Debit Securities Analysis, Ratio & Altman Z Score: Qube Holdings

VerifiedAdded on 2023/06/18

|11

|2915

|493

Report

AI Summary

This report provides a comprehensive analysis of Qube Holdings' debit securities, beginning with an industry structure analysis using Porter's Five Forces, which indicates a strong position for the company. The fundamental analysis employs a 'top-down methodology' to assess economic conditions and industry trends. Key financial ratios, including EBITDA margin, return on capital employed, and EBIT interest coverage, are calculated and analyzed, revealing a recent decline in profitability. The Altman Z-score is used to evaluate the company's risk of bankruptcy. The report also includes a forecast of future ratios using a three-year average. The analysis sheds light on Qube Holding's financial health, debt management, and overall operational efficiency, offering valuable insights into its performance and future prospects.

Debit Securities

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Industry structure analysis..........................................................................................................3

Industry fundamental analysis....................................................................................................4

Ratio analysis..............................................................................................................................4

Altman Z score............................................................................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Industry structure analysis..........................................................................................................3

Industry fundamental analysis....................................................................................................4

Ratio analysis..............................................................................................................................4

Altman Z score............................................................................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

The debit securities are defined as the type of financial asset which entitle the owner with

the interest payment. This can be simply stated as the type of asset which is being created at time

when one of the party lend money to another. The present study is based on company Qube

Holdings which was founded in the year 2006 by Chris Corrigan. The company is the Australia’s

largest import and export logistics provider. The current report will outline the industry structure

analysis along with fundamental analysis. Further the ratios will be calculated along with

forecasting of ratios for next year. In the end, Altman Z score will be calculated in order to

analyse the security.

MAIN BODY

Industry structure analysis

Analysis of industry structure is very important as it outlines the characteristic of the

industry and working patterns of overall industry. For the company to work in better and

effective manner it is necessary that they evaluate all the working patterns and follow the similar

kind of activities in their own operations as well (Marques, de Sousa Ribeiro and Barboza,

2018). for the industry structure analysis use of Porter five forces will be undertaken which as

follows-

Threat of substitute- the threat of substitute for Qube Holding is low as there are only

limited ways through which import and export of goods can be done. Hence, this is good

for company and as a result of this operations of business will be good.

Threat of new entrant- the threat of new people entering within the import and export

logistic industry is high. thus, this is beneficial for Qube Holding as the people will come

less in industry due to high investment so company can be more profitable.

Bargaining power of supplier- the supplier within the logistic industry are many and as a

result of this, Qube Holding has many option to choose from. Thus, this not affects the

profitability of company. the reason underlying this fact is that when the suppliers are

more and if their rates are high the company can go with other supplier.

Bargaining power of buyer- the buyer are the king for the company and business has to

make all its services in direction of betterment of consumers (Cantrell, 2019). Hence, for

The debit securities are defined as the type of financial asset which entitle the owner with

the interest payment. This can be simply stated as the type of asset which is being created at time

when one of the party lend money to another. The present study is based on company Qube

Holdings which was founded in the year 2006 by Chris Corrigan. The company is the Australia’s

largest import and export logistics provider. The current report will outline the industry structure

analysis along with fundamental analysis. Further the ratios will be calculated along with

forecasting of ratios for next year. In the end, Altman Z score will be calculated in order to

analyse the security.

MAIN BODY

Industry structure analysis

Analysis of industry structure is very important as it outlines the characteristic of the

industry and working patterns of overall industry. For the company to work in better and

effective manner it is necessary that they evaluate all the working patterns and follow the similar

kind of activities in their own operations as well (Marques, de Sousa Ribeiro and Barboza,

2018). for the industry structure analysis use of Porter five forces will be undertaken which as

follows-

Threat of substitute- the threat of substitute for Qube Holding is low as there are only

limited ways through which import and export of goods can be done. Hence, this is good

for company and as a result of this operations of business will be good.

Threat of new entrant- the threat of new people entering within the import and export

logistic industry is high. thus, this is beneficial for Qube Holding as the people will come

less in industry due to high investment so company can be more profitable.

Bargaining power of supplier- the supplier within the logistic industry are many and as a

result of this, Qube Holding has many option to choose from. Thus, this not affects the

profitability of company. the reason underlying this fact is that when the suppliers are

more and if their rates are high the company can go with other supplier.

Bargaining power of buyer- the buyer are the king for the company and business has to

make all its services in direction of betterment of consumers (Cantrell, 2019). Hence, for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Qube Holding the bargaining power of consumer is high and this affects the working to a

great extent.

Competitive rivalry- the competition within the industry is very high and because of this

Qube Holding need to work in more effective manner (Manaseer and Al-Oshaibat, 2018).

This is essential for the reason that when competition is high then company need to have

some distinct capabilities so that consumer gets attracted towards the company.

Hence, with the help of Porter five forces it is clear that the company is having good position

within the industry and the performance of company is good.

Industry fundamental analysis

Fundamental analysis is being defined as the examination of the forces which can affect

the well- being of industry, economy and the company as well. for the effective management of

the company it is clear that they properly analyse the working of the industry and its patterns.

The reason underlying this fact is that when the company will be having proper knowledge of

industry then this will result in proper working of the company. This is necessary as it will

acknowledge Qube Holding relating to working trends and as a result of this effective working

will be managed in proper and good manner (Tin and Hii, 2020). Hence, for the proper working

of Qube Holding it is necessary that there is proper track of industry and for this they undertake

the use of ‘top down methodology’. This is a technique wherein the company first analyses the

economic condition and there after studies the trend in the industry. Further after that company

analyses its working in accordance with the industry and make their own strategies. Hence, this

will assist the company in evaluating the working in according to industry practices and then

make strategies for working effectively.

