Design and Security Challenges in Open Banking Applications Deployed in Mobile Devices

VerifiedAdded on 2022/09/07

|43

|12544

|24

AI Summary

.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Design and Security Challenges in Open Banking Applications Deployed in Mobile devices

Name

Institution

Professor

Course

Date

Name

Institution

Professor

Course

Date

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Abstract

Open banking has been adopted by financial institutions to increase the efficiency of the banking

processes. To facilitate open banking, financial institutions provide their APIs which other third

parties use to access and share customer data. Customer grants mobile applications data access

privileges and users can access a unified bank account information at once. Open banking

application has made it easier for customers to manage their funds from different banking

institutions effectively. Despite operational efficiency, open banking mobile application poses

security challenges to financial institutions. Through the sharing of data, confidentiality and

integrity of data may be lost. The security challenges of financial institutions are posed by

mobile applications and operating system vulnerabilities. Security challenges that open mobile

banking applications face are hacking, malware infection, identity theft and loss of data. Open

banking security challenges are mainly caused by poor interfaces, the use of weak encryption

algorithms, and poor implementation of the strong encryption algorithm. System design is an

essential aspect of open banking because developers are required to define system requirements

such as input, output, processing, and data storage. The security of the open banking mobile

application increases if system design and requirements are fully implemented. From the study, it

was observable that PSD2 which was adopted by EU countries to facilitate data sharing needs

some changes. By addressing security issues that are faced by open banking and mobile

applications, it is believed that the security of the data in financial institutions become reliable.

Open banking has been adopted by financial institutions to increase the efficiency of the banking

processes. To facilitate open banking, financial institutions provide their APIs which other third

parties use to access and share customer data. Customer grants mobile applications data access

privileges and users can access a unified bank account information at once. Open banking

application has made it easier for customers to manage their funds from different banking

institutions effectively. Despite operational efficiency, open banking mobile application poses

security challenges to financial institutions. Through the sharing of data, confidentiality and

integrity of data may be lost. The security challenges of financial institutions are posed by

mobile applications and operating system vulnerabilities. Security challenges that open mobile

banking applications face are hacking, malware infection, identity theft and loss of data. Open

banking security challenges are mainly caused by poor interfaces, the use of weak encryption

algorithms, and poor implementation of the strong encryption algorithm. System design is an

essential aspect of open banking because developers are required to define system requirements

such as input, output, processing, and data storage. The security of the open banking mobile

application increases if system design and requirements are fully implemented. From the study, it

was observable that PSD2 which was adopted by EU countries to facilitate data sharing needs

some changes. By addressing security issues that are faced by open banking and mobile

applications, it is believed that the security of the data in financial institutions become reliable.

Contents

Abstract......................................................................................................................................................2

1. Introduction.......................................................................................................................................4

1.1. Motivation..................................................................................................................................5

1.2. Overview of the dissertation chapters......................................................................................5

2. Study Background.............................................................................................................................7

2.1. Problem domain.........................................................................................................................7

3. Literature review...............................................................................................................................9

3.1. What is open banking?............................................................................................................10

3.2. Open Banking Architecture and Mobile Banking at a Glance.............................................10

3.3. Security Challenges in Mobile Application Banking.............................................................12

3.4. IOS security challenges...........................................................................................................12

3.5. Android Security Challenges..................................................................................................15

3.6. Mobile Application Banking Security Challenges.................................................................16

4. Experimental /System Design.........................................................................................................19

4.1. Fundamentals of Open banking application design..............................................................21

4.2. Open Banking Architecture and Design................................................................................22

4.3. Open Banking API’s................................................................................................................25

5. Evaluation........................................................................................................................................28

5.1. Threat Analysis........................................................................................................................28

5.2. Assets........................................................................................................................................28

5.3. Threat agents............................................................................................................................29

5.4. Security threats........................................................................................................................30

5.5. Vulnerabilities..........................................................................................................................31

6. Discussions of findings.....................................................................................................................34

7. Conclusion........................................................................................................................................37

8. Bibliography.....................................................................................................................................38

Abstract......................................................................................................................................................2

1. Introduction.......................................................................................................................................4

1.1. Motivation..................................................................................................................................5

1.2. Overview of the dissertation chapters......................................................................................5

2. Study Background.............................................................................................................................7

2.1. Problem domain.........................................................................................................................7

3. Literature review...............................................................................................................................9

3.1. What is open banking?............................................................................................................10

3.2. Open Banking Architecture and Mobile Banking at a Glance.............................................10

3.3. Security Challenges in Mobile Application Banking.............................................................12

3.4. IOS security challenges...........................................................................................................12

3.5. Android Security Challenges..................................................................................................15

3.6. Mobile Application Banking Security Challenges.................................................................16

4. Experimental /System Design.........................................................................................................19

4.1. Fundamentals of Open banking application design..............................................................21

4.2. Open Banking Architecture and Design................................................................................22

4.3. Open Banking API’s................................................................................................................25

5. Evaluation........................................................................................................................................28

5.1. Threat Analysis........................................................................................................................28

5.2. Assets........................................................................................................................................28

5.3. Threat agents............................................................................................................................29

5.4. Security threats........................................................................................................................30

5.5. Vulnerabilities..........................................................................................................................31

6. Discussions of findings.....................................................................................................................34

7. Conclusion........................................................................................................................................37

8. Bibliography.....................................................................................................................................38

1. Introduction

Open banking is the process of allowing providers to have direct access to financial

information. With open banking, it is possible to have new products or services that are

consumed by users to offer greater value. Customers' are also able to have a better understanding

of their accounts, which makes it possible to benefit more from their money. The power of

fintech, open banking can change how both technologies and consumers interact with each other.

