Critically Analyze and Evaluate Key Audit Matters in the Independent Auditors Report

VerifiedAdded on 2022/11/24

|20

|3547

|469

AI Summary

This report critically analyzes and evaluates the key audit matters in the independent auditors report. It discusses the rationale and purpose of key audit matters, the requirement and application of key audit matters, the Lehman Brothers case issue, and the importance of going concern for auditors. The report also evaluates the efficiency of reporting key audit matters in the chosen banks.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CRITICALLY ANALYZE AND EVALUATE KEY AUDIT MATTERS IN

THE INDEPENDENT AUDITORS REPORT

Critically analyze and evaluate key audit matters in the independent auditors report

Name of the student

Name of the university

Student ID

Author note

THE INDEPENDENT AUDITORS REPORT

Critically analyze and evaluate key audit matters in the independent auditors report

Name of the student

Name of the university

Student ID

Author note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CRITICALLY ANALYZE AND EVALUATE KEY AUDIT MATTERS IN THE

INDEPENDENT AUDITORS REPORT

Executive summary:

The report demonstrates an understanding of the new auditing standard ASA 701

communicating key auditor matter in the independent auditor report. With regard to this, the

key audit matters of the companies listed in the consumer discretionary sector of Australia

stock exchange has been analyzed. These companies include JB Hi-Fi, Tabcorp holding

limited, Aristocrat leisure limited, Wesfarmers limited and Nine entertainment. It has been

ascertained from the analysis of the key audit matters of all companies that the users and

investors are provided with the transparent information and enable them to make strategic

investment decision.

INDEPENDENT AUDITORS REPORT

Executive summary:

The report demonstrates an understanding of the new auditing standard ASA 701

communicating key auditor matter in the independent auditor report. With regard to this, the

key audit matters of the companies listed in the consumer discretionary sector of Australia

stock exchange has been analyzed. These companies include JB Hi-Fi, Tabcorp holding

limited, Aristocrat leisure limited, Wesfarmers limited and Nine entertainment. It has been

ascertained from the analysis of the key audit matters of all companies that the users and

investors are provided with the transparent information and enable them to make strategic

investment decision.

CRITICALLY ANALYZE AND EVALUATE KEY AUDIT MATTERS IN THE

INDEPENDENT AUDITORS REPORT

Table of Contents

Introduction:...............................................................................................................................3

Discussion:.................................................................................................................................4

Rationale and purpose of key audit matters:..............................................................................4

Requirement and application of key audit matter:.....................................................................5

Lehman brother case issue:........................................................................................................5

How key audit matters would have addressed the issue:...........................................................6

Revision of ASA 570:................................................................................................................6

Importance of going concern for auditors:.................................................................................7

Evaluating the efficiency of reporting of key audit matters of the chosen banks:.....................7

Does key audit matters achieved the purpose in the industry:.................................................11

Conclusion:..............................................................................................................................11

References list:.........................................................................................................................12

Appendix:.................................................................................................................................15

INDEPENDENT AUDITORS REPORT

Table of Contents

Introduction:...............................................................................................................................3

Discussion:.................................................................................................................................4

Rationale and purpose of key audit matters:..............................................................................4

Requirement and application of key audit matter:.....................................................................5

Lehman brother case issue:........................................................................................................5

How key audit matters would have addressed the issue:...........................................................6

Revision of ASA 570:................................................................................................................6

Importance of going concern for auditors:.................................................................................7

Evaluating the efficiency of reporting of key audit matters of the chosen banks:.....................7

Does key audit matters achieved the purpose in the industry:.................................................11

Conclusion:..............................................................................................................................11

References list:.........................................................................................................................12

Appendix:.................................................................................................................................15

CRITICALLY ANALYZE AND EVALUATE KEY AUDIT MATTERS IN THE

INDEPENDENT AUDITORS REPORT

Introduction:

The report is prepared to analyze and evaluate the key audit matters of the

independent auditor report of the companies that have been chosen from the list of Australian

stock exchange. For conducting an analysis on the key audit matters of different companies, it

is essential to take into accounts the facts presented under the new auditing standard ASA

701 for communication key audit maters in the independent report. The introduction of the

new auditing standard was in the wake of global financial crisis due to the failure of some

organization resulting from issuing unqualified audit report. The new auditing standard

intends to enhance the auditor report because so that the investors are provided with true and

fair view of the financial performance of the company. In this regard, the case of Lehman

brother has been evaluated along with identifying the issue of going concern with the revision

of ASA 570. It is also required by the auditor to draw their attention on the ability of the

reporting entity to continue as going concern. Key audit matters are the items ascertained

from the financial statement of the reporting entity that considerably influence the auditing of

the financial statements according to the professional judgment of the auditors

(Legislation.gov.au 2019). The importance of auditor to account for the issues associated

with the going concern is also evaluated and presented in the report.

Discussion:

Rationale and purpose of key audit matters:

It is the responsibility of the auditors to communicate the key audit matters that they

have ascertained in the auditor report as it intends to address the judgment of auditor as to

which should be communicated in the report along with the content and form of such

communication. Communicating the key audit matters help in providing greater transparency

and thereby contribute in enhancing the auditor’ report communicative value. The intended

users of the auditor also received great assistance in understanding the areas of significant

judgment made by management and entity as a whole. In addition to this, users are provided a

basis for furthering engaging with the people charged with governance and those with the

management (Auasb.gov.au 2019).

Requirement and application of key audit matter:

The reporting entity is required to present the key audit matters in their annual or

financial report as such matters are considered to be of relevance in the process of decision

making. It is due to the fact that such matters tends to create a material impact on the

financial statements and thereby results in the material misstatement due to existence of

materiality in the identified account. Therefore, it is required by the auditor to make reporting

of the key audit matters for enhancing the decision making process of investors.

From researching several papers, it has been ascertained that key audit matters have

provided numerous benefits in terms of benefits to the audit process, good governance and

financial reporting benefits. Hence, in light of these benefits, it can be inferred that the

identification of key audit matters by auditors would help in improving the several areas of

reporting entity and it generates a positive impact on the reporting process of entity. With

regard to the audit issues, the key audit matters helps in creating transparency between the

discussion of such issues between the audit committee and auditor along with creating a

positive impact on the audit quality (Auasb.gov.au 2019).

INDEPENDENT AUDITORS REPORT

Introduction:

The report is prepared to analyze and evaluate the key audit matters of the

independent auditor report of the companies that have been chosen from the list of Australian

stock exchange. For conducting an analysis on the key audit matters of different companies, it

is essential to take into accounts the facts presented under the new auditing standard ASA

701 for communication key audit maters in the independent report. The introduction of the

new auditing standard was in the wake of global financial crisis due to the failure of some

organization resulting from issuing unqualified audit report. The new auditing standard

intends to enhance the auditor report because so that the investors are provided with true and

fair view of the financial performance of the company. In this regard, the case of Lehman

brother has been evaluated along with identifying the issue of going concern with the revision

of ASA 570. It is also required by the auditor to draw their attention on the ability of the

reporting entity to continue as going concern. Key audit matters are the items ascertained

from the financial statement of the reporting entity that considerably influence the auditing of

the financial statements according to the professional judgment of the auditors

(Legislation.gov.au 2019). The importance of auditor to account for the issues associated

with the going concern is also evaluated and presented in the report.

Discussion:

Rationale and purpose of key audit matters:

It is the responsibility of the auditors to communicate the key audit matters that they

have ascertained in the auditor report as it intends to address the judgment of auditor as to

which should be communicated in the report along with the content and form of such

communication. Communicating the key audit matters help in providing greater transparency

and thereby contribute in enhancing the auditor’ report communicative value. The intended

users of the auditor also received great assistance in understanding the areas of significant

judgment made by management and entity as a whole. In addition to this, users are provided a

basis for furthering engaging with the people charged with governance and those with the

management (Auasb.gov.au 2019).

Requirement and application of key audit matter:

The reporting entity is required to present the key audit matters in their annual or

financial report as such matters are considered to be of relevance in the process of decision

making. It is due to the fact that such matters tends to create a material impact on the

financial statements and thereby results in the material misstatement due to existence of

materiality in the identified account. Therefore, it is required by the auditor to make reporting

of the key audit matters for enhancing the decision making process of investors.

