Risk Modelling: Investment Risks in Emerging vs. Other Markets

VerifiedAdded on 2022/08/25

|14

|3332

|19

Report

AI Summary

This report presents a data analytics analysis of the risks associated with investing in emerging markets compared to other markets. The study utilizes the EDHEC data set on index returns on investments, focusing on the Emerging Markets variable. The methodology includes descriptive statistics, data visualization (time series plot), and inferential analysis using Value at Risk (VaR) to quantify the potential losses. The results reveal that while the average index return is positive, the VaR analysis indicates a 5% probability of a significant reduction in investment returns, leading to the conclusion that investments in emerging markets carry a high level of risk. The report includes detailed statistical analysis, visualizations, and R code to support the findings.

Risks Associated with Investing into Emerging Markets in Comparison with other Markets

Contents

Contents

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Data Analytics-Risk Modelling

Introduction.................................................................................................................................................3

Motivation...................................................................................................................................................4

Hypothesis...................................................................................................................................................5

Data and Methodology................................................................................................................................6

Data.........................................................................................................................................................6

Methodology...........................................................................................................................................7

Results.........................................................................................................................................................8

Descriptive Statistics...............................................................................................................................8

Data Visualization...................................................................................................................................9

Value at Risk (VaR)..............................................................................................................................10

Conclusion.................................................................................................................................................10

References.................................................................................................................................................12

Appendix: R Code and Output Screenshots...............................................................................................14

2

Introduction.................................................................................................................................................3

Motivation...................................................................................................................................................4

Hypothesis...................................................................................................................................................5

Data and Methodology................................................................................................................................6

Data.........................................................................................................................................................6

Methodology...........................................................................................................................................7

Results.........................................................................................................................................................8

Descriptive Statistics...............................................................................................................................8

Data Visualization...................................................................................................................................9

Value at Risk (VaR)..............................................................................................................................10

Conclusion.................................................................................................................................................10

References.................................................................................................................................................12

Appendix: R Code and Output Screenshots...............................................................................................14

2

Data Analytics-Risk Modelling

Introduction

Risk can be defined as the concept of taking a chance at carrying out an activity without

being certain of its success (Kiechel, 2010; Cameroon, 2013). In business terms, risk would

relate to making of financial decisions such as investing, acquiring a loan, giving out a loan and

selling stakes without being certain of the profitability of this decision (Laudon & Guercio, 2014;

Fawcett & Provost, 2013). This highlights the critical nature of risk and risk evaluation. Hence, it

is important to understand; what informs the decision to take a risk and is there a possibility of

quantifying the expected risk associated with a decision.

The modern business environment is fast paced, resulting in decisions making being

critical for any business entity. Unlike in past where the business environment allowed time for a

decision to be changed with minimal consequences, the fast pace of the modern environment has

eliminated the possibility of decision change with minimal losses. This is due to the dynamic

nature of the modern business environment. Aspects in the market place change very rapidly,

therefore a high-risk decision can quickly turn into massive losses without the possibility of

reverting the decision or mitigating losses.

Despite the nature of the modern business environment, it does not imply that risks

should not be taken by business entities (Albright & Winston, 2014; Provost & Fawcett, 2013).

Acquiring competitive advantage, new market entries, disruptive innovations and maintaining

market dominance all require exposing the business entities to a level of risk (Prescott, 2014). In

general, risk is an agent of progress in the business world. In more aggressive and competitive

markets, risk is the difference between a company going out of business or surviving (French,

2017).

3

Introduction

Risk can be defined as the concept of taking a chance at carrying out an activity without

being certain of its success (Kiechel, 2010; Cameroon, 2013). In business terms, risk would

relate to making of financial decisions such as investing, acquiring a loan, giving out a loan and

selling stakes without being certain of the profitability of this decision (Laudon & Guercio, 2014;

Fawcett & Provost, 2013). This highlights the critical nature of risk and risk evaluation. Hence, it

is important to understand; what informs the decision to take a risk and is there a possibility of

quantifying the expected risk associated with a decision.

The modern business environment is fast paced, resulting in decisions making being

critical for any business entity. Unlike in past where the business environment allowed time for a

decision to be changed with minimal consequences, the fast pace of the modern environment has

eliminated the possibility of decision change with minimal losses. This is due to the dynamic

nature of the modern business environment. Aspects in the market place change very rapidly,

therefore a high-risk decision can quickly turn into massive losses without the possibility of

reverting the decision or mitigating losses.

