Comprehensive Analysis of Cash Flow, Financial Ratios, and Costs

VerifiedAdded on 2023/01/12

|11

|1800

|92

Homework Assignment

AI Summary

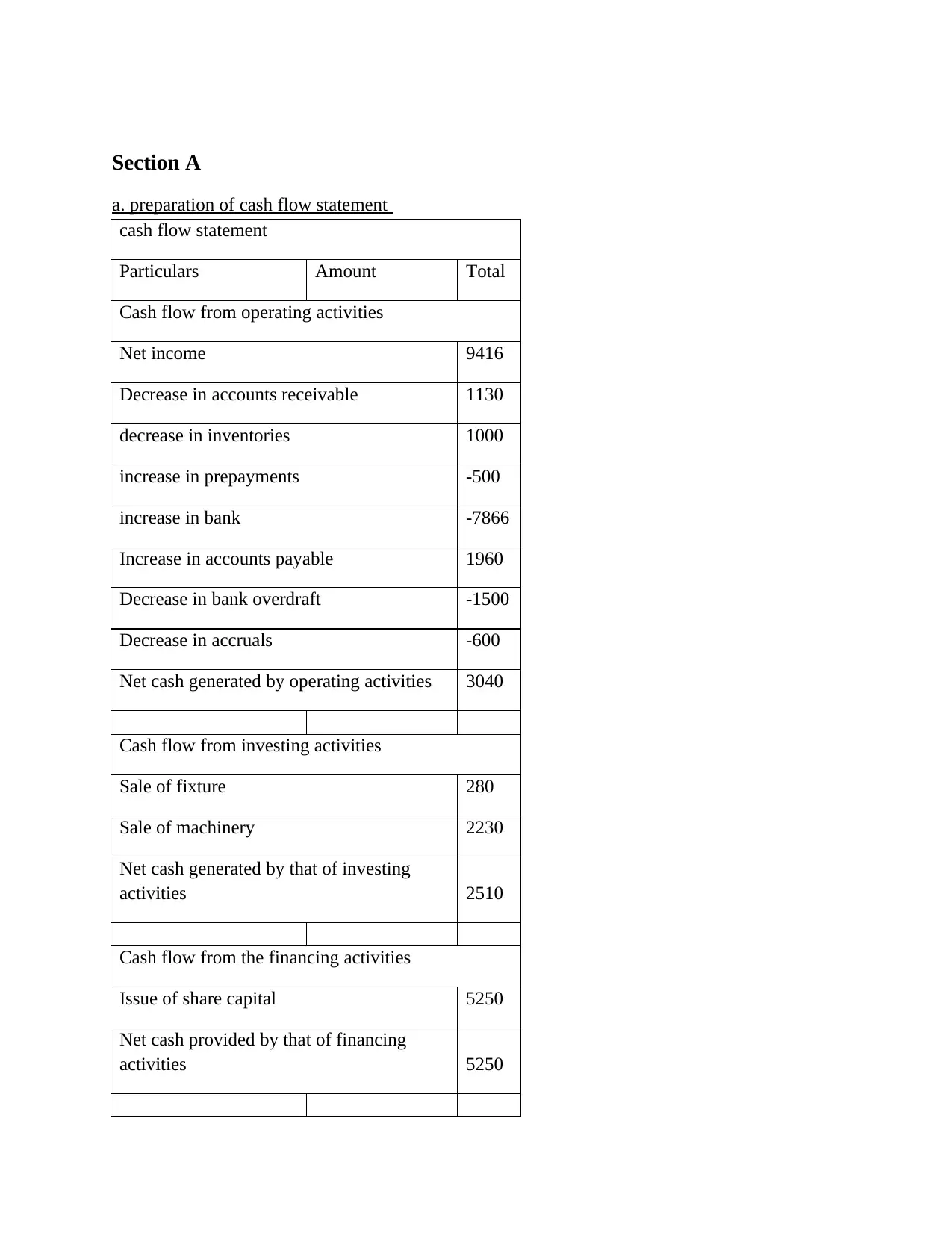

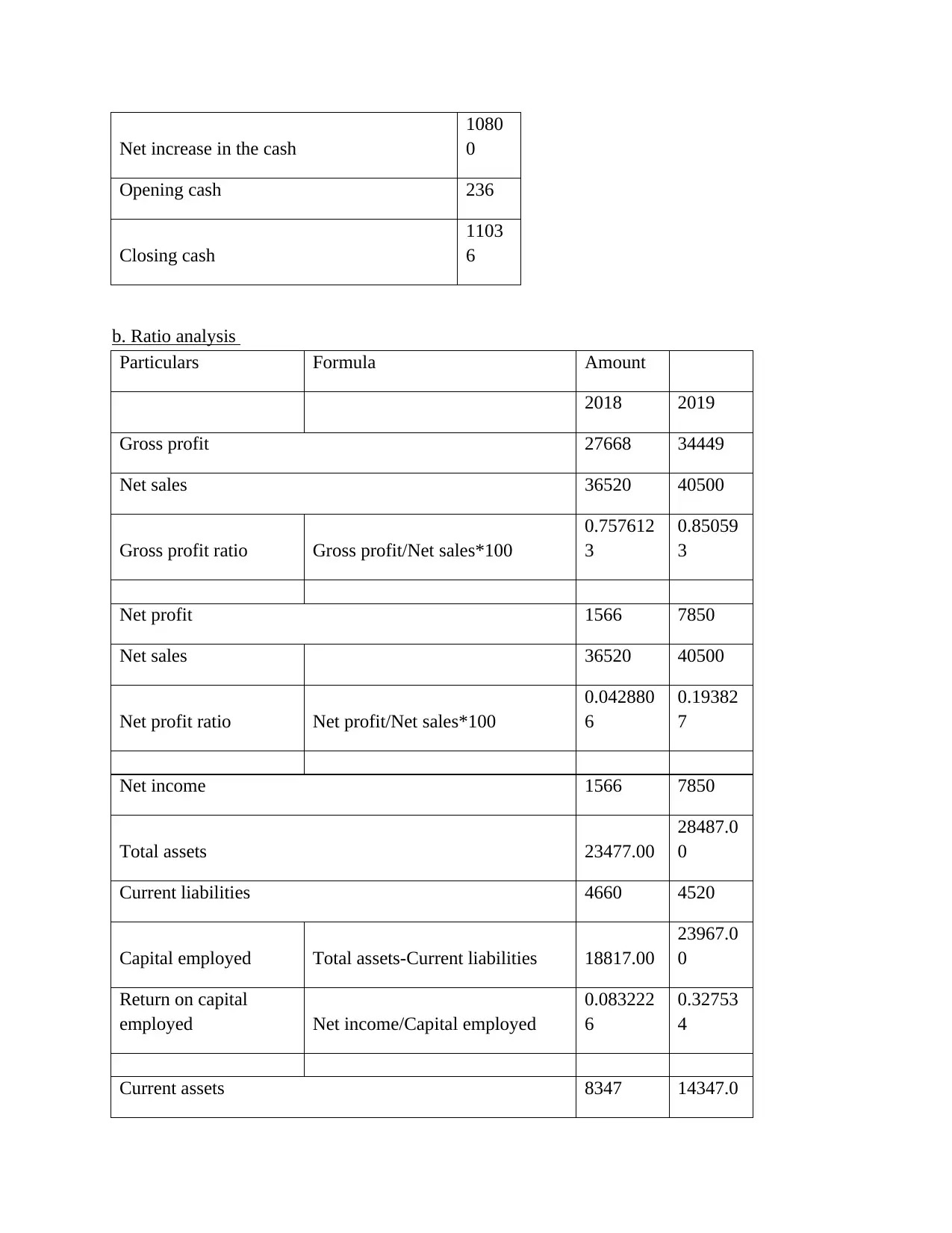

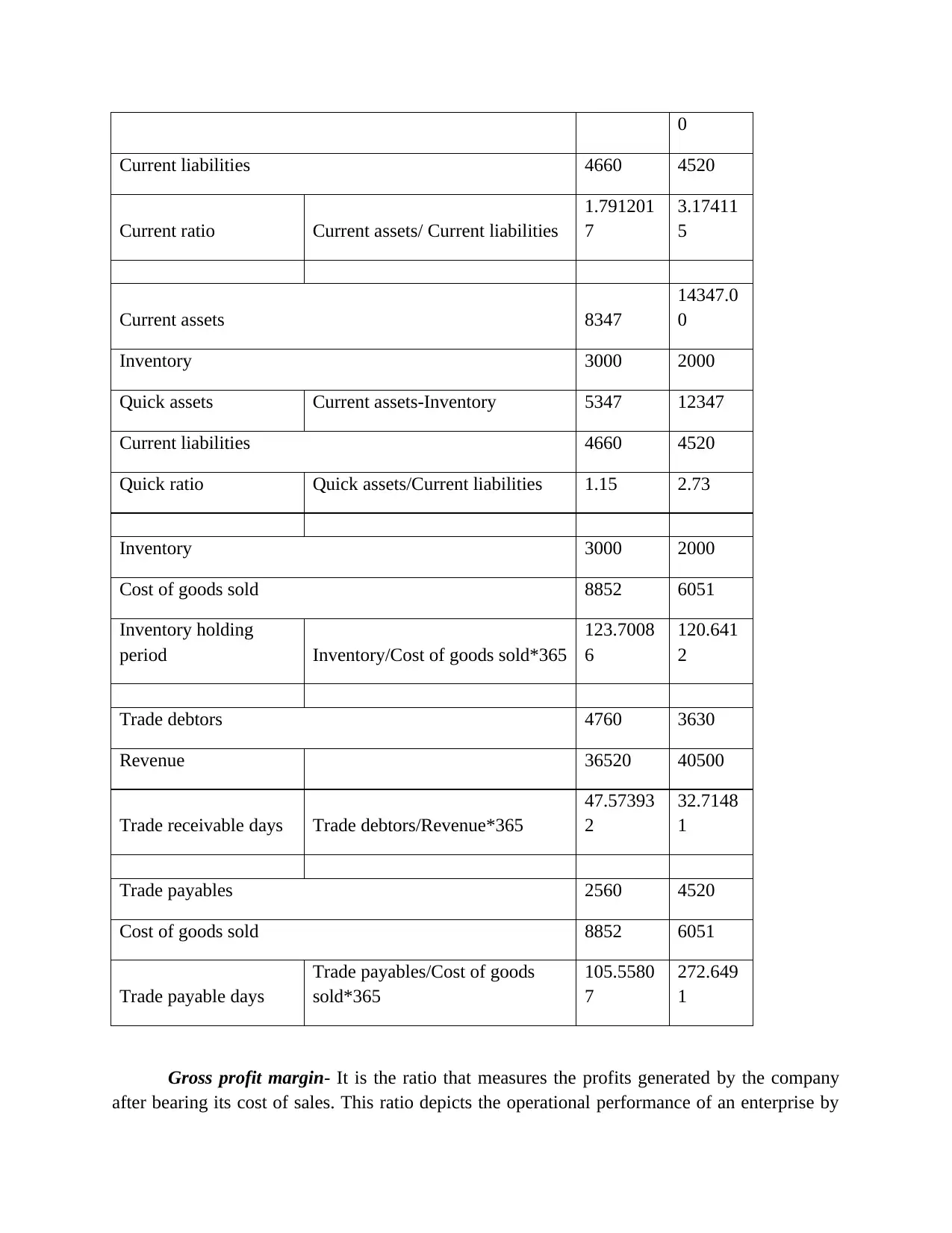

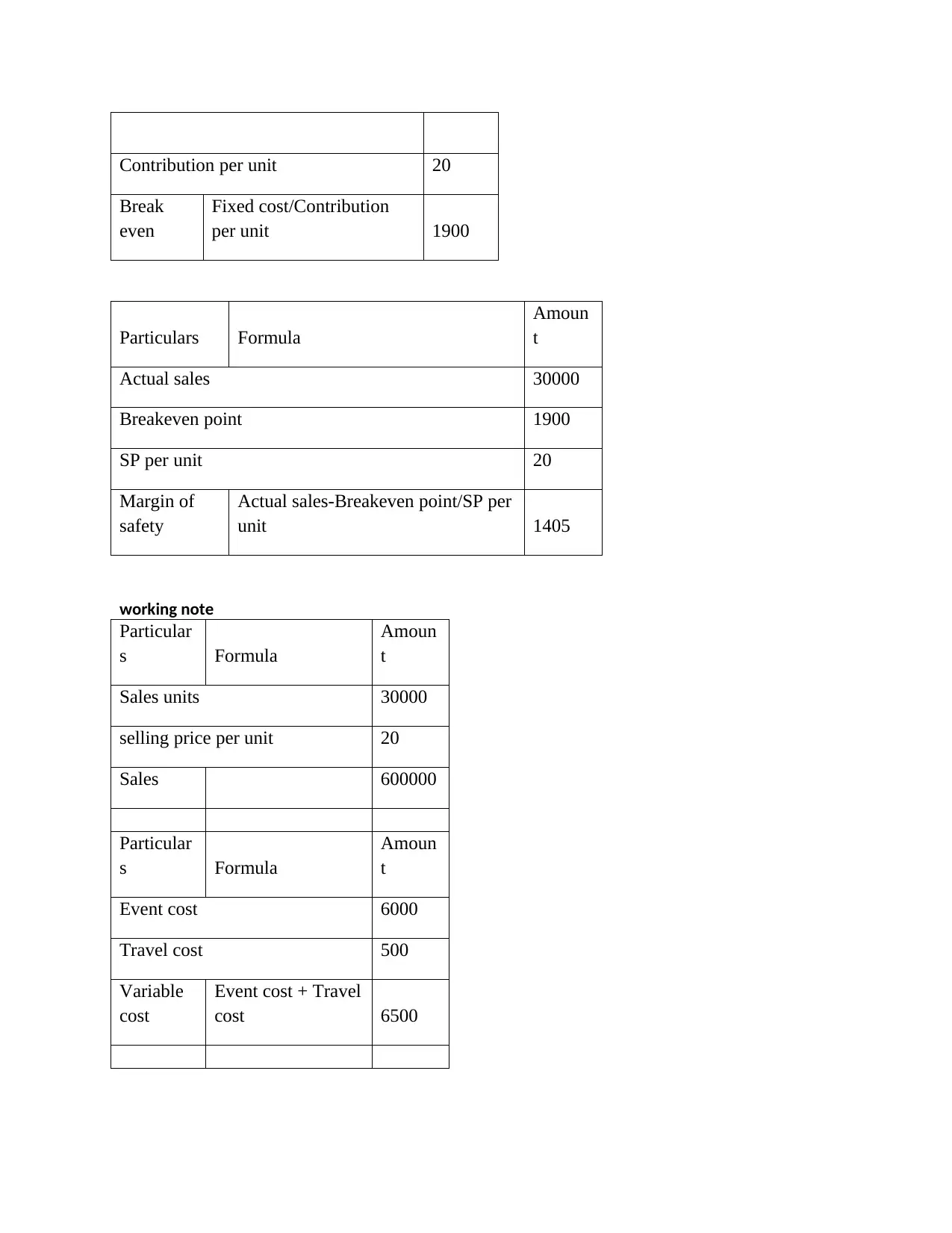