From researching several papers, it has been ascertained that key audit matters have

provided numerous benefits in terms of benefits to the audit process, good governance and

financial reporting benefits. Hence, in light of these benefits, it can be inferred that the

identification of key audit matters by auditors would help in improving the several areas of

reporting entity and it generates a positive impact on the reporting process of entity. With

regard to the audit issues, the key audit matters helps in creating transparency between the

discussion of such issues between the audit committee and auditor along with creating a

positive impact on the audit quality (Auasb.gov.au 2019).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CRITICALLY ANALYZE AND EVALUATE KEY AUDIT MATTERS IN THE

INDEPENDENT AUDITORS REPORT

Lehman brother case issue:

The collapse of Lehman brother is considered as one of the largest failure in the

financial system of the world and one of the reasons cited for the collapse and investors

losing money was their ineffective auditing policies laid down by the old auditing standard.

The auditors of Lehman brother conducted audit in accordance with the requirement of the

old auditing standard that did not provide assistance to the users in fully understanding the

financial position of the entity and the collapse of the organization was instigated eventually.

The defective accounting policy named Repo 105 implemented by the large investment bank

was not investigated and verified by the auditors and a qualified audit opinion was issued on

their prepared financial report. The commitment of the bank towards the subprime loans was

not reviewed due to the negligence of the auditors and they failed to make long term

projections considering the risks and market uncertainties. Moreover, the excess borrowing

should be reported by the auditors and their incapability to reflect the true view of the

financial information of bank. This resulted in improving the standard of auditing that

required identification and reporting of the key audit matters in the annual report of the

entities. In addition to this, reviewing of the auditing standard and the introduction of ASA

701 was also motivated due to the global financial crisis.

How key audit matters would have addressed the issue:

The new auditing standard intends to address judgment of auditors regarding what

should be communicated in the auditor’s report. Identification of the key audit matters would

have enhanced the transparency of the report by highlighting the areas of higher assessed risk

of material misstatement or areas of significant risk in accordance with the auditing standard.

Moreover, the areas involving significant judgment by the management of entity such as

uncertainty, estimates and accounting estimates would have been evaluated by the auditors

forming significant judgment. Therefore, under the current auditing standard 701, auditors

would have been able to identify the areas requiring their professional judgment and the

matters that are significant and requires the users to apply their judgment in evaluating the

accounts. Thus, the users of the financial report would have been alerted on the key audit

matters and helped them in making better strategic investment.

Revision of ASA 570:

The failure of several organizations and the event of global financial crisis have made

the investors acquainted with the issues of the capability of organization to continue as going

concern. The auditor report should conduct an assessment of the going concern of the entities

by disclosing of the matters associated with the going concern where it is applicable. In

addition to this, it is required by the auditor to determine and evaluate the appropriateness of

accounting for going concern. The use of going concern accounting by the management

should be concluded by the auditor that is one of the enhanced descriptions regarding their

responsibilities. It is also required by the auditor to identify and report any material

uncertainty associated with the going concern.

Importance of going concern for auditors:

The ability of reporting entity to continue as going concern should be evaluated and

analyzed by the auditors. In the event of any entity using an inappropriate use of assumption

of the going concern would result the auditor in issuing an adverse opinion on the financial

statements issued. Therefore, they are required to obtain sufficient and appropriate audit

evidences about the assumptions used by the management to continue as going concern. In

INDEPENDENT AUDITORS REPORT

Lehman brother case issue:

The collapse of Lehman brother is considered as one of the largest failure in the

financial system of the world and one of the reasons cited for the collapse and investors

losing money was their ineffective auditing policies laid down by the old auditing standard.

The auditors of Lehman brother conducted audit in accordance with the requirement of the

old auditing standard that did not provide assistance to the users in fully understanding the

financial position of the entity and the collapse of the organization was instigated eventually.

The defective accounting policy named Repo 105 implemented by the large investment bank

was not investigated and verified by the auditors and a qualified audit opinion was issued on

their prepared financial report. The commitment of the bank towards the subprime loans was

not reviewed due to the negligence of the auditors and they failed to make long term

projections considering the risks and market uncertainties. Moreover, the excess borrowing

should be reported by the auditors and their incapability to reflect the true view of the

financial information of bank. This resulted in improving the standard of auditing that

required identification and reporting of the key audit matters in the annual report of the

entities. In addition to this, reviewing of the auditing standard and the introduction of ASA

701 was also motivated due to the global financial crisis.

How key audit matters would have addressed the issue:

The new auditing standard intends to address judgment of auditors regarding what

should be communicated in the auditor’s report. Identification of the key audit matters would

have enhanced the transparency of the report by highlighting the areas of higher assessed risk

of material misstatement or areas of significant risk in accordance with the auditing standard.

Moreover, the areas involving significant judgment by the management of entity such as

uncertainty, estimates and accounting estimates would have been evaluated by the auditors

forming significant judgment. Therefore, under the current auditing standard 701, auditors

would have been able to identify the areas requiring their professional judgment and the

matters that are significant and requires the users to apply their judgment in evaluating the

accounts. Thus, the users of the financial report would have been alerted on the key audit

matters and helped them in making better strategic investment.

Revision of ASA 570:

The failure of several organizations and the event of global financial crisis have made

the investors acquainted with the issues of the capability of organization to continue as going

concern. The auditor report should conduct an assessment of the going concern of the entities

by disclosing of the matters associated with the going concern where it is applicable. In

addition to this, it is required by the auditor to determine and evaluate the appropriateness of

accounting for going concern. The use of going concern accounting by the management

should be concluded by the auditor that is one of the enhanced descriptions regarding their

responsibilities. It is also required by the auditor to identify and report any material

uncertainty associated with the going concern.

Importance of going concern for auditors:

The ability of reporting entity to continue as going concern should be evaluated and

analyzed by the auditors. In the event of any entity using an inappropriate use of assumption

of the going concern would result the auditor in issuing an adverse opinion on the financial

statements issued. Therefore, they are required to obtain sufficient and appropriate audit

evidences about the assumptions used by the management to continue as going concern. In

CRITICALLY ANALYZE AND EVALUATE KEY AUDIT MATTERS IN THE

INDEPENDENT AUDITORS REPORT

addition to this, they are also required to make conclusion on the existence of material

uncertainty concerning the ability of entity to continue as going concern.

Evaluating the efficiency of reporting of key audit matters of the chosen banks:

This section demonstrates the analysis of the key audit matters from the financial

report of the companies in the consumer discretionary sector such as JB Hi-Fi, Tabcorp

holding limited, Aristocrat leisure limited, Wesfarmers limited and Nine entertainment. The

key audit maters of all the reporting entities chosen were addressed by the auditors in the

context of the audit of the financial report for the financial year 2018.

