Amity Global Business Review: CSR and Financial Performance in India

VerifiedAdded on 2023/06/08

|11

|7707

|441

Report

AI Summary

This report, published in the Amity Global Business Review, investigates the impact of Corporate Social Responsibility (CSR) on the financial performance of consumer goods companies in India. The study examines the relationship between CSR initiatives and financial metrics such as Return on Assets (ROA), Return on Equity (ROE), and Earnings Per Share (EPS). Utilizing secondary data from company reports, the research employs descriptive statistics, correlations, and regression analysis to assess the influence of CSR, while controlling for factors like company age, size, and leverage. The findings reveal a significant positive impact of CSR on ROA and ROE, although no significant impact was found on EPS. The report contributes to the ongoing debate about the financial implications of CSR, providing valuable insights for businesses and researchers in the Indian context.

50 Amity Global Business Review February

Impact of Corporate Social Responsibility on Corporate

Financial Performance: A Study Of The Consumer

Goods Industry of India

Uzma Amin Mir & Farooq Ahmad Shah

Corporate social responsibility (CSR) is a self-regulatory mechanism whereby a business monitors

and ensures its active compliance with the socio-ethical standards and international norms. A firm’s

implementation of CSR goes beyond legal compliance and it involves actions that appear to further

some social good, above the interests of the firm. Companies aim to embrace social responsibility in

corporate actions and encourage their positive impact on the environment and stakeholders including

customers, employees, investors and communities. Realizing the significance of CSR initiatives in social

development, India is the first country to have declared 2% of the company’s average net profits as a

mandatory spending on CSR initiatives with effect from April 1, 2014.

The last few decades have seen an increasing focus of the companies on fulfilling their social obligations. This

has led to the emergence of CSR as a widely researched area at the global level. Further, the relationship

between CSR and the financial performance of the companies is an area that has been extensively studied

by researchers all over the world. As the main aim of an organisation is to make profits, researchers

have attempted to find the impact of CSR spending on the Financial Performance, i.e. if it is a cost or an

investment for the organisation. Even though an extensive research has been conducted in the area, the

relationship between the two variables in hotel industry of India is yet to be investigated. This research,

therefore, aims to study the impact of CSR (measured as the total of five CSR dimensions) on the Corporate

Financial Performance (measured using ROA, ROE, EPS) in the consumer goods companies of India after

controlling for the effect of other variables (Age, Size and Leverage) on financial performance. The data for

the study has been collected from secondary sources, mainly consisting of the official published reports

of the companies included in the study. Descriptive statistics, correlations and regression and have been

used to analyze the data. The results reveal a significant positive impact of ROA and ROE on CSR. Also,

CSR does not have any significant impact on EPS.

Keywords: Corporate Social Responsibility, Financial Performance.

Introduction

Traditionally, a business focused mainly on

increasing its profits and a business was said to be

socially accountable if it produces goods and renders

services for profit maximisation which was considered

to be the sole aim of a business. Gradually, companies

realised that focussing only on profit maximisation is

not adequate to sustain in the changing world. This

led to the modern concept of social accountability

known as CSR (Corporate Social Responsibility).

According to Carroll (1979), the modern era of CSR

started with Howard R. Bowen’s publication “Social

Responsibilitiesof Businessman”in 1953. Bowen

(1953) was the first to comprehensivelydiscuss

social responsibility and business ethics and laid a

foundation for business executives and academicians

alike to consider them in managerial decision-making

and strategic planning.

Business for Social Responsibility (BSR) defines CSR

as “achieving commercial success in ways that honour

ethical values and respect people, communities, and

the natural environment.” McWilliams and Siegel

(2000) describe CSR as “actions that appear to further

some social good, beyond the interest of the firm and

that which is required by law.” The Commission of

European Communities (2002) defines CSR as “A

concept whereby companiesintegratesocial and

environment concerns in their business operations

and in their interaction with their stakeholders on a

voluntary basis, as they are increasingly aware that

responsible behaviour leads to sustainable business

success”.

From the perspective of a firm seeking profit, benefits

and implications of investments in socially responsible

activities have tom be taken into consideration. This

is studied in the form of organisational performance,

particularly financial performance. CSR spending

by a firm should enhance its triple bottom line,

otherwise such investment may not be considered

beneficial for the company in the long run. For

this purpose, the relationship between Corporate

Department of Management Studies, Central University of Kashmir, Kashmir

Impact of Corporate Social Responsibility on Corporate

Financial Performance: A Study Of The Consumer

Goods Industry of India

Uzma Amin Mir & Farooq Ahmad Shah

Corporate social responsibility (CSR) is a self-regulatory mechanism whereby a business monitors

and ensures its active compliance with the socio-ethical standards and international norms. A firm’s

implementation of CSR goes beyond legal compliance and it involves actions that appear to further

some social good, above the interests of the firm. Companies aim to embrace social responsibility in

corporate actions and encourage their positive impact on the environment and stakeholders including

customers, employees, investors and communities. Realizing the significance of CSR initiatives in social

development, India is the first country to have declared 2% of the company’s average net profits as a

mandatory spending on CSR initiatives with effect from April 1, 2014.

The last few decades have seen an increasing focus of the companies on fulfilling their social obligations. This

has led to the emergence of CSR as a widely researched area at the global level. Further, the relationship

between CSR and the financial performance of the companies is an area that has been extensively studied

by researchers all over the world. As the main aim of an organisation is to make profits, researchers

have attempted to find the impact of CSR spending on the Financial Performance, i.e. if it is a cost or an

investment for the organisation. Even though an extensive research has been conducted in the area, the

relationship between the two variables in hotel industry of India is yet to be investigated. This research,

therefore, aims to study the impact of CSR (measured as the total of five CSR dimensions) on the Corporate

Financial Performance (measured using ROA, ROE, EPS) in the consumer goods companies of India after

controlling for the effect of other variables (Age, Size and Leverage) on financial performance. The data for

the study has been collected from secondary sources, mainly consisting of the official published reports

of the companies included in the study. Descriptive statistics, correlations and regression and have been

used to analyze the data. The results reveal a significant positive impact of ROA and ROE on CSR. Also,

CSR does not have any significant impact on EPS.

Keywords: Corporate Social Responsibility, Financial Performance.

Introduction

Traditionally, a business focused mainly on

increasing its profits and a business was said to be

socially accountable if it produces goods and renders

services for profit maximisation which was considered

to be the sole aim of a business. Gradually, companies

realised that focussing only on profit maximisation is

not adequate to sustain in the changing world. This

led to the modern concept of social accountability

known as CSR (Corporate Social Responsibility).

According to Carroll (1979), the modern era of CSR

started with Howard R. Bowen’s publication “Social

Responsibilitiesof Businessman”in 1953. Bowen

(1953) was the first to comprehensivelydiscuss

social responsibility and business ethics and laid a

foundation for business executives and academicians

alike to consider them in managerial decision-making

and strategic planning.

Business for Social Responsibility (BSR) defines CSR

as “achieving commercial success in ways that honour

ethical values and respect people, communities, and

the natural environment.” McWilliams and Siegel

(2000) describe CSR as “actions that appear to further

some social good, beyond the interest of the firm and

that which is required by law.” The Commission of

European Communities (2002) defines CSR as “A

concept whereby companiesintegratesocial and

environment concerns in their business operations

and in their interaction with their stakeholders on a

voluntary basis, as they are increasingly aware that

responsible behaviour leads to sustainable business

success”.

From the perspective of a firm seeking profit, benefits

and implications of investments in socially responsible

activities have tom be taken into consideration. This

is studied in the form of organisational performance,

particularly financial performance. CSR spending

by a firm should enhance its triple bottom line,

otherwise such investment may not be considered

beneficial for the company in the long run. For

this purpose, the relationship between Corporate

Department of Management Studies, Central University of Kashmir, Kashmir

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2018 51

Social Responsibility (CSR) and Corporate Financial

Performance (CFP) needs to be established i.e. does

socially responsible behaviour by a company lead to

an improved financial performance or not.

Literature Review

The basic problem that needs to be addressed

is whether firms actively participatingin CSR

outperform firms that do not exhibit the same

degree of social participation (Lee & Park, 2009;

McWilliams & Siegel, 2001).Critics of CSR argue

that the responsibility of a business is to carry out its

operations in accordance to its desires, which mainly

is maximising profits (Friedman, 1970). Furthermore,

investing in CSR could lead agency problems as

the corporate resources or the profits are used by

the managers for pursuing socially responsible

activities instead of maximising the shareholder’s

wealth (Brammer & Millington, 2008). Scholars in

support of CSR have proposed CSR as a source of

competitiveadvantage(Porter & Kramer, 2006).

CSR has been shown to be positively affecting firm

reputation (Brammer & Millington, 2005; Turban

&Greening,1996),consumersatisfaction(Luo &

Bhattacharya, 2006), attractiveness of a firm as an

employer (Backhaus, Stone, & Heiner, 2002; Turban

& Greening, 1996), and organizational commitment

among employees (Peterson, 2004).

