Management Accounting Report: Imda Tech (UK) Limited Analysis

VerifiedAdded on 2020/01/07

|15

|4132

|185

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and their application within a business context. It begins by defining and distinguishing management accounting from financial accounting, emphasizing its role in providing crucial information for departmental managers to achieve organizational goals. The report then delves into various cost accounting systems, including actual, normal, and standard costing, explaining their methodologies and how they can improve the functionality of different departments. Inventory management systems, such as Just-In-Time and Materials Requirement Planning, are also discussed. Furthermore, the report presents income statements prepared using both absorption and marginal costing methods for Imda Tech (UK) Limited. It explores different types of budgets, their advantages and disadvantages, and the process of preparing them, along with a discussion of pricing strategies. Finally, the report examines the Balanced Scorecard approach and its application in measuring a range of performance metrics. The report aims to enhance financial governance and effective strategies for business development.

MANAGEMENT ACCOUNTING

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of contents

Introduction......................................................................................................................................3

Task 1...............................................................................................................................................3

a) Preparation of research report based on the function of management accounting......................3

b) Discussing the different types of cost accounting system and explaining the ways it can be

used to improve the functionality of various departments...............................................................4

Task 2...............................................................................................................................................6

a) Preparing the income statements for the month of September....................................................6

Task 3.............................................................................................................................................10

a) Discussing different types of budgets in the research report and explaining their advantages

and disadvantages..........................................................................................................................10

b) Discussing the process of preparing various budgets................................................................11

c) Discussing the pricing strategies...............................................................................................11

Task 4.............................................................................................................................................12

a) Explaining the approach of balance score card and describing how it can be used to measure

range of performance.....................................................................................................................12

Conclusion.....................................................................................................................................13

Reference list.................................................................................................................................14

2

Introduction......................................................................................................................................3

Task 1...............................................................................................................................................3

a) Preparation of research report based on the function of management accounting......................3

b) Discussing the different types of cost accounting system and explaining the ways it can be

used to improve the functionality of various departments...............................................................4

Task 2...............................................................................................................................................6

a) Preparing the income statements for the month of September....................................................6

Task 3.............................................................................................................................................10

a) Discussing different types of budgets in the research report and explaining their advantages

and disadvantages..........................................................................................................................10

b) Discussing the process of preparing various budgets................................................................11

c) Discussing the pricing strategies...............................................................................................11

Task 4.............................................................................................................................................12

a) Explaining the approach of balance score card and describing how it can be used to measure

range of performance.....................................................................................................................12

Conclusion.....................................................................................................................................13

Reference list.................................................................................................................................14

2

Introduction

Management accounting may be defined as the process identifying and measuring the business

information with an aim to evaluate, interpret and communicate them with the departmental

managers for achieving goals and objectives. The study aims to express the management

accounting along with its need in the context of emerging business for achieving specific targets,

based on the measurement of performance of the business. It has also been aimed to understand

the various types of cost accounting both theoretically and practically to deliver the need if

budgeting and pricing strategy. In addition to these, with the help of balance score card, it has

been aimed to improve financials governance and effective strategies.

Task 1

a) Preparation of research report based on the function of management

accounting

1) Defining and distinguishing management accounting with financial accounting

Cost accounting may sometimes refer to the management accounting, which is completely

different from financial accounting. In management accounting, both business and financial

information are identified, measured, analyzed and interpreted with an aim to communicate them

with various management departments to achieve goal and objectives. It simply encompasses all

the relevant fields of accounting that are aimed to inform the business operation metrics to the

management. In this approach, information related to the cost of the goods and services

purchased and produced by the organization are considered (Fullerton et al. 2014). It can be said

that management accounting or cost accounting are the basis of financial accounting, because,

without the result of cost accounting any decision made by the department will become void and

the actual cause and effect of the cost of production will remain unknown. Therefore, it will

become impossible to know the actual volume of sale, revenue, and profit (Fullerton et al. 2013).

In cost accounting, various budgets are prepared to estimate the various requirement of the

department and once the actual results are disclosed, the estimated value is compared with the

actual results to understand the variance.

However, in financial accounting, especially the financial information are identified, measured,

interpreted, summarized and recorded in a chronological order with an aim to communications

3

Management accounting may be defined as the process identifying and measuring the business

information with an aim to evaluate, interpret and communicate them with the departmental

managers for achieving goals and objectives. The study aims to express the management

accounting along with its need in the context of emerging business for achieving specific targets,

based on the measurement of performance of the business. It has also been aimed to understand

the various types of cost accounting both theoretically and practically to deliver the need if

budgeting and pricing strategy. In addition to these, with the help of balance score card, it has

been aimed to improve financials governance and effective strategies.

Task 1

a) Preparation of research report based on the function of management

accounting

1) Defining and distinguishing management accounting with financial accounting

Cost accounting may sometimes refer to the management accounting, which is completely

different from financial accounting. In management accounting, both business and financial

information are identified, measured, analyzed and interpreted with an aim to communicate them

with various management departments to achieve goal and objectives. It simply encompasses all

the relevant fields of accounting that are aimed to inform the business operation metrics to the

management. In this approach, information related to the cost of the goods and services

purchased and produced by the organization are considered (Fullerton et al. 2014). It can be said

that management accounting or cost accounting are the basis of financial accounting, because,

without the result of cost accounting any decision made by the department will become void and

the actual cause and effect of the cost of production will remain unknown. Therefore, it will

become impossible to know the actual volume of sale, revenue, and profit (Fullerton et al. 2013).

