Demand and Supply in Contemporary Business Economics

VerifiedAdded on 2023/06/18

|12

|2790

|158

AI Summary

This report discusses the law of demand, movement with the demand curve, and change in the demand curve. It also explains the law of supply, change in supply curve, and factors affecting demand and supply. Additionally, it compares and contrasts emerging theories and models in 21st century economics with those of the 20th century and explains their relationship with modern business practices.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Contemporary Business

Economics

Economics

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

INTRODUCTION

Economics is the study of people and their values in a specific production, distribution

and consumption of products and services. It mainly focuses on the behaviour and interactions of

the economist and their working(Opeskin, 202). It based on the various aspect of the market such

as demand, supply and change in demand and change in supply. This report is based on the

McDonald's, it is the American company which is founded in 1940 as the restaurant which is

operated by the Richard and Maurice McDonald in California. This report will cover the

demand and supply of the specific business and also evaluate the change in demand and supply.

Lastly, It will evaluate the theories and models which are emerging in 21st century contemporary

economics.

TASK 1

1.1 Explain the law of demand, movement with the demand curve & change in the demand

curve with the help of appropriate diagram.

Demand refers to the principle stating the consumer's desire in order to purchase the

specific goods and services and also the having the willingness to pay the prices of the specific

commodity.

Law of Demand:

The law of demand stated that there is the inverse relationship in the price of the

commodity and the specific quantity of the given goods and other factors will remain constant.

When the price of the product increases from P0 To P1 then the demand of the quantity

decreases form OQ0 to OQ1 and vice versa, other factors will remain constant. This law of

demand shows that demand of the particular gods is inversely related to the price of the given

commodity. In context to McDonald's, when they price of variety of burger increases, then the

demand for such good decreases as the people will love to buy the affordable food items.

1

Economics is the study of people and their values in a specific production, distribution

and consumption of products and services. It mainly focuses on the behaviour and interactions of

the economist and their working(Opeskin, 202). It based on the various aspect of the market such

as demand, supply and change in demand and change in supply. This report is based on the

McDonald's, it is the American company which is founded in 1940 as the restaurant which is

operated by the Richard and Maurice McDonald in California. This report will cover the

demand and supply of the specific business and also evaluate the change in demand and supply.

Lastly, It will evaluate the theories and models which are emerging in 21st century contemporary

economics.

TASK 1

1.1 Explain the law of demand, movement with the demand curve & change in the demand

curve with the help of appropriate diagram.

Demand refers to the principle stating the consumer's desire in order to purchase the

specific goods and services and also the having the willingness to pay the prices of the specific

commodity.

Law of Demand:

The law of demand stated that there is the inverse relationship in the price of the

commodity and the specific quantity of the given goods and other factors will remain constant.

When the price of the product increases from P0 To P1 then the demand of the quantity

decreases form OQ0 to OQ1 and vice versa, other factors will remain constant. This law of

demand shows that demand of the particular gods is inversely related to the price of the given

commodity. In context to McDonald's, when they price of variety of burger increases, then the

demand for such good decreases as the people will love to buy the affordable food items.

