Analysis of Average Hourly Earnings and Housing Trends

VerifiedAdded on 2020/03/16

|35

|4832

|44

AI Summary

This assignment delves into the analysis of average hourly earnings, investigating factors like age, gender, and education level to determine their influence on earnings. The report also examines housing trends in Sydney, Australia, focusing on interest rates, principal amounts, and year-over-year changes. Additionally, it explores the portfolio ratio as a key metric for financial analysis.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: DATA ANALYSIS OF ECONOMETRICS

Data Analysis of Econometrics

Name of the University:

Name of the Student:

Author’s Note:

Data Analysis of Econometrics

Name of the University:

Name of the Student:

Author’s Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

DATA ANALYSIS OF ECONOMETRICS 1

Executive Summary:

The report describes economic skills with the help of regression analysis. We answered three

questions and their subparts. We have provided the necessary calculations and tables. We

interpreted from the analysis with the help of MS Office, Minitab and R. We finally have

drawn the conclusions from each question.

Executive Summary:

The report describes economic skills with the help of regression analysis. We answered three

questions and their subparts. We have provided the necessary calculations and tables. We

interpreted from the analysis with the help of MS Office, Minitab and R. We finally have

drawn the conclusions from each question.

DATA ANALYSIS OF ECONOMETRICS 2

Table of Contents

Introduction:...............................................................................................................................3

Questions and Answers:.............................................................................................................3

Question A.............................................................................................................................3

Question B..............................................................................................................................6

Question C............................................................................................................................23

Conclusion:..............................................................................................................................29

Bibliography List:....................................................................................................................30

Table of Contents

Introduction:...............................................................................................................................3

Questions and Answers:.............................................................................................................3

Question A.............................................................................................................................3

Question B..............................................................................................................................6

Question C............................................................................................................................23

Conclusion:..............................................................................................................................29

Bibliography List:....................................................................................................................30

DATA ANALYSIS OF ECONOMETRICS 3

Introduction:

We described here the group-survey of Australian data of different cities. The answers

of three questions are provided in the analysis. We derived the comparative study of different

Australian cities in the first part. In the second part, we calculated the analysis of economic

situation and relation of chosen three sectors. In the third part, we analyzed the data of age,

average hourly earnings and different factors.

We have elaborately analyzed the dataset with the help of MS Office, Minitab and R.

We installed add-ins in MS excel for advance analysis (Slazek et al. 2013). The report would

help the economic investigators of Australia.

Data analysis on econometrics in this report shows the overview of three different

segments of economics in this report.

Questions and Answers:

Question A (Australian House Price Index):

A1.

Introduction:

We described here the group-survey of Australian data of different cities. The answers

of three questions are provided in the analysis. We derived the comparative study of different

Australian cities in the first part. In the second part, we calculated the analysis of economic

situation and relation of chosen three sectors. In the third part, we analyzed the data of age,

average hourly earnings and different factors.

We have elaborately analyzed the dataset with the help of MS Office, Minitab and R.

We installed add-ins in MS excel for advance analysis (Slazek et al. 2013). The report would

help the economic investigators of Australia.

Data analysis on econometrics in this report shows the overview of three different

segments of economics in this report.

Questions and Answers:

Question A (Australian House Price Index):

A1.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

DATA ANALYSIS OF ECONOMETRICS 4

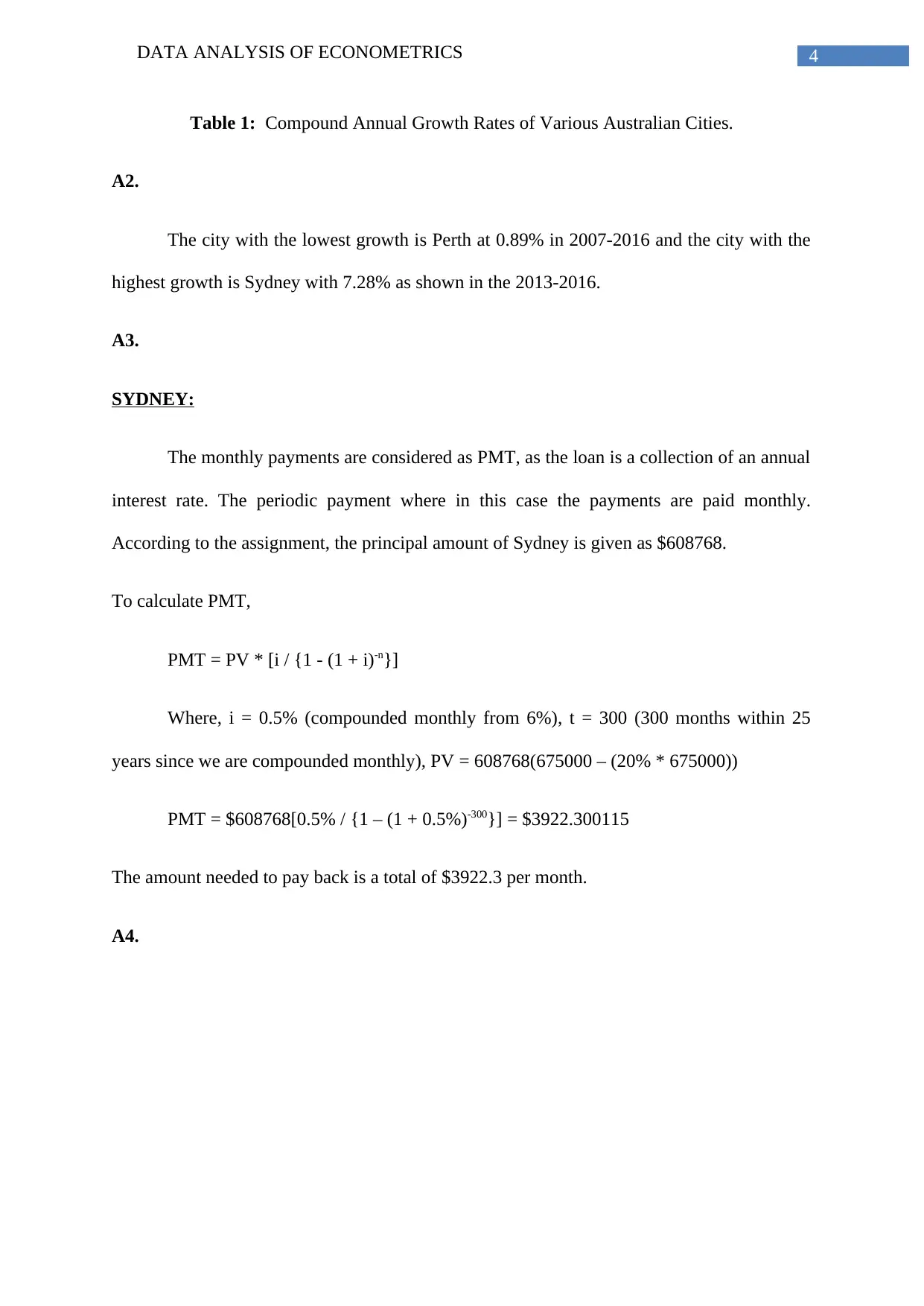

Table 1: Compound Annual Growth Rates of Various Australian Cities.

A2.

The city with the lowest growth is Perth at 0.89% in 2007-2016 and the city with the

highest growth is Sydney with 7.28% as shown in the 2013-2016.

A3.

SYDNEY:

The monthly payments are considered as PMT, as the loan is a collection of an annual

interest rate. The periodic payment where in this case the payments are paid monthly.

According to the assignment, the principal amount of Sydney is given as $608768.

To calculate PMT,

PMT = PV * [i / {1 - (1 + i)-n}]

Where, i = 0.5% (compounded monthly from 6%), t = 300 (300 months within 25

years since we are compounded monthly), PV = 608768(675000 – (20% * 675000))

PMT = $608768[0.5% / {1 – (1 + 0.5%)-300}] = $3922.300115

The amount needed to pay back is a total of $3922.3 per month.

A4.

Table 1: Compound Annual Growth Rates of Various Australian Cities.

A2.

The city with the lowest growth is Perth at 0.89% in 2007-2016 and the city with the

highest growth is Sydney with 7.28% as shown in the 2013-2016.

A3.

SYDNEY:

The monthly payments are considered as PMT, as the loan is a collection of an annual

interest rate. The periodic payment where in this case the payments are paid monthly.

According to the assignment, the principal amount of Sydney is given as $608768.

To calculate PMT,

PMT = PV * [i / {1 - (1 + i)-n}]

Where, i = 0.5% (compounded monthly from 6%), t = 300 (300 months within 25

years since we are compounded monthly), PV = 608768(675000 – (20% * 675000))

PMT = $608768[0.5% / {1 – (1 + 0.5%)-300}] = $3922.300115

The amount needed to pay back is a total of $3922.3 per month.

A4.

DATA ANALYSIS OF ECONOMETRICS 5

1

3

5

7

9

11

13

15

17

19

21

23

25

27

29

31

33

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Principal Amount

Interest Amount of SYDNEY

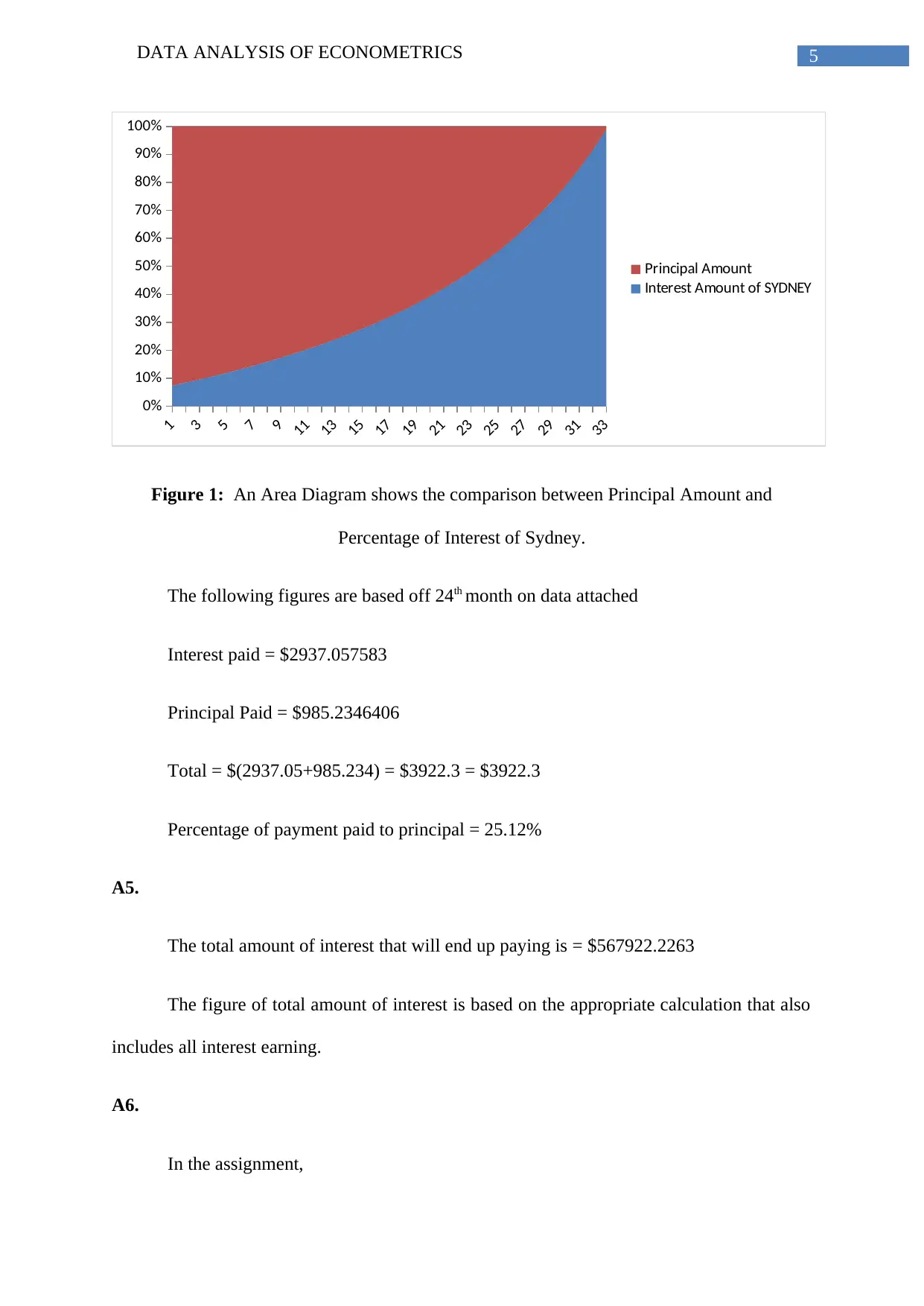

Figure 1: An Area Diagram shows the comparison between Principal Amount and

Percentage of Interest of Sydney.