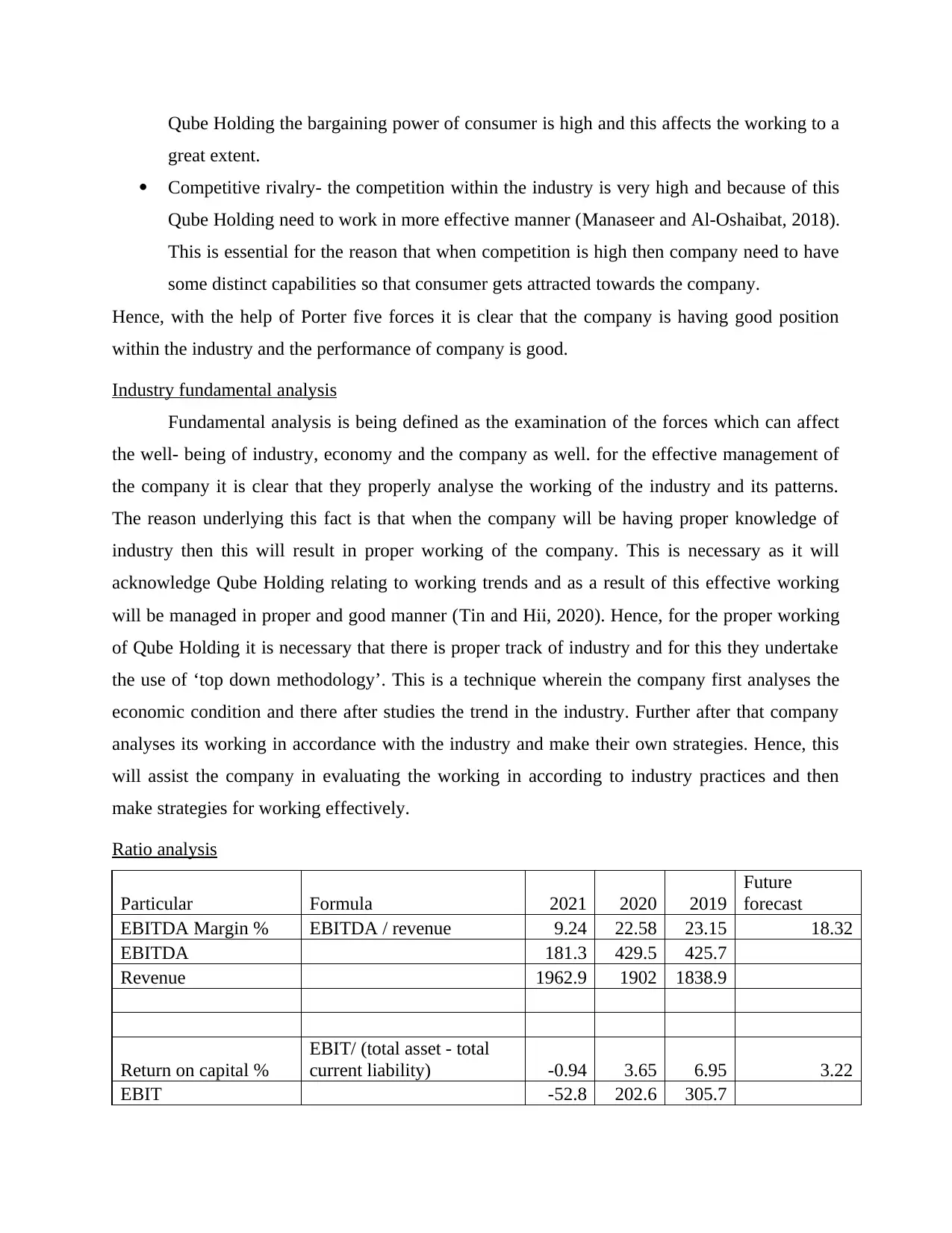

Ratio analysis

Particular Formula 2021 2020 2019

Future

forecast

EBITDA Margin % EBITDA / revenue 9.24 22.58 23.15 18.32

EBITDA 181.3 429.5 425.7

Revenue 1962.9 1902 1838.9

Return on capital %

EBIT/ (total asset - total

current liability) -0.94 3.65 6.95 3.22

EBIT -52.8 202.6 305.7

great extent.

Competitive rivalry- the competition within the industry is very high and because of this

Qube Holding need to work in more effective manner (Manaseer and Al-Oshaibat, 2018).

This is essential for the reason that when competition is high then company need to have

some distinct capabilities so that consumer gets attracted towards the company.

Hence, with the help of Porter five forces it is clear that the company is having good position

within the industry and the performance of company is good.

Industry fundamental analysis

Fundamental analysis is being defined as the examination of the forces which can affect

the well- being of industry, economy and the company as well. for the effective management of

the company it is clear that they properly analyse the working of the industry and its patterns.

The reason underlying this fact is that when the company will be having proper knowledge of

industry then this will result in proper working of the company. This is necessary as it will

acknowledge Qube Holding relating to working trends and as a result of this effective working

will be managed in proper and good manner (Tin and Hii, 2020). Hence, for the proper working

of Qube Holding it is necessary that there is proper track of industry and for this they undertake

the use of ‘top down methodology’. This is a technique wherein the company first analyses the

economic condition and there after studies the trend in the industry. Further after that company

analyses its working in accordance with the industry and make their own strategies. Hence, this

will assist the company in evaluating the working in according to industry practices and then

make strategies for working effectively.