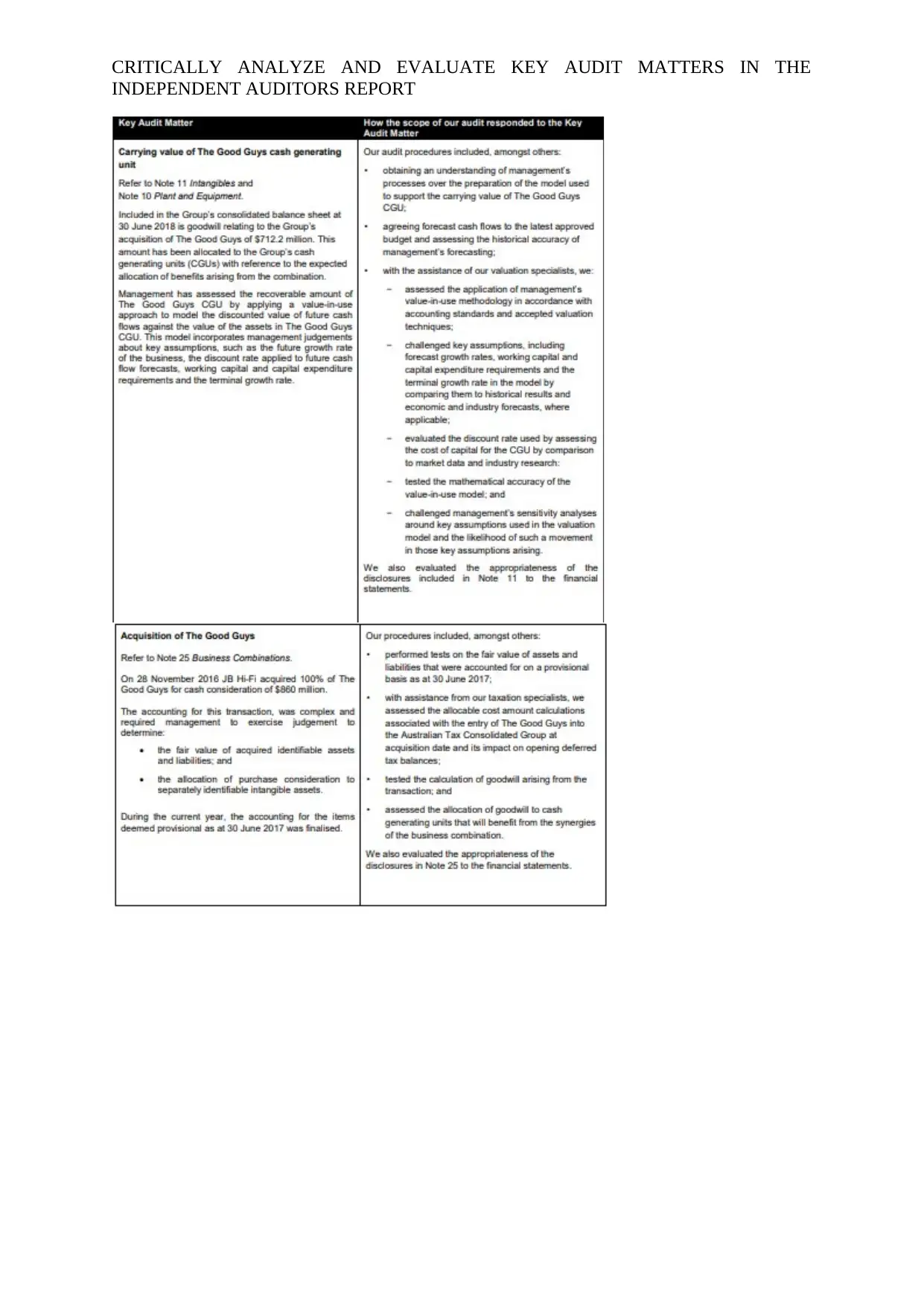

The auditor of JB Hi-Fi limited is Deloitte which identified two key audit matters

named acquisition of the good guys and carrying value of the good guys in the cash

generating unit while assessing the financial information provided by the company. The

details of such accounts have been detailed in the notes to financial statements such as note

10, 11 and 25. Such accounts were considered as key audit matters because of the judgment

of the management in estimating the amount and complexities involved in the valuation. The

appropriateness of the disclosures relating to such accounts was identified by the auditors by

employing the procedures such as performing the tests and assessing the methodology of

value in use. The model was tested for its accuracy by developing the appropriate test of

controls (member.afraccess.com 2019).

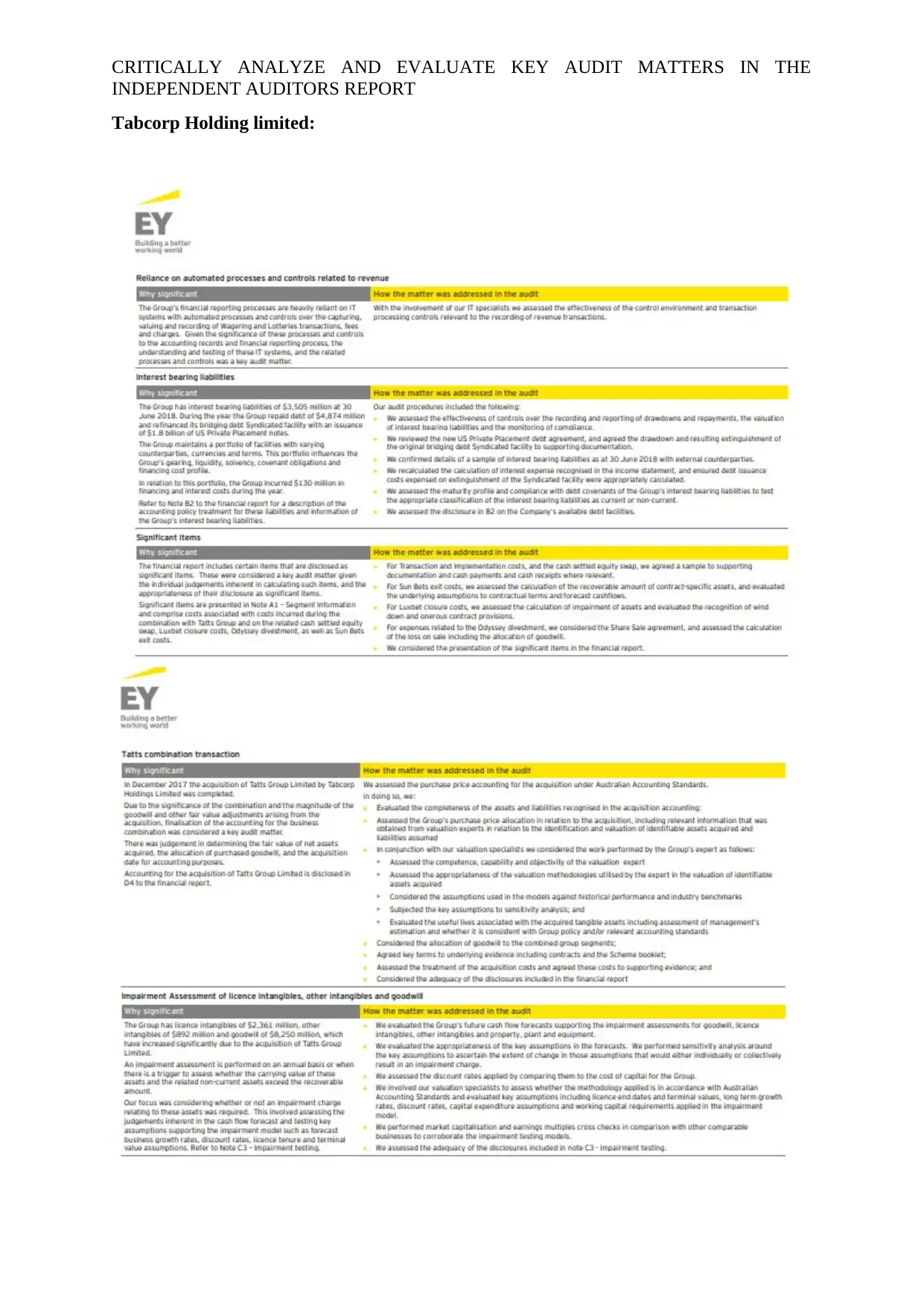

When looking at the annual report of Tabcorp Holding limited that Ernst and Young

have identified the key audit matters and have adopted proper procedures in addressing such

matters. The combination transaction of Tabcorp after the acquisition of Tatts group was

considered as key audit matters because of the judgment of the management in determining

its value. In this regard, the assessment of the purchase price accounting was done by the

auditor. Some other identified key audit maters include assessment of impairment for license

intangibles and goodwill, interest bearing abilities and reliance on the automated control and

process related to revenue. Assessment of all such matters was done by developing the

appropriate audit procedure. The auditors have also presented adequate reasons why the

matter is considered to have a material impact on the statements. From the section of key

audit matters in the financial report of Tabcorp limited, it has been ascertained that the

auditor have addressed all the key audit matters in separate section along with the addressing

all such matters using appropriate procedures. They have formed the opinion on the

presentation of the financial statements by determining the materiality and thereby providing

investors with transparency (Tabcorp.com.au 2019).