1

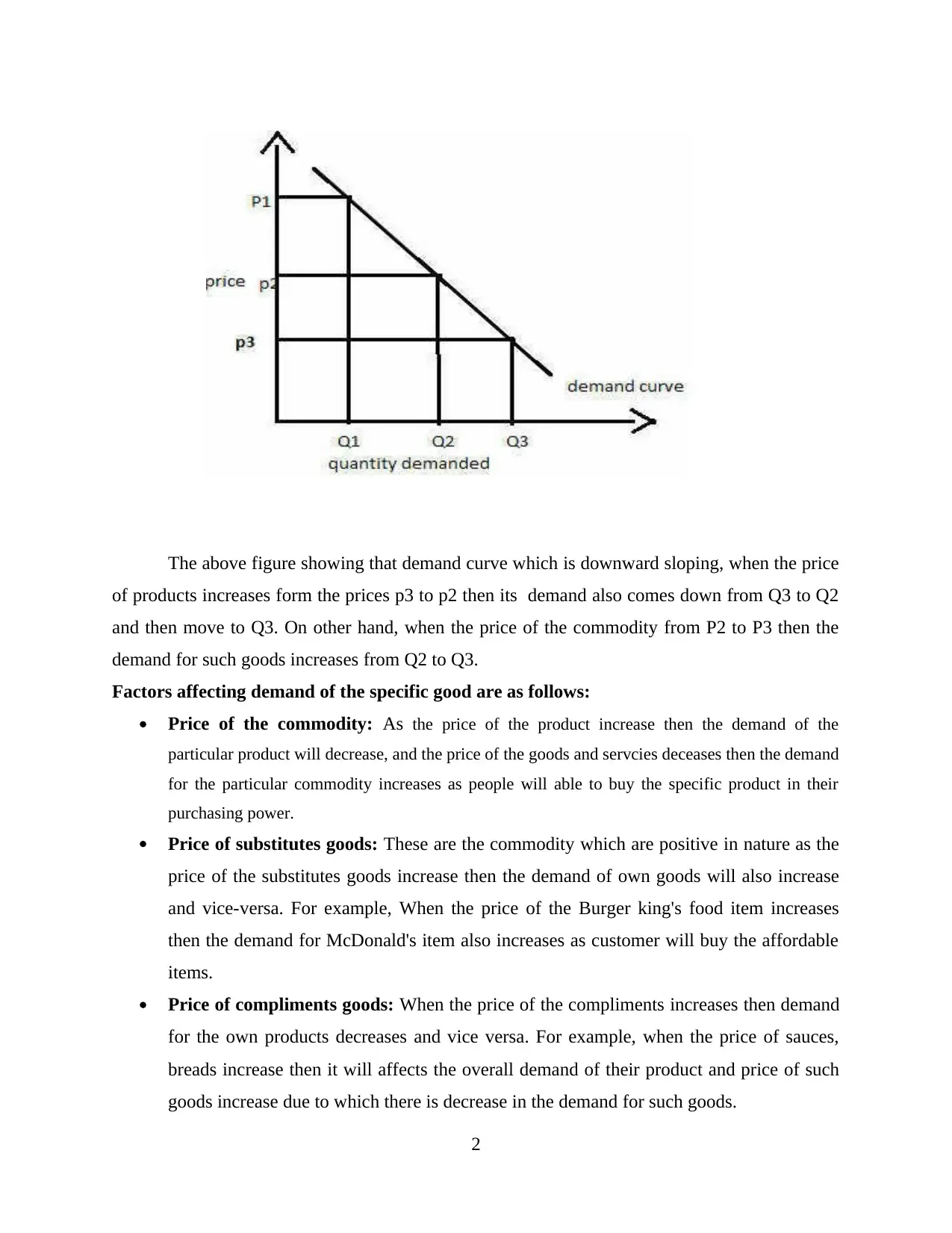

The above figure showing that demand curve which is downward sloping, when the price

of products increases form the prices p3 to p2 then its demand also comes down from Q3 to Q2

and then move to Q3. On other hand, when the price of the commodity from P2 to P3 then the

demand for such goods increases from Q2 to Q3.

Factors affecting demand of the specific good are as follows:

Price of the commodity: As the price of the product increase then the demand of the

particular product will decrease, and the price of the goods and servcies deceases then the demand

for the particular commodity increases as people will able to buy the specific product in their

purchasing power.

Price of substitutes goods: These are the commodity which are positive in nature as the

price of the substitutes goods increase then the demand of own goods will also increase

and vice-versa. For example, When the price of the Burger king's food item increases

then the demand for McDonald's item also increases as customer will buy the affordable

items.

Price of compliments goods: When the price of the compliments increases then demand

for the own products decreases and vice versa. For example, when the price of sauces,

breads increase then it will affects the overall demand of their product and price of such

goods increase due to which there is decrease in the demand for such goods.

2

of products increases form the prices p3 to p2 then its demand also comes down from Q3 to Q2

and then move to Q3. On other hand, when the price of the commodity from P2 to P3 then the

demand for such goods increases from Q2 to Q3.

Factors affecting demand of the specific good are as follows:

Price of the commodity: As the price of the product increase then the demand of the

particular product will decrease, and the price of the goods and servcies deceases then the demand

for the particular commodity increases as people will able to buy the specific product in their

purchasing power.

Price of substitutes goods: These are the commodity which are positive in nature as the

price of the substitutes goods increase then the demand of own goods will also increase

and vice-versa. For example, When the price of the Burger king's food item increases

then the demand for McDonald's item also increases as customer will buy the affordable

items.

Price of compliments goods: When the price of the compliments increases then demand

for the own products decreases and vice versa. For example, when the price of sauces,

breads increase then it will affects the overall demand of their product and price of such

goods increase due to which there is decrease in the demand for such goods.

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Income of the consumer: When the disposable income of the consumer increases then

the demand for the normal goods also increase but demand for the inferior goods

decreases. On other aspects, when the income of the consumer reduce then the demand

for normal goods also decreases and demand for inferior goods increases, other factors

remain constant.

Taste and preferences of the consumer: When the taste & preferences of the consumer

are in favour of the given food item, then the demand for the given goods increase. While

taste and preferences of the consumer are not in favour of given food item then demand

for such good decreases.

Change in future expectations: It is directly related to the supply of the products, when

there is an increase in the expectations of the consumer then will rise in the supply of the

products as It will directly impact the profitability of the company(Feng and et. al., 2021).

For example, As the supplier is expecting the increase in the future expectation then there

will be rise in the supply of the goods.