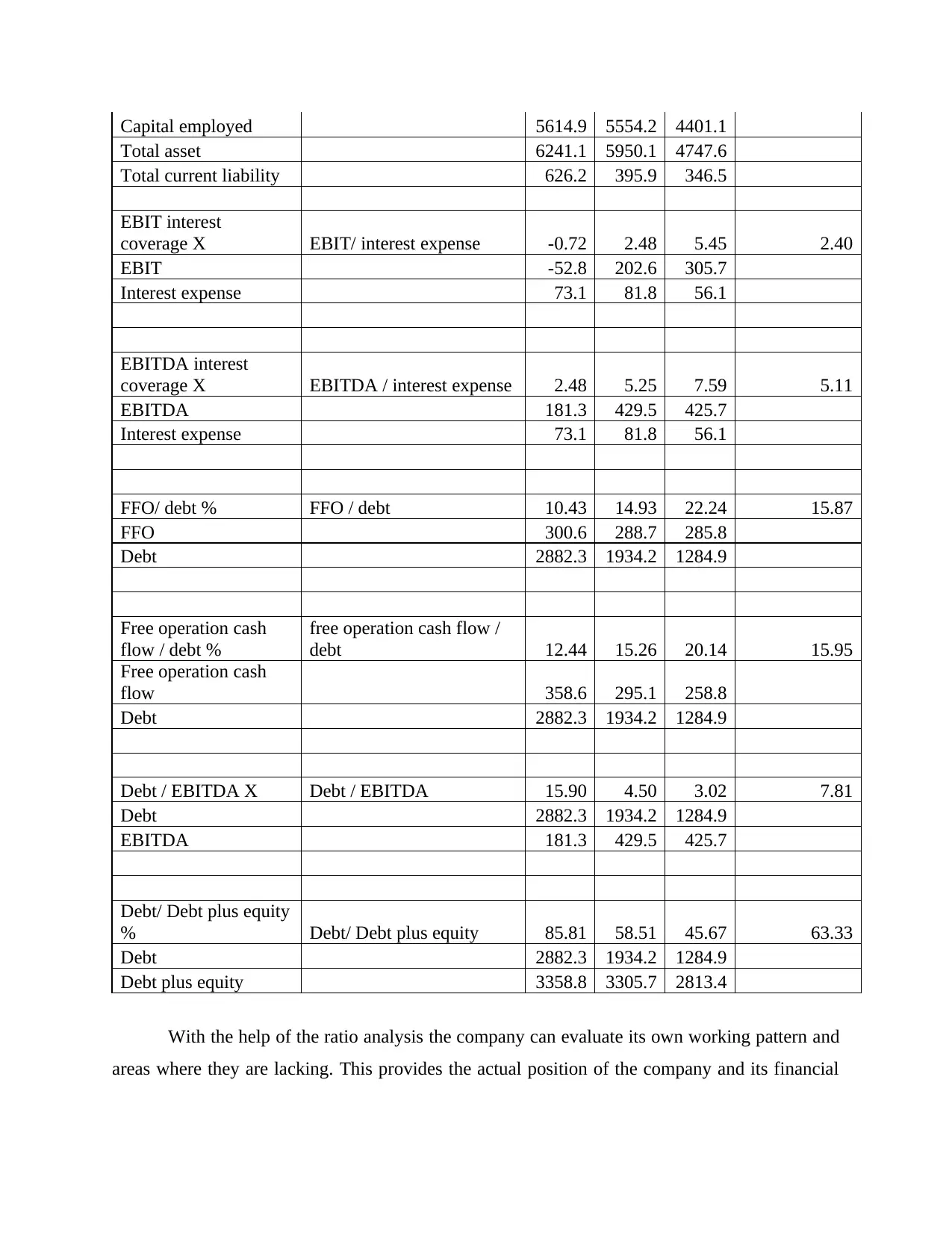

Ratio analysis

Particular Formula 2021 2020 2019

Future

forecast

EBITDA Margin % EBITDA / revenue 9.24 22.58 23.15 18.32

EBITDA 181.3 429.5 425.7

Revenue 1962.9 1902 1838.9

Return on capital %

EBIT/ (total asset - total

current liability) -0.94 3.65 6.95 3.22

EBIT -52.8 202.6 305.7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Capital employed 5614.9 5554.2 4401.1

Total asset 6241.1 5950.1 4747.6

Total current liability 626.2 395.9 346.5

EBIT interest

coverage X EBIT/ interest expense -0.72 2.48 5.45 2.40

EBIT -52.8 202.6 305.7

Interest expense 73.1 81.8 56.1

EBITDA interest

coverage X EBITDA / interest expense 2.48 5.25 7.59 5.11

EBITDA 181.3 429.5 425.7

Interest expense 73.1 81.8 56.1

FFO/ debt % FFO / debt 10.43 14.93 22.24 15.87

FFO 300.6 288.7 285.8

Debt 2882.3 1934.2 1284.9

Free operation cash

flow / debt %

free operation cash flow /

debt 12.44 15.26 20.14 15.95

Free operation cash

flow 358.6 295.1 258.8

Debt 2882.3 1934.2 1284.9

Debt / EBITDA X Debt / EBITDA 15.90 4.50 3.02 7.81

Debt 2882.3 1934.2 1284.9

EBITDA 181.3 429.5 425.7

Debt/ Debt plus equity

% Debt/ Debt plus equity 85.81 58.51 45.67 63.33

Debt 2882.3 1934.2 1284.9

Debt plus equity 3358.8 3305.7 2813.4

With the help of the ratio analysis the company can evaluate its own working pattern and

areas where they are lacking. This provides the actual position of the company and its financial

Total asset 6241.1 5950.1 4747.6

Total current liability 626.2 395.9 346.5

EBIT interest

coverage X EBIT/ interest expense -0.72 2.48 5.45 2.40

EBIT -52.8 202.6 305.7

Interest expense 73.1 81.8 56.1

EBITDA interest

coverage X EBITDA / interest expense 2.48 5.25 7.59 5.11

EBITDA 181.3 429.5 425.7

Interest expense 73.1 81.8 56.1

FFO/ debt % FFO / debt 10.43 14.93 22.24 15.87

FFO 300.6 288.7 285.8

Debt 2882.3 1934.2 1284.9

Free operation cash

flow / debt %

free operation cash flow /

debt 12.44 15.26 20.14 15.95

Free operation cash

flow 358.6 295.1 258.8

Debt 2882.3 1934.2 1284.9

Debt / EBITDA X Debt / EBITDA 15.90 4.50 3.02 7.81

Debt 2882.3 1934.2 1284.9

EBITDA 181.3 429.5 425.7

Debt/ Debt plus equity

% Debt/ Debt plus equity 85.81 58.51 45.67 63.33

Debt 2882.3 1934.2 1284.9

Debt plus equity 3358.8 3305.7 2813.4

With the help of the ratio analysis the company can evaluate its own working pattern and

areas where they are lacking. This provides the actual position of the company and its financial

aspect. The reason for using the ratio is that it will assist company in comparing the performance

for past three years and predict the future performance.

With help of the EBITDA Margin it is clear that in the current year the performance of

the company is not good (Szelągowska and Staszkiewicz, 2018). The reason underlying this fact

is that in the current year this margin was 9.24 % only but in the past two year the performance

was good like 22.58 % and 23.15 %. Thus, with this it can be analysed that the profitability of

company has reduced to a great extent. This is necessary for the reason that this EBITDA

highlights the profitability of company and this need to be high.

Further with help of return on capital employed it is clear that in the current year the

company is having negative return. This implies that company is not in condition to provide

good return to the shareholders. But in past year the company was providing return to the

company and it started decreasing gradually.

Along with this, the EBIT interest coverage ratio is the one which highlights the interest

payment made by the company. this interest coverage ratio is a performance metrics which assist

company in determining the fact that how much company is paying the interest. This is very

important because of the reason that when the interest paid will be good then this will motivate

the people to invest more in company (Subburaj, 2019). with the help of ratio analysis, it is clear

that in the current year the ratio is in negative as the there is negative EBIT. But in the past two

years the company has worked in proper and effective manner. Moreover, in case when EBITDA

was undertaken then at that time the interest coverage ratio was good. Hence, it is evident that

EBITDA provides more reliable and relevant information relating to the working.

