Assignment about What is Your Definition of Accounting?

VerifiedAdded on 2022/09/13

|16

|2214

|13

Assignment

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ACCOUNTING

Accounting

April 6

2020

Accounting

April 6

2020

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACCOUNTING 2

Contents

Question 1...................................................................................................................................................1

Question 2...................................................................................................................................................4

Part A......................................................................................................................................................4

Part B.......................................................................................................................................................6

Part C...........................................................................................................................................................8

Question 3.............................................................................................................................................10

Bibliography..............................................................................................................................................13

Contents

Question 1...................................................................................................................................................1

Question 2...................................................................................................................................................4

Part A......................................................................................................................................................4

Part B.......................................................................................................................................................6

Part C...........................................................................................................................................................8

Question 3.............................................................................................................................................10

Bibliography..............................................................................................................................................13

ACCOUNTING 3

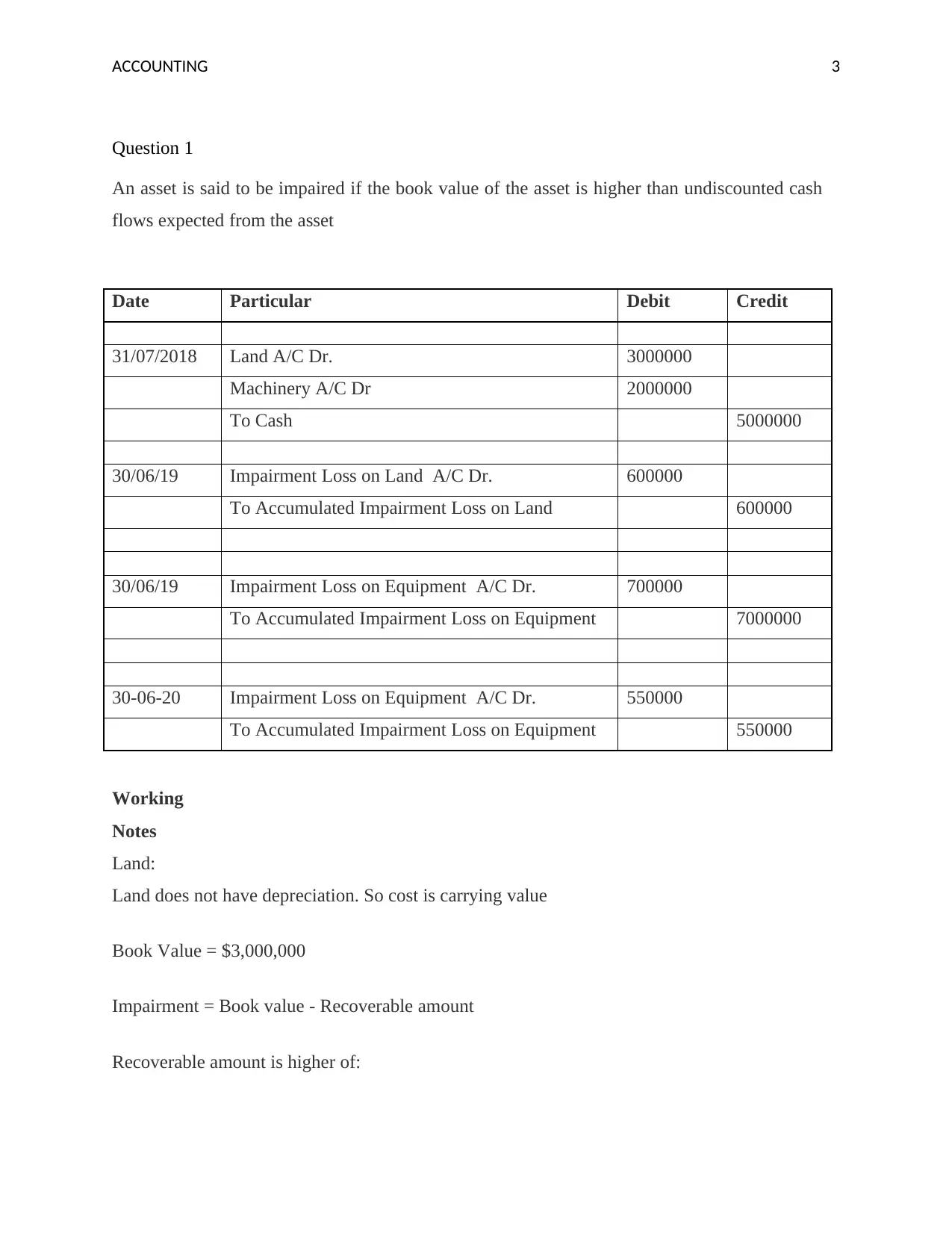

Question 1

An asset is said to be impaired if the book value of the asset is higher than undiscounted cash

flows expected from the asset

Date Particular Debit Credit

31/07/2018 Land A/C Dr. 3000000

Machinery A/C Dr 2000000

To Cash 5000000

30/06/19 Impairment Loss on Land A/C Dr. 600000

To Accumulated Impairment Loss on Land 600000

30/06/19 Impairment Loss on Equipment A/C Dr. 700000

To Accumulated Impairment Loss on Equipment 7000000

30-06-20 Impairment Loss on Equipment A/C Dr. 550000

To Accumulated Impairment Loss on Equipment 550000

Working

Notes

Land:

Land does not have depreciation. So cost is carrying value

Book Value = $3,000,000

Impairment = Book value - Recoverable amount

Recoverable amount is higher of:

Question 1

An asset is said to be impaired if the book value of the asset is higher than undiscounted cash

flows expected from the asset

Date Particular Debit Credit

31/07/2018 Land A/C Dr. 3000000

Machinery A/C Dr 2000000

To Cash 5000000

30/06/19 Impairment Loss on Land A/C Dr. 600000

To Accumulated Impairment Loss on Land 600000

30/06/19 Impairment Loss on Equipment A/C Dr. 700000

To Accumulated Impairment Loss on Equipment 7000000

30-06-20 Impairment Loss on Equipment A/C Dr. 550000

To Accumulated Impairment Loss on Equipment 550000

Working

Notes

Land:

Land does not have depreciation. So cost is carrying value

Book Value = $3,000,000

Impairment = Book value - Recoverable amount

Recoverable amount is higher of:

ACCOUNTING 4

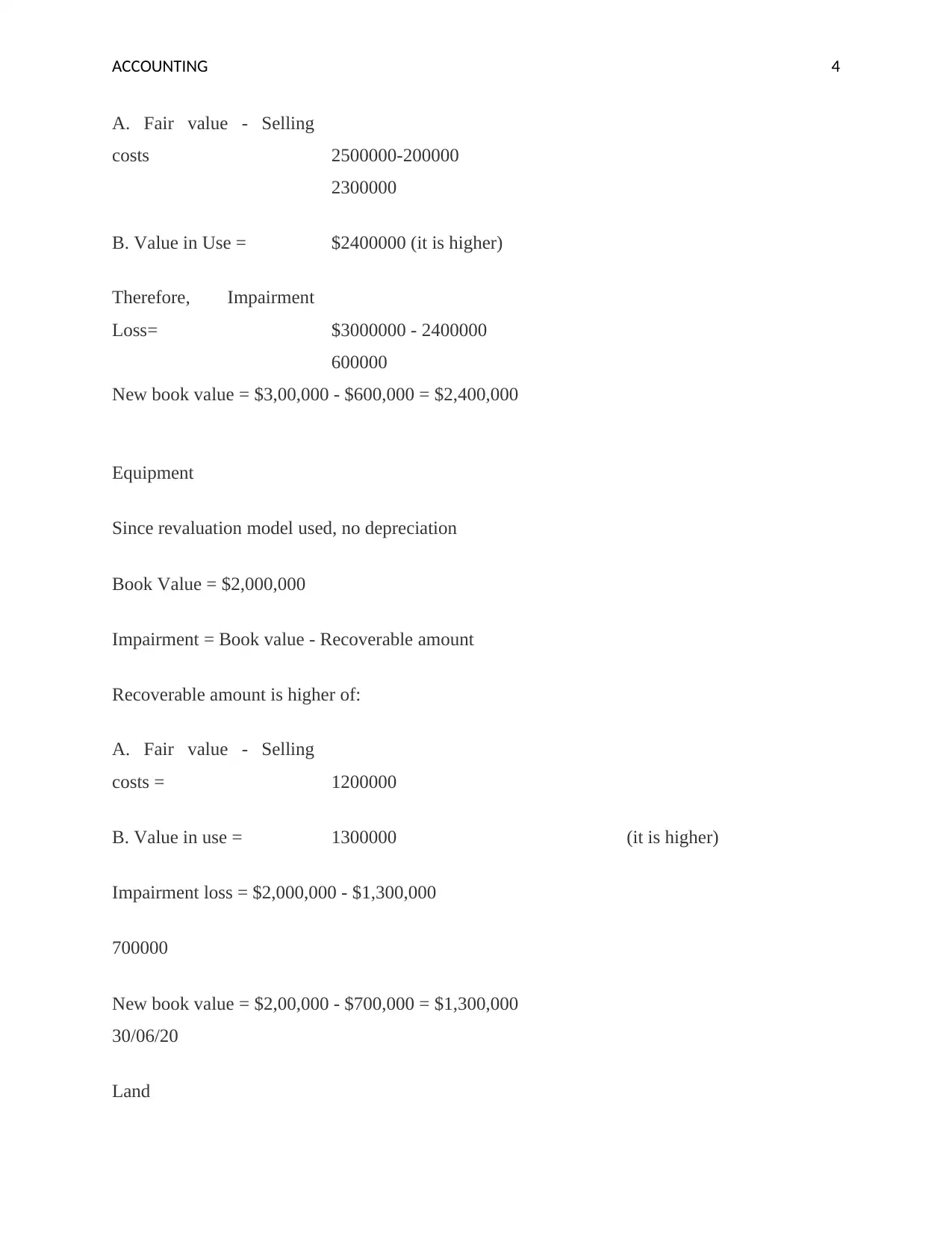

A. Fair value - Selling

costs 2500000-200000

2300000

B. Value in Use = $2400000 (it is higher)

Therefore, Impairment

Loss= $3000000 - 2400000

600000

New book value = $3,00,000 - $600,000 = $2,400,000

Equipment

Since revaluation model used, no depreciation

Book Value = $2,000,000

Impairment = Book value - Recoverable amount

Recoverable amount is higher of:

A. Fair value - Selling

costs = 1200000

B. Value in use = 1300000 (it is higher)

Impairment loss = $2,000,000 - $1,300,000

700000

New book value = $2,00,000 - $700,000 = $1,300,000

30/06/20

Land

A. Fair value - Selling

costs 2500000-200000

2300000

B. Value in Use = $2400000 (it is higher)

Therefore, Impairment

Loss= $3000000 - 2400000

600000

New book value = $3,00,000 - $600,000 = $2,400,000

Equipment

Since revaluation model used, no depreciation

Book Value = $2,000,000

Impairment = Book value - Recoverable amount

Recoverable amount is higher of:

A. Fair value - Selling

costs = 1200000

B. Value in use = 1300000 (it is higher)

Impairment loss = $2,000,000 - $1,300,000

700000

New book value = $2,00,000 - $700,000 = $1,300,000

30/06/20

Land

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACCOUNTING 5

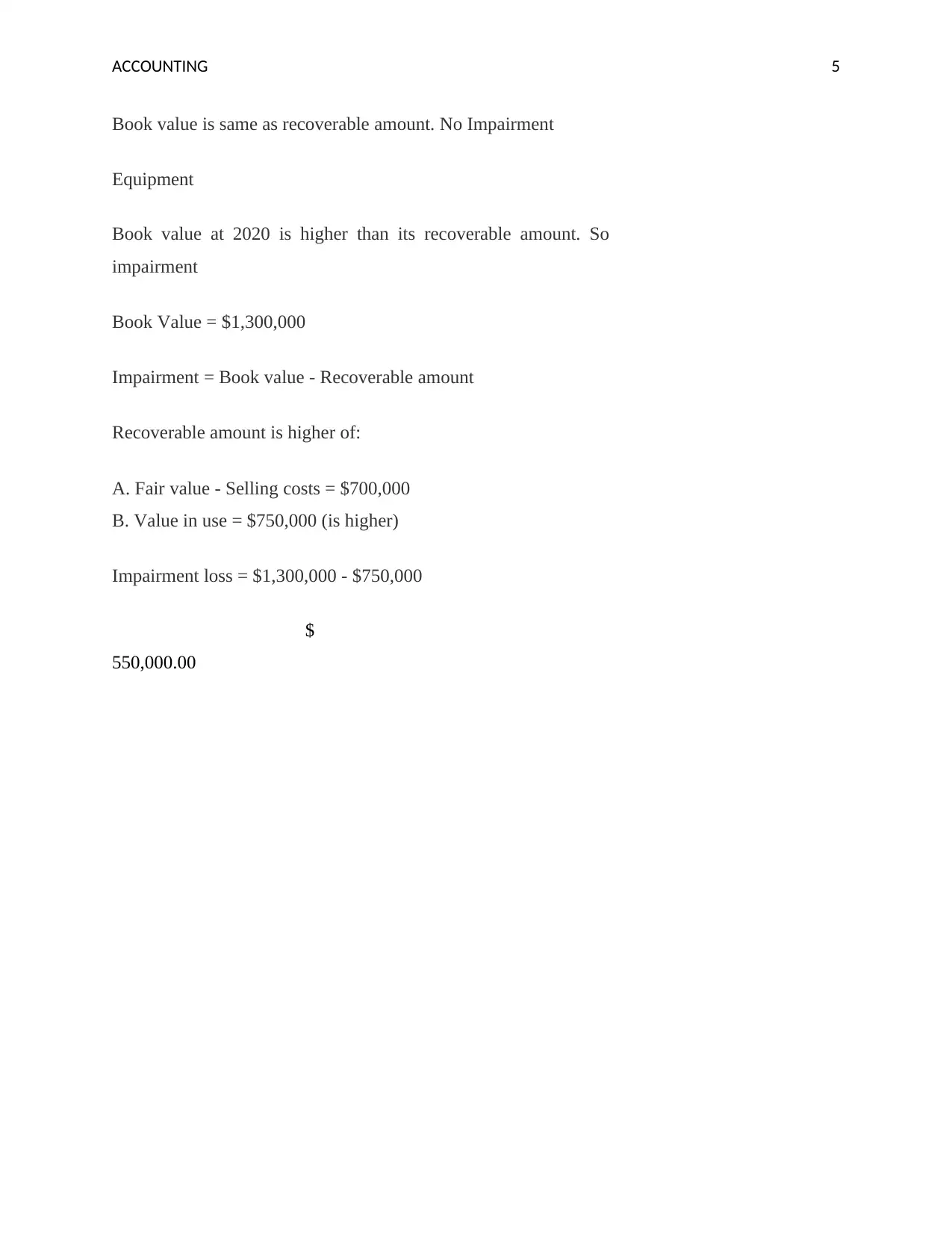

Book value is same as recoverable amount. No Impairment

Equipment

Book value at 2020 is higher than its recoverable amount. So

impairment

Book Value = $1,300,000

Impairment = Book value - Recoverable amount

Recoverable amount is higher of:

A. Fair value - Selling costs = $700,000

B. Value in use = $750,000 (is higher)

Impairment loss = $1,300,000 - $750,000

$

550,000.00

Book value is same as recoverable amount. No Impairment

Equipment

Book value at 2020 is higher than its recoverable amount. So

impairment

Book Value = $1,300,000

Impairment = Book value - Recoverable amount

Recoverable amount is higher of:

A. Fair value - Selling costs = $700,000

B. Value in use = $750,000 (is higher)

Impairment loss = $1,300,000 - $750,000

$

550,000.00

ACCOUNTING 6

Question 2

Part A

Provisions of AASB 16 'Leases'

In compliance with paragraph 9, at the very outset, an agency must determine whether the

provider is a lease or includes a lease. If, in return for payment, the arrangement allows for the

right to manage the use of defined properties, it can be claimed that this deal is a lease or a lease.