In spite of the empirical evidence demonstrating

the positive relationship between CSR and various

aspects of firm performance, the results still remain

inconclusive (Godfrey & Hatch, 2007; Margolis &

Walsh, 2003; McWilliams & Siegel, 2000). Corporate

Financial Performancehas been measured in

terms of company’s market value or the short-

term profitability of the firm (Schuler & Cording,

2006).The literaturerelating the CSR-CFP link

has revealed mixed set of results which includes

positive, negative and neutral relationships;

thereby revealing lack of agreement on whether

or not increased CSR spending leads to improved

CFP (Margolis & Walsh, 2003; McWilliams &

Siegel, 2000).

Various researchers have found a negative

relationship between CSR and CFP following that

increased CSR spending involves costs and these

costs deplete the profits meaning a negative impact

on the profitability of the firm (Moore, 2001; Vance,

1975; Wright and Ferris, 1997). Scholars like Preston

and O’Bannon 1997; Ruf et al. 2001; Russo and Fouts

1997; Simpson and Kohers 2002; Tsoutsoura (2004);

Waddock and Graves (1997) have shown CSR and

CFP to have a positive relationship. They propose

that if organisationsexhibit socially responsible

activities,then the financial performanceshows

a significant increase. Also, increased social

involvement creates a favourable public image for

the company (Krishna, 1992; Rashid and Ibrahim,

2002). Customers prefer to buy from a company

with a positive public image and one which is

socially responsible (Creyer and William 1997; Mohr

and Webb 2005). Inconclusive relation between CSR

and CFP has been found by Abbott and Monsen

(1979), Griffin and Mahon (1997), and McWilliams

and Siegel (2000). They found that there is no effect

of improved CSR bon CFP of the firm. Ullmann

(1985) stated that the relationship between CSR and

CFP does not exist as there are many intervening

variables between the CSR-CFP relationships.

Moskowitz (1972)studied the CSR-CFP link by

studying 14 firms. He studied the social performance

of these firms and notices that these firms exhibited

a 7.28 percent increase in the stock price over a

period of six months. The findings reveal that firms

that exhibit socially responsiblebehaviour show

a positive relationshipbetween CSR and CFP.

However, Moskowitz did not mention the criteria

for selectingthese 14 firms. Later, Vance (1975)

studied the market performanceof the same 14

firms for a period of 3 years i.e. 1972-1975 and found

that the stock price of all the 14 firms declined thus

establishing a negative relation between CSR and

market value of the firms.

Abbott and Monsen (1979) studied 450 firms out

of the Fortune 500 firms to study the impact of

CSR on the investor’s return. CSR was measured

by developing SID (Social Development Index) for

these firms for the year 1974. SID was generated

by applying content analysis on the annual reports

of the firms for that particular year. The results

revealed that there exists no association between the

variables under study.

Ullmann (1985) examined the work done by other

researchers on the CSR and economic performance

link. Among the 13 reviews, 8 were found to have

a positive relationship, 4 showed no association and

only one revealed a negative relation between the

variables. This variation in results may be due to

lack in theory, inappropriate sample size, different

methods used for CSR measurement. Also, proper

Uzma Amin Mir & Farooq Ahmad Shah

Social Responsibility (CSR) and Corporate Financial

Performance (CFP) needs to be established i.e. does

socially responsible behaviour by a company lead to

an improved financial performance or not.

Literature Review

The basic problem that needs to be addressed

is whether firms actively participatingin CSR

outperform firms that do not exhibit the same

degree of social participation (Lee & Park, 2009;

McWilliams & Siegel, 2001).Critics of CSR argue

that the responsibility of a business is to carry out its

operations in accordance to its desires, which mainly

is maximising profits (Friedman, 1970). Furthermore,

investing in CSR could lead agency problems as

the corporate resources or the profits are used by

the managers for pursuing socially responsible

activities instead of maximising the shareholder’s

wealth (Brammer & Millington, 2008). Scholars in

support of CSR have proposed CSR as a source of

competitiveadvantage(Porter & Kramer, 2006).

CSR has been shown to be positively affecting firm

reputation (Brammer & Millington, 2005; Turban

&Greening,1996),consumersatisfaction(Luo &

Bhattacharya, 2006), attractiveness of a firm as an

employer (Backhaus, Stone, & Heiner, 2002; Turban

& Greening, 1996), and organizational commitment

among employees (Peterson, 2004).

In spite of the empirical evidence demonstrating

the positive relationship between CSR and various

aspects of firm performance, the results still remain

inconclusive (Godfrey & Hatch, 2007; Margolis &

Walsh, 2003; McWilliams & Siegel, 2000). Corporate

Financial Performancehas been measured in

terms of company’s market value or the short-

term profitability of the firm (Schuler & Cording,

2006).The literaturerelating the CSR-CFP link

has revealed mixed set of results which includes

positive, negative and neutral relationships;

thereby revealing lack of agreement on whether

or not increased CSR spending leads to improved

CFP (Margolis & Walsh, 2003; McWilliams &

Siegel, 2000).

Various researchers have found a negative

relationship between CSR and CFP following that

increased CSR spending involves costs and these

costs deplete the profits meaning a negative impact

on the profitability of the firm (Moore, 2001; Vance,

1975; Wright and Ferris, 1997). Scholars like Preston

and O’Bannon 1997; Ruf et al. 2001; Russo and Fouts

1997; Simpson and Kohers 2002; Tsoutsoura (2004);

Waddock and Graves (1997) have shown CSR and

CFP to have a positive relationship. They propose

that if organisationsexhibit socially responsible

activities,then the financial performanceshows

a significant increase. Also, increased social

involvement creates a favourable public image for

the company (Krishna, 1992; Rashid and Ibrahim,

2002). Customers prefer to buy from a company

with a positive public image and one which is

socially responsible (Creyer and William 1997; Mohr

and Webb 2005). Inconclusive relation between CSR

and CFP has been found by Abbott and Monsen

(1979), Griffin and Mahon (1997), and McWilliams

and Siegel (2000). They found that there is no effect

of improved CSR bon CFP of the firm. Ullmann

(1985) stated that the relationship between CSR and

CFP does not exist as there are many intervening

variables between the CSR-CFP relationships.

Moskowitz (1972)studied the CSR-CFP link by

studying 14 firms. He studied the social performance

of these firms and notices that these firms exhibited

a 7.28 percent increase in the stock price over a

period of six months. The findings reveal that firms

that exhibit socially responsiblebehaviour show

a positive relationshipbetween CSR and CFP.

However, Moskowitz did not mention the criteria

for selectingthese 14 firms. Later, Vance (1975)

studied the market performanceof the same 14

firms for a period of 3 years i.e. 1972-1975 and found

that the stock price of all the 14 firms declined thus

establishing a negative relation between CSR and

market value of the firms.

Abbott and Monsen (1979) studied 450 firms out

of the Fortune 500 firms to study the impact of

CSR on the investor’s return. CSR was measured

by developing SID (Social Development Index) for

these firms for the year 1974. SID was generated

by applying content analysis on the annual reports

of the firms for that particular year. The results

revealed that there exists no association between the

variables under study.

Ullmann (1985) examined the work done by other

researchers on the CSR and economic performance

link. Among the 13 reviews, 8 were found to have

a positive relationship, 4 showed no association and

only one revealed a negative relation between the

variables. This variation in results may be due to

lack in theory, inappropriate sample size, different

methods used for CSR measurement. Also, proper

Uzma Amin Mir & Farooq Ahmad Shah

52 Amity Global Business Review February

control variables like size, leverage, risk, industry,

etc. have not been included to control for the effects

of the additional variables.

Griffin and Mohan (1997) studied seven companies

of chemical industry to examine the CSR-CFP

relation. CFP was measured using ROA (Return

in Assets), ROE (Return on Equity), ROS (Return

on Sales), Assets age and Total assets. The data

for Corporate Social Responsibility was obtained

from Fortune reputation survey, Toxic Release

Inventory (TRI) index, Kinder, LyndenbergDomini

& Co. (KLD) index and CorporatePhilanthropy. The

results reveal a positive relation between CSR and

CFP when Fortune and KLD measures of CSR were

used. However CSR and CFP showed no association

when TRI and Corporate Philanthropy measured

were used. These results reveal that the choice of

CSR measures has an impact on the relationship

between the two variables.

Inoue and Lee (2001) have attempted to disaggregate

CSR dimension-wise based on corporate voluntary

activities for five primary stakeholders.The five

dimensionsused are: employee relations,product

quality, community relations, environment and

diversity. The effect of each of these dimensions

on financial performance of firms among the four

tourism-related industries (airline, casino, hotel, and

restaurant) has been studied. The results have revealed

a positive impact of all the five CSR dimensions on

the financial performance of the firms.

Aggarwal (2013) has attempted to assess the relation

between CSR and FP (Financial Performance). To

measure FP, both market- based measures (PE Ratio

and Beta) and accounting-based measures (ROA and

ROE) have been considered. CRISIL’s ESG index

has been used to measure CSR. Data for a period of

five years i.e. 2008 to 2012 has been collected. Her

findings reveal that there is no significant association

between the variables under study.

Govindrajan and Amilan (2013) have studied

the CSR-CFP link in the oil and gas products

industry in India consisting of 12 companies. The

analysis was done for a period of four years i.e.

from 2007 to 2010. CSR has been measured using

three parametersi.e. Karmayog ratings;NGO

ratings for companies exhibiting CSR activities;

the amount of CSR spend and the focus area of

CSR. EPS (Earnings per Share) has been used as

a measure of Financial Performance. The findings

demonstrate a positiveimpact of CSR initiatives

on EPS.