Change in demand curve:

It refers to the change in the entire demand curve which can cause by the various factors

such as change in the taste and preferences of the consumer, change in income, change in price

of substitute gods and complements goods. In these cases, the demand curve will shift to right or

life.

3

the demand for the normal goods also increase but demand for the inferior goods

decreases. On other aspects, when the income of the consumer reduce then the demand

for normal goods also decreases and demand for inferior goods increases, other factors

remain constant.

Taste and preferences of the consumer: When the taste & preferences of the consumer

are in favour of the given food item, then the demand for the given goods increase. While

taste and preferences of the consumer are not in favour of given food item then demand

for such good decreases.

Change in future expectations: It is directly related to the supply of the products, when

there is an increase in the expectations of the consumer then will rise in the supply of the

products as It will directly impact the profitability of the company(Feng and et. al., 2021).

For example, As the supplier is expecting the increase in the future expectation then there

will be rise in the supply of the goods.

Change in demand curve:

It refers to the change in the entire demand curve which can cause by the various factors

such as change in the taste and preferences of the consumer, change in income, change in price

of substitute gods and complements goods. In these cases, the demand curve will shift to right or

life.

3

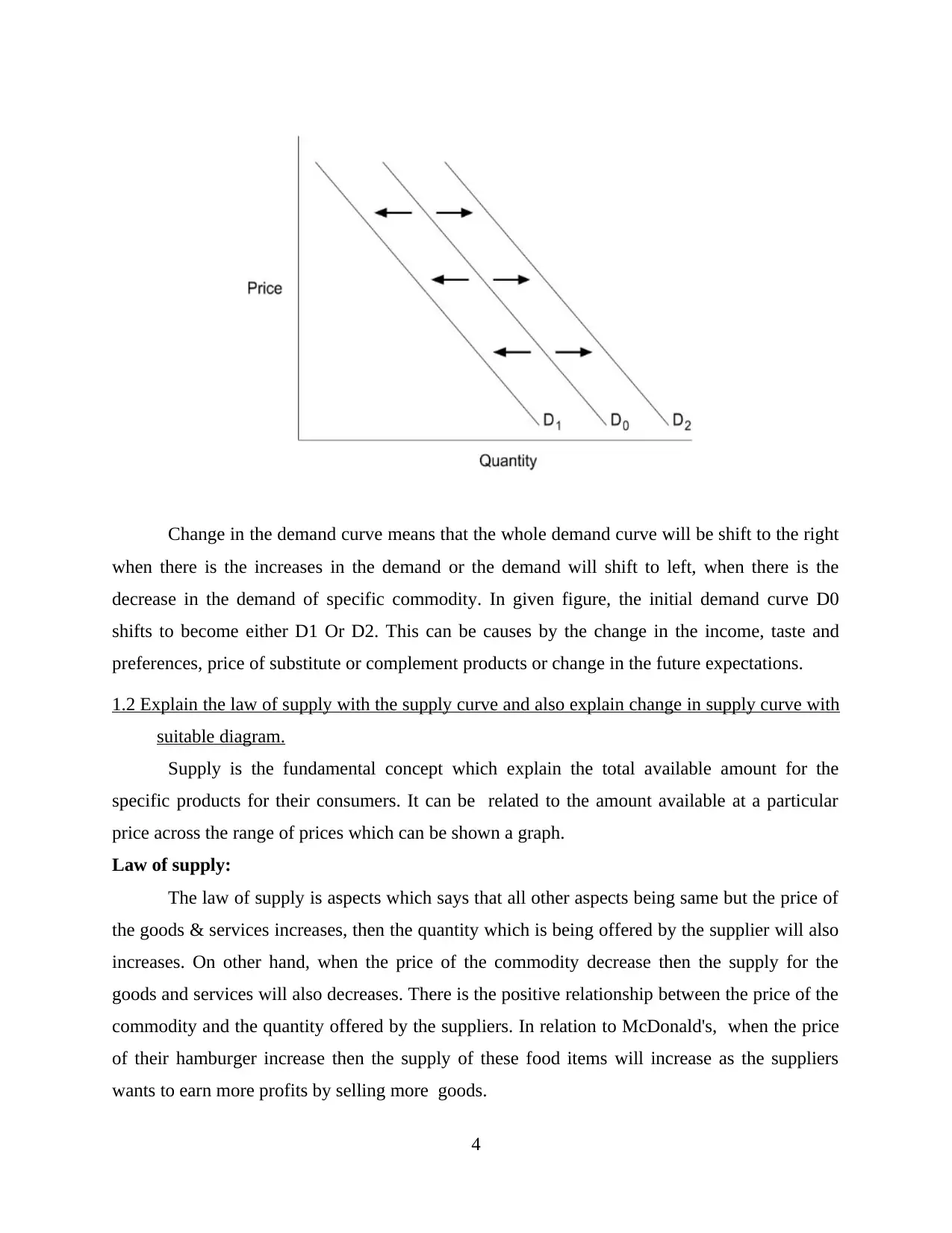

Change in the demand curve means that the whole demand curve will be shift to the right

when there is the increases in the demand or the demand will shift to left, when there is the

decrease in the demand of specific commodity. In given figure, the initial demand curve D0

shifts to become either D1 Or D2. This can be causes by the change in the income, taste and

preferences, price of substitute or complement products or change in the future expectations.

