Analyzing Delay Process in Banks for SMEs

VerifiedAdded on 2020/10/22

|14

|3319

|439

AI Summary

The given assignment requires a detailed analysis of the delay process in banks, particularly focusing on the challenges faced by Small and Medium-sized Enterprises (SMEs). It highlights the importance of online applications in reducing delays and discusses the need for banks to cater to customers with varying technological expertise. The assignment draws from academic literature and online sources to provide insights into bank branch efficiency, credit scoring, and social capital among information technology and business units.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Static Growth in SME lending

1

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

TASK...............................................................................................................................................3

High handling cost..................................................................................................................3

SME operational efficiency in processing bank applications.................................................5

Credit score Risk assessment in SME lending.......................................................................7

SME OPERATIONAL EFFICENCY IN PROCESSING CREDIT APPLICATIONS........8

Turn around time..................................................................................................................10

Customer delays...................................................................................................................11

REFERENCES..............................................................................................................................13

.......................................................................................................................................................14

2

TASK...............................................................................................................................................3

High handling cost..................................................................................................................3

SME operational efficiency in processing bank applications.................................................5

Credit score Risk assessment in SME lending.......................................................................7

SME OPERATIONAL EFFICENCY IN PROCESSING CREDIT APPLICATIONS........8

Turn around time..................................................................................................................10

Customer delays...................................................................................................................11

REFERENCES..............................................................................................................................13

.......................................................................................................................................................14

2

TASK

High handling cost

According to views of Paradi and Zhu, (2013) it is stated that the term handling cost

means cash paid to cover the cost of performing a transaction, packaging, transporting and more

used in manufacturing process of a product by a company. Generally small companies used to

rise funds from money lenders, investors and from bank on fixed rate of interest.

Over some past years, it has been observed that charges rate of banks are much hiked and

increasing at rapid rate. Therefore, to handle such type of lending by small companies are so

difficult which affects performance of business. In context with small lending companies, they

used to provide loan to other firms and individuals for their business on easy terms and condition

from established banks.

Management of these organisations are needed to control internal rates of banks so that

they can attract more customers to provide loan to them on small rates. This would help them in

generating more profit.

With the change in course of time, technology has changed different kinds of lending

industry process and made this easier (Brooks and Mukherjee, 2013). Now SMEs can take loans

easily. There are some of the criteria that company can think while doing this entire process.

No need to borrow money which cannot be repay: While borrowing loan, first thing that

should be kept in mind is of time under which company can repay this money that was taken. For

example: while taking a personal loan EMI for this must not be more that 10% according to the

net monthly income.

3

High handling cost

According to views of Paradi and Zhu, (2013) it is stated that the term handling cost

means cash paid to cover the cost of performing a transaction, packaging, transporting and more

used in manufacturing process of a product by a company. Generally small companies used to

rise funds from money lenders, investors and from bank on fixed rate of interest.

Over some past years, it has been observed that charges rate of banks are much hiked and

increasing at rapid rate. Therefore, to handle such type of lending by small companies are so

difficult which affects performance of business. In context with small lending companies, they

used to provide loan to other firms and individuals for their business on easy terms and condition

from established banks.

Management of these organisations are needed to control internal rates of banks so that

they can attract more customers to provide loan to them on small rates. This would help them in

generating more profit.

With the change in course of time, technology has changed different kinds of lending

industry process and made this easier (Brooks and Mukherjee, 2013). Now SMEs can take loans

easily. There are some of the criteria that company can think while doing this entire process.

No need to borrow money which cannot be repay: While borrowing loan, first thing that

should be kept in mind is of time under which company can repay this money that was taken. For

example: while taking a personal loan EMI for this must not be more that 10% according to the

net monthly income.

3

Keeping tenure for short period of time: While taking loan long term repay system

should be avoided as with the increase in durations interest rates may gets higher which small

scale industries can find it difficult in paying the same.

Ensure timely and regular repayment: In case of repayment of dues, management of

SME are required to pay the same in disciplined manner. They should not miss such kinds of

payments which are linked with short-term and long-term loan for business.