Yang and Baasandorj (2017) analyses the impact

of CSR on the Financial Performance of low-cost

carriers (LCC) and full-service air carriers (FSC). The

period under study is from 2006 to 2015. Panel data

analysis has been used to study the impact. FSC’s

show an improved financial performance with an

increase in environmentaland social activities.

LCC’s show an increase in the financial performance

with an increased firm size and environmental CSR

activities. Also, firm age shows a significant negative

influence in LCCs, while leverage shows a mixed

influence in FSCs. It means that increased CSR lead

to an increasein current and expectedfinancial

performance for FSCs and LCCs, respectively.

To explain the inconclusive results of the CSR-CFP

link over time, the researches have tried to identify

the methodologicalissues in the studied trying

to establish the CSR-CFP link (Godfrey & Hatch,

2007; Griffin & Mahon, 1997; Margolis & Walsh,

2003; McWilliams & Siegel, 2000). Godfrey & Hatch

(2007) identified three main issues: the use of multi-

industry sample, cross-sectional observations and

the aggregationof various CSR dimensions.For

these reasons, it has been suggested that a long-

term relation between the two variables within a

single industry using disaggregated CSR measures

should be studied. Keeping this in view, this study

has employed different CSR dimensions to study

the CSR-CFP link in the consumer goods industry in

India. This study proposed that CSR can be divided

into five different dimensions i.e. Community &

Society, Environmentalcontribution,Employees,

Customer Relation & Product Contributionand

Others (Includes investors, legal and ethical

dimensions).

Objectives of the Study

To study the impact of Corporate Social Responsibility

onCorporate Financial Performance of the consumer

goods sector in India.

To study the relation of the CSR dimensions i.e.

Community & Society, Environmental contribution,

Employees, Customer Relation & Product

Contribution and Others (Includes investors,legal

and ethical dimensions) with Financial performance

(measured by ROA-Return on Assets; ROE- Return

on Equity and EPS-Earningsper Share) of the

companies under study.

control variables like size, leverage, risk, industry,

etc. have not been included to control for the effects

of the additional variables.

Griffin and Mohan (1997) studied seven companies

of chemical industry to examine the CSR-CFP

relation. CFP was measured using ROA (Return

in Assets), ROE (Return on Equity), ROS (Return

on Sales), Assets age and Total assets. The data

for Corporate Social Responsibility was obtained

from Fortune reputation survey, Toxic Release

Inventory (TRI) index, Kinder, LyndenbergDomini

& Co. (KLD) index and CorporatePhilanthropy. The

results reveal a positive relation between CSR and

CFP when Fortune and KLD measures of CSR were

used. However CSR and CFP showed no association

when TRI and Corporate Philanthropy measured

were used. These results reveal that the choice of

CSR measures has an impact on the relationship

between the two variables.

Inoue and Lee (2001) have attempted to disaggregate

CSR dimension-wise based on corporate voluntary

activities for five primary stakeholders.The five

dimensionsused are: employee relations,product

quality, community relations, environment and

diversity. The effect of each of these dimensions

on financial performance of firms among the four

tourism-related industries (airline, casino, hotel, and

restaurant) has been studied. The results have revealed

a positive impact of all the five CSR dimensions on

the financial performance of the firms.

Aggarwal (2013) has attempted to assess the relation

between CSR and FP (Financial Performance). To

measure FP, both market- based measures (PE Ratio

and Beta) and accounting-based measures (ROA and

ROE) have been considered. CRISIL’s ESG index

has been used to measure CSR. Data for a period of

five years i.e. 2008 to 2012 has been collected. Her

findings reveal that there is no significant association

between the variables under study.

Govindrajan and Amilan (2013) have studied

the CSR-CFP link in the oil and gas products

industry in India consisting of 12 companies. The

analysis was done for a period of four years i.e.

from 2007 to 2010. CSR has been measured using

three parametersi.e. Karmayog ratings;NGO

ratings for companies exhibiting CSR activities;

the amount of CSR spend and the focus area of

CSR. EPS (Earnings per Share) has been used as

a measure of Financial Performance. The findings

demonstrate a positiveimpact of CSR initiatives

on EPS.

Yang and Baasandorj (2017) analyses the impact

of CSR on the Financial Performance of low-cost

carriers (LCC) and full-service air carriers (FSC). The

period under study is from 2006 to 2015. Panel data

analysis has been used to study the impact. FSC’s

show an improved financial performance with an

increase in environmentaland social activities.

LCC’s show an increase in the financial performance

with an increased firm size and environmental CSR

activities. Also, firm age shows a significant negative

influence in LCCs, while leverage shows a mixed

influence in FSCs. It means that increased CSR lead

to an increasein current and expectedfinancial

performance for FSCs and LCCs, respectively.

To explain the inconclusive results of the CSR-CFP

link over time, the researches have tried to identify

the methodologicalissues in the studied trying

to establish the CSR-CFP link (Godfrey & Hatch,

2007; Griffin & Mahon, 1997; Margolis & Walsh,

2003; McWilliams & Siegel, 2000). Godfrey & Hatch

(2007) identified three main issues: the use of multi-

industry sample, cross-sectional observations and

the aggregationof various CSR dimensions.For

these reasons, it has been suggested that a long-

term relation between the two variables within a

single industry using disaggregated CSR measures

should be studied. Keeping this in view, this study

has employed different CSR dimensions to study

the CSR-CFP link in the consumer goods industry in

India. This study proposed that CSR can be divided

into five different dimensions i.e. Community &

Society, Environmentalcontribution,Employees,

Customer Relation & Product Contributionand

Others (Includes investors, legal and ethical

dimensions).

Objectives of the Study

To study the impact of Corporate Social Responsibility

onCorporate Financial Performance of the consumer

goods sector in India.

To study the relation of the CSR dimensions i.e.

Community & Society, Environmental contribution,

Employees, Customer Relation & Product

Contribution and Others (Includes investors,legal

and ethical dimensions) with Financial performance

(measured by ROA-Return on Assets; ROE- Return

on Equity and EPS-Earningsper Share) of the

companies under study.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2018 53

Research Methodology

Sample

To study the relationship between the variables,

15 consumer goods companies have been selected.

These companiesare a part of Nifty 100 Index

(based on market capitalisation). Out of these 15,

only 13 form a part of the sample as the data for the

remaining 2 was not available. These 13 consumer

goods companies are represented below in Table 1:

Table 1: Sample of the Study

Sample for the Study

Asian Paints Ltd. Hindustan Unilever Ltd.

Britannia Industries Ltd. I T C Ltd.

Colgate Palmolive (India)

Ltd.

Marico Ltd.

Dabur India Ltd. Titan Company Ltd

Emami Ltd. United Breweries Ltd

Godrej Consumer Products

Ltd.

United Spirits Ltd.

Havells India Ltd

Variables

CSR (Corporate Social Responsibility): In

accordance with Kim et al. (2014), Seo et al.

(2015) and Ding et al. (2016), CSR scoreshave

been used to study its impact on financial

performance. The CSR score includes the total

score of all the CSR dimensions i.e. Community &

Society, Environmental contribution, Employees,

Customer Relation & Product Contribution and

Others (Includes investors, legal and ethical

dimensions).

Financial Performance: Accounting-based

measures i.e. ROA (Return on Assets), ROE

(Return on Equity) and market-based measure

i.e. EPS (Earnings per Share) have been used

to measure financial performance. Accounting-

based measures indicate a firm’s current

financial performance, whereas market-based

measurements indicate market expectation of

future financial performance (McGuire et al.,

1988).

In accordance with Roberts and Dowling (2002),

Guenster et al. (2011) and (Gama Boaventura et

al., 2012), ROA and ROEhave been selected as the

accounting-based measures to indicate a firm’s

financial performance and profitability toward

corporate social performance. Eq. (1) presents

the ROA calculation formula:

ROA = Net Profit (1)

Total Assets

Eq (2), given below presents the ROE calculation

formula:

ROE= Net Income (2)

Shareholder’s equity

Also, Govindrajan and Amilan (2013) have been

referred to in selecting EPS as the market-based

measure of financial performance. Eq. (3) denotes

the EPS calculation formula:

EPS = (Net Income - Preferred Dividends)(3)

Number of Common Shares Outstanding

Control Variables: The effects of the following

variables on financial performance has been

controlled for in this study:

Firm Size: Firm size show a positive influence

towards CSR participation (Kim et al., 2014)

i.e. large firms are more likely to employ CSR

initiatives than small firms (Luo & Bhattacharya,

2006; McWilliams & Siegel, 2001; Waddock &

Graves, 1997). For a majority of firms, firm size

causes a significant positive increase in corporate

profit (Roberts and Dowling, 2002). Following

Kim et al. (2014); Chen and Gavious (2015); Seo

et al. (2015), and Ding et al. (2016), firm size

has been selected to identify the causal effect

toward financial performance. Previous research

has also established a significant influence of

firm size onfinancial performance, though no

agreement appears to the direction of its effects

(e.g., Hillman & Keim, 2001; Kang et al., 2010;

Waddock & Graves, 1997). Relying on Previous

literature (e.g., Hillman & Keim, 2001; Lee & Park,

2009; Waddock & Graves, 1997), Size has been

operationalised as the log of the total assets.

