AFA 3: Advice Strategy Paper: Post-retirement Case Study Analysis

VerifiedAdded on 2021/04/21

|16

|7241

|25

Homework Assignment

AI Summary

This document presents a comprehensive analysis of a financial advice strategy paper, focusing on a post-retirement case study. The assignment, completed for the AFA 3 course, addresses the financial situation of a 75-year-old widow, Ida, who is dealing with inheritance, superannuation, and age pension implications. The paper outlines the client's financial goals, including maintaining her lifestyle, managing inheritance, and ensuring a tax-effective estate plan for her children and grandchildren. The analysis covers various aspects of financial planning, such as managing living expenses, insurance, investments, and the impact of superannuation and age pension on the client's financial well-being. The assignment also explores strategies to minimize tax liabilities and protect assets, particularly for the client's daughter. The document provides detailed calculations and addresses key considerations for providing sound financial advice in a post-retirement scenario, including inheritance and estate planning.

AFA 3 Advanced Advice Solutions

Assessment 2: Advice Strategy Paper

Assessment marks: 45 | Presentation marks: 5

Total marks: 50

Your assessment should be loaded into KapLearn by 11.30 pm on the due date.

All times are based on AEDT/AEST time zones.

Refer to ‘Time remaining’ on the ‘Assessment’ page in KapLearn to ensure you submit

your assessment by the specified due date and time.

Important: This document must be submitted in Microsoft Word format, and not in PDF.

Name: <Type here>

Student number: <Type here>

Grade

Grade Abbreviation Mark range (%) Mark (%)

High Distinction HD 85–100 <Mark here>

Distinction D 75–84 <Mark here>

Credit CR 65–74 <Mark here>

Pass P 50–64 <Mark here>

Fail F 0–49 <Mark here>

Assessment feedback

For marker use only.

1

Assessment 2: Advice Strategy Paper

Assessment marks: 45 | Presentation marks: 5

Total marks: 50

Your assessment should be loaded into KapLearn by 11.30 pm on the due date.

All times are based on AEDT/AEST time zones.

Refer to ‘Time remaining’ on the ‘Assessment’ page in KapLearn to ensure you submit

your assessment by the specified due date and time.

Important: This document must be submitted in Microsoft Word format, and not in PDF.

Name: <Type here>

Student number: <Type here>

Grade

Grade Abbreviation Mark range (%) Mark (%)

High Distinction HD 85–100 <Mark here>

Distinction D 75–84 <Mark here>

Credit CR 65–74 <Mark here>

Pass P 50–64 <Mark here>

Fail F 0–49 <Mark here>

Assessment feedback

For marker use only.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Instructions to students

• This assessment covers Topics 5 to 8 and accounts for 50% of your final grade.

• There are two (2) short-answer questions and one (1) extended response in this assessment.

You should answer all questions.

• The overall word limit for the assessment is 3200 words. Headings, quotes and references within the

body of the answer are included in the word count. Numerical tables, calculations, and reference lists

are not included.

• Refer to the Criteria-based Marking Guide for guidelines on what is expected for each question.

• The ‘General assessment information’ section in KapLearn contains information about format and

presentation, word limits, citations and referencing, collusion, plagiarism and other policies,

useful resources, submitting your assessment and accessing your results.

• Full workings must be shown for all calculations. Show all calculations in the text of your assessment

and NOT attached as an additional document. Additional documents will NOT be considered in the

marking.

• Answers are to be in your own words. Reference and cite all your sources (within the text of your

answer) when quoting or using material from external sources. Include a reference list at the end of

your assessment. Refer to the ‘Referencing and Citations Guide’ available from the ‘Library Learning

Hub’ in KapLearn for further information on referencing.

• Indicative weightings are noted beside each question. Use these weightings to assist you with your

allocation of time and resources. The weightings indicate the relative importance of each question.

• State all assumptions used in providing your answer.

• Requests for special consideration or information pertaining to special consideration written in the

body of the assessment will not be considered by the marker. Refer to the ‘special consideration’

section of the Assessment Policy on Kaplan’s website for more information.

2

• This assessment covers Topics 5 to 8 and accounts for 50% of your final grade.

• There are two (2) short-answer questions and one (1) extended response in this assessment.

You should answer all questions.

• The overall word limit for the assessment is 3200 words. Headings, quotes and references within the

body of the answer are included in the word count. Numerical tables, calculations, and reference lists

are not included.

• Refer to the Criteria-based Marking Guide for guidelines on what is expected for each question.

• The ‘General assessment information’ section in KapLearn contains information about format and

presentation, word limits, citations and referencing, collusion, plagiarism and other policies,

useful resources, submitting your assessment and accessing your results.

• Full workings must be shown for all calculations. Show all calculations in the text of your assessment

and NOT attached as an additional document. Additional documents will NOT be considered in the

marking.

• Answers are to be in your own words. Reference and cite all your sources (within the text of your

answer) when quoting or using material from external sources. Include a reference list at the end of

your assessment. Refer to the ‘Referencing and Citations Guide’ available from the ‘Library Learning

Hub’ in KapLearn for further information on referencing.

• Indicative weightings are noted beside each question. Use these weightings to assist you with your

allocation of time and resources. The weightings indicate the relative importance of each question.

• State all assumptions used in providing your answer.

