Assessment Task 2: Prepare Financial Reports - BSBFIA401

VerifiedAdded on 2020/02/24

|18

|3875

|192

Report

AI Summary

This document presents a student's completed assignment for the BSBFIA401 Prepare Financial Reports unit. The assignment is divided into three main questions. Question 1 requires research and summarization of the Occupational Health & Safety Act 2004 (Vic), WHS Codes of Practice, and the Australian Consumer Law (ACL). Question 2 involves illustrating and explaining accounting principles (Matching Principle, Historic Cost Principle, Consistency Principle) and qualitative characteristics (Relevance, Disclosure, Comparability, Materiality, Reliability) with examples. The student was also required to present and discuss one example with another student in class. Question 3 presents a case study involving Rodney's business, requiring calculations for depreciation using the reducing balance method for an excavator and straight-line depreciation for a ute. This includes journal entries for depreciation and asset disposal, along with the completion of an asset register card. The assignment adheres to specific formatting and submission guidelines, including a cover sheet and a presentation component.

CRS157

Rev 104

July 2016

Page 1 of 18

Assessment Submission Cover Sheet(VET)

Student to complete relevant sections and attach this cover sheet to each assessment task for submission.

Student Information To be completed by Student

Student Name . Student ID .

Program/Course Information To be completed by Student

Department BDIT, Business Studies

Group/CRN/Block . Teacher Name Uthaya Kumaran, Carolyn Hayes,

Leanne Pagano, Ken Pattison

Qualification

Code FNS40615

FNS40215

FNS30315

Qualification Title Certificate 1V in Accounting, Certificate

1V in Bookkeeping, Certificate 111 in

Accounts Admin

Subject/Unit Code

(if cluster, list all the

clustered subjects/units)

BSBFIA401 Subject/Unit Title

(if cluster, list all the

clustered subjects/units)

Prepare Financial Reports

Assessment Information To be completed by Student

Assessment title Assessment Task 2Report and

Presentation

Assessment task 2 out of 4 Ffor

this subject/unit.

Due Date Session 8 during

class time

Date Submitted . Re-Submission ☐

Student Declaration

By submitting this assessment task and signing the below, I acknowledge and agree that:

1. This completed assessment task is my own work.

2. I understand the serious nature of plagiarism and I am aware of the penalties that exist for breaching this.

3. I have kept a copy of this assessment task.

4. The assessor may provide a copy of this assessment task to another member of the Institute for validation and/or

benchmarking purposes.

Student signature

For electronic submissions: By typing your name in the

student signature field, you are accepting the above

declaration.

Click here to enter text.

Assessor Feedback To be completed by Teacher/Assessor

Assessor to provide feedback to the student and document on this coversheet.

Click here to enter text.

Assessment Task Result ☐Satisfactory ☐Not Satisfactory☐ Other (e.g.points) Click here to

enter text.

Assessor Name Click here to enter

text.

Assessor Signature Date Click here to

enter a date.

Note: Final result of the subject/unit will be entered on Banner by the teacher/assessor once all assessment tasks have been assessed.

PUBLIC Holmesglen: MT BAF 3-Feb-2017 L:\Teaching\!AQTF Documents\Training Packages\2017 S1\FNS15\FNS40615 Certificate IV in Accounting\BSBFIA401 Prepare Financial Reports\Ass\A3\2017 S1 BSBFIA401 report- task 3 C

Day MT.docx

Rev 104

July 2016

Page 1 of 18

Assessment Submission Cover Sheet(VET)

Student to complete relevant sections and attach this cover sheet to each assessment task for submission.

Student Information To be completed by Student

Student Name . Student ID .

Program/Course Information To be completed by Student

Department BDIT, Business Studies

Group/CRN/Block . Teacher Name Uthaya Kumaran, Carolyn Hayes,

Leanne Pagano, Ken Pattison

Qualification

Code FNS40615

FNS40215

FNS30315

Qualification Title Certificate 1V in Accounting, Certificate

1V in Bookkeeping, Certificate 111 in

Accounts Admin

Subject/Unit Code

(if cluster, list all the

clustered subjects/units)

BSBFIA401 Subject/Unit Title

(if cluster, list all the

clustered subjects/units)

Prepare Financial Reports

Assessment Information To be completed by Student

Assessment title Assessment Task 2Report and

Presentation

Assessment task 2 out of 4 Ffor

this subject/unit.

Due Date Session 8 during

class time

Date Submitted . Re-Submission ☐

Student Declaration

By submitting this assessment task and signing the below, I acknowledge and agree that:

1. This completed assessment task is my own work.

2. I understand the serious nature of plagiarism and I am aware of the penalties that exist for breaching this.

3. I have kept a copy of this assessment task.

4. The assessor may provide a copy of this assessment task to another member of the Institute for validation and/or

benchmarking purposes.

Student signature

For electronic submissions: By typing your name in the

student signature field, you are accepting the above

declaration.

Click here to enter text.

Assessor Feedback To be completed by Teacher/Assessor

Assessor to provide feedback to the student and document on this coversheet.

Click here to enter text.

Assessment Task Result ☐Satisfactory ☐Not Satisfactory☐ Other (e.g.points) Click here to

enter text.

Assessor Name Click here to enter

text.

Assessor Signature Date Click here to

enter a date.

Note: Final result of the subject/unit will be entered on Banner by the teacher/assessor once all assessment tasks have been assessed.

PUBLIC Holmesglen: MT BAF 3-Feb-2017 L:\Teaching\!AQTF Documents\Training Packages\2017 S1\FNS15\FNS40615 Certificate IV in Accounting\BSBFIA401 Prepare Financial Reports\Ass\A3\2017 S1 BSBFIA401 report- task 3 C

Day MT.docx

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CRS157

Rev 104

July 2016

Page 2 of 18

PUBLIC Holmesglen: MT BAF 3-Feb-2017 L:\Teaching\!AQTF Documents\Training Packages\2017 S1\FNS15\FNS40615 Certificate IV in Accounting\BSBFIA401 Prepare Financial Reports\Ass\A3\2017 S1 BSBFIA401 report- task 3 C

Day MT.docx

Rev 104

July 2016

Page 2 of 18

PUBLIC Holmesglen: MT BAF 3-Feb-2017 L:\Teaching\!AQTF Documents\Training Packages\2017 S1\FNS15\FNS40615 Certificate IV in Accounting\BSBFIA401 Prepare Financial Reports\Ass\A3\2017 S1 BSBFIA401 report- task 3 C

Day MT.docx

CRS159

Revision 101

August 2016

Page 3 of 18

Assessment Instruction for Student

Section A – Program/Course details

Qualification Code FNS40615, FNS40215,

FNS30315 QualificationTitle

Certificate 1V in Accounting,

Certificate 1V in

Bookkeeping, Certificate

111 in Accounts Admin

Subject/Unit Code BSBFIM401 Subject/Unit Title Prepare Financial Reports

Section B – Assessment task details

Assessment

number Task 2 Semester/Year: Semester 2, 2017

Assessment title: Assignment and Presentation

Assessment method ☐A –Direct observation/

simulation activities

☒ B – Written/Verbal Questioning

☐ C – Third party evidence

☐ D – Portfolio/Product

☐E – Project/Report

☒ F – Presentation

☐ G – Role plays

☐ H – Practical demonstration

☐ I – Other

Assessment Task

Results

This assessment task will be marked as:

☒ Ungraded result: Satisfactory or Not Satisfactory

☐ Other (e.g. points): _______

Assessment

Task

Students must satisfactorily complete assignment to demonstrate skills and

knowledge as outlined in the Competency and below in the assessment

criteria.