Section B9-B31 provides guidelines for the assessment of a contract to determine if a contract

does or does not contain a mortgage. In para B13 the property is defined as the expressly referred

asset or indirectly stated asset for the customer's use when the property is available1.

Para B9 notes that if the organizations have the following two items in the usage period, a

contract protects the right to monitor the use of the defined asset:

The right to significantly gain all economic benefits through the use of the resources

defined

Ability to use the defined commodity directly2

The Para line B22, where the business is entitled to economic advantages under the stated

restrictions of the customer's right to use services, it does not have the right to adversity in the

usage of the existing asset in the pursuit of substantive financial benefits. B22 When an

arrangement stipulates, for instance, that a corporation can only operate a car for a certain

number of miles within a term of operation; the entity shall not increase the expense of driving a

vehicle within the specified kilometer if the deal only pays for a certain number of miles during

the duration of operation.3.

1Michelle JoubertLLeandaGarvie, and Gabrielle Parle. "Implications of the New Accounting Standard for Leases

AASB 16 (IFRS 16) with the Inclusion of Operating Leases in the Balance Sheet." (2017), 15.2 The Journal of New

Business Ideas & Trends 1-11.

2SilvanaFilomenaSECINARO et al. "Relevance in the Application of IFRS 16 for Financial Statements: Empirical

Evidence the Impact of the Financial Method in SMEs." (2020): 1-15.

3David Bond, Brett Govendir, and Peter Wells. "An evaluation of asset impairment decisions by Australian firms

and whether this was impacted by AASB 136." (2016).

Question 2

Part A

Provisions of AASB 16 'Leases'

In compliance with paragraph 9, at the very outset, an agency must determine whether the

provider is a lease or includes a lease. If, in return for payment, the arrangement allows for the

right to manage the use of defined properties, it can be claimed that this deal is a lease or a lease.

Section B9-B31 provides guidelines for the assessment of a contract to determine if a contract

does or does not contain a mortgage. In para B13 the property is defined as the expressly referred

asset or indirectly stated asset for the customer's use when the property is available1.

Para B9 notes that if the organizations have the following two items in the usage period, a

contract protects the right to monitor the use of the defined asset:

The right to significantly gain all economic benefits through the use of the resources

defined

Ability to use the defined commodity directly2

The Para line B22, where the business is entitled to economic advantages under the stated

restrictions of the customer's right to use services, it does not have the right to adversity in the

usage of the existing asset in the pursuit of substantive financial benefits. B22 When an

arrangement stipulates, for instance, that a corporation can only operate a car for a certain

number of miles within a term of operation; the entity shall not increase the expense of driving a

vehicle within the specified kilometer if the deal only pays for a certain number of miles during

the duration of operation.3.

1Michelle JoubertLLeandaGarvie, and Gabrielle Parle. "Implications of the New Accounting Standard for Leases

AASB 16 (IFRS 16) with the Inclusion of Operating Leases in the Balance Sheet." (2017), 15.2 The Journal of New

Business Ideas & Trends 1-11.

2SilvanaFilomenaSECINARO et al. "Relevance in the Application of IFRS 16 for Financial Statements: Empirical

Evidence the Impact of the Financial Method in SMEs." (2020): 1-15.

3David Bond, Brett Govendir, and Peter Wells. "An evaluation of asset impairment decisions by Australian firms

and whether this was impacted by AASB 136." (2016).

ACCOUNTING 7

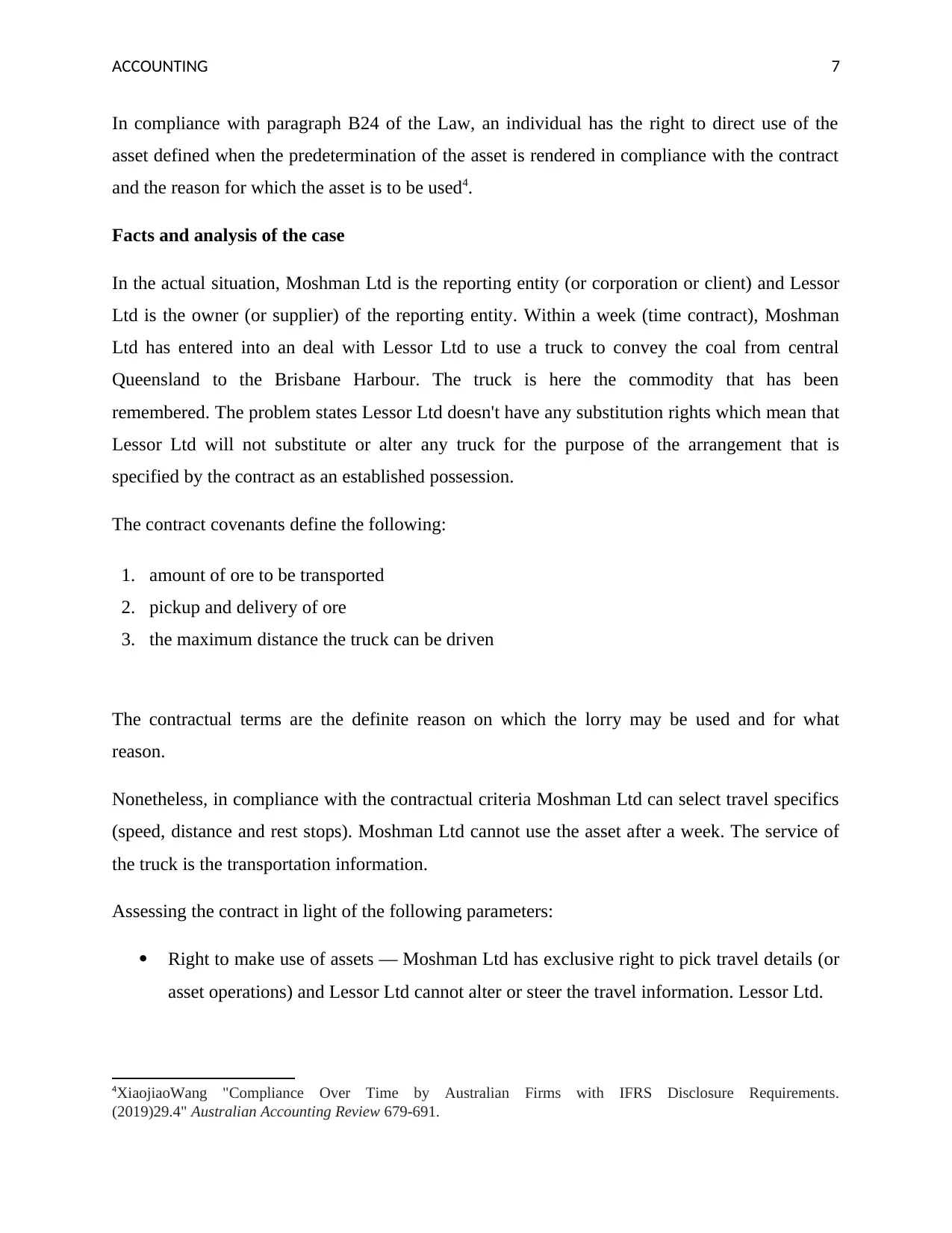

In compliance with paragraph B24 of the Law, an individual has the right to direct use of the

asset defined when the predetermination of the asset is rendered in compliance with the contract

and the reason for which the asset is to be used4.

