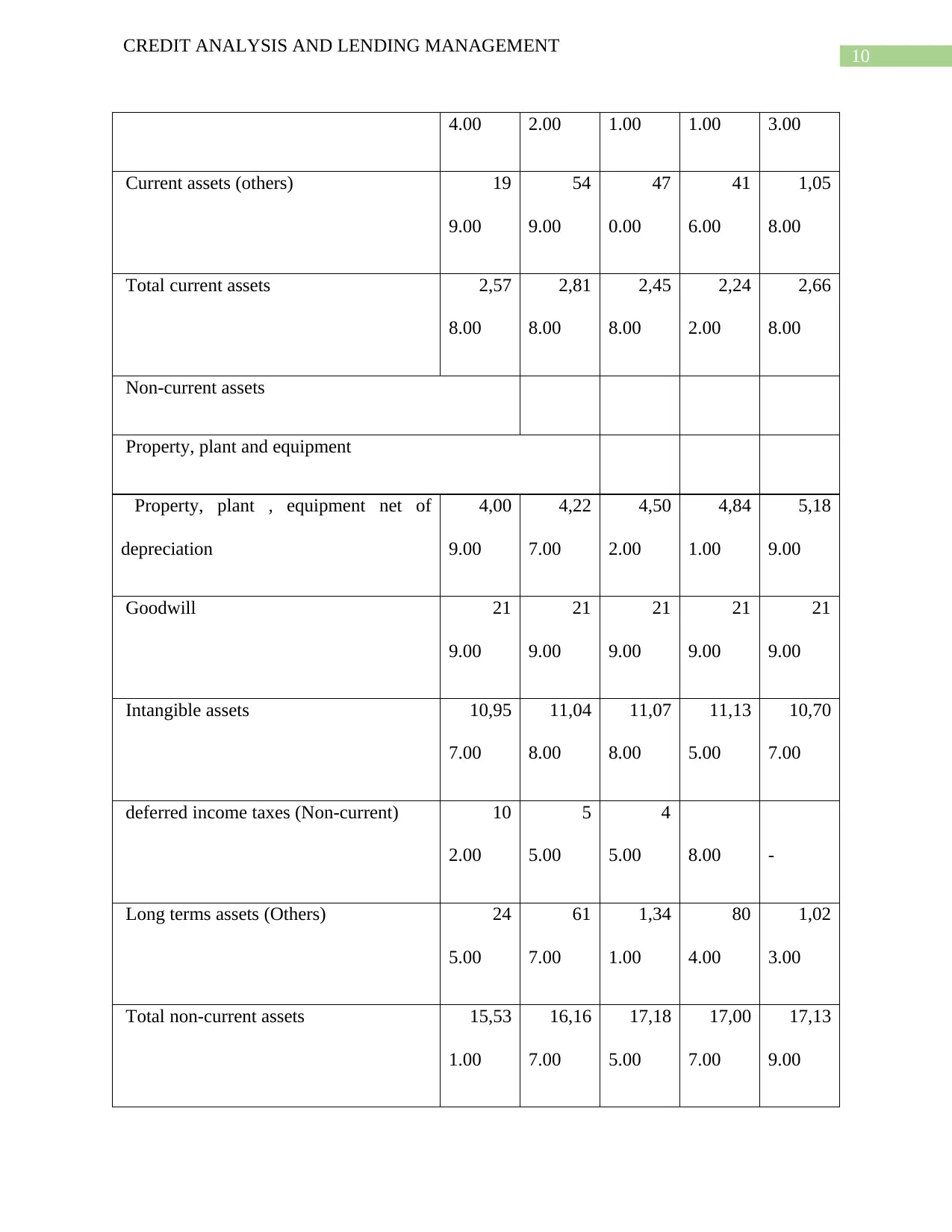

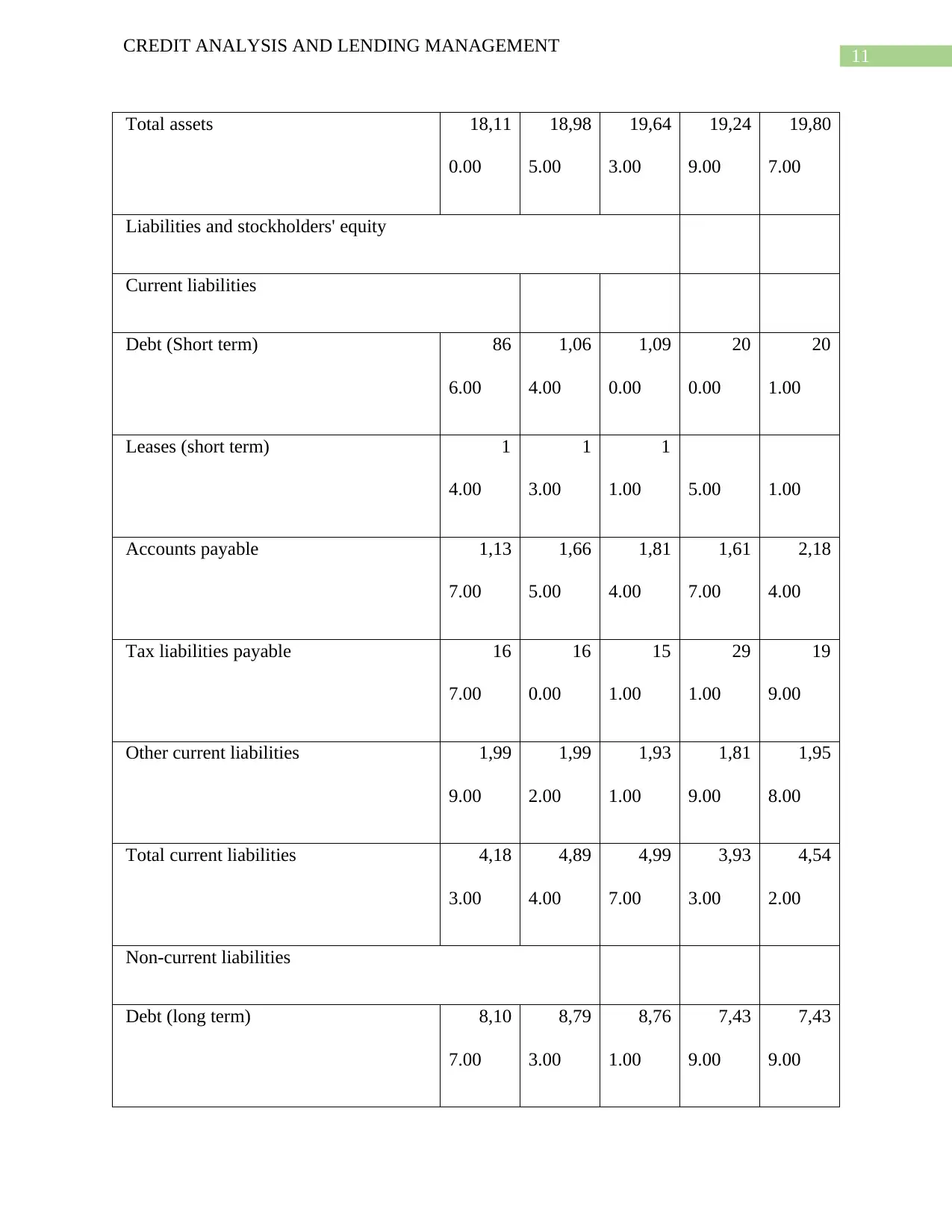

Financial position analysis of the company:

Again in order assess the financial position of the company which is crucial to the evaluation of

the capacity of the company to repay the borrowed amount the financial position statement of the

company over the last five years have been accumulated in a single place (RODRÍGUEZ-

PÉREZ, SLOF, SOLÀ, TORRENT & VILARDELL, 2017).

BALANCE SHEET

Amounts are in MYR millions. 2014-

12

2015-

12

2016-

12

2017-

12

2018-

12

Assets

Current assets

Cash and cash equivalents 1,53

1.00

1,29

6.00

68

2.00

60

2.00

56

0.00

Accounts receivables 57

2.00

68

8.00

95

8.00

91

8.00

71

0.00

Inventories 1

2.00

1

3.00 6.00 4.00

1

6.00

Expenses prepaid 26 27 34 30 32

CREDIT ANALYSIS AND LENDING MANAGEMENT

down to 7.20 times from 22.42 in 2017. Thus, it is clear that the company’s ability to pay interest

on borrowed funds have declined significantly (LANGREHR & LANGREHR, 2018).

Financial position analysis of the company:

Again in order assess the financial position of the company which is crucial to the evaluation of

the capacity of the company to repay the borrowed amount the financial position statement of the

company over the last five years have been accumulated in a single place (RODRÍGUEZ-

PÉREZ, SLOF, SOLÀ, TORRENT & VILARDELL, 2017).

