CVP and Financial Statement Analysis of Ytrew Limited and Competitor

VerifiedAdded on 2023/01/06

|11

|1449

|39

Report

AI Summary

This report presents a comprehensive financial analysis of Ytrew Limited, comparing its performance to a competitor using financial ratios and a break-even analysis. Part A delves into the financial statements, assessing liquidity, capital structure, and operating profit. Key ratios like the current ratio, quick ratio, debt ratio, and return on equity are calculated and compared. The analysis reveals that while both firms have strong liquidity positions, Ytrew Limited's operating profit lags behind its competitor. Part B focuses on the break-even point and cost-volume-profit (CVP) analysis, exploring the impact of changes in selling price, variable costs, and production methods on profitability. The report recommends that Ytrew Limited consider changes in production methods to improve its long-term profitability based on projected profit increases with the new methods. The conclusion emphasizes the importance of financial statement analysis for effective business decision-making, highlighting the use of ratios in assessing a company's position within a competitive market.

CVP AND FINANCIAL STATEMENT

ANALYSIS

ANALYSIS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Current report is divided into two part. Part A highlight the Financial statement analysis of Ytrew

Limited and its competitor. On the basis of the same after that repost highlights the comparison

between both the company on the basis of operating profit, Liquidity and Return on Equity. In the

PART B of the report highlights the break even point for the company and on the basis of the same

Cost volume profit chart of the company. In the end report recommend whether desire changes in

production and machinery need to be made by the organization or not.

Current report is divided into two part. Part A highlight the Financial statement analysis of Ytrew

Limited and its competitor. On the basis of the same after that repost highlights the comparison

between both the company on the basis of operating profit, Liquidity and Return on Equity. In the

PART B of the report highlights the break even point for the company and on the basis of the same

Cost volume profit chart of the company. In the end report recommend whether desire changes in

production and machinery need to be made by the organization or not.

Table of Contents

PART A.................................................................................................................................................4

PART B.................................................................................................................................................6

CONCLUSION....................................................................................................................................8

APPENDIX.........................................................................................................................................11

PART A.................................................................................................................................................4

PART B.................................................................................................................................................6

CONCLUSION....................................................................................................................................8

APPENDIX.........................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

