Accounting Theory and Issues: A Review on Crown Resort Limited’s Conceptual Framework and Australian Accounting Standard Board

VerifiedAdded on 2023/06/09

|17

|2949

|139

AI Summary

This report analyzes and evaluates the compliance of Crown Resorts Limited with the conceptual framework of AASB in the process of financial reporting. It covers the company profile, GPFR, remuneration report, critical analysis, and recent news. The report concludes that Crown Resorts has complied with all the required regulations and principles of the Conceptual Framework of AASB at the time of the preparation and presentation of their financial statements.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ACCOUNTING THEORY AND ISSUES

Accounting Theory and Issues

A Review on Crown Resort Limited’s Conceptual Framework and Australian Accounting

Standard Board

Name of the Student

Name of the University

Author’s Note

Accounting Theory and Issues

A Review on Crown Resort Limited’s Conceptual Framework and Australian Accounting

Standard Board

Name of the Student

Name of the University

Author’s Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1ACCOUNTING THEORY AND ISSUES

Executive Summary

The main aim of this report lies in the analysis and evaluation of the compliance of Crown

Resorts Limited with the conceptual framework of AASB in the process of financial reporting.

From the analysis of the report, it can be observed that the company has made compliance with

all the needed rules and regulations of conceptual framework of AASB for the purpose of the

preparation and presentation of their financial statements. It can also be seen from the analysis

that the company has published all the required financial statements for providing the users with

all the required information for the purpose of investment decision-making.

Executive Summary

The main aim of this report lies in the analysis and evaluation of the compliance of Crown

Resorts Limited with the conceptual framework of AASB in the process of financial reporting.

From the analysis of the report, it can be observed that the company has made compliance with

all the needed rules and regulations of conceptual framework of AASB for the purpose of the

preparation and presentation of their financial statements. It can also be seen from the analysis

that the company has published all the required financial statements for providing the users with

all the required information for the purpose of investment decision-making.

2ACCOUNTING THEORY AND ISSUES

Table of Contents

Introduction......................................................................................................................................3

Company Profile..............................................................................................................................3

Conceptual Framework....................................................................................................................5

General Purpose Financial Reporting (GPFR)................................................................................6

Remuneration Report.......................................................................................................................7

Critical Analysis..............................................................................................................................9

Property, Plant and Equipment (PPE).........................................................................................9

Contingent Liability...................................................................................................................10

Inventories.................................................................................................................................10

Revenue.....................................................................................................................................11

Dividends...................................................................................................................................12

Recent News..................................................................................................................................13

Conclusion.....................................................................................................................................13

References......................................................................................................................................15

Table of Contents

Introduction......................................................................................................................................3

Company Profile..............................................................................................................................3

Conceptual Framework....................................................................................................................5

General Purpose Financial Reporting (GPFR)................................................................................6

Remuneration Report.......................................................................................................................7

Critical Analysis..............................................................................................................................9

Property, Plant and Equipment (PPE).........................................................................................9

Contingent Liability...................................................................................................................10

Inventories.................................................................................................................................10

Revenue.....................................................................................................................................11

Dividends...................................................................................................................................12

Recent News..................................................................................................................................13

Conclusion.....................................................................................................................................13

References......................................................................................................................................15

3ACCOUNTING THEORY AND ISSUES

Introduction

In today’s business world, one cannot ignore the importance of conceptual framework as

its helps the companies in dealing with various kinds of accounting issues like objectives of the

financial statements, their uses along with their characteristics and others. At the same time, it

assists the companies in the development and presentation of the financial statements like

income statement, balance sheet, cash flow statements and others. The presence of accounting

conceptual framework can be seen in Australia developed by Australian Accounting Standard

Board (AASB) (Henderson et al., 2015). It is the obligation on the companies to follow all the

principles and rules of AASB for ensuring the correct development and true presentation of their

financial statements. The main aim of this report lies in the analysis and evaluation of the

compliance of Crown Resorts Limited with the conceptual framework of AASB in the process

of financial reporting.

Company Profile

Crown Resorts is regarded as the largest entertainment group operating in different

regions of Australia. The presence of the core businesses and investments of this company can be

Introduction

In today’s business world, one cannot ignore the importance of conceptual framework as

its helps the companies in dealing with various kinds of accounting issues like objectives of the

financial statements, their uses along with their characteristics and others. At the same time, it

assists the companies in the development and presentation of the financial statements like

income statement, balance sheet, cash flow statements and others. The presence of accounting

conceptual framework can be seen in Australia developed by Australian Accounting Standard

Board (AASB) (Henderson et al., 2015). It is the obligation on the companies to follow all the

principles and rules of AASB for ensuring the correct development and true presentation of their

financial statements. The main aim of this report lies in the analysis and evaluation of the

compliance of Crown Resorts Limited with the conceptual framework of AASB in the process

of financial reporting.

Company Profile

Crown Resorts is regarded as the largest entertainment group operating in different

regions of Australia. The presence of the core businesses and investments of this company can be

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4ACCOUNTING THEORY AND ISSUES