1.2 Explain the law of supply with the supply curve and also explain change in supply curve with

suitable diagram.

Supply is the fundamental concept which explain the total available amount for the

specific products for their consumers. It can be related to the amount available at a particular

price across the range of prices which can be shown a graph.

Law of supply:

The law of supply is aspects which says that all other aspects being same but the price of

the goods & services increases, then the quantity which is being offered by the supplier will also

increases. On other hand, when the price of the commodity decrease then the supply for the

goods and services will also decreases. There is the positive relationship between the price of the

commodity and the quantity offered by the suppliers. In relation to McDonald's, when the price

of their hamburger increase then the supply of these food items will increase as the suppliers

wants to earn more profits by selling more goods.

4

when there is the increases in the demand or the demand will shift to left, when there is the

decrease in the demand of specific commodity. In given figure, the initial demand curve D0

shifts to become either D1 Or D2. This can be causes by the change in the income, taste and

preferences, price of substitute or complement products or change in the future expectations.

1.2 Explain the law of supply with the supply curve and also explain change in supply curve with

suitable diagram.

Supply is the fundamental concept which explain the total available amount for the

specific products for their consumers. It can be related to the amount available at a particular

price across the range of prices which can be shown a graph.

Law of supply:

The law of supply is aspects which says that all other aspects being same but the price of

the goods & services increases, then the quantity which is being offered by the supplier will also

increases. On other hand, when the price of the commodity decrease then the supply for the

goods and services will also decreases. There is the positive relationship between the price of the

commodity and the quantity offered by the suppliers. In relation to McDonald's, when the price

of their hamburger increase then the supply of these food items will increase as the suppliers

wants to earn more profits by selling more goods.