• Requests for special consideration or information pertaining to special consideration written in the

body of the assessment will not be considered by the marker. Refer to the ‘special consideration’

section of the Assessment Policy on Kaplan’s website for more information.

2

Assessment presentation and referencing (5 marks)

Your answers are expected to be presented in a manner that would be befitting a real client

scenario. You may be required to research beyond the subject notes in answering the questions in

this assessment. Reference and cite all your sources when quoting or using material from external

sources. Include a reference list at the end of your assessment.

You are required to:

• use appropriate presentation and format for your assessment

• demonstrate independent research and analysis

• demonstrate appropriate use of relevant references

• follow the Harvard referencing style as recommended in the ‘Referencing and Citations available

from the ‘Library Learning Hub’ in KapLearn

• include a reference list at the end of your assessment following the recommended

referencing style

• adhere with the assessment word limit.

Criteria-based marking guide for presentation and referencing

The Criteria-based Marking Guide provided at the end of each question is designed to assist students

to understand what is expected of them in each question and to let them know how their

performance will be judged. It provides advice about the criteria used in the marking of the question

and what discriminates between an excellent, satisfactory and unsatisfactory answer.

Excellent

(Mark range: 4–5 marks)

Satisfactory

(Mark range: 2.5–3.5 marks)

Unsatisfactory

(Mark range: 0–2 marks)

• clear and appropriate assessment

layout and structure

• clear evidence of independent

research and analysis incorporated

throughout assessment

• appropriate use of referencing

• accurate use of Harvard referencing

style

• comprehensive reference list provided

at end of assessment

• adequate assessment layout and

structure

• some evidence of independent research

and analysis

• appropriate use of referencing

• use of Harvard referencing style

• reference list provided at end of

assessment

• poor assessment layout and/or structure

• assessment is significantly under or over

the word limit

• no demonstrated independent research

or analysis

• no use of references

• referencing does not use Harvard

referencing style

• no or inadequate reference list provided

at end of assessment

3

Your answers are expected to be presented in a manner that would be befitting a real client

scenario. You may be required to research beyond the subject notes in answering the questions in

this assessment. Reference and cite all your sources when quoting or using material from external

sources. Include a reference list at the end of your assessment.

You are required to:

• use appropriate presentation and format for your assessment

• demonstrate independent research and analysis

• demonstrate appropriate use of relevant references

• follow the Harvard referencing style as recommended in the ‘Referencing and Citations available

from the ‘Library Learning Hub’ in KapLearn

• include a reference list at the end of your assessment following the recommended

referencing style

• adhere with the assessment word limit.

Criteria-based marking guide for presentation and referencing

The Criteria-based Marking Guide provided at the end of each question is designed to assist students

to understand what is expected of them in each question and to let them know how their

performance will be judged. It provides advice about the criteria used in the marking of the question

and what discriminates between an excellent, satisfactory and unsatisfactory answer.

Excellent

(Mark range: 4–5 marks)

Satisfactory

(Mark range: 2.5–3.5 marks)

Unsatisfactory

(Mark range: 0–2 marks)

• clear and appropriate assessment

layout and structure

• clear evidence of independent

research and analysis incorporated

throughout assessment

• appropriate use of referencing

• accurate use of Harvard referencing

style

• comprehensive reference list provided

at end of assessment

• adequate assessment layout and

structure

• some evidence of independent research

and analysis

• appropriate use of referencing

• use of Harvard referencing style

• reference list provided at end of

assessment

• poor assessment layout and/or structure

• assessment is significantly under or over

the word limit

• no demonstrated independent research

or analysis

• no use of references

• referencing does not use Harvard

referencing style

• no or inadequate reference list provided

at end of assessment

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Post-retirement case study

You are required to use the following case study to complete the assessment questions.

Please read it carefully and pay particular attention to the quantitative measures of the scenario.

Ida, who is 75, has recently been widowed following the death of her husband Eric, who was aged

77. Ida and Eric have three children, John (51), Philip (48), and Cheyenne (45). All three children are

independent, with Philip and John having their own family. Cheyenne has had numerous relationship

problems, has been married twice, and has three children from separate fathers.

Ida owned her home as joint tenants with her late husband and this is now in her own name. There

is no outstanding mortgage nor other debts. She has recently received a $200,000 inheritance from

her late mother’s estate.

Ida is fully retired and only worked for a few years before she married Eric.

Ida’s general living expenses are $3,000 per month (this does not include any of the specific

expenses mentioned below).

Ida’s home and contents insurance premium is $749 per annum. Ida also has a ten-year-old Honda

Civic. The comprehensive insurance premium for the car is $565 p.a. and she has compulsory third

party insurance with a premium of $626 per annum. She also has health insurance with a premium

of $1,152 p.a. She pays all these bills by cheque. Ida does not have any other insurance.

Ida goes on regular National Seniors coach trips that cost on average $675 per quarter. She is also

planning an organised European Heritage tour. The total package, including airfares, etc. is $9,000.

Ida has a four-year term deposit of $20,000, earning 2.5%, with the interest paid monthly. This term

deposit is due to mature in six months. In addition, she has a cheque account, which rarely has a

balance of over $1,000, that does not pay interest and she is charged $5 per month.