The following figures are based off 24th month on data attached

Interest paid = $2937.057583

Principal Paid = $985.2346406

Total = $(2937.05+985.234) = $3922.3 = $3922.3

Percentage of payment paid to principal = 25.12%

A5.

The total amount of interest that will end up paying is = $567922.2263

The figure of total amount of interest is based on the appropriate calculation that also

includes all interest earning.

A6.

In the assignment,

1

3

5

7

9

11

13

15

17

19

21

23

25

27

29

31

33

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Principal Amount

Interest Amount of SYDNEY

Figure 1: An Area Diagram shows the comparison between Principal Amount and

Percentage of Interest of Sydney.

The following figures are based off 24th month on data attached

Interest paid = $2937.057583

Principal Paid = $985.2346406

Total = $(2937.05+985.234) = $3922.3 = $3922.3

Percentage of payment paid to principal = 25.12%

A5.

The total amount of interest that will end up paying is = $567922.2263

The figure of total amount of interest is based on the appropriate calculation that also

includes all interest earning.

A6.

In the assignment,

DATA ANALYSIS OF ECONOMETRICS 6

Sydney House Price: $675000

CAGR: 5.05%

Year 25: FV = Current Value*(1+r) n = 675000(1+5.05%) 25 = $2314128.793

House Appreciation = Future Value of House Price – Current Value of House Price

= 2314128.793 – 675000 = $1639128.793

As, $1639128.793 > $567922.2263; Therefore, we can say that, House Appreciation

> Total Interest Paid.

From our above calculation, we can conclude that the value of the house is greater

than the interest paid thus the value appreciation is sufficient to cover the total interest paid.

Question B.

The three chosen securities are industrial in Mix. And Fix., consumer services in

travel and tourism and healthcare providers. The value of ri in the industrial, consumer

services and Healthcare services are calculated separately.

B1.

A. Orthogonal Least Square (OLS) model of Adelaide Brighton (Market Value and

Stock Value):

Sydney House Price: $675000

CAGR: 5.05%

Year 25: FV = Current Value*(1+r) n = 675000(1+5.05%) 25 = $2314128.793

House Appreciation = Future Value of House Price – Current Value of House Price

= 2314128.793 – 675000 = $1639128.793

As, $1639128.793 > $567922.2263; Therefore, we can say that, House Appreciation

> Total Interest Paid.

From our above calculation, we can conclude that the value of the house is greater

than the interest paid thus the value appreciation is sufficient to cover the total interest paid.

Question B.

The three chosen securities are industrial in Mix. And Fix., consumer services in

travel and tourism and healthcare providers. The value of ri in the industrial, consumer

services and Healthcare services are calculated separately.

B1.

A. Orthogonal Least Square (OLS) model of Adelaide Brighton (Market Value and

Stock Value):

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DATA ANALYSIS OF ECONOMETRICS 7

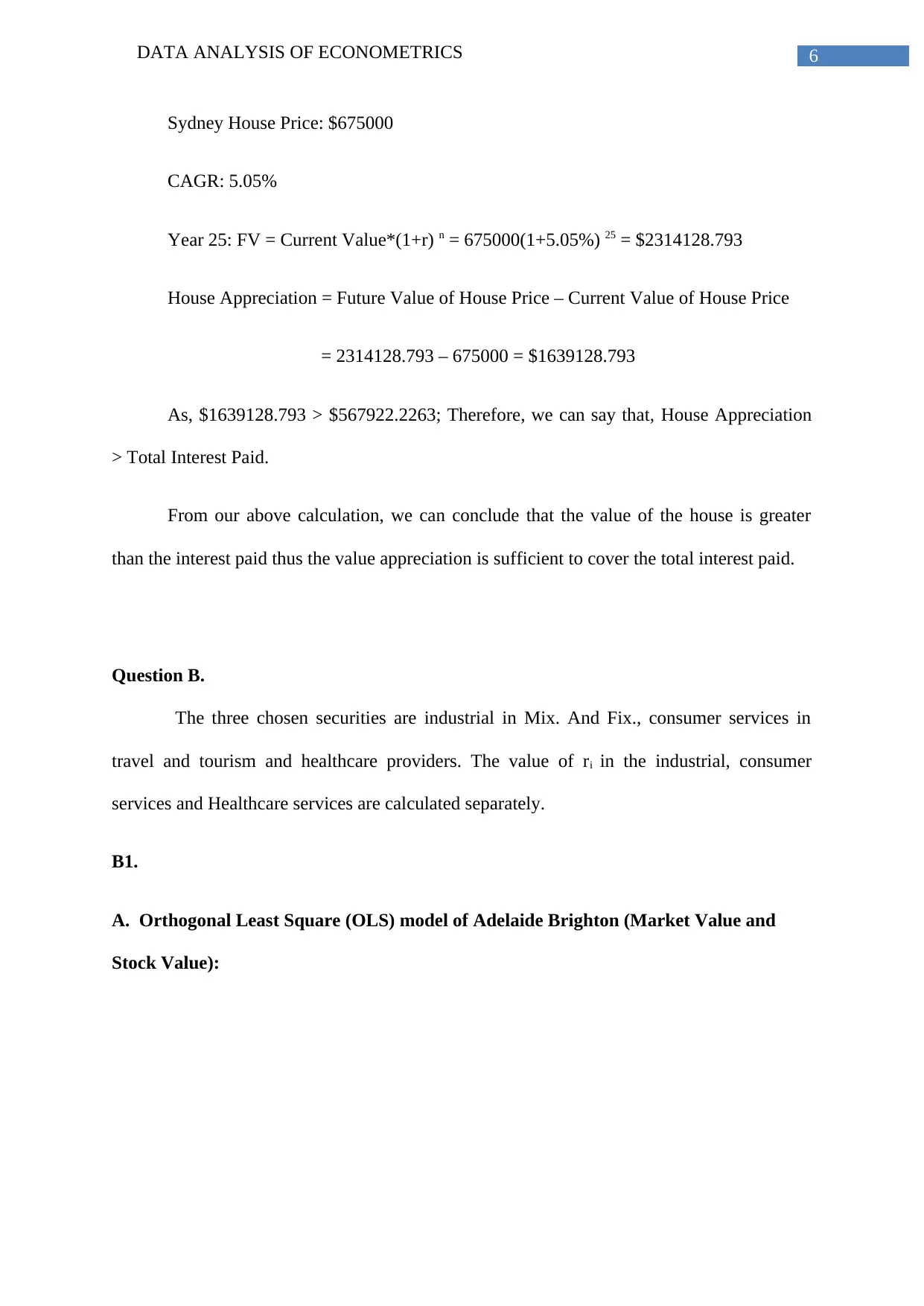

Table 2: Orthogonal Least Square regression model of Adelaide Brighton

-0.06 -0.04 -0.02 0 0.02 0.04 0.06 0.08 0.1

-2

-1.5

-1

-0.5

0

0.5

1

1.5

Adelaide Brighton Residual Plot

Residuals

Figure 2: Residual Plot of Adelaide Brighton

Table 2: Orthogonal Least Square regression model of Adelaide Brighton

-0.06 -0.04 -0.02 0 0.02 0.04 0.06 0.08 0.1

-2

-1.5

-1

-0.5

0

0.5

1

1.5

Adelaide Brighton Residual Plot

Residuals

Figure 2: Residual Plot of Adelaide Brighton

DATA ANALYSIS OF ECONOMETRICS 8

0.005617978 0.024657534 0 0.005847953 0.033268102 0.014035088

0

1

2

3

4

5

6

7

Adelaide Brighton Line Fit Plot

Y

Predicted Y

Adelaide Brighton Prediction value

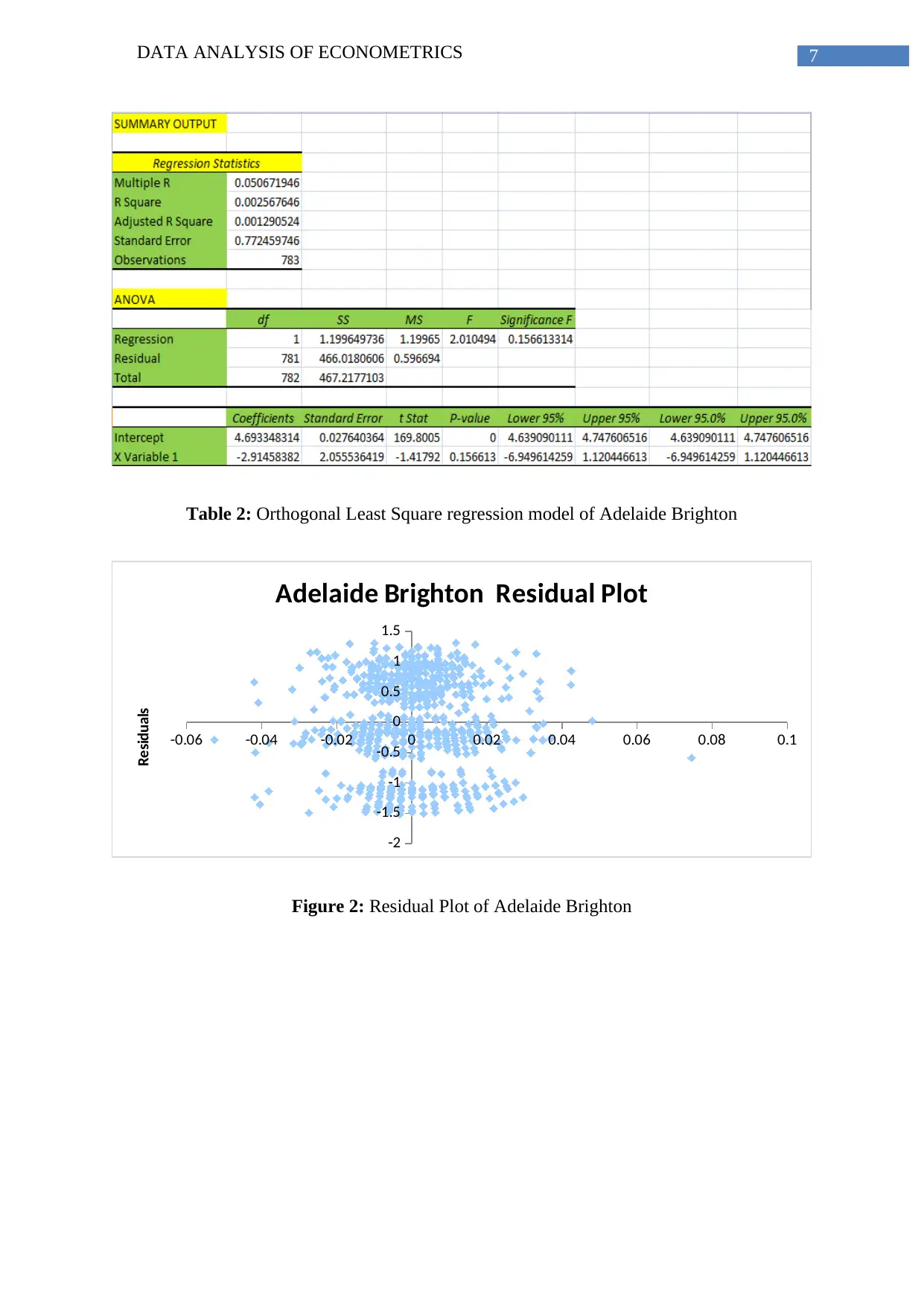

Y

Figure 3: Fitted residual line plot of Adelaide Brighton

B. Orthogonal Least Square (OLS) model of WEBJET (Market Value and Stock

Value):

Table 3: Orthogonal Least Square regression model of WEBJET

0.005617978 0.024657534 0 0.005847953 0.033268102 0.014035088

0

1

2

3

4

5

6

7

Adelaide Brighton Line Fit Plot

Y

Predicted Y

Adelaide Brighton Prediction value

Y

Figure 3: Fitted residual line plot of Adelaide Brighton

B. Orthogonal Least Square (OLS) model of WEBJET (Market Value and Stock

Value):