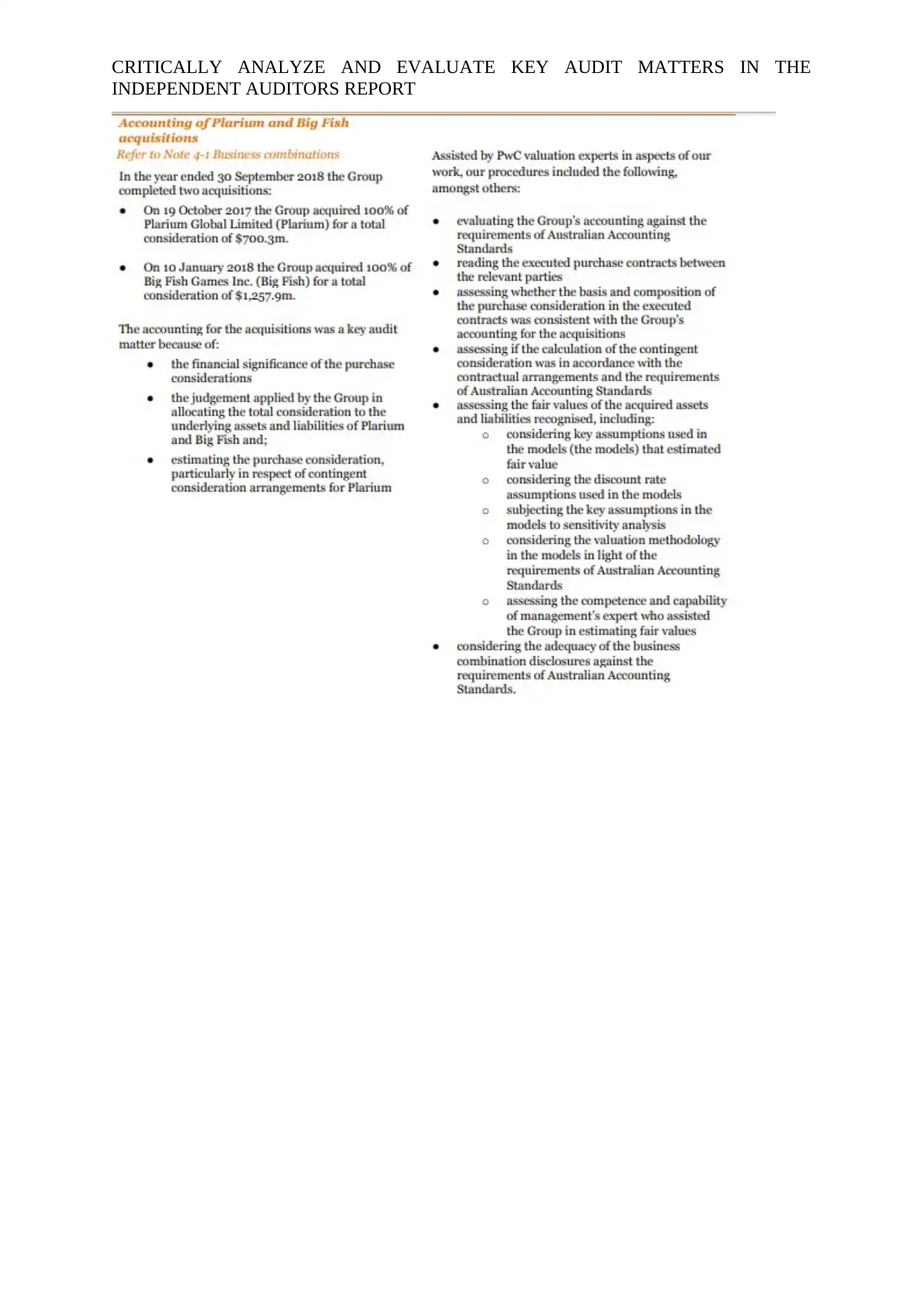

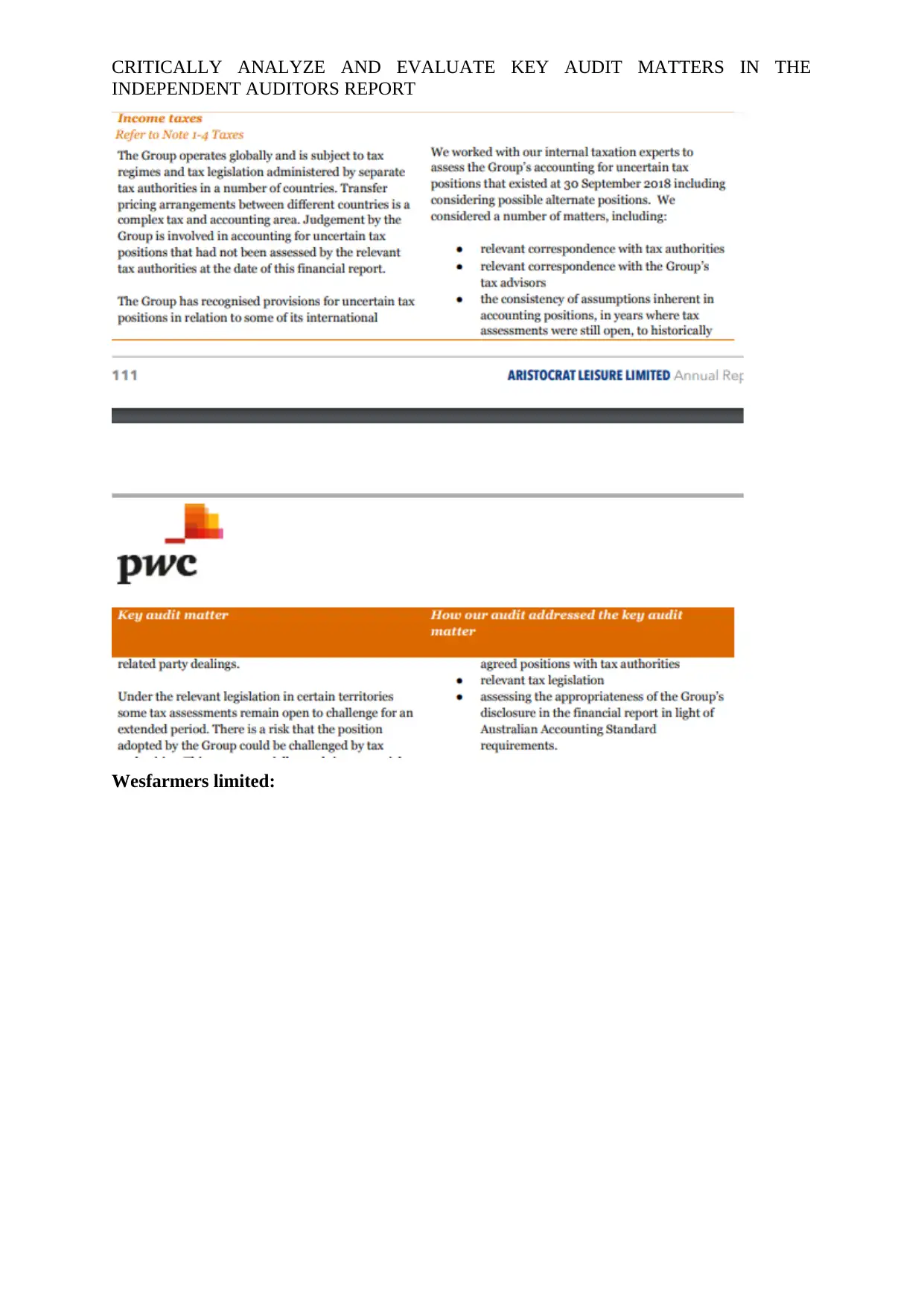

The annual report of the Aristocrat leisure limited has a separate section of the key

audit matter reported by its auditor Pwc. Key audit matters identified by auditors are income

tax, recognition of revenue, estimating recoverable amount of goodwill and accounting for

big fish and plarium acquisition. In addition to this, auditors have presented the proper reason

associated why the matter is regarded as key audit matter. Income tax is considered as key

audit matter because of the judgment involved in accounting for some uncertain tax positions

which the taxation authorities have not assessed. All the identified key audit matters have

been addressed by developing an in depth understanding of the system and developing the

test of controls (Ir.aristocrat.com 2019). The accounting of the group is evaluated against the

Australian accounting standard. The details of key audit matters are also identified by making

reference to the notes to the financial statements.

