Current Development in Accounting Thought

VerifiedAdded on 2022/11/28

|18

|3495

|317

AI Summary

This article discusses the current development in accounting thought, specifically focusing on credit impairments. It highlights the main concerns related to credit impairments and the impact on a company's financial assets. The article also reviews an exposure draft on financial instruments credit losses and discusses the major issues and comments from professional institutions. Overall, it provides valuable insights into the evolving accounting landscape.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running Head: CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

Name of the Student

Name of the University

Author Note

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

Name of the Student

Name of the University

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

Table of Contents

Question 1..................................................................................................................................2

Review of Article...................................................................................................................2

Question 2..................................................................................................................................5

Exposure Draft Major Issues..................................................................................................5

Comments Letter Views.........................................................................................................6

Comment Letter Assessments................................................................................................7

Comment Letter Actions Interpretation.................................................................................8

Reference..................................................................................................................................10

Table of Contents

Question 1..................................................................................................................................2

Review of Article...................................................................................................................2

Question 2..................................................................................................................................5

Exposure Draft Major Issues..................................................................................................5

Comments Letter Views.........................................................................................................6

Comment Letter Assessments................................................................................................7

Comment Letter Actions Interpretation.................................................................................8

Reference..................................................................................................................................10

2CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

Question 1

Review of Article

An article has been published on August 8, 2019, which has highlighted the main

concerns related to credit impairments. The financial assets of the company is termed as

credit impairment when the occurrences of the one or more than one events have detrimental

impact on estimated future cash flows of the financial assets. It generally occurs when the

creditworthiness of the company deteriorates. It is reflected by the assignment of the

reduction in credit rating to the organization. The impairment of the credit makes it difficult

for the company for borrowing more funds. The company might have the impaired credit if

their financial situations change in theway that of having greaterlikelihood of defaulting on

bond. In case of the business organization, creditworthiness would decline, if there is

deterioration of their financial position over time because of the weaker economy, poor

management as well as increasing competition. The impaired credit might requires for having

drastic changes to the procedures or the operations for alleviating the financial stress that

leads towards eventual improvements in the conditions of the balance sheet. The changes

includes reduction of the using of the cash flows for paying down the outstanding debt,

selling of the assets as well as reducing the expenses for bringing it to the manageable level.

The Article published in the news portal of Sydney Morning Herald has raised the

greatest example of credit loss of AMP. This is the financial services company in the country

of Australia as well as New Zealand. The company provides the product and services such as

banking advice and banking products that includes savings accounts and loans as well as

superannuation and the investment products. The issue of the company that has been

highlighted was involvement of the company for choosing to prioritize profit of short-term at

the expense of their best interest and the compliance with the regulatory. It has been found

Question 1

Review of Article

An article has been published on August 8, 2019, which has highlighted the main

concerns related to credit impairments. The financial assets of the company is termed as

credit impairment when the occurrences of the one or more than one events have detrimental

impact on estimated future cash flows of the financial assets. It generally occurs when the

creditworthiness of the company deteriorates. It is reflected by the assignment of the

reduction in credit rating to the organization. The impairment of the credit makes it difficult

for the company for borrowing more funds. The company might have the impaired credit if

their financial situations change in theway that of having greaterlikelihood of defaulting on

bond. In case of the business organization, creditworthiness would decline, if there is

deterioration of their financial position over time because of the weaker economy, poor

management as well as increasing competition. The impaired credit might requires for having

drastic changes to the procedures or the operations for alleviating the financial stress that

leads towards eventual improvements in the conditions of the balance sheet. The changes

includes reduction of the using of the cash flows for paying down the outstanding debt,

selling of the assets as well as reducing the expenses for bringing it to the manageable level.

The Article published in the news portal of Sydney Morning Herald has raised the

greatest example of credit loss of AMP. This is the financial services company in the country

of Australia as well as New Zealand. The company provides the product and services such as

banking advice and banking products that includes savings accounts and loans as well as

superannuation and the investment products. The issue of the company that has been

highlighted was involvement of the company for choosing to prioritize profit of short-term at

the expense of their best interest and the compliance with the regulatory. It has been found

3CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

that there was the involvement of company’s senior executive in the misconduct. In this

situation, apart from raising concerns, the company’s employees chosen for not disclosing the

knowledge they were having regarding the actions of the company in breaching of license

duties (Amp.com.au. 2019).

The issue has been raised in the article regarding the fact that how troubled AMP

wealth manager has taken steps in launching massive raising of the capital to underpin new

looking structure for their business controversial sale of life insurance, which is just after

having loss of $2.3 billion, during first half of financial year (Banks, 2016). AMP has

revealed regarding massive business restructure advice that would be affecting slash number

of the financial planners. There was halt of company’s shares to raise $650 million in highly

discounted raising of the capital from the existing investors of institutions. Credit Suisse as

well as UBS have fully underwritten the capital raised. The extension was done of bids

window, which indicated certain price pressures (Brown & Moles, 2014).