Leverage: Leverage is the defined as the ratio

of total liabilities to total assets. This has been

introduced into the model by McWilliams &

Siegel, 2000; Waddock & Graves, 1997. It has

also been used as a control variable by Kim et al.

(2014); Seo et al. (2015); Chen and Gavious (2015),

and Ding et al. (2016) as it controls for the effect

of firm specific capital structure. Leverage affects

Uzma Amin Mir & Farooq Ahmad Shah

Research Methodology

Sample

To study the relationship between the variables,

15 consumer goods companies have been selected.

These companiesare a part of Nifty 100 Index

(based on market capitalisation). Out of these 15,

only 13 form a part of the sample as the data for the

remaining 2 was not available. These 13 consumer

goods companies are represented below in Table 1:

Table 1: Sample of the Study

Sample for the Study

Asian Paints Ltd. Hindustan Unilever Ltd.

Britannia Industries Ltd. I T C Ltd.

Colgate Palmolive (India)

Ltd.

Marico Ltd.

Dabur India Ltd. Titan Company Ltd

Emami Ltd. United Breweries Ltd

Godrej Consumer Products

Ltd.

United Spirits Ltd.

Havells India Ltd

Variables

CSR (Corporate Social Responsibility): In

accordance with Kim et al. (2014), Seo et al.

(2015) and Ding et al. (2016), CSR scoreshave

been used to study its impact on financial

performance. The CSR score includes the total

score of all the CSR dimensions i.e. Community &

Society, Environmental contribution, Employees,

Customer Relation & Product Contribution and

Others (Includes investors, legal and ethical

dimensions).

Financial Performance: Accounting-based

measures i.e. ROA (Return on Assets), ROE

(Return on Equity) and market-based measure

i.e. EPS (Earnings per Share) have been used

to measure financial performance. Accounting-

based measures indicate a firm’s current

financial performance, whereas market-based

measurements indicate market expectation of

future financial performance (McGuire et al.,

1988).

In accordance with Roberts and Dowling (2002),

Guenster et al. (2011) and (Gama Boaventura et

al., 2012), ROA and ROEhave been selected as the

accounting-based measures to indicate a firm’s

financial performance and profitability toward

corporate social performance. Eq. (1) presents

the ROA calculation formula:

ROA = Net Profit (1)

Total Assets

Eq (2), given below presents the ROE calculation

formula:

ROE= Net Income (2)

Shareholder’s equity

Also, Govindrajan and Amilan (2013) have been

referred to in selecting EPS as the market-based

measure of financial performance. Eq. (3) denotes

the EPS calculation formula:

EPS = (Net Income - Preferred Dividends)(3)

Number of Common Shares Outstanding

Control Variables: The effects of the following

variables on financial performance has been

controlled for in this study:

Firm Size: Firm size show a positive influence

towards CSR participation (Kim et al., 2014)

i.e. large firms are more likely to employ CSR

initiatives than small firms (Luo & Bhattacharya,

2006; McWilliams & Siegel, 2001; Waddock &

Graves, 1997). For a majority of firms, firm size

causes a significant positive increase in corporate

profit (Roberts and Dowling, 2002). Following

Kim et al. (2014); Chen and Gavious (2015); Seo

et al. (2015), and Ding et al. (2016), firm size

has been selected to identify the causal effect

toward financial performance. Previous research

has also established a significant influence of

firm size onfinancial performance, though no

agreement appears to the direction of its effects

(e.g., Hillman & Keim, 2001; Kang et al., 2010;

Waddock & Graves, 1997). Relying on Previous

literature (e.g., Hillman & Keim, 2001; Lee & Park,

2009; Waddock & Graves, 1997), Size has been

operationalised as the log of the total assets.

Leverage: Leverage is the defined as the ratio

of total liabilities to total assets. This has been

introduced into the model by McWilliams &

Siegel, 2000; Waddock & Graves, 1997. It has

also been used as a control variable by Kim et al.

(2014); Seo et al. (2015); Chen and Gavious (2015),

and Ding et al. (2016) as it controls for the effect

of firm specific capital structure. Leverage affects

Uzma Amin Mir & Farooq Ahmad Shah

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

54 Amity Global Business Review February

the CSR-CFP link as high leverage firms (high

risk tolerant firms) may behave differently than

low risk tolerant firms in terms of CSR investment

because of different levels of risks involved in

CSR investment (Waddock & Graves, 1997).

Age of the firm: Firm’s age also influences the

CSR-CFP link as given by Saeidi et al. (2015)

and has therefore been incorporated as one of

the control variables.

Data Collection

Data for this study has been collected from secondary

sources. The data has been collected for a period

of 10 years from 2006-07 to 2015-16 with 130 firm-

year observations.To measure CorporateSocial

Responsibility, a CSR measurement scale consisting

of 62 items has been formulated for this purpose.

To collect data using this scale, the technique of

content analysis has been used. Content analysis

of the annual reports, sustainability reports, CSR

reports and other published data of the companies

under study has been done. Content analysis is the

attributionof the incidence of an event as indicated

by the mention of the event under question in the

literary document that constitutesthe raw data

(Abbott and Monsen 1979). But one of the limitations

of using this method is that it does not give any

priority to the information items which have been

given more importance by the company (Gray et

al. 1995). The CSR scoring procedure adopted is in

accordance with Ernst and Ernst (1978)and Abbott

and Monsen (1979) wherein an item if disclosed is

scored one and an item not disclosed is given a zero.

In this scoring technique, all the CSR items across all

the dimensions get an equal importance i.e. equal

weightage. The final CSR is calculated using the

following formula:

CSR Score of a company = No. of CSR items adopted by a Company×100

(In percentage) Total no. of items in the CSR

Measurement instrument

Further, secondary data for Financial Performance measures and control variables has been collected from

Capitaline which is a digital corporate financial database for Indian listed companies.

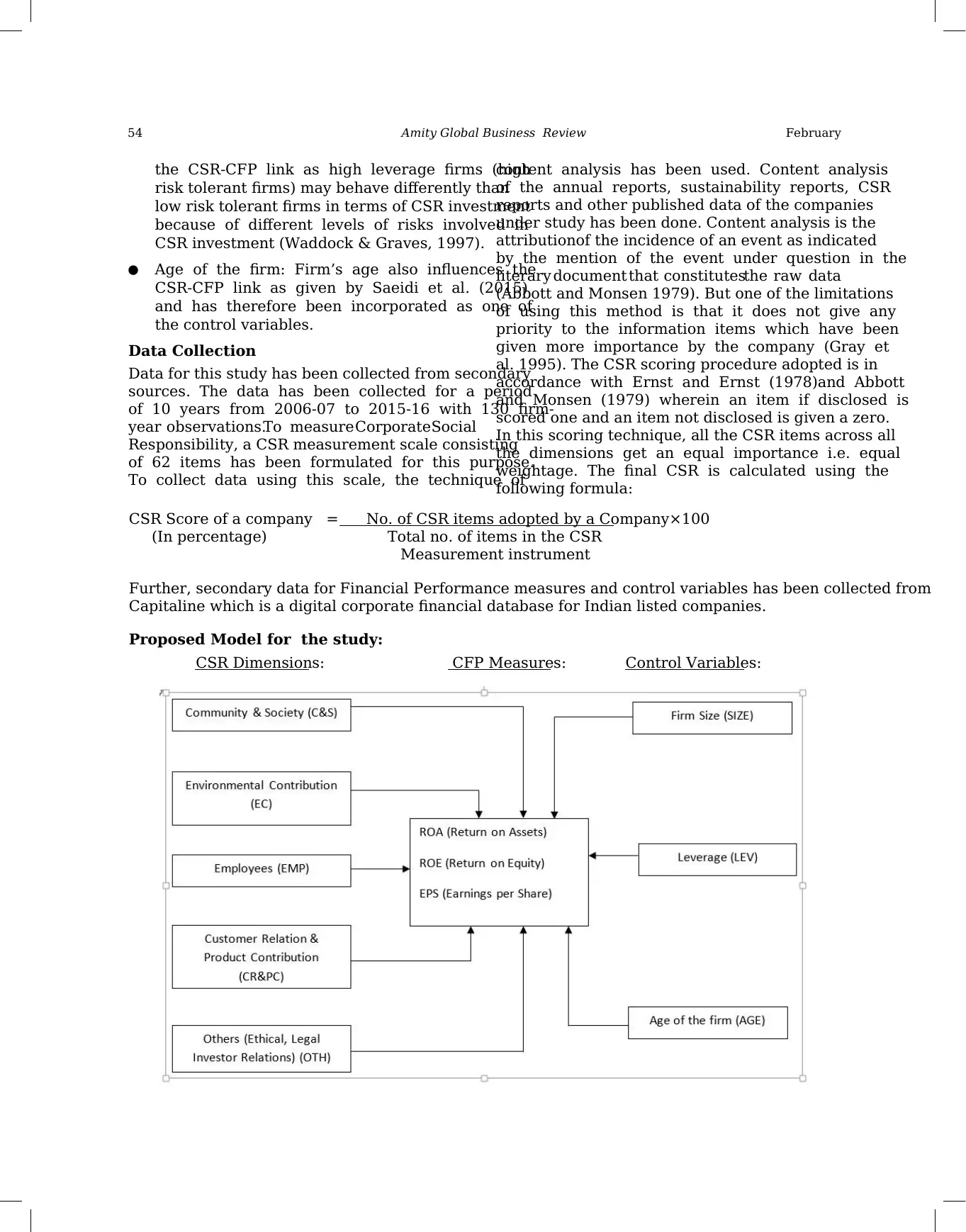

Proposed Model for the study:

CSR Dimensions: CFP Measures: Control Variables:

the CSR-CFP link as high leverage firms (high

risk tolerant firms) may behave differently than

low risk tolerant firms in terms of CSR investment

because of different levels of risks involved in

CSR investment (Waddock & Graves, 1997).