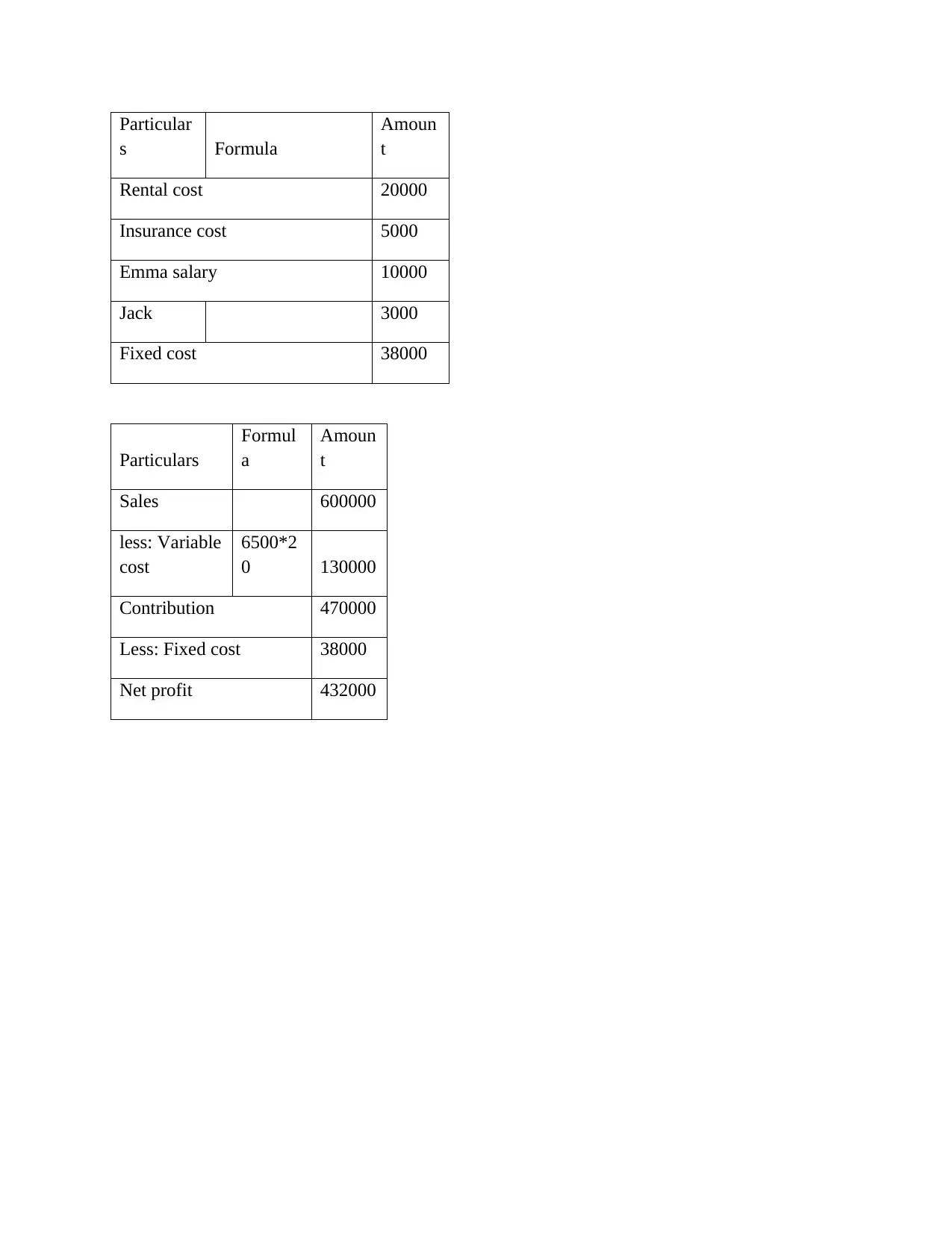

This assignment presents a comprehensive financial analysis, beginning with the preparation of a cash flow statement, detailing cash flows from operating, investing, and financing activities. It then delves into a thorough ratio analysis, evaluating profitability (gross profit margin, net profit margin, return on capital employed), liquidity (current ratio, quick ratio), and efficiency ratios (inventory days, trade receivable days, trade payable days) for Button Ltd. The analysis includes interpretations of each ratio's implications on the company's financial health and performance, along with a discussion of the limitations of financial ratios. Section B explores cost analysis, including product and period costs, their importance, and the preparation of project budgets. It also covers break-even analysis and margin of safety calculations, providing insights into sales, costs, and profitability. The assignment concludes with a detailed calculation of fixed and variable costs, contribution margin, and net profit, supported by relevant formulas and working notes, to provide a complete financial picture of the company's performance and financial position.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.