During the loss of the AMP of the first half of financial year, there were impairments

of $2.35 billion on financial planning part of the company. The impairments have been

occurred, which includes writing-down of the amount of $1.5 billion on the goodwill of the

business wealth management. In was done in wake of banking royal commission of the

previous year, in which it has been accused of misconduct. There was decline of 22 percent

on the company’s operating profit because of the misconduct done by the company (Creal et

al. 2014) This has resulted into non-payment of interim dividend as there was reduction of

around $1.3 million of earnings of wealth management operations. AMP has suffered on the

part of large net outflows, which was recorded up to $3.1 billion. For re-cutting the deals to

sell the insurance to the group of the UK/Bermudan Resolution Life for the amount of

$3billion, which is less than that of the original resolution of offer of $3.3 billion for the

business, the wealth manager of AMP would be using cash. This new deal would result in

that there was the involvement of company’s senior executive in the misconduct. In this

situation, apart from raising concerns, the company’s employees chosen for not disclosing the

knowledge they were having regarding the actions of the company in breaching of license

duties (Amp.com.au. 2019).

The issue has been raised in the article regarding the fact that how troubled AMP

wealth manager has taken steps in launching massive raising of the capital to underpin new

looking structure for their business controversial sale of life insurance, which is just after

having loss of $2.3 billion, during first half of financial year (Banks, 2016). AMP has

revealed regarding massive business restructure advice that would be affecting slash number

of the financial planners. There was halt of company’s shares to raise $650 million in highly

discounted raising of the capital from the existing investors of institutions. Credit Suisse as

well as UBS have fully underwritten the capital raised. The extension was done of bids

window, which indicated certain price pressures (Brown & Moles, 2014).

During the loss of the AMP of the first half of financial year, there were impairments

of $2.35 billion on financial planning part of the company. The impairments have been

occurred, which includes writing-down of the amount of $1.5 billion on the goodwill of the

business wealth management. In was done in wake of banking royal commission of the

previous year, in which it has been accused of misconduct. There was decline of 22 percent

on the company’s operating profit because of the misconduct done by the company (Creal et

al. 2014) This has resulted into non-payment of interim dividend as there was reduction of

around $1.3 million of earnings of wealth management operations. AMP has suffered on the

part of large net outflows, which was recorded up to $3.1 billion. For re-cutting the deals to

sell the insurance to the group of the UK/Bermudan Resolution Life for the amount of

$3billion, which is less than that of the original resolution of offer of $3.3 billion for the

business, the wealth manager of AMP would be using cash. This new deal would result in

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

receiving cash for the amount of $2.5 billion as well as $500 from equity interest of the

Resolution Life Australia. This particular deal would hold no interest in the matured business

that would be selling to Resolution life. The original planning was done to retain 40 percent

stake in matured business of the cash producing. Executive chairman of the Resolution life

Clive cowdery has welcomed this re-deal and has stated that it is delightful that resolution is

present in the country of Australia as well as New Zealand (Annappindi, 2014).

There was great impact of this on the company. Hence, it is now planning to reset and

draw new bright future of the company. AMP has stated that there are short-term impacts of

shocks and crisis but company is now taking steps for doing repositioning of their business to

gain clients trust. In this respect, the total amount of $778 million has been taken aside in

order to fund the costs to compensate their customers. AMP has also made provisions of $1.3

billion to fund any future reconstructions of wealth arm (Siriwardane, 2015).

This article has raised issue that relates to criticism received by AMP for the new deal

with Resolution. It is because of forceful act of re-cutting after the refusal by Reserve Bank

of New Zealand to approve deal over local policy holders concerns. The company has cope

up with the flaming from the investors over deal with resolution with shareholders

(Domnikov, Khomenko & Chebotareva, 2014). Several questions have been raised by the

company as the result of problem faced by company for the significance of re-cutting deals to

satisfy the concerns raised by Reserve Bank of New Zealand. It is because of this there has

been new appointment of chief financial officer after the resignation of John Patrick, who

was CFO of the company (Harris, Khan & Nissim, 2018).

Hence, from the review of the article, it can be concluded that impairments of credit

needs major amount of procedures changes in the business organization, in order to alleviate

receiving cash for the amount of $2.5 billion as well as $500 from equity interest of the

Resolution Life Australia. This particular deal would hold no interest in the matured business

that would be selling to Resolution life. The original planning was done to retain 40 percent

stake in matured business of the cash producing. Executive chairman of the Resolution life

Clive cowdery has welcomed this re-deal and has stated that it is delightful that resolution is

present in the country of Australia as well as New Zealand (Annappindi, 2014).