Ida has a superannuation fund with a balance of $79,000 made up of $36,000 tax free component

and $43,000 taxable component (element taxed). She has continued to hold her superannuation

benefit within the accumulation phase so she can use it to cover any excess costs and to use as an

emergency fund. Her belief is that if it is used as an income stream she will lose access to the funds.

Eric’s superannuation benefit was in the pension phase, that he commenced just prior to attaining

age 65 with a purchase price of $225,000. At the time of Eric’s death, the balance was $161,000

made up of $68,000 tax-free component and $93,000 taxable component (element taxed), he was

receiving income payments of $9,660 per annum. Eric commenced this account based pension prior

to 1 January 2015, and has continuously received aged pension since this date. Ida is the automatic

reversionary beneficiary.

Ida has been advised that she will have a reduction in her Age Pension entitlement, which she is unhappy

about. She would like to have the same amount of Age Pension she had when Eric was still alive.

Further, Ida is confused concerning Eric’s superannuation benefit. She has been receiving conflicting

information from various sources. Some say she can continue receiving Eric’s income stream, other

say if she receives it as a lump sum she will be entitled to a greater amount than the current balance.

In addition, she is concerned that if she receives Eric’s superannuation money she will have to pay

tax on any benefits she receives. Everyone she speaks to tells her superannuation is taxed on the

way in, taxed when it’s there, and taxed on the way out. She is also concerned that receiving the

superannuation benefit will also lead to an even smaller amount of Age Pension.

4

You are required to use the following case study to complete the assessment questions.

Please read it carefully and pay particular attention to the quantitative measures of the scenario.

Ida, who is 75, has recently been widowed following the death of her husband Eric, who was aged

77. Ida and Eric have three children, John (51), Philip (48), and Cheyenne (45). All three children are

independent, with Philip and John having their own family. Cheyenne has had numerous relationship

problems, has been married twice, and has three children from separate fathers.

Ida owned her home as joint tenants with her late husband and this is now in her own name. There

is no outstanding mortgage nor other debts. She has recently received a $200,000 inheritance from

her late mother’s estate.

Ida is fully retired and only worked for a few years before she married Eric.

Ida’s general living expenses are $3,000 per month (this does not include any of the specific

expenses mentioned below).

Ida’s home and contents insurance premium is $749 per annum. Ida also has a ten-year-old Honda

Civic. The comprehensive insurance premium for the car is $565 p.a. and she has compulsory third

party insurance with a premium of $626 per annum. She also has health insurance with a premium

of $1,152 p.a. She pays all these bills by cheque. Ida does not have any other insurance.

Ida goes on regular National Seniors coach trips that cost on average $675 per quarter. She is also

planning an organised European Heritage tour. The total package, including airfares, etc. is $9,000.

Ida has a four-year term deposit of $20,000, earning 2.5%, with the interest paid monthly. This term

deposit is due to mature in six months. In addition, she has a cheque account, which rarely has a

balance of over $1,000, that does not pay interest and she is charged $5 per month.

Ida has a superannuation fund with a balance of $79,000 made up of $36,000 tax free component

and $43,000 taxable component (element taxed). She has continued to hold her superannuation

benefit within the accumulation phase so she can use it to cover any excess costs and to use as an

emergency fund. Her belief is that if it is used as an income stream she will lose access to the funds.

Eric’s superannuation benefit was in the pension phase, that he commenced just prior to attaining

age 65 with a purchase price of $225,000. At the time of Eric’s death, the balance was $161,000

made up of $68,000 tax-free component and $93,000 taxable component (element taxed), he was

receiving income payments of $9,660 per annum. Eric commenced this account based pension prior

to 1 January 2015, and has continuously received aged pension since this date. Ida is the automatic

reversionary beneficiary.

Ida has been advised that she will have a reduction in her Age Pension entitlement, which she is unhappy

about. She would like to have the same amount of Age Pension she had when Eric was still alive.

Further, Ida is confused concerning Eric’s superannuation benefit. She has been receiving conflicting

information from various sources. Some say she can continue receiving Eric’s income stream, other

say if she receives it as a lump sum she will be entitled to a greater amount than the current balance.

In addition, she is concerned that if she receives Eric’s superannuation money she will have to pay

tax on any benefits she receives. Everyone she speaks to tells her superannuation is taxed on the

way in, taxed when it’s there, and taxed on the way out. She is also concerned that receiving the

superannuation benefit will also lead to an even smaller amount of Age Pension.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Ida would like to use the $200,000 inheritance to assist in funding her lifestyle and ensuring she can

stay at home for as long as possible but making sure it has minimal impact on her Age Pension and

taxation. She is not overly concerned regarding access to it as she has her superannuation benefit to

use if she needs money. In addition, she would like to pass an inheritance to her children.

Like Ida’s inheritance, she would like all her assets to go evenly to her children. However, she is

concerned that any funds flowing to her daughter, Cheyenne, may be lost and end up going to her

next partner. She would like to make sure that her grandchildren will eventually receive the benefits

of her estate but allowing Cheyenne to use any income that may be generated from her portion of

Ida’s estate. In addition, Ida would like her estate paid to her children in the most tax effective way

and would like to see this detailed.

Ida wants to make sure that any advice she receives she can understand, is tax effective, and has a

minimal impact on or enhances her Age Pension entitlements.

5

stay at home for as long as possible but making sure it has minimal impact on her Age Pension and

taxation. She is not overly concerned regarding access to it as she has her superannuation benefit to

use if she needs money. In addition, she would like to pass an inheritance to her children.