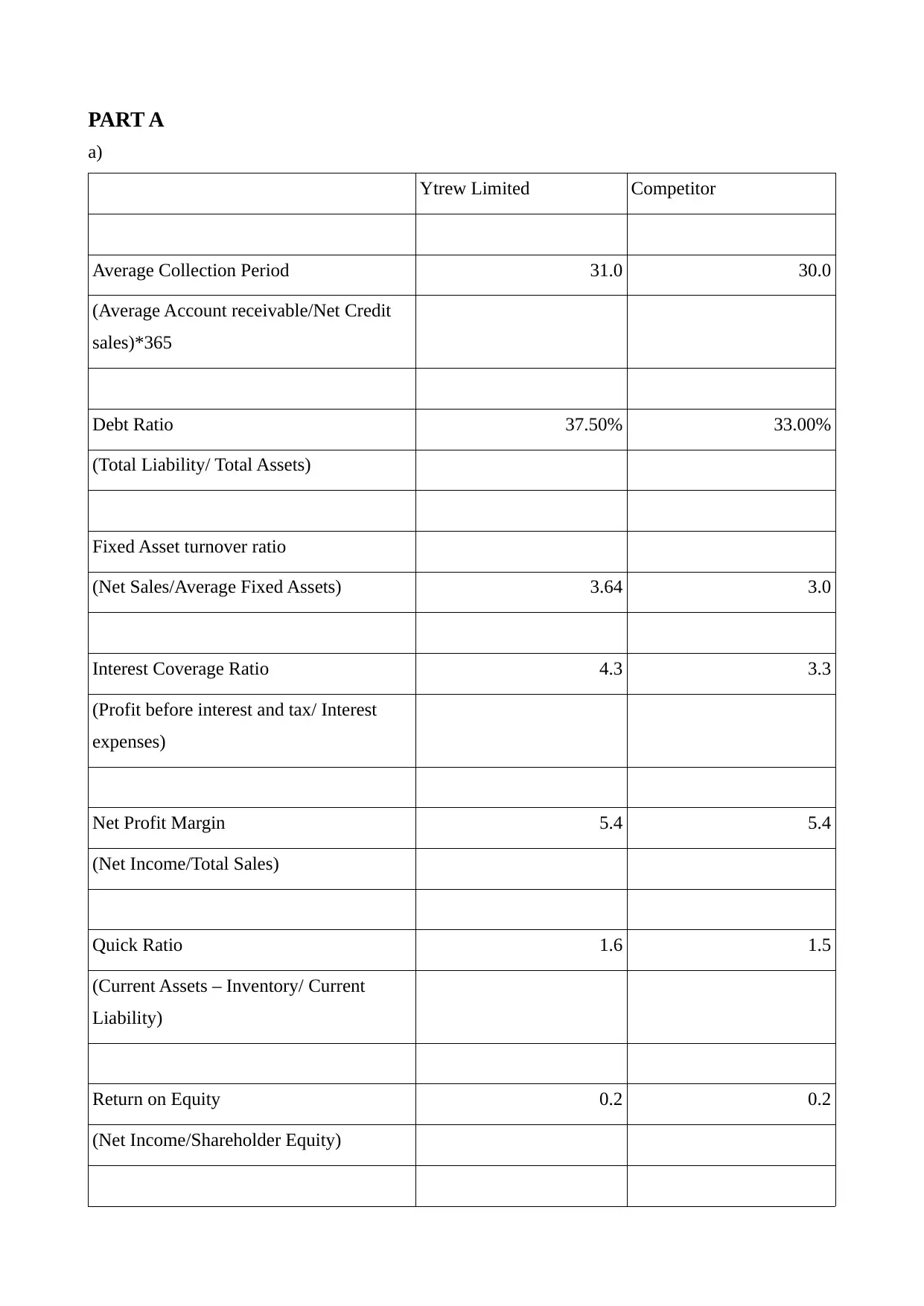

PART A

a)

Ytrew Limited Competitor

Average Collection Period 31.0 30.0

(Average Account receivable/Net Credit

sales)*365

Debt Ratio 37.50% 33.00%

(Total Liability/ Total Assets)

Fixed Asset turnover ratio

(Net Sales/Average Fixed Assets) 3.64 3.0

Interest Coverage Ratio 4.3 3.3

(Profit before interest and tax/ Interest

expenses)

Net Profit Margin 5.4 5.4

(Net Income/Total Sales)

Quick Ratio 1.6 1.5

(Current Assets – Inventory/ Current

Liability)

Return on Equity 0.2 0.2

(Net Income/Shareholder Equity)

a)

Ytrew Limited Competitor

Average Collection Period 31.0 30.0

(Average Account receivable/Net Credit

sales)*365

Debt Ratio 37.50% 33.00%

(Total Liability/ Total Assets)

Fixed Asset turnover ratio

(Net Sales/Average Fixed Assets) 3.64 3.0

Interest Coverage Ratio 4.3 3.3

(Profit before interest and tax/ Interest

expenses)

Net Profit Margin 5.4 5.4

(Net Income/Total Sales)

Quick Ratio 1.6 1.5

(Current Assets – Inventory/ Current

Liability)

Return on Equity 0.2 0.2

(Net Income/Shareholder Equity)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