There was great impact of this on the company. Hence, it is now planning to reset and

draw new bright future of the company. AMP has stated that there are short-term impacts of

shocks and crisis but company is now taking steps for doing repositioning of their business to

gain clients trust. In this respect, the total amount of $778 million has been taken aside in

order to fund the costs to compensate their customers. AMP has also made provisions of $1.3

billion to fund any future reconstructions of wealth arm (Siriwardane, 2015).

This article has raised issue that relates to criticism received by AMP for the new deal

with Resolution. It is because of forceful act of re-cutting after the refusal by Reserve Bank

of New Zealand to approve deal over local policy holders concerns. The company has cope

up with the flaming from the investors over deal with resolution with shareholders

(Domnikov, Khomenko & Chebotareva, 2014). Several questions have been raised by the

company as the result of problem faced by company for the significance of re-cutting deals to

satisfy the concerns raised by Reserve Bank of New Zealand. It is because of this there has

been new appointment of chief financial officer after the resignation of John Patrick, who

was CFO of the company (Harris, Khan & Nissim, 2018).

Hence, from the review of the article, it can be concluded that impairments of credit

needs major amount of procedures changes in the business organization, in order to alleviate

5CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

financial stress. These changes would lead towards improvements of the balance-sheet

conditions (Bahnsen et al. 2014).

Question 2

Exposure Draft Major Issues

On June 2, 2019, FASB has issued their exposure draft on “Financial Instruments

credit Losses. It was the proposed standards of the Accounting update on the Targeted

Transition relief for Topic 326. FASB has received various requests since long regarding

amendments in the transitions guidance for update of the 2016-13. Various professional

institutions have taken steps for submitting agenda letter that have stated that certain

preparers of financial statements are planning for electing the options of fair value in order to

purchase financial assets (Cohen & Edwards, 2017). However, those particular firms have

used for measuring financial assets on historically historical based cost of the amortization.

Further, those firms would be adopting the method of dual measurement techniques, if in case

no amendments would have been done by FASB. Hence, as a result of which, there won’t be

any kind of comparisons of the financial statements by users. Further, if this amendment is

done then it would help in providing relief of the transition that is targeted with the intention

to increase comparability of the information of the financial statements for the certain

business organization, which would otherwise helpful for the measurement of the same

financial instruments by other measurement methodologies. (Weber, Hoque & Ayub Islam,

2015). In addition, there would be reduction of the cost of preparers of the financial

statements. This would result in the enhancement of the users for taking decisions that are

based on useful information (Fasb.org. 2019). Hence, some of the major issues, which are

covered in FASB proposed update for which individuals and the professional institutions are

invited to providing their valuable comments:

financial stress. These changes would lead towards improvements of the balance-sheet

conditions (Bahnsen et al. 2014).

Question 2

Exposure Draft Major Issues

On June 2, 2019, FASB has issued their exposure draft on “Financial Instruments

credit Losses. It was the proposed standards of the Accounting update on the Targeted

Transition relief for Topic 326. FASB has received various requests since long regarding

amendments in the transitions guidance for update of the 2016-13. Various professional

institutions have taken steps for submitting agenda letter that have stated that certain

preparers of financial statements are planning for electing the options of fair value in order to

purchase financial assets (Cohen & Edwards, 2017). However, those particular firms have

used for measuring financial assets on historically historical based cost of the amortization.

Further, those firms would be adopting the method of dual measurement techniques, if in case

no amendments would have been done by FASB. Hence, as a result of which, there won’t be

any kind of comparisons of the financial statements by users. Further, if this amendment is

done then it would help in providing relief of the transition that is targeted with the intention

to increase comparability of the information of the financial statements for the certain

business organization, which would otherwise helpful for the measurement of the same

financial instruments by other measurement methodologies. (Weber, Hoque & Ayub Islam,

2015). In addition, there would be reduction of the cost of preparers of the financial

statements. This would result in the enhancement of the users for taking decisions that are

based on useful information (Fasb.org. 2019). Hence, some of the major issues, which are

covered in FASB proposed update for which individuals and the professional institutions are

invited to providing their valuable comments:

6CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

The option of irrevocable electing of the fair value is provided to the institutions in

subtopic of the eligible instruments. This is based on assumption that irrevocable

electing of fair value must be within area of subtopic 326-20. It is except debt

securities held for maturity.

The proposed amendments require the options of irrevocable electing the fair value,

which should be applied based on the instruments by instruments (Fasb.org. 2019).

The decisions of the board for providing firms with the option for continuing the

measurement of fair value of the financial assets is measuring raw materials with the

technique of fair value with net income. The application of guidance in the

measurement is given in subtopic 325-30 (Linnenluecke et al. 2015).

There is the requirement for additional disclosures in the proposed amendments that is

beyond to the disclosures requirements of topic 250, subtopics 825-10 and the

changes in the accounting as well as corrections of the error.

If any firms have already adopted the topic 326 the board of director needs effective

date and the transitions for amendments that is proposed.