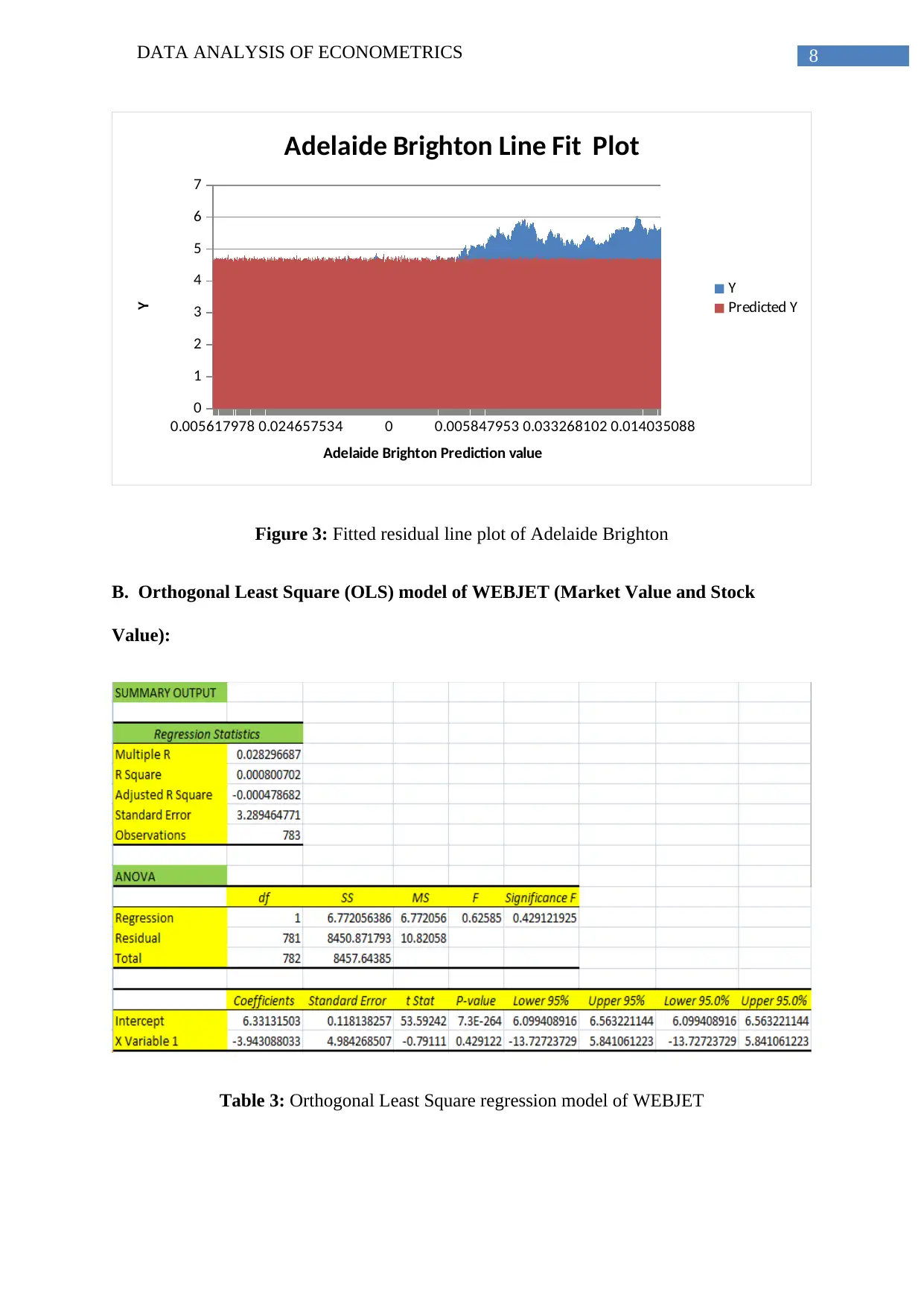

Table 3: Orthogonal Least Square regression model of WEBJET

DATA ANALYSIS OF ECONOMETRICS 9

-0.15 -0.1 -0.05 0 0.05 0.1 0.15 0.2 0.25

-6

-4

-2

0

2

4

6

8

WEBJET Residual Plot

WEBJET Value

Residuals

Figure 4: Residual Plot of WEBJET

-0.024303985 0 0.019935154-0.018556895 0.01187447 -0.007880911

0

2

4

6

8

10

12

14

WEBJET Line Fit Plot

Y

Predicted Y

WEBJET predicted Value

Y

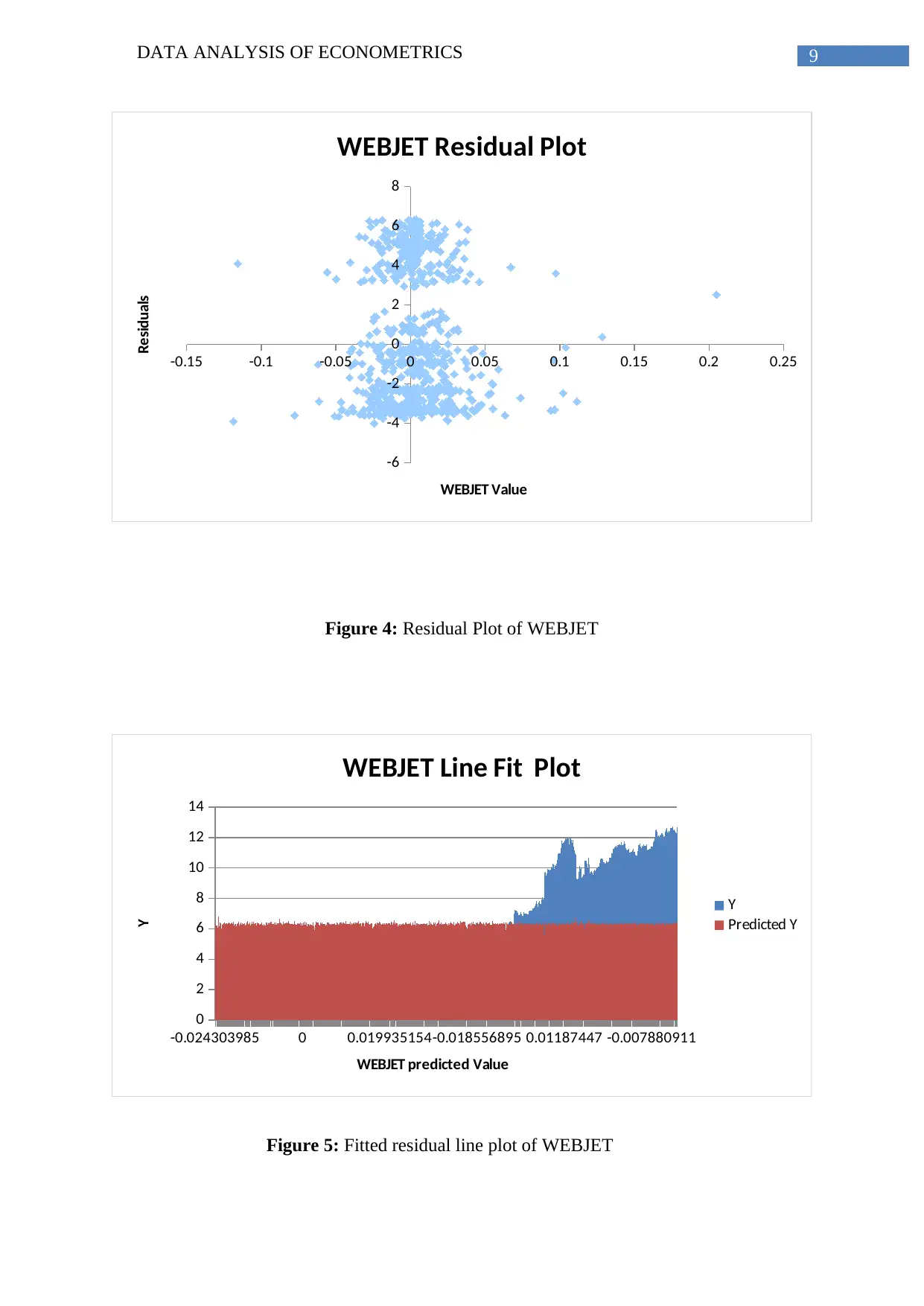

Figure 5: Fitted residual line plot of WEBJET

-0.15 -0.1 -0.05 0 0.05 0.1 0.15 0.2 0.25

-6

-4

-2

0

2

4

6

8

WEBJET Residual Plot

WEBJET Value

Residuals

Figure 4: Residual Plot of WEBJET

-0.024303985 0 0.019935154-0.018556895 0.01187447 -0.007880911

0

2

4

6

8

10

12

14

WEBJET Line Fit Plot

Y

Predicted Y

WEBJET predicted Value

Y

Figure 5: Fitted residual line plot of WEBJET

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

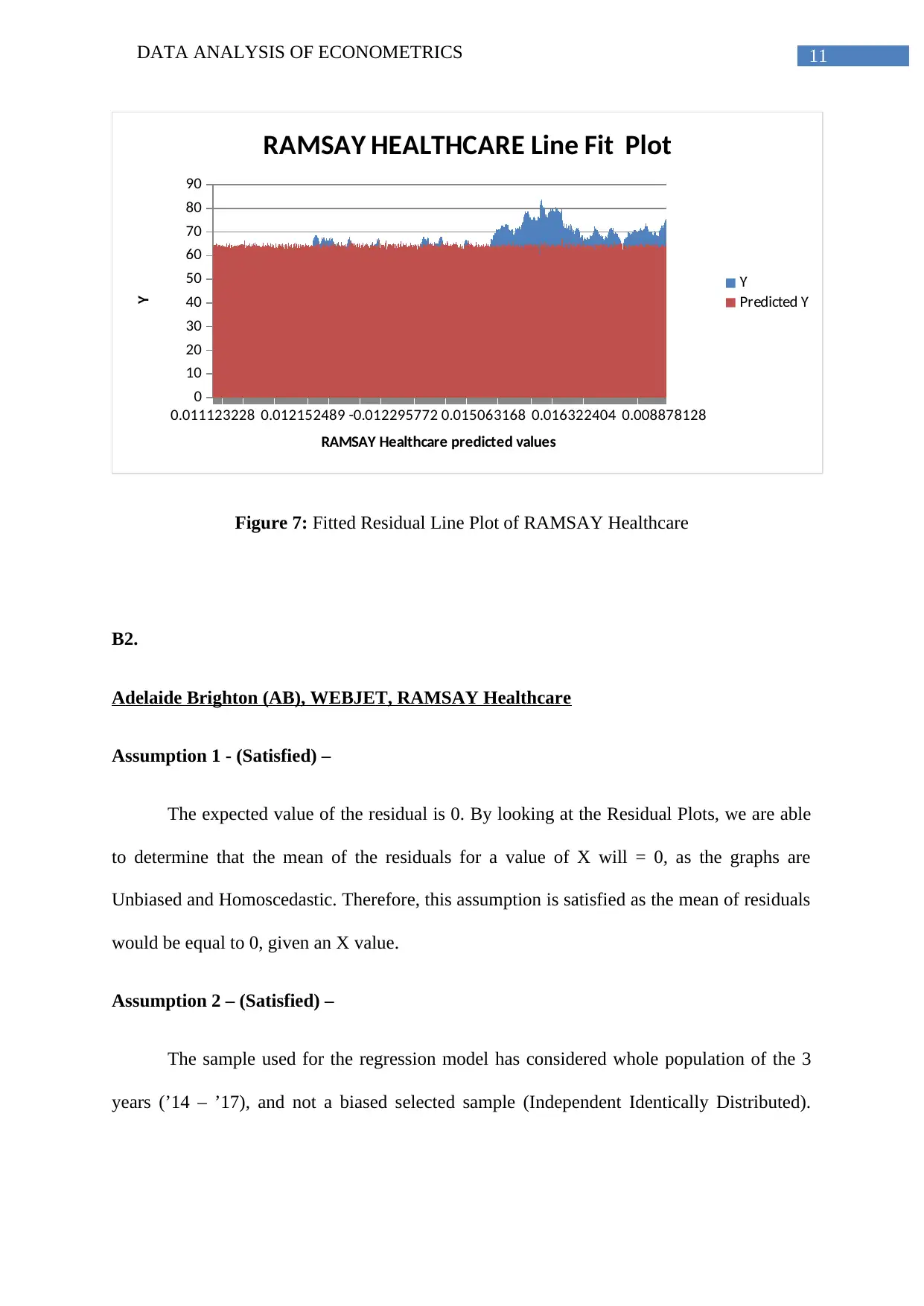

DATA ANALYSIS OF ECONOMETRICS 10

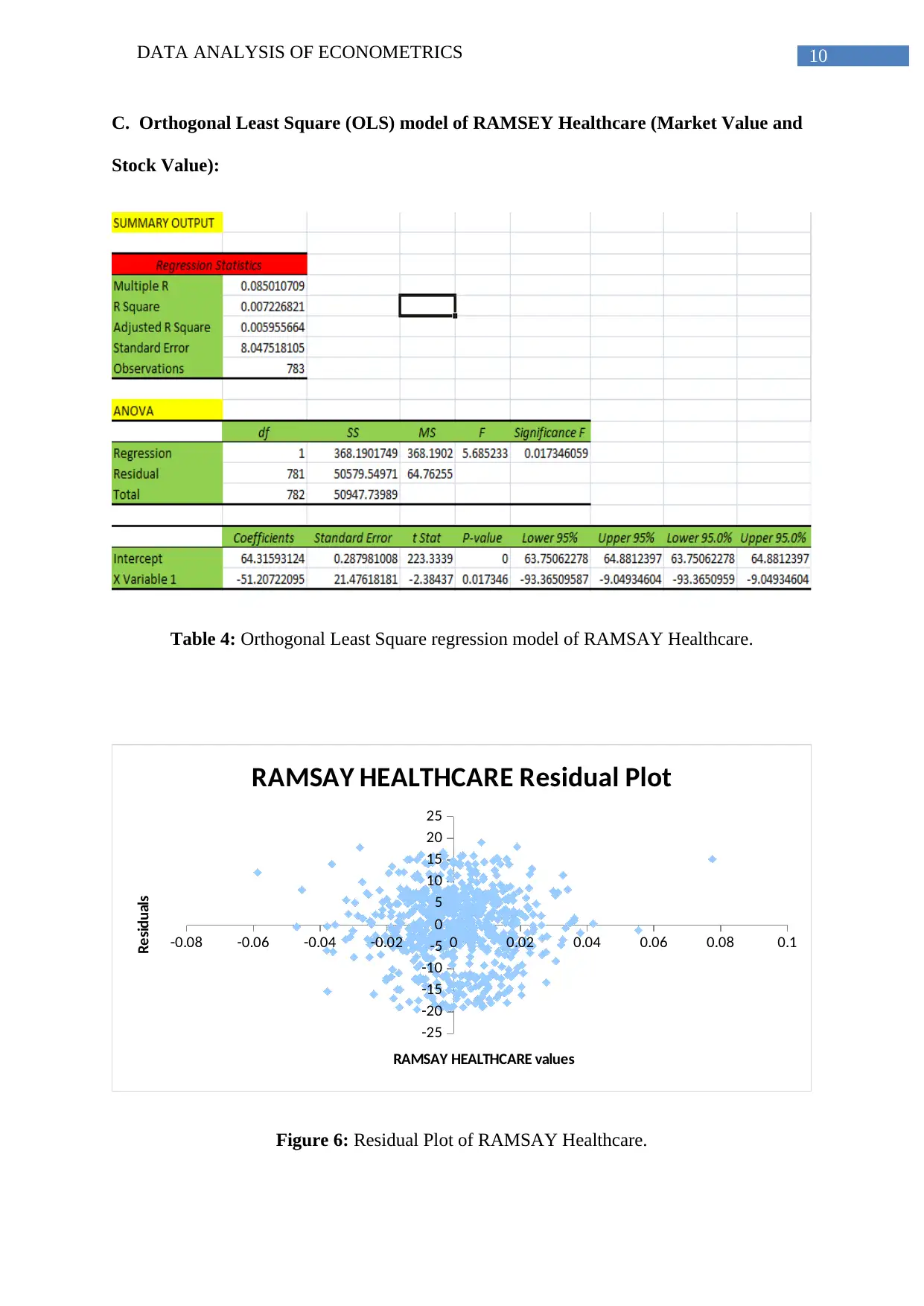

C. Orthogonal Least Square (OLS) model of RAMSEY Healthcare (Market Value and

Stock Value):

Table 4: Orthogonal Least Square regression model of RAMSAY Healthcare.

-0.08 -0.06 -0.04 -0.02 0 0.02 0.04 0.06 0.08 0.1

-25

-20

-15

-10

-5

0

5

10

15

20

25

RAMSAY HEALTHCARE Residual Plot

RAMSAY HEALTHCARE values

Residuals

Figure 6: Residual Plot of RAMSAY Healthcare.

C. Orthogonal Least Square (OLS) model of RAMSEY Healthcare (Market Value and

Stock Value):

Table 4: Orthogonal Least Square regression model of RAMSAY Healthcare.

-0.08 -0.06 -0.04 -0.02 0 0.02 0.04 0.06 0.08 0.1

-25

-20

-15

-10

-5

0

5

10

15

20

25

RAMSAY HEALTHCARE Residual Plot

RAMSAY HEALTHCARE values

Residuals

Figure 6: Residual Plot of RAMSAY Healthcare.

DATA ANALYSIS OF ECONOMETRICS 11

0.011123228 0.012152489 -0.012295772 0.015063168 0.016322404 0.008878128

0

10

20

30

40

50

60

70

80

90

RAMSAY HEALTHCARE Line Fit Plot

Y

Predicted Y

RAMSAY Healthcare predicted values

Y

Figure 7: Fitted Residual Line Plot of RAMSAY Healthcare

B2.

Adelaide Brighton (AB), WEBJET, RAMSAY Healthcare

Assumption 1 - (Satisfied) –

The expected value of the residual is 0. By looking at the Residual Plots, we are able

to determine that the mean of the residuals for a value of X will = 0, as the graphs are

Unbiased and Homoscedastic. Therefore, this assumption is satisfied as the mean of residuals

would be equal to 0, given an X value.

Assumption 2 – (Satisfied) –

The sample used for the regression model has considered whole population of the 3

years (’14 – ’17), and not a biased selected sample (Independent Identically Distributed).

0.011123228 0.012152489 -0.012295772 0.015063168 0.016322404 0.008878128

0

10

20

30

40

50

60

70

80

90

RAMSAY HEALTHCARE Line Fit Plot

Y

Predicted Y

RAMSAY Healthcare predicted values

Y

Figure 7: Fitted Residual Line Plot of RAMSAY Healthcare

B2.

Adelaide Brighton (AB), WEBJET, RAMSAY Healthcare

Assumption 1 - (Satisfied) –

The expected value of the residual is 0. By looking at the Residual Plots, we are able

to determine that the mean of the residuals for a value of X will = 0, as the graphs are

Unbiased and Homoscedastic. Therefore, this assumption is satisfied as the mean of residuals

would be equal to 0, given an X value.

Assumption 2 – (Satisfied) –

The sample used for the regression model has considered whole population of the 3

years (’14 – ’17), and not a biased selected sample (Independent Identically Distributed).

DATA ANALYSIS OF ECONOMETRICS 12

Further, as each daily return does not affect any other daily returns, they are independent to

each other. Therefore, this assumption is satisfied as the selected data is IID.

Assumption 3 – (Satisfied) –

It can be determined that there are no outliers, which can be determined by inspecting

the line fit plot. Since, there are no outliers which can be determined by inspecting the line fit

plot, since there are no outliers it can be concluded in a meaningless value of an estimated

“Beta 1”, in which this assumption is satisfied.

Assumption 4 – (Satisfied) –

The error term has a zero-conditional mean. In other words, each stock OLS specifies

each linear model such that there are no omitted variables.

Assumption 5 – (Satisfied) –

The error term (e) is constant across all stocks. They all remain with the same

variance and are not correlated with each other in anyway. This is known to be in a state of

homoscedasticity.

B3.

Beta Values

The beta values are calculated from the coefficient of the ASX 200 market return

independent variable from the regression. The three estimated betas (slopes) from three

stocks are respectively (-2.92) (industrial), (-3.94) (consumer services), (-51.07) (healthcare

providers).

The betas do not line as our expectation. The reason is that the market and stock

factors are not properly linearly related.

Further, as each daily return does not affect any other daily returns, they are independent to

each other. Therefore, this assumption is satisfied as the selected data is IID.

Assumption 3 – (Satisfied) –

It can be determined that there are no outliers, which can be determined by inspecting

the line fit plot. Since, there are no outliers which can be determined by inspecting the line fit

plot, since there are no outliers it can be concluded in a meaningless value of an estimated

“Beta 1”, in which this assumption is satisfied.

Assumption 4 – (Satisfied) –

The error term has a zero-conditional mean. In other words, each stock OLS specifies

each linear model such that there are no omitted variables.

Assumption 5 – (Satisfied) –

The error term (e) is constant across all stocks. They all remain with the same