Despite the nature of the modern business environment, it does not imply that risks

should not be taken by business entities (Albright & Winston, 2014; Provost & Fawcett, 2013).

Acquiring competitive advantage, new market entries, disruptive innovations and maintaining

market dominance all require exposing the business entities to a level of risk (Prescott, 2014). In

general, risk is an agent of progress in the business world. In more aggressive and competitive

markets, risk is the difference between a company going out of business or surviving (French,

2017).

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Data Analytics-Risk Modelling

There are a number of parameters used for the quantification of the amount of risk

associated with a financial decision. Among these parameters is the quantile risk measure. The

quantile risk measure is a risk measure that evaluates the worst-case scenario associated with

decisions based on a probability of 1-α, with α referring to the percentage quantile on which the

risk measure is to be computed (Douglas, William, & Samuel, 2012; Pappas, 2016). This study is

going to consider the application of the quantile risk measure to a case study. The case study for

this research is the purchasing of stocks in the emerging markets. This study will consider the

research question; is investment into the emerging markets a high-risk investment. The research

considers that motivation underlying this study followed by definition of the hypothesis for the

study. The source of the data used for the study and the analyses processes conducted will then

be stated. Finally, the results and conclusions will be presented.

Motivation

Emerging markets refers to markets that are located in economies that are not in the

developed world (first world) (Grinin, Korotayev, & Tausch, 2016). This term is mostly used in

the share trading and stock exchange context. In this context, the markets refer to companies

either registered or operating in economies that are not in the developed world (Georgina, 2015).

Traditionally, the emerging markets have been associated with instability, which has deterred

investment into such markets (Besanko, Dranove, & Shanley, 2012). The high level of volatility

of the shares of companies in the emerging markets has in the past, been the reason why

investors hesitated to buy such shares (Heyne, Boettke, & Prychitko, 2010).

4

There are a number of parameters used for the quantification of the amount of risk

associated with a financial decision. Among these parameters is the quantile risk measure. The

quantile risk measure is a risk measure that evaluates the worst-case scenario associated with

decisions based on a probability of 1-α, with α referring to the percentage quantile on which the

risk measure is to be computed (Douglas, William, & Samuel, 2012; Pappas, 2016). This study is

going to consider the application of the quantile risk measure to a case study. The case study for

this research is the purchasing of stocks in the emerging markets. This study will consider the

research question; is investment into the emerging markets a high-risk investment. The research

considers that motivation underlying this study followed by definition of the hypothesis for the

study. The source of the data used for the study and the analyses processes conducted will then

be stated. Finally, the results and conclusions will be presented.

Motivation

Emerging markets refers to markets that are located in economies that are not in the

developed world (first world) (Grinin, Korotayev, & Tausch, 2016). This term is mostly used in

the share trading and stock exchange context. In this context, the markets refer to companies

either registered or operating in economies that are not in the developed world (Georgina, 2015).

Traditionally, the emerging markets have been associated with instability, which has deterred

investment into such markets (Besanko, Dranove, & Shanley, 2012). The high level of volatility

of the shares of companies in the emerging markets has in the past, been the reason why

investors hesitated to buy such shares (Heyne, Boettke, & Prychitko, 2010).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Data Analytics-Risk Modelling

However, over the past two decades there has been a drop in deterring factors in the

economies not in the developed world. A reduction in the internal conflicts, improvement in

leadership, increased development into the infrastructure and exploitation of resources has meant

that the shares of companies in the emerging markets has overtime become more attractive. The

above mentioned changes represent a move to a more stable economy, this stability encourages

investors by ensuring their investment will not be exposed to extreme non-market factors.

Although both market and non-market forces affect stock markets, minimum influence on stock

markets by non-market factors is preferred to encourage trading (Besanko, Dranove, & Shanley,

2012).

Despite the progresses made in the emerging economies to improve on their stability, it

still represent a risky market to invest. This is since, unlike the developed world, which has had a

long-term stability in their economies, economies that are not in the first world have only been

stable for a short period. This research aims at quantifying the amount of risk involved in the

purchasing of stocks in the emerging markets based on historical data.

Hypothesis

This study tests the hypothesis below:

Null Hypothesis (H0): The risks associated with emerging markets are high.

Alternative Hypothesis (H1): The risks associated with emerging markets are low.