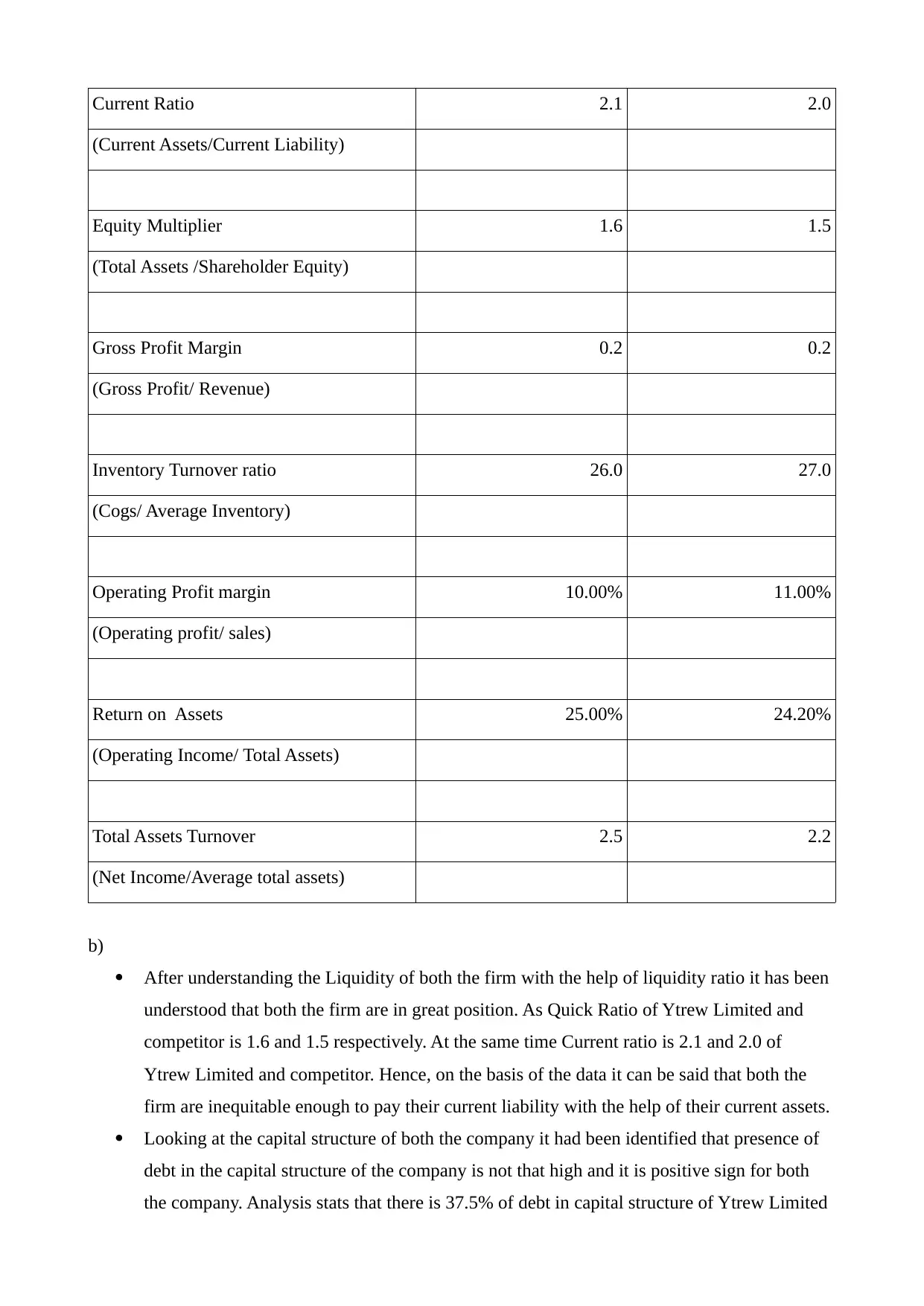

Current Ratio 2.1 2.0

(Current Assets/Current Liability)

Equity Multiplier 1.6 1.5

(Total Assets /Shareholder Equity)

Gross Profit Margin 0.2 0.2

(Gross Profit/ Revenue)

Inventory Turnover ratio 26.0 27.0

(Cogs/ Average Inventory)

Operating Profit margin 10.00% 11.00%

(Operating profit/ sales)

Return on Assets 25.00% 24.20%

(Operating Income/ Total Assets)

Total Assets Turnover 2.5 2.2

(Net Income/Average total assets)

b)

After understanding the Liquidity of both the firm with the help of liquidity ratio it has been

understood that both the firm are in great position. As Quick Ratio of Ytrew Limited and

competitor is 1.6 and 1.5 respectively. At the same time Current ratio is 2.1 and 2.0 of

Ytrew Limited and competitor. Hence, on the basis of the data it can be said that both the

firm are inequitable enough to pay their current liability with the help of their current assets.

Looking at the capital structure of both the company it had been identified that presence of

debt in the capital structure of the company is not that high and it is positive sign for both

the company. Analysis stats that there is 37.5% of debt in capital structure of Ytrew Limited

(Current Assets/Current Liability)

Equity Multiplier 1.6 1.5

(Total Assets /Shareholder Equity)

Gross Profit Margin 0.2 0.2

(Gross Profit/ Revenue)

Inventory Turnover ratio 26.0 27.0

(Cogs/ Average Inventory)

Operating Profit margin 10.00% 11.00%

(Operating profit/ sales)

Return on Assets 25.00% 24.20%

(Operating Income/ Total Assets)

Total Assets Turnover 2.5 2.2

(Net Income/Average total assets)

b)

After understanding the Liquidity of both the firm with the help of liquidity ratio it has been

understood that both the firm are in great position. As Quick Ratio of Ytrew Limited and

competitor is 1.6 and 1.5 respectively. At the same time Current ratio is 2.1 and 2.0 of

Ytrew Limited and competitor. Hence, on the basis of the data it can be said that both the

firm are inequitable enough to pay their current liability with the help of their current assets.

