Loan Amount Involvement Risk Analysis

VerifiedAdded on 2020/10/22

|13

|3121

|239

AI Summary

The provided report analyzes the risk associated with a loan amount of 30,000,000 for a project valued at 41,000,000. The analysis indicates that almost 70% of the project's establishment cost is being funded by the loan, which may not be a good indication for the bank. The report also suggests that if the same loan amount were applied to the construction firm, the bank should apply strict regulation and monitoring policies to evaluate the construction project.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

CREDIT AND LENDING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

QUESTION 2...................................................................................................................................3

QUESTION 3...................................................................................................................................4

QUESTION 4...................................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

QUESTION 2...................................................................................................................................3

QUESTION 3...................................................................................................................................4

QUESTION 4...................................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION

Credit means to give purchase things at present at pay the price at some future date. In

context of the banking regulation it is defined as to lend money to the parties or client of the

bank after taking into some securities and deposited against that money landed. In the present

report a bank is being advised on whether it should land a loan of $30,000,000 to a construction

company for building a five star hotel near a beach. Detailed report is presented on inherited risk

related with the risk and recommendations are also provided to the bank for the extent of

financial involvement in the proposed project.

QUESTION 1

Background

This paper is presented for fulfilling requirements of the MBA (Chartered Banker)

program Bangor Business School, University of Bangor, UK. The scope of study is to answer

four questions presented in module.

Methodology-

The project is completed by taking into account all the relevant magazines, study packs,

text books, journals and related reliable sources.

CREDIT MEMORANDUM

To: Management Credit Committee

From: Relationship Manager

Date: 12th December 2018

Subject: In Approval for lending loan

Introduction

Loan syndication is to be provided regarding secured construction

loan totalling $30,000,000 for constructing five-star luxury hotel at a beach area distance within

15 minutes ravelling time from Nassau (Bluhm, Overbeck and Wagner, 2016). Cable Beach

Hotel is to be constructed and developer will be local firm Consultancy (PVT) Limited hired on

contract basis. This means that loan will be sanctioned in accordance to performance of

company.

Character and Ability

1

Credit means to give purchase things at present at pay the price at some future date. In

context of the banking regulation it is defined as to lend money to the parties or client of the

bank after taking into some securities and deposited against that money landed. In the present

report a bank is being advised on whether it should land a loan of $30,000,000 to a construction

company for building a five star hotel near a beach. Detailed report is presented on inherited risk

related with the risk and recommendations are also provided to the bank for the extent of

financial involvement in the proposed project.

QUESTION 1

Background

This paper is presented for fulfilling requirements of the MBA (Chartered Banker)

program Bangor Business School, University of Bangor, UK. The scope of study is to answer

four questions presented in module.

Methodology-

The project is completed by taking into account all the relevant magazines, study packs,

text books, journals and related reliable sources.

CREDIT MEMORANDUM

To: Management Credit Committee

From: Relationship Manager

Date: 12th December 2018

Subject: In Approval for lending loan

Introduction

Loan syndication is to be provided regarding secured construction

loan totalling $30,000,000 for constructing five-star luxury hotel at a beach area distance within

15 minutes ravelling time from Nassau (Bluhm, Overbeck and Wagner, 2016). Cable Beach

Hotel is to be constructed and developer will be local firm Consultancy (PVT) Limited hired on

contract basis. This means that loan will be sanctioned in accordance to performance of

company.

Character and Ability

1

The firm is prestigious architects in Nassau and investigation regarding loan is to be

provided whether bank should approve loan or not. The competitive advantage of firm is high

standards and quality of work. The active involvement of developer would be required so as to

develop loan amount in effectual manner.

