BUS 301: Decision Support Tools: Assignment Analysis and Solutions

VerifiedAdded on 2020/04/01

|20

|1472

|33

Homework Assignment

AI Summary

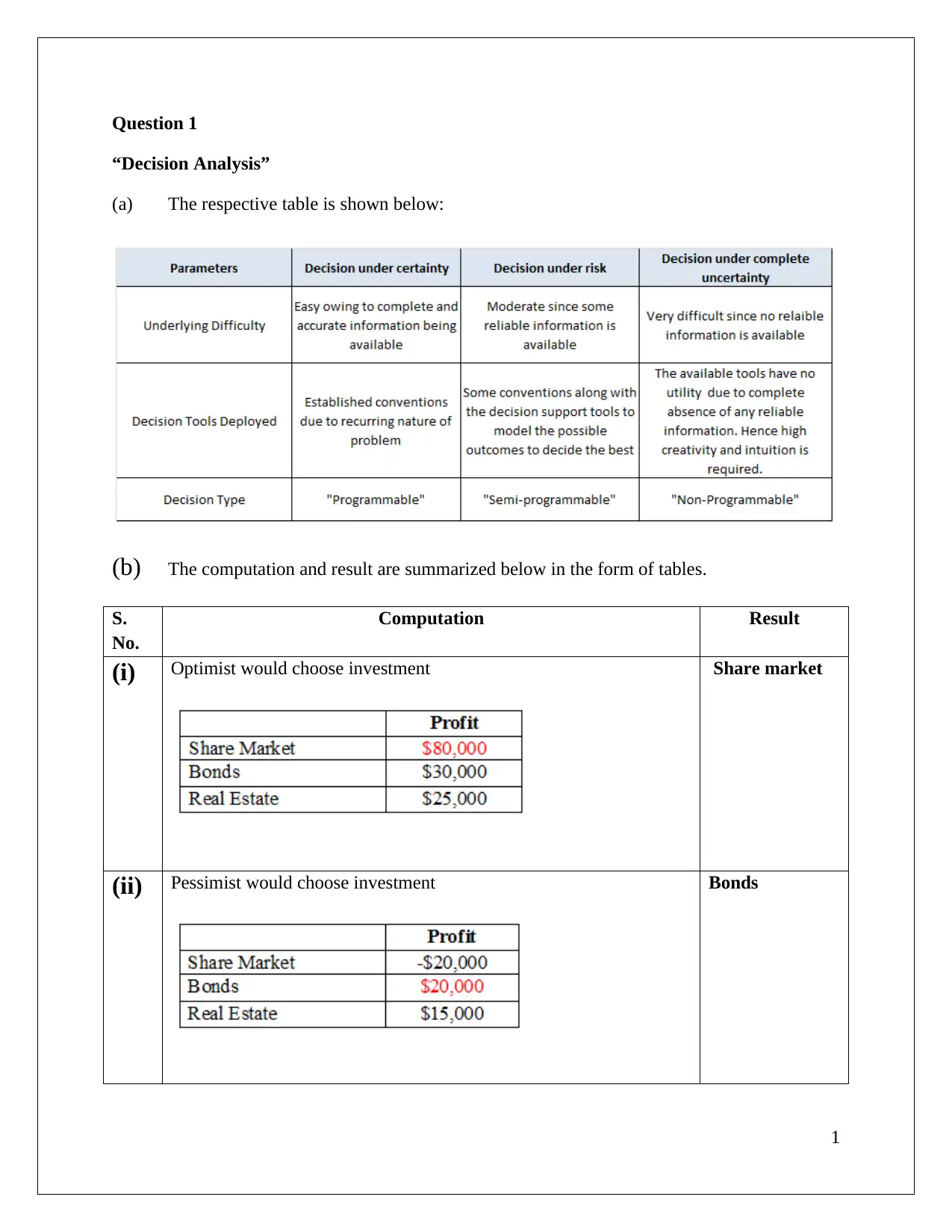

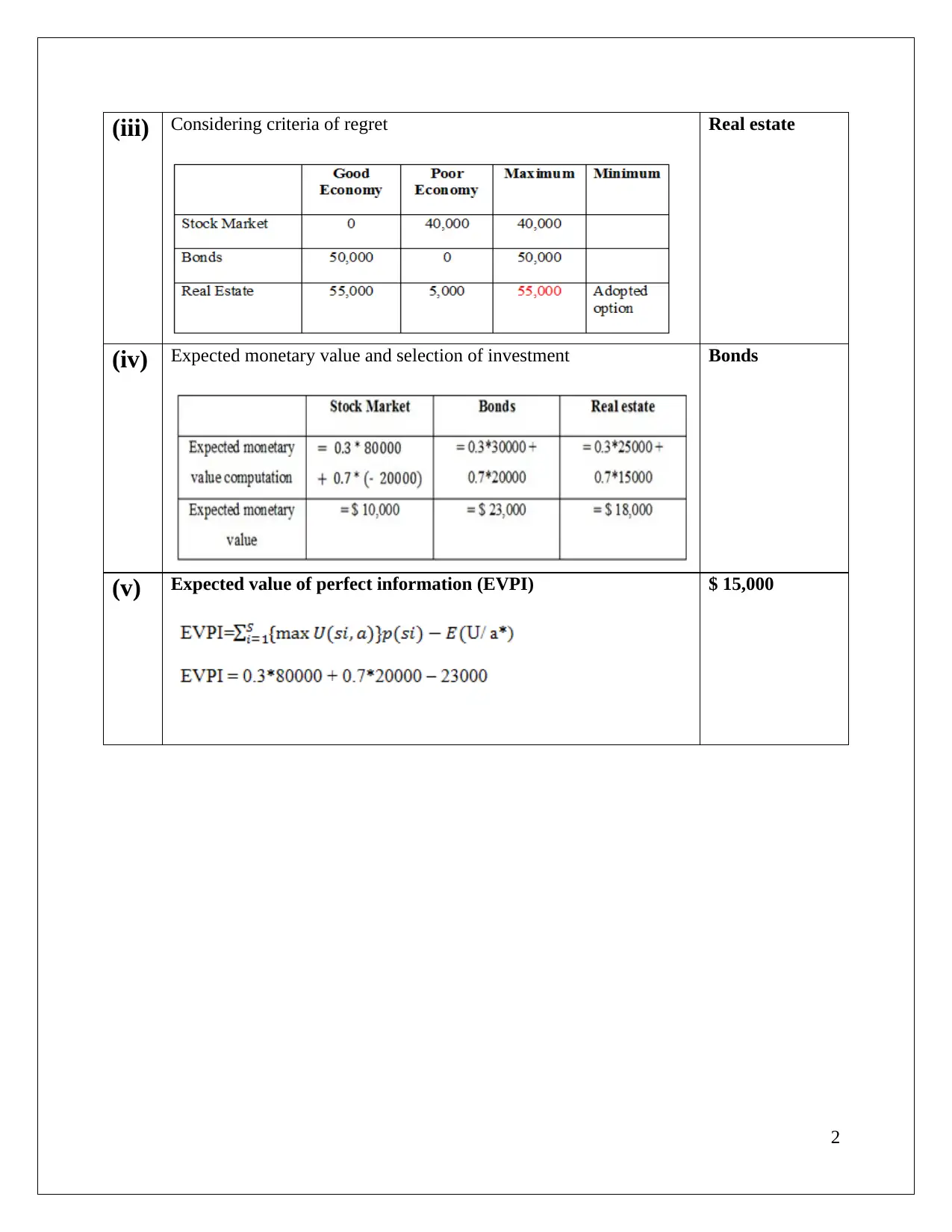

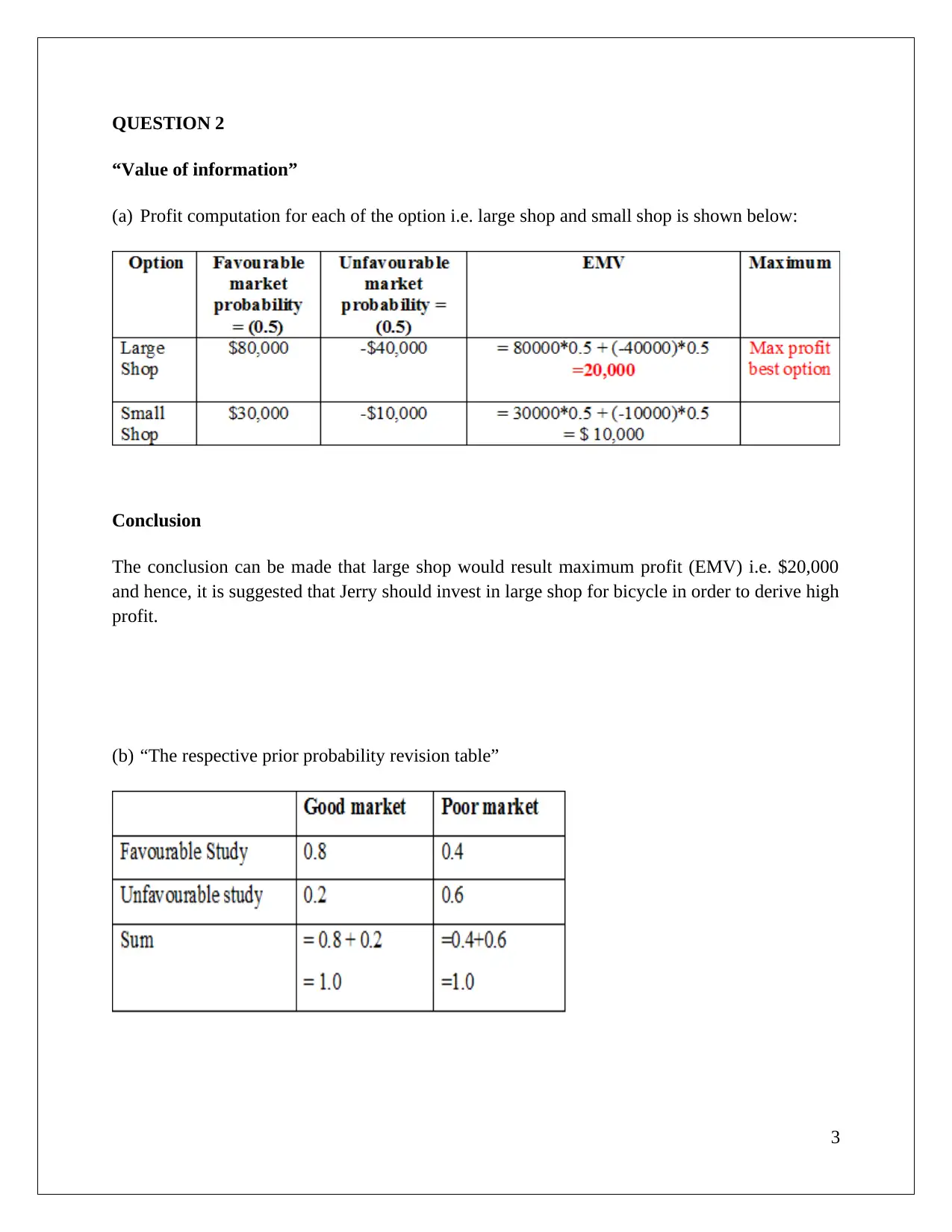