Like Ida’s inheritance, she would like all her assets to go evenly to her children. However, she is

concerned that any funds flowing to her daughter, Cheyenne, may be lost and end up going to her

next partner. She would like to make sure that her grandchildren will eventually receive the benefits

of her estate but allowing Cheyenne to use any income that may be generated from her portion of

Ida’s estate. In addition, Ida would like her estate paid to her children in the most tax effective way

and would like to see this detailed.

Ida wants to make sure that any advice she receives she can understand, is tax effective, and has a

minimal impact on or enhances her Age Pension entitlements.

5

Question 1 The client’s position (10 marks)

Criteria-based marking guide for Question 1(a)–(b)

Excellent

(Mark range: 8–10 marks)

Satisfactory

(Mark range: 5–7.5 marks)

Unsatisfactory

(Mark range: 0–4.5 marks)

• all client outcomes shown in a clear and

appropriate manner

• clear evidence of understanding the

technical complications that may arise

in the advice process

• accurate financial calculations and data

used to explained sections A & B

• client outcomes listed, but not defined

against their current situation

• some technical knowledge shown

through the identification of

complications

• basic financial data used to explain

sections A & B

• no clear client outcomes or vague

explanation

• little or no evidence of understanding

the technical complications that may

arise in the advice process

• no financial calculations and data used

to explain sections A & B

6

Criteria-based marking guide for Question 1(a)–(b)

Excellent

(Mark range: 8–10 marks)

Satisfactory

(Mark range: 5–7.5 marks)

Unsatisfactory

(Mark range: 0–4.5 marks)

• all client outcomes shown in a clear and

appropriate manner

• clear evidence of understanding the

technical complications that may arise

in the advice process

• accurate financial calculations and data

used to explained sections A & B

• client outcomes listed, but not defined

against their current situation

• some technical knowledge shown

through the identification of

complications

• basic financial data used to explain

sections A & B

• no clear client outcomes or vague

explanation

• little or no evidence of understanding

the technical complications that may

arise in the advice process

• no financial calculations and data used

to explain sections A & B

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(a) Outline the outcomes that are important to the client. (5 marks)

This case study is concerned with Ida, who is a 75 year widowed women. Her husband has recently

expired and she has three children. Eric, Ida’s father expired at the age of 77 years and her three

children are John who is aged 51 years, Philip who is aged 48 years and Cheyenne who is aged 45

years. All the three children are impendent and out of them Philip and John have their own

families. On the other hand, Cheyenne has a problem with making relationships and therefore

have been married twice and currently have three children from her two husbands.

Ida is a retired lady and she has been living alone in the house that was earlier named after her

and her husband and after the death of her husband, she is the owner of the house. Ida being an

old lady has the main concern of generating adequate amount of money that would be helpful in

creating a healthy and sustainable life in the coming future. Ida wants to maintain a life and

maintain her standard of living equivalent to the lifestyle that she had prior to retirement age.

Ida has not undertaken several investments and purchase of insurance but has sufficient money

with the help of which she would be able to make investments in order to increase her level of

income. She has received a lump sum amount of $200,000 as an inheritance from the estate of her

late mother. She would like to make an effective investment of this amount she has received in

order to gain effective returns and thereby maintaining a lifestyle that is desired by Ida.

She is even worried about the superannuation fund of her husband as she is worried whether she

would be receiving the value that is available in the superannuation fund of her husband. She even

wants to know in case she receives the superannuation amount of her husband how would be

receive whether in lump sum or in monthly instalments. She has been advised that there are two

ways in which she can receive her husband’s superannuation and therefore she requires a

suggestions as to in which way she would like to receive the amount and which one of these

strategies would be more tax effective for Ida.

Ida is aged and therefore she may fall sick at a later stage of life and therefore it is important that

she purchases a healthcare insurance in order to meet any expenses that are related to health.

Ida has even found that after receiving the superannuation benefits it would even lead to smaller

amount of Age Pensions and therefore she requires assistance as to the strategies that can be

implemented with the help of which she would be able to increase her age pension amount.

Ida wants to give out her inheritance to her children equally and therefore requires assistance as

to in what manner her assets are distributed so that all of their children receive equal amount of

asset. As Cheyenne does not have stable relationship Ida is worried that the asset that would be

given to her would go to her next partner. Hence, Ida wants to make sure that her grandchildren

receives the benefits and therefore requires advice over the same. These are the aspects with

respect to which Ida requires assistance so that she would understand properly the advises that

would be tax effective for her and would have the minimum impact in order to increase the Age

Pension values.

(b) What are the issues/complications you have identified that may hamper the client’s

achieving their objectives? Provide financial data and calculations. (5 marks)

There are several issues and complications that may hamper the financial and the non-financial

goals of Ida. One of the essential issue that has been discovered for Ida has been the fact that Ida

does not have sufficient amount of investments and savings in the bank account and her main

source of income has been through superannuation fund. She does not have any other source of

income as she is retired and is mainly dependent on the money she receives from the

superannuation fund. Ida is satisfied about the fact that the money that is available in the

7

This case study is concerned with Ida, who is a 75 year widowed women. Her husband has recently

expired and she has three children. Eric, Ida’s father expired at the age of 77 years and her three

children are John who is aged 51 years, Philip who is aged 48 years and Cheyenne who is aged 45

years. All the three children are impendent and out of them Philip and John have their own

families. On the other hand, Cheyenne has a problem with making relationships and therefore

have been married twice and currently have three children from her two husbands.