Facts and analysis of the case

In the actual situation, Moshman Ltd is the reporting entity (or corporation or client) and Lessor

Ltd is the owner (or supplier) of the reporting entity. Within a week (time contract), Moshman

Ltd has entered into an deal with Lessor Ltd to use a truck to convey the coal from central

Queensland to the Brisbane Harbour. The truck is here the commodity that has been

remembered. The problem states Lessor Ltd doesn't have any substitution rights which mean that

Lessor Ltd will not substitute or alter any truck for the purpose of the arrangement that is

specified by the contract as an established possession.

The contract covenants define the following:

1. amount of ore to be transported

2. pickup and delivery of ore

3. the maximum distance the truck can be driven

The contractual terms are the definite reason on which the lorry may be used and for what

reason.

Nonetheless, in compliance with the contractual criteria Moshman Ltd can select travel specifics

(speed, distance and rest stops). Moshman Ltd cannot use the asset after a week. The service of

the truck is the transportation information.

Assessing the contract in light of the following parameters:

Right to make use of assets — Moshman Ltd has exclusive right to pick travel details (or

asset operations) and Lessor Ltd cannot alter or steer the travel information. Lessor Ltd.

4XiaojiaoWang "Compliance Over Time by Australian Firms with IFRS Disclosure Requirements.

(2019)29.4" Australian Accounting Review 679-691.

In compliance with paragraph B24 of the Law, an individual has the right to direct use of the

asset defined when the predetermination of the asset is rendered in compliance with the contract

and the reason for which the asset is to be used4.

Facts and analysis of the case

In the actual situation, Moshman Ltd is the reporting entity (or corporation or client) and Lessor

Ltd is the owner (or supplier) of the reporting entity. Within a week (time contract), Moshman

Ltd has entered into an deal with Lessor Ltd to use a truck to convey the coal from central

Queensland to the Brisbane Harbour. The truck is here the commodity that has been

remembered. The problem states Lessor Ltd doesn't have any substitution rights which mean that

Lessor Ltd will not substitute or alter any truck for the purpose of the arrangement that is

specified by the contract as an established possession.

The contract covenants define the following:

1. amount of ore to be transported

2. pickup and delivery of ore

3. the maximum distance the truck can be driven

The contractual terms are the definite reason on which the lorry may be used and for what

reason.

Nonetheless, in compliance with the contractual criteria Moshman Ltd can select travel specifics

(speed, distance and rest stops). Moshman Ltd cannot use the asset after a week. The service of

the truck is the transportation information.

Assessing the contract in light of the following parameters:

Right to make use of assets — Moshman Ltd has exclusive right to pick travel details (or

asset operations) and Lessor Ltd cannot alter or steer the travel information. Lessor Ltd.

4XiaojiaoWang "Compliance Over Time by Australian Firms with IFRS Disclosure Requirements.

(2019)29.4" Australian Accounting Review 679-691.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING 8

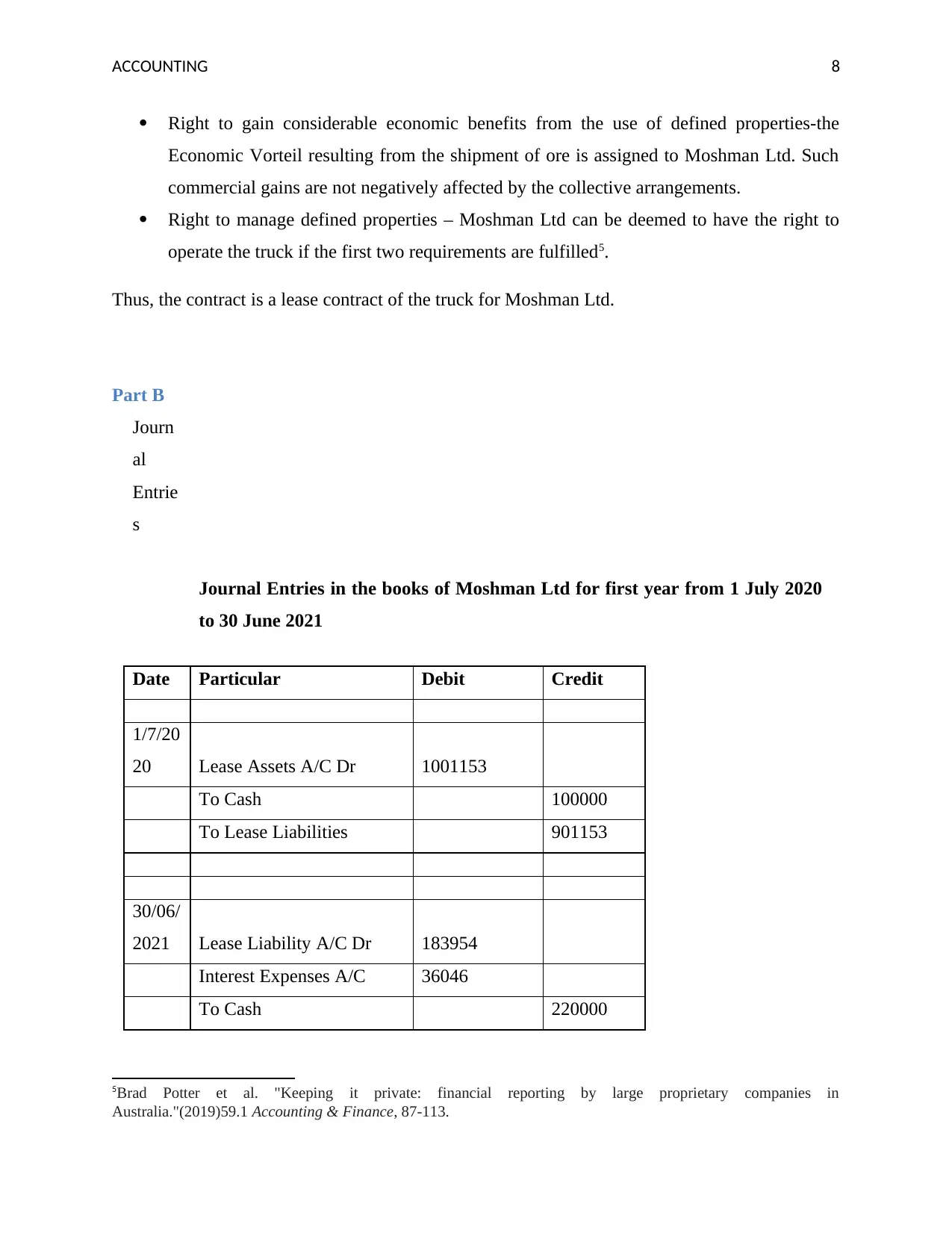

Right to gain considerable economic benefits from the use of defined properties-the

Economic Vorteil resulting from the shipment of ore is assigned to Moshman Ltd. Such

commercial gains are not negatively affected by the collective arrangements.

Right to manage defined properties – Moshman Ltd can be deemed to have the right to

operate the truck if the first two requirements are fulfilled5.

Thus, the contract is a lease contract of the truck for Moshman Ltd.