Don't borrow to invest: It concerns with basic rules of investing which forbade small

firms to use borrowed money for invest purpose (Wagner, Beimborn and Weitzel, 2014). In

addition to this, ultra-safe investments such as fixed deposits, bonds and more also not needed to

use for loan payment.

In a country, SMEs are considered as the backbone in context with economic

development. As per Moro and Fink, (2013), it has stated that about 97% to 99% of total

organisations running in UK, SMEs help in making this nation as best among top ten competitive

countries. As per incomplete characteristics of market information in terms of credit, SME face

different problems related to credit rationing.

It results to low economic status of such companies and ambiguous information structure

through which small firms are often subject to demanding credit constraints as compared to those

organisations which operate at large level. To overcome from this kind of issues, management of

these companies apply measures as per approval of public financial bodies for inadequate market

mechanism. It includes policy oriented loans, credit guaranteed scheme supported by

government and so on.

4

should be avoided as with the increase in durations interest rates may gets higher which small

scale industries can find it difficult in paying the same.

Ensure timely and regular repayment: In case of repayment of dues, management of

SME are required to pay the same in disciplined manner. They should not miss such kinds of

payments which are linked with short-term and long-term loan for business.

Don't borrow to invest: It concerns with basic rules of investing which forbade small

firms to use borrowed money for invest purpose (Wagner, Beimborn and Weitzel, 2014). In

addition to this, ultra-safe investments such as fixed deposits, bonds and more also not needed to

use for loan payment.

In a country, SMEs are considered as the backbone in context with economic

development. As per Moro and Fink, (2013), it has stated that about 97% to 99% of total

organisations running in UK, SMEs help in making this nation as best among top ten competitive

countries. As per incomplete characteristics of market information in terms of credit, SME face

different problems related to credit rationing.

It results to low economic status of such companies and ambiguous information structure

through which small firms are often subject to demanding credit constraints as compared to those

organisations which operate at large level. To overcome from this kind of issues, management of

these companies apply measures as per approval of public financial bodies for inadequate market

mechanism. It includes policy oriented loans, credit guaranteed scheme supported by

government and so on.

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

In addition to this, institutions which work in finance sectors, used to receive deposits

from public therefore, they are considered as relatively conservative as per lending policy. In

case of recession period, conservative lending practices carried by banks and financial

institutions used to impose a credit squeeze on company in sharp manner. Under this condition,

SME's are observed as one who bears the burnt more than large companies (Paradi and Zhu,

2013).

SME operational efficiency in processing bank applications

On the basis of view point of Cowling, Liu and Ledger, (2012) it has been stated that

small scale firm arrange money for doing activities in better manner. Without ability to manage

process of loan orientation in effective manner.

There are many developments are ascertained in technologies which enable small

organisation is use them for the purpose of ease of their different transactions. There are many

bank applications are emerges which improve the operational efficiency of bank regarding

raising of funds in short period of time.

This will termed as the main reason through static growth is ascertain in SME lending.

For example: Now small scale industries don't have to stand for a long queue for the approval of

bank loans. Bank are taking help of new tools and technologies along with some applications so

that time can be reduced and work can be done in quick time. Digitalisation has changed the

entire procedure of filling up of application forms and now clients don't have to face the long

process of documentation.

As per point of view Du, Guariglia and Newman, (2015) It is important for every small

business organisation to keep proper fund to operate their business in most effective manner. For

5

from public therefore, they are considered as relatively conservative as per lending policy. In

case of recession period, conservative lending practices carried by banks and financial

institutions used to impose a credit squeeze on company in sharp manner. Under this condition,

SME's are observed as one who bears the burnt more than large companies (Paradi and Zhu,

2013).

SME operational efficiency in processing bank applications

On the basis of view point of Cowling, Liu and Ledger, (2012) it has been stated that

small scale firm arrange money for doing activities in better manner. Without ability to manage

process of loan orientation in effective manner.