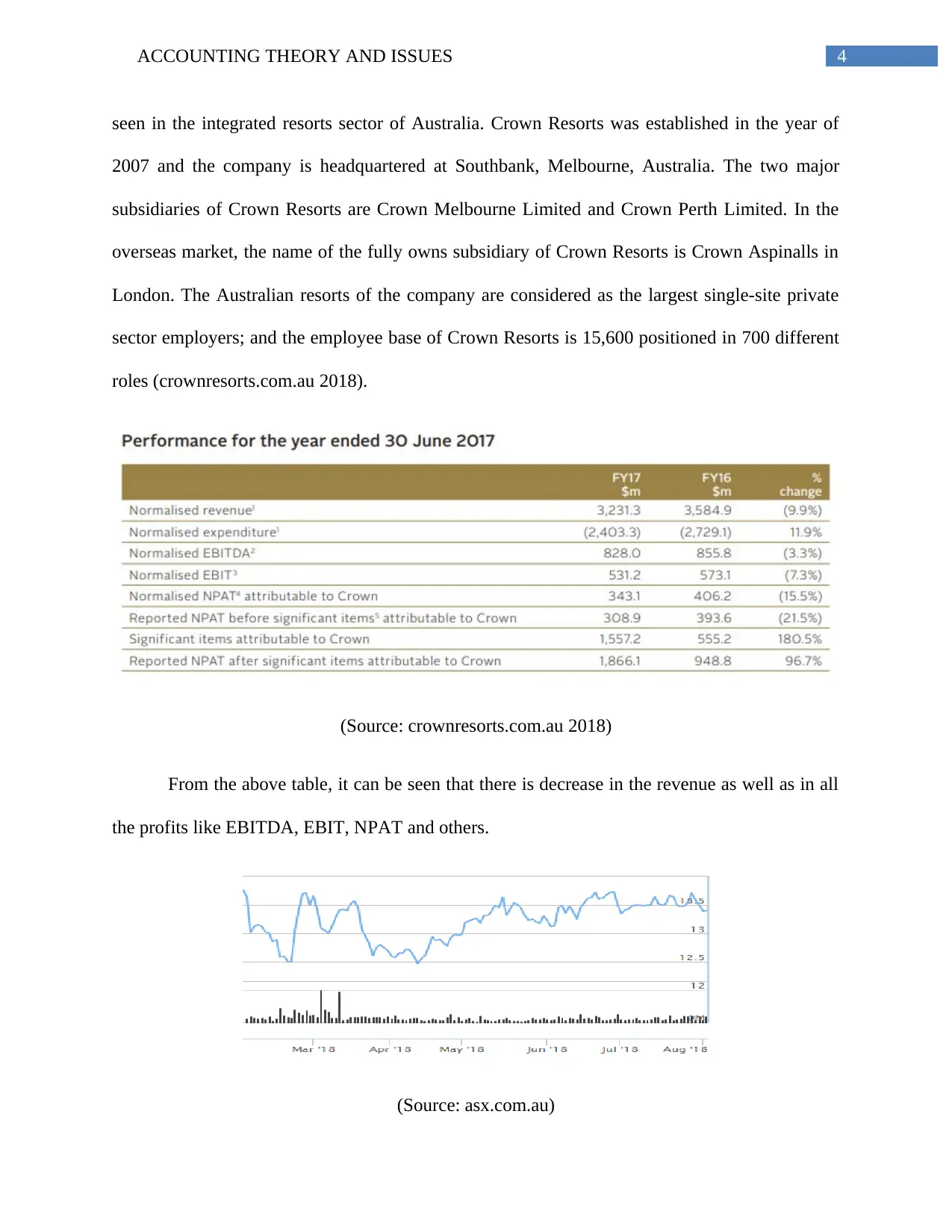

seen in the integrated resorts sector of Australia. Crown Resorts was established in the year of

2007 and the company is headquartered at Southbank, Melbourne, Australia. The two major

subsidiaries of Crown Resorts are Crown Melbourne Limited and Crown Perth Limited. In the

overseas market, the name of the fully owns subsidiary of Crown Resorts is Crown Aspinalls in

London. The Australian resorts of the company are considered as the largest single-site private

sector employers; and the employee base of Crown Resorts is 15,600 positioned in 700 different

roles (crownresorts.com.au 2018).

(Source: crownresorts.com.au 2018)

From the above table, it can be seen that there is decrease in the revenue as well as in all

the profits like EBITDA, EBIT, NPAT and others.

(Source: asx.com.au)

seen in the integrated resorts sector of Australia. Crown Resorts was established in the year of

2007 and the company is headquartered at Southbank, Melbourne, Australia. The two major

subsidiaries of Crown Resorts are Crown Melbourne Limited and Crown Perth Limited. In the

overseas market, the name of the fully owns subsidiary of Crown Resorts is Crown Aspinalls in

London. The Australian resorts of the company are considered as the largest single-site private

sector employers; and the employee base of Crown Resorts is 15,600 positioned in 700 different

roles (crownresorts.com.au 2018).

(Source: crownresorts.com.au 2018)

From the above table, it can be seen that there is decrease in the revenue as well as in all

the profits like EBITDA, EBIT, NPAT and others.

(Source: asx.com.au)

5ACCOUNTING THEORY AND ISSUES

It can also be observed from the table that there is decrease in the share price of the

company in the recent months. Hence, it can be observed that the recent financial performance of

the company is not good as compared to the previous period; and the loss of business can be held

responsible for this.

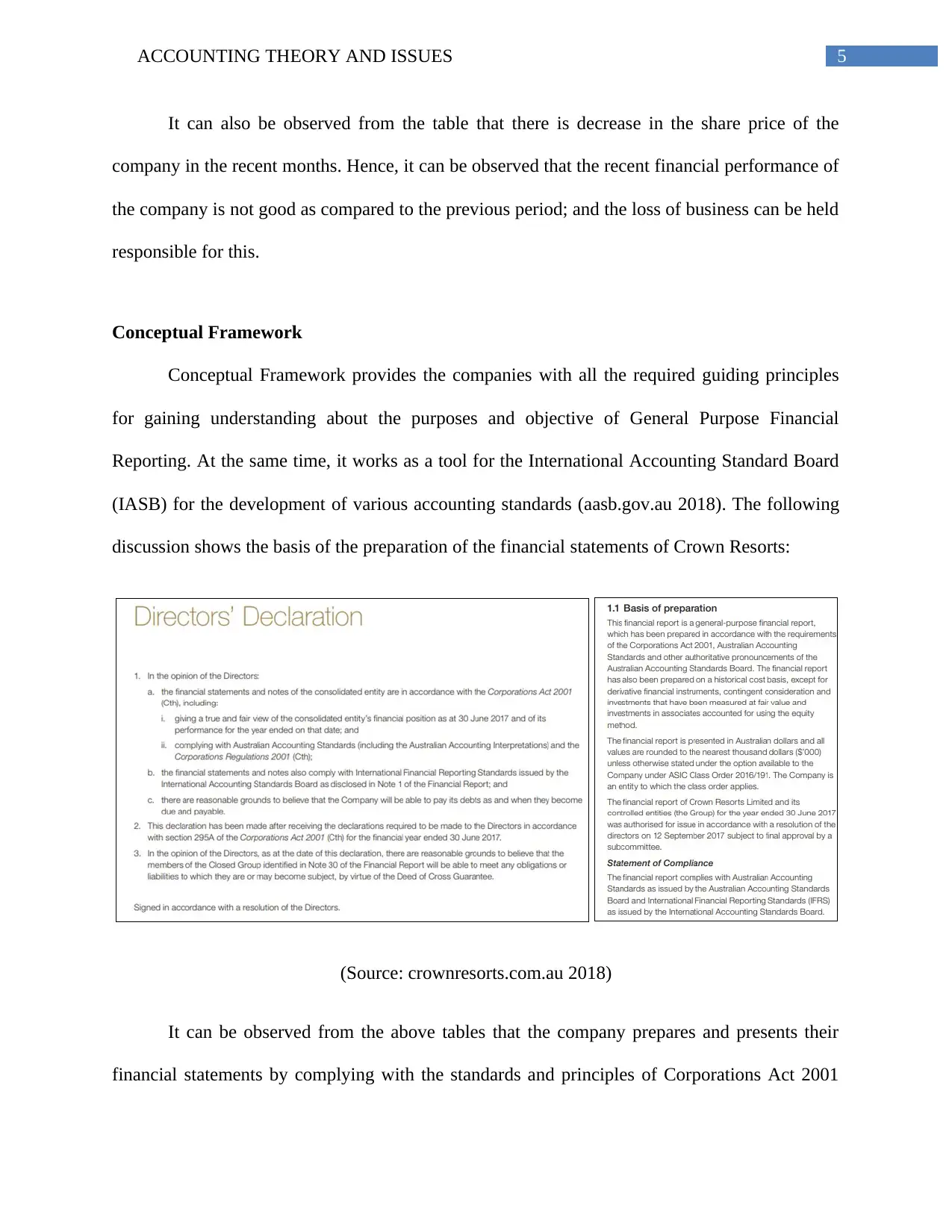

Conceptual Framework

Conceptual Framework provides the companies with all the required guiding principles

for gaining understanding about the purposes and objective of General Purpose Financial

Reporting. At the same time, it works as a tool for the International Accounting Standard Board

(IASB) for the development of various accounting standards (aasb.gov.au 2018). The following

discussion shows the basis of the preparation of the financial statements of Crown Resorts:

(Source: crownresorts.com.au 2018)

It can be observed from the above tables that the company prepares and presents their

financial statements by complying with the standards and principles of Corporations Act 2001

It can also be observed from the table that there is decrease in the share price of the

company in the recent months. Hence, it can be observed that the recent financial performance of

the company is not good as compared to the previous period; and the loss of business can be held

responsible for this.