Part B

Journ

al

Entrie

s

Journal Entries in the books of Moshman Ltd for first year from 1 July 2020

to 30 June 2021

Date Particular Debit Credit

1/7/20

20 Lease Assets A/C Dr 1001153

To Cash 100000

To Lease Liabilities 901153

30/06/

2021 Lease Liability A/C Dr 183954

Interest Expenses A/C 36046

To Cash 220000

5Brad Potter et al. "Keeping it private: financial reporting by large proprietary companies in

Australia."(2019)59.1 Accounting & Finance, 87-113.

Right to gain considerable economic benefits from the use of defined properties-the

Economic Vorteil resulting from the shipment of ore is assigned to Moshman Ltd. Such

commercial gains are not negatively affected by the collective arrangements.

Right to manage defined properties – Moshman Ltd can be deemed to have the right to

operate the truck if the first two requirements are fulfilled5.

Thus, the contract is a lease contract of the truck for Moshman Ltd.

Part B

Journ

al

Entrie

s

Journal Entries in the books of Moshman Ltd for first year from 1 July 2020

to 30 June 2021

Date Particular Debit Credit

1/7/20

20 Lease Assets A/C Dr 1001153

To Cash 100000

To Lease Liabilities 901153

30/06/

2021 Lease Liability A/C Dr 183954

Interest Expenses A/C 36046

To Cash 220000

5Brad Potter et al. "Keeping it private: financial reporting by large proprietary companies in

Australia."(2019)59.1 Accounting & Finance, 87-113.

ACCOUNTING 9

Worki

ng

Notes

1)

Year Payment

Discounted

Factor

Present

Value

0 2020 100000 1 100000

1 2021 220000 0.961538462

211538.46

15

2 2022 220000 0.924556213

203402.36

69

3 2023 220000 0.888996359

195579.19

89

4 2024 340000 0.854804191

290633.42

5

1100000

1001153.4

52

2)

As Net present value of

minimum lease payment is

morethan 90% as standard

condition

Prese

nt

Value 1001153.452

Fair

Value 1001154

Worki

ng

Notes

1)

Year Payment

Discounted

Factor

Present

Value

0 2020 100000 1 100000

1 2021 220000 0.961538462

211538.46

15

2 2022 220000 0.924556213

203402.36

69

3 2023 220000 0.888996359

195579.19

89

4 2024 340000 0.854804191

290633.42

5

1100000

1001153.4

52

2)

As Net present value of

minimum lease payment is

morethan 90% as standard

condition

Prese

nt

Value 1001153.452

Fair

Value 1001154

ACCOUNTING 10

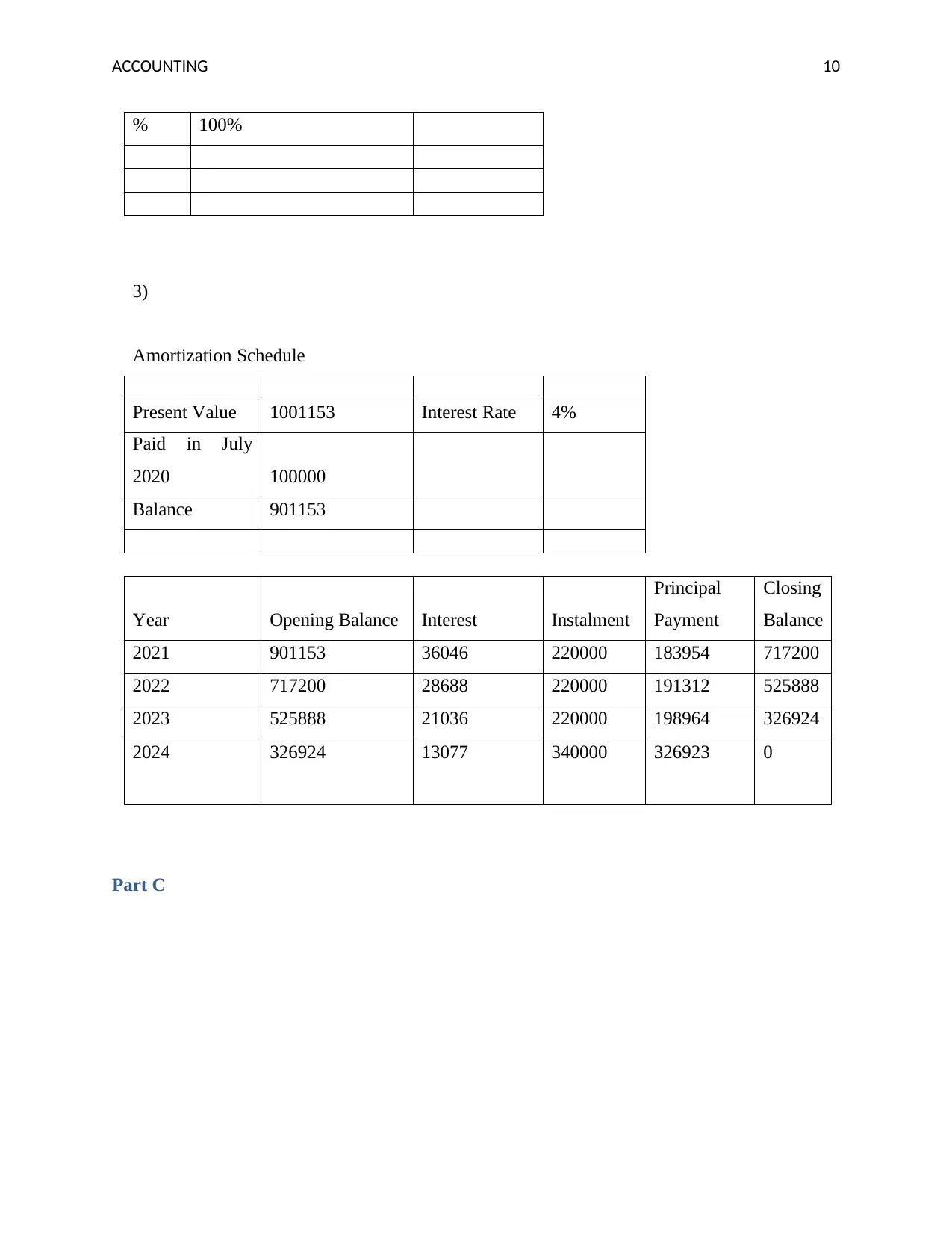

% 100%

3)

Amortization Schedule

Present Value 1001153 Interest Rate 4%

Paid in July

2020 100000

Balance 901153

Year Opening Balance Interest Instalment

Principal

Payment

Closing

Balance

2021 901153 36046 220000 183954 717200

2022 717200 28688 220000 191312 525888

2023 525888 21036 220000 198964 326924

2024 326924 13077 340000 326923 0

Part C

% 100%

3)

Amortization Schedule

Present Value 1001153 Interest Rate 4%

Paid in July

2020 100000

Balance 901153

Year Opening Balance Interest Instalment

Principal

Payment

Closing

Balance

2021 901153 36046 220000 183954 717200

2022 717200 28688 220000 191312 525888

2023 525888 21036 220000 198964 326924

2024 326924 13077 340000 326923 0

Part C

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACCOUNTING 11

In the leasing countries, AASB 116 'Leases' states that, according to paragraphs 17 to 23, the

term of the lease cannot be cancelled and justifies that the lease can be extended only if the lessor

wishes to extend the term of the lease. While deciding whether the leaser is reasonably confident

of exercising or not a lease extension of a right to terminate a lease, an entity shall review any

relevant fact and situation which provides for the right of renewal of the lease to be exercised by

it to create a Federal Register of Legislative Instruments for Standard Economic Motivation. If

the non-cancellable term of a lease is changed, an agency may amend the lease term. For

instance, if: (a) the lease has an option which the company did not previously take into account

when deciding the lease term. The leaser would not then exercise an option which the agency has

previously provided in deciding the lease term. Therefore, an occurrence obligates the renter to

apply an option not included previously in the lease term on a contractual basis. The rental was

also assessed under other criteria set out in paragraphs 23 to 28, where the rental obligation

calculation was based on the present value of the rent set in paragraph 26. An estimation of the

cost for a lower party in dismantle and disposal of the asset, restoration of the site at which it

resides or reconstruction of the underlying asset, unless such costs occur in the process of

product growth, under the conditions stated in the contract. At the date of commencement or as a

result of using the underlying properties within a defined period, the lessor shall be responsible

for these expenses6.