There are many developments are ascertained in technologies which enable small

organisation is use them for the purpose of ease of their different transactions. There are many

bank applications are emerges which improve the operational efficiency of bank regarding

raising of funds in short period of time.

This will termed as the main reason through static growth is ascertain in SME lending.

For example: Now small scale industries don't have to stand for a long queue for the approval of

bank loans. Bank are taking help of new tools and technologies along with some applications so

that time can be reduced and work can be done in quick time. Digitalisation has changed the

entire procedure of filling up of application forms and now clients don't have to face the long

process of documentation.

As per point of view Du, Guariglia and Newman, (2015) It is important for every small

business organisation to keep proper fund to operate their business in most effective manner. For

5

this, SME make their operational efficiency appropriate. This will lead in operating all the

process of banking application. In this context, small business can easily apply to bank and

another financial institution such as commercial loans, credit unions and so on. As small business

so not take loan to start a new business but they make loans for their ongoing business in which

they should follow all the procedures towards the loan application process (Cenni and et. al.,

2015). In addition of this, for taking loan SME should make a plan and make the appointment

with loan officer.

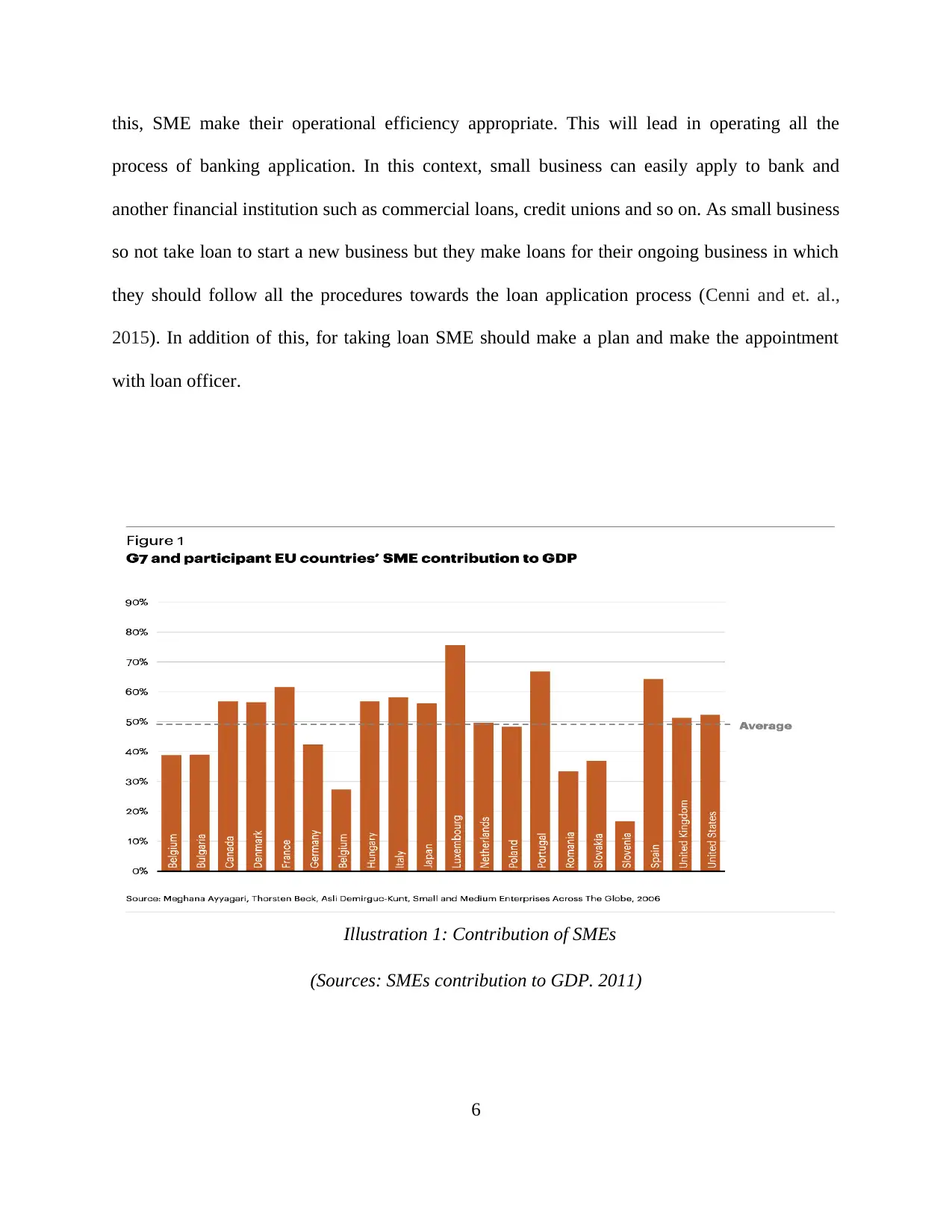

(Sources: SMEs contribution to GDP. 2011)

6

Illustration 1: Contribution of SMEs

process of banking application. In this context, small business can easily apply to bank and

another financial institution such as commercial loans, credit unions and so on. As small business

so not take loan to start a new business but they make loans for their ongoing business in which

they should follow all the procedures towards the loan application process (Cenni and et. al.,

2015). In addition of this, for taking loan SME should make a plan and make the appointment

with loan officer.

(Sources: SMEs contribution to GDP. 2011)

6

Illustration 1: Contribution of SMEs

From above mention graph, it can be said that SMEs contribute on average 53 percent of

GDI. On the other hand in United Kingdom, contribution of small business organisations have

raised up GDP of this country. This can be considered as a good position that has been carried by

United Kingdom in all over world (SME Clients: Do It Smart, Win Their Hearts, 2011).

Credit score Risk assessment in SME lending

As per views of Moro and Fink, (2013) Credit score is being considered as a numerical

appearance. These numbers rely on different levels of small business firm’s credit limit. In

regulatory body of any country, it is being found that ample number of small business enterprises

are doing business at small level but they are generating small amounts. Because of involvement