Comments Letter Views

When the exposure draft has been prepared by the standard setting body FASB then it

is presented to all the parties interested and along with that invitation for the comments by the

different financial institutions, professional institutions as well as individuals is done so that

before making it as the standard, steps are taken to know the feedback. Following are certain

comments given by well known institutions.

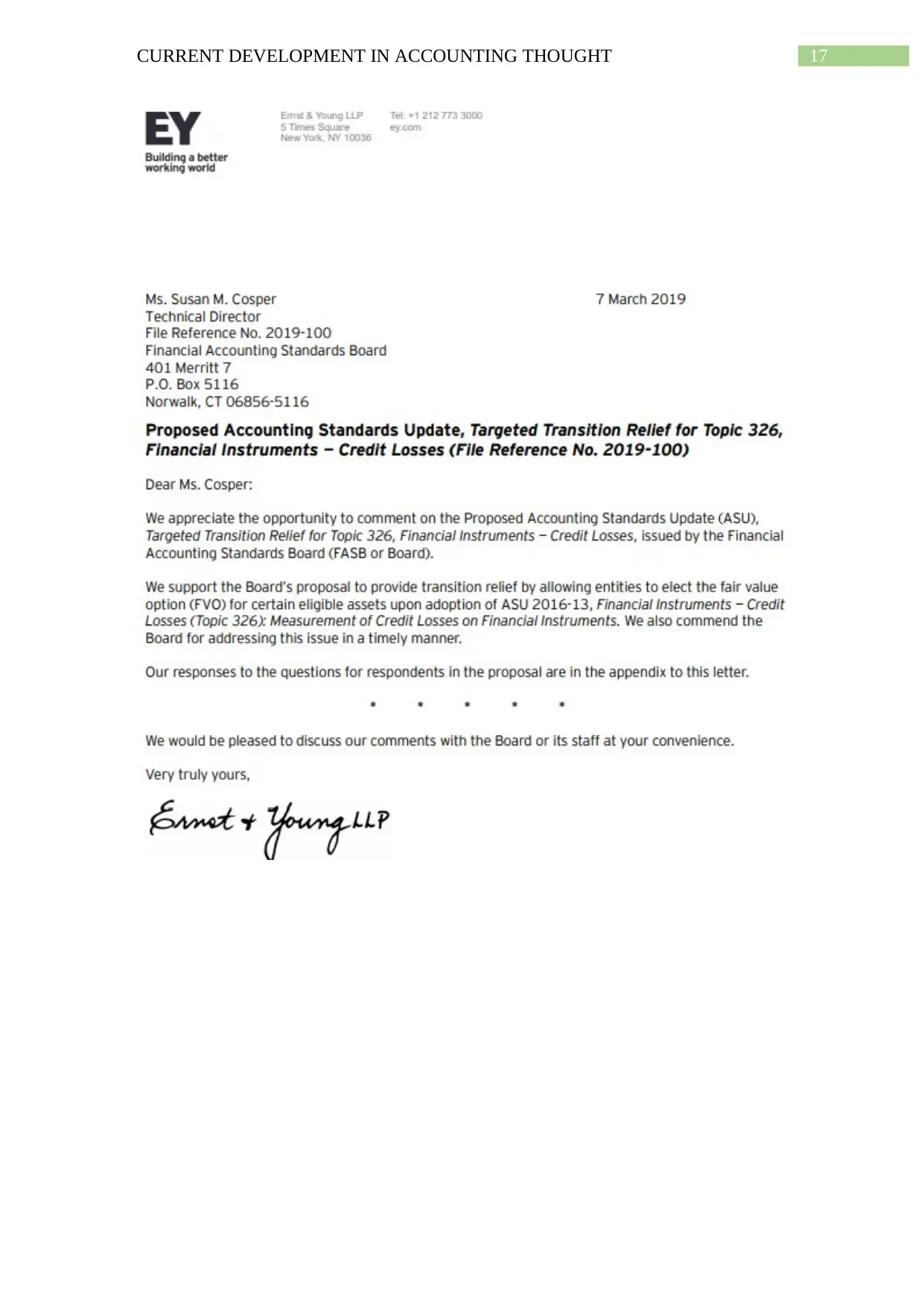

Ernst & Young- The comment given by the multinational professional services firm,

Ernst & Young is in the support of the proposed exposure draft. This institution has

the view that this proposal would give relief in electing the option of fair value

The option of irrevocable electing of the fair value is provided to the institutions in

subtopic of the eligible instruments. This is based on assumption that irrevocable

electing of fair value must be within area of subtopic 326-20. It is except debt

securities held for maturity.

The proposed amendments require the options of irrevocable electing the fair value,

which should be applied based on the instruments by instruments (Fasb.org. 2019).

The decisions of the board for providing firms with the option for continuing the

measurement of fair value of the financial assets is measuring raw materials with the

technique of fair value with net income. The application of guidance in the

measurement is given in subtopic 325-30 (Linnenluecke et al. 2015).