Further, the FFO that is funds from operation was calculated and with this it was analysed

that company was effective in using its funds from operations. This is a total debt leverage ratio

which assist Qube Holding in assessing the risk of the company. this is necessary to be

calculated as when the company is not able to analyse its risk then strategies cannot be

formulated in proper and effective manner. In the present case as well the company is not having

higher FFO as compared the past performance.

In addition to this, free operation cash flow was also calculated in order to analyse the

fact that how much money is being left or is being generated from the normal business

operations (Dempsey, 2019). The ratio of free cash flow to debt signifies the amount of debt

which will be paid in current year in case all the free cash flow will be used for payment of debt.

for past three years and predict the future performance.

With help of the EBITDA Margin it is clear that in the current year the performance of

the company is not good (Szelągowska and Staszkiewicz, 2018). The reason underlying this fact

is that in the current year this margin was 9.24 % only but in the past two year the performance

was good like 22.58 % and 23.15 %. Thus, with this it can be analysed that the profitability of

company has reduced to a great extent. This is necessary for the reason that this EBITDA

highlights the profitability of company and this need to be high.

Further with help of return on capital employed it is clear that in the current year the

company is having negative return. This implies that company is not in condition to provide

good return to the shareholders. But in past year the company was providing return to the

company and it started decreasing gradually.

Along with this, the EBIT interest coverage ratio is the one which highlights the interest

payment made by the company. this interest coverage ratio is a performance metrics which assist

company in determining the fact that how much company is paying the interest. This is very

important because of the reason that when the interest paid will be good then this will motivate

the people to invest more in company (Subburaj, 2019). with the help of ratio analysis, it is clear

that in the current year the ratio is in negative as the there is negative EBIT. But in the past two

years the company has worked in proper and effective manner. Moreover, in case when EBITDA

was undertaken then at that time the interest coverage ratio was good. Hence, it is evident that

EBITDA provides more reliable and relevant information relating to the working.

Further, the FFO that is funds from operation was calculated and with this it was analysed

that company was effective in using its funds from operations. This is a total debt leverage ratio

which assist Qube Holding in assessing the risk of the company. this is necessary to be

calculated as when the company is not able to analyse its risk then strategies cannot be

formulated in proper and effective manner. In the present case as well the company is not having

higher FFO as compared the past performance.

In addition to this, free operation cash flow was also calculated in order to analyse the

fact that how much money is being left or is being generated from the normal business

operations (Dempsey, 2019). The ratio of free cash flow to debt signifies the amount of debt

which will be paid in current year in case all the free cash flow will be used for payment of debt.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

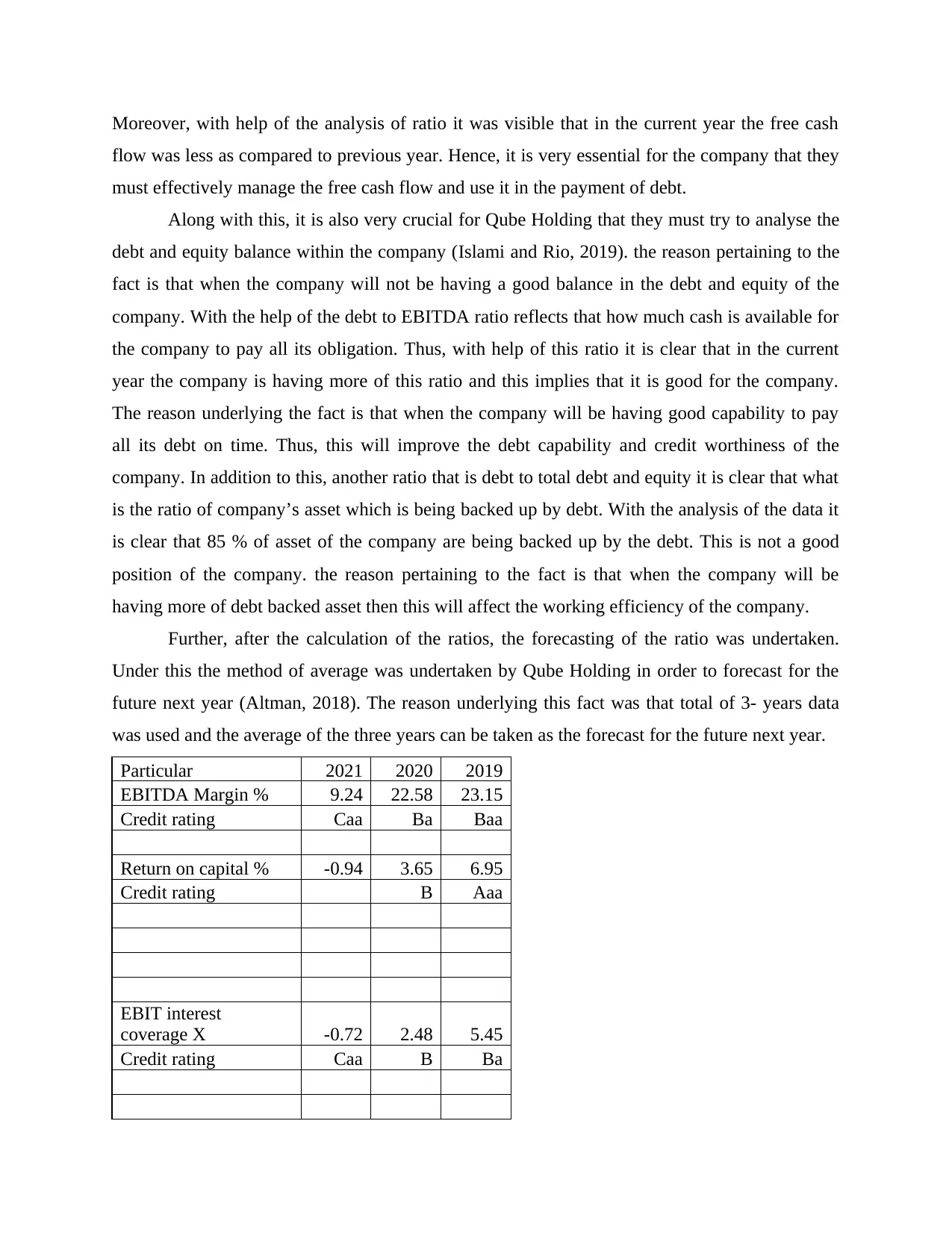

Moreover, with help of the analysis of ratio it was visible that in the current year the free cash

flow was less as compared to previous year. Hence, it is very essential for the company that they

must effectively manage the free cash flow and use it in the payment of debt.