Purpose and Amount

Main purpose of company is to construct project comprising 253 bed, five-star hotel

located on the beach in effective manner which will enhance customer satisfaction. The

developer has been granted lease to a land by the government (Ongena, Schindele and Vonnák,

2017). The initial rent is $8,560 in the first year, rising to $15,360 in the twentieth year. The

developer has identified good demand of luxury class resort-based hotel and is dominated by 62

% of US travellers. For accomplishing this, amount of loan $30,000,000 is needed. The

financials of company reveals that hotel will have good growth rate. This is evident from the fact

that total revenue will be 17568 in 2019, increased to 21622 in 2020. Followed by it, figure will

reach 22065 in next year and further maximise to 25510 in 2022, The sales will also elevate in

2023 to 29378 and 30931 in next period and will reach to 32389 in 2025. The net income is

steady but it would be difficult bank to provide loan amount as higher construction cost will be

required which will be approximately $41,000,000 purely for construction of Cable Beach Hotel.

Repayment Capacity

The bank facilities are to be served through the operating income. The Debt Service

Coverage ratio of the firm is on an average more than 1.20 and will reach to 1.92 at the end of

2025. Sales are gone up but profitability has not much increased as operating expenses are

incurred in higher manner. Moreover, liquidity position is moderate of firm.

Securities

Bank has different security options and most appropriate one will be chosen when final

approval will be met out (Cingano, Manares and Sette, 2016). It can be analysed that securities

are to be mortgaged so that bank safety may be carried out in a better manner. This will provide

bank with higher safety and in case of default of loan, bank can sell-off mortgaged assets for

recovering amount in the best manner possible. Movable and immovable assets both could be

chosen for supporting the collateral and as a result, security can be attained in a better manner.

2

provided whether bank should approve loan or not. The competitive advantage of firm is high

standards and quality of work. The active involvement of developer would be required so as to

develop loan amount in effectual manner.

Purpose and Amount

Main purpose of company is to construct project comprising 253 bed, five-star hotel

located on the beach in effective manner which will enhance customer satisfaction. The

developer has been granted lease to a land by the government (Ongena, Schindele and Vonnák,

2017). The initial rent is $8,560 in the first year, rising to $15,360 in the twentieth year. The

developer has identified good demand of luxury class resort-based hotel and is dominated by 62

% of US travellers. For accomplishing this, amount of loan $30,000,000 is needed. The

financials of company reveals that hotel will have good growth rate. This is evident from the fact

that total revenue will be 17568 in 2019, increased to 21622 in 2020. Followed by it, figure will

reach 22065 in next year and further maximise to 25510 in 2022, The sales will also elevate in

2023 to 29378 and 30931 in next period and will reach to 32389 in 2025. The net income is

steady but it would be difficult bank to provide loan amount as higher construction cost will be

required which will be approximately $41,000,000 purely for construction of Cable Beach Hotel.

Repayment Capacity

The bank facilities are to be served through the operating income. The Debt Service

Coverage ratio of the firm is on an average more than 1.20 and will reach to 1.92 at the end of

2025. Sales are gone up but profitability has not much increased as operating expenses are

incurred in higher manner. Moreover, liquidity position is moderate of firm.

Securities

Bank has different security options and most appropriate one will be chosen when final

approval will be met out (Cingano, Manares and Sette, 2016). It can be analysed that securities

are to be mortgaged so that bank safety may be carried out in a better manner. This will provide

bank with higher safety and in case of default of loan, bank can sell-off mortgaged assets for

recovering amount in the best manner possible. Movable and immovable assets both could be

chosen for supporting the collateral and as a result, security can be attained in a better manner.

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Recommendation and Approval

The recommendation and principle approval can be made in view of;

Business Reputation and growing sales revenue

Adequate financials

Owners commitment New lending opportunity

Subject to;

Visiting customer Obtaining full details and submitting proposal for final approval

Revenue and Sales Turnover-

The sales revenue is growing at a rapid rate indicating ability of demand for architectural

services and attaining success of enterprise in effective manner. Good business strategies are

adapted by firm in meeting industry challenges.

Profitability-

The profitability of company is steady and is not growing at a rapid rate. This could be

due to economic downturn in the country and increasing competition. Moreover, due to increase

in operating and non-operating expenses, profits are not increased (di Patti and Sette, 2016).

Leverage and gearing-

The Debt Service Coverage ratio should be high showing that firm may be able to attain

loan from the bank as it shows ability of firm in making debt payments in a better manner

(Faleye and Krishnan, 2017). The ratio is increased and average is more than 1.20.