5

However, over the past two decades there has been a drop in deterring factors in the

economies not in the developed world. A reduction in the internal conflicts, improvement in

leadership, increased development into the infrastructure and exploitation of resources has meant

that the shares of companies in the emerging markets has overtime become more attractive. The

above mentioned changes represent a move to a more stable economy, this stability encourages

investors by ensuring their investment will not be exposed to extreme non-market factors.

Although both market and non-market forces affect stock markets, minimum influence on stock

markets by non-market factors is preferred to encourage trading (Besanko, Dranove, & Shanley,

2012).

Despite the progresses made in the emerging economies to improve on their stability, it

still represent a risky market to invest. This is since, unlike the developed world, which has had a

long-term stability in their economies, economies that are not in the first world have only been

stable for a short period. This research aims at quantifying the amount of risk involved in the

purchasing of stocks in the emerging markets based on historical data.

Hypothesis

This study tests the hypothesis below:

Null Hypothesis (H0): The risks associated with emerging markets are high.

Alternative Hypothesis (H1): The risks associated with emerging markets are low.

5

Data Analytics-Risk Modelling

Data and Methodology

Data

The data utilized for the analysis process in this study is the edhec data set on the index

returns on investments. The data was collected from the EDHEC (EDHEC, 2019). The EDHEC

Risk Institute is an institution that is involved in conducting research in the finance industry

regarding different market and performance indices (EDHEC, 2019). The edhec data set used in

this study is continuously updated by the EDHEC-Risk Institute to include the most recent data

on the index returns on investments.

The data consist of information from the index returns on investments by hedge funds;

Hedge funds are firms that invest capital into trading based on speculations and mostly source

the capitals from funds saved in offshore accounts (Keller, 2015). Hedge funds are significant

financial institutions that offer privacy of investors when it comes to trading, with the investor

often represented by offshore companies.

The data contains information on 13 variables for a total of 275 observations. The edhec

data set is a time series data set with the observations representing monthly index returns on

investment for each of the 13 variables from 1997 through to 2019. This study is interested in the

investment into the emerging markets, and hence it utilizes the Emerging Markets variable in the

edhec data set. The Emerging Markets variable represents information on the monthly index

returns on the investment made by hedge funds into the emerging markets for the period from

1997 to 2019. This variable is numerical in nature and measured on the ratio scale.

6

Data and Methodology

Data

The data utilized for the analysis process in this study is the edhec data set on the index

returns on investments. The data was collected from the EDHEC (EDHEC, 2019). The EDHEC

Risk Institute is an institution that is involved in conducting research in the finance industry

regarding different market and performance indices (EDHEC, 2019). The edhec data set used in

this study is continuously updated by the EDHEC-Risk Institute to include the most recent data

on the index returns on investments.

The data consist of information from the index returns on investments by hedge funds;

Hedge funds are firms that invest capital into trading based on speculations and mostly source

the capitals from funds saved in offshore accounts (Keller, 2015). Hedge funds are significant

financial institutions that offer privacy of investors when it comes to trading, with the investor

often represented by offshore companies.

The data contains information on 13 variables for a total of 275 observations. The edhec

data set is a time series data set with the observations representing monthly index returns on

investment for each of the 13 variables from 1997 through to 2019. This study is interested in the

investment into the emerging markets, and hence it utilizes the Emerging Markets variable in the

edhec data set. The Emerging Markets variable represents information on the monthly index

returns on the investment made by hedge funds into the emerging markets for the period from

1997 to 2019. This variable is numerical in nature and measured on the ratio scale.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Data Analytics-Risk Modelling

Methodology

Three statistical methods are applied in this research, for the analysis of the edhec data

set; descriptive statistics analysis, data visualization and inferential analysis. Descriptive

Statistics analysis is a statistical method that provides an overview of the characteristics of the

variables making up the dataset of interest (Everitt & Skrondal, 2010). The descriptive statistics

in this study provides information on the measures of central tendency and variation for the

Emerging Market variable in the edhec data set. This information will be significant in gaining a

general picture of the attributes of the Emerging Markets over the period from 1997 to 2019.

Data visualization is the tabular and (or) graphical presentation of analysis findings in a research

(Kirk, 2016). The data visualization in this study will concern producing a time series plot for the

Emerging Market variable in the edhec data set. The plot will visualize the trend in the Emerging

Markets index returns from 1997 to 2019.