variance and are not correlated with each other in anyway. This is known to be in a state of

homoscedasticity.

B3.

Beta Values

The beta values are calculated from the coefficient of the ASX 200 market return

independent variable from the regression. The three estimated betas (slopes) from three

stocks are respectively (-2.92) (industrial), (-3.94) (consumer services), (-51.07) (healthcare

providers).

The betas do not line as our expectation. The reason is that the market and stock

factors are not properly linearly related.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DATA ANALYSIS OF ECONOMETRICS 13

Adelaide Brighton:

The beta is -2.92. This beta is in line with our expectation for the following reasons:

1. The Adelaide Brighton stock is more volatile than the market and contains higher

risk compared to the other two stocks mainly due to its market capitalization.

2. Adelaide Brighton has a large weighting of close to 9% of the ASX 200 relating to

market capitalization and therefore its performance would be closely correlated to

the ASX 200 performance.

Statistical Significance

H0: β ̂ market=0. If there is a low p-value or high-test statistic (t-stat), then we

reject the null. Here the P-Value is 0.15663 >0.05, which implies that the critical

value does not lie within the rejection region. Therefore, we cannot reject the null

hypothesis. These statistics indicate that the market does have a statistically

significant impact on the returns of Adelaide Brighton.

WEBJET

The Beta of WEBJET is (-3.94).This Beta is in line with our expectations for the

following reasons:

1. WEBJET is a market leader in the Airlines industry. As the demand for Airlines

will be stable it is less volatile than the market, hence has minimal risk. Another

influencing factor in this is that the industry is not as competitive as the other

comparing stocks contributing to the stability of the beta.

Adelaide Brighton:

The beta is -2.92. This beta is in line with our expectation for the following reasons:

1. The Adelaide Brighton stock is more volatile than the market and contains higher

risk compared to the other two stocks mainly due to its market capitalization.

2. Adelaide Brighton has a large weighting of close to 9% of the ASX 200 relating to

market capitalization and therefore its performance would be closely correlated to

the ASX 200 performance.

Statistical Significance

H0: β ̂ market=0. If there is a low p-value or high-test statistic (t-stat), then we

reject the null. Here the P-Value is 0.15663 >0.05, which implies that the critical

value does not lie within the rejection region. Therefore, we cannot reject the null

hypothesis. These statistics indicate that the market does have a statistically

significant impact on the returns of Adelaide Brighton.

WEBJET

The Beta of WEBJET is (-3.94).This Beta is in line with our expectations for the

following reasons:

1. WEBJET is a market leader in the Airlines industry. As the demand for Airlines

will be stable it is less volatile than the market, hence has minimal risk. Another

influencing factor in this is that the industry is not as competitive as the other

comparing stocks contributing to the stability of the beta.

DATA ANALYSIS OF ECONOMETRICS 14

2. Thus, WEBJET’s business will also be stable and more resilient to market shocks.

3. WEBJET is an Australian company and therefore it will still have some

correlation with the market risk and therefore we would not expect a beta close to

0.

Statistical Significance

H0: β ̂ market = 0. If there is a low p-value or high-test statistic (t-stat), then we

reject the null. For WEBJET, the P-Value is 0.429 > 0.05, which implies that the

critical value does not lie within the rejection region. Therefore, we cannot reject

the null hypothesis. These statistics indicate that the market statistically significant

impact on the returns of WEBJET.

RAMSAY Healthcare

The Beta of Ramsay Healthcare is (-51.207). The volatility is minimal and so is

the risk. This is maybe contributed by the industry, which Ramsay Healthcare is in,

where the competition is tolerable.

1. Ramsay Healthcare lies within the pharmaceutical sector where the primary

factor in return is the sales of it’s products. Thus, compared to other stocks in the

ASX200 the volatility is minimal and so is the risk.

2. The primary factor affecting RAMSAY Healthcare's consumption of its

products and public’s view is its services. Therefore, it has higher than the market that

is demonstrated by its beta being > 1.

3. Ramsay Healthcare is an Australian company and therefore it will still have

some correlation with the market risk and therefore we would not expect a beta close

to 0.

2. Thus, WEBJET’s business will also be stable and more resilient to market shocks.

3. WEBJET is an Australian company and therefore it will still have some

correlation with the market risk and therefore we would not expect a beta close to

0.

Statistical Significance

H0: β ̂ market = 0. If there is a low p-value or high-test statistic (t-stat), then we

reject the null. For WEBJET, the P-Value is 0.429 > 0.05, which implies that the

critical value does not lie within the rejection region. Therefore, we cannot reject

the null hypothesis. These statistics indicate that the market statistically significant

impact on the returns of WEBJET.

RAMSAY Healthcare

The Beta of Ramsay Healthcare is (-51.207). The volatility is minimal and so is

the risk. This is maybe contributed by the industry, which Ramsay Healthcare is in,

where the competition is tolerable.

1. Ramsay Healthcare lies within the pharmaceutical sector where the primary

factor in return is the sales of it’s products. Thus, compared to other stocks in the

ASX200 the volatility is minimal and so is the risk.