QUESTION 2

a.) For banks, lending covenants are the essential part which is included in loan agreement

documents. Before, sanctioning loan banks will negotiate covenants with borrower which is

known as permanent agreement for the bank where both the parties' lender and borrower tie up in

an agreement in which expectation is followed regarding risk for repayment period. Covenants

3

The recommendation and principle approval can be made in view of;

Business Reputation and growing sales revenue

Adequate financials

Owners commitment New lending opportunity

Subject to;

Visiting customer Obtaining full details and submitting proposal for final approval

Revenue and Sales Turnover-

The sales revenue is growing at a rapid rate indicating ability of demand for architectural

services and attaining success of enterprise in effective manner. Good business strategies are

adapted by firm in meeting industry challenges.

Profitability-

The profitability of company is steady and is not growing at a rapid rate. This could be

due to economic downturn in the country and increasing competition. Moreover, due to increase

in operating and non-operating expenses, profits are not increased (di Patti and Sette, 2016).

Leverage and gearing-

The Debt Service Coverage ratio should be high showing that firm may be able to attain

loan from the bank as it shows ability of firm in making debt payments in a better manner

(Faleye and Krishnan, 2017). The ratio is increased and average is more than 1.20.

QUESTION 2

a.) For banks, lending covenants are the essential part which is included in loan agreement

documents. Before, sanctioning loan banks will negotiate covenants with borrower which is

known as permanent agreement for the bank where both the parties' lender and borrower tie up in

an agreement in which expectation is followed regarding risk for repayment period. Covenants

3

are of two types that is financial and non financial (Immergluck, 2016). In financial agreement,

customer is abided to follow certain financial measures which may be positive or negative.

b.) To cover financial needs through operating cycle of company an overdraft is provided. This

overdraft is helpful for company to meet short term finance needs of the company. When both

the credit and debit side of the overdraft matched perfectly, it measures that overall business

operations of the company are running smoothly. But unbalance overdraft has occurred with

measurement then it measures that company has having problems in developing effective

business operation. This problems may be of liquidity due which is due to bad collection method,

accumulating stocks or operational losses (Aiyar, Calomiris and Wieladek, 2016).

c.) Liquidation is the process adopted by limited liability companies to wind up their business

operation in business market. To wind up process there are both options for companies that

compulsory or voluntary. Following powers are provided to liquidator to start winding up

process of companies which are as follows-

Liquidator will able to sale any property of the company.

Liquidator will also able to prove financial position of the company that bankruptcy, insolvency

or any contributory.

Has power to appoint agent in business organisation to carry functions with him.

d.) For affairs of company, administrator has been appointed by the court (Chen, Hanson and

Stein, 2017). He is known to be a agent of the company where he has to check all business

operations and has to manage and control entire business of the company.

QUESTION 3

A).

For the present case certain items that can be considered form the given facts and figures

of the project data base are:

The occupancy level of the room in the hotel for a budgeted period of 6 year have shown

a growth of 13% with a hike in the rates of the room by almost $100 which is can be

consider as a good indicator but this not reflate high growths in sales and revenues.

The raise in the operating revenues as compared to the operating expenses for a period of

6 years is propositional higher (Advanced Liquidity and Funding Risk Management,

4

customer is abided to follow certain financial measures which may be positive or negative.

b.) To cover financial needs through operating cycle of company an overdraft is provided. This

overdraft is helpful for company to meet short term finance needs of the company. When both

the credit and debit side of the overdraft matched perfectly, it measures that overall business

operations of the company are running smoothly. But unbalance overdraft has occurred with

measurement then it measures that company has having problems in developing effective

business operation. This problems may be of liquidity due which is due to bad collection method,

accumulating stocks or operational losses (Aiyar, Calomiris and Wieladek, 2016).

c.) Liquidation is the process adopted by limited liability companies to wind up their business

operation in business market. To wind up process there are both options for companies that

compulsory or voluntary. Following powers are provided to liquidator to start winding up

process of companies which are as follows-

Liquidator will able to sale any property of the company.