Age of the firm: Firm’s age also influences the

CSR-CFP link as given by Saeidi et al. (2015)

and has therefore been incorporated as one of

the control variables.

Data Collection

Data for this study has been collected from secondary

sources. The data has been collected for a period

of 10 years from 2006-07 to 2015-16 with 130 firm-

year observations.To measure CorporateSocial

Responsibility, a CSR measurement scale consisting

of 62 items has been formulated for this purpose.

To collect data using this scale, the technique of

content analysis has been used. Content analysis

of the annual reports, sustainability reports, CSR

reports and other published data of the companies

under study has been done. Content analysis is the

attributionof the incidence of an event as indicated

by the mention of the event under question in the

literary document that constitutesthe raw data

(Abbott and Monsen 1979). But one of the limitations

of using this method is that it does not give any

priority to the information items which have been

given more importance by the company (Gray et

al. 1995). The CSR scoring procedure adopted is in

accordance with Ernst and Ernst (1978)and Abbott

and Monsen (1979) wherein an item if disclosed is

scored one and an item not disclosed is given a zero.

In this scoring technique, all the CSR items across all

the dimensions get an equal importance i.e. equal

weightage. The final CSR is calculated using the

following formula:

CSR Score of a company = No. of CSR items adopted by a Company×100

(In percentage) Total no. of items in the CSR

Measurement instrument

Further, secondary data for Financial Performance measures and control variables has been collected from

Capitaline which is a digital corporate financial database for Indian listed companies.

Proposed Model for the study:

CSR Dimensions: CFP Measures: Control Variables:

2018 55

Analysis

In accordance withKapoor, S. & Sandhu, H.S. (2010)

and Inoue, H. & Lee, S. (2011), descriptive analysis,

correlation and OLS regression analysis has been

used to analyse the data to determine the relation

between the variables.The relationshipbetween

CSR and the accounting-based measure i.e. ROA

(Return on Assets) and ROE (Return on Equity) can

be analysed using Eq.(3) and Eq (4):

ROAit= α0 +α1CSRit*+ α2 SIZEit + α3LEVit + α4 AGE

it + εit (3)

ROEit= α0 + α1CSRit*+ α2 SIZEit + α3LEVit + α4 AGE

it + εit (4)

Similarly, for the market-basedmeasure of the

financial performance i.e. EPS (Earnings per

Share), Eq. (5) has been developed to analyse the

relation between CSR and EPS. The equation can be

represented as follows:

EPSit = β0 +β1 CSRit*+ β2 SIZEit + β3 LE Vit +β4AG

E it + μit (5)

where, ROAitrepresents Return on Assets i.e. the

financial performanceof the company attime t;

ROE itrepresents Return on Assets i.e. the financial

performanceof the company at time t ; EPS it

representsEarningsper Share i.e. the Corporate

financial performance of the company at time t CSR

it* represents the total CSR score of company at time

t [Total CSR score is the sum of the scores of the 5

dimensions of CSR used in the study i.e.Community

& Society, Environmental contribution, Employees,

Customer Relation & Product Contributionand

Others (Includes investors, legal and ethical

dimensions)]; SIZEitrepresents the log of the total

assets of the company at time t; LEVitrepresents the

ratio of total liabilities over the total asset of company

at time t; AGEitrepresents the age of the company at

time t;it and μ it signifies the error terms of company

at time t for the models. The sub-variables for CSR

include C&Sitwhich denotes the total Community

& Society score of the company at time t; ECit

denotes the total Environmental Contribution score

of the company at time t; EMPit denotes the total

Employees score of the company at time t; CR&PC

it denotes the total of Customer Relation & Product

Contribution dimension of company at time t and

OTH it denotes the total of the others dimension of

company at time t.

Results and Discussions:

Primarily, the normality of the data has been

examined using skewness and kurtosis measures.

The data was found to be approximately normal

except for EPS which was positively skewed. To

correct this, the natural logarithm transformation

was conducted, and the improvement of the

normality of the variable was confirmed (Hair et al.

2005 & Malhotra. 2007). The final data as shown in

Table 2 revealed the values between +1.96 and -1.96

for skewness (Kline, 2015) and between +3 and -3

for kurtosis (DeCarlo, 1997). These values reveal

that the data is normal and further analysis can be

conducted on it.

After this, the basic assumptionsfor regression

have been checked including normality, linearity,

homoscedasticity and multicollinearity have been

checked and successfully met. Normality has been

checked using kurtosis and skewnessmeasures.

Linearity has been checked using partial regression

plots. For multicollinearity the correlation matrix

has been checkedfor values above 0.7 amongst

the dependent variables, but as all the values were

found to be below 0.7, the issue of multicollinearity

did not exist. Also, to check the assumptionof

homoscedasticityBreusch-Pagantest (Breusch&

Pagan, 1979)and Koenker test have been used,

proving that the assumption holds true.

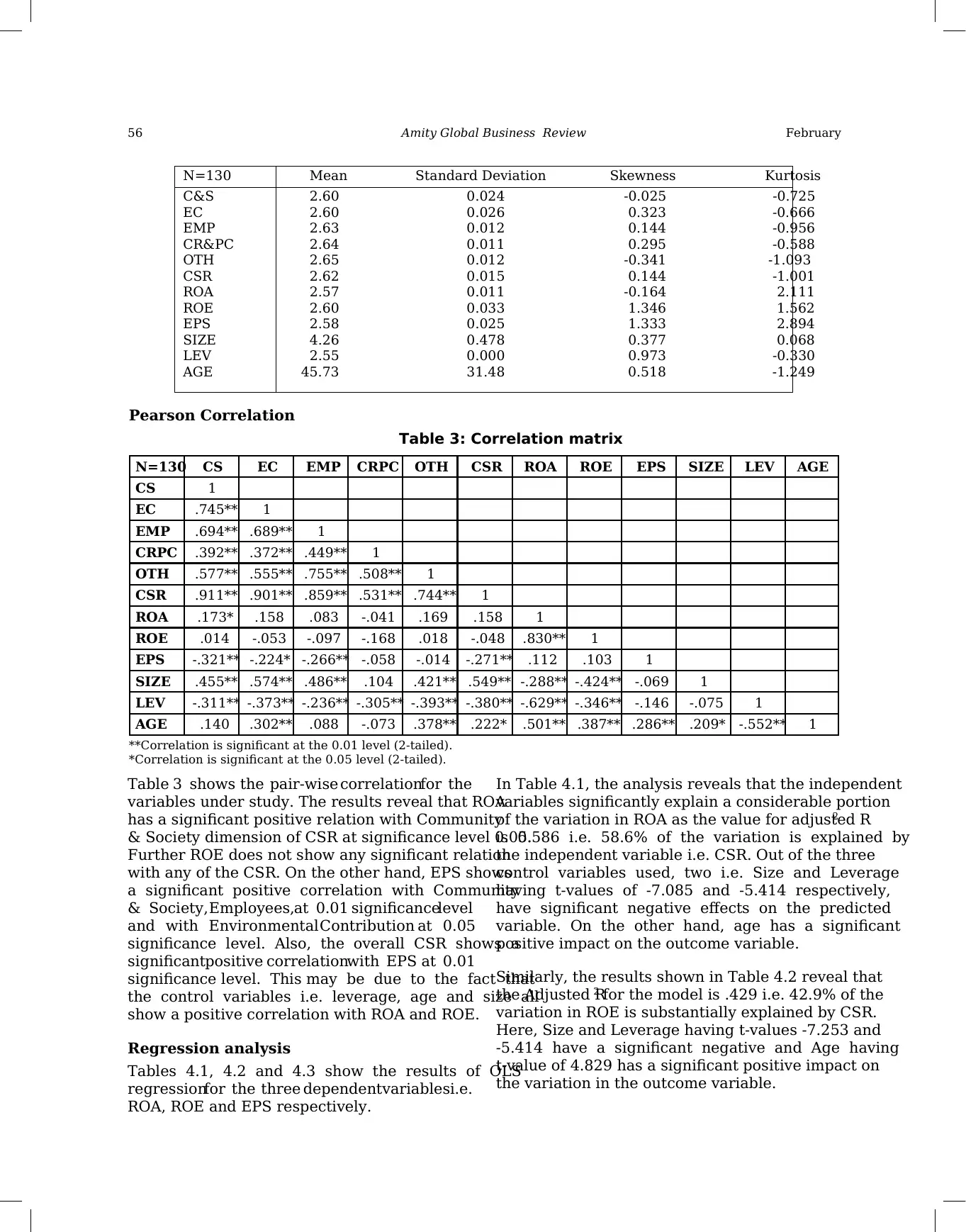

Descriptive Statistics:

Table 2 presentsthe descriptivestatisticsof the

variables under study. The table reveals that all the

five CSR dimensions have a mean score in the range

of 2.60 to 2.65 with the total CSR mean being 2.62

for the 13 companies under study. Also, the average

age of these 13 companies are 45.73 and the average

size being 4.26. Also, the respective kurtosis and

skewness values for the variables under study have

been given in the table.