Ida is a retired lady and she has been living alone in the house that was earlier named after her

and her husband and after the death of her husband, she is the owner of the house. Ida being an

old lady has the main concern of generating adequate amount of money that would be helpful in

creating a healthy and sustainable life in the coming future. Ida wants to maintain a life and

maintain her standard of living equivalent to the lifestyle that she had prior to retirement age.

Ida has not undertaken several investments and purchase of insurance but has sufficient money

with the help of which she would be able to make investments in order to increase her level of

income. She has received a lump sum amount of $200,000 as an inheritance from the estate of her

late mother. She would like to make an effective investment of this amount she has received in

order to gain effective returns and thereby maintaining a lifestyle that is desired by Ida.

She is even worried about the superannuation fund of her husband as she is worried whether she

would be receiving the value that is available in the superannuation fund of her husband. She even

wants to know in case she receives the superannuation amount of her husband how would be

receive whether in lump sum or in monthly instalments. She has been advised that there are two

ways in which she can receive her husband’s superannuation and therefore she requires a

suggestions as to in which way she would like to receive the amount and which one of these

strategies would be more tax effective for Ida.

Ida is aged and therefore she may fall sick at a later stage of life and therefore it is important that

she purchases a healthcare insurance in order to meet any expenses that are related to health.

Ida has even found that after receiving the superannuation benefits it would even lead to smaller

amount of Age Pensions and therefore she requires assistance as to the strategies that can be

implemented with the help of which she would be able to increase her age pension amount.

Ida wants to give out her inheritance to her children equally and therefore requires assistance as

to in what manner her assets are distributed so that all of their children receive equal amount of

asset. As Cheyenne does not have stable relationship Ida is worried that the asset that would be

given to her would go to her next partner. Hence, Ida wants to make sure that her grandchildren

receives the benefits and therefore requires advice over the same. These are the aspects with

respect to which Ida requires assistance so that she would understand properly the advises that

would be tax effective for her and would have the minimum impact in order to increase the Age

Pension values.

(b) What are the issues/complications you have identified that may hamper the client’s

achieving their objectives? Provide financial data and calculations. (5 marks)

There are several issues and complications that may hamper the financial and the non-financial

goals of Ida. One of the essential issue that has been discovered for Ida has been the fact that Ida

does not have sufficient amount of investments and savings in the bank account and her main

source of income has been through superannuation fund. She does not have any other source of

income as she is retired and is mainly dependent on the money she receives from the

superannuation fund. Ida is satisfied about the fact that the money that is available in the

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

superannuation fund would be able to meet any kind of unprecedented expenses but in case there

exists is an emergency situation the amount that is available may not be sufficient to meet the

expenses. It is seen that Ida is aged 75 years and therefore there can be scenarios that she may fall

sick, which may lead to rise in the amount of expenses. The daily expenses of Ida is very less

however on a regular basis, she goes for a National Senior coach trips and has even looked to go

for an organized European Heritage trip. In order to meet these expenses she may require

additional funds as well.

The term deposit that Ida has would be maturing in the next six months and therefore if the

money is not re-invested then it can hamper Ida as well. Even though Ida feels that she has

sufficient amount of value in the superannuation fund, but reduction in the Age Pension can have

an impact on their income and lifestyle. These are issues that can be faced by Ida.