Liquidator will also able to prove financial position of the company that bankruptcy, insolvency

or any contributory.

Has power to appoint agent in business organisation to carry functions with him.

d.) For affairs of company, administrator has been appointed by the court (Chen, Hanson and

Stein, 2017). He is known to be a agent of the company where he has to check all business

operations and has to manage and control entire business of the company.

QUESTION 3

A).

For the present case certain items that can be considered form the given facts and figures

of the project data base are:

The occupancy level of the room in the hotel for a budgeted period of 6 year have shown

a growth of 13% with a hike in the rates of the room by almost $100 which is can be

consider as a good indicator but this not reflate high growths in sales and revenues.

The raise in the operating revenues as compared to the operating expenses for a period of

6 years is propositional higher (Advanced Liquidity and Funding Risk Management,

4

2018). This shows that with increment the profits the organization will infidelity put

effort to control the cost.

The net operating income in 2019 is expected to get doubled in 2025 which indicated

the hotel will earn a good position in the market in short span of time.

For the repayment of the loan hotel management have decides a time frame of 10 years

and for this time the bank is required to keep a close watch on the operation and accounts

of the hotel in order to ensure timely repayment of the loan without any default.

The projected budget of the hotel is depicting good indicators of growth but in spite of

this the occupancy level is not good as expected to be and this is one of the major criteria

oh hotel business, so loan must be advance after taking into consideration this factors of

growth as well.

B) The business plan is required to be made so that firm may be able to perform in accordance to

the same. Moreover, it is important when new borrowing relationship is to be build and current

status of business, set objectives can be attained. It is a useful tool for monitoring actual

performance against planned targets and make corrective action.

Key Objectives

To provide luxurious five-star hotel with various amenities for maximising satisfaction

level of customers

To attain desired sales turnover in next six months

Contact Details of key persons

Tom Harris- Hotel Manager

He posses master's degree in the hotel management and has twenty years of experience.

He has good interpersonal skills, communication and high level of managing skills.

George Rosemary- Hotel Accountant

He holds bachelor's degree in accounting and has six yeas of experience. He has good

communication skills and numeracy skills.

Business Background

5

effort to control the cost.

The net operating income in 2019 is expected to get doubled in 2025 which indicated

the hotel will earn a good position in the market in short span of time.

For the repayment of the loan hotel management have decides a time frame of 10 years

and for this time the bank is required to keep a close watch on the operation and accounts

of the hotel in order to ensure timely repayment of the loan without any default.

The projected budget of the hotel is depicting good indicators of growth but in spite of

this the occupancy level is not good as expected to be and this is one of the major criteria

oh hotel business, so loan must be advance after taking into consideration this factors of

growth as well.

B) The business plan is required to be made so that firm may be able to perform in accordance to

the same. Moreover, it is important when new borrowing relationship is to be build and current

status of business, set objectives can be attained. It is a useful tool for monitoring actual

performance against planned targets and make corrective action.

Key Objectives

To provide luxurious five-star hotel with various amenities for maximising satisfaction

level of customers

To attain desired sales turnover in next six months

Contact Details of key persons

Tom Harris- Hotel Manager

He posses master's degree in the hotel management and has twenty years of experience.

He has good interpersonal skills, communication and high level of managing skills.

George Rosemary- Hotel Accountant

He holds bachelor's degree in accounting and has six yeas of experience. He has good

communication skills and numeracy skills.

Business Background

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The business is engaged in hospitality sector providing luxurious resort-based hotel to

people in effective manner. Luxurious hotels are provided in accordance to growth of company

and customers are satisfied.

Products and Services

The hotel resort-based services are provided by Cable Beach Hotel in providing efficient

services in a better manner. Room services, attached swimming pool and landscaping are

provided by firm to guests.

PESTLE Analysis

Political

Political instability

Fiscal policy

Economical

Rise in inflation rate

Economic growth

patterns

Social

Cultural trends

Demographics

Technological

Automation

Research &

Development

Legal

Changes in laws

Safety standards

Environmental

Geographic location

Changes in climate

Market Segment and Competitors' Analysis

The market segment of first class people so that they may be satisfied in a better way.