The requirements of AASB 116 ‘Leases’ states that lease term that is a contract between a lessor

and a lessee that is non-cancellable. In the given facts there is a lease of four years that Moshman

Ltd does not wants to extend. From the above statements of the lessee term that has been given

as the lease term is already been agreed between the parties and it concludes that the Lease

contract made between the Moshman Ltd and the Lessor Ltd was justified. In addition, it was

provided that a residual value of $120,000 was decided upon by Moshman. At the start of the

contract the fair value of the equipment is $1.001.154 and also the 4 per cent of the interest rate

specified in the contract. So in accordance with AASB 116 Leases Mohsam has paid according

to the present rate and also according to the rate of interest. So it has been concluded that the

Lessor Ltd lease agreement is justified. Threforen it has been assumed that the lessor and the

6 Michelle Joubert, Leanda Garvie, and Gabrielle Parle. "Implications of the New Accounting Standard for Leases

AASB 16 (IFRS 16) with the Inclusion of Operating Leases in the Balance Sheet." The Journal of New Business

Ideas & Trends 15.2 (2017): 1-11.

In the leasing countries, AASB 116 'Leases' states that, according to paragraphs 17 to 23, the

term of the lease cannot be cancelled and justifies that the lease can be extended only if the lessor

wishes to extend the term of the lease. While deciding whether the leaser is reasonably confident

of exercising or not a lease extension of a right to terminate a lease, an entity shall review any

relevant fact and situation which provides for the right of renewal of the lease to be exercised by

it to create a Federal Register of Legislative Instruments for Standard Economic Motivation. If

the non-cancellable term of a lease is changed, an agency may amend the lease term. For

instance, if: (a) the lease has an option which the company did not previously take into account

when deciding the lease term. The leaser would not then exercise an option which the agency has

previously provided in deciding the lease term. Therefore, an occurrence obligates the renter to

apply an option not included previously in the lease term on a contractual basis. The rental was

also assessed under other criteria set out in paragraphs 23 to 28, where the rental obligation

calculation was based on the present value of the rent set in paragraph 26. An estimation of the

cost for a lower party in dismantle and disposal of the asset, restoration of the site at which it

resides or reconstruction of the underlying asset, unless such costs occur in the process of

product growth, under the conditions stated in the contract. At the date of commencement or as a

result of using the underlying properties within a defined period, the lessor shall be responsible

for these expenses6.

The requirements of AASB 116 ‘Leases’ states that lease term that is a contract between a lessor

and a lessee that is non-cancellable. In the given facts there is a lease of four years that Moshman

Ltd does not wants to extend. From the above statements of the lessee term that has been given

as the lease term is already been agreed between the parties and it concludes that the Lease

contract made between the Moshman Ltd and the Lessor Ltd was justified. In addition, it was

provided that a residual value of $120,000 was decided upon by Moshman. At the start of the

contract the fair value of the equipment is $1.001.154 and also the 4 per cent of the interest rate

specified in the contract. So in accordance with AASB 116 Leases Mohsam has paid according

to the present rate and also according to the rate of interest. So it has been concluded that the

Lessor Ltd lease agreement is justified. Threforen it has been assumed that the lessor and the

6 Michelle Joubert, Leanda Garvie, and Gabrielle Parle. "Implications of the New Accounting Standard for Leases

AASB 16 (IFRS 16) with the Inclusion of Operating Leases in the Balance Sheet." The Journal of New Business

Ideas & Trends 15.2 (2017): 1-11.

ACCOUNTING 12

lessee has made the lease contract in accordance with all the norms and rules of AASB 116

Leasse7.

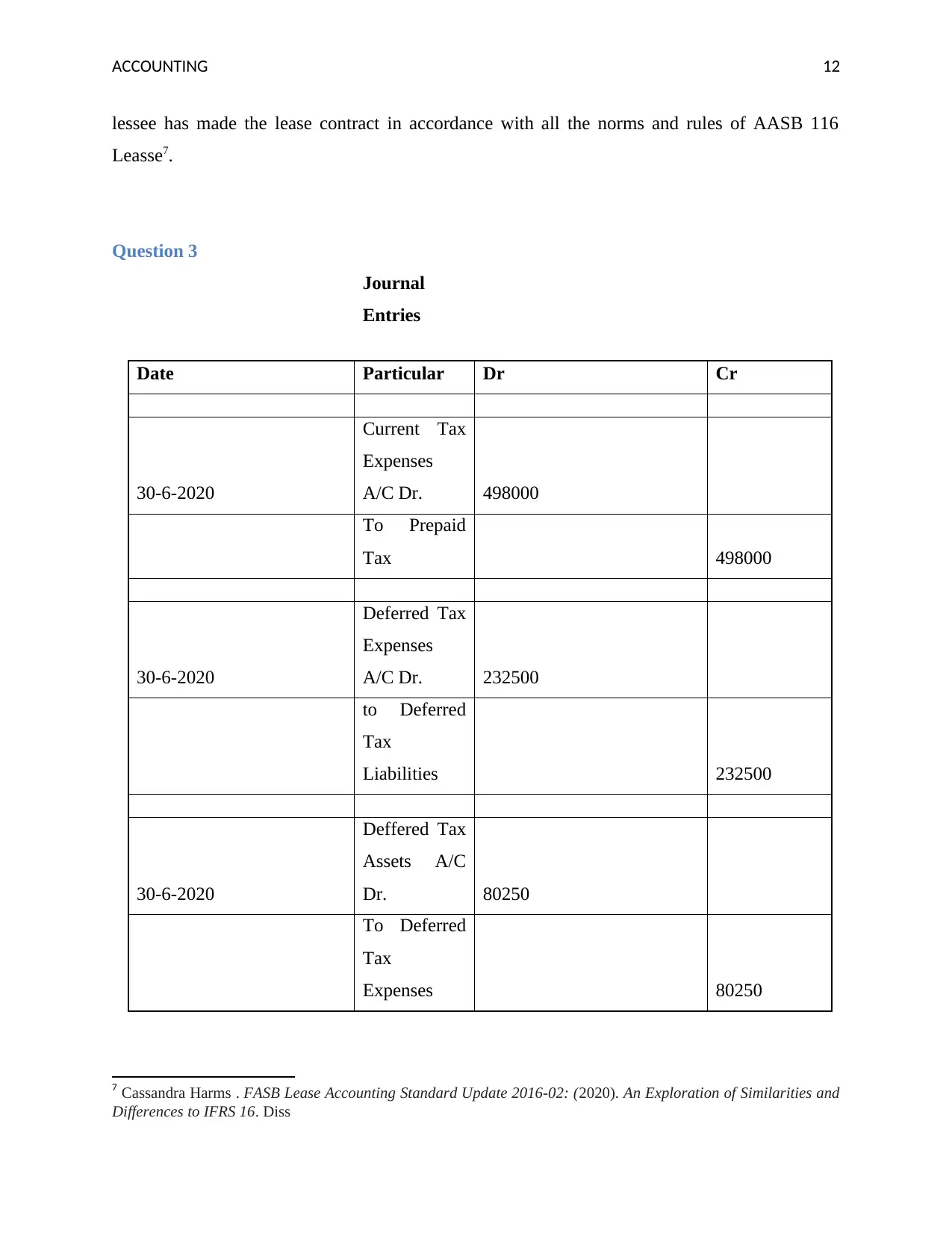

Question 3

Journal

Entries

Date Particular Dr Cr

30-6-2020

Current Tax

Expenses

A/C Dr. 498000

To Prepaid

Tax 498000

30-6-2020

Deferred Tax

Expenses

A/C Dr. 232500

to Deferred

Tax

Liabilities 232500

30-6-2020

Deffered Tax

Assets A/C

Dr. 80250

To Deferred

Tax

Expenses 80250

7 Cassandra Harms . FASB Lease Accounting Standard Update 2016-02: (2020). An Exploration of Similarities and

Differences to IFRS 16. Diss

lessee has made the lease contract in accordance with all the norms and rules of AASB 116

Leasse7.