The inferential analysis refers to in depth research on the characteristics of data with the

aim of understanding why the data behaves the way it does as well as drawing inferences about

the data (Barbara & Susan, 2014). In this study, the inferential analysis will involve computation

of the quantile risk measure. The Value at Risk (VaR) will be the quantile risk measure

computed in the inferential analysis in this study. Value at Risk (VaR) is a quantile risk measure

estimating the expected loss for investment assuming the market conditions are normal (Pappas,

2016). This quantile risk measure considers a given probability and time for the estimation. For

the case in this research, the Value at Risk (VaR) will estimate the expected loss in investments

made in emerging markets by hedge funds over a period of one month at 5% probability. This

loss will be computed in the form of an index value.

7

Methodology

Three statistical methods are applied in this research, for the analysis of the edhec data

set; descriptive statistics analysis, data visualization and inferential analysis. Descriptive

Statistics analysis is a statistical method that provides an overview of the characteristics of the

variables making up the dataset of interest (Everitt & Skrondal, 2010). The descriptive statistics

in this study provides information on the measures of central tendency and variation for the

Emerging Market variable in the edhec data set. This information will be significant in gaining a

general picture of the attributes of the Emerging Markets over the period from 1997 to 2019.

Data visualization is the tabular and (or) graphical presentation of analysis findings in a research

(Kirk, 2016). The data visualization in this study will concern producing a time series plot for the

Emerging Market variable in the edhec data set. The plot will visualize the trend in the Emerging

Markets index returns from 1997 to 2019.

The inferential analysis refers to in depth research on the characteristics of data with the

aim of understanding why the data behaves the way it does as well as drawing inferences about

the data (Barbara & Susan, 2014). In this study, the inferential analysis will involve computation

of the quantile risk measure. The Value at Risk (VaR) will be the quantile risk measure

computed in the inferential analysis in this study. Value at Risk (VaR) is a quantile risk measure

estimating the expected loss for investment assuming the market conditions are normal (Pappas,

2016). This quantile risk measure considers a given probability and time for the estimation. For

the case in this research, the Value at Risk (VaR) will estimate the expected loss in investments

made in emerging markets by hedge funds over a period of one month at 5% probability. This

loss will be computed in the form of an index value.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Data Analytics-Risk Modelling

The R Statistical Software will be utilized for the analysis process in this study. The

Performance Analytics package will be specifically used for the evaluation of the Value at Risk

(VaR) for the index returns on investment into the emerging markets using the VaR () function.