In cost accounting, various budgets are prepared to estimate the various requirement of the

department and once the actual results are disclosed, the estimated value is compared with the

actual results to understand the variance.

However, in financial accounting, especially the financial information are identified, measured,

interpreted, summarized and recorded in a chronological order with an aim to communications

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the financial information with the stakeholders (internal and external users of financial

statements). Financial accounting is done based on certain accounting principles or policies or

accounting standards since the concept of relevancy, reliability, and objectivity gets attracted, so

that it cannot divert the mindset of the users of financial accounting (Beatty and Liao, 2014).

Thus, it can be said that financial accounting is the sum or aggregation of all the financial

information of the business.

2) Describing the importance of cost accounting and how it can be considered as the

decision making tool for the various departmental managers

Management accounting helps in making short-term and long-term decisions by the managers

with the help of financial and statistical information periodically. Cost accounting helps in

forecasting decision, making or buying decision, evaluating the rate of return and predicting the

cash flows. In a broader concept, managerial accounting deals with the preparation of report,

which includes budgeting for estimating and forecasting. Variance analysis is used for making

comparison of actual with the standards and identifying any reason behind favorable and

unfavorable variance (Christ and Burritt, 2015). In addition to these, trend analysis helps the

managers to make future estimation regarding their ability of achieving the targets by comparing

with historical records and other records of other organization. Thus, it can be said that cost

accounting is the key decision making tool for various departmental managers, like production

manager, sales manager, purchase manager, etc.

b) Discussing the different types of cost accounting system and explaining the

ways it can be used to improve the functionality of various departments

1) Describing different cost accounting system individually

Actual costing

Actual costing is the part of the accounting system, where the actual cost of the actual qualities

of the product is used along with the direct cost rates in the production unit to ascertain the cost

of a particular good. Generally, in actual cost accounting system, the direct cost of the object is

traced which can be measured in terms of labor cost and material cost, which are directly linked

with the production unit (Greenberg and Wilner, 2015). With the help of actual costing method,

managers evaluate the actual time and cost required for the production of goods and services. In

other words, it addresses the time to be taken for manufacturing the product with respect to the

4

statements). Financial accounting is done based on certain accounting principles or policies or

accounting standards since the concept of relevancy, reliability, and objectivity gets attracted, so

that it cannot divert the mindset of the users of financial accounting (Beatty and Liao, 2014).

Thus, it can be said that financial accounting is the sum or aggregation of all the financial

information of the business.

2) Describing the importance of cost accounting and how it can be considered as the

decision making tool for the various departmental managers

Management accounting helps in making short-term and long-term decisions by the managers

with the help of financial and statistical information periodically. Cost accounting helps in

forecasting decision, making or buying decision, evaluating the rate of return and predicting the

cash flows. In a broader concept, managerial accounting deals with the preparation of report,

which includes budgeting for estimating and forecasting. Variance analysis is used for making

comparison of actual with the standards and identifying any reason behind favorable and

unfavorable variance (Christ and Burritt, 2015). In addition to these, trend analysis helps the

managers to make future estimation regarding their ability of achieving the targets by comparing

with historical records and other records of other organization. Thus, it can be said that cost

accounting is the key decision making tool for various departmental managers, like production

manager, sales manager, purchase manager, etc.

b) Discussing the different types of cost accounting system and explaining the

ways it can be used to improve the functionality of various departments

1) Describing different cost accounting system individually

Actual costing

Actual costing is the part of the accounting system, where the actual cost of the actual qualities

of the product is used along with the direct cost rates in the production unit to ascertain the cost

of a particular good. Generally, in actual cost accounting system, the direct cost of the object is

traced which can be measured in terms of labor cost and material cost, which are directly linked

with the production unit (Greenberg and Wilner, 2015). With the help of actual costing method,

managers evaluate the actual time and cost required for the production of goods and services. In

other words, it addresses the time to be taken for manufacturing the product with respect to the

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

actual cost incurred in that product. Direct labor hour rate determines how long the particular

product takes to get converted into finished goods based on the cost incurred on the raw

materials.

Normal costing

Normal costing helps in deriving the cost of a particular product. Normal costing is used in

measuring the value of the manufactured product in accordance with the actual material and

direct labor cost and manufacturing overhead (Kutač et al. 2014). However, these three costs of

production determine the cost of goods sold and ascertains the inventory valuation. In this

approach variance between the actual cost incurred in the production and the budgeted overhead

is analyzed. If the amount of variance is found insignificant to the actual production cost, it will

simply be assigned to the cost of goods sold. On the other hand, if the amount of variance is

found significant, it will simply be assigned to the cost of goods sold and work in progress on a

proportionate ratio basis.