Section C – Assessment Requirements

Conditions:

The assignment is to be completed in the students own time.

Use of computer resources - Office 2013, PC, Printer, Memory stick/USB/flash drive, internet access

Individual assessment (not group work)

Open Book, teacher feedback and assistance available

The student is to provide a hard copy (printed) to the teacher with the submission cover sheet completed and

signed at the front of the document.

Instructions to Learner: The assignment must be word processed and presented in a businesslikeand professional

manner, in line with industry standards. Summary of internet or other information sources is

expected, not just copy & paste.

Deadline/time limit –The due date for the assignment is in class time in session 8. The student is to provide a hard copy (printed) to the teacher with the submission cover sheet completed and

signed at the front of the document. The student is to present one element of the report to another member of the group (in pairs)and be able to

INTERNAL Holmesglen: chbaf 13-Apr-2017 L:\Teaching\!AQTF Documents\Training Packages\2017 S1\FNS15\FNS40615 Certificate IV in Accounting\BSBFIA401 Prepare Financial Reports\Ass\Instruction_Assessor BSBFIA401 Ass

2 V1 OL and Ev SOLUTION.docx

Revision 101

August 2016

Page 3 of 18

Assessment Instruction for Student

Section A – Program/Course details

Qualification Code FNS40615, FNS40215,

FNS30315 QualificationTitle

Certificate 1V in Accounting,

Certificate 1V in

Bookkeeping, Certificate

111 in Accounts Admin

Subject/Unit Code BSBFIM401 Subject/Unit Title Prepare Financial Reports

Section B – Assessment task details

Assessment

number Task 2 Semester/Year: Semester 2, 2017

Assessment title: Assignment and Presentation

Assessment method ☐A –Direct observation/

simulation activities

☒ B – Written/Verbal Questioning

☐ C – Third party evidence

☐ D – Portfolio/Product

☐E – Project/Report

☒ F – Presentation

☐ G – Role plays

☐ H – Practical demonstration

☐ I – Other

Assessment Task

Results

This assessment task will be marked as:

☒ Ungraded result: Satisfactory or Not Satisfactory

☐ Other (e.g. points): _______

Assessment

Task

Students must satisfactorily complete assignment to demonstrate skills and

knowledge as outlined in the Competency and below in the assessment

criteria.

Section C – Assessment Requirements

Conditions:

The assignment is to be completed in the students own time.

Use of computer resources - Office 2013, PC, Printer, Memory stick/USB/flash drive, internet access

Individual assessment (not group work)

Open Book, teacher feedback and assistance available

The student is to provide a hard copy (printed) to the teacher with the submission cover sheet completed and

signed at the front of the document.

Instructions to Learner: The assignment must be word processed and presented in a businesslikeand professional

manner, in line with industry standards. Summary of internet or other information sources is

expected, not just copy & paste.

Deadline/time limit –The due date for the assignment is in class time in session 8. The student is to provide a hard copy (printed) to the teacher with the submission cover sheet completed and

signed at the front of the document. The student is to present one element of the report to another member of the group (in pairs)and be able to

INTERNAL Holmesglen: chbaf 13-Apr-2017 L:\Teaching\!AQTF Documents\Training Packages\2017 S1\FNS15\FNS40615 Certificate IV in Accounting\BSBFIA401 Prepare Financial Reports\Ass\Instruction_Assessor BSBFIA401 Ass

2 V1 OL and Ev SOLUTION.docx

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CRS159

Revision 101

August 2016

Page 4 of 18

show an understanding of what they have written.

Section D – Assessment Criteria

Observation

of

competency

skill or

knowledge

(tick)

Assignment Questions and assessment criteria Satisfactory Unsatisfactory

KE, F-R,W

GWD

Question 1 – Student has shown evidence of research and been

able to summarize in own language

KE, F-

R,W,GWD

Question 2 – Student has been able to process the information and

draw conclusions.

KE, F-

R,W,GWD

Presentation: Oral presentation –

Students participated appropriately in roleplay/presentation as both

client and presenter.Student asks questions and responds

appropriately.

Students must be able to use appropriate and relevant language.

P, F-R,W Question 3 (1) Student needs to be able to calculate the capitalized

value of the asset

P, F-R,W

Question 3(1) Student needs to be able to recognize the period for

calculation of depreciation and calculate the appropriate

depreciation

P,K,F-R,W

Question 3(2) Students needs to be able record transactions in

general journal for depreciation calculations and disposal of an

asset.

P,F-R,W Question 3(3) Student needs to be able to correctly fill in details of

the asset on the asset register card.

Overall S or NS

ASSESSMENT TASK 2

Question (1)

Research each of the following areas of law (or pieces of legislation) and provide a

brief overview of the purpose of the particular law. Your response should be

approximately 150 – 200 words for each

Occupational Health & Safety Act 2004 (Vic) / WHS Codes of practice

The Australian Consumer Law (ACL)

INTERNAL Holmesglen: chbaf 13-Apr-2017 L:\Teaching\!AQTF Documents\Training Packages\2017 S1\FNS15\FNS40615 Certificate IV in Accounting\BSBFIA401 Prepare Financial Reports\Ass\Instruction_Assessor BSBFIA401 Ass

2 V1 OL and Ev SOLUTION.docx

Revision 101

August 2016

Page 4 of 18

show an understanding of what they have written.

Section D – Assessment Criteria

Observation

of

competency

skill or

knowledge

(tick)

Assignment Questions and assessment criteria Satisfactory Unsatisfactory

KE, F-R,W

GWD

Question 1 – Student has shown evidence of research and been

able to summarize in own language

KE, F-

R,W,GWD

Question 2 – Student has been able to process the information and

draw conclusions.

KE, F-

R,W,GWD

Presentation: Oral presentation –

Students participated appropriately in roleplay/presentation as both

client and presenter.Student asks questions and responds

appropriately.

Students must be able to use appropriate and relevant language.

P, F-R,W Question 3 (1) Student needs to be able to calculate the capitalized

value of the asset

P, F-R,W

Question 3(1) Student needs to be able to recognize the period for

calculation of depreciation and calculate the appropriate

depreciation

P,K,F-R,W

Question 3(2) Students needs to be able record transactions in

general journal for depreciation calculations and disposal of an

asset.

P,F-R,W Question 3(3) Student needs to be able to correctly fill in details of

the asset on the asset register card.