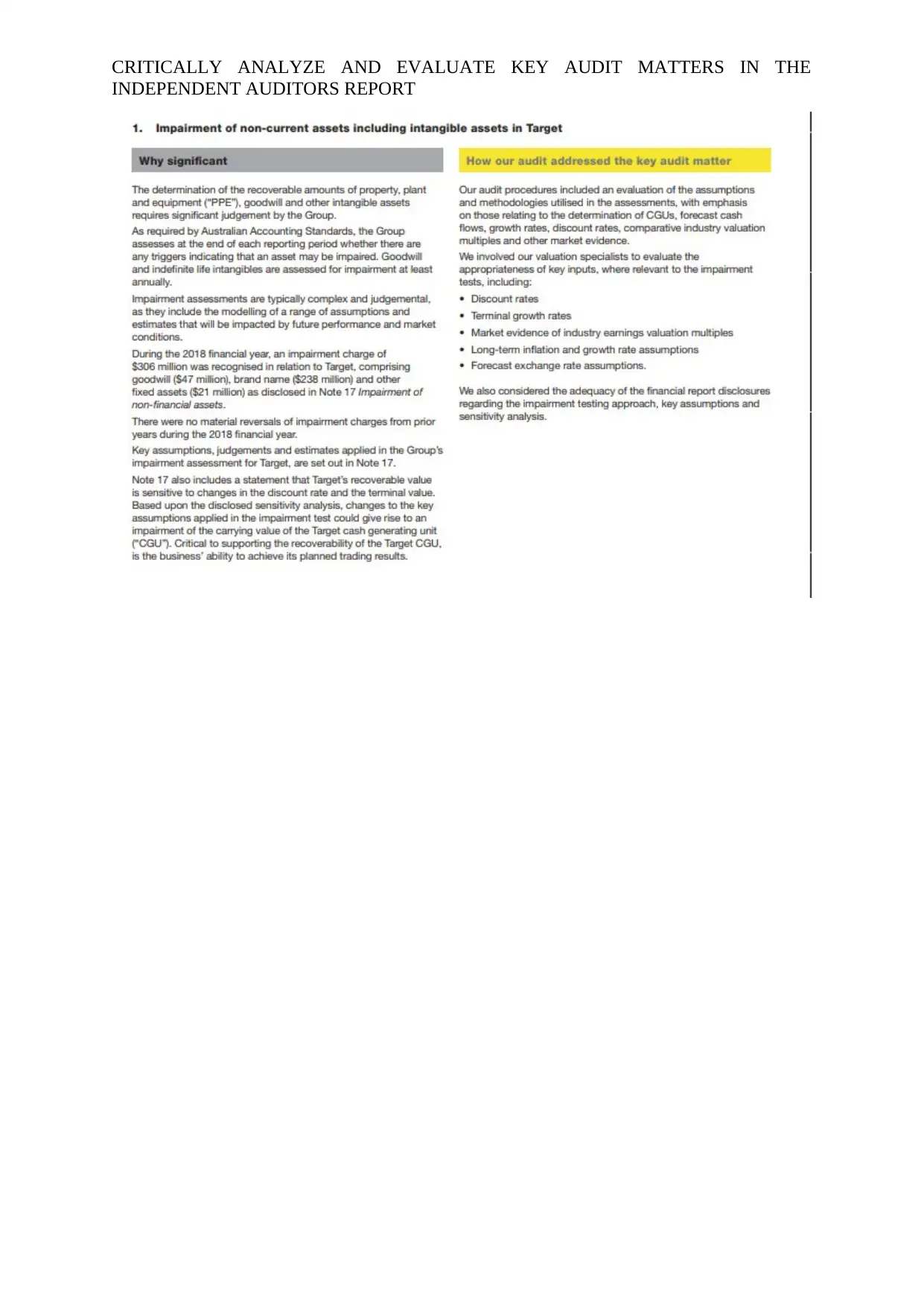

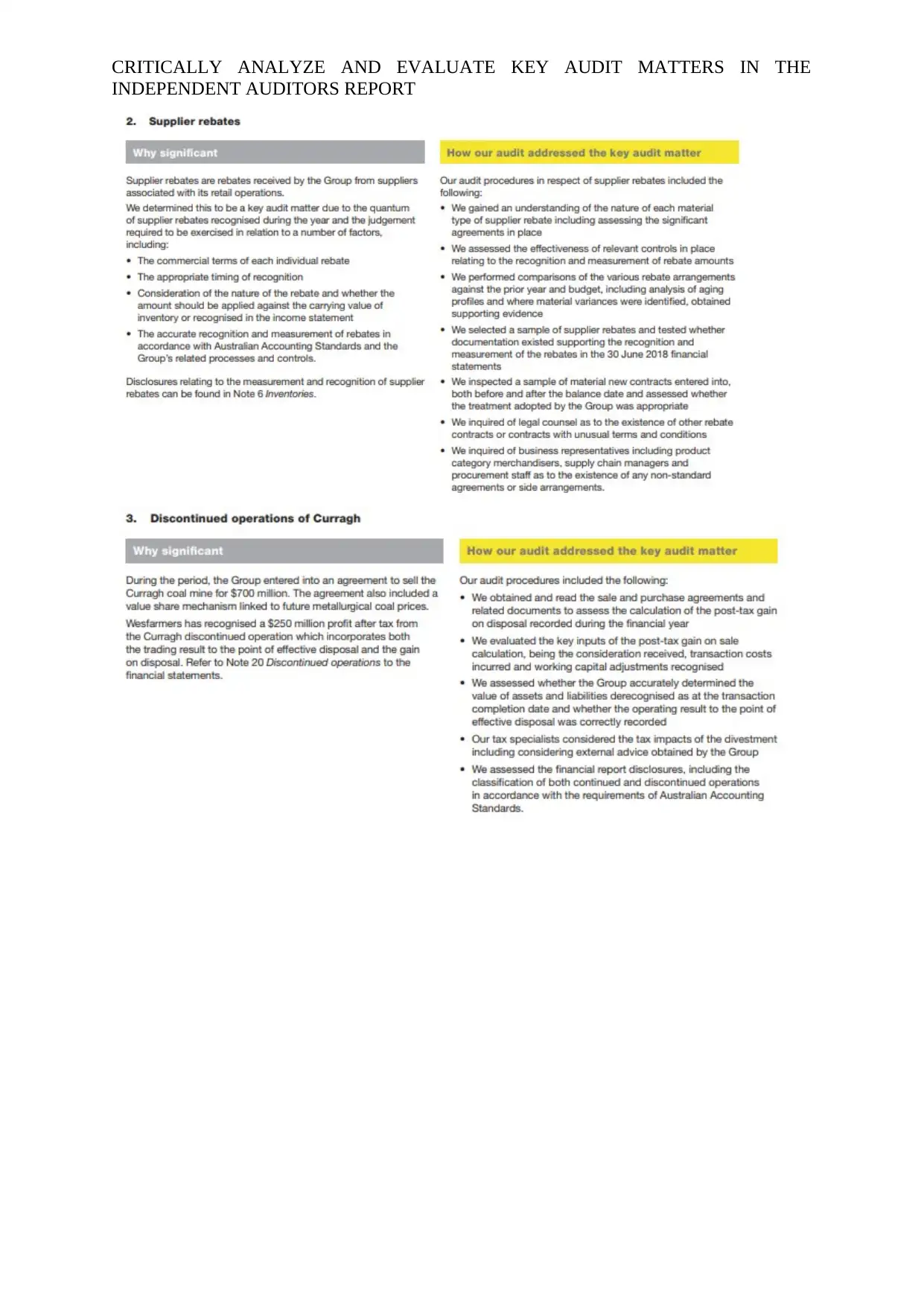

The auditors of Wesfarmers have identified some of the key matters for which they do

not provide separate opinion. However, a detailed description of how all the identified audit

INDEPENDENT AUDITORS REPORT

addition to this, they are also required to make conclusion on the existence of material

uncertainty concerning the ability of entity to continue as going concern.

Evaluating the efficiency of reporting of key audit matters of the chosen banks:

This section demonstrates the analysis of the key audit matters from the financial

report of the companies in the consumer discretionary sector such as JB Hi-Fi, Tabcorp

holding limited, Aristocrat leisure limited, Wesfarmers limited and Nine entertainment. The

key audit maters of all the reporting entities chosen were addressed by the auditors in the

context of the audit of the financial report for the financial year 2018.

The auditor of JB Hi-Fi limited is Deloitte which identified two key audit matters

named acquisition of the good guys and carrying value of the good guys in the cash

generating unit while assessing the financial information provided by the company. The

details of such accounts have been detailed in the notes to financial statements such as note

10, 11 and 25. Such accounts were considered as key audit matters because of the judgment

of the management in estimating the amount and complexities involved in the valuation. The

appropriateness of the disclosures relating to such accounts was identified by the auditors by

employing the procedures such as performing the tests and assessing the methodology of

value in use. The model was tested for its accuracy by developing the appropriate test of

controls (member.afraccess.com 2019).

When looking at the annual report of Tabcorp Holding limited that Ernst and Young

have identified the key audit matters and have adopted proper procedures in addressing such

matters. The combination transaction of Tabcorp after the acquisition of Tatts group was

considered as key audit matters because of the judgment of the management in determining

its value. In this regard, the assessment of the purchase price accounting was done by the

auditor. Some other identified key audit maters include assessment of impairment for license

intangibles and goodwill, interest bearing abilities and reliance on the automated control and

process related to revenue. Assessment of all such matters was done by developing the

appropriate audit procedure. The auditors have also presented adequate reasons why the

matter is considered to have a material impact on the statements. From the section of key

audit matters in the financial report of Tabcorp limited, it has been ascertained that the

auditor have addressed all the key audit matters in separate section along with the addressing

all such matters using appropriate procedures. They have formed the opinion on the

presentation of the financial statements by determining the materiality and thereby providing

investors with transparency (Tabcorp.com.au 2019).