There is the requirement for additional disclosures in the proposed amendments that is

beyond to the disclosures requirements of topic 250, subtopics 825-10 and the

changes in the accounting as well as corrections of the error.

If any firms have already adopted the topic 326 the board of director needs effective

date and the transitions for amendments that is proposed.

Comments Letter Views

When the exposure draft has been prepared by the standard setting body FASB then it

is presented to all the parties interested and along with that invitation for the comments by the

different financial institutions, professional institutions as well as individuals is done so that

before making it as the standard, steps are taken to know the feedback. Following are certain

comments given by well known institutions.

Ernst & Young- The comment given by the multinational professional services firm,

Ernst & Young is in the support of the proposed exposure draft. This institution has

the view that this proposal would give relief in electing the option of fair value

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

measurement. The board of the company would be helped in addressing issues and

that too in the timely manner (Ey.com. 2019).

Moody Analytics- The international rating agency, Moody Analytics has given their

comment in favor of proposed agenda. This institution has stated that the proposed

exposure draft would provide transition ease for standards of the credit losses by the

help of options for the measurement of the assets of the particular by fair value

method (Moodysanalytics.com. 2019).

Grant Thornton- The sixth largest US accounting and the advisory organization,

Grant Thornton have given the comment, which shows disagreement on exposure

draft framed by FASB. This organization has stated that this amendment would

require to adopt ASU 2016-13 in the fiscal year that means prior to the beginning of

December 15, 2021, which is applicable to all reporting firm except that of the public

firm. Moreover, during the fiscal year after December 15, 2021, there won’t be any

impact of ASU 2018-19 of requirement of effective date for public firm. Further, from

scope of the ASC 326-20, receivables of operating leases are being excluded.

However, this has to be instead accounts for the impairments of the receivables that

result from operating lease, under ASC 842 guidance (Grantthornton.com. 2019).

KPMG- The comment given by the well known accounting firm, KPMG has

supported FASB for the amendments proposed by them. They stated that the proposal

by KPMG would increase measurement of fair value of loan amount. The method

proposed by the FASB would be helpful in respect of allocation of the fair value of

the gains and the losses of the financial statements in the presentations of the separate

interest income. For the investors of the financial institutions, this measurement

approach would be considered as important (Frv.kpmg.us. 2019).

measurement. The board of the company would be helped in addressing issues and

that too in the timely manner (Ey.com. 2019).

Moody Analytics- The international rating agency, Moody Analytics has given their

comment in favor of proposed agenda. This institution has stated that the proposed

exposure draft would provide transition ease for standards of the credit losses by the

help of options for the measurement of the assets of the particular by fair value

method (Moodysanalytics.com. 2019).

Grant Thornton- The sixth largest US accounting and the advisory organization,

Grant Thornton have given the comment, which shows disagreement on exposure

draft framed by FASB. This organization has stated that this amendment would

require to adopt ASU 2016-13 in the fiscal year that means prior to the beginning of

December 15, 2021, which is applicable to all reporting firm except that of the public

firm. Moreover, during the fiscal year after December 15, 2021, there won’t be any

impact of ASU 2018-19 of requirement of effective date for public firm. Further, from

scope of the ASC 326-20, receivables of operating leases are being excluded.

However, this has to be instead accounts for the impairments of the receivables that

result from operating lease, under ASC 842 guidance (Grantthornton.com. 2019).

KPMG- The comment given by the well known accounting firm, KPMG has

supported FASB for the amendments proposed by them. They stated that the proposal

by KPMG would increase measurement of fair value of loan amount. The method

proposed by the FASB would be helpful in respect of allocation of the fair value of

the gains and the losses of the financial statements in the presentations of the separate

interest income. For the investors of the financial institutions, this measurement

approach would be considered as important (Frv.kpmg.us. 2019).

8CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

Comment Letter Assessments

The theory of public interest is defined as that theory of regulator, under which

benefits are being provided by the concerned body in order to protect the public at large. This

theory aims for allocating resources in the best possible ways for individual as well as

collective purposes. The regulation made in public interest employs legal instruments with

the aim of implementing policies of socio-economies (Majid, 2015).

The behaviors that are being displayed by the financial institutions of the amendments

that are presented in the exposure draft by FASB have justified the theory of public interest.

The major reason for this behavior is the fact that this amendment would address major

stakeholders concerns with the help of giving options for electing irrecoverably fair value for

some financial assets that is measured earlier on amortization costs (Fasb.org. 2019). The

targeted transition relief would increase information comparability of methodologies of

measurement for the same financial assets. Moreover, targeted relief transition would reduce

certain organizational costs to comply with amendments done in update 2016-13. This

amendment would be promoting public welfare because this would provide assistance for

providing useful information of the financial statements. This would be enhancing user’s

decision making (Darrough, Guler & Wang, 2014).