Along with this, it is also very crucial for Qube Holding that they must try to analyse the

debt and equity balance within the company (Islami and Rio, 2019). the reason pertaining to the

fact is that when the company will not be having a good balance in the debt and equity of the

company. With the help of the debt to EBITDA ratio reflects that how much cash is available for

the company to pay all its obligation. Thus, with help of this ratio it is clear that in the current

year the company is having more of this ratio and this implies that it is good for the company.

The reason underlying the fact is that when the company will be having good capability to pay

all its debt on time. Thus, this will improve the debt capability and credit worthiness of the

company. In addition to this, another ratio that is debt to total debt and equity it is clear that what

is the ratio of company’s asset which is being backed up by debt. With the analysis of the data it

is clear that 85 % of asset of the company are being backed up by the debt. This is not a good

position of the company. the reason pertaining to the fact is that when the company will be

having more of debt backed asset then this will affect the working efficiency of the company.

Further, after the calculation of the ratios, the forecasting of the ratio was undertaken.

Under this the method of average was undertaken by Qube Holding in order to forecast for the

future next year (Altman, 2018). The reason underlying this fact was that total of 3- years data

was used and the average of the three years can be taken as the forecast for the future next year.

Particular 2021 2020 2019

EBITDA Margin % 9.24 22.58 23.15

Credit rating Caa Ba Baa

Return on capital % -0.94 3.65 6.95

Credit rating B Aaa

EBIT interest

coverage X -0.72 2.48 5.45

Credit rating Caa B Ba

flow was less as compared to previous year. Hence, it is very essential for the company that they

must effectively manage the free cash flow and use it in the payment of debt.

Along with this, it is also very crucial for Qube Holding that they must try to analyse the

debt and equity balance within the company (Islami and Rio, 2019). the reason pertaining to the

fact is that when the company will not be having a good balance in the debt and equity of the

company. With the help of the debt to EBITDA ratio reflects that how much cash is available for

the company to pay all its obligation. Thus, with help of this ratio it is clear that in the current

year the company is having more of this ratio and this implies that it is good for the company.

The reason underlying the fact is that when the company will be having good capability to pay

all its debt on time. Thus, this will improve the debt capability and credit worthiness of the

company. In addition to this, another ratio that is debt to total debt and equity it is clear that what

is the ratio of company’s asset which is being backed up by debt. With the analysis of the data it

is clear that 85 % of asset of the company are being backed up by the debt. This is not a good

position of the company. the reason pertaining to the fact is that when the company will be

having more of debt backed asset then this will affect the working efficiency of the company.

Further, after the calculation of the ratios, the forecasting of the ratio was undertaken.

Under this the method of average was undertaken by Qube Holding in order to forecast for the

future next year (Altman, 2018). The reason underlying this fact was that total of 3- years data

was used and the average of the three years can be taken as the forecast for the future next year.