4

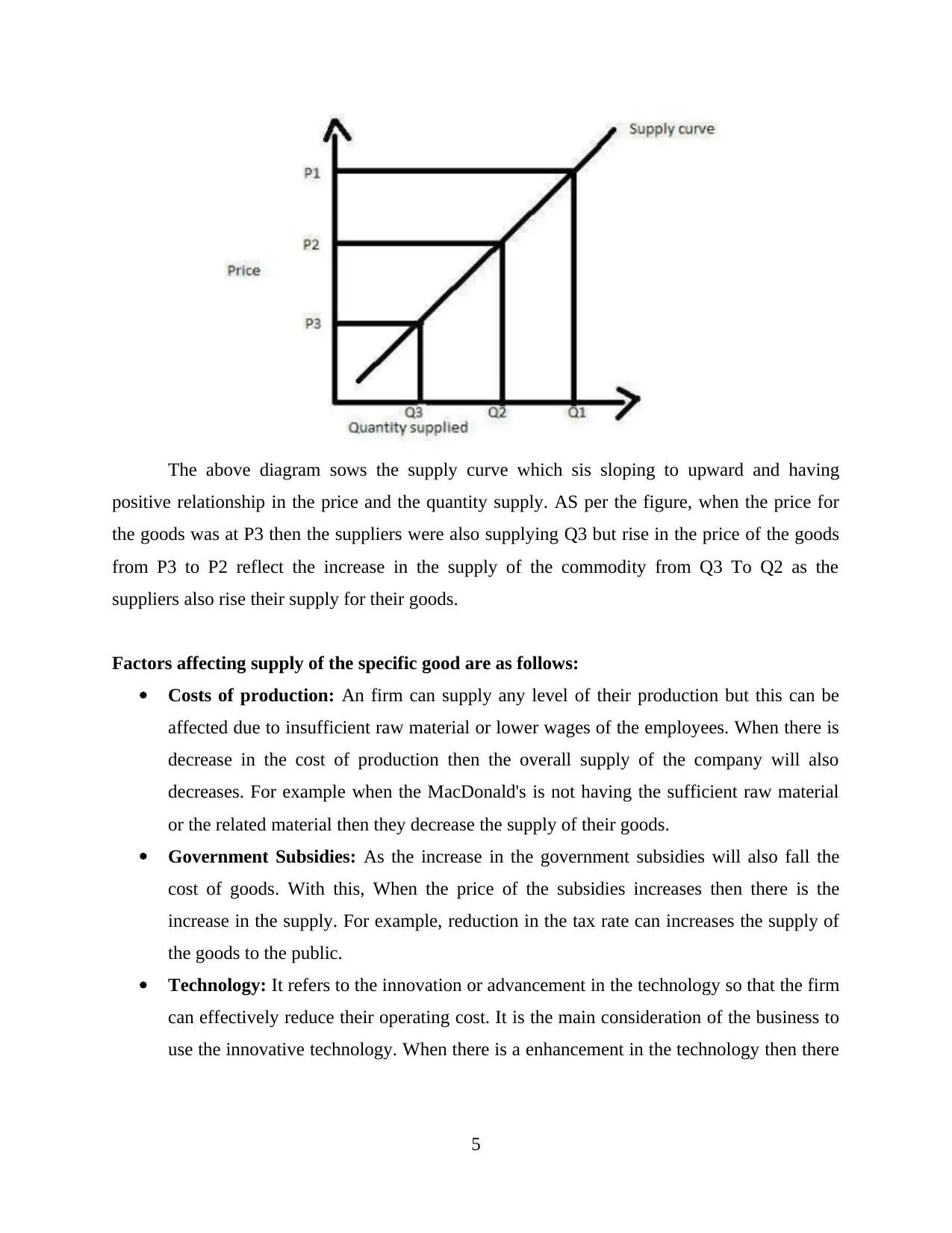

The above diagram sows the supply curve which sis sloping to upward and having

positive relationship in the price and the quantity supply. AS per the figure, when the price for

the goods was at P3 then the suppliers were also supplying Q3 but rise in the price of the goods

from P3 to P2 reflect the increase in the supply of the commodity from Q3 To Q2 as the

suppliers also rise their supply for their goods.

Factors affecting supply of the specific good are as follows:

Costs of production: An firm can supply any level of their production but this can be

affected due to insufficient raw material or lower wages of the employees. When there is

decrease in the cost of production then the overall supply of the company will also

decreases. For example when the MacDonald's is not having the sufficient raw material

or the related material then they decrease the supply of their goods.

Government Subsidies: As the increase in the government subsidies will also fall the

cost of goods. With this, When the price of the subsidies increases then there is the

increase in the supply. For example, reduction in the tax rate can increases the supply of

the goods to the public.

Technology: It refers to the innovation or advancement in the technology so that the firm

can effectively reduce their operating cost. It is the main consideration of the business to

use the innovative technology. When there is a enhancement in the technology then there

5

positive relationship in the price and the quantity supply. AS per the figure, when the price for

the goods was at P3 then the suppliers were also supplying Q3 but rise in the price of the goods

from P3 to P2 reflect the increase in the supply of the commodity from Q3 To Q2 as the

suppliers also rise their supply for their goods.

Factors affecting supply of the specific good are as follows:

Costs of production: An firm can supply any level of their production but this can be

affected due to insufficient raw material or lower wages of the employees. When there is

decrease in the cost of production then the overall supply of the company will also

decreases. For example when the MacDonald's is not having the sufficient raw material

or the related material then they decrease the supply of their goods.

Government Subsidies: As the increase in the government subsidies will also fall the

cost of goods. With this, When the price of the subsidies increases then there is the

increase in the supply. For example, reduction in the tax rate can increases the supply of

the goods to the public.

Technology: It refers to the innovation or advancement in the technology so that the firm

can effectively reduce their operating cost. It is the main consideration of the business to

use the innovative technology. When there is a enhancement in the technology then there

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

will increase the supply of the goods and services due to reduction in the entire firms

costs.

Objectives of firms: There are organisation which is motive is to increase their supply so

hat they can cover the large market and some are with the main consideration of

generating higher profitability. When the try to increase their profit then they will

decrease the supply of their goods in the large market as there motive s to increase the

profits.

Weather: These are the factors which is having direct impact on the profitability and

supply of the firm. In relation to Agriculture industry, there is a major impact on their

functionality. In context to MacDonald's, they are dealing in food item so there is a

major impact of weather on their functionality.

More firms: When there is the competition in the large market so it will impact the

overall supply f the firm as due to more number of firms in the market impact the supply

of the existing company. When there is decrease in the prices of the products then there

will fall in the supply of the commodity.

Change in Supply Curve:

A change in supply refers to the shift in the supply curve due to change in the various

factors such as taxes, production costs and technology. When the supply for the commodity

increases then the sully curve shift from S0 to S1. On other hand, when the supply of the

products decreases then the supply curve shift from S0 to S2(Choi, 2018).

6

costs.

Objectives of firms: There are organisation which is motive is to increase their supply so

hat they can cover the large market and some are with the main consideration of

generating higher profitability. When the try to increase their profit then they will

decrease the supply of their goods in the large market as there motive s to increase the

profits.

Weather: These are the factors which is having direct impact on the profitability and

supply of the firm. In relation to Agriculture industry, there is a major impact on their

functionality. In context to MacDonald's, they are dealing in food item so there is a

major impact of weather on their functionality.