Results

Descriptive Statistics

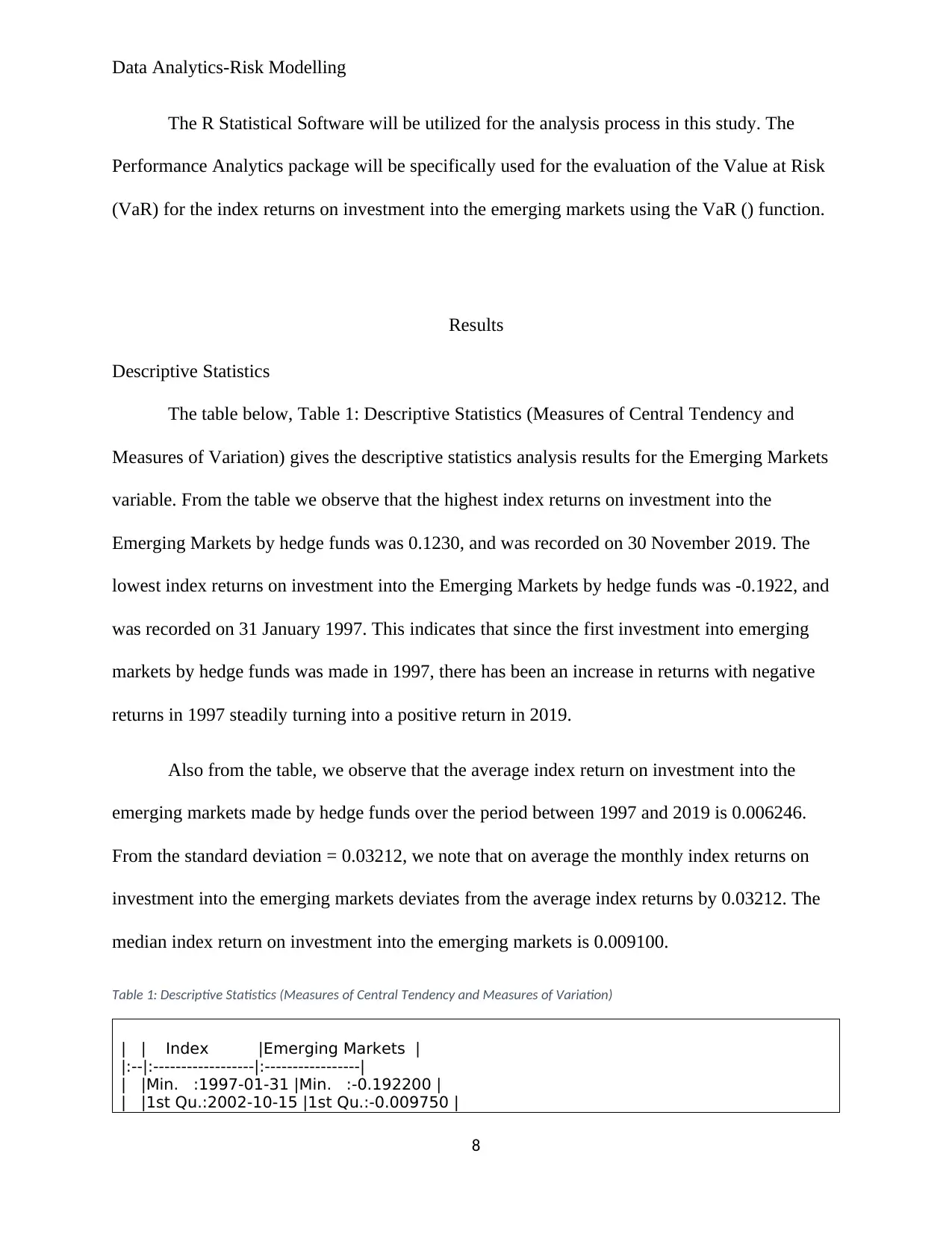

The table below, Table 1: Descriptive Statistics (Measures of Central Tendency and

Measures of Variation) gives the descriptive statistics analysis results for the Emerging Markets

variable. From the table we observe that the highest index returns on investment into the

Emerging Markets by hedge funds was 0.1230, and was recorded on 30 November 2019. The

lowest index returns on investment into the Emerging Markets by hedge funds was -0.1922, and

was recorded on 31 January 1997. This indicates that since the first investment into emerging

markets by hedge funds was made in 1997, there has been an increase in returns with negative

returns in 1997 steadily turning into a positive return in 2019.

Also from the table, we observe that the average index return on investment into the

emerging markets made by hedge funds over the period between 1997 and 2019 is 0.006246.

From the standard deviation = 0.03212, we note that on average the monthly index returns on

investment into the emerging markets deviates from the average index returns by 0.03212. The

median index return on investment into the emerging markets is 0.009100.

Table 1: Descriptive Statistics (Measures of Central Tendency and Measures of Variation)

| | Index |Emerging Markets |

|:--|:------------------|:-----------------|

| |Min. :1997-01-31 |Min. :-0.192200 |

| |1st Qu.:2002-10-15 |1st Qu.:-0.009750 |

8

The R Statistical Software will be utilized for the analysis process in this study. The

Performance Analytics package will be specifically used for the evaluation of the Value at Risk

(VaR) for the index returns on investment into the emerging markets using the VaR () function.

Results

Descriptive Statistics

The table below, Table 1: Descriptive Statistics (Measures of Central Tendency and

Measures of Variation) gives the descriptive statistics analysis results for the Emerging Markets

variable. From the table we observe that the highest index returns on investment into the

Emerging Markets by hedge funds was 0.1230, and was recorded on 30 November 2019. The

lowest index returns on investment into the Emerging Markets by hedge funds was -0.1922, and

was recorded on 31 January 1997. This indicates that since the first investment into emerging

markets by hedge funds was made in 1997, there has been an increase in returns with negative

returns in 1997 steadily turning into a positive return in 2019.

Also from the table, we observe that the average index return on investment into the

emerging markets made by hedge funds over the period between 1997 and 2019 is 0.006246.

From the standard deviation = 0.03212, we note that on average the monthly index returns on

investment into the emerging markets deviates from the average index returns by 0.03212. The

median index return on investment into the emerging markets is 0.009100.