Uzma Amin Mir & Farooq Ahmad Shah

Analysis

In accordance withKapoor, S. & Sandhu, H.S. (2010)

and Inoue, H. & Lee, S. (2011), descriptive analysis,

correlation and OLS regression analysis has been

used to analyse the data to determine the relation

between the variables.The relationshipbetween

CSR and the accounting-based measure i.e. ROA

(Return on Assets) and ROE (Return on Equity) can

be analysed using Eq.(3) and Eq (4):

ROAit= α0 +α1CSRit*+ α2 SIZEit + α3LEVit + α4 AGE

it + εit (3)

ROEit= α0 + α1CSRit*+ α2 SIZEit + α3LEVit + α4 AGE

it + εit (4)

Similarly, for the market-basedmeasure of the

financial performance i.e. EPS (Earnings per

Share), Eq. (5) has been developed to analyse the

relation between CSR and EPS. The equation can be

represented as follows:

EPSit = β0 +β1 CSRit*+ β2 SIZEit + β3 LE Vit +β4AG

E it + μit (5)

where, ROAitrepresents Return on Assets i.e. the

financial performanceof the company attime t;

ROE itrepresents Return on Assets i.e. the financial

performanceof the company at time t ; EPS it

representsEarningsper Share i.e. the Corporate

financial performance of the company at time t CSR

it* represents the total CSR score of company at time

t [Total CSR score is the sum of the scores of the 5

dimensions of CSR used in the study i.e.Community

& Society, Environmental contribution, Employees,

Customer Relation & Product Contributionand

Others (Includes investors, legal and ethical

dimensions)]; SIZEitrepresents the log of the total

assets of the company at time t; LEVitrepresents the

ratio of total liabilities over the total asset of company

at time t; AGEitrepresents the age of the company at

time t;it and μ it signifies the error terms of company

at time t for the models. The sub-variables for CSR

include C&Sitwhich denotes the total Community

& Society score of the company at time t; ECit

denotes the total Environmental Contribution score

of the company at time t; EMPit denotes the total

Employees score of the company at time t; CR&PC

it denotes the total of Customer Relation & Product

Contribution dimension of company at time t and

OTH it denotes the total of the others dimension of

company at time t.

Results and Discussions:

Primarily, the normality of the data has been

examined using skewness and kurtosis measures.

The data was found to be approximately normal

except for EPS which was positively skewed. To

correct this, the natural logarithm transformation

was conducted, and the improvement of the

normality of the variable was confirmed (Hair et al.

2005 & Malhotra. 2007). The final data as shown in

Table 2 revealed the values between +1.96 and -1.96

for skewness (Kline, 2015) and between +3 and -3

for kurtosis (DeCarlo, 1997). These values reveal

that the data is normal and further analysis can be

conducted on it.

After this, the basic assumptionsfor regression

have been checked including normality, linearity,

homoscedasticity and multicollinearity have been

checked and successfully met. Normality has been

checked using kurtosis and skewnessmeasures.

Linearity has been checked using partial regression

plots. For multicollinearity the correlation matrix

has been checkedfor values above 0.7 amongst

the dependent variables, but as all the values were

found to be below 0.7, the issue of multicollinearity

did not exist. Also, to check the assumptionof

homoscedasticityBreusch-Pagantest (Breusch&

Pagan, 1979)and Koenker test have been used,

proving that the assumption holds true.

Descriptive Statistics:

Table 2 presentsthe descriptivestatisticsof the

variables under study. The table reveals that all the

five CSR dimensions have a mean score in the range

of 2.60 to 2.65 with the total CSR mean being 2.62

for the 13 companies under study. Also, the average

age of these 13 companies are 45.73 and the average

size being 4.26. Also, the respective kurtosis and

skewness values for the variables under study have

been given in the table.

Uzma Amin Mir & Farooq Ahmad Shah

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

56 Amity Global Business Review February

N=130 Mean Standard Deviation Skewness Kurtosis

C&S

EC

EMP

CR&PC

OTH

CSR

ROA

ROE

EPS

SIZE

LEV

AGE

2.60 0.024 -0.025 -0.725

2.60 0.026 0.323 -0.666

2.63 0.012 0.144 -0.956

2.64 0.011 0.295 -0.588

2.65 0.012 -0.341 -1.093

2.62 0.015 0.144 -1.001

2.57 0.011 -0.164 2.111

2.60 0.033 1.346 1.562

2.58 0.025 1.333 2.894

4.26 0.478 0.377 0.068

2.55 0.000 0.973 -0.330

45.73 31.48 0.518 -1.249

Pearson Correlation

Table 3: Correlation matrix

N=130 CS EC EMP CRPC OTH CSR ROA ROE EPS SIZE LEV AGE

CS 1

EC .745** 1

EMP .694** .689** 1

CRPC .392** .372** .449** 1

OTH .577** .555** .755** .508** 1

CSR .911** .901** .859** .531** .744** 1

ROA .173* .158 .083 -.041 .169 .158 1

ROE .014 -.053 -.097 -.168 .018 -.048 .830** 1

EPS -.321** -.224* -.266** -.058 -.014 -.271** .112 .103 1

SIZE .455** .574** .486** .104 .421** .549** -.288** -.424** -.069 1

LEV -.311** -.373** -.236** -.305** -.393** -.380** -.629** -.346** -.146 -.075 1

AGE .140 .302** .088 -.073 .378** .222* .501** .387** .286** .209* -.552** 1

**Correlation is significant at the 0.01 level (2-tailed).

*Correlation is significant at the 0.05 level (2-tailed).

Table 3 shows the pair-wise correlationfor the

variables under study. The results reveal that ROA

has a significant positive relation with Community

& Society dimension of CSR at significance level 0.05.

Further ROE does not show any significant relation

with any of the CSR. On the other hand, EPS shows

a significant positive correlation with Community

& Society, Employees,at 0.01 significancelevel

and with Environmental Contribution at 0.05

significance level. Also, the overall CSR shows a

significantpositive correlationwith EPS at 0.01

significance level. This may be due to the fact that

the control variables i.e. leverage, age and size all

show a positive correlation with ROA and ROE.

Regression analysis

Tables 4.1, 4.2 and 4.3 show the results of OLS

regressionfor the three dependentvariablesi.e.

ROA, ROE and EPS respectively.

In Table 4.1, the analysis reveals that the independent

variables significantly explain a considerable portion

of the variation in ROA as the value for adjusted R2

is 0.586 i.e. 58.6% of the variation is explained by

the independent variable i.e. CSR. Out of the three

control variables used, two i.e. Size and Leverage

having t-values of -7.085 and -5.414 respectively,

have significant negative effects on the predicted

variable. On the other hand, age has a significant

positive impact on the outcome variable.

Similarly, the results shown in Table 4.2 reveal that

the Adjusted R2 for the model is .429 i.e. 42.9% of the

variation in ROE is substantially explained by CSR.

Here, Size and Leverage having t-values -7.253 and

-5.414 have a significant negative and Age having

t-value of 4.829 has a significant positive impact on

the variation in the outcome variable.

N=130 Mean Standard Deviation Skewness Kurtosis

C&S

EC

EMP

CR&PC

OTH

CSR

ROA

ROE

EPS

SIZE

LEV

AGE

2.60 0.024 -0.025 -0.725

2.60 0.026 0.323 -0.666

2.63 0.012 0.144 -0.956

2.64 0.011 0.295 -0.588

2.65 0.012 -0.341 -1.093

2.62 0.015 0.144 -1.001

2.57 0.011 -0.164 2.111

2.60 0.033 1.346 1.562

2.58 0.025 1.333 2.894

4.26 0.478 0.377 0.068

2.55 0.000 0.973 -0.330

45.73 31.48 0.518 -1.249

Pearson Correlation

Table 3: Correlation matrix

N=130 CS EC EMP CRPC OTH CSR ROA ROE EPS SIZE LEV AGE

CS 1

EC .745** 1

EMP .694** .689** 1

CRPC .392** .372** .449** 1

OTH .577** .555** .755** .508** 1

CSR .911** .901** .859** .531** .744** 1

ROA .173* .158 .083 -.041 .169 .158 1

ROE .014 -.053 -.097 -.168 .018 -.048 .830** 1

EPS -.321** -.224* -.266** -.058 -.014 -.271** .112 .103 1

SIZE .455** .574** .486** .104 .421** .549** -.288** -.424** -.069 1

LEV -.311** -.373** -.236** -.305** -.393** -.380** -.629** -.346** -.146 -.075 1

AGE .140 .302** .088 -.073 .378** .222* .501** .387** .286** .209* -.552** 1

**Correlation is significant at the 0.01 level (2-tailed).

*Correlation is significant at the 0.05 level (2-tailed).