2. The primary factor affecting RAMSAY Healthcare's consumption of its

products and public’s view is its services. Therefore, it has higher than the market that

is demonstrated by its beta being > 1.

3. Ramsay Healthcare is an Australian company and therefore it will still have

some correlation with the market risk and therefore we would not expect a beta close

to 0.

DATA ANALYSIS OF ECONOMETRICS 15

Statistical Significance

1. H0: β ̂ market=0. If there is a low p-value or high-test statistic (t-stat), then we

reject the null. For Ramsay Industries, the P-Value is 0.0173 < 0.05, which

implies that the critical value does lie within the rejection region. Therefore, we

can reject the null hypothesis. These statistics indicate that the market does have a

statistically significant impact on the returns of Ramsay Industries.

2. All three betas are mostly in line with our expectations due to their characteristics

within the market. However, we expected Ramsay Healthcare’s beta to be closer

to 1 due to the fact that they are market leaders within their industry.

3. Beta is the measure of the stock’s volatility in relation to the market. The market

is considered to have a beta of 1 and stocks are ranked based on how much they

deviate from the market. Stocks with a beta of less than 1 are less volatile than the

market and stocks with a beta of more than 1 are more volatile. Zero beta stocks

have zero correlation with market movements. They are expected to have a low

risk free returns.

Beta Equal to One: The Beta which is the level of risk of the market is considered = 1

and is called "Systematic Risk". If a stock has a Beta = 1, it therefore has the same

risk level as the market. If the market moves by 1 point, the stock should also reflect

this movement by 1 unit.

Beta Equal to Zero: A zero Beta stock implies that is has no "Systematic Risk", and

would be considered a "Risk- Free" rate. Further, this would imply that the return on

this stock will has no correlation with the market. This can be seen through regression

analysis as the coefficient of an independent variable (Beta) would be multiplied by 0,

and therefore would not impact the dependent variable i.e. Return.

Statistical Significance

1. H0: β ̂ market=0. If there is a low p-value or high-test statistic (t-stat), then we

reject the null. For Ramsay Industries, the P-Value is 0.0173 < 0.05, which

implies that the critical value does lie within the rejection region. Therefore, we

can reject the null hypothesis. These statistics indicate that the market does have a

statistically significant impact on the returns of Ramsay Industries.

2. All three betas are mostly in line with our expectations due to their characteristics

within the market. However, we expected Ramsay Healthcare’s beta to be closer

to 1 due to the fact that they are market leaders within their industry.

3. Beta is the measure of the stock’s volatility in relation to the market. The market

is considered to have a beta of 1 and stocks are ranked based on how much they

deviate from the market. Stocks with a beta of less than 1 are less volatile than the

market and stocks with a beta of more than 1 are more volatile. Zero beta stocks

have zero correlation with market movements. They are expected to have a low

risk free returns.

Beta Equal to One: The Beta which is the level of risk of the market is considered = 1

and is called "Systematic Risk". If a stock has a Beta = 1, it therefore has the same

risk level as the market. If the market moves by 1 point, the stock should also reflect

this movement by 1 unit.

Beta Equal to Zero: A zero Beta stock implies that is has no "Systematic Risk", and

would be considered a "Risk- Free" rate. Further, this would imply that the return on

this stock will has no correlation with the market. This can be seen through regression

analysis as the coefficient of an independent variable (Beta) would be multiplied by 0,

and therefore would not impact the dependent variable i.e. Return.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

DATA ANALYSIS OF ECONOMETRICS 16

B4.

Stock R2

Adelaide Brighton 0.050672

WEBJET 0.028297

Ramsay Healthcare 0.085010709

Adelaide Brighton

The Adelaide Brighton R-square indicated that 5% of the variance in each stock

return is contributed by the changes of the market index. It has the highest R-square

compared to the other stocks. Thus, concluding that it is the best fit for this model. This is in

line with our expectations because the financial sector is influenced by economic

performance which moves in parallel with the market index.

Expectations of Adelaide Brighton

1.From the R2 is in line with our expectations as we can expect that Adelaide

Brighton’s performance is correlated to the ASX 200 performance have close beta of

1 (ASX Beta) – 0.0506 (AB Beta).

2. An R2 of 0.0506 is in the 0.00 to 1.00 range which means. This is in line with

expectations as noted from Question B2, the data plots are clustered around the trend

line, however does not perfectly fit.

B4.

Stock R2

Adelaide Brighton 0.050672

WEBJET 0.028297

Ramsay Healthcare 0.085010709

Adelaide Brighton

The Adelaide Brighton R-square indicated that 5% of the variance in each stock

return is contributed by the changes of the market index. It has the highest R-square

compared to the other stocks. Thus, concluding that it is the best fit for this model. This is in

line with our expectations because the financial sector is influenced by economic

performance which moves in parallel with the market index.

Expectations of Adelaide Brighton

1.From the R2 is in line with our expectations as we can expect that Adelaide

Brighton’s performance is correlated to the ASX 200 performance have close beta of

1 (ASX Beta) – 0.0506 (AB Beta).

2. An R2 of 0.0506 is in the 0.00 to 1.00 range which means. This is in line with

expectations as noted from Question B2, the data plots are clustered around the trend

line, however does not perfectly fit.

DATA ANALYSIS OF ECONOMETRICS 17

WEBJET

The WEBJET R2 indicated that 2.829% of the variance in the stock return is

correlated to the market index. This can be justified by the characteristics of the stock

within the market due to its low competitive forces in a stable market.

Expectations of WEBJET

1. From the R2 is in line with our expectations as we can expect that

WEBJET’s performance is correlated to the ASX 200 performance have close beta of

1 (ASX Beta) – 0.02829 (WEBJET)

2.An R2 of 0.02829 is in the 0.00 to 1.00 range. This is in line with

expectations as noted from Question B2, the data plots are clustered around the trend

line, however does not perfectly fit.

RAMSAY Healthcare:

The Ramsay Healthcare R2 indicated that 8.053% of the variance in the stock return

is associated to the market index. This is the lowest measure of fit out of the three

stocks that is not in line with our expectations. Similar to the comment made in B2 for

the beta, we expected Ramsay Healthcare’s R2 to be higher because they are market

leaders within their industry.

WEBJET

The WEBJET R2 indicated that 2.829% of the variance in the stock return is

correlated to the market index. This can be justified by the characteristics of the stock

within the market due to its low competitive forces in a stable market.

Expectations of WEBJET

1. From the R2 is in line with our expectations as we can expect that

WEBJET’s performance is correlated to the ASX 200 performance have close beta of

1 (ASX Beta) – 0.02829 (WEBJET)

2.An R2 of 0.02829 is in the 0.00 to 1.00 range. This is in line with

expectations as noted from Question B2, the data plots are clustered around the trend

line, however does not perfectly fit.

RAMSAY Healthcare:

The Ramsay Healthcare R2 indicated that 8.053% of the variance in the stock return

is associated to the market index. This is the lowest measure of fit out of the three

stocks that is not in line with our expectations. Similar to the comment made in B2 for

the beta, we expected Ramsay Healthcare’s R2 to be higher because they are market

leaders within their industry.

DATA ANALYSIS OF ECONOMETRICS 18

Expectations of CCL

1.From the R2 is in line with our expectations as we can expect that Ramsay

Healthcare’s performance is correlated to the ASX 200 performance have close beta

of 1 (ASX Beta) – 0.08053 (Ramsay Beta)

2. An R2 of 0.08053 is in the 0.00 to 1.00 range. This is in line with expectations as

noted from Question B2, the data plots are clustered around the trend line, however

does not perfectly fit (Ott and Longnecker 2015).

B5.

We have constructed an equally weighted portfolio consisting of our three chosen

stocks (equally weighted portfolio returns are simply the average of individual stock returns

in that portfolio, r p =r1 +r 2+r 3

3 ). The portfolio beta is given by 0.0374758.

Expectations of CCL

1.From the R2 is in line with our expectations as we can expect that Ramsay

Healthcare’s performance is correlated to the ASX 200 performance have close beta

of 1 (ASX Beta) – 0.08053 (Ramsay Beta)

2. An R2 of 0.08053 is in the 0.00 to 1.00 range. This is in line with expectations as

noted from Question B2, the data plots are clustered around the trend line, however

does not perfectly fit (Ott and Longnecker 2015).

B5.

We have constructed an equally weighted portfolio consisting of our three chosen

stocks (equally weighted portfolio returns are simply the average of individual stock returns

in that portfolio, r p =r1 +r 2+r 3

3 ). The portfolio beta is given by 0.0374758.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DATA ANALYSIS OF ECONOMETRICS 19

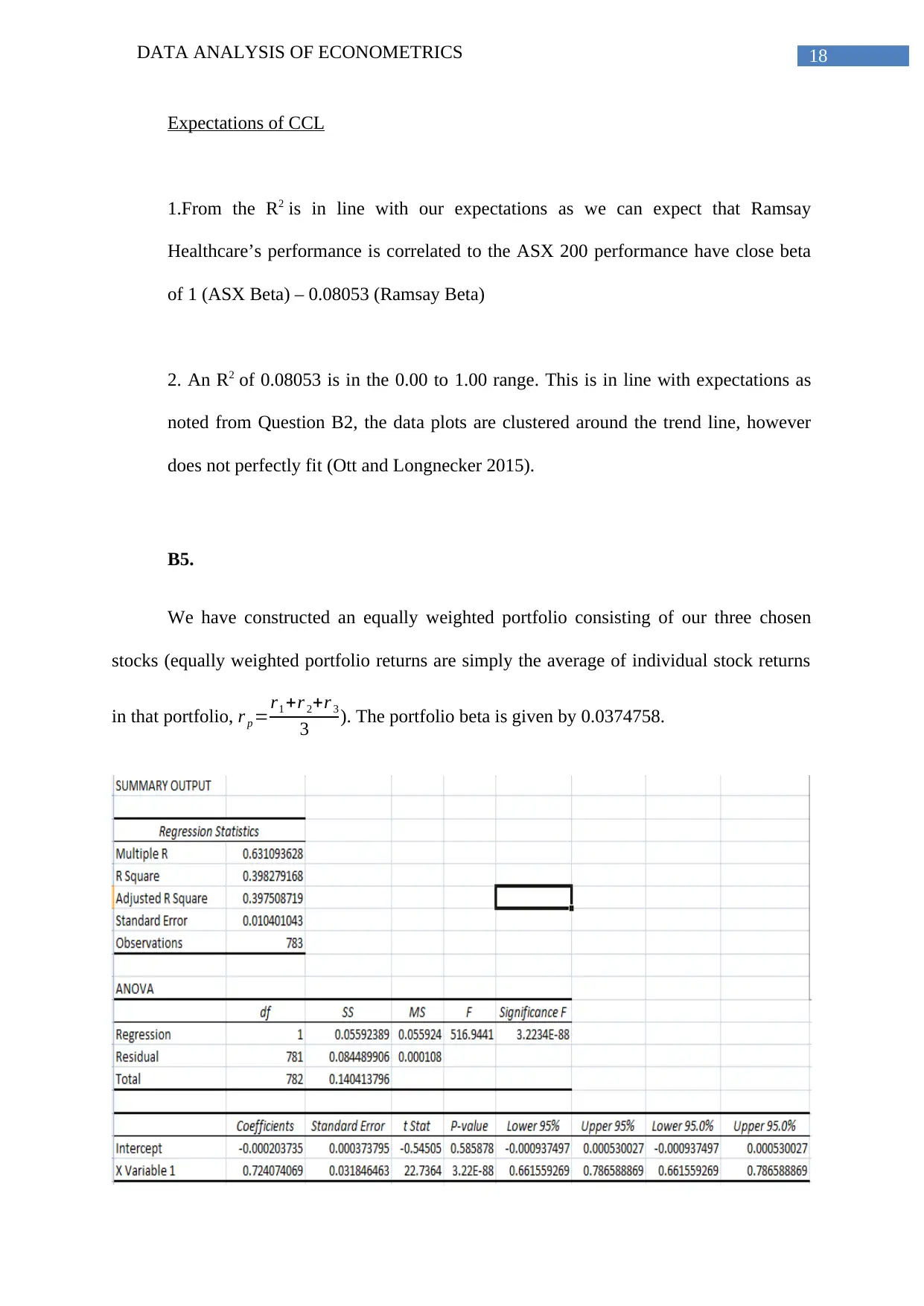

Table 5: Orthogonal Least Square regression model of Portfolio Ratio.