of capital which is applied by owner risks can be huge if business do not run in a successful

manner (Akkoç, 2012). Some of nature is being showed in a survey where small and medium

sized organisations and these are given below:

Lenders check past record of SME in order to their credibility.

Lenders seek specific requirements that needs to be fulfilled by SME's so that they

can lend money as per needed amount.

At the time of lending, lenders seek collateral security.

Henceforth, it is much required for SMEs to look at all the aspects and then only go for

borrowing loan by looking at appropriate credit (Einav, Jenkins and Levin, 2013). On the other

hand, it is responsibility of bank to look at the credit score before lending the loan so that no

fraudulent activities may take place. But, government of any country have made various policies

so that SMEs of this country do get into problem while doing business. Because these are the

organisations that majorly impacts positively on economic conditions of this Qatar.

7

GDI. On the other hand in United Kingdom, contribution of small business organisations have

raised up GDP of this country. This can be considered as a good position that has been carried by

United Kingdom in all over world (SME Clients: Do It Smart, Win Their Hearts, 2011).

Credit score Risk assessment in SME lending

As per views of Moro and Fink, (2013) Credit score is being considered as a numerical

appearance. These numbers rely on different levels of small business firm’s credit limit. In

regulatory body of any country, it is being found that ample number of small business enterprises

are doing business at small level but they are generating small amounts. Because of involvement

of capital which is applied by owner risks can be huge if business do not run in a successful

manner (Akkoç, 2012). Some of nature is being showed in a survey where small and medium

sized organisations and these are given below:

Lenders check past record of SME in order to their credibility.

Lenders seek specific requirements that needs to be fulfilled by SME's so that they

can lend money as per needed amount.

At the time of lending, lenders seek collateral security.

Henceforth, it is much required for SMEs to look at all the aspects and then only go for

borrowing loan by looking at appropriate credit (Einav, Jenkins and Levin, 2013). On the other

hand, it is responsibility of bank to look at the credit score before lending the loan so that no

fraudulent activities may take place. But, government of any country have made various policies

so that SMEs of this country do get into problem while doing business. Because these are the

organisations that majorly impacts positively on economic conditions of this Qatar.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Apart from this, it has also been analysed that in most of the companies around 50% of SMEs

have granted Certification. But the accreditation was not being granted.