Looking at the capital structure of both the company it had been identified that presence of

debt in the capital structure of the company is not that high and it is positive sign for both

the company. Analysis stats that there is 37.5% of debt in capital structure of Ytrew Limited

and 33% in the capital structure of competitor.

c)

Above presented data and Income statement of both the company had helped in

understanding the operating profit possition of competitor is way better than Ytrew Limited

in general. As operating profit of Ytrew Limited is 268500, at the same time operating profit

of competitor is 2858988. Reason behind difference in the both is the amount of sales done

by both the organization. As total sales or revenue of Ytrew is just 2685000 as compare to

that of competitor whose sales is 25990800.

Further analysing the data has helped in understanding that cost of good production is same

for both the firm as ratio of Net sales and Cost of Good sold for both the firm is

1.282051282. Looking at ratio between Net sales and operating expenses it has been

identified that Ytrew Limited is having better position. As indirect expenses incurred by

Ytrew limited on every unit sold is just 8.34 whereas its competitor is incurring $9.1

indirect expenses on every unit sold. Hence, it has been recommended to management of

Ytrew Limited that they have to concentrate more on improving the sales of company to

enhance the operating profit of the company.

d)

Particular Ytrew Limited Competitor

Net Profit Margin 5.4 5.4

Asset Turnover Ratio 2.5 2.2

Financial Leverage 1.6 1.5

Return on Equity 21.5 17.6

Looking at the Du point Decomposition of return of equity of both the company, it had been

understood that Ytrew Limited is having better Return on equity as compare to Competitor. As

Return on Equity of Ytrew Limited is 21.5 whereas return on equity of competitor is 17.6 only. One

of the biggest reason which has been identified for the same is that Ytrew Limited is using their

assets more effectively in regard to generating the sales when compare to Competitor in the market.

As Asset turnover ratio of Ytrew Limited is 2.5 whereas competitor Asset Turnover ratio is just 2.2.

PART B

a)

Profit when selling price is reduced

c)

Above presented data and Income statement of both the company had helped in

understanding the operating profit possition of competitor is way better than Ytrew Limited

in general. As operating profit of Ytrew Limited is 268500, at the same time operating profit

of competitor is 2858988. Reason behind difference in the both is the amount of sales done

by both the organization. As total sales or revenue of Ytrew is just 2685000 as compare to

that of competitor whose sales is 25990800.

Further analysing the data has helped in understanding that cost of good production is same

for both the firm as ratio of Net sales and Cost of Good sold for both the firm is

1.282051282. Looking at ratio between Net sales and operating expenses it has been

identified that Ytrew Limited is having better position. As indirect expenses incurred by

Ytrew limited on every unit sold is just 8.34 whereas its competitor is incurring $9.1

indirect expenses on every unit sold. Hence, it has been recommended to management of

Ytrew Limited that they have to concentrate more on improving the sales of company to

enhance the operating profit of the company.

d)

Particular Ytrew Limited Competitor

Net Profit Margin 5.4 5.4

Asset Turnover Ratio 2.5 2.2

Financial Leverage 1.6 1.5

Return on Equity 21.5 17.6

Looking at the Du point Decomposition of return of equity of both the company, it had been

understood that Ytrew Limited is having better Return on equity as compare to Competitor. As

Return on Equity of Ytrew Limited is 21.5 whereas return on equity of competitor is 17.6 only. One

of the biggest reason which has been identified for the same is that Ytrew Limited is using their

assets more effectively in regard to generating the sales when compare to Competitor in the market.

As Asset turnover ratio of Ytrew Limited is 2.5 whereas competitor Asset Turnover ratio is just 2.2.

PART B

a)