Question 3

Journal

Entries

Date Particular Dr Cr

30-6-2020

Current Tax

Expenses

A/C Dr. 498000

To Prepaid

Tax 498000

30-6-2020

Deferred Tax

Expenses

A/C Dr. 232500

to Deferred

Tax

Liabilities 232500

30-6-2020

Deffered Tax

Assets A/C

Dr. 80250

To Deferred

Tax

Expenses 80250

7 Cassandra Harms . FASB Lease Accounting Standard Update 2016-02: (2020). An Exploration of Similarities and

Differences to IFRS 16. Diss

ACCOUNTING 13

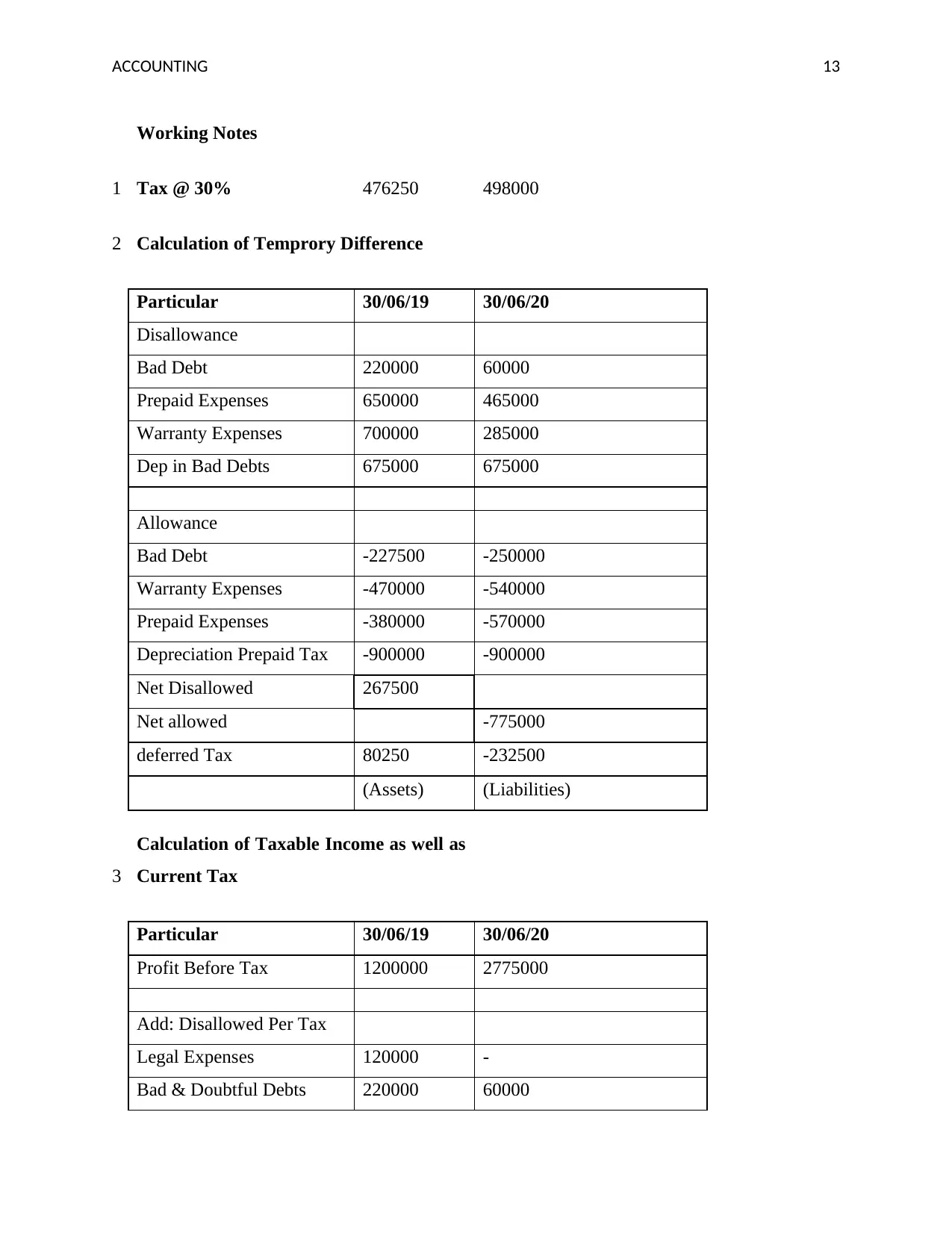

Working Notes

1 Tax @ 30% 476250 498000

2 Calculation of Temprory Difference

Particular 30/06/19 30/06/20

Disallowance

Bad Debt 220000 60000

Prepaid Expenses 650000 465000

Warranty Expenses 700000 285000

Dep in Bad Debts 675000 675000

Allowance

Bad Debt -227500 -250000

Warranty Expenses -470000 -540000

Prepaid Expenses -380000 -570000

Depreciation Prepaid Tax -900000 -900000

Net Disallowed 267500

Net allowed -775000

deferred Tax 80250 -232500

(Assets) (Liabilities)

3

Calculation of Taxable Income as well as

Current Tax

Particular 30/06/19 30/06/20

Profit Before Tax 1200000 2775000

Add: Disallowed Per Tax

Legal Expenses 120000 -

Bad & Doubtful Debts 220000 60000

Working Notes

1 Tax @ 30% 476250 498000

2 Calculation of Temprory Difference

Particular 30/06/19 30/06/20

Disallowance

Bad Debt 220000 60000

Prepaid Expenses 650000 465000

Warranty Expenses 700000 285000

Dep in Bad Debts 675000 675000

Allowance

Bad Debt -227500 -250000

Warranty Expenses -470000 -540000

Prepaid Expenses -380000 -570000

Depreciation Prepaid Tax -900000 -900000

Net Disallowed 267500

Net allowed -775000

deferred Tax 80250 -232500

(Assets) (Liabilities)

3

Calculation of Taxable Income as well as

Current Tax

Particular 30/06/19 30/06/20

Profit Before Tax 1200000 2775000

Add: Disallowed Per Tax

Legal Expenses 120000 -

Bad & Doubtful Debts 220000 60000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING 14