Overall S or NS

ASSESSMENT TASK 2

Question (1)

Research each of the following areas of law (or pieces of legislation) and provide a

brief overview of the purpose of the particular law. Your response should be

approximately 150 – 200 words for each

Occupational Health & Safety Act 2004 (Vic) / WHS Codes of practice

The Australian Consumer Law (ACL)

INTERNAL Holmesglen: chbaf 13-Apr-2017 L:\Teaching\!AQTF Documents\Training Packages\2017 S1\FNS15\FNS40615 Certificate IV in Accounting\BSBFIA401 Prepare Financial Reports\Ass\Instruction_Assessor BSBFIA401 Ass

2 V1 OL and Ev SOLUTION.docx

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CRS159

Revision 101

August 2016

Page 5 of 18

Occupational Health & Safety Act 2004 (Vic) / WHS Codes of practice:

The main objective of this Act is to form a legal framework to revoke the Occupational Health and Safety

Act 1985 and also to provide matters for involving a process of change and amendments by considering

changing norms of society(Botha and Cronjé, 2015). Act aims to ensure safety, well-being, health and

welfare of all employees at work. It also ensures that the health and safety of the public are not disturbed by

the conduct of employers. Formulation and implementation of policies and principles of health and safety

Act (section 4) are supported by team work by the involvement of employers and employees (Reese, 2015)..

The intent of parliament is that administration of the Act should be according to the principles of health and

safety protection set out in section 4. This Act came into functioning on 1 july2005.

The Australian Consumer Law (ACL)

Australian consumer law is made to protect the right and interest of every consumer in Australia. This law

deals with fair trading practice and protects the interest of the consumer. This law replaces many former

consumer laws, and it is applied across Australia (Zohar, 2014). Australian consumer law is scheduled to

Competition and Consumer Act 2010, and it is jointly regulated by Australian competition and consumer

commission (ACCC) and state and territory consumer protection agencies. In some relevant matters,

Australian Securities and investment commissions (ASIC) are also involved (Collier, 2015).

In 2005 government of Australia feel to bring reforms in consumer law then in 2006, a task force is made

which in 2008 present the draft of development and implementation national consumer law. This law

protects consumer from misleading, unfair conduct of businesses. Goods and services which consumer

purchased are mandatorily covered by consumer guarantees (Kloss, 2013). This means businesses must fulfil

all the necessary rule and regulation of ACL. .

INTERNAL Holmesglen: chbaf 13-Apr-2017 L:\Teaching\!AQTF Documents\Training Packages\2017 S1\FNS15\FNS40615 Certificate IV in Accounting\BSBFIA401 Prepare Financial Reports\Ass\Instruction_Assessor BSBFIA401 Ass

2 V1 OL and Ev SOLUTION.docx

Revision 101

August 2016

Page 5 of 18

Occupational Health & Safety Act 2004 (Vic) / WHS Codes of practice:

The main objective of this Act is to form a legal framework to revoke the Occupational Health and Safety

Act 1985 and also to provide matters for involving a process of change and amendments by considering

changing norms of society(Botha and Cronjé, 2015). Act aims to ensure safety, well-being, health and

welfare of all employees at work. It also ensures that the health and safety of the public are not disturbed by

the conduct of employers. Formulation and implementation of policies and principles of health and safety

Act (section 4) are supported by team work by the involvement of employers and employees (Reese, 2015)..

The intent of parliament is that administration of the Act should be according to the principles of health and

safety protection set out in section 4. This Act came into functioning on 1 july2005.

The Australian Consumer Law (ACL)

Australian consumer law is made to protect the right and interest of every consumer in Australia. This law

deals with fair trading practice and protects the interest of the consumer. This law replaces many former

consumer laws, and it is applied across Australia (Zohar, 2014). Australian consumer law is scheduled to

Competition and Consumer Act 2010, and it is jointly regulated by Australian competition and consumer

commission (ACCC) and state and territory consumer protection agencies. In some relevant matters,

Australian Securities and investment commissions (ASIC) are also involved (Collier, 2015).

In 2005 government of Australia feel to bring reforms in consumer law then in 2006, a task force is made

which in 2008 present the draft of development and implementation national consumer law. This law

protects consumer from misleading, unfair conduct of businesses. Goods and services which consumer

purchased are mandatorily covered by consumer guarantees (Kloss, 2013). This means businesses must fulfil

all the necessary rule and regulation of ACL. .

INTERNAL Holmesglen: chbaf 13-Apr-2017 L:\Teaching\!AQTF Documents\Training Packages\2017 S1\FNS15\FNS40615 Certificate IV in Accounting\BSBFIA401 Prepare Financial Reports\Ass\Instruction_Assessor BSBFIA401 Ass

2 V1 OL and Ev SOLUTION.docx

CRS159

Revision 101

August 2016

Page 6 of 18

Question (2)

Chose one each from the given list of accounting principlesor qualitative

characteristics and illustrate them with an example. Your response should be

approximately 150 – 250 words for each. You will be required to present/ explain

your example to another student in class. You will then swap roles and also you can

pose questions to the presenter in order to clarify their understanding of the chosen

principle or characteristic.

Accounting principles Qualitative characteristics

Matching principle Relevance

Historic Cost Principle Disclosure

Comparability Materiality

Consistency Principle Reliability

INTERNAL Holmesglen: chbaf 13-Apr-2017 L:\Teaching\!AQTF Documents\Training Packages\2017 S1\FNS15\FNS40615 Certificate IV in Accounting\BSBFIA401 Prepare Financial Reports\Ass\Instruction_Assessor BSBFIA401 Ass

2 V1 OL and Ev SOLUTION.docx

Revision 101

August 2016

Page 6 of 18

Question (2)

Chose one each from the given list of accounting principlesor qualitative

characteristics and illustrate them with an example. Your response should be

approximately 150 – 250 words for each. You will be required to present/ explain

your example to another student in class. You will then swap roles and also you can

pose questions to the presenter in order to clarify their understanding of the chosen

principle or characteristic.

Accounting principles Qualitative characteristics

Matching principle Relevance

Historic Cost Principle Disclosure

Comparability Materiality

Consistency Principle Reliability

INTERNAL Holmesglen: chbaf 13-Apr-2017 L:\Teaching\!AQTF Documents\Training Packages\2017 S1\FNS15\FNS40615 Certificate IV in Accounting\BSBFIA401 Prepare Financial Reports\Ass\Instruction_Assessor BSBFIA401 Ass

2 V1 OL and Ev SOLUTION.docx

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CRS159

Revision 101

August 2016

Page 7 of 18

Accounting principles: Matching Principle

The matching principle is practice for recording accounting transactions in which firms recognize

revenues and their expenses related to accounting transactions in the same accounting period. In accordance

with this principle business is required to show an expense on their profit and loss account in the accounting

period in which related revenue is recognised. This principle provides business a systematic allocation of

incurred expenses in the accounting periods to avoid misstating of earnings.