Conceptual Framework

Conceptual Framework provides the companies with all the required guiding principles

for gaining understanding about the purposes and objective of General Purpose Financial

Reporting. At the same time, it works as a tool for the International Accounting Standard Board

(IASB) for the development of various accounting standards (aasb.gov.au 2018). The following

discussion shows the basis of the preparation of the financial statements of Crown Resorts:

(Source: crownresorts.com.au 2018)

It can be observed from the above tables that the company prepares and presents their

financial statements by complying with the standards and principles of Corporations Act 2001

6ACCOUNTING THEORY AND ISSUES

and AASB. At the same time, they comply with the standards of both International Financial

Reporting Standards (IFRS) and International Accounting Standard Board (IASB).

The main contribution of Conceptual Framework towards AASB can be notices in the

promotion and maintenance of accounting standards, regulations and procedures. Moreover, it

can be regarded as a statement of Generally Accepted Accounting Standard (GAAP) for the

creation of structure for reviewing standards along with the development of the same

(aasb.gov.au 2018). Most importantly, it helps in delivering crucial information to the investors

for assisting in the indecent decision-making process. Additionally, the auditors can use it as a

major tool in order to ensure that the financial statements are developed as per the required

standards or not.

General Purpose Financial Reporting (GPFR)

The main contribution of GPRF can be seen in providing assistance to the investors and

creditors for the purpose of investment decision-making. The major components of GPFR are

income statement, balance sheet, cash flow statement and statement of change in equity. The

corporation is responsible for the preparation of GPFR so that valuable information can be

delivered to the shareholders for decision-making process (Zeff 2013). It is also the

responsibility of GPFR to provide information to the existing as well as potential investors for

the decision-making process. The main qualitative fundamental and enhancing characteristics of

GPFR are relevance, faithful representation, understandability, verifiability, timeliness and

comparability. The presence of all of these characteristics makes the financial information more

useful and acceptable for their users. From the earlier discussion, it can be seen that Crown

and AASB. At the same time, they comply with the standards of both International Financial

Reporting Standards (IFRS) and International Accounting Standard Board (IASB).

The main contribution of Conceptual Framework towards AASB can be notices in the

promotion and maintenance of accounting standards, regulations and procedures. Moreover, it

can be regarded as a statement of Generally Accepted Accounting Standard (GAAP) for the

creation of structure for reviewing standards along with the development of the same

(aasb.gov.au 2018). Most importantly, it helps in delivering crucial information to the investors

for assisting in the indecent decision-making process. Additionally, the auditors can use it as a

major tool in order to ensure that the financial statements are developed as per the required

standards or not.

General Purpose Financial Reporting (GPFR)

The main contribution of GPRF can be seen in providing assistance to the investors and

creditors for the purpose of investment decision-making. The major components of GPFR are

income statement, balance sheet, cash flow statement and statement of change in equity. The

corporation is responsible for the preparation of GPFR so that valuable information can be

delivered to the shareholders for decision-making process (Zeff 2013). It is also the

responsibility of GPFR to provide information to the existing as well as potential investors for

the decision-making process. The main qualitative fundamental and enhancing characteristics of

GPFR are relevance, faithful representation, understandability, verifiability, timeliness and

comparability. The presence of all of these characteristics makes the financial information more

useful and acceptable for their users. From the earlier discussion, it can be seen that Crown

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING THEORY AND ISSUES

Resorts follow the principles and standards of Corporations Act 2001, AASB, IFRS and IASB as

a part of GPFR (Warren, Reeve and Duchac 2013).

Remuneration Report

From the 2017 Annual Report of Crown Resorts, it can be observed that the company

prepares their remuneration report for the executives as per the policies and standards of

Corporations Act 2001 and the Corporations Regulations 2001. According to the remuneration

policy of Crown Resorts, the main aim of the company is to make it sure that the remuneration

package of the executives properly reflects their roles and responsibilities. The presence of three

major parts can be seen in the remuneration structure of the company; they are Fixed

Remuneration, Short-Term Incentives (STI) and Long-Term Incentives (LTI). The main aim of

fixed remuneration is to provide the executives with a base level of remuneration as per the

responsibilities and roles of them. On the other hand, both the STI and LTI are based on the

performance of the executive directors.