The annual report of the Aristocrat leisure limited has a separate section of the key

audit matter reported by its auditor Pwc. Key audit matters identified by auditors are income

tax, recognition of revenue, estimating recoverable amount of goodwill and accounting for

big fish and plarium acquisition. In addition to this, auditors have presented the proper reason

associated why the matter is regarded as key audit matter. Income tax is considered as key

audit matter because of the judgment involved in accounting for some uncertain tax positions

which the taxation authorities have not assessed. All the identified key audit matters have

been addressed by developing an in depth understanding of the system and developing the

test of controls (Ir.aristocrat.com 2019). The accounting of the group is evaluated against the

Australian accounting standard. The details of key audit matters are also identified by making

reference to the notes to the financial statements.

The auditors of Wesfarmers have identified some of the key matters for which they do

not provide separate opinion. However, a detailed description of how all the identified audit

CRITICALLY ANALYZE AND EVALUATE KEY AUDIT MATTERS IN THE

INDEPENDENT AUDITORS REPORT

matters have been addressed is provided by the auditor. The key audit matters identified by

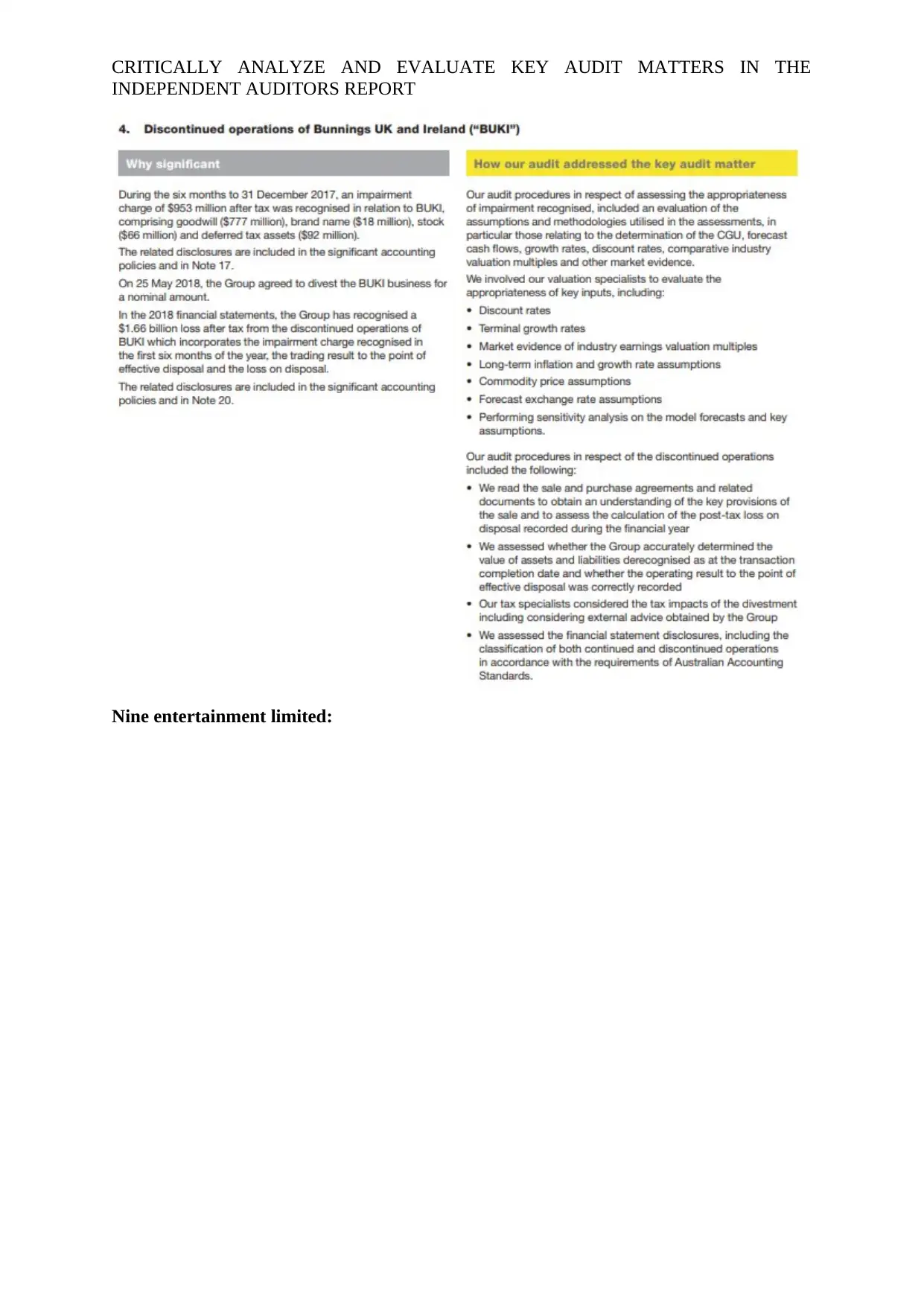

the auditors include noncurrent assets impairment such as intangible assets in Target,

discontinued operations of Carragh, supplier rebates and discontinued operations of Ireland

and Bunnings UK. Moreover, the reasons why all these matters are of significant importance

for auditor in the auditing process have been adequately explained in the section of key audit

matters. The assessment of all the matters is done by developing the appropriate audit

procedures that helped them in gaining an understanding of why the accounts are considered

to be material. One thing that is to be noted in the presentation and disclosure of the key audit

matter by the auditor of Wasfarmer limited is that that they have not referred to the notes to

the financial statements concerning the particular account they are addressing

(Wesfarmers.com.au 2019).

The audit of the financial report of Nine entertainment limited for the financial year

2018 has been done by Ernst and Young in accordance with the responsibilities for the

financial report audit. The audit opinion made on the financial report is based on the results

of the audit procedures that have been developed to address the key audit matters that have

been identified. Some key audit matters that is reported in a separate section of the annual

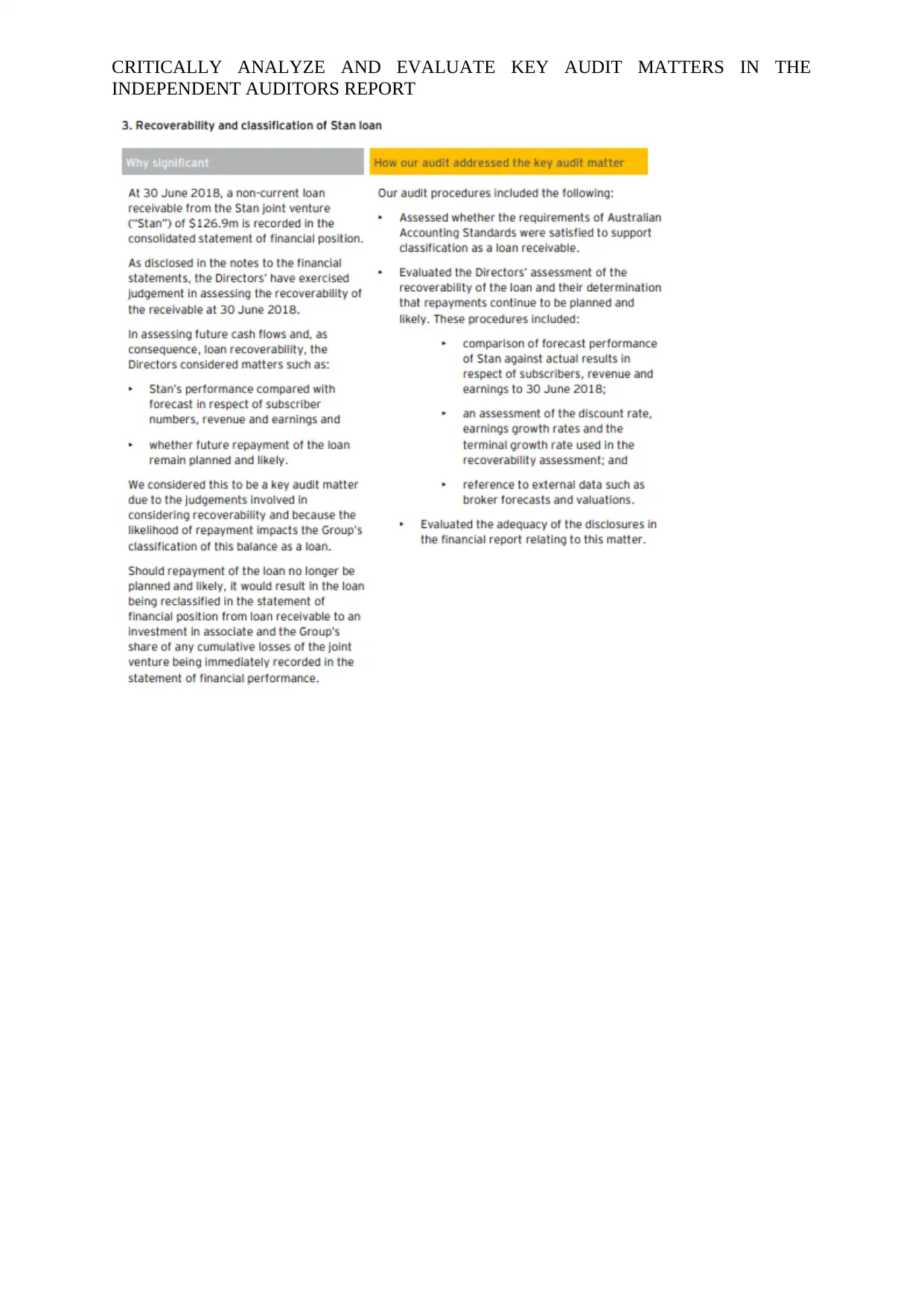

report of Nine entertainment include intangible assets carrying value, program rights