BALANCE SHEET

Amounts are in MYR millions. 2014-

12

2015-

12

2016-

12

2017-

12

2018-

12

Assets

Current assets

Cash and cash equivalents 1,53

1.00

1,29

6.00

68

2.00

60

2.00

56

0.00

Accounts receivables 57

2.00

68

8.00

95

8.00

91

8.00

71

0.00

Inventories 1

2.00

1

3.00 6.00 4.00

1

6.00

Expenses prepaid 26 27 34 30 32

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CREDIT ANALYSIS AND LENDING MANAGEMENT

4.00 2.00 1.00 1.00 3.00

Current assets (others) 19

9.00

54

9.00

47

0.00

41

6.00

1,05

8.00

Total current assets 2,57

8.00

2,81

8.00

2,45

8.00

2,24

2.00

2,66

8.00

Non-current assets

Property, plant and equipment

Property, plant , equipment net of

depreciation

4,00

9.00

4,22

7.00

4,50

2.00

4,84

1.00

5,18

9.00

Goodwill 21

9.00

21

9.00

21

9.00

21

9.00

21

9.00

Intangible assets 10,95

7.00

11,04

8.00

11,07

8.00

11,13

5.00

10,70

7.00

deferred income taxes (Non-current) 10

2.00

5

5.00

4

5.00 8.00 -

Long terms assets (Others) 24

5.00

61

7.00

1,34

1.00

80

4.00

1,02

3.00

Total non-current assets 15,53

1.00

16,16

7.00

17,18

5.00

17,00

7.00

17,13

9.00

CREDIT ANALYSIS AND LENDING MANAGEMENT

4.00 2.00 1.00 1.00 3.00

Current assets (others) 19

9.00

54

9.00

47

0.00

41

6.00

1,05

8.00

Total current assets 2,57

8.00

2,81

8.00

2,45

8.00

2,24

2.00

2,66

8.00

Non-current assets

Property, plant and equipment

Property, plant , equipment net of

depreciation

4,00

9.00

4,22

7.00

4,50

2.00

4,84

1.00

5,18

9.00

Goodwill 21

9.00

21

9.00

21

9.00

21

9.00

21

9.00

Intangible assets 10,95

7.00

11,04

8.00

11,07

8.00

11,13

5.00

10,70

7.00

deferred income taxes (Non-current) 10

2.00

5

5.00

4

5.00 8.00 -

Long terms assets (Others) 24

5.00

61

7.00

1,34

1.00

80

4.00

1,02

3.00

Total non-current assets 15,53

1.00

16,16

7.00

17,18

5.00

17,00

7.00

17,13

9.00

11

CREDIT ANALYSIS AND LENDING MANAGEMENT

Total assets 18,11

0.00

18,98

5.00

19,64

3.00

19,24

9.00

19,80

7.00

Liabilities and stockholders' equity

Current liabilities

Debt (Short term) 86

6.00

1,06

4.00

1,09

0.00

20

0.00

20

1.00

Leases (short term) 1

4.00

1

3.00

1

1.00 5.00 1.00

Accounts payable 1,13

7.00

1,66

5.00

1,81

4.00

1,61

7.00

2,18

4.00

Tax liabilities payable 16

7.00

16

0.00

15

1.00

29

1.00

19

9.00

Other current liabilities 1,99

9.00

1,99

2.00

1,93

1.00

1,81

9.00

1,95

8.00

Total current liabilities 4,18

3.00

4,89

4.00

4,99

7.00

3,93

3.00

4,54

2.00

Non-current liabilities

Debt (long term) 8,10

7.00

8,79

3.00

8,76

1.00

7,43

9.00

7,43

9.00

CREDIT ANALYSIS AND LENDING MANAGEMENT

Total assets 18,11

0.00

18,98

5.00

19,64

3.00

19,24

9.00

19,80

7.00

Liabilities and stockholders' equity

Current liabilities

Debt (Short term) 86

6.00

1,06

4.00

1,09

0.00

20

0.00

20

1.00

Leases (short term) 1

4.00

1

3.00

1

1.00 5.00 1.00

Accounts payable 1,13

7.00

1,66

5.00

1,81

4.00

1,61

7.00

2,18

4.00

Tax liabilities payable 16

7.00

16

0.00

15

1.00

29

1.00

19

9.00

Other current liabilities 1,99

9.00

1,99

2.00

1,93

1.00

1,81

9.00

1,95

8.00

Total current liabilities 4,18

3.00

4,89

4.00

4,99

7.00

3,93

3.00

4,54

2.00

Non-current liabilities

Debt (long term) 8,10

7.00

8,79

3.00

8,76

1.00

7,43

9.00

7,43

9.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.