Moreover, luxury services will be provided to rich class people for enhancing customer

satisfaction. Competition is required to be analysed so that strategies may be implemented to

overcome challenges.

Distribution channels and Promotion

The distribution channels are available from suppliers for receiving raw materials for

preparing food. Moreover, promotion is required which would be done through social media

marketing, advertising on TV etc.

Financial Performance and Risk Analysis

6

people in effective manner. Luxurious hotels are provided in accordance to growth of company

and customers are satisfied.

Products and Services

The hotel resort-based services are provided by Cable Beach Hotel in providing efficient

services in a better manner. Room services, attached swimming pool and landscaping are

provided by firm to guests.

PESTLE Analysis

Political

Political instability

Fiscal policy

Economical

Rise in inflation rate

Economic growth

patterns

Social

Cultural trends

Demographics

Technological

Automation

Research &

Development

Legal

Changes in laws

Safety standards

Environmental

Geographic location

Changes in climate

Market Segment and Competitors' Analysis

The market segment of first class people so that they may be satisfied in a better way.

Moreover, luxury services will be provided to rich class people for enhancing customer

satisfaction. Competition is required to be analysed so that strategies may be implemented to

overcome challenges.

Distribution channels and Promotion

The distribution channels are available from suppliers for receiving raw materials for

preparing food. Moreover, promotion is required which would be done through social media

marketing, advertising on TV etc.