Cited principle is combination of accrual accounting and revenue recognition principle which states that

transactions must be recorded as they occurred irrespective of their associated cash transaction and earning

should be recognised while accounting transaction no at the time of receiving of cash ((Dimitropoulos and et

al. 2014)).

For example:

If a company had made advertisement expenses for promotion of sales by signing a contract with celebrity

then entire cost paid will not be recorded in same year as this promotion will provide long term benefit to

business. As a consequence, advertisement expenses will be deferred into multiple years as per matching

principle.

Qualitative characteristics: Materiality

Materiality concept states that only those financial information could be added to the financial statement

which would be capable of changing the decision of stakeholders of the enterprise. The materiality of

financial information varies from entity to entity. Other principals are ignored if the information is not

material and same is not included in financial statement (Landsbergis and et al. 2014). Materiality is

depending upon several factors like sum of total amount of immaterial financial information, size and nature

of the organization.

For example – Fire has occurred in a factory of the organization and stock is destroyed due to the same.

After a long fight with the insurance company, the organization says it is an abnormal loss of $5000. Net

income of the organization is $1000000, so in this case material concept says that it is not relevant

information because the amount of loss is not affecting much to the organization (Weygandt and et al. 2015).

On the other hand, if the same situation will arise in front of an organization whose net income is $50000

then it is material information for the entity and their stakeholders.

INTERNAL Holmesglen: chbaf 13-Apr-2017 L:\Teaching\!AQTF Documents\Training Packages\2017 S1\FNS15\FNS40615 Certificate IV in Accounting\BSBFIA401 Prepare Financial Reports\Ass\Instruction_Assessor BSBFIA401 Ass

2 V1 OL and Ev SOLUTION.docx

Revision 101

August 2016

Page 7 of 18

Accounting principles: Matching Principle

The matching principle is practice for recording accounting transactions in which firms recognize

revenues and their expenses related to accounting transactions in the same accounting period. In accordance

with this principle business is required to show an expense on their profit and loss account in the accounting

period in which related revenue is recognised. This principle provides business a systematic allocation of

incurred expenses in the accounting periods to avoid misstating of earnings.

Cited principle is combination of accrual accounting and revenue recognition principle which states that

transactions must be recorded as they occurred irrespective of their associated cash transaction and earning

should be recognised while accounting transaction no at the time of receiving of cash ((Dimitropoulos and et

al. 2014)).

For example:

If a company had made advertisement expenses for promotion of sales by signing a contract with celebrity

then entire cost paid will not be recorded in same year as this promotion will provide long term benefit to

business. As a consequence, advertisement expenses will be deferred into multiple years as per matching

principle.

Qualitative characteristics: Materiality

Materiality concept states that only those financial information could be added to the financial statement

which would be capable of changing the decision of stakeholders of the enterprise. The materiality of

financial information varies from entity to entity. Other principals are ignored if the information is not

material and same is not included in financial statement (Landsbergis and et al. 2014). Materiality is

depending upon several factors like sum of total amount of immaterial financial information, size and nature

of the organization.

For example – Fire has occurred in a factory of the organization and stock is destroyed due to the same.

After a long fight with the insurance company, the organization says it is an abnormal loss of $5000. Net

income of the organization is $1000000, so in this case material concept says that it is not relevant

information because the amount of loss is not affecting much to the organization (Weygandt and et al. 2015).

On the other hand, if the same situation will arise in front of an organization whose net income is $50000

then it is material information for the entity and their stakeholders.

INTERNAL Holmesglen: chbaf 13-Apr-2017 L:\Teaching\!AQTF Documents\Training Packages\2017 S1\FNS15\FNS40615 Certificate IV in Accounting\BSBFIA401 Prepare Financial Reports\Ass\Instruction_Assessor BSBFIA401 Ass

2 V1 OL and Ev SOLUTION.docx

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CRS159

Revision 101

August 2016

Page 8 of 18

2)

Question (3)

Rodney has been providing demolition and excavation service for the past seven

years. On the 1 October 2012, Rodney bought a new excavatorfor $88,000 including

GST from Farm Machinery P/L. Its registration number was JDH 123 and he decided to

keep the excavator in shed number 1.

Additional costs associated with this purchase included:

Cab air conditioning $990 (inc GST)

Delivery fee $1,100 (inc GST

Registration $600 (GST free)

Insurance $550 (inc GST)

He made a deposit of $10,000 and financed the remainder by negotiating a loan from

the Farmer’s Union. The balance of the loan was due on the1 March 2013.Because

the efficiency of excavator reduces over time it was decided to depreciate the

excavator using the reducing balance method at a rate of 15% per annum.

January 2013 proved to be a good season for excavation work with perfect weather

and large amount of road work in Melbourne. On the 1February 2013Rodney

received a cheque for $330,000 which included GST for the services he had provided.

Rodney had coveted a cool new red Holden Storm HBD ute for years and with his

higher than expected cheque decided that he could afford one. On the 1 April 2013

he purchased his ute registration number “Cool Wally” for cash from Nhill Cool Cars

for a sum of $38,500 including GST. To protect its shiny duco Wally decided to park

the ute under the carport rather than out in the paddock.

Additional Costs associated with this purchase included:

Air Conditioning $770 (inc GST)

Tow Bar $550 (inc GST)

Registration $500 (GST free)

Insurance $440 (inc GST)

The estimated residual value of the ute after 5 years was expected to be $6,200. It

was decided to depreciate the ute on a straight line basis.

INTERNAL Holmesglen: chbaf 13-Apr-2017 L:\Teaching\!AQTF Documents\Training Packages\2017 S1\FNS15\FNS40615 Certificate IV in Accounting\BSBFIA401 Prepare Financial Reports\Ass\Instruction_Assessor BSBFIA401 Ass

2 V1 OL and Ev SOLUTION.docx

Revision 101

August 2016

Page 8 of 18

2)

Question (3)

Rodney has been providing demolition and excavation service for the past seven

years. On the 1 October 2012, Rodney bought a new excavatorfor $88,000 including

GST from Farm Machinery P/L. Its registration number was JDH 123 and he decided to

keep the excavator in shed number 1.

Additional costs associated with this purchase included:

Cab air conditioning $990 (inc GST)

Delivery fee $1,100 (inc GST

Registration $600 (GST free)

Insurance $550 (inc GST)

He made a deposit of $10,000 and financed the remainder by negotiating a loan from

the Farmer’s Union. The balance of the loan was due on the1 March 2013.Because

the efficiency of excavator reduces over time it was decided to depreciate the

excavator using the reducing balance method at a rate of 15% per annum.

January 2013 proved to be a good season for excavation work with perfect weather

and large amount of road work in Melbourne. On the 1February 2013Rodney

received a cheque for $330,000 which included GST for the services he had provided.

Rodney had coveted a cool new red Holden Storm HBD ute for years and with his

higher than expected cheque decided that he could afford one. On the 1 April 2013

he purchased his ute registration number “Cool Wally” for cash from Nhill Cool Cars

for a sum of $38,500 including GST. To protect its shiny duco Wally decided to park

the ute under the carport rather than out in the paddock.