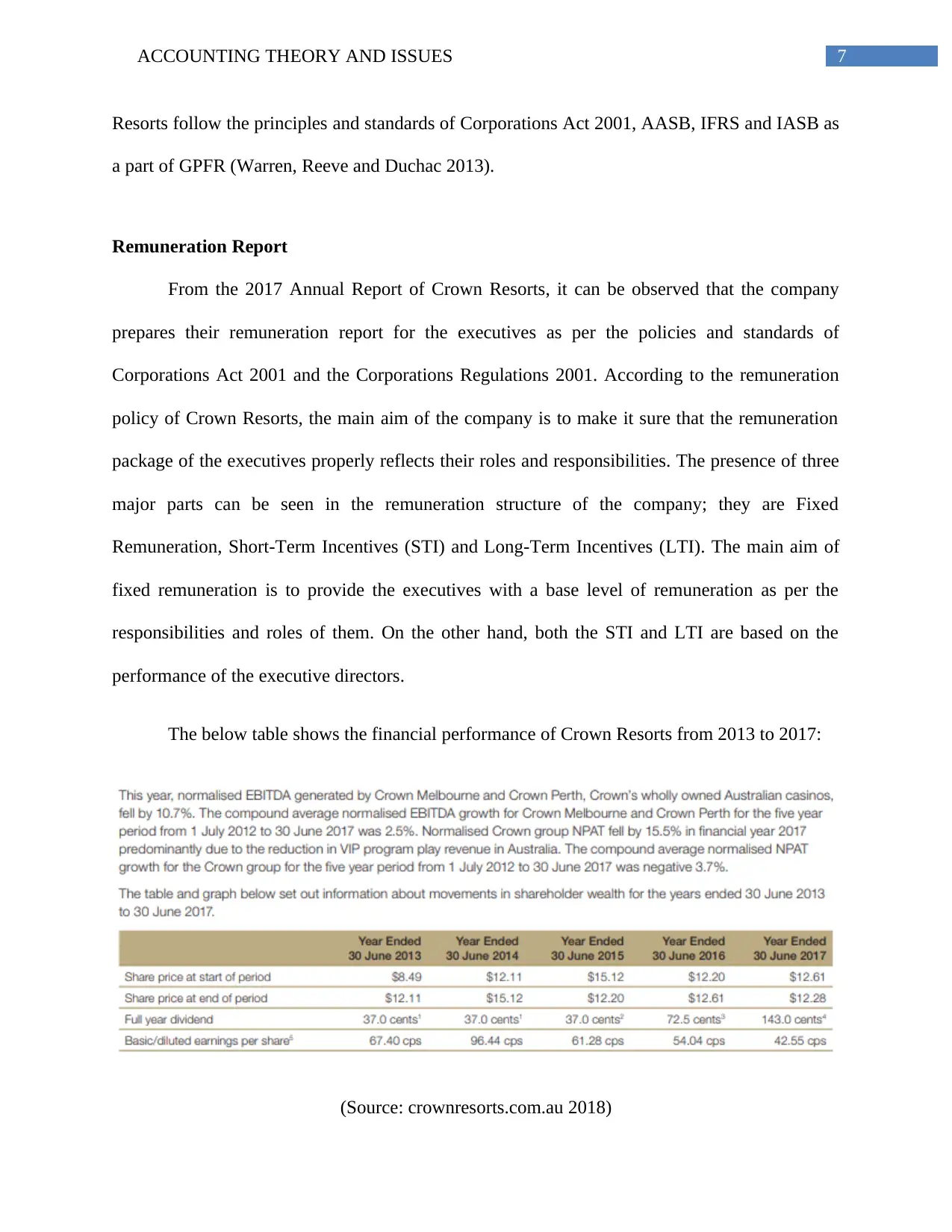

The below table shows the financial performance of Crown Resorts from 2013 to 2017:

(Source: crownresorts.com.au 2018)

Resorts follow the principles and standards of Corporations Act 2001, AASB, IFRS and IASB as

a part of GPFR (Warren, Reeve and Duchac 2013).

Remuneration Report

From the 2017 Annual Report of Crown Resorts, it can be observed that the company

prepares their remuneration report for the executives as per the policies and standards of

Corporations Act 2001 and the Corporations Regulations 2001. According to the remuneration

policy of Crown Resorts, the main aim of the company is to make it sure that the remuneration

package of the executives properly reflects their roles and responsibilities. The presence of three

major parts can be seen in the remuneration structure of the company; they are Fixed

Remuneration, Short-Term Incentives (STI) and Long-Term Incentives (LTI). The main aim of

fixed remuneration is to provide the executives with a base level of remuneration as per the

responsibilities and roles of them. On the other hand, both the STI and LTI are based on the

performance of the executive directors.

The below table shows the financial performance of Crown Resorts from 2013 to 2017:

(Source: crownresorts.com.au 2018)

8ACCOUNTING THEORY AND ISSUES

It can be seen from the above that there is a drop in the normalized EBITDA by 10.7%%.

At the same time, 15.5% fall in the normalized NAPT can be seen in the company for the year

2017. Apart from this, increase in the share prices can also be seen. This situation indicates

towards the failure of the directors to achieve the Key Performance Objectives (KPO) of the

company.

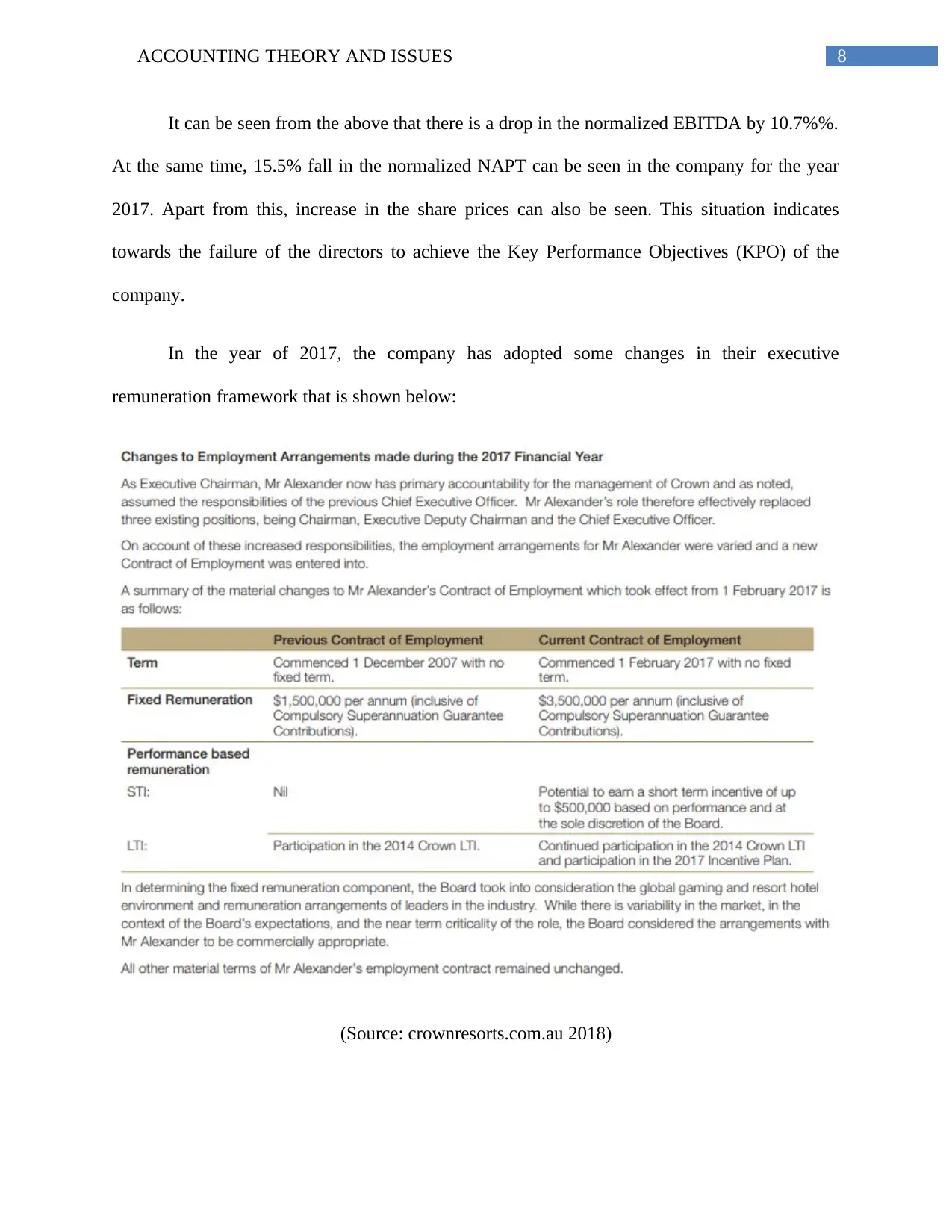

In the year of 2017, the company has adopted some changes in their executive

remuneration framework that is shown below:

(Source: crownresorts.com.au 2018)

It can be seen from the above that there is a drop in the normalized EBITDA by 10.7%%.