Financial Performance and Risk Analysis

6

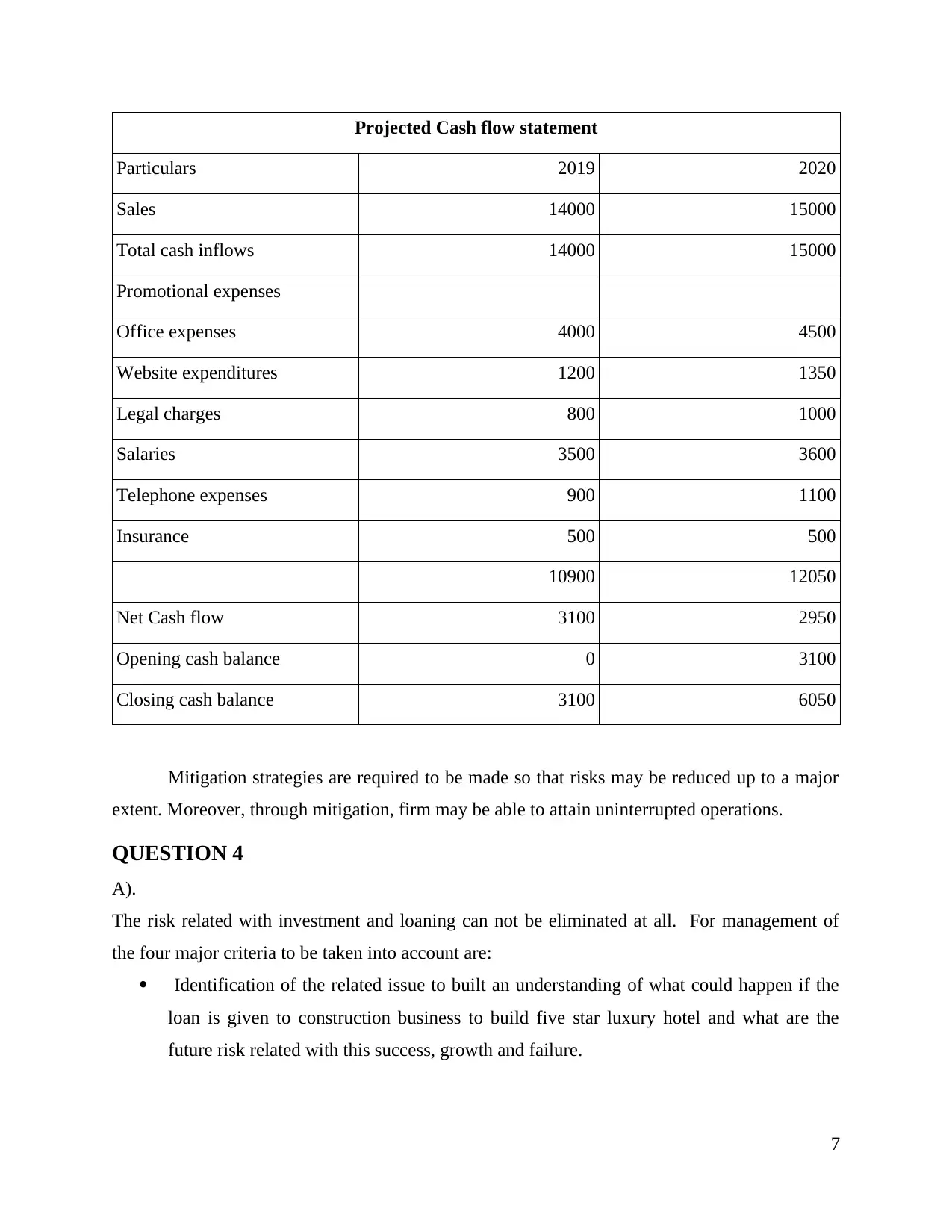

Projected Cash flow statement

Particulars 2019 2020

Sales 14000 15000

Total cash inflows 14000 15000

Promotional expenses

Office expenses 4000 4500

Website expenditures 1200 1350

Legal charges 800 1000

Salaries 3500 3600

Telephone expenses 900 1100

Insurance 500 500

10900 12050

Net Cash flow 3100 2950

Opening cash balance 0 3100

Closing cash balance 3100 6050

Mitigation strategies are required to be made so that risks may be reduced up to a major

extent. Moreover, through mitigation, firm may be able to attain uninterrupted operations.

QUESTION 4

A).

The risk related with investment and loaning can not be eliminated at all. For management of

the four major criteria to be taken into account are:

Identification of the related issue to built an understanding of what could happen if the

loan is given to construction business to build five star luxury hotel and what are the

future risk related with this success, growth and failure.

7

Particulars 2019 2020

Sales 14000 15000

Total cash inflows 14000 15000

Promotional expenses

Office expenses 4000 4500

Website expenditures 1200 1350

Legal charges 800 1000

Salaries 3500 3600

Telephone expenses 900 1100

Insurance 500 500

10900 12050

Net Cash flow 3100 2950

Opening cash balance 0 3100

Closing cash balance 3100 6050

Mitigation strategies are required to be made so that risks may be reduced up to a major

extent. Moreover, through mitigation, firm may be able to attain uninterrupted operations.

QUESTION 4

A).

The risk related with investment and loaning can not be eliminated at all. For management of

the four major criteria to be taken into account are:

Identification of the related issue to built an understanding of what could happen if the

loan is given to construction business to build five star luxury hotel and what are the

future risk related with this success, growth and failure.

7

To estimate the probability of the occurrence of what have been determined in the earlier

step.

Preparation of the plans and them implementing them to mitigate the risk involved with

extending the loan to the hotel and with determining the intensity of the probability of the

occurrence of the risk.

To establish effective and efficient monitoring and controlling measure to deal with the

potential outcomes of the risk so determined in the earlier stages.

B).

Risk is inevitable as this come along with each and every new plan be it related with

investment, finance of anything else (Definition of 'Risk Management', 2018). This also stay

through the implementation process and do no go away after completion of the project. But the

intensity of the risk involves gets lower down with stages of completions the end its existence

gets negligible. The element that are considered for the management of the risks within

commercial banking are:

Market and Industry Risk Assessment: the cost structure of the hotel business reflects

that major investment and expenses are incurred for a period on initial 5 years. With

decrease in the cost into major increment is profits is seen in the budgeted financial

statements of the construction project. The implication of the political factors is

determined with implementation new and amendments in exiting regularization of

operation of hotels. Major risk that is associated with climatic and weather changes as

with high tides and lows and risk of cyclones must also be considered.