SME OPERATIONAL EFFICENCY IN PROCESSING CREDIT APPLICATIONS

Credit processing solution is getting changed from the past few years to the current

period. In past years, it was hard for anybody to take advantages of credit opportunities in a

manual term. These activities are all related to different services that provided by individual's to

others in the terms of money on the basis of their requirement and need.

Now a days, these services are provided by financial institution as well as banks. They

use manual as well as automate lending option for these services. The information on these

application is basically consider analysis of lender's past history, earnings status and abilities to

repay amount of credit at proper time period. This process takes a proper time to provide proper

approval for a credit loan (Brooks and Mukherjee, 2013).

In this, different teams and level of operations are analyse effectiveness to perceiving

different activities. At a time, different banks uses manual tools and spreadsheets to review and

analyse several terms properly. These activities are based on process of loan approval approaches

that take a specific time but not such organisations are adopt automate techniques to proceed

quickly for approval. There are different terms determine below that used to efficiently

processing loan application as-

Inside Mindtree's Flexible – This term basically uses in advance monitoring processing

activity in which technology uses as integrated manner as well as securely. Main objective of this

process is reduce risk within loan process and activities. This is a most specific and beneficial

approach that result as a convenient platform for firm as well as individual.

8

have granted Certification. But the accreditation was not being granted.

SME OPERATIONAL EFFICENCY IN PROCESSING CREDIT APPLICATIONS

Credit processing solution is getting changed from the past few years to the current

period. In past years, it was hard for anybody to take advantages of credit opportunities in a

manual term. These activities are all related to different services that provided by individual's to

others in the terms of money on the basis of their requirement and need.

Now a days, these services are provided by financial institution as well as banks. They

use manual as well as automate lending option for these services. The information on these

application is basically consider analysis of lender's past history, earnings status and abilities to

repay amount of credit at proper time period. This process takes a proper time to provide proper

approval for a credit loan (Brooks and Mukherjee, 2013).

In this, different teams and level of operations are analyse effectiveness to perceiving

different activities. At a time, different banks uses manual tools and spreadsheets to review and

analyse several terms properly. These activities are based on process of loan approval approaches

that take a specific time but not such organisations are adopt automate techniques to proceed

quickly for approval. There are different terms determine below that used to efficiently

processing loan application as-

Inside Mindtree's Flexible – This term basically uses in advance monitoring processing

activity in which technology uses as integrated manner as well as securely. Main objective of this

process is reduce risk within loan process and activities. This is a most specific and beneficial

approach that result as a convenient platform for firm as well as individual.

8

All these activities and procedures are used to manage corporate loan life-cycle (Wagner,

Beimborn and Weitzel, 2014). Through this, banks can easily manage their activities in effective

as well as appropriate manner. The Mindtree process basically determine as a pre-build approach

which is beneficial for each bank to processing easily in terms of credit approaches. This is a

most beneficial and specific process that aid to maximise productivity and reduce extra

approaches to manage time related terms in specific manner.

Credit processing solution – Now a days, organisations uses different kind of activities

for credit proceeding terms. These approaches are based on different element that working as a

proper structured format. In this, employees of organisation collect data of customers on the

basis of required documentation and information files.

After this employees assist to provide proper information to particular candidate about

credit risk rating. Loan servicing system is also a part of this activity that uses to provide

facilities to individual on the basis of organisational policies and terms. All these activities assist

in credit processing solution approaches of banks and financial bodies.

Existing IT infrastructure are determine reporting approach, control and analysis or

document management activities. Through this, manager of this division can manage proposal

process to analyse proper timing for final approval (Cowling, Liu and Ledger, 2012). All these

activities are held on automotive technique to manage vast information within a specific storage.