At the same time, 15.5% fall in the normalized NAPT can be seen in the company for the year

2017. Apart from this, increase in the share prices can also be seen. This situation indicates

towards the failure of the directors to achieve the Key Performance Objectives (KPO) of the

company.

In the year of 2017, the company has adopted some changes in their executive

remuneration framework that is shown below:

(Source: crownresorts.com.au 2018)

9ACCOUNTING THEORY AND ISSUES

Hence, from the above discussion, it can be observed that Crown Resorts has complied

with the principles of Conceptual Framework at the time of the preparation of their remuneration

report. In the presence of accurate and effective remuneration structure, the employees as well as

senior executives of Crown Resorts become motivated to achieve the organizational goals with

their good performance.

Critical Analysis

Property, Plant and Equipment (PPE)

All the required accounting requirements for treating property, plant and equipment can

be seen in AASB 116 Property, Plant and Equipment and the Australian Standard Board (ASB)

has developed this requirement under section 334 of the Corporations Act 2001 (aasb.gov.au

2018). As per this standard, the companies are needed to determine the carrying value of these

assets along with depreciation and the amount of impairment losses. The requirement is to

recognize them at the cost value after the deduction of depreciation. The following figure shows

the accounting treatment of PPE by Crown Resorts:

(Source: crownresorts.com.au 2018)

Hence, from the above discussion, it can be observed that Crown Resorts has complied

with the principles of Conceptual Framework at the time of the preparation of their remuneration

report. In the presence of accurate and effective remuneration structure, the employees as well as

senior executives of Crown Resorts become motivated to achieve the organizational goals with

their good performance.

Critical Analysis

Property, Plant and Equipment (PPE)

All the required accounting requirements for treating property, plant and equipment can

be seen in AASB 116 Property, Plant and Equipment and the Australian Standard Board (ASB)

has developed this requirement under section 334 of the Corporations Act 2001 (aasb.gov.au

2018). As per this standard, the companies are needed to determine the carrying value of these

assets along with depreciation and the amount of impairment losses. The requirement is to

recognize them at the cost value after the deduction of depreciation. The following figure shows

the accounting treatment of PPE by Crown Resorts:

(Source: crownresorts.com.au 2018)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10ACCOUNTING THEORY AND ISSUES

It can be seen that Crown Resorts follows the AASB conceptual framework for the

accounting treatment of PPE.

Contingent Liability

Contingent liabilities are considered as the obligation of the companies occurring from

any past event. Timeliness needs to be there in the contingent liability for the availability of

proper information at the time to make the decisions related to these liabilities. All the required

accounting principles and standards for the treatment of contingent liabilities can be seen in

AASB 137 Provision, Contingent Liabilities and Contingent Assets under section 334

(aasb.gov.au 2018). There is a need to have verifiability characteristic in contingent liability so

that the users can gain understanding about these liabilities. The following figure shows the

contingent liability treatment in Crown Resorts:

(Source: crownresorts.com.au 2018)

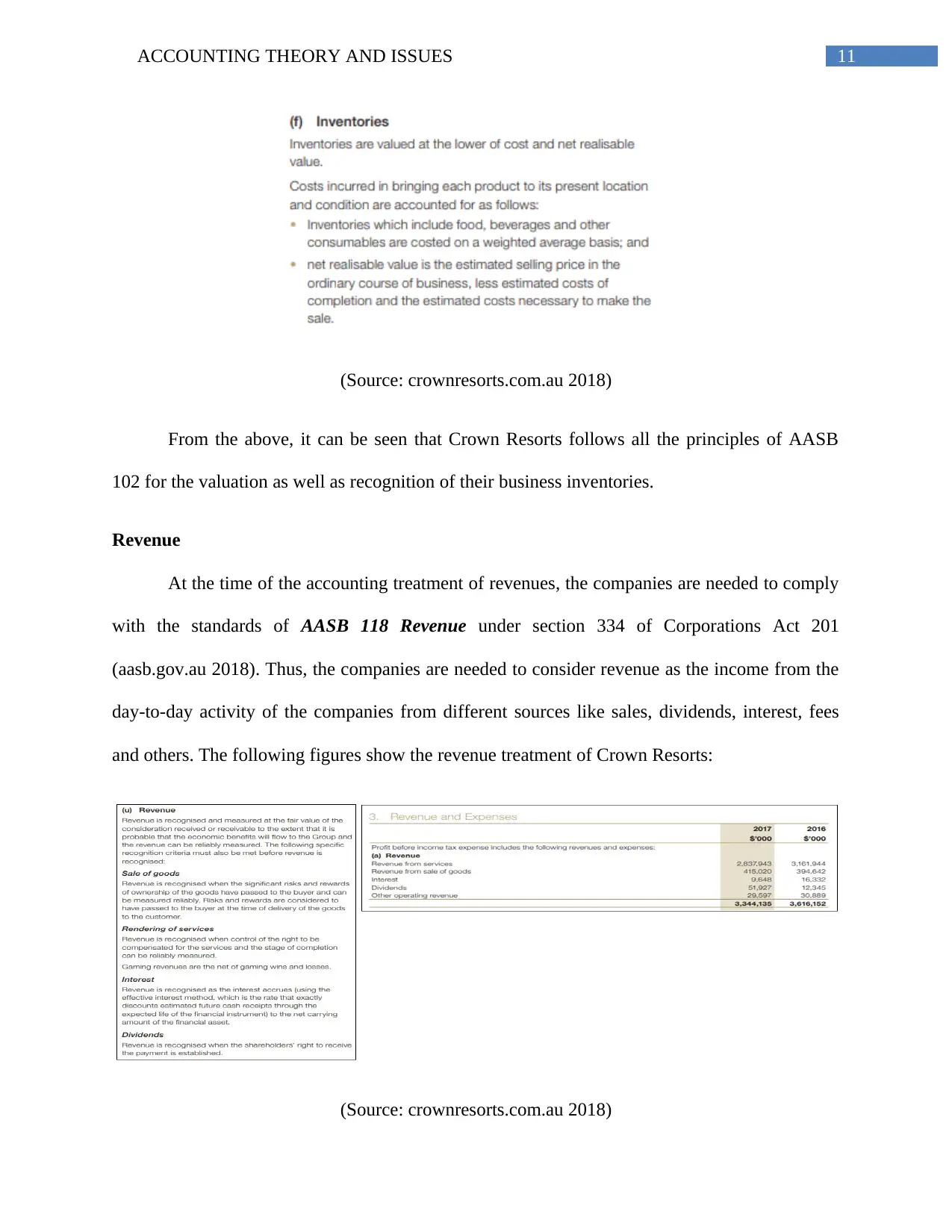

Inventories

The Australian Accounting Standard has provided all the regulations and standards for

the treatment of inventories in AASB 102 Inventories under section 334 of the Corporations Act

2001 (aasb.gov.au 2018). As per the guidelines of this section, the companies are needed to

recognize the expenses as well as the write downs to the net realizable value. The following

figure shows the inventory treatment by Crown Resorts:

It can be seen that Crown Resorts follows the AASB conceptual framework for the

accounting treatment of PPE.

