Depreciation, Construction, and Impairment Problems

VerifiedAdded on 2020/03/15

|6

|1037

|228

Homework Assignment

AI Summary

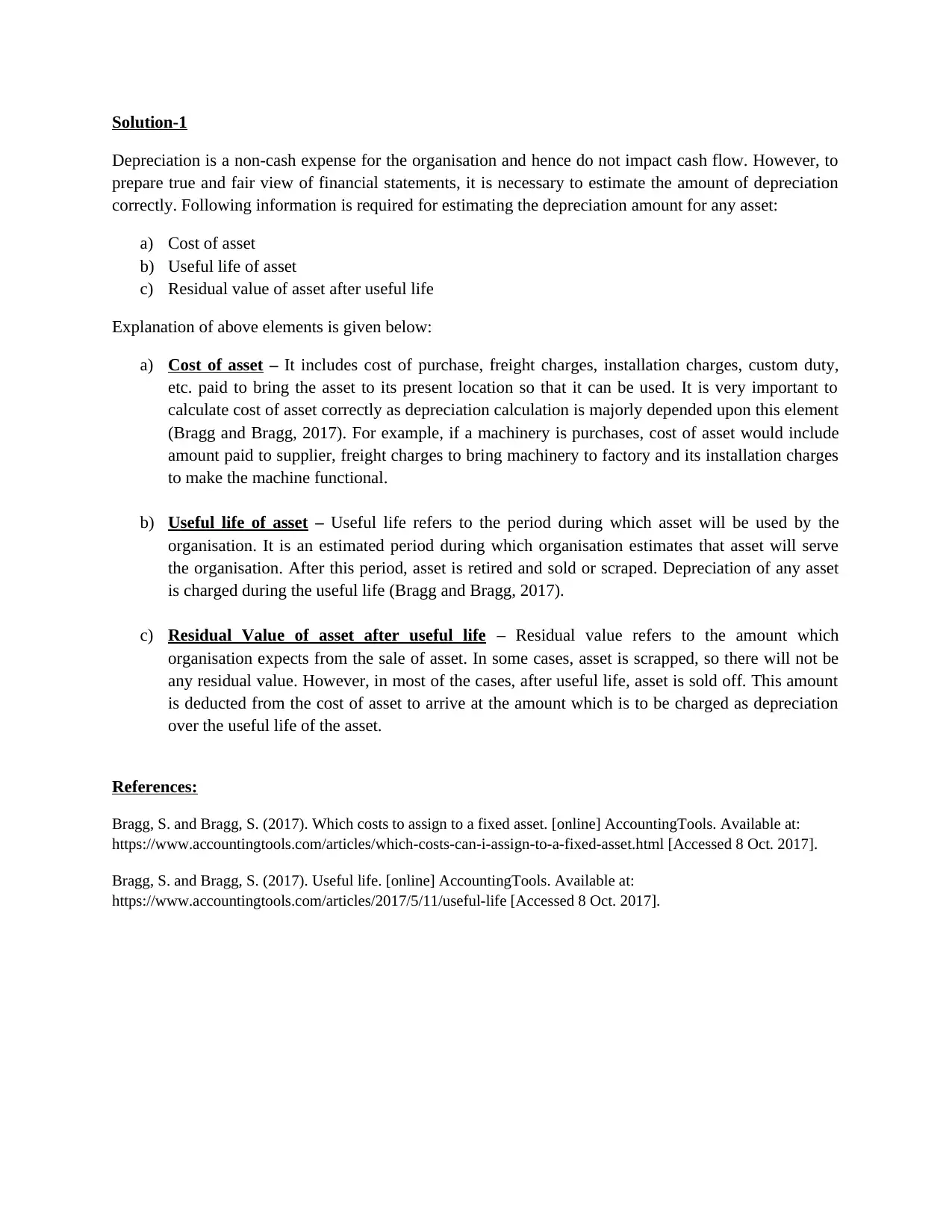

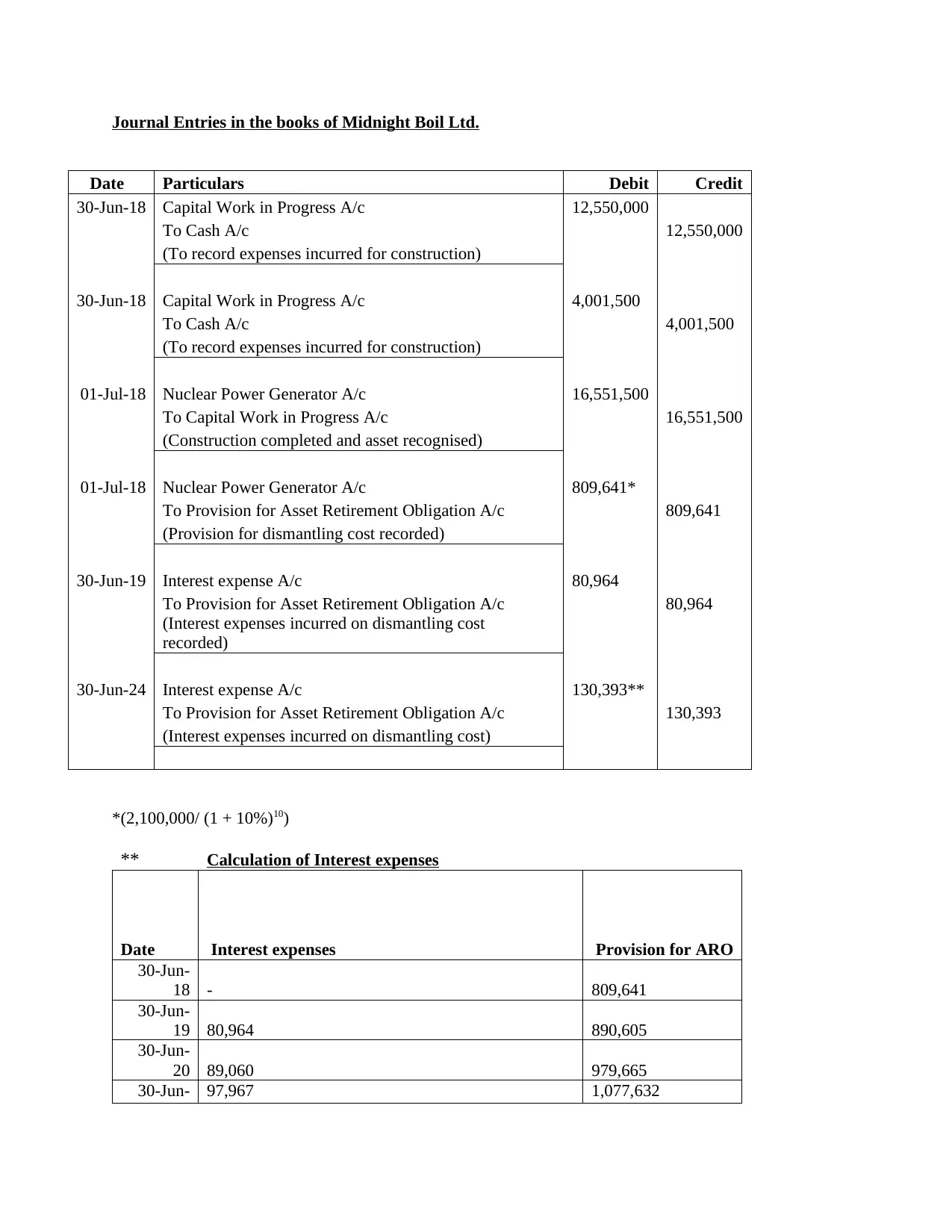

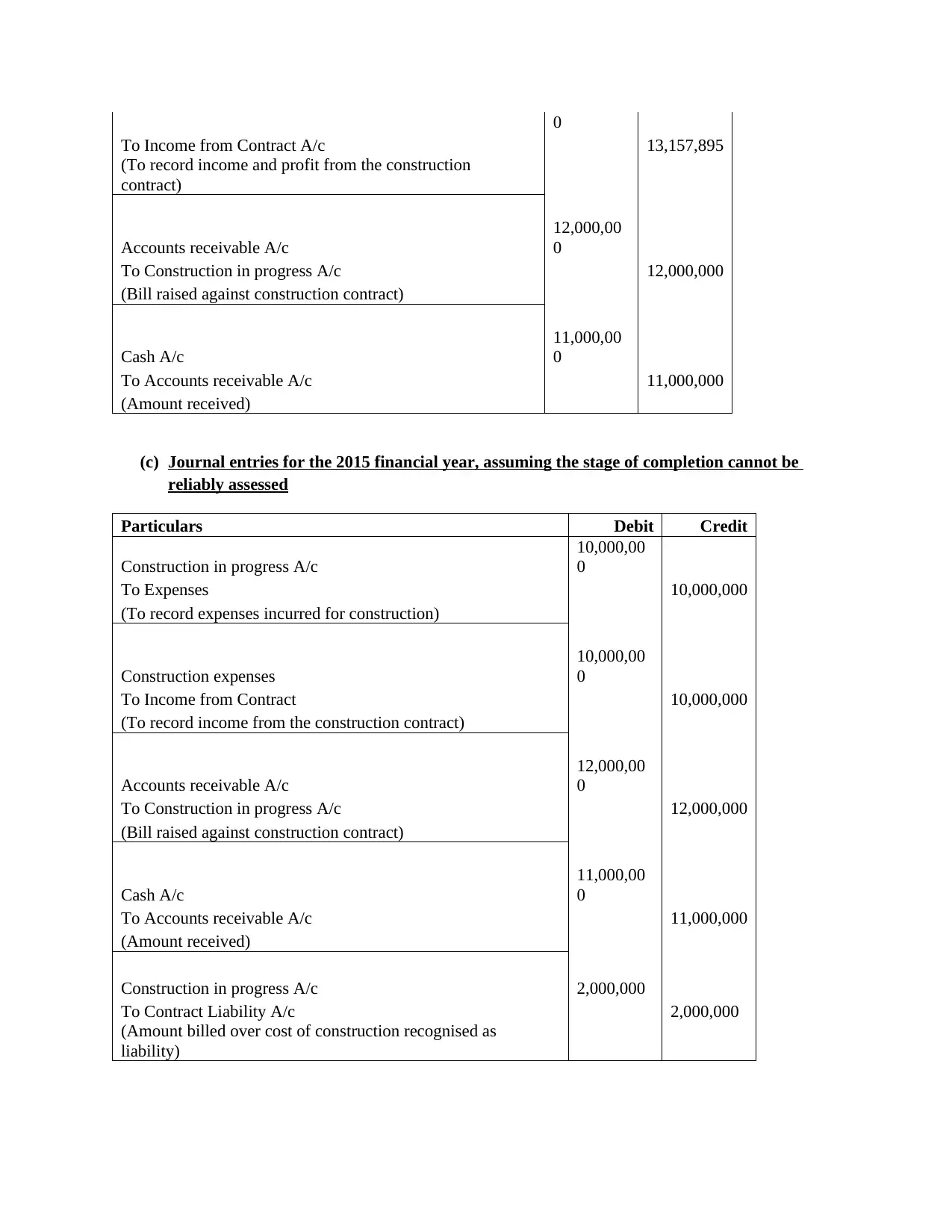