Table 1: Descriptive Statistics (Measures of Central Tendency and Measures of Variation)

| | Index |Emerging Markets |

|:--|:------------------|:-----------------|

| |Min. :1997-01-31 |Min. :-0.192200 |

| |1st Qu.:2002-10-15 |1st Qu.:-0.009750 |

8

Data Analytics-Risk Modelling

| |Median :2008-06-30 |Median : 0.009100 |

| |Mean :2008-06-30 |Mean : 0.006246 |

| |3rd Qu.:2014-03-15 |3rd Qu.: 0.025600 |

| |Max. :2019-11-30 |Max. : 0.123000 |

| | | |

|:-------------------|:------------------|:-------------------|

|Variance |Standard Deviation |Interquartile Range |

|0.00103173278354346 |0.0321205974966759 |0.03535 |

Data Visualization

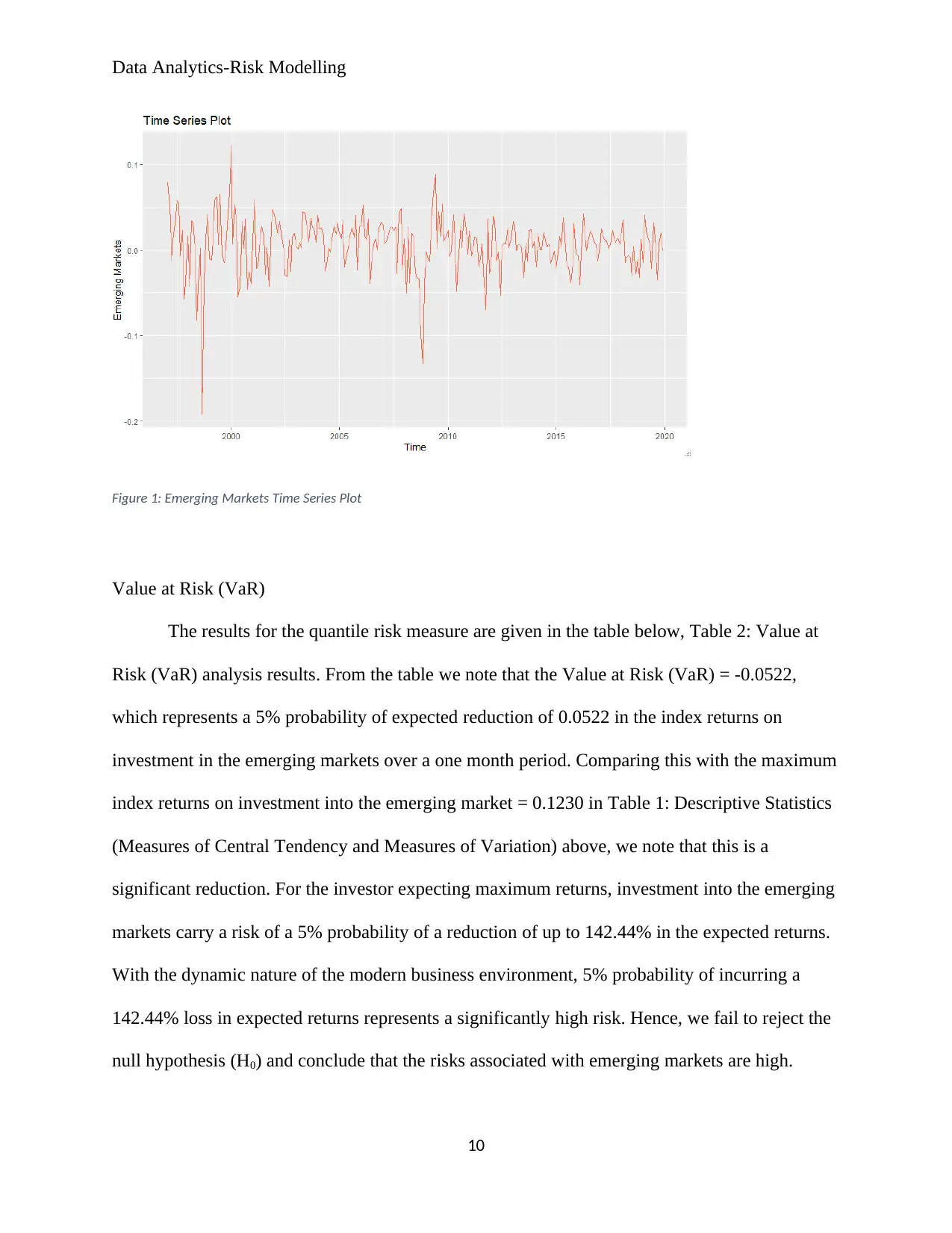

The plot in Figure 1: Emerging Markets Time Series Plot below shows the graph of the