-0.06 -0.04 -0.02 0 0.02 0.04 0.06 0.08

-0.08

-0.06

-0.04

-0.02

0

0.02

0.04

0.06

0.08

Portfolio Ratio Residual Plot

Portfolio stock ratio

Residuals

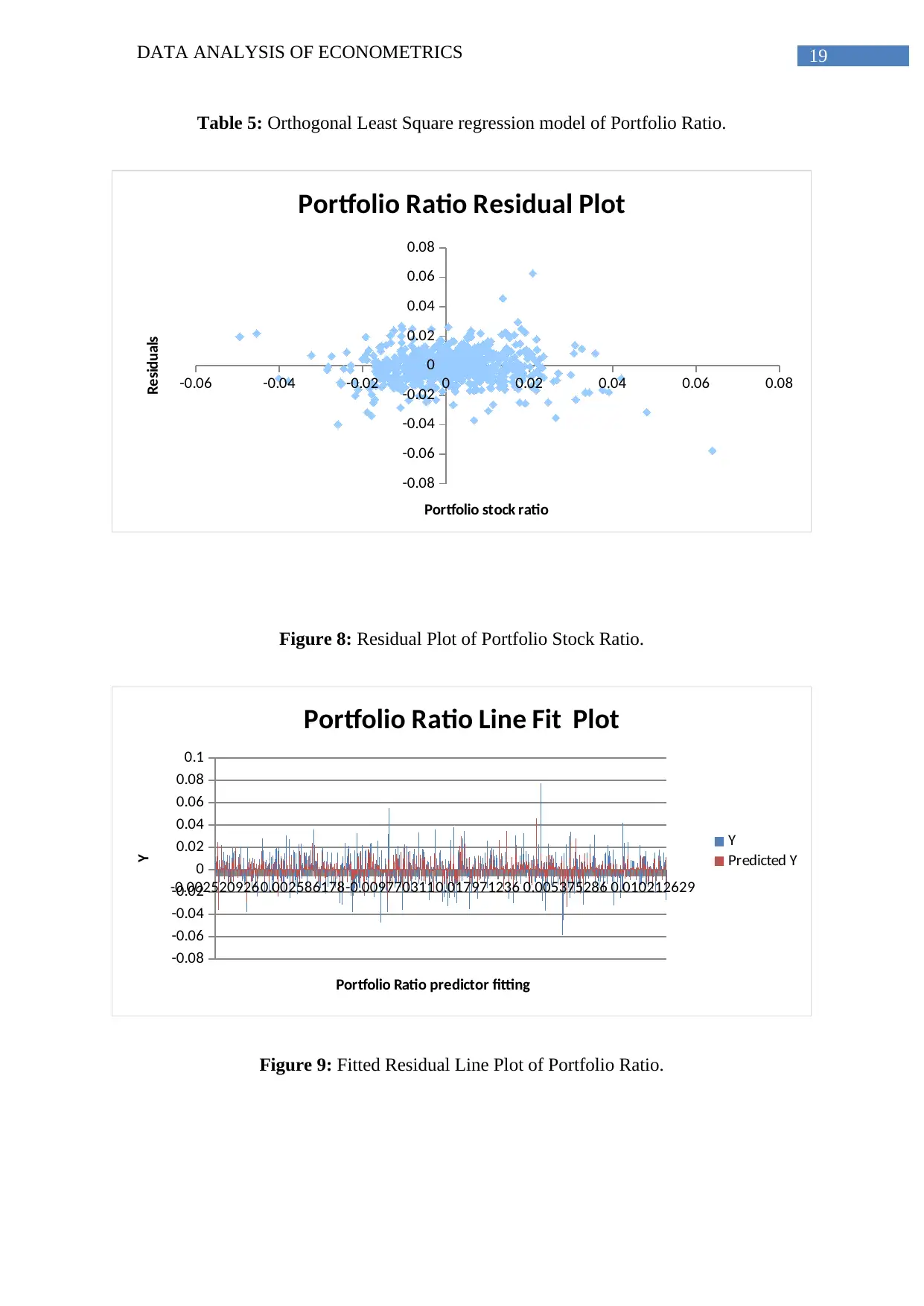

Figure 8: Residual Plot of Portfolio Stock Ratio.

-0.0025209260.002586178-0.0097703110.017971236 0.005375286 0.010212629

-0.08

-0.06

-0.04

-0.02

0

0.02

0.04

0.06

0.08

0.1

Portfolio Ratio Line Fit Plot

Y

Predicted Y

Portfolio Ratio predictor fitting

Y

Figure 9: Fitted Residual Line Plot of Portfolio Ratio.

Table 5: Orthogonal Least Square regression model of Portfolio Ratio.

-0.06 -0.04 -0.02 0 0.02 0.04 0.06 0.08

-0.08

-0.06

-0.04

-0.02

0

0.02

0.04

0.06

0.08

Portfolio Ratio Residual Plot

Portfolio stock ratio

Residuals

Figure 8: Residual Plot of Portfolio Stock Ratio.

-0.0025209260.002586178-0.0097703110.017971236 0.005375286 0.010212629

-0.08

-0.06

-0.04

-0.02

0

0.02

0.04

0.06

0.08

0.1

Portfolio Ratio Line Fit Plot

Y

Predicted Y

Portfolio Ratio predictor fitting

Y

Figure 9: Fitted Residual Line Plot of Portfolio Ratio.

DATA ANALYSIS OF ECONOMETRICS 20

0.00 0.02 0.04 0.06 0.08

-1 0 1 2 3 4 5

Leverage

S ta n d a rd iz e d re s id u a ls

lm(sqrt(rp) ~ sqrt(consumer.services.stock) + sqrt(healthcare.stock) + sqrt ...

Cook's distance

0.5

Residuals vs Leverage

5

506232

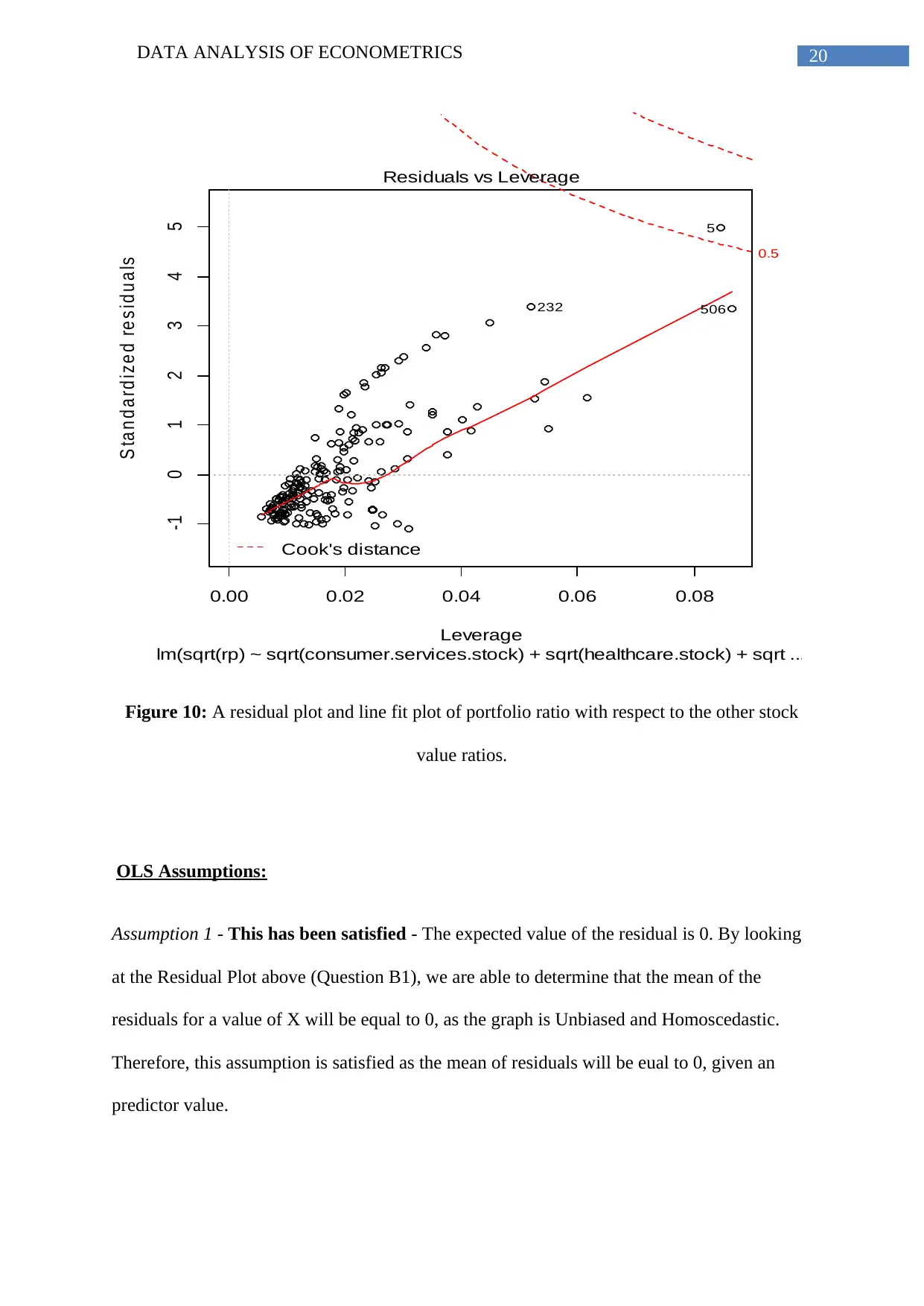

Figure 10: A residual plot and line fit plot of portfolio ratio with respect to the other stock

value ratios.

OLS Assumptions:

Assumption 1 - This has been satisfied - The expected value of the residual is 0. By looking

at the Residual Plot above (Question B1), we are able to determine that the mean of the

residuals for a value of X will be equal to 0, as the graph is Unbiased and Homoscedastic.

Therefore, this assumption is satisfied as the mean of residuals will be eual to 0, given an

predictor value.

0.00 0.02 0.04 0.06 0.08

-1 0 1 2 3 4 5

Leverage

S ta n d a rd iz e d re s id u a ls

lm(sqrt(rp) ~ sqrt(consumer.services.stock) + sqrt(healthcare.stock) + sqrt ...

Cook's distance

0.5

Residuals vs Leverage

5

506232

Figure 10: A residual plot and line fit plot of portfolio ratio with respect to the other stock

value ratios.

OLS Assumptions:

Assumption 1 - This has been satisfied - The expected value of the residual is 0. By looking

at the Residual Plot above (Question B1), we are able to determine that the mean of the

residuals for a value of X will be equal to 0, as the graph is Unbiased and Homoscedastic.

Therefore, this assumption is satisfied as the mean of residuals will be eual to 0, given an

predictor value.

DATA ANALYSIS OF ECONOMETRICS 21

Assumption 2 - This has been satisfied - The sample used for the regression model has taken

into account the whole population of the 3 years (14’-17’), and not a biased selected sample

(Identically Distributed). Further, as each daily return does not affect any other daily returns,

they are independent of each other (Independently Distributed). Therefore, this assumption is

satisfied as the selected data is independent and identically distributed.

Assumption 3 - This has not been satisfied - It can be determined that there are no outliners

which can be determined by inspecting the line fit plot. There are outliners in the plotting. It

can be concluded in a meaningless value of an estimated Beta 1, which shows this

assumption is satisfied.

Assumption 4 - This has been satisfied - The error term has a zero-conditional mean. In

other words, each stock OLS specifies each linear model such that there are no omitted

variables.

Assumption 5 - This has been satisfied - The error term u is constant across all stocks. They

all remain with the same variance and are not correlated with each other in anyway. This is

known to be in a state of homoscedasticity.

Portfolio Beta:

The Portfolio has a slope (beta) of 0.7204, which is computed from the coefficient of the

ASX 200 market return independent variable from the regression.

Statistical significance:

H0: β ̂ market=0. If there is a low p-value or high-test statistic (t-stat), then we reject the null.

For this portfolio, the P-Value is 3.2E-88 < 0.05, which implies that the critical value does lie

within the rejection region. Therefore, we can reject the null hypothesis. These statistics

Assumption 2 - This has been satisfied - The sample used for the regression model has taken

into account the whole population of the 3 years (14’-17’), and not a biased selected sample

(Identically Distributed). Further, as each daily return does not affect any other daily returns,

they are independent of each other (Independently Distributed). Therefore, this assumption is

satisfied as the selected data is independent and identically distributed.

Assumption 3 - This has not been satisfied - It can be determined that there are no outliners

which can be determined by inspecting the line fit plot. There are outliners in the plotting. It

can be concluded in a meaningless value of an estimated Beta 1, which shows this

assumption is satisfied.

Assumption 4 - This has been satisfied - The error term has a zero-conditional mean. In

other words, each stock OLS specifies each linear model such that there are no omitted

variables.

Assumption 5 - This has been satisfied - The error term u is constant across all stocks. They

all remain with the same variance and are not correlated with each other in anyway. This is

known to be in a state of homoscedasticity.

Portfolio Beta:

The Portfolio has a slope (beta) of 0.7204, which is computed from the coefficient of the

ASX 200 market return independent variable from the regression.