Comment Letter Actions Interpretation

Public interest theory promotes general public welfare rather than well-organized

stakeholders. Moreover, the regulation acknowledges the individual and group form for

pursuing self-interest. This theory in general, helps in dominating the regulatory processes.

The regulations in the private interest theory are more concerned regarding power

competition rather than public interests. In general, the private groups are more engaged with

lobbying activities. In case, when the markets of the regulation are based on the supply and

the demand then in that case, there is more chance of lobbying (Fernandes et al. 2016). At

Comment Letter Assessments

The theory of public interest is defined as that theory of regulator, under which

benefits are being provided by the concerned body in order to protect the public at large. This

theory aims for allocating resources in the best possible ways for individual as well as

collective purposes. The regulation made in public interest employs legal instruments with

the aim of implementing policies of socio-economies (Majid, 2015).

The behaviors that are being displayed by the financial institutions of the amendments

that are presented in the exposure draft by FASB have justified the theory of public interest.

The major reason for this behavior is the fact that this amendment would address major

stakeholders concerns with the help of giving options for electing irrecoverably fair value for

some financial assets that is measured earlier on amortization costs (Fasb.org. 2019). The

targeted transition relief would increase information comparability of methodologies of

measurement for the same financial assets. Moreover, targeted relief transition would reduce

certain organizational costs to comply with amendments done in update 2016-13. This

amendment would be promoting public welfare because this would provide assistance for

providing useful information of the financial statements. This would be enhancing user’s

decision making (Darrough, Guler & Wang, 2014).

Comment Letter Actions Interpretation

Public interest theory promotes general public welfare rather than well-organized

stakeholders. Moreover, the regulation acknowledges the individual and group form for

pursuing self-interest. This theory in general, helps in dominating the regulatory processes.

The regulations in the private interest theory are more concerned regarding power

competition rather than public interests. In general, the private groups are more engaged with

lobbying activities. In case, when the markets of the regulation are based on the supply and

the demand then in that case, there is more chance of lobbying (Fernandes et al. 2016). At

9CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

last, capture theory aims for manipulating the regulations for getting fit in requirements of the

concerned organizations or the individuals that are affected by theory. It helps in serving

interests of the concerned industry over particular period. This holds assumptions that

regulations are being supplied in the response of demands of groups that is interests in it and

those who are trying for maximizing income or members interest (Fasb.org. 2019).

Ernst & Young, stated that the amendments proposed in exposure draft would help to

serve interests of all organizations and the general investors. Moreover, Moody Analytics

statement also justifies the theory of public interest. As per them, this amendment can be

applied in the every reporting firm within the scope. Further, Grant Thornton stated that this

particular amendment would aims for meeting the needs of private organization rather than

public organizations (Fasb.org. 2019). KPMG, stated that the amendments proposed in the

exposure draft serve investors need in measurements of the fair value in the financial

statement. This statement by Ernst & Young gives justification of the public interest theory.

Hence, statement given by these institutions would help in serving public interest theory

(Calem, Lambie-Hanson & Nakamura, 2015).

Hence, it can be concluded after looking at the view points and comments of the

professional institutions that public interest theory is being served by the exposure draft. The

proposed amendments would be beneficial for the public as a whole.

last, capture theory aims for manipulating the regulations for getting fit in requirements of the

concerned organizations or the individuals that are affected by theory. It helps in serving

interests of the concerned industry over particular period. This holds assumptions that

regulations are being supplied in the response of demands of groups that is interests in it and

those who are trying for maximizing income or members interest (Fasb.org. 2019).

Ernst & Young, stated that the amendments proposed in exposure draft would help to

serve interests of all organizations and the general investors. Moreover, Moody Analytics

statement also justifies the theory of public interest. As per them, this amendment can be

applied in the every reporting firm within the scope. Further, Grant Thornton stated that this

particular amendment would aims for meeting the needs of private organization rather than

public organizations (Fasb.org. 2019). KPMG, stated that the amendments proposed in the

exposure draft serve investors need in measurements of the fair value in the financial

statement. This statement by Ernst & Young gives justification of the public interest theory.

Hence, statement given by these institutions would help in serving public interest theory

(Calem, Lambie-Hanson & Nakamura, 2015).

Hence, it can be concluded after looking at the view points and comments of the

professional institutions that public interest theory is being served by the exposure draft. The

proposed amendments would be beneficial for the public as a whole.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

Reference

Amp.com.au. 2019. loans, H., retirement, S., & hub, F.. AMP Personal Banking - Accounts,

Super, Home Loans & Insurance | AMP. Retrieved 4 September 2019, from

https://www.amp.com.au/

Annappindi, S. K. (2014). U.S. Patent No. 8,799,150. Washington, DC: U.S. Patent and

Trademark Office.

Bahnsen, A. C., Stojanovic, A., Aouada, D., &Ottersten, B. (2014, April). Improving credit

card fraud detection with calibrated probabilities. In Proceedings of the 2014 SIAM

international conference on data mining (pp. 677-685). Society for Industrial and

Applied Mathematics.