Additional Costs associated with this purchase included:

Air Conditioning $770 (inc GST)

Tow Bar $550 (inc GST)

Registration $500 (GST free)

Insurance $440 (inc GST)

The estimated residual value of the ute after 5 years was expected to be $6,200. It

was decided to depreciate the ute on a straight line basis.

INTERNAL Holmesglen: chbaf 13-Apr-2017 L:\Teaching\!AQTF Documents\Training Packages\2017 S1\FNS15\FNS40615 Certificate IV in Accounting\BSBFIA401 Prepare Financial Reports\Ass\Instruction_Assessor BSBFIA401 Ass

2 V1 OL and Ev SOLUTION.docx

CRS159

Revision 101

August 2016

Page 9 of 18

On 1January 2015 after Rodney’s new girlfriend had told him that she was too

embarrassed to be seen in a red ute, Rodney traded in his red ute for a yellow one.

Nhill Cool Cars offered him a trade in of $25,000 on his old ute. The new yellow ute’s

cost was $44,000 including GST and cash was paid for the balance.

Additional Information:

20 May 2013 An electrical fault on the ute was repaired under guarantee

(no cost)

15 July 2013 Ute was serviced By Nhill Motors at a cost of $198 including

GST

22 October 2013 Excavatorreceived its annual service from Farm Machinery P/L

at a cost of $440 including GST

29 October 2013 Dent in ute after Rodney came home late one night from the

pub and hit the gate post was repaired by Dents R Us at a cost

of $1,100 including GST

20 April 2014 Ute serviced by Nhill Cool cars at a cost of $220 including GST

15 October 2014 Excavator received its annual service from Farm Machinery P/L

at a cost of $770 including GST

Required

1. Please show workings as indicated.

2. Record all the transactions in the general journal

3. Complete the asset register cards for the Excavator

Workings

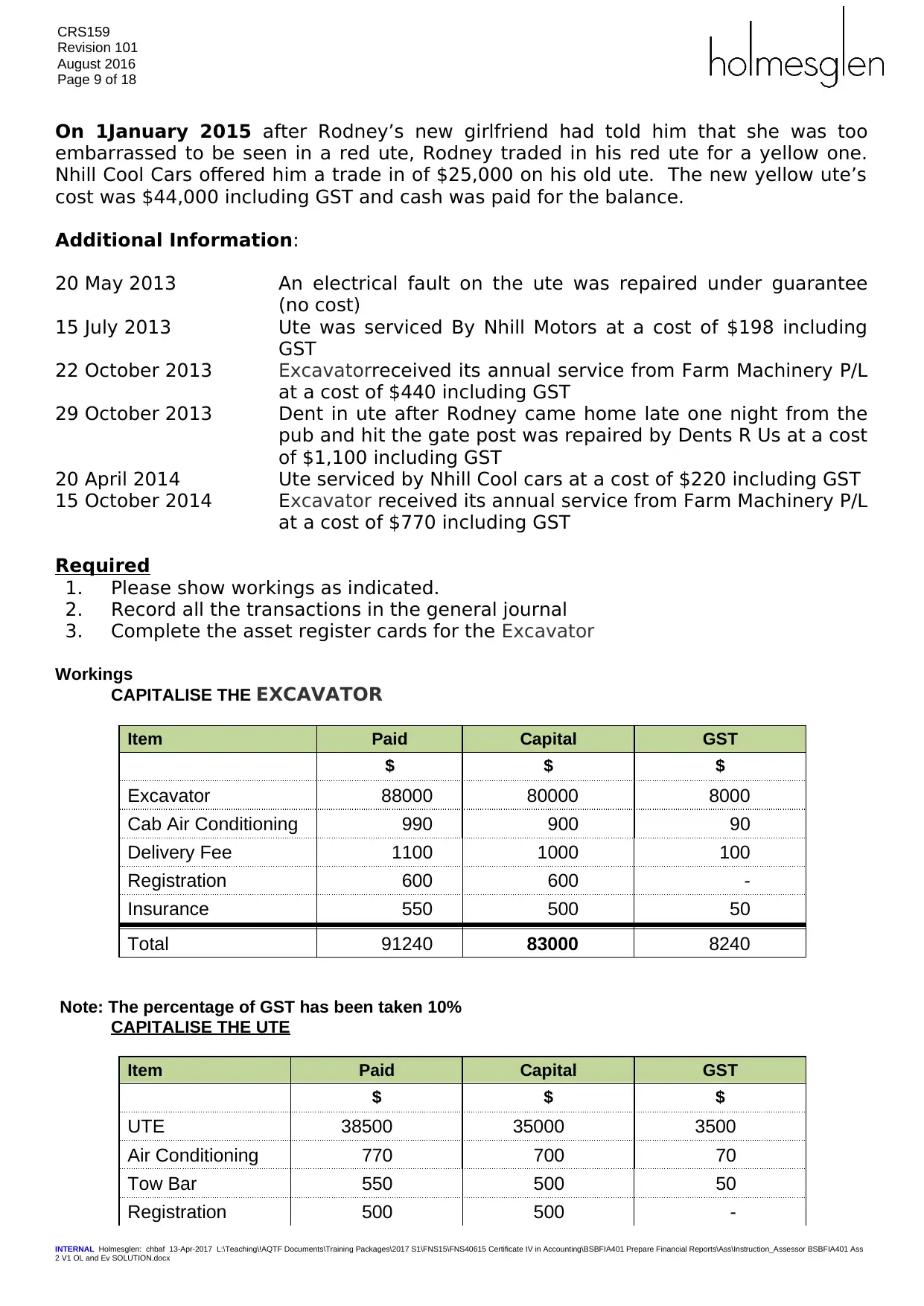

CAPITALISE THE EXCAVATOR

Item Paid Capital GST

$ $ $

Excavator 88000 80000 8000

Cab Air Conditioning 990 900 90

Delivery Fee 1100 1000 100

Registration 600 600 -

Insurance 550 500 50

Total 91240 83000 8240

Note: The percentage of GST has been taken 10%

CAPITALISE THE UTE

Item Paid Capital GST

$ $ $

UTE 38500 35000 3500

Air Conditioning 770 700 70

Tow Bar 550 500 50

Registration 500 500 -

INTERNAL Holmesglen: chbaf 13-Apr-2017 L:\Teaching\!AQTF Documents\Training Packages\2017 S1\FNS15\FNS40615 Certificate IV in Accounting\BSBFIA401 Prepare Financial Reports\Ass\Instruction_Assessor BSBFIA401 Ass

2 V1 OL and Ev SOLUTION.docx

Revision 101

August 2016

Page 9 of 18

On 1January 2015 after Rodney’s new girlfriend had told him that she was too

embarrassed to be seen in a red ute, Rodney traded in his red ute for a yellow one.

Nhill Cool Cars offered him a trade in of $25,000 on his old ute. The new yellow ute’s

cost was $44,000 including GST and cash was paid for the balance.