Business Risk Assessment: with changes in the marketing policies and change in

preference of the consumers the hotel can face certain backdrop in its operations and

profitability. This can directly by linked with the repayment of the loans and interest

there on. The increment in occupancy percentage is predicted at lower growth. For

raising the rates of rooms in the hotel market penetration stagy is used which is good but

in long term this can not be considered as good policy as regulate client will detect this

easily and involves a risk of loosing reliable and potential clients.

Assessment of Financial Risk: this risk is related with growth and profitability along

with determination of cost and expenses (Principles for the Management of Credit Risk,

8

step.

Preparation of the plans and them implementing them to mitigate the risk involved with

extending the loan to the hotel and with determining the intensity of the probability of the

occurrence of the risk.

To establish effective and efficient monitoring and controlling measure to deal with the

potential outcomes of the risk so determined in the earlier stages.

B).

Risk is inevitable as this come along with each and every new plan be it related with

investment, finance of anything else (Definition of 'Risk Management', 2018). This also stay

through the implementation process and do no go away after completion of the project. But the

intensity of the risk involves gets lower down with stages of completions the end its existence

gets negligible. The element that are considered for the management of the risks within

commercial banking are:

Market and Industry Risk Assessment: the cost structure of the hotel business reflects

that major investment and expenses are incurred for a period on initial 5 years. With

decrease in the cost into major increment is profits is seen in the budgeted financial

statements of the construction project. The implication of the political factors is

determined with implementation new and amendments in exiting regularization of

operation of hotels. Major risk that is associated with climatic and weather changes as

with high tides and lows and risk of cyclones must also be considered.

Business Risk Assessment: with changes in the marketing policies and change in

preference of the consumers the hotel can face certain backdrop in its operations and

profitability. This can directly by linked with the repayment of the loans and interest

there on. The increment in occupancy percentage is predicted at lower growth. For

raising the rates of rooms in the hotel market penetration stagy is used which is good but

in long term this can not be considered as good policy as regulate client will detect this

easily and involves a risk of loosing reliable and potential clients.

Assessment of Financial Risk: this risk is related with growth and profitability along

with determination of cost and expenses (Principles for the Management of Credit Risk,

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2018). The net profits are projected to be more than double after considering all expanses

and taxation cost and this reduces the financial risk of repayment of the loan.

Documentation and Pricing risk: this is a risk related with act of frauds and

misrepresentation of the documents of insurance and provision of enforce ability in the

courts. The legal risk involved here can be defined as clauses for litigation to solve the

dispute and how all the legal proceeding will be carried out.

CONCLUSION

From the above report it can be concluded that landing an amount of 30,000,000 for a

project of 41,000,000 defined an involvement of higher risk. Almost more than 70% cost for

establishment of the project has been planned to be funded from the loan amount which is not a

good indication for the loaner that is the bank. Further it can be articulated that as

recommendation bank is given advice to extent the loan of only 505 of the project cost as the

financial cost will also be incurred by the bank for evaluation and survey to monitor the

construction by the independent firm appointed on behalf of bank. The bank has been given a

suggestion that if same loan amount of as applied by the construction firm, bank must apply

strict regulation and monitoring policies to evaluated the construction project of the five star

hotel.

9

and taxation cost and this reduces the financial risk of repayment of the loan.

Documentation and Pricing risk: this is a risk related with act of frauds and

misrepresentation of the documents of insurance and provision of enforce ability in the

courts. The legal risk involved here can be defined as clauses for litigation to solve the

dispute and how all the legal proceeding will be carried out.

CONCLUSION

From the above report it can be concluded that landing an amount of 30,000,000 for a

project of 41,000,000 defined an involvement of higher risk. Almost more than 70% cost for

establishment of the project has been planned to be funded from the loan amount which is not a

good indication for the loaner that is the bank. Further it can be articulated that as

recommendation bank is given advice to extent the loan of only 505 of the project cost as the

financial cost will also be incurred by the bank for evaluation and survey to monitor the

construction by the independent firm appointed on behalf of bank. The bank has been given a

suggestion that if same loan amount of as applied by the construction firm, bank must apply

strict regulation and monitoring policies to evaluated the construction project of the five star

hotel.