valuation, classification and recoverability of stan loan. It can be observed from the financial

report of the company that the auditors have based their opinion on why the matters are

significant by disclosing appropriate reasons. They have made reference to the notes to the

financial statements for assessing the accounts. Furthermore, the judgment of the

management in the assumptions and estimates and methodology of valuation on the

impairment of assets have been considered to create material impact on the financial

information. For addressing the matters, auditors have developed appropriate audit

procedures such as testing the mathematic accuracy of the model, comparing the forecasted

value to the carrying value and evaluating the disclosure adequacy relating to the matters

discussed in the financial report (Nineentertainmentco.com.au 2019).

From the analysis of the key audit matters of the chosen companies in the consumer

discretionary section, it has been observed that the auditors have identified such matters in

accordance with their responsibilities in preparation of the financial report. For all the

companies, no auditors have formed separate opinion on the key audit matters identified,

however, the basis of the opinion on the financial statements have been done taking into

account all those matters. The similarities in reporting of the key audit matters in the financial

report of the companies is that they have developed appropriate procedures for addressing the

matters along with placing adequate reasons why the matters is considered to be significant in

the auditing process (Kelton and Montague 2018). While assessing the key audit matters, it

has been ascertained that auditors is making reference to the details presented in the notes to

financial statements. In one of the financial report that is the financial report of Aristocrat

leisure limited, the section of key audit matters does not present the fact that the auditor

referred to the notes to financial statements.

Does key audit matters achieved the purpose in the industry:

It is inferred from the analysis of the key audit matters presented in the financial

report of the companies that the auditor have made professional judgment in determining the

matters and have accounted for its significance in preparing the auditor’s report. They have

also provided a detail of the description of each of the key audit matters such as why the

matter was considered to be of most significance and how the matter was addressed.

Documentation of all the audit matters is done and the matters are communicated with the

INDEPENDENT AUDITORS REPORT

matters have been addressed is provided by the auditor. The key audit matters identified by

the auditors include noncurrent assets impairment such as intangible assets in Target,

discontinued operations of Carragh, supplier rebates and discontinued operations of Ireland

and Bunnings UK. Moreover, the reasons why all these matters are of significant importance

for auditor in the auditing process have been adequately explained in the section of key audit

matters. The assessment of all the matters is done by developing the appropriate audit

procedures that helped them in gaining an understanding of why the accounts are considered

to be material. One thing that is to be noted in the presentation and disclosure of the key audit

matter by the auditor of Wasfarmer limited is that that they have not referred to the notes to

the financial statements concerning the particular account they are addressing

(Wesfarmers.com.au 2019).

The audit of the financial report of Nine entertainment limited for the financial year

2018 has been done by Ernst and Young in accordance with the responsibilities for the

financial report audit. The audit opinion made on the financial report is based on the results

of the audit procedures that have been developed to address the key audit matters that have

been identified. Some key audit matters that is reported in a separate section of the annual

report of Nine entertainment include intangible assets carrying value, program rights

valuation, classification and recoverability of stan loan. It can be observed from the financial

report of the company that the auditors have based their opinion on why the matters are

significant by disclosing appropriate reasons. They have made reference to the notes to the

financial statements for assessing the accounts. Furthermore, the judgment of the

management in the assumptions and estimates and methodology of valuation on the

impairment of assets have been considered to create material impact on the financial

information. For addressing the matters, auditors have developed appropriate audit

procedures such as testing the mathematic accuracy of the model, comparing the forecasted

value to the carrying value and evaluating the disclosure adequacy relating to the matters

discussed in the financial report (Nineentertainmentco.com.au 2019).

From the analysis of the key audit matters of the chosen companies in the consumer

discretionary section, it has been observed that the auditors have identified such matters in

accordance with their responsibilities in preparation of the financial report. For all the

companies, no auditors have formed separate opinion on the key audit matters identified,

however, the basis of the opinion on the financial statements have been done taking into

account all those matters. The similarities in reporting of the key audit matters in the financial

report of the companies is that they have developed appropriate procedures for addressing the

matters along with placing adequate reasons why the matters is considered to be significant in

the auditing process (Kelton and Montague 2018). While assessing the key audit matters, it

has been ascertained that auditors is making reference to the details presented in the notes to

financial statements. In one of the financial report that is the financial report of Aristocrat

leisure limited, the section of key audit matters does not present the fact that the auditor

referred to the notes to financial statements.

Does key audit matters achieved the purpose in the industry:

It is inferred from the analysis of the key audit matters presented in the financial

report of the companies that the auditor have made professional judgment in determining the

matters and have accounted for its significance in preparing the auditor’s report. They have

also provided a detail of the description of each of the key audit matters such as why the

matter was considered to be of most significance and how the matter was addressed.

Documentation of all the audit matters is done and the matters are communicated with the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CRITICALLY ANALYZE AND EVALUATE KEY AUDIT MATTERS IN THE

INDEPENDENT AUDITORS REPORT

people charged with governance in management (Hkicpa.org.hk 2019). Thus, there is a more

detailed and transparent presentation of the financial information that would provide

assistance to users in their decision making process.

Conclusion:

The report prepared to evaluate the new auditing standard found that introduction of

such auditing standard has improved the transparency of the information and enable the

auditor to form an appropriate opinion on the financial performance of company. The

introduction of the standard had addressed many of the issues such as key audit matters

which resulted in the failure of many corporate organizations. From the analysis of the

annual report of the chosen entities, it can be concluded that the auditors of all the companies

have identified the key audit matters in accordance with the requirements and responsibilities

of the auditing standard. Therefore, it is said that identification of key audit matters have

served their purpose in the industry.

INDEPENDENT AUDITORS REPORT

people charged with governance in management (Hkicpa.org.hk 2019). Thus, there is a more

detailed and transparent presentation of the financial information that would provide

assistance to users in their decision making process.

Conclusion:

The report prepared to evaluate the new auditing standard found that introduction of

such auditing standard has improved the transparency of the information and enable the

auditor to form an appropriate opinion on the financial performance of company. The

introduction of the standard had addressed many of the issues such as key audit matters

which resulted in the failure of many corporate organizations. From the analysis of the

annual report of the chosen entities, it can be concluded that the auditors of all the companies

have identified the key audit matters in accordance with the requirements and responsibilities

of the auditing standard. Therefore, it is said that identification of key audit matters have

served their purpose in the industry.

CRITICALLY ANALYZE AND EVALUATE KEY AUDIT MATTERS IN THE

INDEPENDENT AUDITORS REPORT

References list:

Aristocrat Leisure Limited – IR Site., 2019. Annual Reports - Aristocrat Leisure Limited – IR

Site. [online] Available at: http://ir.aristocrat.com/financial-information/annual-reports

[Accessed 20 May 2019].

Auasb.gov.au., 201). [online] Available at:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_570_2015.pdf [Accessed 20 May

2019].

Auasb.gov.au., 2019. [online] Available at:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_701_2015.pdf [Accessed 20 May

2019].

Christensen, B.E., Glover, S.M., Omer, T.C. and Shelley, M.K., 2016. Understanding audit

quality: Insights from audit professionals and investors. Contemporary Accounting

Research, 33(4), pp.1648-1684.

Cordoş, G.S. and Fülöp, M.T., 2015. Understanding audit reporting changes: introduction of

Key Audit Matters. Accounting & Management Information Systems/Contabilitate si

Informatica de Gestiune, 14(1).

Eutsler, J., Nickell, E.B. and Robb, S.W., 2016. Fraud risk awareness and the likelihood of

audit enforcement action. Accounting Horizons, 30(3), pp.379-392.