By implementing such tools as Mindtree's the credit processing solution get End to End

benefits as -

These kind of procedure assist to improve efficiency and productivity to manage

data in proper formation.

9

Beimborn and Weitzel, 2014). Through this, banks can easily manage their activities in effective

as well as appropriate manner. The Mindtree process basically determine as a pre-build approach

which is beneficial for each bank to processing easily in terms of credit approaches. This is a

most beneficial and specific process that aid to maximise productivity and reduce extra

approaches to manage time related terms in specific manner.

Credit processing solution – Now a days, organisations uses different kind of activities

for credit proceeding terms. These approaches are based on different element that working as a

proper structured format. In this, employees of organisation collect data of customers on the

basis of required documentation and information files.

After this employees assist to provide proper information to particular candidate about

credit risk rating. Loan servicing system is also a part of this activity that uses to provide

facilities to individual on the basis of organisational policies and terms. All these activities assist

in credit processing solution approaches of banks and financial bodies.

Existing IT infrastructure are determine reporting approach, control and analysis or

document management activities. Through this, manager of this division can manage proposal

process to analyse proper timing for final approval (Cowling, Liu and Ledger, 2012). All these

activities are held on automotive technique to manage vast information within a specific storage.

By implementing such tools as Mindtree's the credit processing solution get End to End

benefits as -

These kind of procedure assist to improve efficiency and productivity to manage

data in proper formation.

9

These kind of business activities are totally updated by implementing new

modification and alteration. These approaches assist to insert new terms in business

process and inactivities.

These kind of approaches used to classify task to different person to accomplish

them properly till the approval limits.

By implementing such tools, management control risk and security related issues

and that can impact directly on credit processing.

All these approaches create transparency properly in the perspective of customers

to build trust in their minds as well as to build long term relations.

Turn around time

Turnaround time term can be understood as the time span from application of a loan by a

customer till the final allocation of loan amount. It has been analysed that in modern world,

majorly whenever SMEs looks to expand or to improve productivity (Du, Guariglia and

Newman, 2015).

They go for loans because of lack of capital in their hands. Rise in competition among

small and middle sized company's has impacted positively on banks. Here, providing loan to

business firms can be said is the main aim of Banks. Therefore, it is being found that Banks are

speeding up the Turn around time of providing loans or sanctioning it. With the help of this, it

can be said that organisations can now easily look into different aspects through which many

benefits can easily be gained by them.

Like appropriate funds at the time of expansion or to make modifications in operations

(Cenni and et. al., 2015). Through this, it can be said that firms are easily hitting their targets

10

modification and alteration. These approaches assist to insert new terms in business

process and inactivities.

These kind of approaches used to classify task to different person to accomplish

them properly till the approval limits.

By implementing such tools, management control risk and security related issues

and that can impact directly on credit processing.

All these approaches create transparency properly in the perspective of customers

to build trust in their minds as well as to build long term relations.

Turn around time

Turnaround time term can be understood as the time span from application of a loan by a

customer till the final allocation of loan amount. It has been analysed that in modern world,

majorly whenever SMEs looks to expand or to improve productivity (Du, Guariglia and

Newman, 2015).

They go for loans because of lack of capital in their hands. Rise in competition among

small and middle sized company's has impacted positively on banks. Here, providing loan to

business firms can be said is the main aim of Banks. Therefore, it is being found that Banks are

speeding up the Turn around time of providing loans or sanctioning it. With the help of this, it

can be said that organisations can now easily look into different aspects through which many

benefits can easily be gained by them.

Like appropriate funds at the time of expansion or to make modifications in operations

(Cenni and et. al., 2015). Through this, it can be said that firms are easily hitting their targets

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

because of appropriate money are continuously getting fulfilled. Some of major lenders of Qatar

like HSBC, Barclays, Lloyd and many more have reduced turn around time from application of

loan to sanctioning the funds to half. This have impacted positively on economic conditions of

Qatar as well.

Managers and leaders of Banks have mentioned that, reduction in turn around time can

has helped them in improvising bank's efficiency along with performance. They have also stated

that with the help of this, customers base have also been increased which impacted positively on

percentage of satisfaction that they were providing to customers before.