More firms: When there is the competition in the large market so it will impact the

overall supply f the firm as due to more number of firms in the market impact the supply

of the existing company. When there is decrease in the prices of the products then there

will fall in the supply of the commodity.

Change in Supply Curve:

A change in supply refers to the shift in the supply curve due to change in the various

factors such as taxes, production costs and technology. When the supply for the commodity

increases then the sully curve shift from S0 to S1. On other hand, when the supply of the

products decreases then the supply curve shift from S0 to S2(Choi, 2018).

6

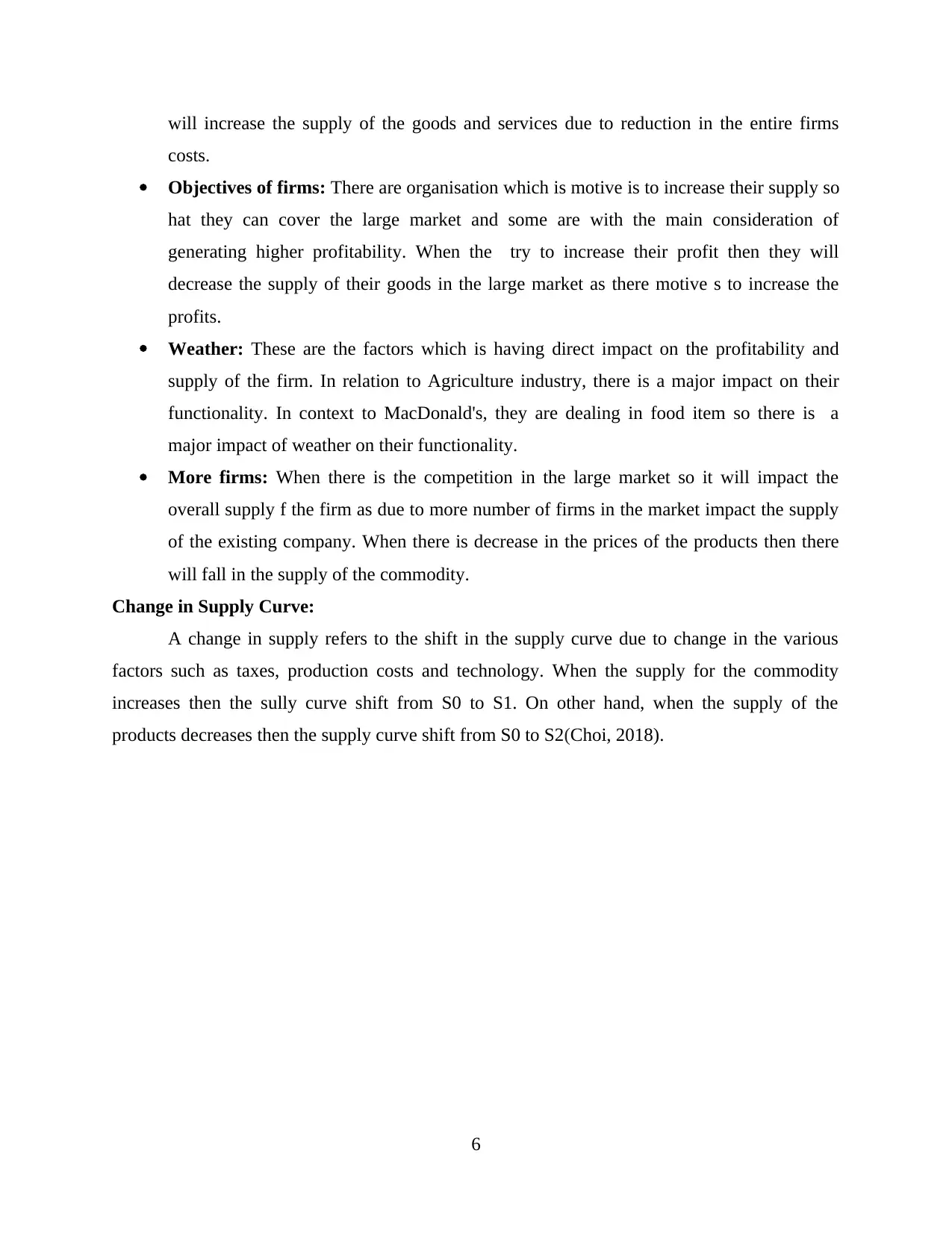

As show in figure, when the price of given products increase then the supply of the goods

will also increase and as per the figure, the supply curve will shift to S0 to S1 and when the price

of the given good decreases then the supply for specific commodity will also fall due to low

market supply of their goods.

TASK 2

Compare & contrast emerging theories & models in 21st century economics with those of the 20th

century and explain the relationship between both modern business practices.