Additional Information:

20 May 2013 An electrical fault on the ute was repaired under guarantee

(no cost)

15 July 2013 Ute was serviced By Nhill Motors at a cost of $198 including

GST

22 October 2013 Excavatorreceived its annual service from Farm Machinery P/L

at a cost of $440 including GST

29 October 2013 Dent in ute after Rodney came home late one night from the

pub and hit the gate post was repaired by Dents R Us at a cost

of $1,100 including GST

20 April 2014 Ute serviced by Nhill Cool cars at a cost of $220 including GST

15 October 2014 Excavator received its annual service from Farm Machinery P/L

at a cost of $770 including GST

Required

1. Please show workings as indicated.

2. Record all the transactions in the general journal

3. Complete the asset register cards for the Excavator

Workings

CAPITALISE THE EXCAVATOR

Item Paid Capital GST

$ $ $

Excavator 88000 80000 8000

Cab Air Conditioning 990 900 90

Delivery Fee 1100 1000 100

Registration 600 600 -

Insurance 550 500 50

Total 91240 83000 8240

Note: The percentage of GST has been taken 10%

CAPITALISE THE UTE

Item Paid Capital GST

$ $ $

UTE 38500 35000 3500

Air Conditioning 770 700 70

Tow Bar 550 500 50

Registration 500 500 -

INTERNAL Holmesglen: chbaf 13-Apr-2017 L:\Teaching\!AQTF Documents\Training Packages\2017 S1\FNS15\FNS40615 Certificate IV in Accounting\BSBFIA401 Prepare Financial Reports\Ass\Instruction_Assessor BSBFIA401 Ass

2 V1 OL and Ev SOLUTION.docx

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CRS159

Revision 101

August 2016

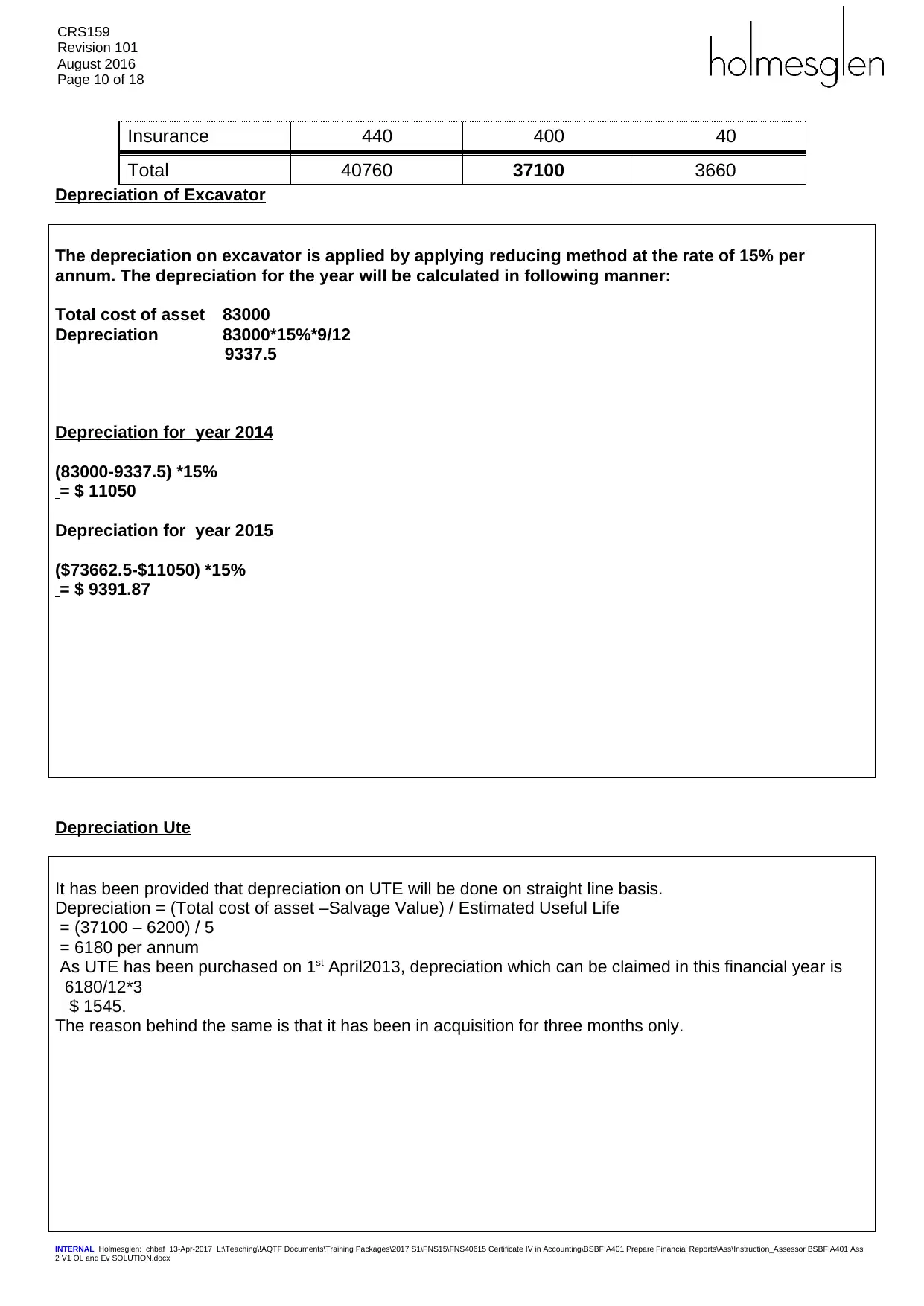

Page 10 of 18

Insurance 440 400 40

Total 40760 37100 3660

Depreciation of Excavator

The depreciation on excavator is applied by applying reducing method at the rate of 15% per

annum. The depreciation for the year will be calculated in following manner:

Total cost of asset 83000

Depreciation 83000*15%*9/12

9337.5

Depreciation for year 2014

(83000-9337.5) *15%

= $ 11050

Depreciation for year 2015

($73662.5-$11050) *15%

= $ 9391.87

Depreciation Ute

It has been provided that depreciation on UTE will be done on straight line basis.

Depreciation = (Total cost of asset –Salvage Value) / Estimated Useful Life

= (37100 – 6200) / 5

= 6180 per annum

As UTE has been purchased on 1st April2013, depreciation which can be claimed in this financial year is

6180/12*3

$ 1545.

The reason behind the same is that it has been in acquisition for three months only.

INTERNAL Holmesglen: chbaf 13-Apr-2017 L:\Teaching\!AQTF Documents\Training Packages\2017 S1\FNS15\FNS40615 Certificate IV in Accounting\BSBFIA401 Prepare Financial Reports\Ass\Instruction_Assessor BSBFIA401 Ass

2 V1 OL and Ev SOLUTION.docx

Revision 101

August 2016

Page 10 of 18

Insurance 440 400 40

Total 40760 37100 3660

Depreciation of Excavator

The depreciation on excavator is applied by applying reducing method at the rate of 15% per

annum. The depreciation for the year will be calculated in following manner:

Total cost of asset 83000

Depreciation 83000*15%*9/12

9337.5

Depreciation for year 2014

(83000-9337.5) *15%

= $ 11050

Depreciation for year 2015

($73662.5-$11050) *15%

= $ 9391.87

Depreciation Ute

It has been provided that depreciation on UTE will be done on straight line basis.