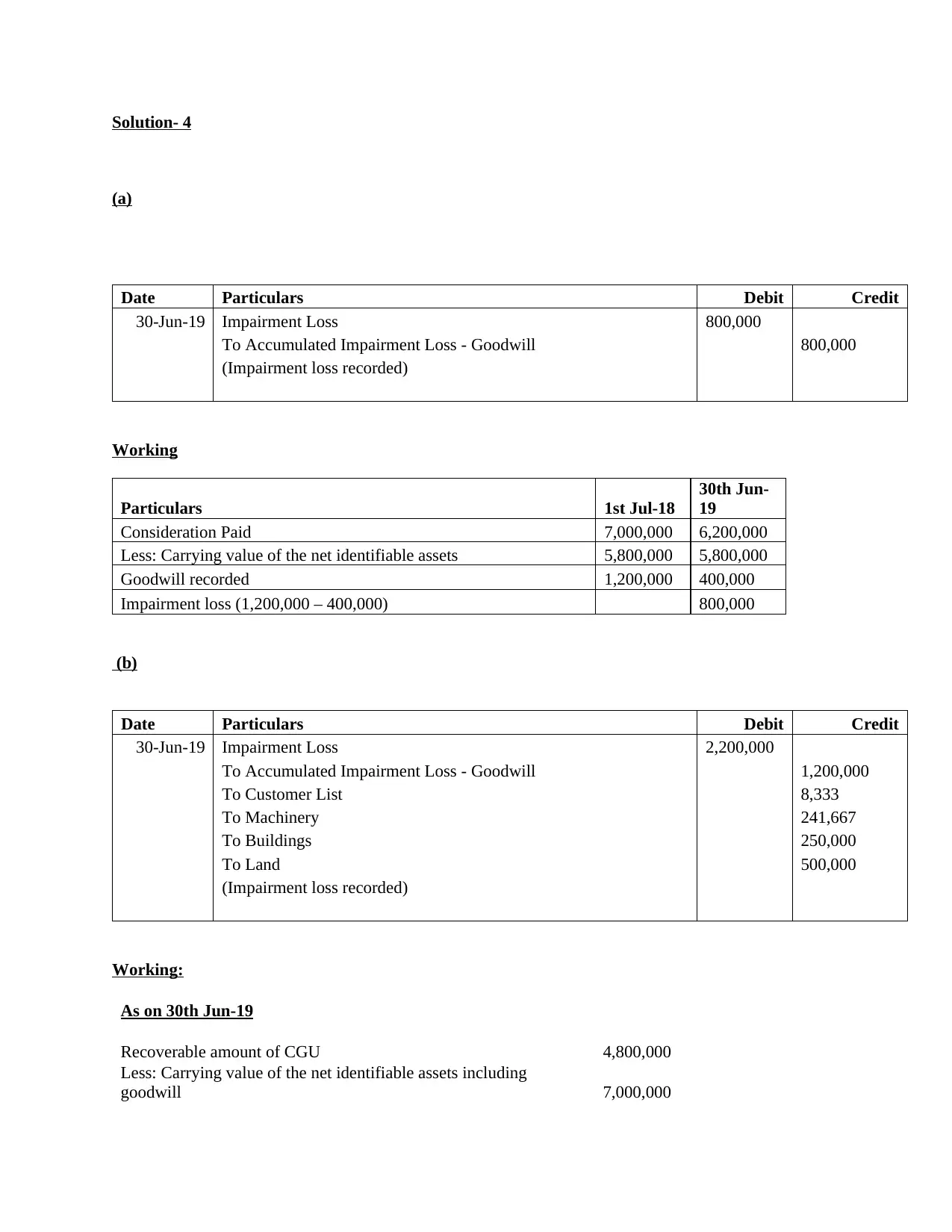

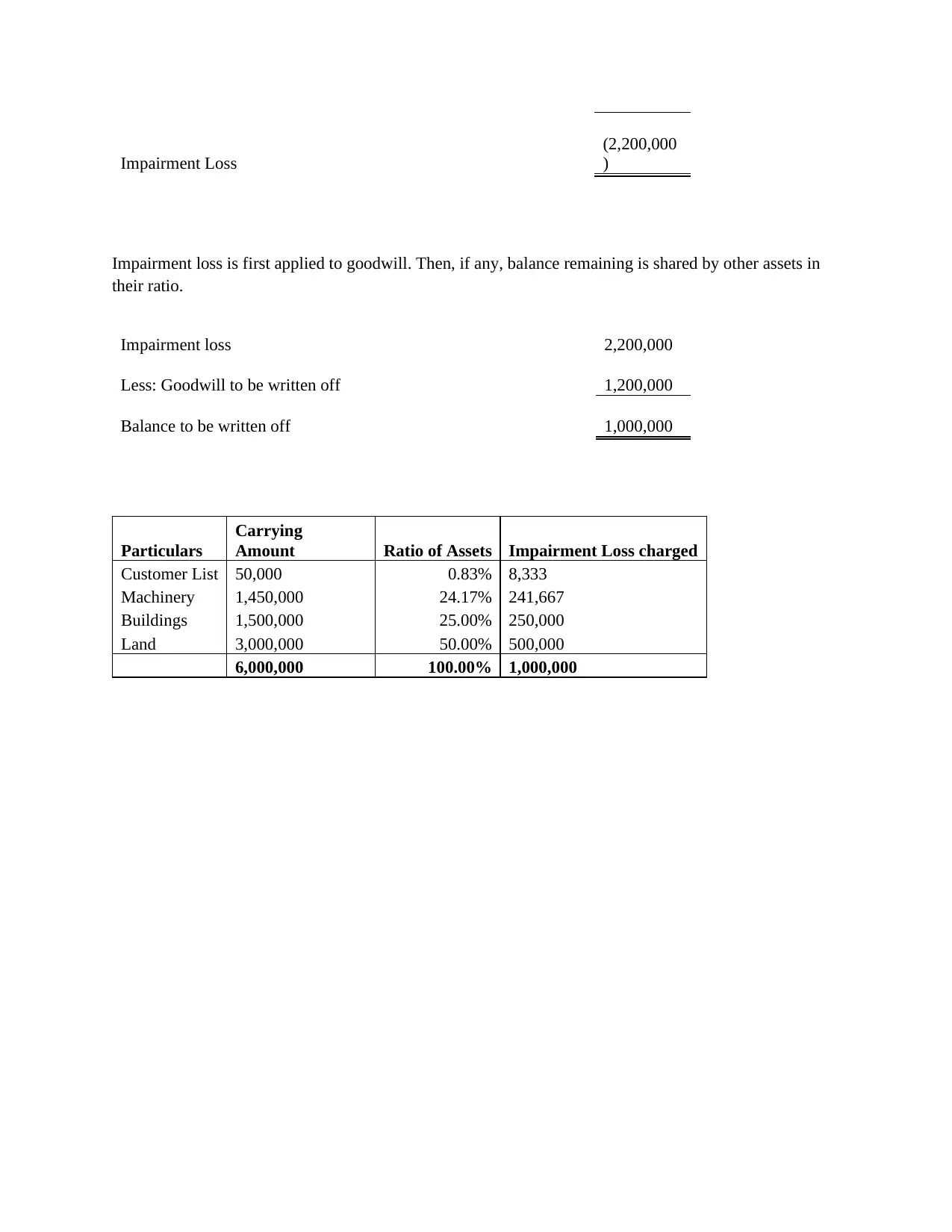

This assignment provides detailed solutions to several financial accounting problems. The first solution addresses depreciation, explaining the key elements required for its calculation, including the cost of the asset, useful life, and residual value, along with related journal entries for a nuclear power generator. The second solution calculates gross profit for a construction contract using the percentage-of-completion method, including journal entries for both the 2015 financial year under two scenarios: reliable assessment and unreliable assessment of the stage of completion. The third solution deals with impairment losses, calculating the impairment loss for goodwill and other assets, including the journal entries for recording the loss. These solutions cover various aspects of accounting, providing a comprehensive understanding of depreciation, construction accounting, and impairment.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.