There are various theories which is given by certain economist in the 20th and 21st century

and they are states as follows:

Neoclassical Growth Theory

It is the economic theory that analyse the economic growth rate with the intregation of

three factors- labour, capital & technology. The national bureau of Economic Research, Robert

Solow & Trevor is have introduce this theory for long run economic development in 1956.

This theory says that short-term equilibrium results from varying amounts of labour and

capital in their productions. This theory also explain that change has the main impact on the

economic growth of the economy and there is no development without advancement in the

technology of production. This theory explains that temporary equilibrium is differ from the

long-term equilibrium that do not require these factors. This theory have the increment in the

7

will also increase and as per the figure, the supply curve will shift to S0 to S1 and when the price

of the given good decreases then the supply for specific commodity will also fall due to low

market supply of their goods.

TASK 2

Compare & contrast emerging theories & models in 21st century economics with those of the 20th

century and explain the relationship between both modern business practices.

There are various theories which is given by certain economist in the 20th and 21st century

and they are states as follows:

Neoclassical Growth Theory

It is the economic theory that analyse the economic growth rate with the intregation of

three factors- labour, capital & technology. The national bureau of Economic Research, Robert

Solow & Trevor is have introduce this theory for long run economic development in 1956.

This theory says that short-term equilibrium results from varying amounts of labour and

capital in their productions. This theory also explain that change has the main impact on the

economic growth of the economy and there is no development without advancement in the

technology of production. This theory explains that temporary equilibrium is differ from the

long-term equilibrium that do not require these factors. This theory have the increment in the

7

capital of the economy & how the people use their capital as it is necessary for the economic

development. furthermore, the relation of capital & labour decide the output form the firm.

Lastly technology can decide the labour productivity & increase in the output of the labour due

to use of the advance technology.

Marx's Social Economic system

Karl Marx is the economist and author and have these theories about capitalism &

communism. Marx was influenced with the classical political economists like David Ricardo and

his own rand of economics. Marx explains that society is made up of two main classes which are

capitalists who are understanding the as a social and economic system, will be valid in the

modern era. Capitalists are the business owners that manage the process of production &

responsible for various means of production such as Factories, tolls and raw material & who are

entitled for all the profits.

Keynesian Economics theory

They are having the assumption that prices and the wages are sticky and this is having

three principal that explain that how the economy will work. First is aggregate demand can

influenced by several economic decision as sometimes the decision taken by the private sector

can be adverse to the macroeconomics outcome such as reduction in consumer spending during

high recession(Chen And et. al., 2018). Second is Prices and wages which responds slowly to

change the supply and demand of the goods and services. Last is change I aggregate demand

whether anticipated or unanticipated, There is the greatest short run affect in employment and

prices.

AS the modern theory is concern with the aggregate demand which is being affected by

the economic decisions of the private and public sector organisations. On other hand,

Neoclassical theory is based on the three factors such as labour, capital and technology so the

final consideration of these theory is to s to get the advancement in the technology and the other

aspect so that economic growth can be maintained.

CONCLUSION

It is concluded from the above report that Demand and supply play significant role in the

growth and the development of the economy. There are certain factors which impact the demand

and the change in demand of the goods and services these are change in income, price of

substitute goods, taste and preferences of the consumers and future expectations. There is

8

development. furthermore, the relation of capital & labour decide the output form the firm.

Lastly technology can decide the labour productivity & increase in the output of the labour due

to use of the advance technology.

Marx's Social Economic system

Karl Marx is the economist and author and have these theories about capitalism &

communism. Marx was influenced with the classical political economists like David Ricardo and

his own rand of economics. Marx explains that society is made up of two main classes which are

capitalists who are understanding the as a social and economic system, will be valid in the

modern era. Capitalists are the business owners that manage the process of production &

responsible for various means of production such as Factories, tolls and raw material & who are

entitled for all the profits.

Keynesian Economics theory

They are having the assumption that prices and the wages are sticky and this is having

three principal that explain that how the economy will work. First is aggregate demand can

influenced by several economic decision as sometimes the decision taken by the private sector

can be adverse to the macroeconomics outcome such as reduction in consumer spending during

high recession(Chen And et. al., 2018). Second is Prices and wages which responds slowly to

change the supply and demand of the goods and services. Last is change I aggregate demand

whether anticipated or unanticipated, There is the greatest short run affect in employment and

prices.

AS the modern theory is concern with the aggregate demand which is being affected by

the economic decisions of the private and public sector organisations. On other hand,

Neoclassical theory is based on the three factors such as labour, capital and technology so the

final consideration of these theory is to s to get the advancement in the technology and the other

aspect so that economic growth can be maintained.