Standard costing

Standard costing may be defined as the process of estimating the cost or expenses, which

normally occurs during the manufacturing of the product. In simple words, standard costing

helps in determining the amount of cost or expenses that a business organization will incur in

producing a particular product under the normal condition (Badem et al. 2013). However,

standard costing can be used in two different ways, which are discussed below.

● In the first way it can be used to make plan that how future production process can be

done and how efficiencies of production can be increased

● In the second way, it can be used to determine whether the cost incurred in the production

process are reasonable or not and if it is found reasonable then to what extent

2) Describing inventory management systems

Inventory management may be defined as the practice of monitoring and overseeing the

ordering, storing and using the components of production items in order to sell them afterward.

In other words, inventory management is the practice of controlling the quantities of finished

products stored for sealing purpose (Ozguven and Ozbay, 2013). Inventory is the major assets of

a business and it can be represented as the investment of the business that is tied up until it is

sold out. The cost of purchasing inventory, the cost of storing and insuring inventory are the key

parts of inventory management within the business organization. Thus, it becomes very

5

product takes to get converted into finished goods based on the cost incurred on the raw

materials.

Normal costing

Normal costing helps in deriving the cost of a particular product. Normal costing is used in

measuring the value of the manufactured product in accordance with the actual material and

direct labor cost and manufacturing overhead (Kutač et al. 2014). However, these three costs of

production determine the cost of goods sold and ascertains the inventory valuation. In this

approach variance between the actual cost incurred in the production and the budgeted overhead

is analyzed. If the amount of variance is found insignificant to the actual production cost, it will

simply be assigned to the cost of goods sold. On the other hand, if the amount of variance is

found significant, it will simply be assigned to the cost of goods sold and work in progress on a

proportionate ratio basis.

Standard costing

Standard costing may be defined as the process of estimating the cost or expenses, which

normally occurs during the manufacturing of the product. In simple words, standard costing

helps in determining the amount of cost or expenses that a business organization will incur in

producing a particular product under the normal condition (Badem et al. 2013). However,

standard costing can be used in two different ways, which are discussed below.

● In the first way it can be used to make plan that how future production process can be

done and how efficiencies of production can be increased

● In the second way, it can be used to determine whether the cost incurred in the production

process are reasonable or not and if it is found reasonable then to what extent

2) Describing inventory management systems

Inventory management may be defined as the practice of monitoring and overseeing the

ordering, storing and using the components of production items in order to sell them afterward.

In other words, inventory management is the practice of controlling the quantities of finished

products stored for sealing purpose (Ozguven and Ozbay, 2013). Inventory is the major assets of

a business and it can be represented as the investment of the business that is tied up until it is

sold out. The cost of purchasing inventory, the cost of storing and insuring inventory are the key

parts of inventory management within the business organization. Thus, it becomes very

5

important for an organization to manage the inventories of the business properly because if the

inventories are mismatched or mismanaged, it might create a huge difference in the financial

statements. Hence, in order to successfully manage the inventories of the business, it becomes

important to create purchase plan ensuring the required inventories are available whenever they

are required. However, it is necessary to keep track on the inventories or monitoring the

inventories, so that excess or under requirements of the inventories are not purchased. The two

common and important strategies for managing inventories are followed by the management,

which is described below.

Just In Time method (JIT)

In this method, inventories are purchased whenever they are required instead of maintaining high

level of stock for future use. This approach helps the companies not only to reduce the wastage

of inventories, but also reducing the cost of carrying, storing and insuring the inventories.

Maximum Requirement Planning (MRP)

In this method deliveries of the material are determined based on the sales forecast. In simpler

words, the management makes accurate sales records to make appropriate planning for carrying

inventories.

3) Describing price optimizing system

Price optimization system is a mathematical approach for determining the response of the

consumers towards different prices of the products manufactured by the company through

different channels. Price optimization technique also helps in determining the price of the

produced goods in the most profitable way, so that cost of production is covered along with the

profit maximization through the selling of that product (Ubando et al. 2014). Companies make

use of this technique to ascertain the price structure for initial, promotional and discount pricing.

In this method, the demand of the consumers is reviewed to know how it varies at different price

points. Based on the evaluation of varied demand of the customers at different price points and

inventory levels, the profitable price point is developed.

Task 2

a) Preparing the income statements for the month of September

1) Absorption costing method

6

inventories are mismatched or mismanaged, it might create a huge difference in the financial

statements. Hence, in order to successfully manage the inventories of the business, it becomes

important to create purchase plan ensuring the required inventories are available whenever they

are required. However, it is necessary to keep track on the inventories or monitoring the

inventories, so that excess or under requirements of the inventories are not purchased. The two

common and important strategies for managing inventories are followed by the management,

which is described below.

Just In Time method (JIT)

In this method, inventories are purchased whenever they are required instead of maintaining high

level of stock for future use. This approach helps the companies not only to reduce the wastage

of inventories, but also reducing the cost of carrying, storing and insuring the inventories.

Maximum Requirement Planning (MRP)

In this method deliveries of the material are determined based on the sales forecast. In simpler

words, the management makes accurate sales records to make appropriate planning for carrying

inventories.