Statistical significance:

H0: β ̂ market=0. If there is a low p-value or high-test statistic (t-stat), then we reject the null.

For this portfolio, the P-Value is 3.2E-88 < 0.05, which implies that the critical value does lie

within the rejection region. Therefore, we can reject the null hypothesis. These statistics

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

DATA ANALYSIS OF ECONOMETRICS 22

indicate that the market does have a statistically significant impact on the returns of this

portfolio.

This Beta is in line with our expectations for the following reasons:

Stock Beta

Adelaide Brighton 0.0204 (4dp)

WEBJET 0.04761 (4dp)

RAMSAY Healthcare 0.08542 (4dp)

Portfolio (Average) 0.0374758

Thus, the average of portfolio beta is 0.0374758, which is in line with the regression beta of

0.7204 as our expectations.

R2 (Line of best fit)

The Portfolio R2 indicated that 0.63109 or 63.10% of the variance in the portfolio

return is correlated to the market index. This can be justified by the characteristics of the

portfolio relative to each stock in the portfolio’s risk.

Expectations of the Portfolio’s line of best fit

From B4, we have analyzed the R2 for each stock contained within the portfolio and

can be compared to the portfolio’s R2 of 63.10%, we expected that Adelaide Brighton’s

R2 carries more of an impact on the portfolio compared to the other R2 stocks, which the other

R2 stocks offset’s Adelaide Brighton’s R2 resulting to the computed portfolio R2.

Portfolio Diversification

indicate that the market does have a statistically significant impact on the returns of this

portfolio.

This Beta is in line with our expectations for the following reasons:

Stock Beta

Adelaide Brighton 0.0204 (4dp)

WEBJET 0.04761 (4dp)

RAMSAY Healthcare 0.08542 (4dp)

Portfolio (Average) 0.0374758

Thus, the average of portfolio beta is 0.0374758, which is in line with the regression beta of

0.7204 as our expectations.

R2 (Line of best fit)

The Portfolio R2 indicated that 0.63109 or 63.10% of the variance in the portfolio

return is correlated to the market index. This can be justified by the characteristics of the

portfolio relative to each stock in the portfolio’s risk.

Expectations of the Portfolio’s line of best fit

From B4, we have analyzed the R2 for each stock contained within the portfolio and

can be compared to the portfolio’s R2 of 63.10%, we expected that Adelaide Brighton’s

R2 carries more of an impact on the portfolio compared to the other R2 stocks, which the other

R2 stocks offset’s Adelaide Brighton’s R2 resulting to the computed portfolio R2.

Portfolio Diversification

DATA ANALYSIS OF ECONOMETRICS 23

Diversification is an investment strategy which protects an investor for unsystematic

risk, by diversifying is done by investing into a variety of stock from various industries, this

restrict the portfolio to be impacted by unsystematic risk which the risk coming from the

market, this can be quantified by the market beta.

Since the portfolio’s beta is 0.63109, it is safe to conclude that the portfolio is

diversified because its beta is less than 1.The measure of fit for the portfolio comparison with

the measures of fit for our individual stocks shows that portfolio stock is far more nicely

fitted. The portfolio diversification effect using our R2s interprets that all the stock values are

significant to the portfolio stock value.

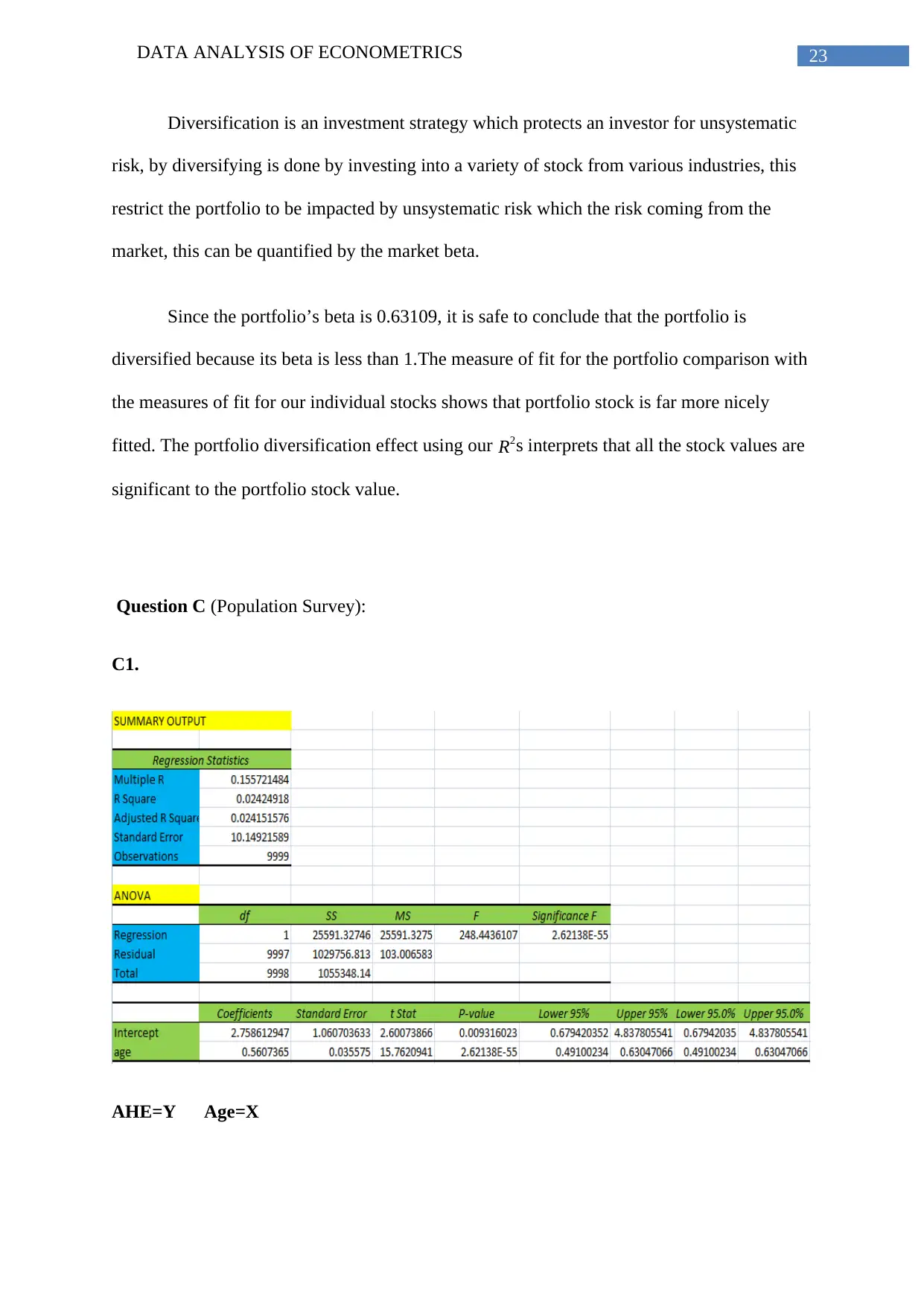

Question C (Population Survey):

C1.

AHE=Y Age=X

Diversification is an investment strategy which protects an investor for unsystematic

risk, by diversifying is done by investing into a variety of stock from various industries, this

restrict the portfolio to be impacted by unsystematic risk which the risk coming from the

market, this can be quantified by the market beta.

Since the portfolio’s beta is 0.63109, it is safe to conclude that the portfolio is

diversified because its beta is less than 1.The measure of fit for the portfolio comparison with

the measures of fit for our individual stocks shows that portfolio stock is far more nicely

fitted. The portfolio diversification effect using our R2s interprets that all the stock values are

significant to the portfolio stock value.

Question C (Population Survey):

C1.

AHE=Y Age=X

DATA ANALYSIS OF ECONOMETRICS 24

Table 6: Summary measures and ANOVA calculation of regression model of age and

average hourly earnings.

The estimated intercept of average hourly income (ahe) on age (Age) is calculated

with help of MS excel and R. The estimated intercept is 2.73951.

The estimated slope is 0.56144.

The fitted linear regression model between Average hourly earnings and Age is given by-

AverageHourlyEarnings= 2.73951 + 0.56144*Age.

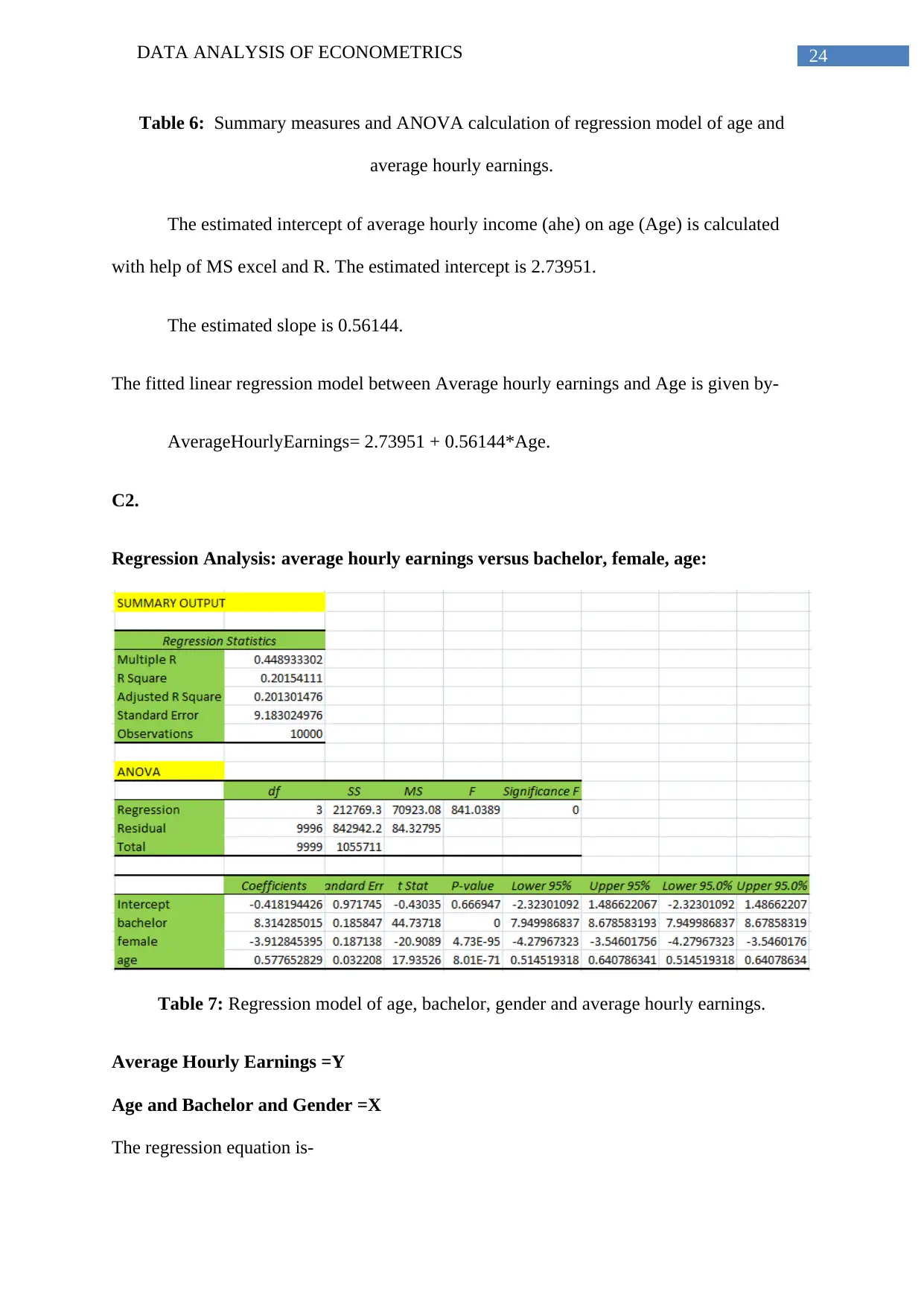

C2.

Regression Analysis: average hourly earnings versus bachelor, female, age:

Table 7: Regression model of age, bachelor, gender and average hourly earnings.

Average Hourly Earnings =Y

Age and Bachelor and Gender =X

The regression equation is-

Table 6: Summary measures and ANOVA calculation of regression model of age and

average hourly earnings.

The estimated intercept of average hourly income (ahe) on age (Age) is calculated

with help of MS excel and R. The estimated intercept is 2.73951.

The estimated slope is 0.56144.

The fitted linear regression model between Average hourly earnings and Age is given by-

AverageHourlyEarnings= 2.73951 + 0.56144*Age.

C2.

Regression Analysis: average hourly earnings versus bachelor, female, age:

Table 7: Regression model of age, bachelor, gender and average hourly earnings.