Profit when selling price is reduced

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

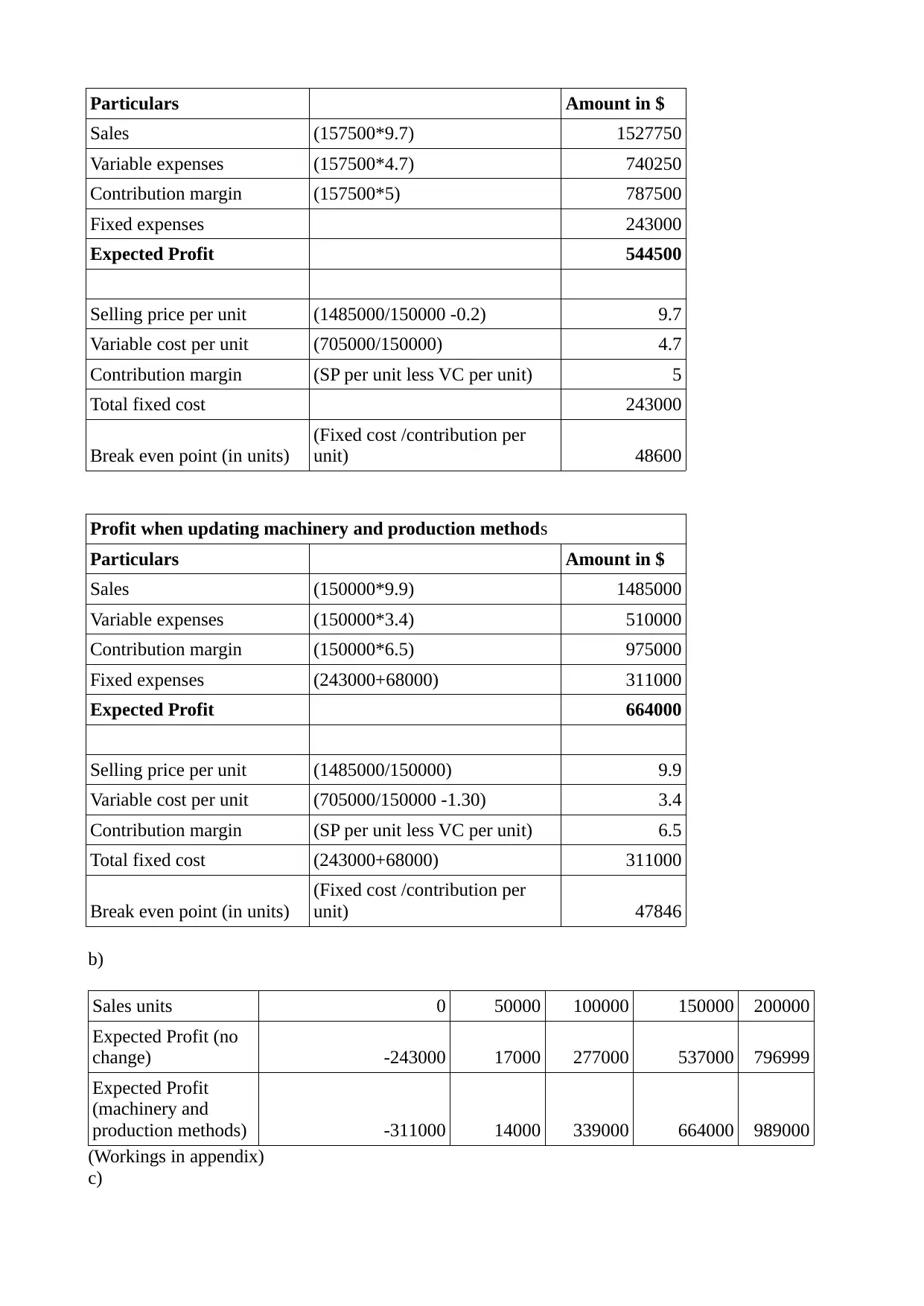

Particulars Amount in $

Sales (157500*9.7) 1527750

Variable expenses (157500*4.7) 740250

Contribution margin (157500*5) 787500

Fixed expenses 243000

Expected Profit 544500

Selling price per unit (1485000/150000 -0.2) 9.7

Variable cost per unit (705000/150000) 4.7

Contribution margin (SP per unit less VC per unit) 5

Total fixed cost 243000

Break even point (in units)

(Fixed cost /contribution per

unit) 48600

Profit when updating machinery and production methods

Particulars Amount in $

Sales (150000*9.9) 1485000

Variable expenses (150000*3.4) 510000

Contribution margin (150000*6.5) 975000

Fixed expenses (243000+68000) 311000

Expected Profit 664000

Selling price per unit (1485000/150000) 9.9

Variable cost per unit (705000/150000 -1.30) 3.4

Contribution margin (SP per unit less VC per unit) 6.5

Total fixed cost (243000+68000) 311000

Break even point (in units)

(Fixed cost /contribution per

unit) 47846

b)

Sales units 0 50000 100000 150000 200000

Expected Profit (no

change) -243000 17000 277000 537000 796999

Expected Profit

(machinery and

production methods) -311000 14000 339000 664000 989000

(Workings in appendix)

c)