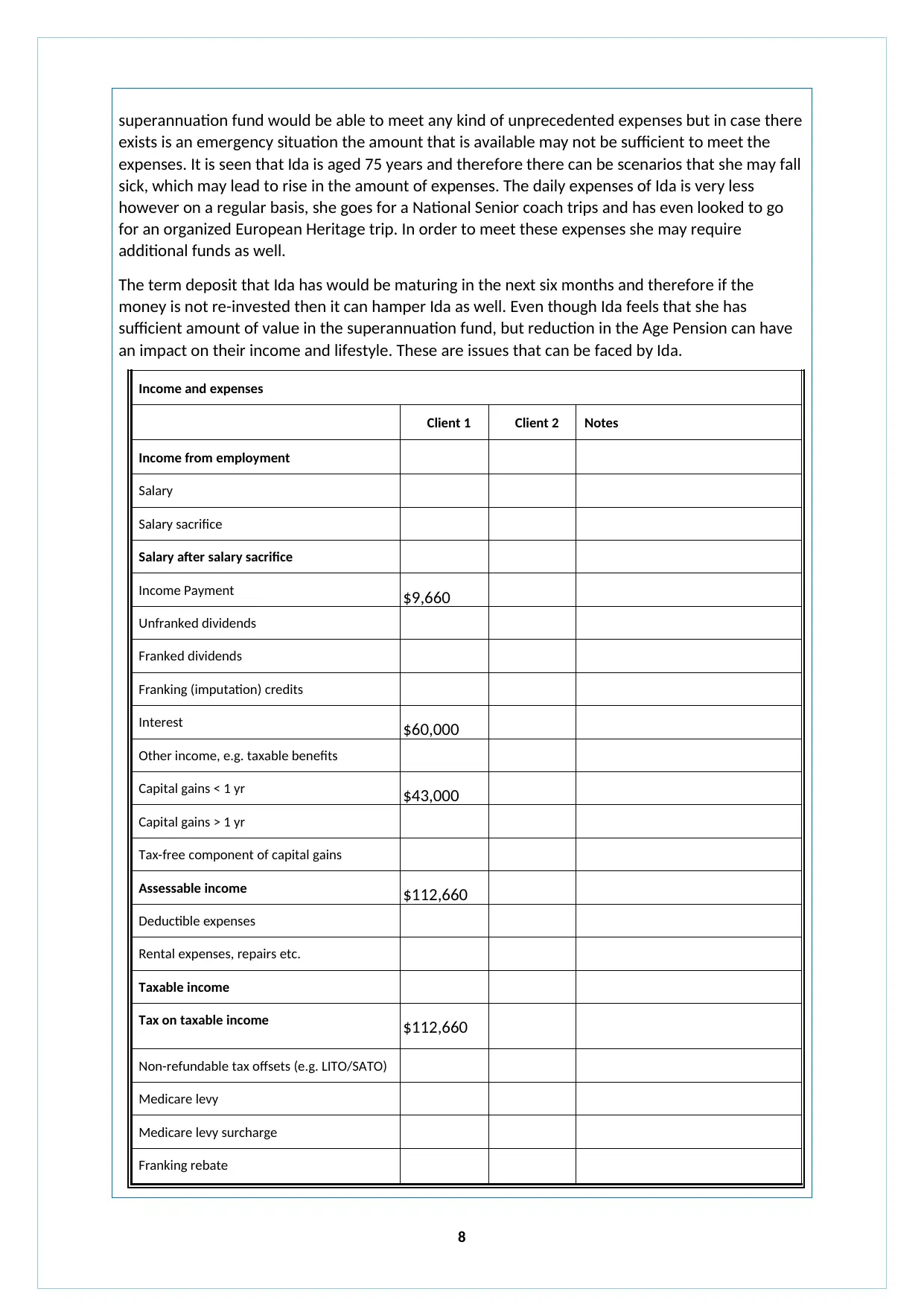

Income and expenses

Client 1 Client 2 Notes

Income from employment

Salary

Salary sacrifice

Salary after salary sacrifice

Income Payment $9,660

Unfranked dividends

Franked dividends

Franking (imputation) credits

Interest $60,000

Other income, e.g. taxable benefits

Capital gains < 1 yr $43,000

Capital gains > 1 yr

Tax-free component of capital gains

Assessable income $112,660

Deductible expenses

Rental expenses, repairs etc.

Taxable income

Tax on taxable income $112,660

Non-refundable tax offsets (e.g. LITO/SATO)

Medicare levy

Medicare levy surcharge

Franking rebate

8

exists is an emergency situation the amount that is available may not be sufficient to meet the

expenses. It is seen that Ida is aged 75 years and therefore there can be scenarios that she may fall

sick, which may lead to rise in the amount of expenses. The daily expenses of Ida is very less

however on a regular basis, she goes for a National Senior coach trips and has even looked to go

for an organized European Heritage trip. In order to meet these expenses she may require

additional funds as well.

The term deposit that Ida has would be maturing in the next six months and therefore if the

money is not re-invested then it can hamper Ida as well. Even though Ida feels that she has

sufficient amount of value in the superannuation fund, but reduction in the Age Pension can have

an impact on their income and lifestyle. These are issues that can be faced by Ida.

Income and expenses

Client 1 Client 2 Notes

Income from employment

Salary

Salary sacrifice

Salary after salary sacrifice

Income Payment $9,660

Unfranked dividends

Franked dividends

Franking (imputation) credits

Interest $60,000

Other income, e.g. taxable benefits

Capital gains < 1 yr $43,000

Capital gains > 1 yr

Tax-free component of capital gains

Assessable income $112,660

Deductible expenses

Rental expenses, repairs etc.

Taxable income

Tax on taxable income $112,660

Non-refundable tax offsets (e.g. LITO/SATO)

Medicare levy

Medicare levy surcharge

Franking rebate

8

Suggested word limit: up to 600 words.

9

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Question 2 Meeting client objectives (10 marks)

Criteria-based marking guide for Question 2

Excellent

(Mark range: 8–10 marks)

Satisfactory

(Mark range: 5–7.5 marks)

Unsatisfactory

(Mark range: 0–4.5 marks)

• clear set of solutions outlined to match

client objectives

• accurate use of financial calculations

and data to explain solutions

• correct identification of appropriate

strategies/solutions

• clear set of solutions outlined to

match client objectives

• basic technical workings shown to

explain solutions

• no clear solutions or vague explanation

• only bullet points used

• little or no technical workings shown

What are the possible solutions for achieving your client’s goals?

There are several solutions that can be given to the client based on the goals and the aims of the

students and therefore one should take extensive measures with the help of which Ida can satisfy

their needs and goals. One of the essential goals of Ida is to maintain adequate level of income

that would be effective in maintaining their normal lifestyle eve in the future. In order to do the

same, Ida needs to purchase certain investments according to her notions and perspectives and

thereby these investments would be able to provide returns that would could be used by Ida in

order to meet her daily expenses and maintain her general living standards. There are numerous

investment plans and products that are available in the market and the ideal product would be

suggested to Ida based on her goals and objectives.