Average Hourly Earnings =Y

Age and Bachelor and Gender =X

The regression equation is-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DATA ANALYSIS OF ECONOMETRICS 25

ahe = - 0.418 + 8.31*bachelor - 3.91*female + 0.578*age

S = 9.18302 R-Sq = 20.2% R-Sq (adj) = 20.1%

The estimated effect of age on earning is = 0.578. For every increase in one year of

age , average hourly earnings increase by 0.578.

The 95% Confidence Interval for the coefficient of Age on linear regression is given

by = ((0.578+ 1.96*0.0322076677), (0.578-1.96*0.0322076677)) = (0.6408, 0.5145)

C3.

The linear regressions regarding average hourly earnings and age in C1 and C2

substantively are different from each other in the way that-

Coefficients of intercept of age in C1 and C2 are respectively 0.56144 and 0.57765.

The value of intercept is lesser than C2 in case of C1. This bias occurred due to involvement

of more two factors in C2 linear regression model.

The amount of bias is calculated as-

(0.57765- 0.56144) = 0.01621. Therefore, no significant bias is observed.

C4.

Bob is a 26-year-old male worker with a high school diploma. We have to predict

Bob's earnings using the estimated regression in C2.

ahe = - 0.418 + 8.31*bachelor - 3.91*female + 0.578*age

= -0.418 + 8.31* 0 – 3.91*0 + .578*26

= 14.61

ahe = - 0.418 + 8.31*bachelor - 3.91*female + 0.578*age

S = 9.18302 R-Sq = 20.2% R-Sq (adj) = 20.1%

The estimated effect of age on earning is = 0.578. For every increase in one year of

age , average hourly earnings increase by 0.578.

The 95% Confidence Interval for the coefficient of Age on linear regression is given

by = ((0.578+ 1.96*0.0322076677), (0.578-1.96*0.0322076677)) = (0.6408, 0.5145)

C3.

The linear regressions regarding average hourly earnings and age in C1 and C2

substantively are different from each other in the way that-

Coefficients of intercept of age in C1 and C2 are respectively 0.56144 and 0.57765.

The value of intercept is lesser than C2 in case of C1. This bias occurred due to involvement

of more two factors in C2 linear regression model.

The amount of bias is calculated as-

(0.57765- 0.56144) = 0.01621. Therefore, no significant bias is observed.

C4.

Bob is a 26-year-old male worker with a high school diploma. We have to predict

Bob's earnings using the estimated regression in C2.

ahe = - 0.418 + 8.31*bachelor - 3.91*female + 0.578*age

= -0.418 + 8.31* 0 – 3.91*0 + .578*26

= 14.61

DATA ANALYSIS OF ECONOMETRICS 26

Alexis is a30-year-old female worker with a college degree. We have to predict

Alexis’s earning using the estimated regression in C2.

ahe = - 0.418 + 8.31*bachelor - 3.91*female + 0.578*age

= -0.418 + 8.31 * 1- 3.91*1 + 0.578*30

ahe = 21.322

C5.

R-square is efficient as it explains the proportion in the variance in response (Y),

which is explained by X. Within multiple regression there is a constant increase in the R-

square due to more variables being introduced in the regression. This does not become a good

fitted model. Therefore, due to this the value of R-square shows inefficiency.

The values of R2 and adjusted R2 of the previous two linear models in C1 and C2 are

(0.0243 and 0.02421) and (0.2015 and 0.2013).

The predictor age has significant effect on the response “average hourly earnings” in

case of C1 regression model. Therefore, the model had less value of residual standard error.

Therefore, the values of residual R2 and adjusted R2 is very near to each other.

Similarly, age, gender and bachelorship have significant effect on the response

“average hourly earnings” in case of C2 regression model. Therefore, the model had less

value of residual standard error. The model in C2 has more appropriateness in case of

goodness of fit.

C6.

a) Average hourly earnings versus gender:

Gender (Female):

Alexis is a30-year-old female worker with a college degree. We have to predict

Alexis’s earning using the estimated regression in C2.

ahe = - 0.418 + 8.31*bachelor - 3.91*female + 0.578*age

= -0.418 + 8.31 * 1- 3.91*1 + 0.578*30

ahe = 21.322

C5.

R-square is efficient as it explains the proportion in the variance in response (Y),

which is explained by X. Within multiple regression there is a constant increase in the R-

square due to more variables being introduced in the regression. This does not become a good

fitted model. Therefore, due to this the value of R-square shows inefficiency.

The values of R2 and adjusted R2 of the previous two linear models in C1 and C2 are

(0.0243 and 0.02421) and (0.2015 and 0.2013).

The predictor age has significant effect on the response “average hourly earnings” in

case of C1 regression model. Therefore, the model had less value of residual standard error.

Therefore, the values of residual R2 and adjusted R2 is very near to each other.

Similarly, age, gender and bachelorship have significant effect on the response

“average hourly earnings” in case of C2 regression model. Therefore, the model had less

value of residual standard error. The model in C2 has more appropriateness in case of

goodness of fit.

C6.

a) Average hourly earnings versus gender:

Gender (Female):

DATA ANALYSIS OF ECONOMETRICS 27

Here the p-value at 95% confidence interval is given by = 4.72533E-95. It is less than

0.05. The small p-value also shows that the null hypothesis cannot be accepted. Therefore we

reject the null hypothesis of relationship of Gender with the average hourly earnings.

Therefore, gender factor can be deleted from the data.

b) Average hourly earnings versus bachelor:

Here the p-value at 95% confidence interval is given by = 0. It is less than 0.05. The

small p-value also shows that the null hypothesis cannot be accepted. Therefore we reject the

null hypothesis of relationship of bachelor with the average hourly earnings. Therefore,

bachelor factor can be deleted from the data.

c) Average hourly earnings vs (gender and bachelor):

The two factors bachelor and gender do not have linear effect on average hourly

earnings as individual variables.

-0.4181944 + 8.3143(Bachelor) – 3.9128(Female) + 0.5777(Age)

F critical=F2, d.f of F2= (10000 -3 -1)= 9996, F2=2.9957

F actual = [0.2154111 – (0.02430482 / 2)] / [(1 – 0.2154111) / (10000 -3 – 1)] = 1216.923

According to the value of f-actual (1216.923), it is greater than f-critical. Therefore, null

hypothesis is rejected so both female and male can be deleted from regression.

C7.

Condition1:

Therefore, we can conclude that we could delete and ignore these two factors for their null

effect on the variability of “average hourly earnings”. The omitted variable must be a

Here the p-value at 95% confidence interval is given by = 4.72533E-95. It is less than

0.05. The small p-value also shows that the null hypothesis cannot be accepted. Therefore we

reject the null hypothesis of relationship of Gender with the average hourly earnings.

Therefore, gender factor can be deleted from the data.

b) Average hourly earnings versus bachelor:

Here the p-value at 95% confidence interval is given by = 0. It is less than 0.05. The

small p-value also shows that the null hypothesis cannot be accepted. Therefore we reject the

null hypothesis of relationship of bachelor with the average hourly earnings. Therefore,

bachelor factor can be deleted from the data.

c) Average hourly earnings vs (gender and bachelor):

The two factors bachelor and gender do not have linear effect on average hourly

earnings as individual variables.

-0.4181944 + 8.3143(Bachelor) – 3.9128(Female) + 0.5777(Age)

F critical=F2, d.f of F2= (10000 -3 -1)= 9996, F2=2.9957

F actual = [0.2154111 – (0.02430482 / 2)] / [(1 – 0.2154111) / (10000 -3 – 1)] = 1216.923

According to the value of f-actual (1216.923), it is greater than f-critical. Therefore, null

hypothesis is rejected so both female and male can be deleted from regression.

C7.

Condition1:

Therefore, we can conclude that we could delete and ignore these two factors for their null

effect on the variability of “average hourly earnings”. The omitted variable must be a

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

DATA ANALYSIS OF ECONOMETRICS 28

determinant of the dependent variable. As the education level has an impact on the Average

Hourly Earnings, then the above condition holds.

Condition2:

Secondly, omitted variable must be correlated with an independent variable specified

in the regression. Since, the education level and gender is not correlated with the age, there is

not enough evidence to suggest this condition holds.

determinant of the dependent variable. As the education level has an impact on the Average

Hourly Earnings, then the above condition holds.

Condition2:

Secondly, omitted variable must be correlated with an independent variable specified

in the regression. Since, the education level and gender is not correlated with the age, there is

not enough evidence to suggest this condition holds.

DATA ANALYSIS OF ECONOMETRICS 29

Conclusion:

The report concludes in the first part that Sydney is most trendy city of Australia. The

interest amount and principal amount of housing is increasing year by year. In the second

part, we have interpreted that portfolio ratio is one of the most favorable ratio than other

stock ratio. The report also helped us to test various hypotheses and draw necessary

inferences about age and other factors about average hourly earnings in the thirdpart.

Conclusion:

The report concludes in the first part that Sydney is most trendy city of Australia. The

interest amount and principal amount of housing is increasing year by year. In the second

part, we have interpreted that portfolio ratio is one of the most favorable ratio than other

stock ratio. The report also helped us to test various hypotheses and draw necessary

inferences about age and other factors about average hourly earnings in the thirdpart.

DATA ANALYSIS OF ECONOMETRICS 30

Bibliography List:

Cruz, C.D., 2013. Genes: a software package for analysis in experimental statistics and

quantitative genetics. Acta Scientiarum. Agronomy, 35(3), pp.271-276.

Guo, Y., Guo, L.Z., Billings, S.A. and Wei, H.L., 2015. Identification of nonlinear systems

with non-persistent excitation using an iterative forward orthogonal least squares regression

algorithm. International Journal of Modelling, Identification and Control, 23(1), pp.1-7.

Kazem, A., Sharifi, E., Hussain, F.K., Saberi, M. and Hussain, O.K., 2013. Support vector

regression with chaos-based firefly algorithm for stock market price forecasting. Applied soft

computing, 13(2), pp.947-958.

O Schabenberger, CA Gotway – 2017, Statistical methods for spatial data analysis,

books.google.com

P Bazeley, K Jackson – 2013, Qualitative data analysis with NVivo, (450-1)

Pfister, R., Schwarz, K., Carson, R. and Jancyzk, M., 2013. Easy methods for extracting

individual regression slopes: comparing SPSS, R, and Excel. Tutor. Quant. Methods

Psychol, 9(2), pp.72-78.

RL Ott, MT Longnecker - 2015 , An introduction to statistical methods and data analysis,

Nelson Education

Slezák, P., Bokes, P., Námer, P. and Waczulíková, I., 2014. Microsoft Excel add-in for the

statistical analysis of contingency tables. International Journal for Innovation Education and

Research, 2(5), pp.90-100.

Wang, N., Er, M.J. and Han, M., 2014. Parsimonious extreme learning machine using

recursive orthogonal least squares. IEEE transactions on neural networks and learning

systems, 25(10), pp.1828-1841.

Bibliography List:

Cruz, C.D., 2013. Genes: a software package for analysis in experimental statistics and

quantitative genetics. Acta Scientiarum. Agronomy, 35(3), pp.271-276.

Guo, Y., Guo, L.Z., Billings, S.A. and Wei, H.L., 2015. Identification of nonlinear systems

with non-persistent excitation using an iterative forward orthogonal least squares regression

algorithm. International Journal of Modelling, Identification and Control, 23(1), pp.1-7.

Kazem, A., Sharifi, E., Hussain, F.K., Saberi, M. and Hussain, O.K., 2013. Support vector

regression with chaos-based firefly algorithm for stock market price forecasting. Applied soft

computing, 13(2), pp.947-958.

O Schabenberger, CA Gotway – 2017, Statistical methods for spatial data analysis,

books.google.com

P Bazeley, K Jackson – 2013, Qualitative data analysis with NVivo, (450-1)

Pfister, R., Schwarz, K., Carson, R. and Jancyzk, M., 2013. Easy methods for extracting

individual regression slopes: comparing SPSS, R, and Excel. Tutor. Quant. Methods

Psychol, 9(2), pp.72-78.

RL Ott, MT Longnecker - 2015 , An introduction to statistical methods and data analysis,

Nelson Education

Slezák, P., Bokes, P., Námer, P. and Waczulíková, I., 2014. Microsoft Excel add-in for the

statistical analysis of contingency tables. International Journal for Innovation Education and

Research, 2(5), pp.90-100.

Wang, N., Er, M.J. and Han, M., 2014. Parsimonious extreme learning machine using

recursive orthogonal least squares. IEEE transactions on neural networks and learning

systems, 25(10), pp.1828-1841.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DATA ANALYSIS OF ECONOMETRICS 31

DATA ANALYSIS OF ECONOMETRICS 32

DATA ANALYSIS OF ECONOMETRICS 33

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

DATA ANALYSIS OF ECONOMETRICS 34

1 out of 35

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.