3) Describing price optimizing system

Price optimization system is a mathematical approach for determining the response of the

consumers towards different prices of the products manufactured by the company through

different channels. Price optimization technique also helps in determining the price of the

produced goods in the most profitable way, so that cost of production is covered along with the

profit maximization through the selling of that product (Ubando et al. 2014). Companies make

use of this technique to ascertain the price structure for initial, promotional and discount pricing.

In this method, the demand of the consumers is reviewed to know how it varies at different price

points. Based on the evaluation of varied demand of the customers at different price points and

inventory levels, the profitable price point is developed.

Task 2

a) Preparing the income statements for the month of September

1) Absorption costing method

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

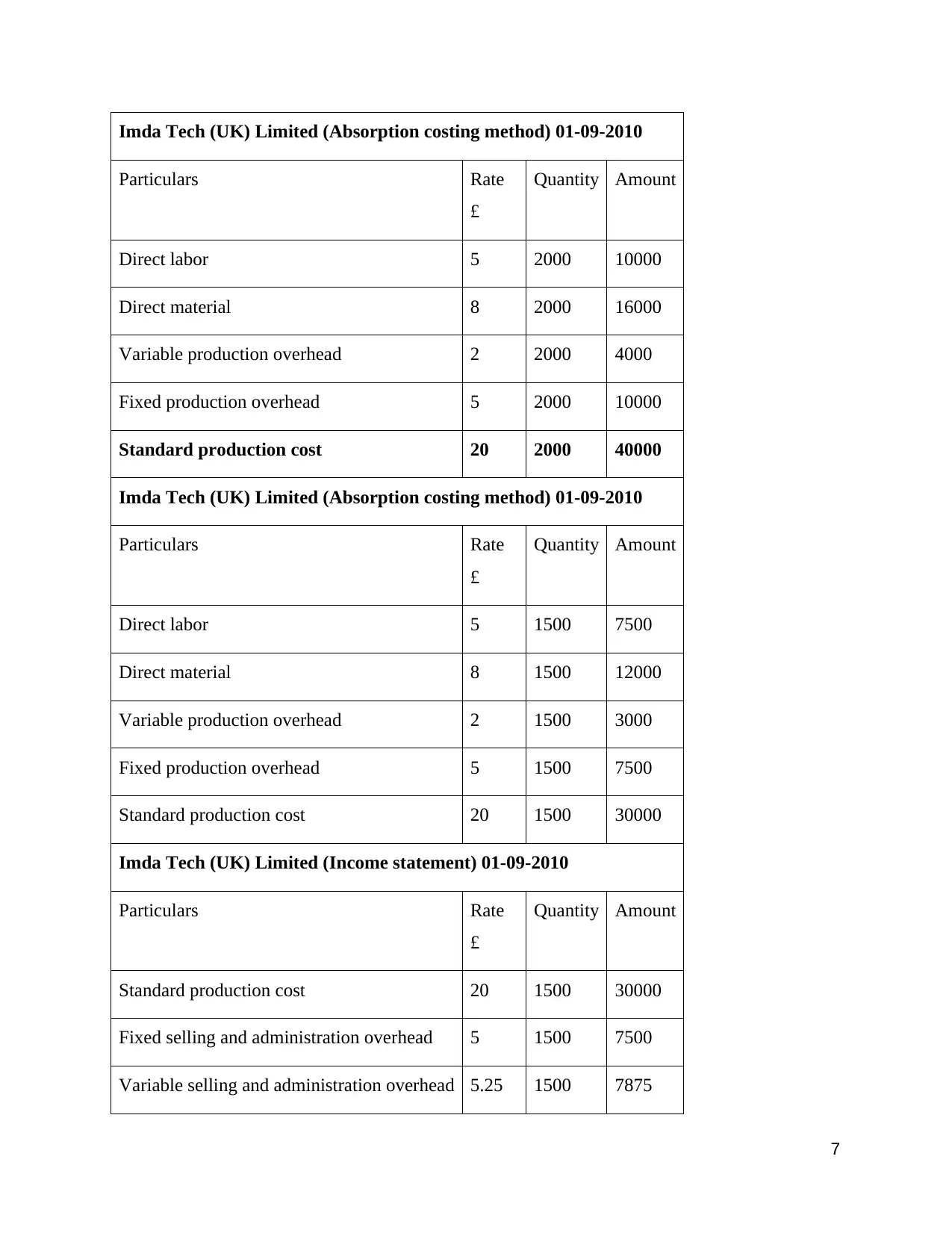

Imda Tech (UK) Limited (Absorption costing method) 01-09-2010

Particulars Rate

£

Quantity Amount

Direct labor 5 2000 10000

Direct material 8 2000 16000

Variable production overhead 2 2000 4000

Fixed production overhead 5 2000 10000

Standard production cost 20 2000 40000

Imda Tech (UK) Limited (Absorption costing method) 01-09-2010