Ida is an aged lady and therefore there are circumstances that she may fall sick that may increase

her expenses. It is therefore essential that Ida purchases a healthcare insurances that would be

effective enough in order to pay for the expenses that she may incur for treating her health.

Ida has received an amount from inheritance of her mother’s estate and Ida want to make

investments from that money in order to earn additional returns that would enhance her level of

income. This money would be invested in such a manner so that Ida would receive the highest

amount of returns by paying for the minimum amount of tax.

An effective level of advice needs to be given to the client with respect to superannuation benefits

she would receive as a beneficiary of Eric. In this circumstances, if Ida receives the money on the

basis of the income stream of Eric, then Ida would receive better returns from the superannuation

of Eric and the amount of tax that would be levied on this money would be lower and effective.

Ida is even concerned that there might be a reduction in her age pension and therefore in order to

balance the amount that has been lost in the age pension Ida needs to undertake additional

investments. The investments can be undertaken by looking at the market and the amount of

interest and the risk that is associated with it so that Ida can increase their level of returns and

maintain their current lifestyle.

Ida needs to take suggestions from her accountants and solicitors with the help of which she can

have an idea of dividing her assets on an equal basis with the help of which all her children would

receive her assets on an equal basis. Ida even wants to ensure that her grandchildren receives the

benefits from her assets and therefore the part that would be given to Cheyenne would be

distributed among her three children so that Cheyenne is unable to transfer the asset to her next

partner. As Cheyenne’s children are dependent therefore indirectly Cheyenne would be able to

handle the money until her children are matured.

10

Criteria-based marking guide for Question 2

Excellent

(Mark range: 8–10 marks)

Satisfactory

(Mark range: 5–7.5 marks)

Unsatisfactory

(Mark range: 0–4.5 marks)

• clear set of solutions outlined to match

client objectives

• accurate use of financial calculations

and data to explain solutions

• correct identification of appropriate

strategies/solutions

• clear set of solutions outlined to

match client objectives

• basic technical workings shown to

explain solutions

• no clear solutions or vague explanation

• only bullet points used

• little or no technical workings shown

What are the possible solutions for achieving your client’s goals?

There are several solutions that can be given to the client based on the goals and the aims of the

students and therefore one should take extensive measures with the help of which Ida can satisfy

their needs and goals. One of the essential goals of Ida is to maintain adequate level of income

that would be effective in maintaining their normal lifestyle eve in the future. In order to do the

same, Ida needs to purchase certain investments according to her notions and perspectives and

thereby these investments would be able to provide returns that would could be used by Ida in

order to meet her daily expenses and maintain her general living standards. There are numerous

investment plans and products that are available in the market and the ideal product would be

suggested to Ida based on her goals and objectives.

Ida is an aged lady and therefore there are circumstances that she may fall sick that may increase

her expenses. It is therefore essential that Ida purchases a healthcare insurances that would be

effective enough in order to pay for the expenses that she may incur for treating her health.

Ida has received an amount from inheritance of her mother’s estate and Ida want to make

investments from that money in order to earn additional returns that would enhance her level of

income. This money would be invested in such a manner so that Ida would receive the highest

amount of returns by paying for the minimum amount of tax.

An effective level of advice needs to be given to the client with respect to superannuation benefits

she would receive as a beneficiary of Eric. In this circumstances, if Ida receives the money on the

basis of the income stream of Eric, then Ida would receive better returns from the superannuation

of Eric and the amount of tax that would be levied on this money would be lower and effective.

Ida is even concerned that there might be a reduction in her age pension and therefore in order to

balance the amount that has been lost in the age pension Ida needs to undertake additional

investments. The investments can be undertaken by looking at the market and the amount of

interest and the risk that is associated with it so that Ida can increase their level of returns and

maintain their current lifestyle.

Ida needs to take suggestions from her accountants and solicitors with the help of which she can

have an idea of dividing her assets on an equal basis with the help of which all her children would

receive her assets on an equal basis. Ida even wants to ensure that her grandchildren receives the

benefits from her assets and therefore the part that would be given to Cheyenne would be

distributed among her three children so that Cheyenne is unable to transfer the asset to her next

partner. As Cheyenne’s children are dependent therefore indirectly Cheyenne would be able to

handle the money until her children are matured.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Ida with the help of her adviser can take measures with respect to which her investments would

be allocated in an effective manner in various assets so that the extent of risk gets reduced and the

extent of return is maintained. The investments should be assessed from time to time so that any

kind of discrepancies like losses is observed from the investment can be mitigated. This is done

due to the fact that in case one of the assets are not performing in effectively then it can be

changed with another product that would provide better returns. These are the probable solutions

in order to attain the goals of Ida.

Suggested word limit: up to 600 words.

11

be allocated in an effective manner in various assets so that the extent of risk gets reduced and the

extent of return is maintained. The investments should be assessed from time to time so that any

kind of discrepancies like losses is observed from the investment can be mitigated. This is done

due to the fact that in case one of the assets are not performing in effectively then it can be

changed with another product that would provide better returns. These are the probable solutions

in order to attain the goals of Ida.

Suggested word limit: up to 600 words.