Table 3 shows the pair-wise correlationfor the

variables under study. The results reveal that ROA

has a significant positive relation with Community

& Society dimension of CSR at significance level 0.05.

Further ROE does not show any significant relation

with any of the CSR. On the other hand, EPS shows

a significant positive correlation with Community

& Society, Employees,at 0.01 significancelevel

and with Environmental Contribution at 0.05

significance level. Also, the overall CSR shows a

significantpositive correlationwith EPS at 0.01

significance level. This may be due to the fact that

the control variables i.e. leverage, age and size all

show a positive correlation with ROA and ROE.

Regression analysis

Tables 4.1, 4.2 and 4.3 show the results of OLS

regressionfor the three dependentvariablesi.e.

ROA, ROE and EPS respectively.

In Table 4.1, the analysis reveals that the independent

variables significantly explain a considerable portion

of the variation in ROA as the value for adjusted R2

is 0.586 i.e. 58.6% of the variation is explained by

the independent variable i.e. CSR. Out of the three

control variables used, two i.e. Size and Leverage

having t-values of -7.085 and -5.414 respectively,

have significant negative effects on the predicted

variable. On the other hand, age has a significant

positive impact on the outcome variable.

Similarly, the results shown in Table 4.2 reveal that

the Adjusted R2 for the model is .429 i.e. 42.9% of the

variation in ROE is substantially explained by CSR.

Here, Size and Leverage having t-values -7.253 and

-5.414 have a significant negative and Age having

t-value of 4.829 has a significant positive impact on

the variation in the outcome variable.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2018 57

To check the model for EPS, the results have been

shown in Table 4.3. According to the results, CSR

does not substantiallyexplain the variation in

EPS as the Adjusted R2 for the model is only .192

showing that only 19.2% variation in EPS is due to

CSR. Also, the t-value of -4.338 shows a significant

negative impact of CSR on EPS. Age, which has a

t-value of 2.822, shows a significant positive impact

on the variation in EPS.

Table 4.1, 4.2, and 4.3: OLS regression analysis

ROA (N=130) ROA it= α0 + α1CSRit*+ α2 SIZEit +

α3LEVit +α4 AGE it +εit

CSR SIZE LEV AGE

Coefficients

t-value

Adj R2 = 0.586

F-Value=46.69

0.206 -0.501 -0.403 0.337

2.756** -7.085*** -5.414*** 4.829***

ROE (N=130) ROA it= α0 + α1CSRit*+ α2 SIZEit +

α3LEVit +α4 AGE it +εit

CSR SIZE LEV AGE

Coefficients

t-value

Adj R2 = 0.429

F-Value = 25.24

0.151 -0.603 -0.099 0.425

1.721* -7.253*** -1.132** 5.179***

EPS (N=130) ROA it= α0 +α1CSRit*+ α2 SIZEit +

α3LEVit +α4 AGE it +εit

CSR SIZE LEV AGE

Coefficients

t-value

Adj R2 = 0.192

F-Value=8.665

0.453 0.111 -0.159 0.275

-4.338*** 1.119 -1.526* 2.822**

*, ** and ***, represent significance level of 0.05, 0.01 and 0.001

respectively.

Conclusion

In accordance with the results, it may be concluded

that if a firm is more socially responsible,i.e.

exhibits an increase in CSR spending, there is an

increase in the profitability of the firm as there is a

positive association between CSR and ROA & ROE.

Also, there is an interference of other variables like

age which explain the variation in the outcome

variables.It may also be noted that CSR has a

minimal association with EPS, which is a market-

based measure of firm performance. These results

reveal that, other variables in addition to ROA, ROE

and EPS have to be included in the model to explain

the CSR-CFP link in a better way.

Limitations and Suggestions for future

research

One of the main limitations of this study is that

equal weight (by assigning binary values) has

been given to each CSR item irrespective of the

importance given to it by the company. Further, a

small sample size of only 13 companies has been

used to study the CSR-CFP link. Future researchers

should consider extending the research by including

more firms to increase the robustness of the study.

Also future researchers may consider taking into

view the reverse causality effects of CSR-CFP link.

References

1. Abbott, W.F., & Monsen, J.R. (1979). On the Measurement

of Corporate Social Responsibility: Self- Reported Disclosure

as a Method of Measuring Corporate Social Involvement’.

Academy of Management Journal, 22(3), 501–515.

2. Aggarwal, M. (2013). Corporate social responsibility

and financial performance linkage evidence from Indian

companies. International Journal of Management and

Development Studies, Vol. 2 (7), 12-24.

3. Backhaus, K. B., Stone, B. A. & Heiner, K. (2002). Exploring

the relationship between corporate social performance and

employer attractiveness. Business & Society, 41, 292-318.

4. Breusch, T.S. & Pagan, A.R. (1979). A Simple Test for

Heteroscedasticity and Random Coefficient Variation.

Econometrical, 47(5), 1287-1294.

5. Chen, E. & Gavious, I. (2015). Does CSR have different value

implications for different shareholders? Finance Research

Letters, 14, 29–35.

6. Bowen, H. R. (1953). Social responsibilities of businessman.

New York: Harper & Row.

7. Brammer, S. & Millington, A. (2005). Corporate reputation

and philanthropy: an empirical analysis. Journal of Business

Ethics, 61, 29-44.

8. Brammer, S. & Millington, A. (2008). Does it pay to be

different? An analysis of the relationship between corporate

social and financial performance. Strategic Management

Journal, 29, 1325-1343.

9. Carroll, A. B. (1979). A three-dimensional model of corporate

social performance. Academy of Management Review, 4,

497-505.

10. Commission of the European Communities. (2002).

Communication from the Commission Concerning Corporate

Social Responsibility: A Business Contribution to Sustainable

Development.

11. Creyer, E. & T.R. William Jr. (1997). The Influence of Firm

Behaviour on Purchase Intention: Do Consumers Really Care

about Business Ethics? Journal of Consumer Marketing, 14(6),

421–32.

Uzma Amin Mir & Farooq Ahmad Shah

To check the model for EPS, the results have been

shown in Table 4.3. According to the results, CSR

does not substantiallyexplain the variation in

EPS as the Adjusted R2 for the model is only .192

showing that only 19.2% variation in EPS is due to

CSR. Also, the t-value of -4.338 shows a significant

negative impact of CSR on EPS. Age, which has a

t-value of 2.822, shows a significant positive impact

on the variation in EPS.

Table 4.1, 4.2, and 4.3: OLS regression analysis

ROA (N=130) ROA it= α0 + α1CSRit*+ α2 SIZEit +

α3LEVit +α4 AGE it +εit

CSR SIZE LEV AGE

Coefficients

t-value

Adj R2 = 0.586

F-Value=46.69

0.206 -0.501 -0.403 0.337

2.756** -7.085*** -5.414*** 4.829***

ROE (N=130) ROA it= α0 + α1CSRit*+ α2 SIZEit +

α3LEVit +α4 AGE it +εit

CSR SIZE LEV AGE

Coefficients

t-value

Adj R2 = 0.429

F-Value = 25.24

0.151 -0.603 -0.099 0.425

1.721* -7.253*** -1.132** 5.179***

EPS (N=130) ROA it= α0 +α1CSRit*+ α2 SIZEit +

α3LEVit +α4 AGE it +εit

CSR SIZE LEV AGE

Coefficients

t-value

Adj R2 = 0.192

F-Value=8.665

0.453 0.111 -0.159 0.275

-4.338*** 1.119 -1.526* 2.822**

*, ** and ***, represent significance level of 0.05, 0.01 and 0.001

respectively.

Conclusion

In accordance with the results, it may be concluded

that if a firm is more socially responsible,i.e.

exhibits an increase in CSR spending, there is an

increase in the profitability of the firm as there is a

positive association between CSR and ROA & ROE.

Also, there is an interference of other variables like

age which explain the variation in the outcome

variables.It may also be noted that CSR has a

minimal association with EPS, which is a market-

based measure of firm performance. These results

reveal that, other variables in addition to ROA, ROE

and EPS have to be included in the model to explain

the CSR-CFP link in a better way.

Limitations and Suggestions for future

research

One of the main limitations of this study is that

equal weight (by assigning binary values) has

been given to each CSR item irrespective of the

importance given to it by the company. Further, a

small sample size of only 13 companies has been

used to study the CSR-CFP link. Future researchers

should consider extending the research by including

more firms to increase the robustness of the study.

Also future researchers may consider taking into

view the reverse causality effects of CSR-CFP link.

References

1. Abbott, W.F., & Monsen, J.R. (1979). On the Measurement

of Corporate Social Responsibility: Self- Reported Disclosure

as a Method of Measuring Corporate Social Involvement’.

Academy of Management Journal, 22(3), 501–515.

2. Aggarwal, M. (2013). Corporate social responsibility

and financial performance linkage evidence from Indian

companies. International Journal of Management and

Development Studies, Vol. 2 (7), 12-24.

3. Backhaus, K. B., Stone, B. A. & Heiner, K. (2002). Exploring

the relationship between corporate social performance and

employer attractiveness. Business & Society, 41, 292-318.

4. Breusch, T.S. & Pagan, A.R. (1979). A Simple Test for

Heteroscedasticity and Random Coefficient Variation.