Sales (157500*9.7) 1527750

Variable expenses (157500*4.7) 740250

Contribution margin (157500*5) 787500

Fixed expenses 243000

Expected Profit 544500

Selling price per unit (1485000/150000 -0.2) 9.7

Variable cost per unit (705000/150000) 4.7

Contribution margin (SP per unit less VC per unit) 5

Total fixed cost 243000

Break even point (in units)

(Fixed cost /contribution per

unit) 48600

Profit when updating machinery and production methods

Particulars Amount in $

Sales (150000*9.9) 1485000

Variable expenses (150000*3.4) 510000

Contribution margin (150000*6.5) 975000

Fixed expenses (243000+68000) 311000

Expected Profit 664000

Selling price per unit (1485000/150000) 9.9

Variable cost per unit (705000/150000 -1.30) 3.4

Contribution margin (SP per unit less VC per unit) 6.5

Total fixed cost (243000+68000) 311000

Break even point (in units)

(Fixed cost /contribution per

unit) 47846

b)

Sales units 0 50000 100000 150000 200000

Expected Profit (no

change) -243000 17000 277000 537000 796999

Expected Profit

(machinery and

production methods) -311000 14000 339000 664000 989000

(Workings in appendix)

c)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

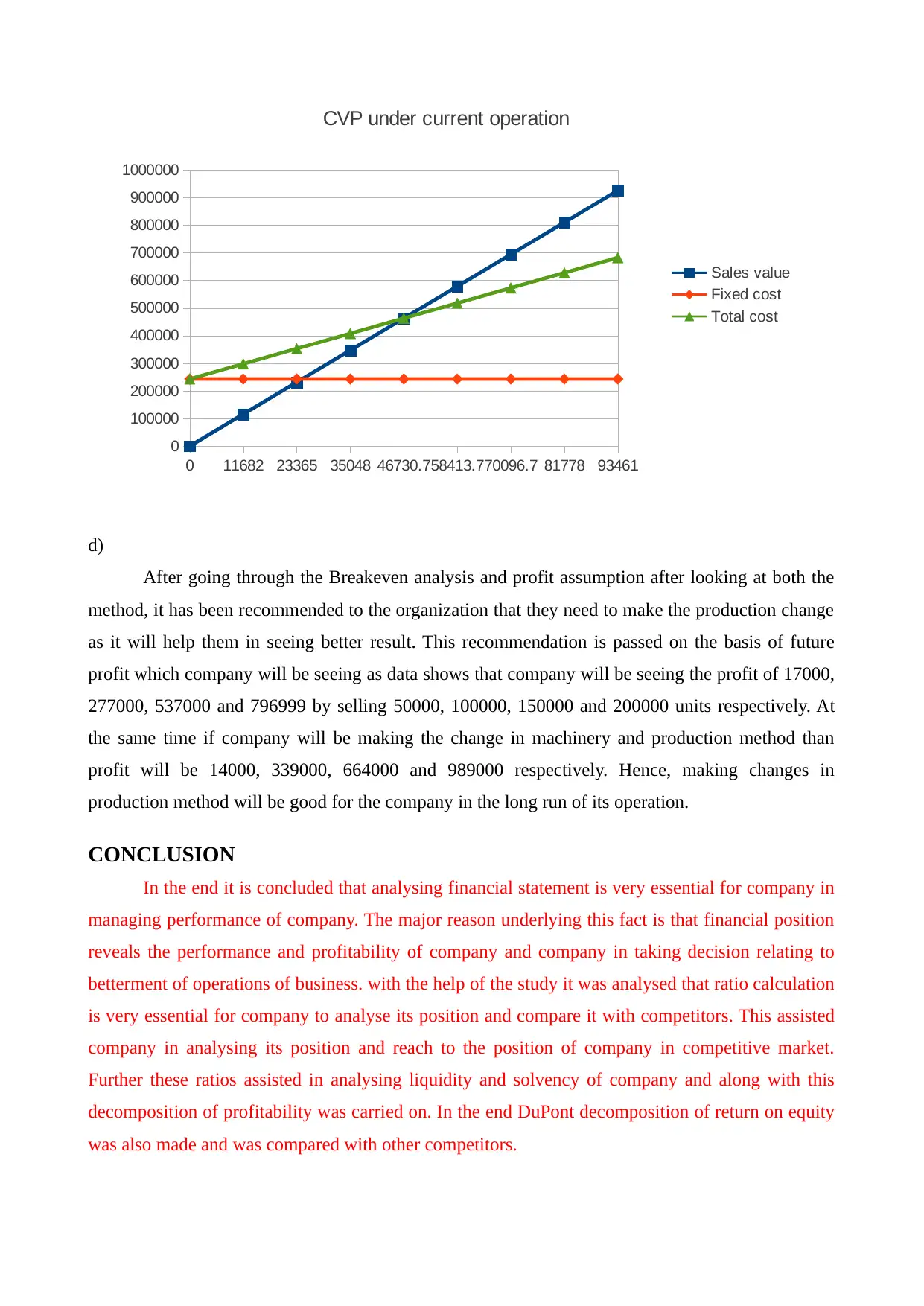

0 11682 23365 35048 46730.758413.770096.7 81778 93461

0

100000

200000

300000

400000

500000

600000

700000

800000

900000

1000000

CVP under current operation

Sales value

Fixed cost

Total cost

d)

After going through the Breakeven analysis and profit assumption after looking at both the

method, it has been recommended to the organization that they need to make the production change

as it will help them in seeing better result. This recommendation is passed on the basis of future

profit which company will be seeing as data shows that company will be seeing the profit of 17000,

277000, 537000 and 796999 by selling 50000, 100000, 150000 and 200000 units respectively. At

the same time if company will be making the change in machinery and production method than

profit will be 14000, 339000, 664000 and 989000 respectively. Hence, making changes in

production method will be good for the company in the long run of its operation.

CONCLUSION

In the end it is concluded that analysing financial statement is very essential for company in

managing performance of company. The major reason underlying this fact is that financial position

