Derivatives Solved Assignment

VerifiedAdded on 2019/11/19

|6

|533

|125

Homework Assignment

AI Summary

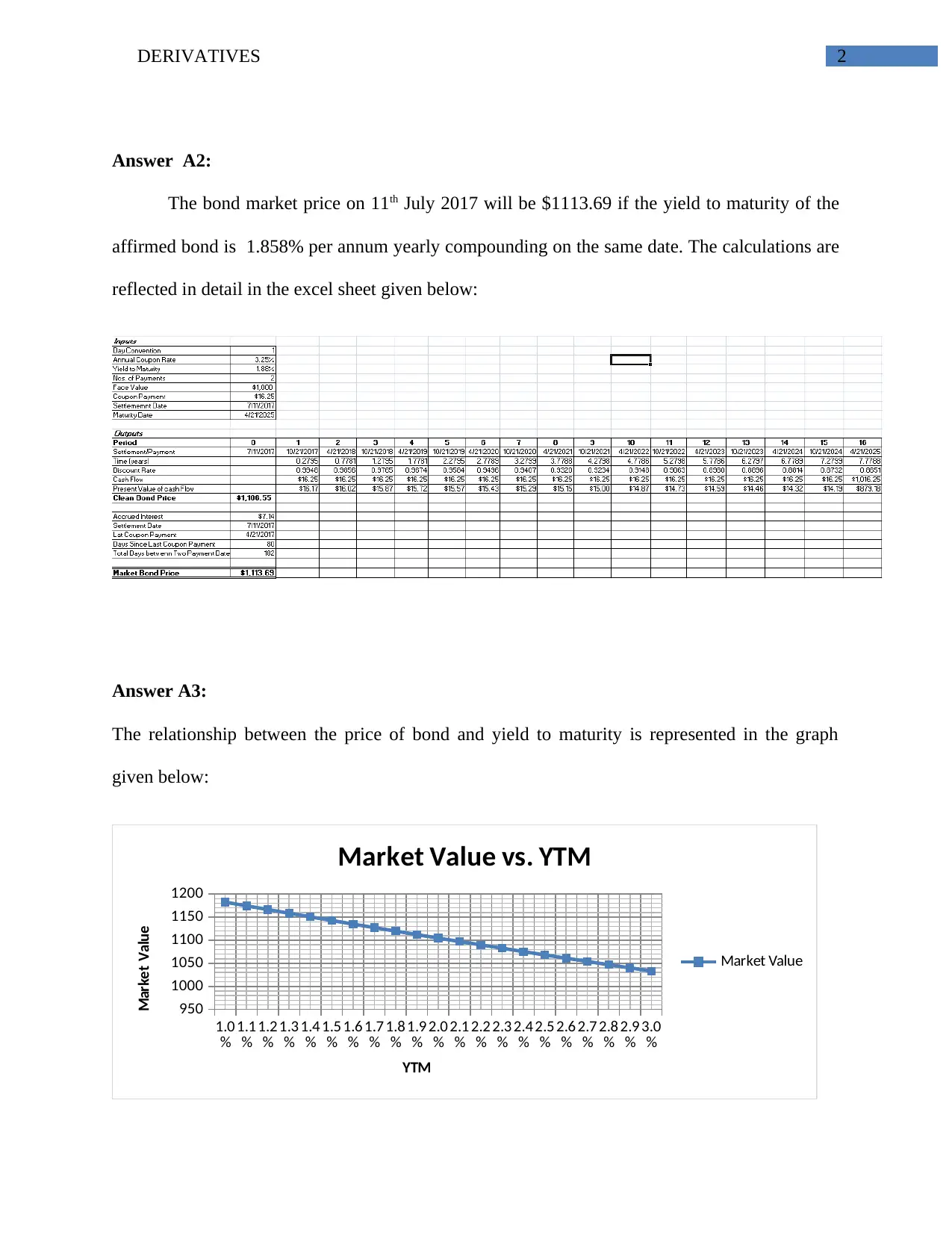

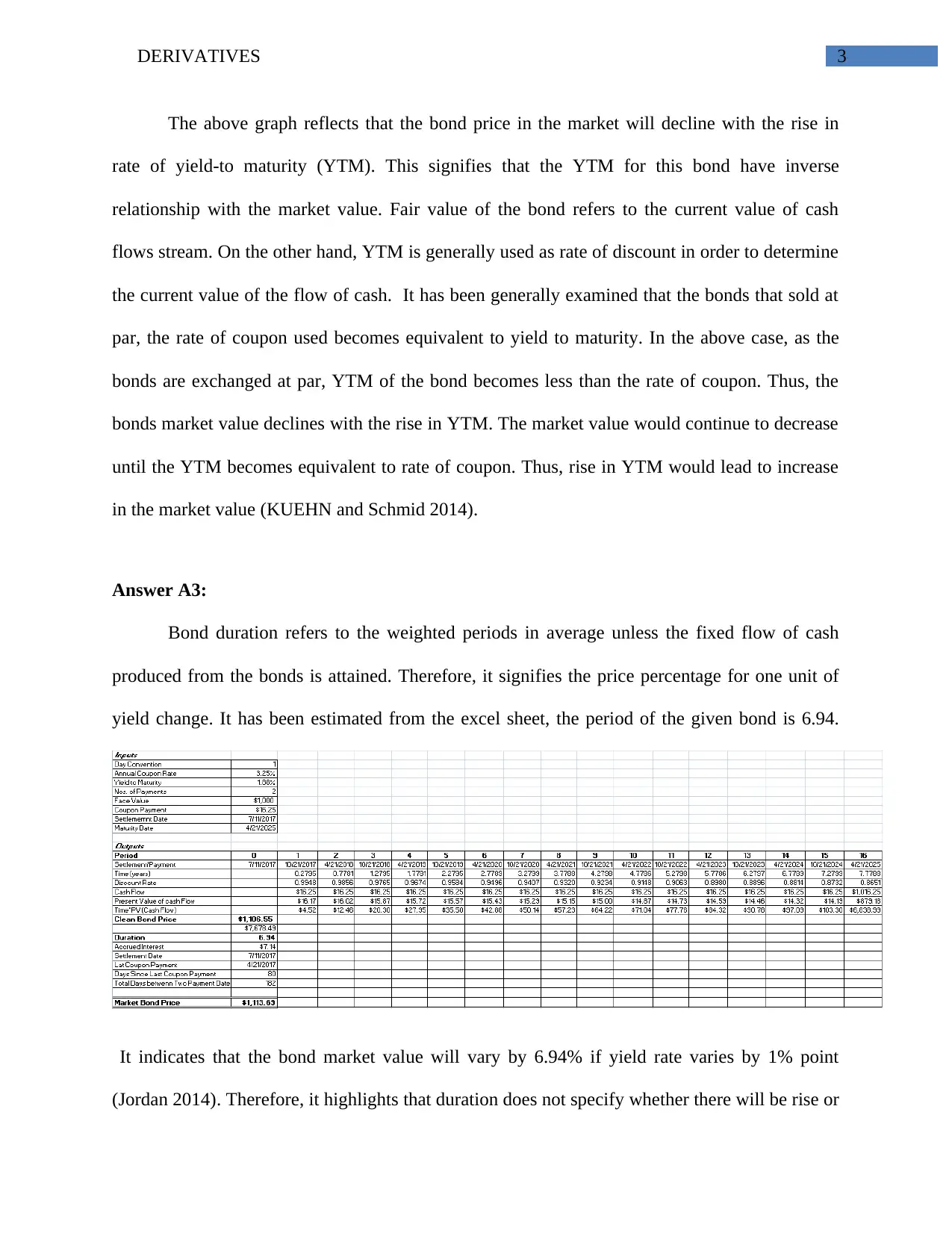

This homework assignment focuses on derivatives, specifically addressing bond pricing and the relationship between bond price and yield to maturity (YTM). The solution includes calculations demonstrating how to determine the bond market price given a specific YTM. A graph illustrates the inverse relationship between bond price and YTM. The concept of bond duration is explained, highlighting its significance in understanding price sensitivity to yield changes. The solution also mentions the importance of considering bond convexity alongside duration for a complete understanding of price movements. The assignment utilizes an Excel sheet (not included in the provided text) for detailed calculations. References to relevant finance textbooks and academic journals are provided.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.