Econometrical, 47(5), 1287-1294.

5. Chen, E. & Gavious, I. (2015). Does CSR have different value

implications for different shareholders? Finance Research

Letters, 14, 29–35.

6. Bowen, H. R. (1953). Social responsibilities of businessman.

New York: Harper & Row.

7. Brammer, S. & Millington, A. (2005). Corporate reputation

and philanthropy: an empirical analysis. Journal of Business

Ethics, 61, 29-44.

8. Brammer, S. & Millington, A. (2008). Does it pay to be

different? An analysis of the relationship between corporate

social and financial performance. Strategic Management

Journal, 29, 1325-1343.

9. Carroll, A. B. (1979). A three-dimensional model of corporate

social performance. Academy of Management Review, 4,

497-505.

10. Commission of the European Communities. (2002).

Communication from the Commission Concerning Corporate

Social Responsibility: A Business Contribution to Sustainable

Development.

11. Creyer, E. & T.R. William Jr. (1997). The Influence of Firm

Behaviour on Purchase Intention: Do Consumers Really Care

about Business Ethics? Journal of Consumer Marketing, 14(6),

421–32.

Uzma Amin Mir & Farooq Ahmad Shah

58 Amity Global Business Review February

12. DeCarlo, L.T. (1997). On the meaning and use of kurtosis.

Psychological methods, 2(3), 292.

13. Ding, D.K., Ferreria, C. & Wongchoti, U. (2016). Does it pay

to be different? Relative CSR and its impact on firm value.

International Review of Financial Analysis, 47, 86–98.

14. Ernst and Ernst. (1978). Social Responsibility Disclosure,1978

Survey. Ohio: Cleveland.

15. Friedman, M. (1970). Social responsibility of business is to

increase profit. The New York Times Magazine, 13, 122-126.

16. Gama Boaventura, J.M., da Silva, R.S. & Bandeira-de-Mello, R.

(2012). Corporate Financial Performance and Corporate Social

Performance: methodological development and the theoretical

contribution of empirical studies. Revista Contabilidade &

Finanças, 23, 232–245.

17. Godfrey, P. C. & Hatch, N. W. (2007). Researching corporate

social responsibility: An agenda for the 21st century. Journal

of Business Ethics, 70, 87-98.

18. Govindarajan, A.L. and Amilan, S. (2013). A Study on linkage

between Corporate Social Responsibility Initiatives with

Financial Performances: Analysis from Oil and Gas Products

Industry in India.Pacific Business Review International, Vol

6 (5), 81-93.

19. Gray, R., R. Kouhy and S. Lavers. 1995. Corporate Socialand

Environmental Reporting: A Review of theLiterature and a

Longitudinal Study of UK Disclosure. Accounting, Auditing

and Accountability, 8(2), 47–77.

20. Griffin, J.J. and J.F. Mahon. (1997). The Corporate Social

Performance and Corporate Financial Performance Debate:

Twenty-Five Years of Incomparable Research.Business and

Society, 36(1), 5–31.

21. Guenster, N., Bauer, R., Derwall, J. & Koedijk, K. (2011).

The economic value of corporate eco-efficiency. European

Financial Management, 17, 679–704.

22. Hair, J.F., Anderson, R.E., Tatham, R.L. & Black, W.C. (2005).

Multivariate Data Analysis. Delhi: Pearson Education Pte Ltd.

23. Hillman, A. J. & Keim, G. D. (2001). Shareholder value,

stakeholder management, and social issues: what’s the bottom

line? Strategic Management Journal, 22, 125-139.

24. Inoue, Y. & Lee, S. (2001). Effects of different dimensions

of corporate social responsibility on corporate financial

performance in tourism-related industries. Tourism

Management.

25. Kang, K. H., Lee, S. & Huh, C. (2010). Impacts of positive and

negative corporate social responsibility activities on company

performance in the tourism industry. International Journal

of Hospitality Management, 29(1), 72-82.

26. Kapoor, S. & Sandhu, H.S. (2010). Does it pay to be Socially

Responsible? An Empirical Examination of Impact of

CorporateSocial Responsibility on Financial Performance.

Global Business Review, 11(2), 185-208.

27. Kim, Y., Li, H. & Li, S. (2014). Corporate social responsibility

and stock price crash risk. Journal of Banking & Finance. 43,

1–13.

28. Kline, R. B. (2015). Principles and practice of structural

equation modelling. Guilford publications.

29. Krishna, C.G. (1992). Corporate Social Responsibility inIndia.

New Delhi: Mittal Publications.

30. Lee, S. & Park, S. (2009). Do socially responsible activities help

hotels and casinos achieve their financial goals? International

Journal of Hospitality Management, 28, 105-112.

31. Luo, X. & Bhattacharya, C. B. (2006). Corporate social

responsibility, customer satisfaction, and market value.

Journal of Marketing, 70, 1-18.

32. Malhotra, N.K. (2007). Marketing Research. Delhi: Pearson

Education, Inc.

33. Margolis, J. D. & Walsh, J. P. (2003). Misery loves companies:

rethinking social initiatives by business. Administrative

Science Quarterly, 48, 268-305.

34. McGuire, J.B., Sundgren, A. & Schneeweis, T. (1988). Corporate

social responsibility and firm financial performance. Academic

ManagementJournal, 31, 854–872.

35. McWilliams, A. & Siegel, D. (2000). Corporate social

responsibility and financial performance: Correlation or

misspecification? Strategic Management Journal, 21 (5), 603-

609.

36. McWilliams, A. & Siegel, D. (2001). Corporate social

responsibility: A theory of the firm perspective. Academy

of Management Review, 26(1), 117-127.

37. Mohr, L.A. &D.J. Webb. (2005). The Effects of Corporate Social

Responsibility and Price on Consumer Responses.Journal of

Consumer Affairs, 39(1), 121–47.

38. Moore, G. (2001). Corporate Social and Financial Performance:

An Investigation in the U.K. Supermarket Industry, Journal

of Business Ethics, 34(3/4), 299–315.

39.Moskowitz, M.R. (1972). Choosing Socially Responsible Stocks.

Business and Society Review, 1(1), 71–75.

40. Peterson, D. (2004). The relationship between perceptions

of corporate citizenship and organizational commitment.

Business and Society, 43(3), 296-319.

45. Porter, M. E. & Kramer, M. R. (2006). Strategy and society:

the link between competitive advantage and corporate social

responsibility. Harvard Business Review, 84(12), 78-92.

46. Preston, L.E. & Bannon. (1997). The Corporate Social-Financial

Performance Relationship: A Typology and Analysis.Business

& Society, 36(4), 419–29.

47. Rashid, Z.A. & Ibrahim, S. (2002). Executive and Management

Attitudes towards Corporate Social Responsibility in

Malaysia.Corporate Governance, 2(4), 10–16.

48. Roberts, P.W. & Dowling, G.R. (2002). Corporate reputation

and sustained superior financial performance. Strategic

Management Journal, 23, 1077–1093.

49. Ruf, B.M., Muralidhar, K., Brown R.M., Janney, J.J. &Paul,

K. (2001). An Empirical Investigation of the Relationship

between Change in Corporate Social Performance and

Financial Performance: A Stakeholder Theory Perspective.

Journal of Business Ethics, 32(2), 143–56.

50. Russo, M.V. & Fouts, P.A.(1997). A Resource-based Perspective

on Corporate Environmental Performance and Profitability.

Academy of Management Journal, 40(3), 534–59.

12. DeCarlo, L.T. (1997). On the meaning and use of kurtosis.

Psychological methods, 2(3), 292.

13. Ding, D.K., Ferreria, C. & Wongchoti, U. (2016). Does it pay

to be different? Relative CSR and its impact on firm value.

International Review of Financial Analysis, 47, 86–98.

14. Ernst and Ernst. (1978). Social Responsibility Disclosure,1978

Survey. Ohio: Cleveland.

15. Friedman, M. (1970). Social responsibility of business is to

increase profit. The New York Times Magazine, 13, 122-126.

16. Gama Boaventura, J.M., da Silva, R.S. & Bandeira-de-Mello, R.

(2012). Corporate Financial Performance and Corporate Social

Performance: methodological development and the theoretical

contribution of empirical studies. Revista Contabilidade &

Finanças, 23, 232–245.

17. Godfrey, P. C. & Hatch, N. W. (2007). Researching corporate

social responsibility: An agenda for the 21st century. Journal

of Business Ethics, 70, 87-98.

18. Govindarajan, A.L. and Amilan, S. (2013). A Study on linkage

between Corporate Social Responsibility Initiatives with

Financial Performances: Analysis from Oil and Gas Products

Industry in India.Pacific Business Review International, Vol

6 (5), 81-93.

19. Gray, R., R. Kouhy and S. Lavers. 1995. Corporate Socialand

Environmental Reporting: A Review of theLiterature and a

Longitudinal Study of UK Disclosure. Accounting, Auditing

and Accountability, 8(2), 47–77.

20. Griffin, J.J. and J.F. Mahon. (1997). The Corporate Social

Performance and Corporate Financial Performance Debate:

Twenty-Five Years of Incomparable Research.Business and

Society, 36(1), 5–31.

21. Guenster, N., Bauer, R., Derwall, J. & Koedijk, K. (2011).