time series data on the index returns on investment for the Emerging Markets variable. The plot

captures the trend in the returns from 1997 to 2019. From the plot, there is no linear trend in the

index returns on investments. The plot also reveals that there is no seasonality in the data, with

no visible oscillations in the curve. We however note that an additive model can be used to

provide further description of the time series since there is an almost constant size in the random

fluctuations in the data.

9

| |Median :2008-06-30 |Median : 0.009100 |

| |Mean :2008-06-30 |Mean : 0.006246 |

| |3rd Qu.:2014-03-15 |3rd Qu.: 0.025600 |

| |Max. :2019-11-30 |Max. : 0.123000 |

| | | |

|:-------------------|:------------------|:-------------------|

|Variance |Standard Deviation |Interquartile Range |

|0.00103173278354346 |0.0321205974966759 |0.03535 |

Data Visualization

The plot in Figure 1: Emerging Markets Time Series Plot below shows the graph of the

time series data on the index returns on investment for the Emerging Markets variable. The plot

captures the trend in the returns from 1997 to 2019. From the plot, there is no linear trend in the

index returns on investments. The plot also reveals that there is no seasonality in the data, with

no visible oscillations in the curve. We however note that an additive model can be used to

provide further description of the time series since there is an almost constant size in the random

fluctuations in the data.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Data Analytics-Risk Modelling

Figure 1: Emerging Markets Time Series Plot

Value at Risk (VaR)

The results for the quantile risk measure are given in the table below, Table 2: Value at

Risk (VaR) analysis results. From the table we note that the Value at Risk (VaR) = -0.0522,

which represents a 5% probability of expected reduction of 0.0522 in the index returns on

investment in the emerging markets over a one month period. Comparing this with the maximum

index returns on investment into the emerging market = 0.1230 in Table 1: Descriptive Statistics

(Measures of Central Tendency and Measures of Variation) above, we note that this is a

significant reduction. For the investor expecting maximum returns, investment into the emerging

markets carry a risk of a 5% probability of a reduction of up to 142.44% in the expected returns.

With the dynamic nature of the modern business environment, 5% probability of incurring a

142.44% loss in expected returns represents a significantly high risk. Hence, we fail to reject the

null hypothesis (H0) and conclude that the risks associated with emerging markets are high.

10

Figure 1: Emerging Markets Time Series Plot

Value at Risk (VaR)

The results for the quantile risk measure are given in the table below, Table 2: Value at

Risk (VaR) analysis results. From the table we note that the Value at Risk (VaR) = -0.0522,

which represents a 5% probability of expected reduction of 0.0522 in the index returns on

investment in the emerging markets over a one month period. Comparing this with the maximum

index returns on investment into the emerging market = 0.1230 in Table 1: Descriptive Statistics

(Measures of Central Tendency and Measures of Variation) above, we note that this is a

significant reduction. For the investor expecting maximum returns, investment into the emerging

markets carry a risk of a 5% probability of a reduction of up to 142.44% in the expected returns.

With the dynamic nature of the modern business environment, 5% probability of incurring a

142.44% loss in expected returns represents a significantly high risk. Hence, we fail to reject the

null hypothesis (H0) and conclude that the risks associated with emerging markets are high.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Data Analytics-Risk Modelling

Table 2: Value at Risk (VaR) analysis results

Emerging Markets

VaR -0.05218143

Conclusion

The analysis in this study have revealed that there has been a steady improvement in the

index returns on investment into the emerging markets since 1997. This steady improvement is

visible from the lowest index returns being recorded in 1997 at -0.1922 and the highest index

returns being recorded in 2019 at 0.123. The results on the lowest index return being recorded in

1997, when the hedge funds began to invest into the emerging markets also indicate that the

emerging markets were initially non-performing markets with negative returns. This supports the

assumption that overtime the economies in the countries that are not in the developed world have

become more stable.