Depreciation = (Total cost of asset –Salvage Value) / Estimated Useful Life

= (37100 – 6200) / 5

= 6180 per annum

As UTE has been purchased on 1st April2013, depreciation which can be claimed in this financial year is

6180/12*3

$ 1545.

The reason behind the same is that it has been in acquisition for three months only.

INTERNAL Holmesglen: chbaf 13-Apr-2017 L:\Teaching\!AQTF Documents\Training Packages\2017 S1\FNS15\FNS40615 Certificate IV in Accounting\BSBFIA401 Prepare Financial Reports\Ass\Instruction_Assessor BSBFIA401 Ass

2 V1 OL and Ev SOLUTION.docx

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CRS159

Revision 101

August 2016

Page 11 of 18

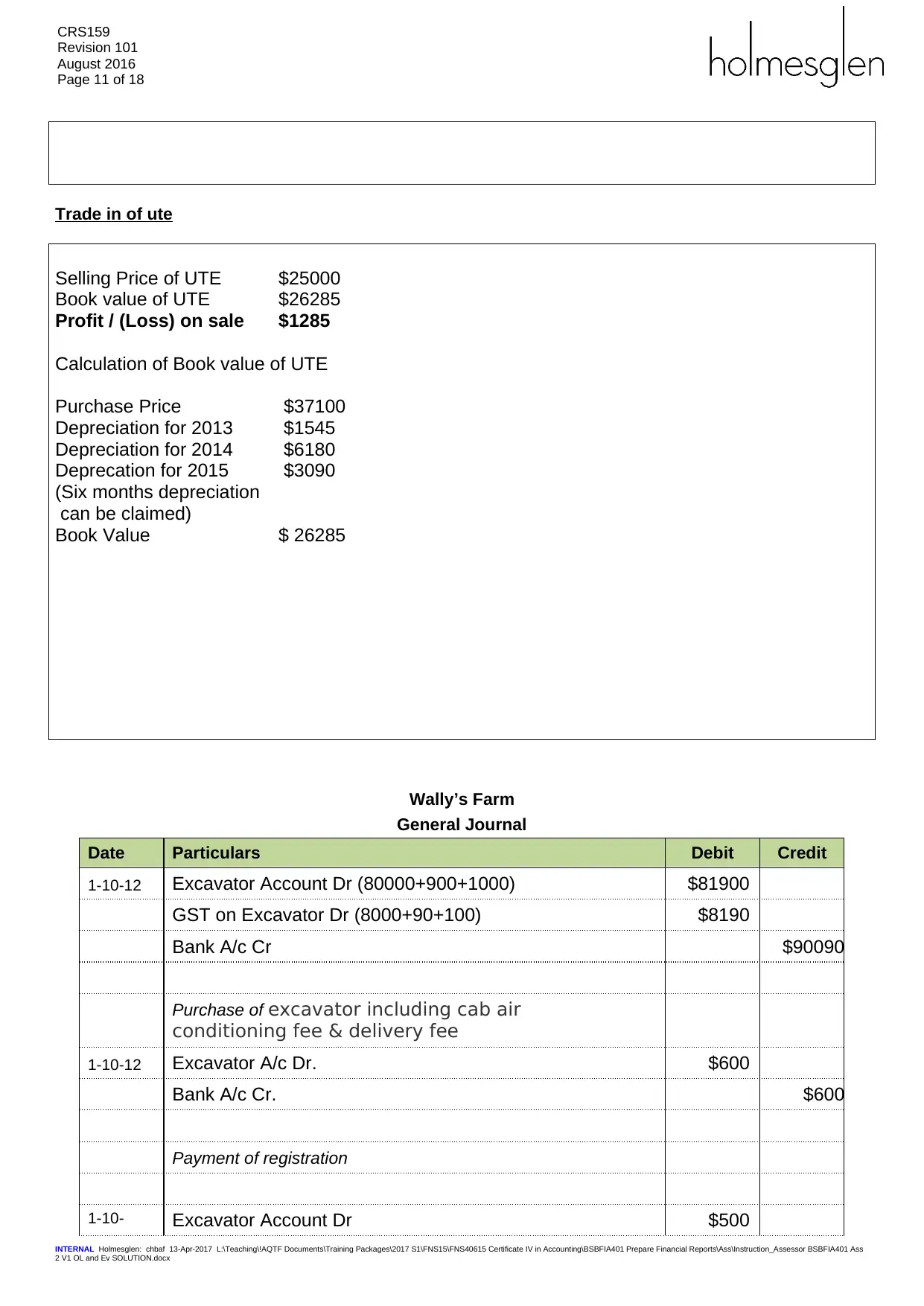

Trade in of ute

Selling Price of UTE $25000

Book value of UTE $26285

Profit / (Loss) on sale $1285

Calculation of Book value of UTE

Purchase Price $37100

Depreciation for 2013 $1545

Depreciation for 2014 $6180

Deprecation for 2015 $3090

(Six months depreciation

can be claimed)

Book Value $ 26285

Wally’s Farm

General Journal

Date Particulars Debit Credit

1-10-12 Excavator Account Dr (80000+900+1000) $81900

GST on Excavator Dr (8000+90+100) $8190

Bank A/c Cr $90090

Purchase of excavator including cab air

conditioning fee & delivery fee

1-10-12 Excavator A/c Dr. $600

Bank A/c Cr. $600

Payment of registration

1-10- Excavator Account Dr $500

INTERNAL Holmesglen: chbaf 13-Apr-2017 L:\Teaching\!AQTF Documents\Training Packages\2017 S1\FNS15\FNS40615 Certificate IV in Accounting\BSBFIA401 Prepare Financial Reports\Ass\Instruction_Assessor BSBFIA401 Ass

2 V1 OL and Ev SOLUTION.docx

Revision 101

August 2016

Page 11 of 18

Trade in of ute

Selling Price of UTE $25000

Book value of UTE $26285

Profit / (Loss) on sale $1285

Calculation of Book value of UTE

Purchase Price $37100

Depreciation for 2013 $1545

Depreciation for 2014 $6180

Deprecation for 2015 $3090

(Six months depreciation

can be claimed)

Book Value $ 26285

Wally’s Farm

General Journal

Date Particulars Debit Credit

1-10-12 Excavator Account Dr (80000+900+1000) $81900

GST on Excavator Dr (8000+90+100) $8190

Bank A/c Cr $90090

Purchase of excavator including cab air

conditioning fee & delivery fee

1-10-12 Excavator A/c Dr. $600

Bank A/c Cr. $600

Payment of registration

1-10- Excavator Account Dr $500

INTERNAL Holmesglen: chbaf 13-Apr-2017 L:\Teaching\!AQTF Documents\Training Packages\2017 S1\FNS15\FNS40615 Certificate IV in Accounting\BSBFIA401 Prepare Financial Reports\Ass\Instruction_Assessor BSBFIA401 Ass