reveals the performance and profitability of company and company in taking decision relating to

betterment of operations of business. with the help of the study it was analysed that ratio calculation

is very essential for company to analyse its position and compare it with competitors. This assisted

company in analysing its position and reach to the position of company in competitive market.

Further these ratios assisted in analysing liquidity and solvency of company and along with this

decomposition of profitability was carried on. In the end DuPont decomposition of return on equity

was also made and was compared with other competitors.

0

100000

200000

300000

400000

500000

600000

700000

800000

900000

1000000

CVP under current operation

Sales value

Fixed cost

Total cost

d)

After going through the Breakeven analysis and profit assumption after looking at both the

method, it has been recommended to the organization that they need to make the production change

as it will help them in seeing better result. This recommendation is passed on the basis of future

profit which company will be seeing as data shows that company will be seeing the profit of 17000,

277000, 537000 and 796999 by selling 50000, 100000, 150000 and 200000 units respectively. At

the same time if company will be making the change in machinery and production method than

profit will be 14000, 339000, 664000 and 989000 respectively. Hence, making changes in

production method will be good for the company in the long run of its operation.

CONCLUSION

In the end it is concluded that analysing financial statement is very essential for company in

managing performance of company. The major reason underlying this fact is that financial position

reveals the performance and profitability of company and company in taking decision relating to

betterment of operations of business. with the help of the study it was analysed that ratio calculation

is very essential for company to analyse its position and compare it with competitors. This assisted

company in analysing its position and reach to the position of company in competitive market.

Further these ratios assisted in analysing liquidity and solvency of company and along with this

decomposition of profitability was carried on. In the end DuPont decomposition of return on equity

was also made and was compared with other competitors.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