Banks, E. (2016). The credit risk of complex derivatives. Springer.

Brown, K., & Moles, P. (2014). Credit risk management. K. Brown & P. Moles, Credit Risk

Management, 16.

Calem, P. S., Lambie-Hanson, L., & Nakamura, L. I. (2015). Information losses in home

purchase appraisals.

Cohen, B. H., & Edwards, G. (2017). The new era of expected credit loss provisioning. BIS

Quarterly Review, March.

Creal, D., Schwaab, B., Koopman, S. J., & Lucas, A. (2014). Observation-driven mixed-

measurement dynamic factor models with an application to credit risk. Review of

Economics and Statistics, 96(5), 898-915.

Darrough, M. N., Guler, L., & Wang, P. (2014). Goodwill impairment losses and CEO

compensation. Journal of Accounting, Auditing & Finance, 29(4), 435-463.

Reference

Amp.com.au. 2019. loans, H., retirement, S., & hub, F.. AMP Personal Banking - Accounts,

Super, Home Loans & Insurance | AMP. Retrieved 4 September 2019, from

https://www.amp.com.au/

Annappindi, S. K. (2014). U.S. Patent No. 8,799,150. Washington, DC: U.S. Patent and

Trademark Office.

Bahnsen, A. C., Stojanovic, A., Aouada, D., &Ottersten, B. (2014, April). Improving credit

card fraud detection with calibrated probabilities. In Proceedings of the 2014 SIAM

international conference on data mining (pp. 677-685). Society for Industrial and

Applied Mathematics.

Banks, E. (2016). The credit risk of complex derivatives. Springer.

Brown, K., & Moles, P. (2014). Credit risk management. K. Brown & P. Moles, Credit Risk

Management, 16.

Calem, P. S., Lambie-Hanson, L., & Nakamura, L. I. (2015). Information losses in home

purchase appraisals.

Cohen, B. H., & Edwards, G. (2017). The new era of expected credit loss provisioning. BIS

Quarterly Review, March.

Creal, D., Schwaab, B., Koopman, S. J., & Lucas, A. (2014). Observation-driven mixed-

measurement dynamic factor models with an application to credit risk. Review of

Economics and Statistics, 96(5), 898-915.

Darrough, M. N., Guler, L., & Wang, P. (2014). Goodwill impairment losses and CEO

compensation. Journal of Accounting, Auditing & Finance, 29(4), 435-463.

11CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

Domnikov, A., Khomenko, P., &Chebotareva, G. (2014). A risk-oriented approach to capital

management at a power generation company in Russia. WIT Trans. Ecol. Environ, 1,

13-24.

Ey.com. 2019. Retrieved 4 September 2019, from

https://www.ey.com/publication/vwluassetsdld/commentletter_06005-191us_fvo-

ed_7march2019/$file/commentletter_06005-191us_fvo-ed_7march2019.pdf?

OpenElement

Fasb.org. (2019). Proposed Accounting Standards Update—Targeted Transition Relief for

Topic 326, Financial Instruments—Credit Losses. Retrieved 4 September 2019, from

https://www.fasb.org/cs/Satellite?

c=Document_C&cid=1176172031887&pagename=FASB%2FDocument_C

%2FDocumentPage

Fernandes, J. S., Gonçalves, C., Guerreiro, C., & Pereira, L. (2016). Impairment losses:

causes and impacts. RBGN-RevistaBrasileira de Gestão De Negócios, 18(60), 305-

318.

Frv.kpmg.us. 2019. Retrieved 4 September 2019, from

https://frv.kpmg.us/content/dam/frv/en/pdfs/2019/kpmg_comment_letter_credit_loss_

standard.pdf

Grantthornton.com. 2019. On The Horizon: FASB amends credit losses guidance. Retrieved

4 September 2019, from

https://www.grantthornton.com/library/newsletters/audit/2018/on-the-horizon/

november/FASB-amends-credit-losses-guidance.aspx

Harris, T. S., Khan, U., &Nissim, D. (2018). The Expected Rate of Credit Losses on Banks'

Loan Portfolios. The Accounting Review, 93(5), 245-271.

Domnikov, A., Khomenko, P., &Chebotareva, G. (2014). A risk-oriented approach to capital

management at a power generation company in Russia. WIT Trans. Ecol. Environ, 1,

13-24.

Ey.com. 2019. Retrieved 4 September 2019, from

https://www.ey.com/publication/vwluassetsdld/commentletter_06005-191us_fvo-

ed_7march2019/$file/commentletter_06005-191us_fvo-ed_7march2019.pdf?