Contingent Liability

Contingent liabilities are considered as the obligation of the companies occurring from

any past event. Timeliness needs to be there in the contingent liability for the availability of

proper information at the time to make the decisions related to these liabilities. All the required

accounting principles and standards for the treatment of contingent liabilities can be seen in

AASB 137 Provision, Contingent Liabilities and Contingent Assets under section 334

(aasb.gov.au 2018). There is a need to have verifiability characteristic in contingent liability so

that the users can gain understanding about these liabilities. The following figure shows the

contingent liability treatment in Crown Resorts:

(Source: crownresorts.com.au 2018)

Inventories

The Australian Accounting Standard has provided all the regulations and standards for

the treatment of inventories in AASB 102 Inventories under section 334 of the Corporations Act

2001 (aasb.gov.au 2018). As per the guidelines of this section, the companies are needed to

recognize the expenses as well as the write downs to the net realizable value. The following

figure shows the inventory treatment by Crown Resorts:

11ACCOUNTING THEORY AND ISSUES

(Source: crownresorts.com.au 2018)

From the above, it can be seen that Crown Resorts follows all the principles of AASB

102 for the valuation as well as recognition of their business inventories.

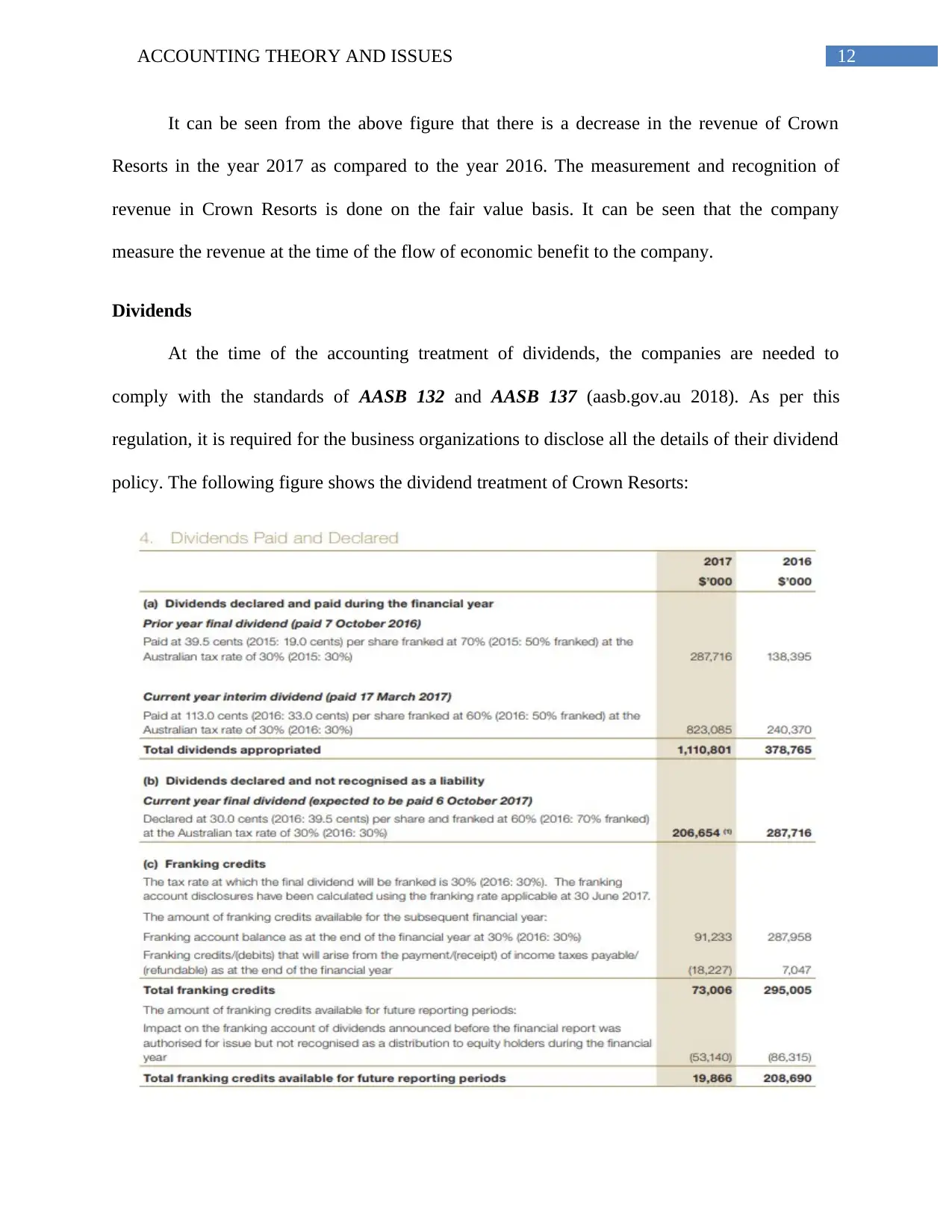

Revenue

At the time of the accounting treatment of revenues, the companies are needed to comply

with the standards of AASB 118 Revenue under section 334 of Corporations Act 201

(aasb.gov.au 2018). Thus, the companies are needed to consider revenue as the income from the

day-to-day activity of the companies from different sources like sales, dividends, interest, fees

and others. The following figures show the revenue treatment of Crown Resorts:

(Source: crownresorts.com.au 2018)

(Source: crownresorts.com.au 2018)

From the above, it can be seen that Crown Resorts follows all the principles of AASB

102 for the valuation as well as recognition of their business inventories.

Revenue

At the time of the accounting treatment of revenues, the companies are needed to comply

with the standards of AASB 118 Revenue under section 334 of Corporations Act 201

(aasb.gov.au 2018). Thus, the companies are needed to consider revenue as the income from the

day-to-day activity of the companies from different sources like sales, dividends, interest, fees

and others. The following figures show the revenue treatment of Crown Resorts:

(Source: crownresorts.com.au 2018)

12ACCOUNTING THEORY AND ISSUES

It can be seen from the above figure that there is a decrease in the revenue of Crown

Resorts in the year 2017 as compared to the year 2016. The measurement and recognition of

revenue in Crown Resorts is done on the fair value basis. It can be seen that the company

measure the revenue at the time of the flow of economic benefit to the company.