The average index returns on investment into the emerging markets is found to be equal

to 0.006246, which is a very low figure. This might be as a result of the negative index returns in

the early years of investment into the emerging markets, with the negative values weighing down

the average index returns. Hence, a calculation of more recent index returns on investment into

the emerging markets may present a different and (or) clearer picture. However, this might also

not be entirely accurate considering the fluctuations shown in the time series plot, which

suggests that value of the index returns on investment into the emerging markets fluctuates a lot.

The fluctuations in the time series plot as well point to possible high risk in investing into the

emerging markets.

11

Table 2: Value at Risk (VaR) analysis results

Emerging Markets

VaR -0.05218143

Conclusion

The analysis in this study have revealed that there has been a steady improvement in the

index returns on investment into the emerging markets since 1997. This steady improvement is

visible from the lowest index returns being recorded in 1997 at -0.1922 and the highest index

returns being recorded in 2019 at 0.123. The results on the lowest index return being recorded in

1997, when the hedge funds began to invest into the emerging markets also indicate that the

emerging markets were initially non-performing markets with negative returns. This supports the

assumption that overtime the economies in the countries that are not in the developed world have

become more stable.

The average index returns on investment into the emerging markets is found to be equal

to 0.006246, which is a very low figure. This might be as a result of the negative index returns in

the early years of investment into the emerging markets, with the negative values weighing down

the average index returns. Hence, a calculation of more recent index returns on investment into

the emerging markets may present a different and (or) clearer picture. However, this might also

not be entirely accurate considering the fluctuations shown in the time series plot, which

suggests that value of the index returns on investment into the emerging markets fluctuates a lot.

The fluctuations in the time series plot as well point to possible high risk in investing into the

emerging markets.

11

Data Analytics-Risk Modelling

The analysis on the quantile risk measure, Value at Risk (VaR), reveal that there exist a

5% probability of a 142.44% loss in the expected returns from the investment made into the

emerging markets over a one month period. Despite the 5% probability being small, the amount

of loss in expected returns, 142.44% is notably high. This is further amplified by the low average

returns of 0.006246 in the index returns on investment, which would necessitate a significantly

large amount of investment to yield tangible returns. However, this large amount in investment

would mean the 5% probability of a 142.44% loss in the expected returns would also represent a

significantly large amount. Therefore, from the findings of the quantile risk measure, Value at

Risk (VaR), we conclude that investment into the emerging markets remain a highly risky

investment.

References

Albright, C. S., & Winston, W. L. (2014). Business Analytics: Data Analysis & Decision Making

(1st ed.). New York: Cengage Learning.

Barbara, I., & Susan, D. (2014). Introductory Statistics (1st ed.). New York: OpenStax CNX.

Besanko, D., Dranove, D., & Shanley, M. (2012). Economics of Strategy (1st ed.). New York:

John Wiley & Sons.

Cameroon, P. D. (2013). Liability for Catastrophic Risk in the Oil and Gas Industry. OGEL ,

2(2013), 5-9.

Douglas, L. A., William, M. G., & Samuel, W. A. (2012). Statistical Techniques in Business and

Economics (15th ed.). New York: McGraw Hill Irwin .

12

The analysis on the quantile risk measure, Value at Risk (VaR), reveal that there exist a

5% probability of a 142.44% loss in the expected returns from the investment made into the

emerging markets over a one month period. Despite the 5% probability being small, the amount

of loss in expected returns, 142.44% is notably high. This is further amplified by the low average

returns of 0.006246 in the index returns on investment, which would necessitate a significantly

large amount of investment to yield tangible returns. However, this large amount in investment

would mean the 5% probability of a 142.44% loss in the expected returns would also represent a

significantly large amount. Therefore, from the findings of the quantile risk measure, Value at

Risk (VaR), we conclude that investment into the emerging markets remain a highly risky

investment.

References

Albright, C. S., & Winston, W. L. (2014). Business Analytics: Data Analysis & Decision Making

(1st ed.). New York: Cengage Learning.

Barbara, I., & Susan, D. (2014). Introductory Statistics (1st ed.). New York: OpenStax CNX.

Besanko, D., Dranove, D., & Shanley, M. (2012). Economics of Strategy (1st ed.). New York:

John Wiley & Sons.

Cameroon, P. D. (2013). Liability for Catastrophic Risk in the Oil and Gas Industry. OGEL ,

2(2013), 5-9.

Douglas, L. A., William, M. G., & Samuel, W. A. (2012). Statistical Techniques in Business and

Economics (15th ed.). New York: McGraw Hill Irwin .

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.