CONCLUSION

It is concluded from the above report that Demand and supply play significant role in the

growth and the development of the economy. There are certain factors which impact the demand

and the change in demand of the goods and services these are change in income, price of

substitute goods, taste and preferences of the consumers and future expectations. There is

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

positive relationship between the price and the supply of the commodity and government

subsidy, weather, Objectives of firms, Costs of production and Technology are the factors which

affects the supply curve ad overall profitability of the firm. Marx's Social Economic system,

Keynesian Economics theory and neoclassical theory are the certain assumptions of the

economist so that they can ensure the economic development of the economy in the large market.

9

subsidy, weather, Objectives of firms, Costs of production and Technology are the factors which

affects the supply curve ad overall profitability of the firm. Marx's Social Economic system,

Keynesian Economics theory and neoclassical theory are the certain assumptions of the

economist so that they can ensure the economic development of the economy in the large market.

9

REFERENCES

Books and Journals

Chen, X.M. And et. al., 2018. Spatial visitation prediction of on-demand ride services using the

scaling law. Physica A: Statistical Mechanics and its Applications, 508, pp.84-94.

Choi, H., 2018. Disproving Market Demand and Market Supply. Available at SSRN 3203158.

Feng, G. and et. al., 2021, March. Research on the Demand Distribution of Aviation Equipment

Maintenance Spare Parts. In 2021 IEEE 6th International Conference on Big Data

Analytics (ICBDA) (pp. 301-304). IEEE.

Grübler, J., Ghodsi, M. and Stehrer, R., 2021. Import demand elasticities revisited. The Journal

of International Trade & Economic Development, pp.1-29.

Jianchao, R.E.N. and Qing, H.A.N., 2018. Reason Analysis for Difference Between Consumer

Food Safety Risk Perception and Real Situation: From Information Supply and Demand

Perspective. Journal of Beijing University of Aeronautics and Astronautics Social

Sciences Edition, 31(4), p.75.

Opeskin, B., 2021. Rationing Justice: Tempering Demand for Courts in the Managerialist

State. University of New South Wales Law Journal, Forthcoming.

Reisman, D., 2018. Demand Management. In James Edward Meade (pp. 147-165). Palgrave

Macmillan, Cham.

Scheutz, M., 2017. Demand and charitable supply: Poverty and poor relief in Austria in the 18th

and 19th centuries. In Health Care and Poor Relief in 18th and 19th Century Southern

Europe (pp. 52-95). Routledge.

Shapiro, D.B., 2018. Payment to egg donors is the best way to ensure supply meets demand. Best

Practice & Research Clinical Obstetrics & Gynaecology, 53, pp.73-84.

Taghizadeh-Yazdi, M., Farrokhi, Z. and Mohammadi-Balani, A., 2020. An integrated inventory

model for multi-echelon supply chains with deteriorating items: a price-dependent

demand approach. Journal of Industrial and Production Engineering, 37(2-3), pp.87-

96.

10

Books and Journals

Chen, X.M. And et. al., 2018. Spatial visitation prediction of on-demand ride services using the

scaling law. Physica A: Statistical Mechanics and its Applications, 508, pp.84-94.

Choi, H., 2018. Disproving Market Demand and Market Supply. Available at SSRN 3203158.

Feng, G. and et. al., 2021, March. Research on the Demand Distribution of Aviation Equipment

Maintenance Spare Parts. In 2021 IEEE 6th International Conference on Big Data

Analytics (ICBDA) (pp. 301-304). IEEE.

Grübler, J., Ghodsi, M. and Stehrer, R., 2021. Import demand elasticities revisited. The Journal

of International Trade & Economic Development, pp.1-29.

Jianchao, R.E.N. and Qing, H.A.N., 2018. Reason Analysis for Difference Between Consumer

Food Safety Risk Perception and Real Situation: From Information Supply and Demand

Perspective. Journal of Beijing University of Aeronautics and Astronautics Social

Sciences Edition, 31(4), p.75.

Opeskin, B., 2021. Rationing Justice: Tempering Demand for Courts in the Managerialist

State. University of New South Wales Law Journal, Forthcoming.

Reisman, D., 2018. Demand Management. In James Edward Meade (pp. 147-165). Palgrave

Macmillan, Cham.

Scheutz, M., 2017. Demand and charitable supply: Poverty and poor relief in Austria in the 18th

and 19th centuries. In Health Care and Poor Relief in 18th and 19th Century Southern

Europe (pp. 52-95). Routledge.

Shapiro, D.B., 2018. Payment to egg donors is the best way to ensure supply meets demand. Best

Practice & Research Clinical Obstetrics & Gynaecology, 53, pp.73-84.

Taghizadeh-Yazdi, M., Farrokhi, Z. and Mohammadi-Balani, A., 2020. An integrated inventory

model for multi-echelon supply chains with deteriorating items: a price-dependent

demand approach. Journal of Industrial and Production Engineering, 37(2-3), pp.87-

96.

10

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.