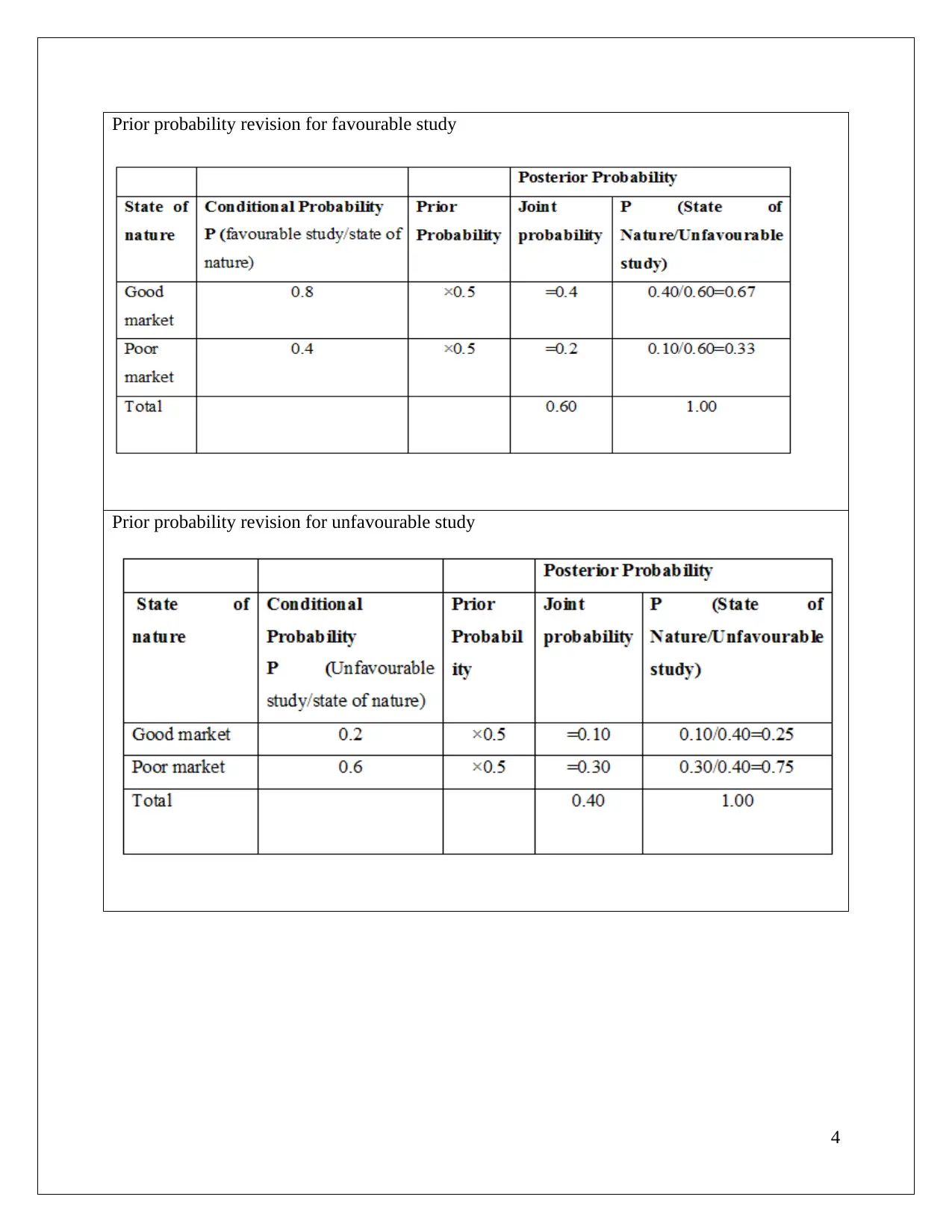

This document presents a comprehensive solution to a Decision Support Tools assignment, addressing various aspects of business decision-making. The assignment covers decision analysis, including the selection of investments based on different criteria and the value of information. It also includes a Monte Carlo simulation to analyze profit margins and a regression analysis to determine the impact of machine hours and batches on overhead costs. Furthermore, the document explores CVP analysis, determining break-even points and profit levels under different scenarios. The solution incorporates calculations, tables, and conclusions to provide a complete understanding of each concept, referencing relevant business research methods and statistical techniques.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.