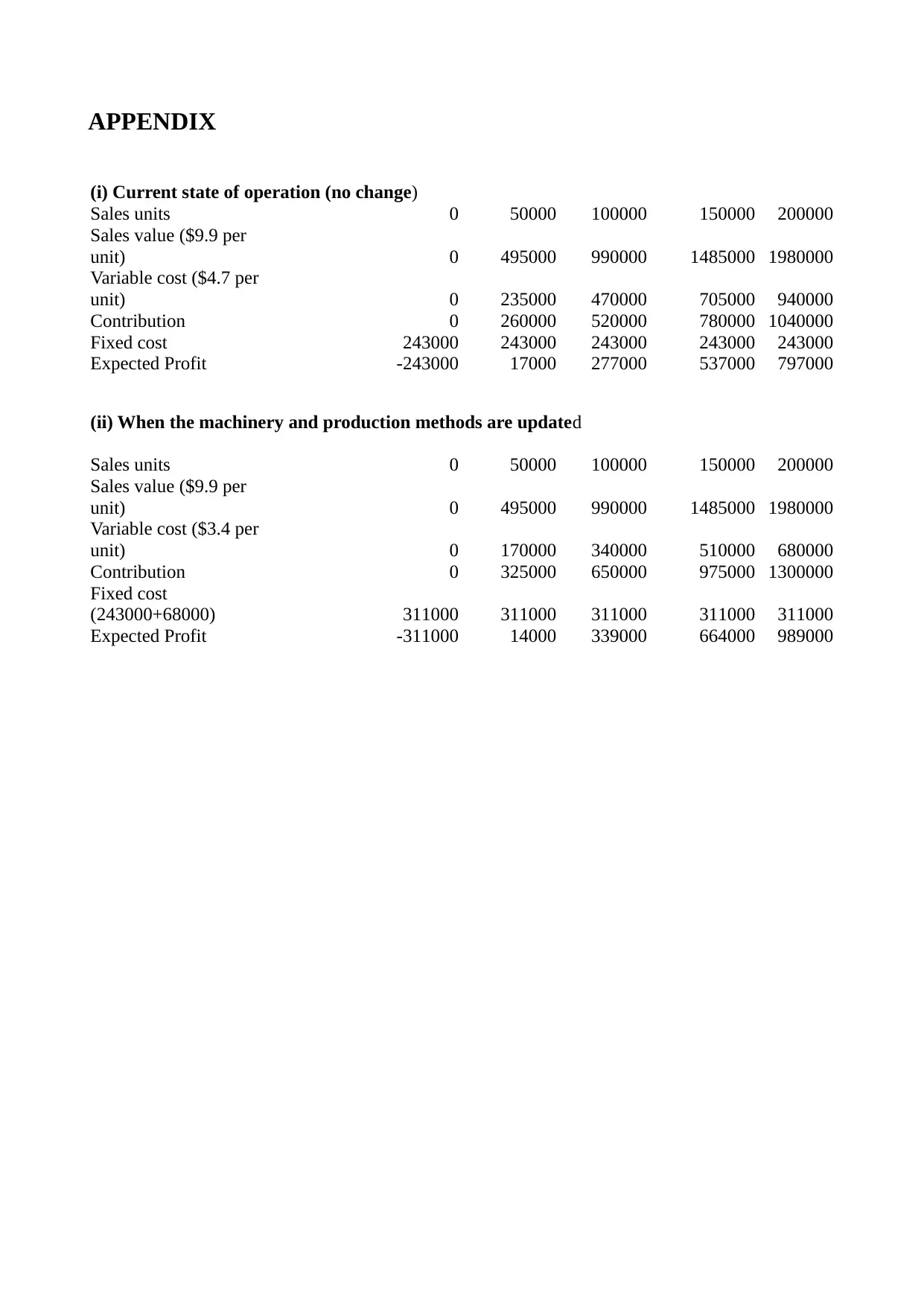

APPENDIX

(i) Current state of operation (no change)

Sales units 0 50000 100000 150000 200000

Sales value ($9.9 per

unit) 0 495000 990000 1485000 1980000

Variable cost ($4.7 per

unit) 0 235000 470000 705000 940000

Contribution 0 260000 520000 780000 1040000

Fixed cost 243000 243000 243000 243000 243000

Expected Profit -243000 17000 277000 537000 797000

(ii) When the machinery and production methods are updated

Sales units 0 50000 100000 150000 200000

Sales value ($9.9 per

unit) 0 495000 990000 1485000 1980000

Variable cost ($3.4 per

unit) 0 170000 340000 510000 680000

Contribution 0 325000 650000 975000 1300000

Fixed cost

(243000+68000) 311000 311000 311000 311000 311000

Expected Profit -311000 14000 339000 664000 989000

(i) Current state of operation (no change)

Sales units 0 50000 100000 150000 200000

Sales value ($9.9 per

unit) 0 495000 990000 1485000 1980000

Variable cost ($4.7 per

unit) 0 235000 470000 705000 940000

Contribution 0 260000 520000 780000 1040000

Fixed cost 243000 243000 243000 243000 243000

Expected Profit -243000 17000 277000 537000 797000

(ii) When the machinery and production methods are updated

Sales units 0 50000 100000 150000 200000

Sales value ($9.9 per

unit) 0 495000 990000 1485000 1980000

Variable cost ($3.4 per

unit) 0 170000 340000 510000 680000

Contribution 0 325000 650000 975000 1300000

Fixed cost

(243000+68000) 311000 311000 311000 311000 311000

Expected Profit -311000 14000 339000 664000 989000

1 out of 11