It also affected positively on their expenses as well. Because, in previous years people

used to wait for a longer period of time may be for months. But nowadays, when customer puts

an application of asking for loans or for some other credits it can be said that there are ample

number of situations which a person or SMEs have to go through.

But the time span have got reduced from months to few days. Digitalisation has helped

banks in improvising performances. Because of this, money can easily be transferred from one

place to another with in few seconds (Moro and Fink, 2013).

Customer delays

It has been analysed that, consumers mostly faces ample number of issues when they

reaches a bank to take loan or for some other service. As per analysis, Britain's largest banks that

are much faster in nature mentioned that, around 56 days on an average they are taking to

sanction a loan after when an application of customer reaches to them. During, 2007, UK banks

went through financial crisis. This happened because banks enhanced number of delinquencies

mortgages. The impact was really very huge which declined over all macroeconomic activities.

11

like HSBC, Barclays, Lloyd and many more have reduced turn around time from application of

loan to sanctioning the funds to half. This have impacted positively on economic conditions of

Qatar as well.

Managers and leaders of Banks have mentioned that, reduction in turn around time can

has helped them in improvising bank's efficiency along with performance. They have also stated

that with the help of this, customers base have also been increased which impacted positively on

percentage of satisfaction that they were providing to customers before.

It also affected positively on their expenses as well. Because, in previous years people

used to wait for a longer period of time may be for months. But nowadays, when customer puts

an application of asking for loans or for some other credits it can be said that there are ample

number of situations which a person or SMEs have to go through.

But the time span have got reduced from months to few days. Digitalisation has helped

banks in improvising performances. Because of this, money can easily be transferred from one

place to another with in few seconds (Moro and Fink, 2013).

Customer delays

It has been analysed that, consumers mostly faces ample number of issues when they

reaches a bank to take loan or for some other service. As per analysis, Britain's largest banks that

are much faster in nature mentioned that, around 56 days on an average they are taking to

sanction a loan after when an application of customer reaches to them. During, 2007, UK banks

went through financial crisis. This happened because banks enhanced number of delinquencies

mortgages. The impact was really very huge which declined over all macroeconomic activities.

11

Therefore, this was the reason where Banks started going through credit scores of companies and

of person and makes surety that if they can repay it or not (Cowling, Liu and Ledger, 2012).

Because of this, customers of these banks face delays in all the processes. On the other

hand, most of employees of banks are of middle age which are not aware of new and updated

technology. This can be considered as a reason which can slower down the transactional process

at bank that may irritate its consumers. Scenario which has discussed above may raise conflicts

among executives of banks and customers. These issues may also pull up thinking in mind of

users that they should end up accounts and open in another which is faster and cooperative.

Delay process can be reduced to zero, if banks will provide online applications to their

customers. Through this, it can be said that delay process can easily be reduced if this facility is

being provided by bank where person can easily transfer the money without going at bank.

On the other hand, it has also been analysed that most of people who are having age

around 50, do not know how to use online applications. Therefore, it is required for banks to take

various initiatives through which customer may get good experience through less delays in

different processes (Brooks and Mukherjee, 2013).

12

of person and makes surety that if they can repay it or not (Cowling, Liu and Ledger, 2012).

Because of this, customers of these banks face delays in all the processes. On the other

hand, most of employees of banks are of middle age which are not aware of new and updated

technology. This can be considered as a reason which can slower down the transactional process

at bank that may irritate its consumers. Scenario which has discussed above may raise conflicts

among executives of banks and customers. These issues may also pull up thinking in mind of

users that they should end up accounts and open in another which is faster and cooperative.

Delay process can be reduced to zero, if banks will provide online applications to their

customers. Through this, it can be said that delay process can easily be reduced if this facility is

being provided by bank where person can easily transfer the money without going at bank.

On the other hand, it has also been analysed that most of people who are having age

around 50, do not know how to use online applications. Therefore, it is required for banks to take

various initiatives through which customer may get good experience through less delays in

different processes (Brooks and Mukherjee, 2013).