Particular 2021 2020 2019

EBITDA Margin % 9.24 22.58 23.15

Credit rating Caa Ba Baa

Return on capital % -0.94 3.65 6.95

Credit rating B Aaa

EBIT interest

coverage X -0.72 2.48 5.45

Credit rating Caa B Ba

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

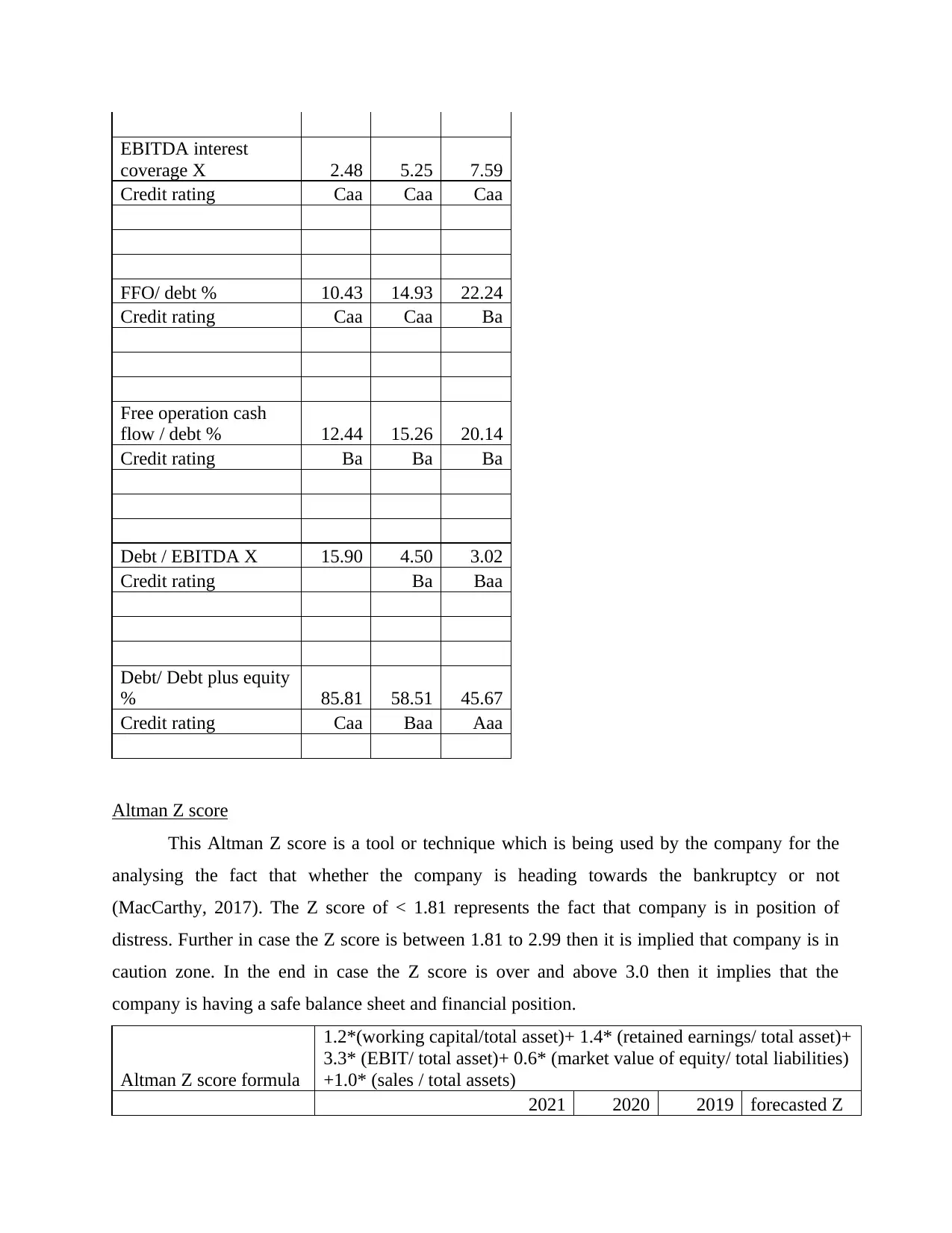

EBITDA interest

coverage X 2.48 5.25 7.59

Credit rating Caa Caa Caa

FFO/ debt % 10.43 14.93 22.24

Credit rating Caa Caa Ba

Free operation cash

flow / debt % 12.44 15.26 20.14

Credit rating Ba Ba Ba

Debt / EBITDA X 15.90 4.50 3.02

Credit rating Ba Baa

Debt/ Debt plus equity

% 85.81 58.51 45.67

Credit rating Caa Baa Aaa

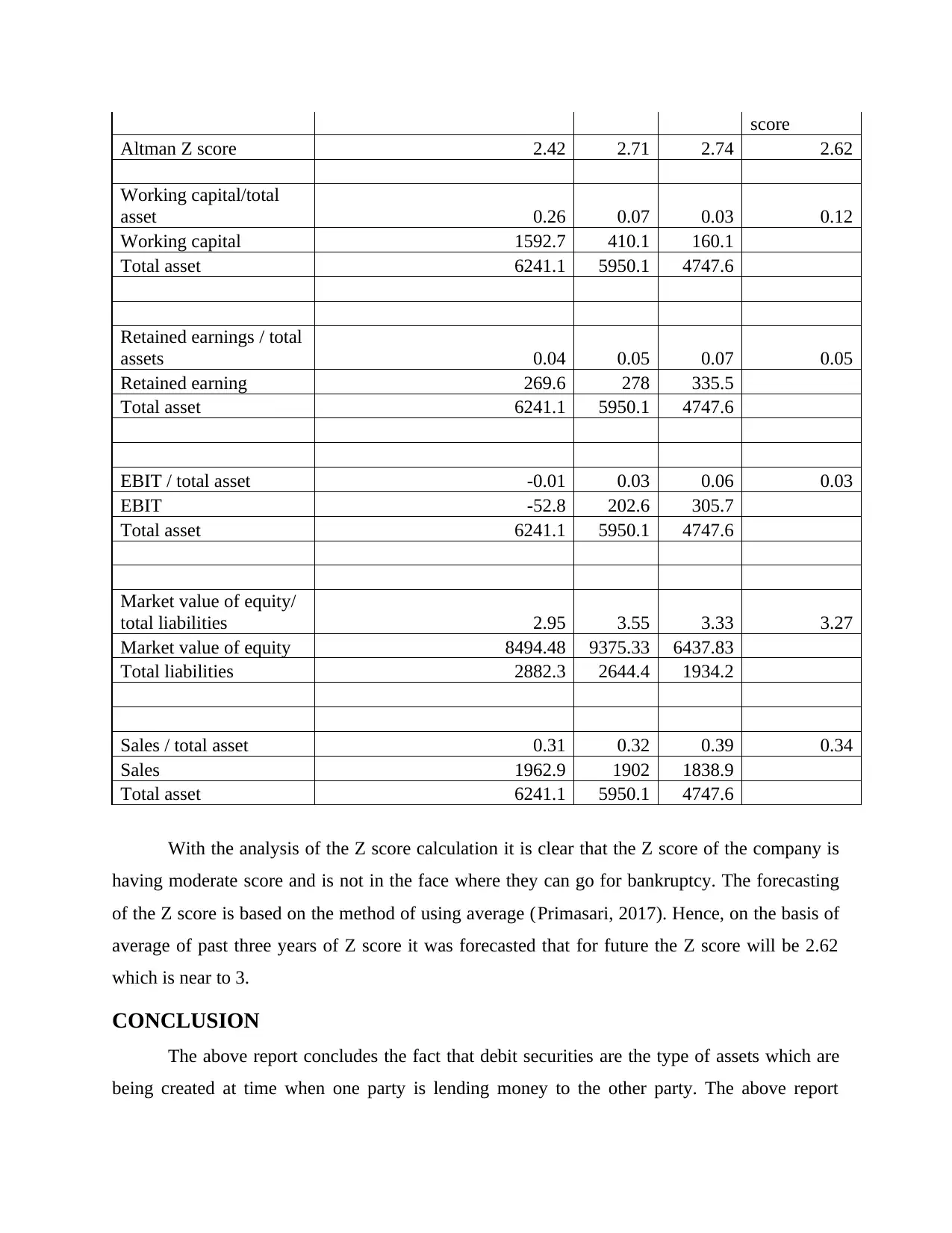

Altman Z score

This Altman Z score is a tool or technique which is being used by the company for the

analysing the fact that whether the company is heading towards the bankruptcy or not

(MacCarthy, 2017). The Z score of < 1.81 represents the fact that company is in position of

distress. Further in case the Z score is between 1.81 to 2.99 then it is implied that company is in

caution zone. In the end in case the Z score is over and above 3.0 then it implies that the

company is having a safe balance sheet and financial position.

Altman Z score formula

1.2*(working capital/total asset)+ 1.4* (retained earnings/ total asset)+

3.3* (EBIT/ total asset)+ 0.6* (market value of equity/ total liabilities)

+1.0* (sales / total assets)

2021 2020 2019 forecasted Z

coverage X 2.48 5.25 7.59

Credit rating Caa Caa Caa

FFO/ debt % 10.43 14.93 22.24

Credit rating Caa Caa Ba

Free operation cash

flow / debt % 12.44 15.26 20.14

Credit rating Ba Ba Ba

Debt / EBITDA X 15.90 4.50 3.02

Credit rating Ba Baa

Debt/ Debt plus equity

% 85.81 58.51 45.67

Credit rating Caa Baa Aaa

Altman Z score

This Altman Z score is a tool or technique which is being used by the company for the

analysing the fact that whether the company is heading towards the bankruptcy or not

(MacCarthy, 2017). The Z score of < 1.81 represents the fact that company is in position of

distress. Further in case the Z score is between 1.81 to 2.99 then it is implied that company is in

caution zone. In the end in case the Z score is over and above 3.0 then it implies that the

company is having a safe balance sheet and financial position.

