SPSS Coursework: Analysis of EUR/USD Exchange Rate Data and Models

VerifiedAdded on 2020/06/06

|11

|1089

|54

Homework Assignment

AI Summary

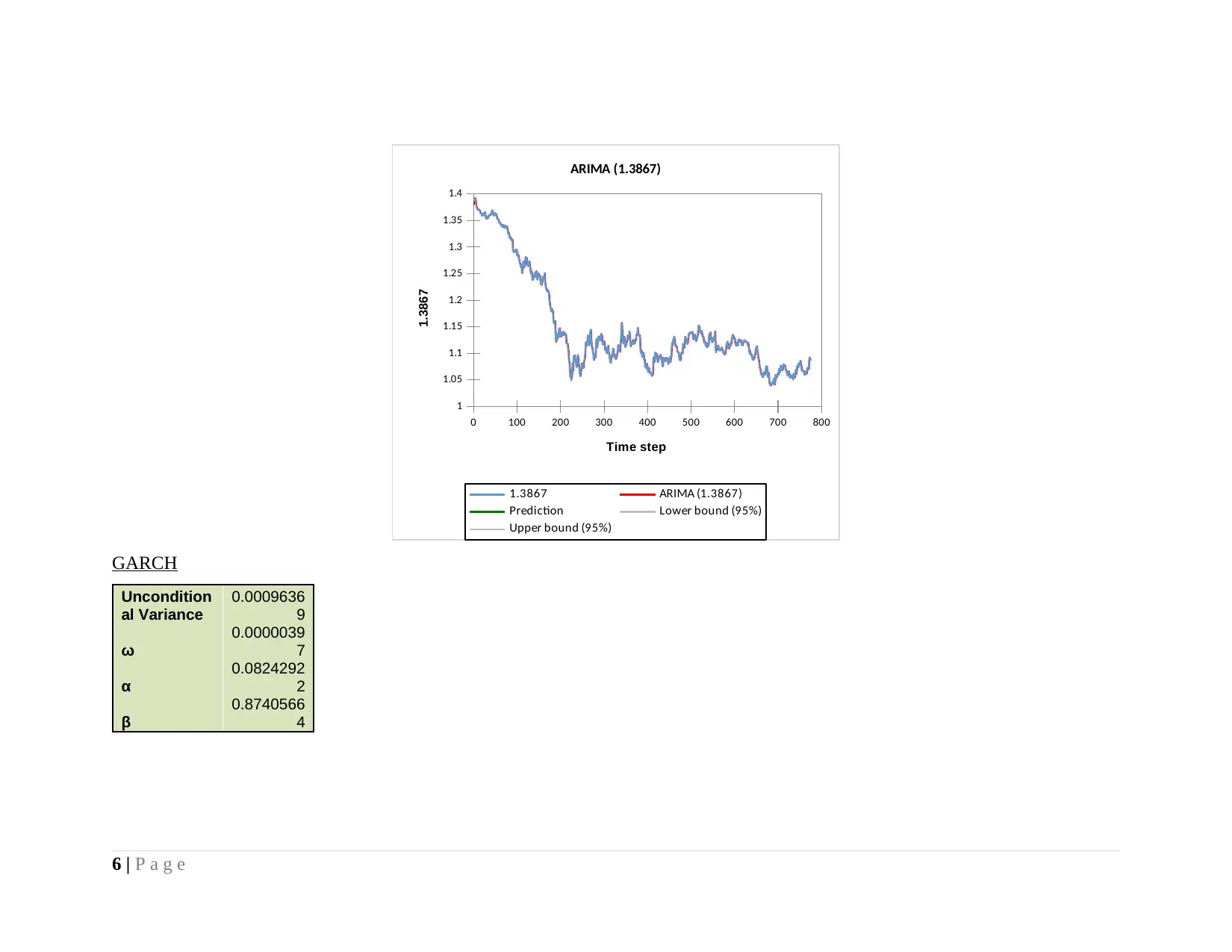

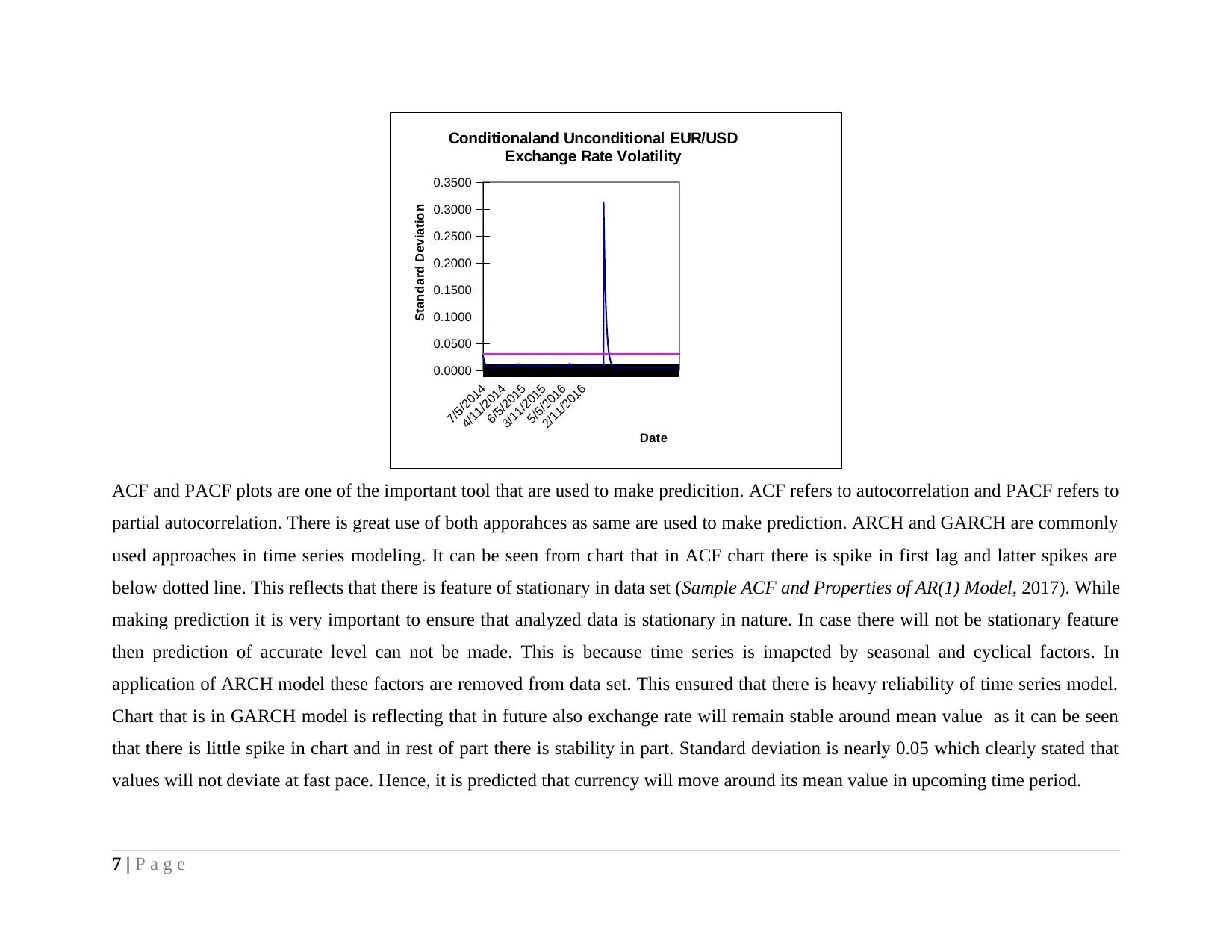

This document presents an analysis of EUR/USD exchange rates using SPSS, focusing on descriptive statistics and time series modeling techniques. The analysis begins with an introduction to time series methods and their importance in prediction, particularly within the context of currency exchange rates. Descriptive statistics, including measures of central tendency, dispersion, and skewness, are computed to provide an initial understanding of the data's characteristics. The analysis then proceeds to apply ARCH and GARCH models to forecast currency exchange rate movements. ARIMA modeling is also employed, with detailed results presented, including goodness-of-fit statistics, parameter values, and residual analysis. The document includes ACF and PACF plots and discusses their role in time series prediction. The conclusion emphasizes the significance of time series methods for business firms and the benefits of using time series modeling for analysts, offering valuable insights into financial forecasting. The document is a student's assignment, available on Desklib, a platform offering AI-based study tools.

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.