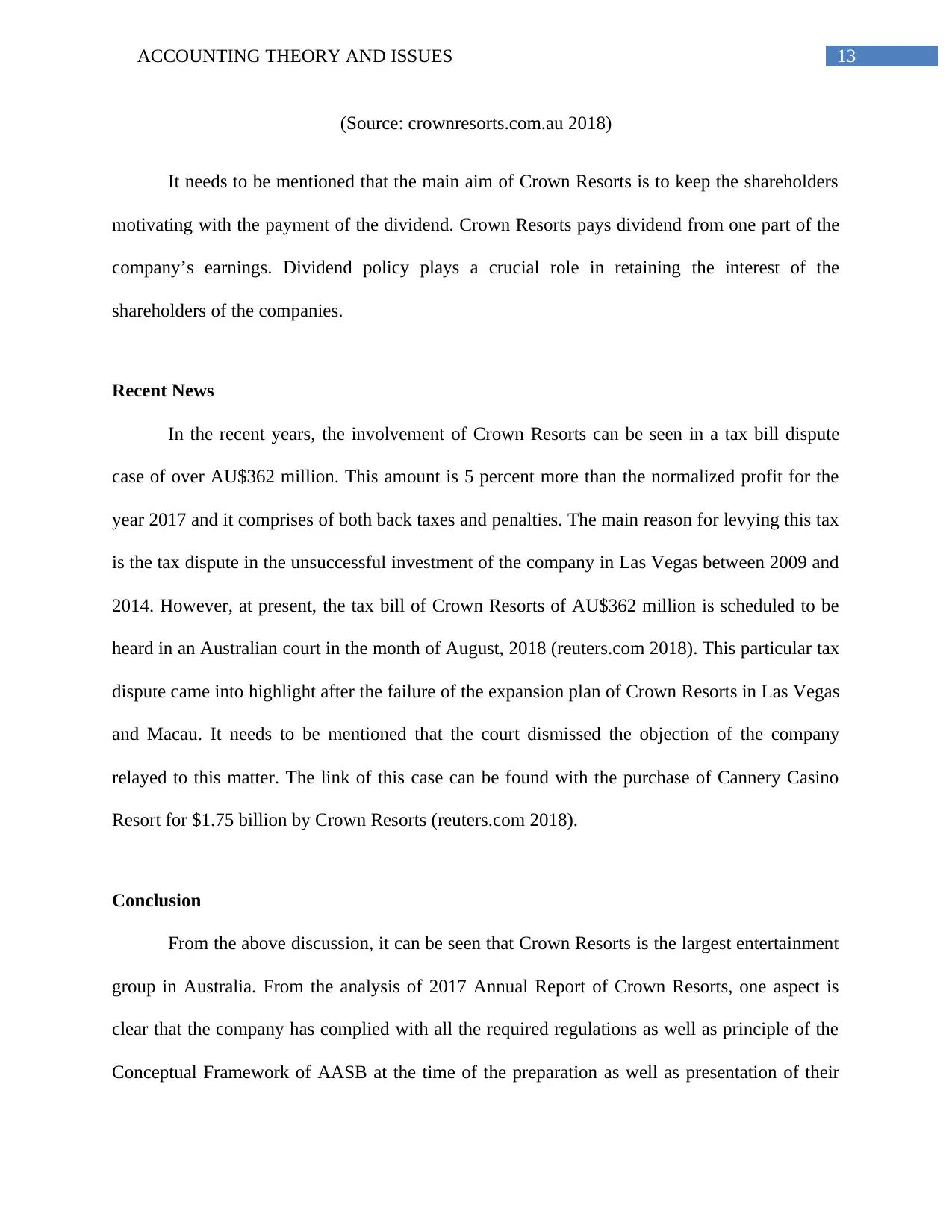

Dividends

At the time of the accounting treatment of dividends, the companies are needed to

comply with the standards of AASB 132 and AASB 137 (aasb.gov.au 2018). As per this

regulation, it is required for the business organizations to disclose all the details of their dividend

policy. The following figure shows the dividend treatment of Crown Resorts:

It can be seen from the above figure that there is a decrease in the revenue of Crown

Resorts in the year 2017 as compared to the year 2016. The measurement and recognition of

revenue in Crown Resorts is done on the fair value basis. It can be seen that the company

measure the revenue at the time of the flow of economic benefit to the company.

Dividends

At the time of the accounting treatment of dividends, the companies are needed to

comply with the standards of AASB 132 and AASB 137 (aasb.gov.au 2018). As per this

regulation, it is required for the business organizations to disclose all the details of their dividend

policy. The following figure shows the dividend treatment of Crown Resorts:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13ACCOUNTING THEORY AND ISSUES

(Source: crownresorts.com.au 2018)

It needs to be mentioned that the main aim of Crown Resorts is to keep the shareholders

motivating with the payment of the dividend. Crown Resorts pays dividend from one part of the

company’s earnings. Dividend policy plays a crucial role in retaining the interest of the

shareholders of the companies.

Recent News

In the recent years, the involvement of Crown Resorts can be seen in a tax bill dispute

case of over AU$362 million. This amount is 5 percent more than the normalized profit for the

year 2017 and it comprises of both back taxes and penalties. The main reason for levying this tax

is the tax dispute in the unsuccessful investment of the company in Las Vegas between 2009 and

2014. However, at present, the tax bill of Crown Resorts of AU$362 million is scheduled to be

heard in an Australian court in the month of August, 2018 (reuters.com 2018). This particular tax

dispute came into highlight after the failure of the expansion plan of Crown Resorts in Las Vegas

and Macau. It needs to be mentioned that the court dismissed the objection of the company

relayed to this matter. The link of this case can be found with the purchase of Cannery Casino

Resort for $1.75 billion by Crown Resorts (reuters.com 2018).

Conclusion

From the above discussion, it can be seen that Crown Resorts is the largest entertainment

group in Australia. From the analysis of 2017 Annual Report of Crown Resorts, one aspect is

clear that the company has complied with all the required regulations as well as principle of the

Conceptual Framework of AASB at the time of the preparation as well as presentation of their

(Source: crownresorts.com.au 2018)

It needs to be mentioned that the main aim of Crown Resorts is to keep the shareholders

motivating with the payment of the dividend. Crown Resorts pays dividend from one part of the

company’s earnings. Dividend policy plays a crucial role in retaining the interest of the

shareholders of the companies.

Recent News

In the recent years, the involvement of Crown Resorts can be seen in a tax bill dispute

case of over AU$362 million. This amount is 5 percent more than the normalized profit for the

year 2017 and it comprises of both back taxes and penalties. The main reason for levying this tax

is the tax dispute in the unsuccessful investment of the company in Las Vegas between 2009 and

2014. However, at present, the tax bill of Crown Resorts of AU$362 million is scheduled to be

heard in an Australian court in the month of August, 2018 (reuters.com 2018). This particular tax

dispute came into highlight after the failure of the expansion plan of Crown Resorts in Las Vegas

and Macau. It needs to be mentioned that the court dismissed the objection of the company

relayed to this matter. The link of this case can be found with the purchase of Cannery Casino

Resort for $1.75 billion by Crown Resorts (reuters.com 2018).

Conclusion

From the above discussion, it can be seen that Crown Resorts is the largest entertainment

group in Australia. From the analysis of 2017 Annual Report of Crown Resorts, one aspect is

clear that the company has complied with all the required regulations as well as principle of the

Conceptual Framework of AASB at the time of the preparation as well as presentation of their

14ACCOUNTING THEORY AND ISSUES

financial statements. It implies that Crown Resorts has been able in providing the true as well as

fair financial picture of their business. As a part of the compliance with the required GPFR

principles, Crown Resorts has provided all the required financial statements like income

statement, balance sheet, cash flow statement and the statement of change in equity. However,

from the analysis of the remuneration report, it can be seen that the senior executives of the

Crown Resorts has failed in achieving the required financial target. At the time of the accounting

treatment of assets, liabilities, contingent liabilities and others, the company follows different

principles of AASB Conceptual Framework. However, one area of worry for Crown Resorts is

their tax dispute of AU$362 million due to the failure in the investment in Las Vegas and Macau.