Altman Z score formula

1.2*(working capital/total asset)+ 1.4* (retained earnings/ total asset)+

3.3* (EBIT/ total asset)+ 0.6* (market value of equity/ total liabilities)

+1.0* (sales / total assets)

2021 2020 2019 forecasted Z

score

Altman Z score 2.42 2.71 2.74 2.62

Working capital/total

asset 0.26 0.07 0.03 0.12

Working capital 1592.7 410.1 160.1

Total asset 6241.1 5950.1 4747.6

Retained earnings / total

assets 0.04 0.05 0.07 0.05

Retained earning 269.6 278 335.5

Total asset 6241.1 5950.1 4747.6

EBIT / total asset -0.01 0.03 0.06 0.03

EBIT -52.8 202.6 305.7

Total asset 6241.1 5950.1 4747.6

Market value of equity/

total liabilities 2.95 3.55 3.33 3.27

Market value of equity 8494.48 9375.33 6437.83

Total liabilities 2882.3 2644.4 1934.2

Sales / total asset 0.31 0.32 0.39 0.34

Sales 1962.9 1902 1838.9

Total asset 6241.1 5950.1 4747.6

With the analysis of the Z score calculation it is clear that the Z score of the company is

having moderate score and is not in the face where they can go for bankruptcy. The forecasting

of the Z score is based on the method of using average (Primasari, 2017). Hence, on the basis of

average of past three years of Z score it was forecasted that for future the Z score will be 2.62

which is near to 3.

CONCLUSION

The above report concludes the fact that debit securities are the type of assets which are

being created at time when one party is lending money to the other party. The above report

Altman Z score 2.42 2.71 2.74 2.62

Working capital/total

asset 0.26 0.07 0.03 0.12

Working capital 1592.7 410.1 160.1

Total asset 6241.1 5950.1 4747.6

Retained earnings / total

assets 0.04 0.05 0.07 0.05

Retained earning 269.6 278 335.5

Total asset 6241.1 5950.1 4747.6

EBIT / total asset -0.01 0.03 0.06 0.03

EBIT -52.8 202.6 305.7

Total asset 6241.1 5950.1 4747.6

Market value of equity/

total liabilities 2.95 3.55 3.33 3.27

Market value of equity 8494.48 9375.33 6437.83

Total liabilities 2882.3 2644.4 1934.2

Sales / total asset 0.31 0.32 0.39 0.34

Sales 1962.9 1902 1838.9

Total asset 6241.1 5950.1 4747.6

With the analysis of the Z score calculation it is clear that the Z score of the company is

having moderate score and is not in the face where they can go for bankruptcy. The forecasting

of the Z score is based on the method of using average (Primasari, 2017). Hence, on the basis of

average of past three years of Z score it was forecasted that for future the Z score will be 2.62

which is near to 3.

CONCLUSION

The above report concludes the fact that debit securities are the type of assets which are

being created at time when one party is lending money to the other party. The above report

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

concludes that the use of ratio analysis is very important for the business as this will assist them

in analysing and evaluating the financial position of the company. the reason underlying this fact

is that when the company will be having proper calculation based on ratio then they can decide

that how to improve the working. Further it was evaluated that use of Z score is important for

analysing that whether the company is in phase of bankruptcy or not. But with the calculation it

is analysed that Qube Holding is not in phase of bankruptcy.

in analysing and evaluating the financial position of the company. the reason underlying this fact

is that when the company will be having proper calculation based on ratio then they can decide

that how to improve the working. Further it was evaluated that use of Z score is important for

analysing that whether the company is in phase of bankruptcy or not. But with the calculation it

is analysed that Qube Holding is not in phase of bankruptcy.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