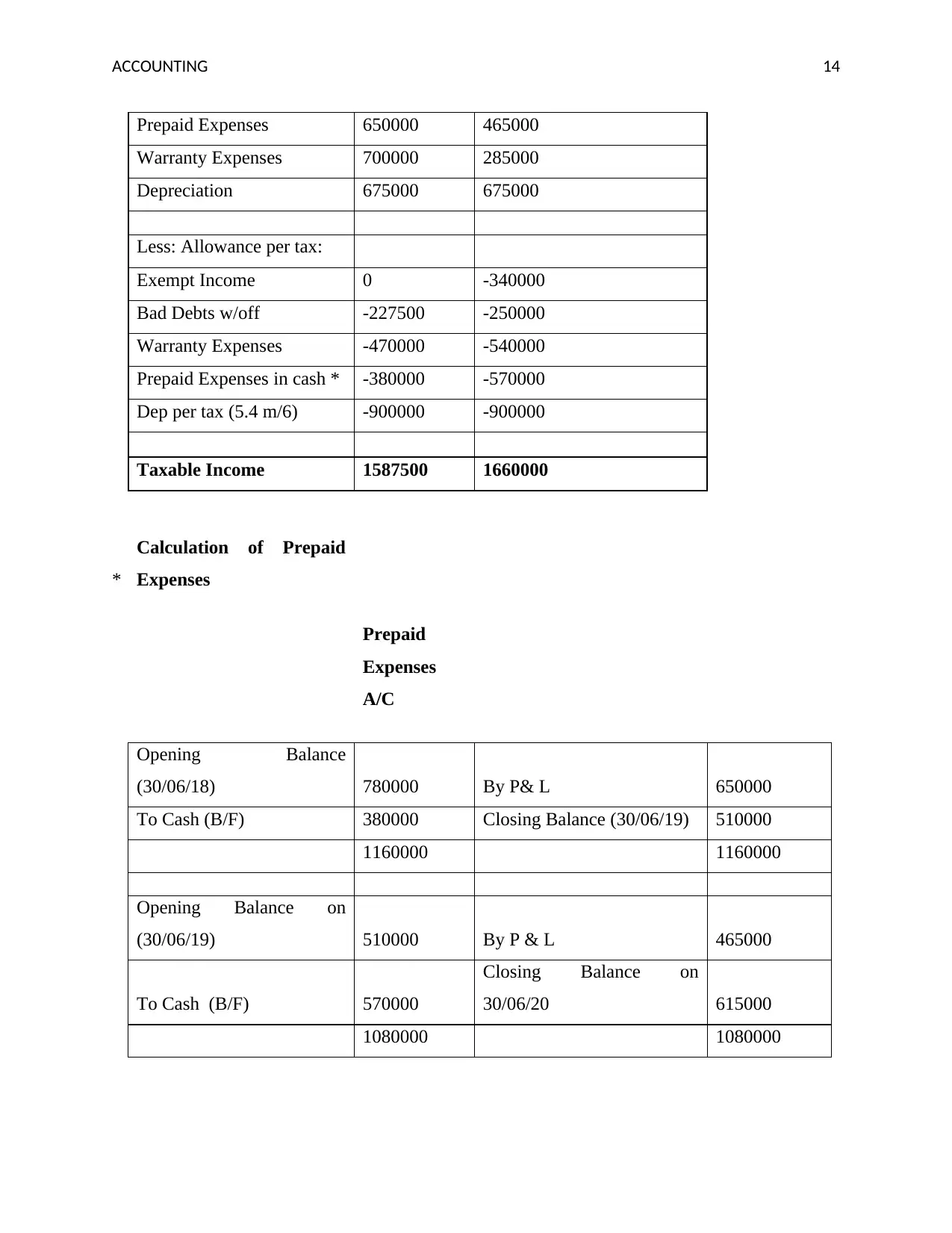

Prepaid Expenses 650000 465000

Warranty Expenses 700000 285000

Depreciation 675000 675000

Less: Allowance per tax:

Exempt Income 0 -340000

Bad Debts w/off -227500 -250000

Warranty Expenses -470000 -540000

Prepaid Expenses in cash * -380000 -570000

Dep per tax (5.4 m/6) -900000 -900000

Taxable Income 1587500 1660000

*

Calculation of Prepaid

Expenses

Prepaid

Expenses

A/C

Opening Balance

(30/06/18) 780000 By P& L 650000

To Cash (B/F) 380000 Closing Balance (30/06/19) 510000

1160000 1160000

Opening Balance on

(30/06/19) 510000 By P & L 465000

To Cash (B/F) 570000

Closing Balance on

30/06/20 615000

1080000 1080000

Prepaid Expenses 650000 465000

Warranty Expenses 700000 285000

Depreciation 675000 675000

Less: Allowance per tax:

Exempt Income 0 -340000

Bad Debts w/off -227500 -250000

Warranty Expenses -470000 -540000

Prepaid Expenses in cash * -380000 -570000

Dep per tax (5.4 m/6) -900000 -900000

Taxable Income 1587500 1660000

*

Calculation of Prepaid

Expenses

Prepaid

Expenses

A/C

Opening Balance

(30/06/18) 780000 By P& L 650000

To Cash (B/F) 380000 Closing Balance (30/06/19) 510000

1160000 1160000

Opening Balance on

(30/06/19) 510000 By P & L 465000

To Cash (B/F) 570000

Closing Balance on

30/06/20 615000

1080000 1080000

ACCOUNTING 15

Bibliography

Joubert, Michelle, LeandaGarvie, and Gabrielle Parle."Implications of the New Accounting

Standard for Leases AASB 16 (IFRS 16) with the Inclusion of Operating Leases in the Balance

Sheet."(2017), 15(2 The Journal of New Business Ideas & Trends 1-11

SECINARO, SilvanaFilomena, et al. "Relevance in the Application of IFRS 16 for Financial

Statements: Empirical Evidence the Impact of the Financial Method in SMEs." (2020): 1-15.

Bond, David, Brett Govendir, and Peter Wells. "An evaluation of asset impairment decisions by

Australian firms and whether this was impacted by AASB 136." (2016).

Wang, Xiaojiao. "Compliance Over Time by Australian Firms with IFRS Disclosure

Requirements." (2019), 29(4) Australian Accounting Review : 679-691.

Potter, Brad, et al. "Keeping it private: financial reporting by large proprietary companies in

Australia." (2019) 59(1) Accounting & Finance : 87-113.

Joubert, Michelle, Leanda Garvie, and Gabrielle Parle. "Implications of the New Accounting

Standard for Leases AASB 16 (IFRS 16) with the Inclusion of Operating Leases in the Balance

Sheet." The Journal of New Business Ideas & Trends 15.2 (2017): 1-11.

Harms, Cassandra. FASB Lease Accounting Standard Update 2016-02: (2020). An Exploration

of Similarities and Differences to IFRS 16. Diss

Bibliography

Joubert, Michelle, LeandaGarvie, and Gabrielle Parle."Implications of the New Accounting

Standard for Leases AASB 16 (IFRS 16) with the Inclusion of Operating Leases in the Balance

Sheet."(2017), 15(2 The Journal of New Business Ideas & Trends 1-11

SECINARO, SilvanaFilomena, et al. "Relevance in the Application of IFRS 16 for Financial

Statements: Empirical Evidence the Impact of the Financial Method in SMEs." (2020): 1-15.

Bond, David, Brett Govendir, and Peter Wells. "An evaluation of asset impairment decisions by

Australian firms and whether this was impacted by AASB 136." (2016).

Wang, Xiaojiao. "Compliance Over Time by Australian Firms with IFRS Disclosure

Requirements." (2019), 29(4) Australian Accounting Review : 679-691.

Potter, Brad, et al. "Keeping it private: financial reporting by large proprietary companies in

Australia." (2019) 59(1) Accounting & Finance : 87-113.

Joubert, Michelle, Leanda Garvie, and Gabrielle Parle. "Implications of the New Accounting

Standard for Leases AASB 16 (IFRS 16) with the Inclusion of Operating Leases in the Balance

Sheet." The Journal of New Business Ideas & Trends 15.2 (2017): 1-11.

Harms, Cassandra. FASB Lease Accounting Standard Update 2016-02: (2020). An Exploration

of Similarities and Differences to IFRS 16. Diss

ACCOUNTING 16

1 out of 16

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.