11

Question 3 Technical workings (25 marks)

Criteria-based marking guide for Question 3

Excellent

(Mark range: 20–25 marks)

Satisfactory

(Mark range: 12.5–19 marks)

Unsatisfactory

(Mark range: 0–12 marks)

• well-articulated and easy to follow

advice process

• accurate use of financial calculations and

data

• use of appropriate mix of both imitated

conversation and explanatory writing

• well-articulated and easy to follow

advice process

• Basic technical workings shown to

explain solutions

• no clear solutions or vague explanation

• only bullet points used

• little or no technical workings shown

Detail the way in which you would explain your proposed solution to your client. You must include

all of the required technical workings/calculations for your proposed solution. This should be in

your own words and presented in a manner as if the client was in an appointment with you.

Note: This should detail to the client what the solutions are, how they are meeting their objectives

and the way in which the solution will be implemented.

Dear Ida,

I would like to thank you for taking my assistance with respect to the financial advices that you

require. You are retired and therefore require undertaking a meeting with you is essential in order

to have an idea about your goals and desires. By understanding your desires and ants, it would be

helpful for me in creating a financial structure that would be ideal for you and would provide you

with the returns that is desirable to you. The construction of an effective financial and investment

plan would be helpful in gaining proper savings and income from the investments that can be

utilized in order to pay for the general expenses and the expenses that would be incurred in the

coming time period.

This meeting would be fruitful in generating knowledge and understanding of the actual and the

future risks that may take place at any point of time in the future. The meeting would be helpful in

creating knowledge and understanding of the steps and the actions that needs to be followed and

the policies and strategies that is associated to tax savings and investment by taking assistance of

which you would be able to have a safe, comfortable and secured in the coming time period.

In the primary stage of the meeting it is vital to create knowledge on the areas and the topics that

would be addressed in this meeting so that all the concerns and the issues can be met in an

effective manner. It is seen that the key aim of Ida has been to create a retirement plan as she is

aged 75 years and she lives alone in her house. She needs to preserve a minimal amount which she

would feel is adequate in order to pay her general expenses during the current time period and

even in the future. Ida has a feeling that amount in the superannuation fund is adequate in order

to meet any kind of unprecedented events however, in order to maintain a surplus capital for any

accidents and events it is essential for Ida to create additional cash from the further investments.

The next aspect that would be taken into consideration is the tax effective characteristics of the

investments that would be undertaken so that Ida can enhance her income by paying off the least

amount of tax. A discussion regarding the superannuation needs to be undertaken so that an

understanding can be attained with respect to whether the superannuation amount that is

currently available to Ida would be adequate in meeting her future expenses. A discussion would

be undertaken with respect to the kind of additional investments that would be undertaken by Ida

with the help of the money she received from her mother so as to increase her income level. The

12

Criteria-based marking guide for Question 3

Excellent

(Mark range: 20–25 marks)

Satisfactory

(Mark range: 12.5–19 marks)

Unsatisfactory

(Mark range: 0–12 marks)

• well-articulated and easy to follow

advice process

• accurate use of financial calculations and

data

• use of appropriate mix of both imitated

conversation and explanatory writing

• well-articulated and easy to follow

advice process

• Basic technical workings shown to

explain solutions

• no clear solutions or vague explanation

• only bullet points used

• little or no technical workings shown

Detail the way in which you would explain your proposed solution to your client. You must include

all of the required technical workings/calculations for your proposed solution. This should be in

your own words and presented in a manner as if the client was in an appointment with you.

Note: This should detail to the client what the solutions are, how they are meeting their objectives

and the way in which the solution will be implemented.

Dear Ida,

I would like to thank you for taking my assistance with respect to the financial advices that you

require. You are retired and therefore require undertaking a meeting with you is essential in order

to have an idea about your goals and desires. By understanding your desires and ants, it would be

helpful for me in creating a financial structure that would be ideal for you and would provide you

with the returns that is desirable to you. The construction of an effective financial and investment

plan would be helpful in gaining proper savings and income from the investments that can be

utilized in order to pay for the general expenses and the expenses that would be incurred in the

coming time period.

This meeting would be fruitful in generating knowledge and understanding of the actual and the

future risks that may take place at any point of time in the future. The meeting would be helpful in

creating knowledge and understanding of the steps and the actions that needs to be followed and

the policies and strategies that is associated to tax savings and investment by taking assistance of

which you would be able to have a safe, comfortable and secured in the coming time period.

In the primary stage of the meeting it is vital to create knowledge on the areas and the topics that

would be addressed in this meeting so that all the concerns and the issues can be met in an

effective manner. It is seen that the key aim of Ida has been to create a retirement plan as she is

aged 75 years and she lives alone in her house. She needs to preserve a minimal amount which she

would feel is adequate in order to pay her general expenses during the current time period and

even in the future. Ida has a feeling that amount in the superannuation fund is adequate in order

to meet any kind of unprecedented events however, in order to maintain a surplus capital for any

accidents and events it is essential for Ida to create additional cash from the further investments.

The next aspect that would be taken into consideration is the tax effective characteristics of the

investments that would be undertaken so that Ida can enhance her income by paying off the least

amount of tax. A discussion regarding the superannuation needs to be undertaken so that an

understanding can be attained with respect to whether the superannuation amount that is

currently available to Ida would be adequate in meeting her future expenses. A discussion would

be undertaken with respect to the kind of additional investments that would be undertaken by Ida

with the help of the money she received from her mother so as to increase her income level. The

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.