George-Silviu, C., & Melinda-Timea, F., 2015. New audit reporting challenges: auditing the

going concern basis of accounting. Procedia Economics and Finance, 32, 216-224.

Hkicpa.org.hk., 2019. [online] Available at: https://www.hkicpa.org.hk/-/media/HKICPA-

Website/HKICPA/section6_standards/standards/Audit-n-assurance/hksa-clarity-centre/

FAQ_defltd.pdf?la=en&hash=520AB9B7B5C71E207ECC4613B174DEB2 [Accessed 20

May 2019].

Ir.aristocrat.com., 2019. [online] Available at: http://ir.aristocrat.com/static-files/9527b2df-

e411-4c49-8067-d2f391a0fbe0 [Accessed 20 May 2019].

Kelton, A.S. and Montague, N.R., 2018. The unintended consequences of uncertainty

disclosures made by auditors and managers on nonprofessional investor

judgments. Accounting, Organizations and Society, 65, pp.44-55.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

Köhler, A., Ratzinger-Sakel, N.V. and Theis, J., 2016. The effects of key audit matters on the

auditor's report's communicative value: Experimental evidence from investment professionals

and non-professional investors. Available at SSRN 2838162.

Legislation.gov.au., 2019. ASA 701 - Communicating Key Audit Matters in the Independent

Auditor’s Report - December 2015 . [online] Available at:

https://www.legislation.gov.au/Details/F2015L02016/Explanatory%20Statement/Text

[Accessed 20 May 2019].

Member.afraccess.com., 2019. [online] Available at: http://member.afraccess.com/media?

id=CMN://3A498121&filename=20180813/JBH_02008547.pdf [Accessed 20 May 2019].

Nineentertainmentco.com.au., 2019. Financial Results - Nine. [online] Available at:

https://www.nineentertainmentco.com.au/investor-centre/results [Accessed 20 May 2019].

Sunderland, D. and Trompeter, G.M., 2017. Multinational group audits: Problems faced in

practice and opportunities for research. Auditing: A Journal of Practice & Theory, 36(3),

pp.159-183.

INDEPENDENT AUDITORS REPORT

References list:

Aristocrat Leisure Limited – IR Site., 2019. Annual Reports - Aristocrat Leisure Limited – IR

Site. [online] Available at: http://ir.aristocrat.com/financial-information/annual-reports

[Accessed 20 May 2019].

Auasb.gov.au., 201). [online] Available at:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_570_2015.pdf [Accessed 20 May

2019].

Auasb.gov.au., 2019. [online] Available at:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_701_2015.pdf [Accessed 20 May

2019].

Christensen, B.E., Glover, S.M., Omer, T.C. and Shelley, M.K., 2016. Understanding audit

quality: Insights from audit professionals and investors. Contemporary Accounting

Research, 33(4), pp.1648-1684.

Cordoş, G.S. and Fülöp, M.T., 2015. Understanding audit reporting changes: introduction of

Key Audit Matters. Accounting & Management Information Systems/Contabilitate si

Informatica de Gestiune, 14(1).

Eutsler, J., Nickell, E.B. and Robb, S.W., 2016. Fraud risk awareness and the likelihood of

audit enforcement action. Accounting Horizons, 30(3), pp.379-392.

George-Silviu, C., & Melinda-Timea, F., 2015. New audit reporting challenges: auditing the

going concern basis of accounting. Procedia Economics and Finance, 32, 216-224.

Hkicpa.org.hk., 2019. [online] Available at: https://www.hkicpa.org.hk/-/media/HKICPA-

Website/HKICPA/section6_standards/standards/Audit-n-assurance/hksa-clarity-centre/

FAQ_defltd.pdf?la=en&hash=520AB9B7B5C71E207ECC4613B174DEB2 [Accessed 20

May 2019].

Ir.aristocrat.com., 2019. [online] Available at: http://ir.aristocrat.com/static-files/9527b2df-

e411-4c49-8067-d2f391a0fbe0 [Accessed 20 May 2019].

Kelton, A.S. and Montague, N.R., 2018. The unintended consequences of uncertainty

disclosures made by auditors and managers on nonprofessional investor

judgments. Accounting, Organizations and Society, 65, pp.44-55.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

Köhler, A., Ratzinger-Sakel, N.V. and Theis, J., 2016. The effects of key audit matters on the

auditor's report's communicative value: Experimental evidence from investment professionals

and non-professional investors. Available at SSRN 2838162.

Legislation.gov.au., 2019. ASA 701 - Communicating Key Audit Matters in the Independent

Auditor’s Report - December 2015 . [online] Available at:

https://www.legislation.gov.au/Details/F2015L02016/Explanatory%20Statement/Text

[Accessed 20 May 2019].

Member.afraccess.com., 2019. [online] Available at: http://member.afraccess.com/media?

id=CMN://3A498121&filename=20180813/JBH_02008547.pdf [Accessed 20 May 2019].

Nineentertainmentco.com.au., 2019. Financial Results - Nine. [online] Available at:

https://www.nineentertainmentco.com.au/investor-centre/results [Accessed 20 May 2019].

Sunderland, D. and Trompeter, G.M., 2017. Multinational group audits: Problems faced in

practice and opportunities for research. Auditing: A Journal of Practice & Theory, 36(3),

pp.159-183.

CRITICALLY ANALYZE AND EVALUATE KEY AUDIT MATTERS IN THE

INDEPENDENT AUDITORS REPORT

Tabcorp.com.au., 2019. [online] Available at:

https://www.tabcorp.com.au/TabCorp/media/TabCorp/Investors/Annual%20Report/Tabcorp-

Annual-Report-2018_1.pdf [Accessed 20 May 2019].

Wesfarmers.com.au., 2019. [online] Available at:

https://www.wesfarmers.com.au/docs/default-source/asx-announcements/2018-annual-

report.pdf?sfvrsn=0 [Accessed 20 May 2019].

Appendix:

JB Hi-Fi limited

INDEPENDENT AUDITORS REPORT

Tabcorp.com.au., 2019. [online] Available at:

https://www.tabcorp.com.au/TabCorp/media/TabCorp/Investors/Annual%20Report/Tabcorp-

Annual-Report-2018_1.pdf [Accessed 20 May 2019].

Wesfarmers.com.au., 2019. [online] Available at:

https://www.wesfarmers.com.au/docs/default-source/asx-announcements/2018-annual-

report.pdf?sfvrsn=0 [Accessed 20 May 2019].

Appendix:

JB Hi-Fi limited

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CRITICALLY ANALYZE AND EVALUATE KEY AUDIT MATTERS IN THE

INDEPENDENT AUDITORS REPORT

INDEPENDENT AUDITORS REPORT

CRITICALLY ANALYZE AND EVALUATE KEY AUDIT MATTERS IN THE

INDEPENDENT AUDITORS REPORT

Tabcorp Holding limited:

INDEPENDENT AUDITORS REPORT

Tabcorp Holding limited:

CRITICALLY ANALYZE AND EVALUATE KEY AUDIT MATTERS IN THE

INDEPENDENT AUDITORS REPORT

Aristocrat leisure limited:

INDEPENDENT AUDITORS REPORT

Aristocrat leisure limited:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CRITICALLY ANALYZE AND EVALUATE KEY AUDIT MATTERS IN THE

INDEPENDENT AUDITORS REPORT

INDEPENDENT AUDITORS REPORT

CRITICALLY ANALYZE AND EVALUATE KEY AUDIT MATTERS IN THE

INDEPENDENT AUDITORS REPORT

Wesfarmers limited:

INDEPENDENT AUDITORS REPORT

Wesfarmers limited:

CRITICALLY ANALYZE AND EVALUATE KEY AUDIT MATTERS IN THE

INDEPENDENT AUDITORS REPORT

INDEPENDENT AUDITORS REPORT

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CRITICALLY ANALYZE AND EVALUATE KEY AUDIT MATTERS IN THE

INDEPENDENT AUDITORS REPORT

INDEPENDENT AUDITORS REPORT

CRITICALLY ANALYZE AND EVALUATE KEY AUDIT MATTERS IN THE

INDEPENDENT AUDITORS REPORT

Nine entertainment limited:

INDEPENDENT AUDITORS REPORT

Nine entertainment limited:

CRITICALLY ANALYZE AND EVALUATE KEY AUDIT MATTERS IN THE

INDEPENDENT AUDITORS REPORT

INDEPENDENT AUDITORS REPORT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CRITICALLY ANALYZE AND EVALUATE KEY AUDIT MATTERS IN THE

INDEPENDENT AUDITORS REPORT

INDEPENDENT AUDITORS REPORT

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.