Particulars Rate

£

Quantity Amount

Direct labor 5 1500 7500

Direct material 8 1500 12000

Variable production overhead 2 1500 3000

Fixed production overhead 5 1500 7500

Standard production cost 20 1500 30000

Imda Tech (UK) Limited (Income statement) 01-09-2010

Particulars Rate

£

Quantity Amount

Standard production cost 20 1500 30000

Fixed selling and administration overhead 5 1500 7500

Variable selling and administration overhead 5.25 1500 7875

7

Particulars Rate

£

Quantity Amount

Direct labor 5 2000 10000

Direct material 8 2000 16000

Variable production overhead 2 2000 4000

Fixed production overhead 5 2000 10000

Standard production cost 20 2000 40000

Imda Tech (UK) Limited (Absorption costing method) 01-09-2010

Particulars Rate

£

Quantity Amount

Direct labor 5 1500 7500

Direct material 8 1500 12000

Variable production overhead 2 1500 3000

Fixed production overhead 5 1500 7500

Standard production cost 20 1500 30000

Imda Tech (UK) Limited (Income statement) 01-09-2010

Particulars Rate

£

Quantity Amount

Standard production cost 20 1500 30000

Fixed selling and administration overhead 5 1500 7500

Variable selling and administration overhead 5.25 1500 7875

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

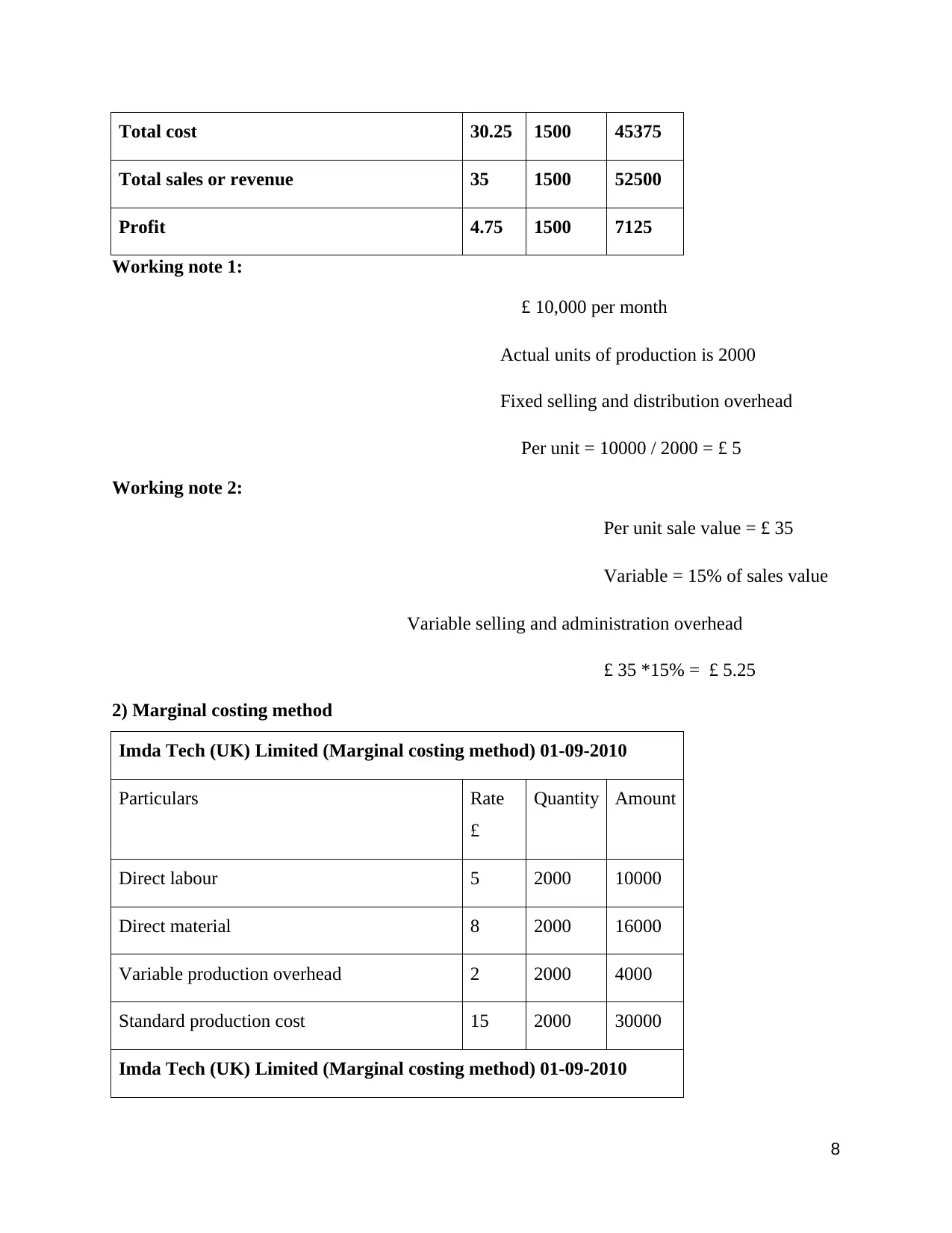

Total cost 30.25 1500 45375

Total sales or revenue 35 1500 52500

Profit 4.75 1500 7125

Working note 1:

£ 10,000 per month

Actual units of production is 2000

Fixed selling and distribution overhead

Per unit = 10000 / 2000 = £ 5

Working note 2:

Per unit sale value = £ 35

Variable = 15% of sales value

Variable selling and administration overhead

£ 35 *15% = £ 5.25

2) Marginal costing method

Imda Tech (UK) Limited (Marginal costing method) 01-09-2010

Particulars Rate

£

Quantity Amount

Direct labour 5 2000 10000

Direct material 8 2000 16000

Variable production overhead 2 2000 4000

Standard production cost 15 2000 30000

Imda Tech (UK) Limited (Marginal costing method) 01-09-2010

8

Total sales or revenue 35 1500 52500

Profit 4.75 1500 7125

Working note 1:

£ 10,000 per month

Actual units of production is 2000

Fixed selling and distribution overhead

Per unit = 10000 / 2000 = £ 5

Working note 2:

Per unit sale value = £ 35

Variable = 15% of sales value

Variable selling and administration overhead

£ 35 *15% = £ 5.25

2) Marginal costing method

Imda Tech (UK) Limited (Marginal costing method) 01-09-2010

Particulars Rate

£

Quantity Amount

Direct labour 5 2000 10000

Direct material 8 2000 16000

Variable production overhead 2 2000 4000

Standard production cost 15 2000 30000

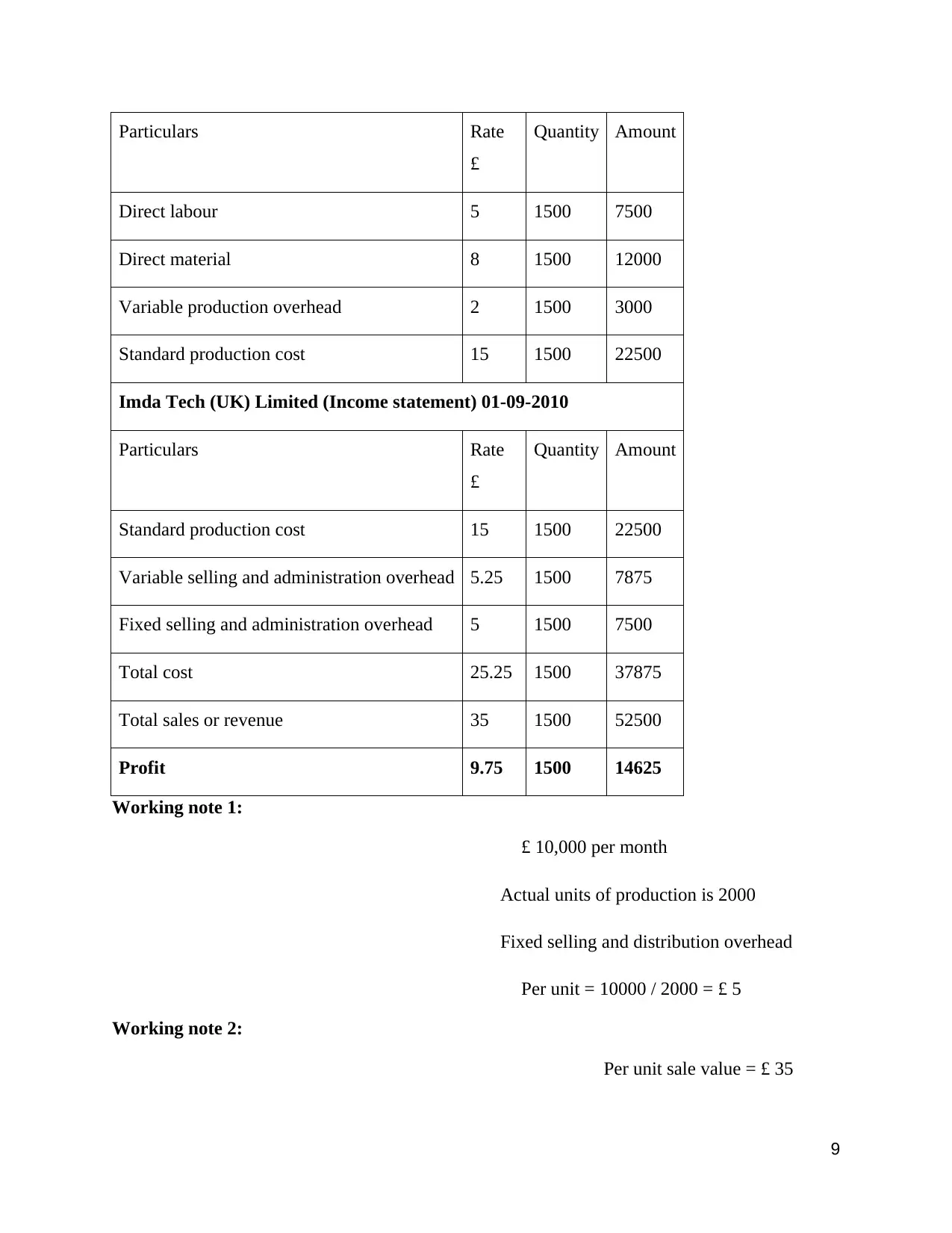

Imda Tech (UK) Limited (Marginal costing method) 01-09-2010

8

Particulars Rate

£

Quantity Amount

Direct labour 5 1500 7500

Direct material 8 1500 12000

Variable production overhead 2 1500 3000

Standard production cost 15 1500 22500

Imda Tech (UK) Limited (Income statement) 01-09-2010

Particulars Rate

£

Quantity Amount

Standard production cost 15 1500 22500

Variable selling and administration overhead 5.25 1500 7875

Fixed selling and administration overhead 5 1500 7500

Total cost 25.25 1500 37875

Total sales or revenue 35 1500 52500

Profit 9.75 1500 14625

Working note 1:

£ 10,000 per month

Actual units of production is 2000

Fixed selling and distribution overhead

Per unit = 10000 / 2000 = £ 5

Working note 2:

Per unit sale value = £ 35

9

£

Quantity Amount

Direct labour 5 1500 7500

Direct material 8 1500 12000

Variable production overhead 2 1500 3000

Standard production cost 15 1500 22500

Imda Tech (UK) Limited (Income statement) 01-09-2010

Particulars Rate

£

Quantity Amount

Standard production cost 15 1500 22500

Variable selling and administration overhead 5.25 1500 7875

Fixed selling and administration overhead 5 1500 7500

Total cost 25.25 1500 37875

Total sales or revenue 35 1500 52500

Profit 9.75 1500 14625

Working note 1:

£ 10,000 per month

Actual units of production is 2000

Fixed selling and distribution overhead

Per unit = 10000 / 2000 = £ 5

Working note 2:

Per unit sale value = £ 35

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Variable = 15% of sales value

Variable selling and administration overhead

£ 35 *15% = £ 5.25

Task 3

a) Discussing different types of budgets in the research report and explaining

their advantages and disadvantages

Master budget

This is the type of the budgets that are being prepared by the organisations. Additionally, these

budgets are used to determine the business expenses (Cox, 2014). Additionally, when the firm’s

or the organisation is doing this budget then they are considering the different expenses of the

organisation weather it may be the sales forecast, purchases, capital investment and other

aspects that are linked with the monetary terms. Moreover, this is also considered as the strategic

plan for the entire organisation.

Operating budget

Additionally, in this budget it can be analyzed that this is being divided in different parts and

they are what will be the expected cost in the future, forecasted income and the know expenses.

Additionally, these three things are being considered to be the most important factors. Moreover,

when owners are commencing their business then they often consider these three parameters and

after that they commence their business. Similarly, this budget is being prepared by the

accountants from beforehand only.

Financial budget

Similarly, this is the budget that is being estimated in a particular financial year. Additionally,

here it is being analyzed that budgets are being prepared and according to that organisations are

doing their work (Isakov and Pekarski, 2016). Moreover, the rate of success and failure of the

organisations or the firms depends on the estimated budgets that are being prepared. In this part

it reflects all the income and the expenses of the organisation.

Cash Flow budget

10

Variable selling and administration overhead

£ 35 *15% = £ 5.25

Task 3

a) Discussing different types of budgets in the research report and explaining

their advantages and disadvantages

Master budget

This is the type of the budgets that are being prepared by the organisations. Additionally, these

budgets are used to determine the business expenses (Cox, 2014). Additionally, when the firm’s

or the organisation is doing this budget then they are considering the different expenses of the

organisation weather it may be the sales forecast, purchases, capital investment and other

aspects that are linked with the monetary terms. Moreover, this is also considered as the strategic

plan for the entire organisation.

Operating budget

Additionally, in this budget it can be analyzed that this is being divided in different parts and

they are what will be the expected cost in the future, forecasted income and the know expenses.

Additionally, these three things are being considered to be the most important factors. Moreover,

when owners are commencing their business then they often consider these three parameters and

after that they commence their business. Similarly, this budget is being prepared by the

accountants from beforehand only.

Financial budget

Similarly, this is the budget that is being estimated in a particular financial year. Additionally,

here it is being analyzed that budgets are being prepared and according to that organisations are

doing their work (Isakov and Pekarski, 2016). Moreover, the rate of success and failure of the

organisations or the firms depends on the estimated budgets that are being prepared. In this part

it reflects all the income and the expenses of the organisation.

Cash Flow budget

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Moreover, this budget also sheds light on the income or the monetary gained that are being

earned by the organisations. Additionally, organisations can make different analysis on the

different facts that from where monetary income will be earned in the organisations. Moreover,

this budget also projects that from which organisations are having a probable chances to gain

money.

Flexible budget

Flexible budget is also called variable budget and it is a financial plan of budgeted income and

expenses. It is prepared based on the current actual output (Tarasi et al. 2013). In simpler terms,

flexible budget is prepared to know how the revenues and expenses changes with the change in

output and due to this, flexible budget are also known as variable budget.

b) Discussing the process of preparing various budgets

The process of preparing budget begins with the submission of budget forms that need to be

completed by cost centre to the finance office. After the submission budget form or first draft,

budget hearing is then held to justify the request of the cost centre. Finally after the Senate’s

consideration, the final budget is prepared for the Board of Trustees and then the approval of

preparing budgets is given. The steps of preparing various budgets are given below.