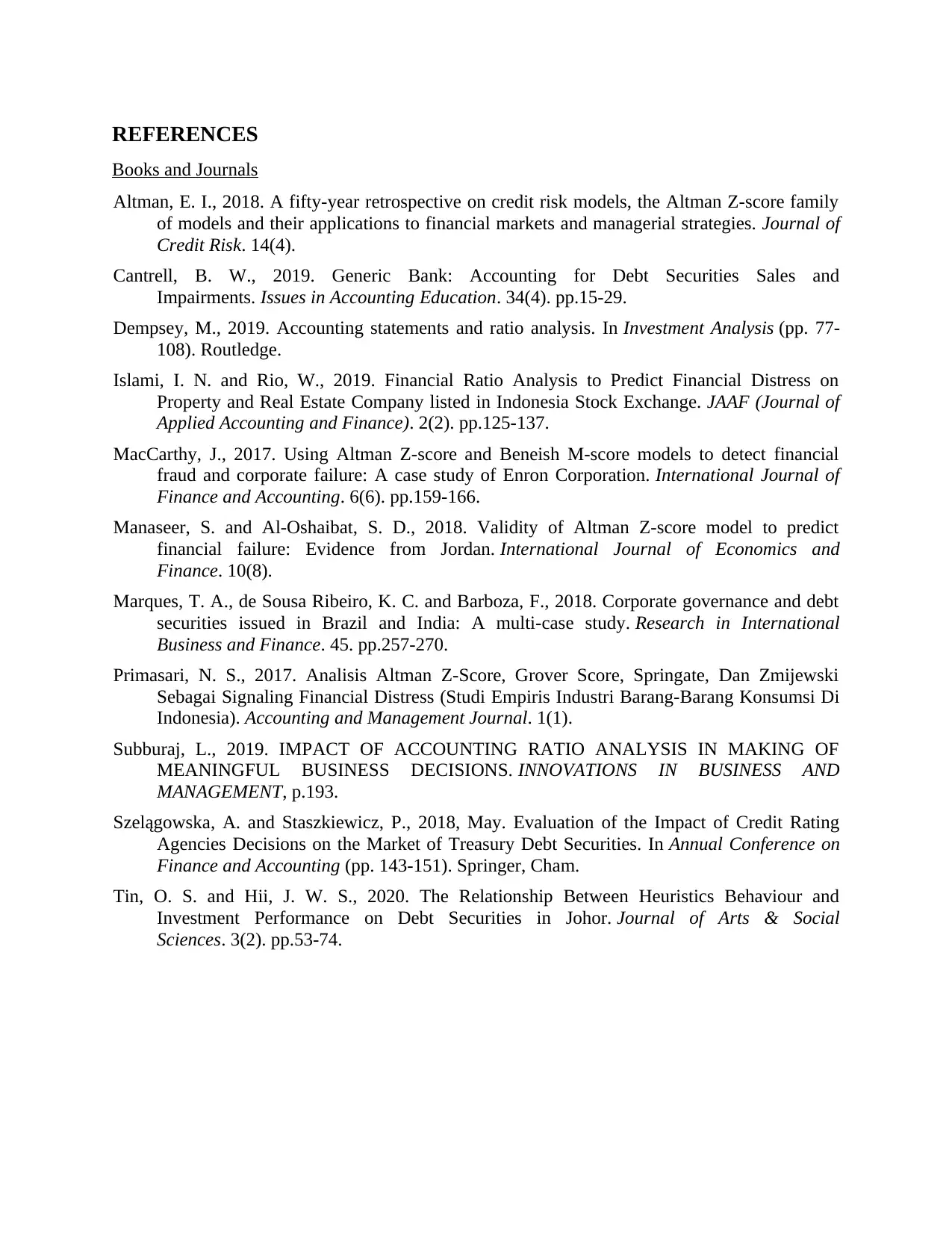

Books and Journals

Altman, E. I., 2018. A fifty-year retrospective on credit risk models, the Altman Z-score family

of models and their applications to financial markets and managerial strategies. Journal of

Credit Risk. 14(4).

Cantrell, B. W., 2019. Generic Bank: Accounting for Debt Securities Sales and

Impairments. Issues in Accounting Education. 34(4). pp.15-29.

Dempsey, M., 2019. Accounting statements and ratio analysis. In Investment Analysis (pp. 77-

108). Routledge.

Islami, I. N. and Rio, W., 2019. Financial Ratio Analysis to Predict Financial Distress on

Property and Real Estate Company listed in Indonesia Stock Exchange. JAAF (Journal of

Applied Accounting and Finance). 2(2). pp.125-137.

MacCarthy, J., 2017. Using Altman Z-score and Beneish M-score models to detect financial

fraud and corporate failure: A case study of Enron Corporation. International Journal of

Finance and Accounting. 6(6). pp.159-166.

Manaseer, S. and Al-Oshaibat, S. D., 2018. Validity of Altman Z-score model to predict

financial failure: Evidence from Jordan. International Journal of Economics and

Finance. 10(8).

Marques, T. A., de Sousa Ribeiro, K. C. and Barboza, F., 2018. Corporate governance and debt

securities issued in Brazil and India: A multi-case study. Research in International

Business and Finance. 45. pp.257-270.

Primasari, N. S., 2017. Analisis Altman Z-Score, Grover Score, Springate, Dan Zmijewski

Sebagai Signaling Financial Distress (Studi Empiris Industri Barang-Barang Konsumsi Di

Indonesia). Accounting and Management Journal. 1(1).

Subburaj, L., 2019. IMPACT OF ACCOUNTING RATIO ANALYSIS IN MAKING OF

MEANINGFUL BUSINESS DECISIONS. INNOVATIONS IN BUSINESS AND

MANAGEMENT, p.193.

Szelągowska, A. and Staszkiewicz, P., 2018, May. Evaluation of the Impact of Credit Rating

Agencies Decisions on the Market of Treasury Debt Securities. In Annual Conference on

Finance and Accounting (pp. 143-151). Springer, Cham.

Tin, O. S. and Hii, J. W. S., 2020. The Relationship Between Heuristics Behaviour and

Investment Performance on Debt Securities in Johor. Journal of Arts & Social

Sciences. 3(2). pp.53-74.

Books and Journals

Altman, E. I., 2018. A fifty-year retrospective on credit risk models, the Altman Z-score family

of models and their applications to financial markets and managerial strategies. Journal of

Credit Risk. 14(4).

Cantrell, B. W., 2019. Generic Bank: Accounting for Debt Securities Sales and

Impairments. Issues in Accounting Education. 34(4). pp.15-29.

Dempsey, M., 2019. Accounting statements and ratio analysis. In Investment Analysis (pp. 77-

108). Routledge.

Islami, I. N. and Rio, W., 2019. Financial Ratio Analysis to Predict Financial Distress on

Property and Real Estate Company listed in Indonesia Stock Exchange. JAAF (Journal of

Applied Accounting and Finance). 2(2). pp.125-137.

MacCarthy, J., 2017. Using Altman Z-score and Beneish M-score models to detect financial

fraud and corporate failure: A case study of Enron Corporation. International Journal of

Finance and Accounting. 6(6). pp.159-166.

Manaseer, S. and Al-Oshaibat, S. D., 2018. Validity of Altman Z-score model to predict

financial failure: Evidence from Jordan. International Journal of Economics and

Finance. 10(8).

Marques, T. A., de Sousa Ribeiro, K. C. and Barboza, F., 2018. Corporate governance and debt

securities issued in Brazil and India: A multi-case study. Research in International

Business and Finance. 45. pp.257-270.

Primasari, N. S., 2017. Analisis Altman Z-Score, Grover Score, Springate, Dan Zmijewski

Sebagai Signaling Financial Distress (Studi Empiris Industri Barang-Barang Konsumsi Di

Indonesia). Accounting and Management Journal. 1(1).

Subburaj, L., 2019. IMPACT OF ACCOUNTING RATIO ANALYSIS IN MAKING OF

MEANINGFUL BUSINESS DECISIONS. INNOVATIONS IN BUSINESS AND

MANAGEMENT, p.193.

Szelągowska, A. and Staszkiewicz, P., 2018, May. Evaluation of the Impact of Credit Rating

Agencies Decisions on the Market of Treasury Debt Securities. In Annual Conference on

Finance and Accounting (pp. 143-151). Springer, Cham.

Tin, O. S. and Hii, J. W. S., 2020. The Relationship Between Heuristics Behaviour and

Investment Performance on Debt Securities in Johor. Journal of Arts & Social

Sciences. 3(2). pp.53-74.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.