OpenElement

Fasb.org. (2019). Proposed Accounting Standards Update—Targeted Transition Relief for

Topic 326, Financial Instruments—Credit Losses. Retrieved 4 September 2019, from

https://www.fasb.org/cs/Satellite?

c=Document_C&cid=1176172031887&pagename=FASB%2FDocument_C

%2FDocumentPage

Fernandes, J. S., Gonçalves, C., Guerreiro, C., & Pereira, L. (2016). Impairment losses:

causes and impacts. RBGN-RevistaBrasileira de Gestão De Negócios, 18(60), 305-

318.

Frv.kpmg.us. 2019. Retrieved 4 September 2019, from

https://frv.kpmg.us/content/dam/frv/en/pdfs/2019/kpmg_comment_letter_credit_loss_

standard.pdf

Grantthornton.com. 2019. On The Horizon: FASB amends credit losses guidance. Retrieved

4 September 2019, from

https://www.grantthornton.com/library/newsletters/audit/2018/on-the-horizon/

november/FASB-amends-credit-losses-guidance.aspx

Harris, T. S., Khan, U., &Nissim, D. (2018). The Expected Rate of Credit Losses on Banks'

Loan Portfolios. The Accounting Review, 93(5), 245-271.

12CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

Linnenluecke, M. K., Birt, J., Lyon, J., & Sidhu, B. K. (2015). Planetary boundaries:

implications for asset impairment. Accounting & Finance, 55(4), 911-929.

Majid, J. A. (2015). Reporting incentives, ownership concentration by the largest outside

shareholder, and reported goodwill impairment losses. Journal of contemporary

accounting & economics, 11(3), 199-214.

Moodysanalytics.com. 2019. FASB Proposes Targeted Transition Relief for Credit Losses

Standard. Retrieved 4 September 2019, from

https://www.moodysanalytics.com/regulatory-news/feb-07-19-fasb-proposes-

targeted-transition-relief-for-credit-losses-standard

Siriwardane, E. N. (2015). Concentrated capital losses and the pricing of corporate credit

risk. Harvard Business School working paper series# 16-007.

Weber, O., Hoque, A., &Ayub Islam, M. (2015). Incorporating environmental criteria into

credit risk management in Bangladeshi banks. Journal of Sustainable Finance &

Investment, 5(1-2), 1-15.

Linnenluecke, M. K., Birt, J., Lyon, J., & Sidhu, B. K. (2015). Planetary boundaries:

implications for asset impairment. Accounting & Finance, 55(4), 911-929.

Majid, J. A. (2015). Reporting incentives, ownership concentration by the largest outside

shareholder, and reported goodwill impairment losses. Journal of contemporary

accounting & economics, 11(3), 199-214.

Moodysanalytics.com. 2019. FASB Proposes Targeted Transition Relief for Credit Losses

Standard. Retrieved 4 September 2019, from

https://www.moodysanalytics.com/regulatory-news/feb-07-19-fasb-proposes-

targeted-transition-relief-for-credit-losses-standard

Siriwardane, E. N. (2015). Concentrated capital losses and the pricing of corporate credit

risk. Harvard Business School working paper series# 16-007.

Weber, O., Hoque, A., &Ayub Islam, M. (2015). Incorporating environmental criteria into

credit risk management in Bangladeshi banks. Journal of Sustainable Finance &

Investment, 5(1-2), 1-15.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

Newspaper Link

https://www.smh.com.au/business/banking-and-finance/amp-to-raise-capital-after-2-

3-billion-loss-20190808-p52ezo.html

Comments Letter Link

https://www.grantthornton.com/library/newsletters/audit/2018/on-the-horizon/

november/FASB-amends-credit-losses-guidance.aspx

https://www.moodysanalytics.com/regulatory-news/feb-07-19-fasb-proposes-

targeted-transition-relief-for-credit-losses-standard

https://frv.kpmg.us/content/dam/frv/en/pdfs/2019/

kpmg_comment_letter_credit_loss_standard.pdf

https://www.ey.com/publication/vwluassetsdld/commentletter_06005-191us_fvo-

ed_7march2019/$file/commentletter_06005-191us_fvo-ed_7march2019.pdf?

OpenElement

Newspaper Link

https://www.smh.com.au/business/banking-and-finance/amp-to-raise-capital-after-2-

3-billion-loss-20190808-p52ezo.html

Comments Letter Link

https://www.grantthornton.com/library/newsletters/audit/2018/on-the-horizon/

november/FASB-amends-credit-losses-guidance.aspx

https://www.moodysanalytics.com/regulatory-news/feb-07-19-fasb-proposes-

targeted-transition-relief-for-credit-losses-standard

https://frv.kpmg.us/content/dam/frv/en/pdfs/2019/

kpmg_comment_letter_credit_loss_standard.pdf

https://www.ey.com/publication/vwluassetsdld/commentletter_06005-191us_fvo-

ed_7march2019/$file/commentletter_06005-191us_fvo-ed_7march2019.pdf?

OpenElement

14CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

Appendix

Appendix

15CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

17CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.