12

REFERENCES

Books and Journals

Paradi, J. C. and Zhu, H., 2013. A survey on bank branch efficiency and performance research

with data envelopment analysis. Omega. 41(1). pp.61-79.

Brooks, R. and Mukherjee, A. K., 2013. Financial management: core concepts. Pearson.

Wagner, H. T., Beimborn, D. and Weitzel, T., 2014. How social capital among information

technology and business units drives operational alignment and IT business value.

Journal of Management Information Systems. 31(1). pp.241-272.

Cowling, M., Liu, W. and Ledger, A., 2012. Small business financing in the UK before and

during the current financial crisis. International Small Business Journal. 30(7). pp.778-800.

Du, J., Guariglia, A. and Newman, A., 2015. Do Social Capital Building Strategies Influence the

Financing Behavior of Chinese Private Small and Medium–Sized Enterprises?.

Entrepreneurship theory and practice. 39(3). pp.601-631.

Cenni, S., and et. al., 2015. Credit rationing and relationship lending. Does firm size matter?.

Journal of banking & finance. 53. pp.249-265.

Moro, A. and Fink, M., 2013. Loan managers’ trust and credit access for SMEs. Journal of

Banking & Finance. 37(3). pp.927-936.

Akkoç, S., 2012. An empirical comparison of conventional techniques, neural networks and the

three stage hybrid Adaptive Neuro Fuzzy Inference System (ANFIS) model for credit

scoring analysis: The case of Turkish credit card data. European Journal of Operational

Research. 222(1). pp.168-178.

13

Books and Journals

Paradi, J. C. and Zhu, H., 2013. A survey on bank branch efficiency and performance research

with data envelopment analysis. Omega. 41(1). pp.61-79.

Brooks, R. and Mukherjee, A. K., 2013. Financial management: core concepts. Pearson.

Wagner, H. T., Beimborn, D. and Weitzel, T., 2014. How social capital among information

technology and business units drives operational alignment and IT business value.

Journal of Management Information Systems. 31(1). pp.241-272.

Cowling, M., Liu, W. and Ledger, A., 2012. Small business financing in the UK before and

during the current financial crisis. International Small Business Journal. 30(7). pp.778-800.

Du, J., Guariglia, A. and Newman, A., 2015. Do Social Capital Building Strategies Influence the

Financing Behavior of Chinese Private Small and Medium–Sized Enterprises?.

Entrepreneurship theory and practice. 39(3). pp.601-631.

Cenni, S., and et. al., 2015. Credit rationing and relationship lending. Does firm size matter?.

Journal of banking & finance. 53. pp.249-265.

Moro, A. and Fink, M., 2013. Loan managers’ trust and credit access for SMEs. Journal of

Banking & Finance. 37(3). pp.927-936.

Akkoç, S., 2012. An empirical comparison of conventional techniques, neural networks and the

three stage hybrid Adaptive Neuro Fuzzy Inference System (ANFIS) model for credit

scoring analysis: The case of Turkish credit card data. European Journal of Operational

Research. 222(1). pp.168-178.

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Einav, L., Jenkins, M. and Levin, J., 2013. The impact of credit scoring on consumer lending.

The RAND Journal of Economics. 44(2). pp.249-274.

Online

SME Clients: Do It Smart, Win Their Hearts, 2011. [Online]. Available through:

<https://www.atkearney.com.au/en/financial-institutions/ideas-insights/article/-/

asset_publisher/LCcgOeS4t85g/content/sme-clients-do-it-smart-win-their-hearts/

10192>.

14

The RAND Journal of Economics. 44(2). pp.249-274.

Online

SME Clients: Do It Smart, Win Their Hearts, 2011. [Online]. Available through:

<https://www.atkearney.com.au/en/financial-institutions/ideas-insights/article/-/

asset_publisher/LCcgOeS4t85g/content/sme-clients-do-it-smart-win-their-hearts/

10192>.

14

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.