2 V1 OL and Ev SOLUTION.docx

CRS159

Revision 101

August 2016

Page 12 of 18

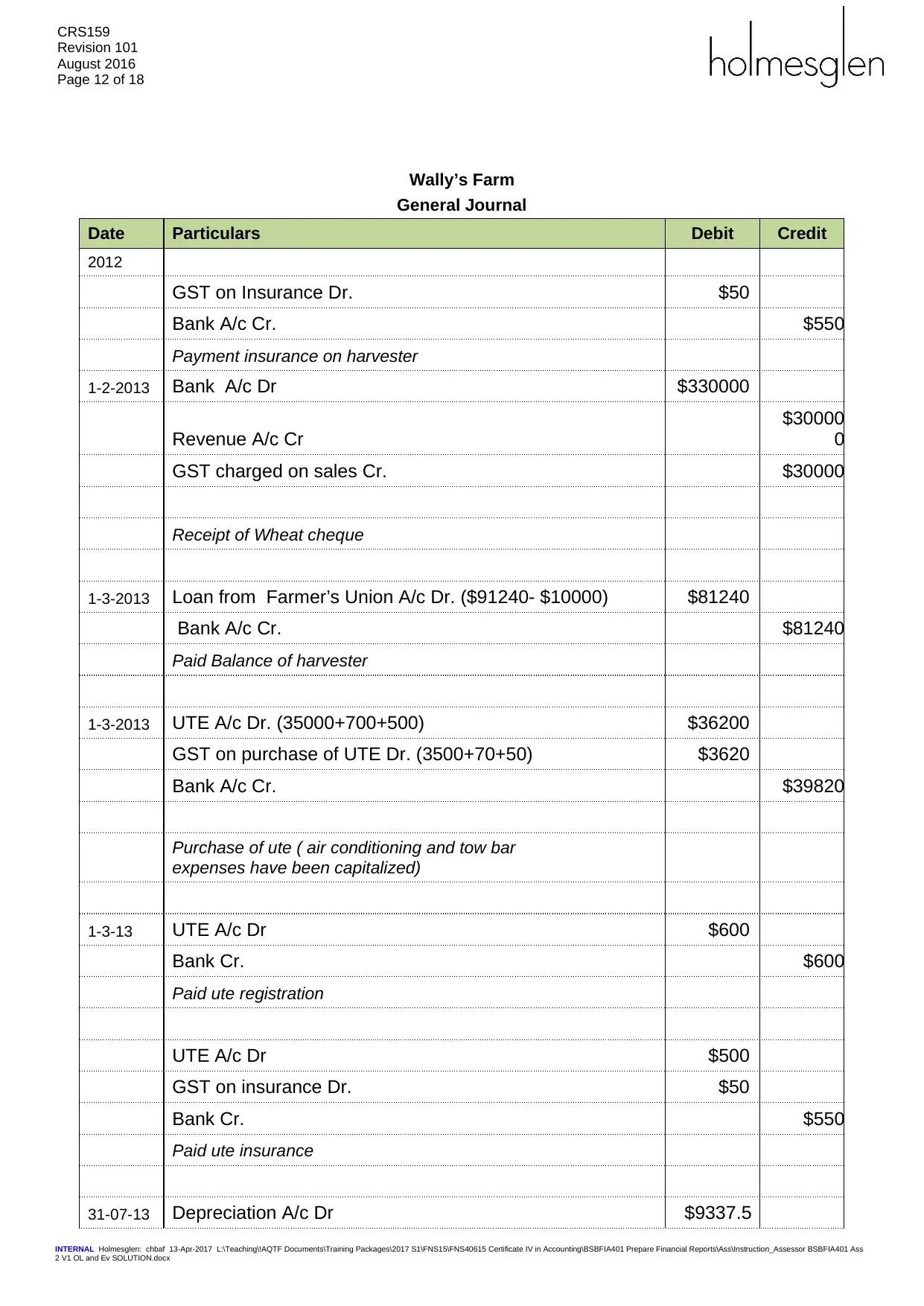

Wally’s Farm

General Journal

Date Particulars Debit Credit

2012

GST on Insurance Dr. $50

Bank A/c Cr. $550

Payment insurance on harvester

1-2-2013 Bank A/c Dr $330000

Revenue A/c Cr

$30000

0

GST charged on sales Cr. $30000

Receipt of Wheat cheque

1-3-2013 Loan from Farmer’s Union A/c Dr. ($91240- $10000) $81240

Bank A/c Cr. $81240

Paid Balance of harvester

1-3-2013 UTE A/c Dr. (35000+700+500) $36200

GST on purchase of UTE Dr. (3500+70+50) $3620

Bank A/c Cr. $39820

Purchase of ute ( air conditioning and tow bar

expenses have been capitalized)

1-3-13 UTE A/c Dr $600

Bank Cr. $600

Paid ute registration

UTE A/c Dr $500

GST on insurance Dr. $50

Bank Cr. $550

Paid ute insurance

31-07-13 Depreciation A/c Dr $9337.5

INTERNAL Holmesglen: chbaf 13-Apr-2017 L:\Teaching\!AQTF Documents\Training Packages\2017 S1\FNS15\FNS40615 Certificate IV in Accounting\BSBFIA401 Prepare Financial Reports\Ass\Instruction_Assessor BSBFIA401 Ass

2 V1 OL and Ev SOLUTION.docx

Revision 101

August 2016

Page 12 of 18

Wally’s Farm

General Journal

Date Particulars Debit Credit

2012

GST on Insurance Dr. $50

Bank A/c Cr. $550

Payment insurance on harvester

1-2-2013 Bank A/c Dr $330000

Revenue A/c Cr

$30000

0

GST charged on sales Cr. $30000

Receipt of Wheat cheque

1-3-2013 Loan from Farmer’s Union A/c Dr. ($91240- $10000) $81240

Bank A/c Cr. $81240

Paid Balance of harvester

1-3-2013 UTE A/c Dr. (35000+700+500) $36200

GST on purchase of UTE Dr. (3500+70+50) $3620

Bank A/c Cr. $39820

Purchase of ute ( air conditioning and tow bar

expenses have been capitalized)

1-3-13 UTE A/c Dr $600

Bank Cr. $600

Paid ute registration

UTE A/c Dr $500

GST on insurance Dr. $50

Bank Cr. $550

Paid ute insurance

31-07-13 Depreciation A/c Dr $9337.5

INTERNAL Holmesglen: chbaf 13-Apr-2017 L:\Teaching\!AQTF Documents\Training Packages\2017 S1\FNS15\FNS40615 Certificate IV in Accounting\BSBFIA401 Prepare Financial Reports\Ass\Instruction_Assessor BSBFIA401 Ass

2 V1 OL and Ev SOLUTION.docx

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.