● Updating budget assumption

● Reviewing bottlenecks

● Determining amount of funding

● Creating budget package

● Issuing budget package

● Obtaining revenue forecast

● Obtaining budgets prepared by various departments

● Obtaining capital budget request

● Updating budget model including all the relevant budget information into the master

budget

● Reviewing the budget with the senior management team

● Issuing and lodging the budget

c) Discussing the pricing strategies

Skimming pricing

11

earned by the organisations. Additionally, organisations can make different analysis on the

different facts that from where monetary income will be earned in the organisations. Moreover,

this budget also projects that from which organisations are having a probable chances to gain

money.

Flexible budget

Flexible budget is also called variable budget and it is a financial plan of budgeted income and

expenses. It is prepared based on the current actual output (Tarasi et al. 2013). In simpler terms,

flexible budget is prepared to know how the revenues and expenses changes with the change in

output and due to this, flexible budget are also known as variable budget.

b) Discussing the process of preparing various budgets

The process of preparing budget begins with the submission of budget forms that need to be

completed by cost centre to the finance office. After the submission budget form or first draft,

budget hearing is then held to justify the request of the cost centre. Finally after the Senate’s

consideration, the final budget is prepared for the Board of Trustees and then the approval of

preparing budgets is given. The steps of preparing various budgets are given below.

● Updating budget assumption

● Reviewing bottlenecks

● Determining amount of funding

● Creating budget package

● Issuing budget package

● Obtaining revenue forecast

● Obtaining budgets prepared by various departments

● Obtaining capital budget request

● Updating budget model including all the relevant budget information into the master

budget

● Reviewing the budget with the senior management team

● Issuing and lodging the budget

c) Discussing the pricing strategies

Skimming pricing

11

This is the pricing strategies that are being applied by the organisations. Additionally, in this

strategy prices are being fixed high for the products that are being sold in the market.

Additionally, producers are fixing these prices and high prices reflect high level of revenue for

the organisation.

Penetration pricing

Similarly, there are different organisations that are charging low prices for the products and

when low prices are being charged by the organisations then customers are having a perception

in their mind that when organisations have lowered the price then they will increase the sales of

the entire products (Spann et al. 2014). Additionally, Imda Tech limited is following this strategy

to retain the customers for a long period of time.

Psychological pricing

Here organisations are fixing the prices in such a manner so that customers have perceptions in

the mind that they are paying low prices for the products (Sun et al. 2016). It can be understood

with the help of the following example. If an organisation is selling particular products and they

are charging $99 for the products instead of charging $100 for the products. Moreover, this is

creating positive impacts in the minds of the customers regarding the organisation.

Task 4

a) Explaining the approach of balance score card and describing how it can be

used to measure range of performance

1) Explaining how balanced scorecard can be used to identify and respond to financial

problems

In strategic management, a balanced scorecard is used as the performance metric, where various

internal business functions along with their outcomes are identified and improved. The balanced

scorecard is used by the managements of the organization to strengthen the good behavioral

system in the organization by diversifying the four different areas that are required to be

analyzed. In the context of financial problems that need to be resolved, balance scorecard

exclusively helps in identifying and responding to the financial problems (Hoque, 2014). The

fourth leg of the balanced scorecard deals with measuring financial information, like sales,

incomes, and expenses to understand the financial performance of the business. Certain financial

ratios, income targets and budget variances and budget variances are critically measured and

12

strategy prices are being fixed high for the products that are being sold in the market.

Additionally, producers are fixing these prices and high prices reflect high level of revenue for

the organisation.

Penetration pricing

Similarly, there are different organisations that are charging low prices for the products and

when low prices are being charged by the organisations then customers are having a perception

in their mind that when organisations have lowered the price then they will increase the sales of

the entire products (Spann et al. 2014). Additionally, Imda Tech limited is following this strategy

to retain the customers for a long period of time.

Psychological pricing

Here organisations are fixing the prices in such a manner so that customers have perceptions in

the mind that they are paying low prices for the products (Sun et al. 2016). It can be understood

with the help of the following example. If an organisation is selling particular products and they

are charging $99 for the products instead of charging $100 for the products. Moreover, this is

creating positive impacts in the minds of the customers regarding the organisation.

Task 4

a) Explaining the approach of balance score card and describing how it can be

used to measure range of performance

1) Explaining how balanced scorecard can be used to identify and respond to financial

problems

In strategic management, a balanced scorecard is used as the performance metric, where various

internal business functions along with their outcomes are identified and improved. The balanced

scorecard is used by the managements of the organization to strengthen the good behavioral

system in the organization by diversifying the four different areas that are required to be

analyzed. In the context of financial problems that need to be resolved, balance scorecard

exclusively helps in identifying and responding to the financial problems (Hoque, 2014). The

fourth leg of the balanced scorecard deals with measuring financial information, like sales,

incomes, and expenses to understand the financial performance of the business. Certain financial

ratios, income targets and budget variances and budget variances are critically measured and

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.