9

REFERENCES

Books and Journals

Aiyar, S., Calomiris, C.W. and Wieladek, T., 2016. How does credit supply respond to monetary

policy and bank minimum capital requirements?. European Economic Review. 82. pp.142-

165.

Bluhm, C., Overbeck, L. and Wagner, C., 2016. Introduction to credit risk modeling. Chapman

and Hall/CRC.

Chen, B. S., Hanson, S. G. and Stein, J. C., 2017. The decline of big-bank lending to small

business: Dynamic impacts on local credit and labor markets (No. w23843). National

Bureau of Economic Research.

Cingano, F., Manaresi, F. and Sette, E., 2016. Does credit crunch investment down? New

evidence on the real effects of the bank-lending channel. The Review of Financial

Studies.29(10). pp.2737-2773.

di Patti, E. B. and Sette, E., 2016. Did the securitization market freeze affect bank lending during

the financial crisis? Evidence from a credit register. Journal of Financial

Intermediation. 25. pp.54-76.

Faleye, O. and Krishnan, K., 2017. Risky lending: Does bank corporate governance

matter?. Journal of Banking & Finance.83.pp.57-69.

Immergluck, D., 2016. Credit to the Community: Community Reinvestment and Fair Lending

Policy in the United States: Community Reinvestment and Fair Lending Policy in the

United States. Routledge.

Ongena, S., Schindele, I. and Vonnák, D., 2017. In lands of foreign currency credit, bank lending

channels run through?.

ONLINE

Advanced Liquidity and Funding Risk Management. 2018. [Online]. Available though

:<https://www.ukfinance.org.uk/training/advanced-liquidity-and-funding-risk-

management-workshop-3/>.

10

Books and Journals

Aiyar, S., Calomiris, C.W. and Wieladek, T., 2016. How does credit supply respond to monetary

policy and bank minimum capital requirements?. European Economic Review. 82. pp.142-

165.

Bluhm, C., Overbeck, L. and Wagner, C., 2016. Introduction to credit risk modeling. Chapman

and Hall/CRC.

Chen, B. S., Hanson, S. G. and Stein, J. C., 2017. The decline of big-bank lending to small

business: Dynamic impacts on local credit and labor markets (No. w23843). National

Bureau of Economic Research.

Cingano, F., Manaresi, F. and Sette, E., 2016. Does credit crunch investment down? New

evidence on the real effects of the bank-lending channel. The Review of Financial

Studies.29(10). pp.2737-2773.

di Patti, E. B. and Sette, E., 2016. Did the securitization market freeze affect bank lending during

the financial crisis? Evidence from a credit register. Journal of Financial

Intermediation. 25. pp.54-76.

Faleye, O. and Krishnan, K., 2017. Risky lending: Does bank corporate governance

matter?. Journal of Banking & Finance.83.pp.57-69.

Immergluck, D., 2016. Credit to the Community: Community Reinvestment and Fair Lending

Policy in the United States: Community Reinvestment and Fair Lending Policy in the

United States. Routledge.

Ongena, S., Schindele, I. and Vonnák, D., 2017. In lands of foreign currency credit, bank lending

channels run through?.

ONLINE

Advanced Liquidity and Funding Risk Management. 2018. [Online]. Available though

:<https://www.ukfinance.org.uk/training/advanced-liquidity-and-funding-risk-

management-workshop-3/>.

10

Definition of 'Risk Management'. 2018. [Online]. Available though

:<https://economictimes.indiatimes.com/definition/risk-management>.

Principles for the Management of Credit Risk. 2018. [PDF]. Available though

:<https://www.bis.org/publ/bcbsc125.pdf>.

11

:<https://economictimes.indiatimes.com/definition/risk-management>.

Principles for the Management of Credit Risk. 2018. [PDF]. Available though

:<https://www.bis.org/publ/bcbsc125.pdf>.

11

1 out of 13

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.