Hence, based on the above discussion, it can be seen that Crown Resorts has complied with the

conceptual framework for the purpose of their financial reporting.

financial statements. It implies that Crown Resorts has been able in providing the true as well as

fair financial picture of their business. As a part of the compliance with the required GPFR

principles, Crown Resorts has provided all the required financial statements like income

statement, balance sheet, cash flow statement and the statement of change in equity. However,

from the analysis of the remuneration report, it can be seen that the senior executives of the

Crown Resorts has failed in achieving the required financial target. At the time of the accounting

treatment of assets, liabilities, contingent liabilities and others, the company follows different

principles of AASB Conceptual Framework. However, one area of worry for Crown Resorts is

their tax dispute of AU$362 million due to the failure in the investment in Las Vegas and Macau.

Hence, based on the above discussion, it can be seen that Crown Resorts has complied with the

conceptual framework for the purpose of their financial reporting.

15ACCOUNTING THEORY AND ISSUES

References

Aasb.gov.au. (2018). Financial Instruments: Presentation. [online] Available at:

http://www.aasb.gov.au/admin/file/content105/c9/AASB132_07-04_COMPoct09_02-10.pdf

[Accessed 3 Aug. 2018].

Aasb.gov.au. (2018). Framework for the Preparation and Presentation of Financial Statements.

[online] Available at: http://www.aasb.gov.au/admin/file/content105/c9/Framework_07-

04_COMPjun14_07-14.pdf [Accessed 3 Aug. 2018].

Aasb.gov.au. (2018). Inventories. [online] Available at:

http://www.aasb.gov.au/admin/file/content105/c9/AASB102_07-04_COMPjun09_01-09.pdf

[Accessed 3 Aug. 2018].

Aasb.gov.au. (2018). Presentation of Financial Statements. [online] Available at:

http://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf [Accessed 3 Aug. 2018].

Aasb.gov.au. (2018). Property, Plant and Equipment. [online] Available at:

http://www.aasb.gov.au/admin/file/content105/c9/AASB116_08-15_COMPoct15_01-18.pdf

[Accessed 3 Aug. 2018].

Aasb.gov.au. (2018). Provisions, Contingent Liabilities and Contingent Assets. [online]

Available at: http://www.aasb.gov.au/admin/file/content105/c9/AASB137_07-

04_COMPjun14_04-14.pdf [Accessed 3 Aug. 2018].

References

Aasb.gov.au. (2018). Financial Instruments: Presentation. [online] Available at:

http://www.aasb.gov.au/admin/file/content105/c9/AASB132_07-04_COMPoct09_02-10.pdf

[Accessed 3 Aug. 2018].

Aasb.gov.au. (2018). Framework for the Preparation and Presentation of Financial Statements.

[online] Available at: http://www.aasb.gov.au/admin/file/content105/c9/Framework_07-

04_COMPjun14_07-14.pdf [Accessed 3 Aug. 2018].

Aasb.gov.au. (2018). Inventories. [online] Available at:

http://www.aasb.gov.au/admin/file/content105/c9/AASB102_07-04_COMPjun09_01-09.pdf

[Accessed 3 Aug. 2018].

Aasb.gov.au. (2018). Presentation of Financial Statements. [online] Available at:

http://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf [Accessed 3 Aug. 2018].

Aasb.gov.au. (2018). Property, Plant and Equipment. [online] Available at:

http://www.aasb.gov.au/admin/file/content105/c9/AASB116_08-15_COMPoct15_01-18.pdf

[Accessed 3 Aug. 2018].

Aasb.gov.au. (2018). Provisions, Contingent Liabilities and Contingent Assets. [online]

Available at: http://www.aasb.gov.au/admin/file/content105/c9/AASB137_07-

04_COMPjun14_04-14.pdf [Accessed 3 Aug. 2018].

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16ACCOUNTING THEORY AND ISSUES

Aasb.gov.au. (2018). Revenue. [online] Available at:

http://www.aasb.gov.au/admin/file/content105/c9/AASB118_07-04_COMPoct10_01-11.pdf

[Accessed 3 Aug. 2018].

Asx.com.au. (2018). [online] Available at:

https://www.asx.com.au/asx/share-price-research/company/CWN [Accessed 3 Aug. 2018].

Crownresorts.com.au. (2018). About Us | Crown Resorts - Crown Resorts . [online] Available at:

http://www.crownresorts.com.au/about-us/crown [Accessed 3 Aug. 2018].

Crownresorts.com.au. (2018). Annual Report 2017. [online] Available at:

http://www.crownresorts.com.au/CrownResorts/files/9d/9df41ad5-de12-465c-ad18-

2925ad3533fa.pdf [Accessed 3 Aug. 2018].

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial accounting.

Pearson Higher Education AU.

U.S. (2018). Crown Resorts' Australian tax dispute headed for court challenge. [online]

Available at: https://www.reuters.com/article/us-crown-resorts-court-tax/crown-resorts-

australian-tax-dispute-headed-for-court-challenge-idUSKBN1KF0CU [Accessed 3 Aug. 2018].

Warren, C., Reeve, J.M. and Duchac, J., 2013. Financial & managerial accounting. Cengage

Learning.

Zeff, S.A., 2013. The objectives of financial reporting: a historical survey and

analysis. Accounting and Business Research, 43(4), pp.262-327.

Aasb.gov.au. (2018). Revenue. [online] Available at:

http://www.aasb.gov.au/admin/file/content105/c9/AASB118_07-04_COMPoct10_01-11.pdf

[Accessed 3 Aug. 2018].

Asx.com.au. (2018). [online] Available at:

https://www.asx.com.au/asx/share-price-research/company/CWN [Accessed 3 Aug. 2018].

Crownresorts.com.au. (2018). About Us | Crown Resorts - Crown Resorts . [online] Available at:

http://www.crownresorts.com.au/about-us/crown [Accessed 3 Aug. 2018].

Crownresorts.com.au. (2018). Annual Report 2017. [online] Available at:

http://www.crownresorts.com.au/CrownResorts/files/9d/9df41ad5-de12-465c-ad18-

2925ad3533fa.pdf [Accessed 3 Aug. 2018].

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial accounting.

Pearson Higher Education AU.

U.S. (2018). Crown Resorts' Australian tax dispute headed for court challenge. [online]

Available at: https://www.reuters.com/article/us-crown-resorts-court-tax/crown-resorts-

australian-tax-dispute-headed-for-court-challenge-idUSKBN1KF0CU [Accessed 3 Aug. 2018].

Warren, C., Reeve, J.M. and Duchac, J., 2013. Financial & managerial accounting. Cengage

Learning.

Zeff, S.A., 2013. The objectives of financial reporting: a historical survey and

analysis. Accounting and Business Research, 43(4), pp.262-327.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.