Developers have been using application programming interfaces (APIs) to create a connection to

any payment network and make a display of all billing details. With the adoption of open

banking in the financial sector, cybersecurity remains a fundamental aspect that all stakeholders

should consider. Its deployment in mobile devices creates an environment that poses security

risks to financial institutions. Formulation of strict rules and regulations play a key role in

establishing a strong foundation under which opening banking operates. The implementation of

PSD2 with open banking has affected the global market and regulators are keenly watching its

adoption in the European Union (EU) (Elkhodr, Shahrestani, & Kourouche 2012, pp. 260). To

build and run secure open banking applications, protection measures such as data encryption,

authentication and creating standard operational guidelines make stakeholders stronger. Unless

all stakeholders in the industry come together to create resilient cybersecurity policies,

developing and maintaining secure open banking APIs remain impossible. Customers of the

financial institution should be able to monitor and control their financial spending from mobile

phones. To offer robust services, open banking should be able to offer a strong legislative

framework that helps financial organizations share data securely.

Open banking is the process of allowing providers to have direct access to financial

information. With open banking, it is possible to have new products or services that are

consumed by users to offer greater value. Customers' are also able to have a better understanding

of their accounts, which makes it possible to benefit more from their money. The power of

fintech, open banking can change how both technologies and consumers interact with each other.

Developers have been using application programming interfaces (APIs) to create a connection to

any payment network and make a display of all billing details. With the adoption of open

banking in the financial sector, cybersecurity remains a fundamental aspect that all stakeholders

should consider. Its deployment in mobile devices creates an environment that poses security

risks to financial institutions. Formulation of strict rules and regulations play a key role in

establishing a strong foundation under which opening banking operates. The implementation of

PSD2 with open banking has affected the global market and regulators are keenly watching its

adoption in the European Union (EU) (Elkhodr, Shahrestani, & Kourouche 2012, pp. 260). To

build and run secure open banking applications, protection measures such as data encryption,

authentication and creating standard operational guidelines make stakeholders stronger. Unless

all stakeholders in the industry come together to create resilient cybersecurity policies,

developing and maintaining secure open banking APIs remain impossible. Customers of the

financial institution should be able to monitor and control their financial spending from mobile

phones. To offer robust services, open banking should be able to offer a strong legislative

framework that helps financial organizations share data securely.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1.1. Motivation

In this case, the rationale behind the study has been motivated by the need to understand

open banking security design and challenges deployed in mobile devices. Consumers embrace

the technology without understanding the security challenges associated with it. To understand

open banking security challenges, the study evaluate all stakeholder interactions and required

security standards that all APIs should meet. In this study, several contributions have been

integrated as part of the rationale behind the study.

1. What security challenges does mobile banking application pose on financial institutions?

2. Is open banking applications safe?

3. Was security all concern considered during the design of the PSD2 on data access and

sharing between entities?

4. What security challenges are faced by open banking applications through device

operating systems (OS) such as IOS and Android?

1.2. Overview of the dissertation chapters

The goal of the study is to evaluate open banking on mobile applications to foster a

robust and manageable security framework. The thesis covers different subsections that helped

the researcher to consolidate important pieces of valuable information. The introduction of the

paper starts with a definition of open banking and fundamental aspects that facilitates data

sharing. The architectural overview of open banking (PSD2) presented showcase interactions

between different application programming interfaces (APIs). It highlights different APIs and

technologies which support open banking. The next section presents a rationale and background

of the study. The background of the study is an important section of the thesis because it forms

the basis of the study. It is at this point where the problem of the study is explained in detail.

Technology has posed so many challenges in the banking industry and through the use of open

In this case, the rationale behind the study has been motivated by the need to understand

open banking security design and challenges deployed in mobile devices. Consumers embrace

the technology without understanding the security challenges associated with it. To understand

open banking security challenges, the study evaluate all stakeholder interactions and required

security standards that all APIs should meet. In this study, several contributions have been

integrated as part of the rationale behind the study.

1. What security challenges does mobile banking application pose on financial institutions?

2. Is open banking applications safe?

3. Was security all concern considered during the design of the PSD2 on data access and

sharing between entities?

4. What security challenges are faced by open banking applications through device

operating systems (OS) such as IOS and Android?

1.2. Overview of the dissertation chapters

The goal of the study is to evaluate open banking on mobile applications to foster a

robust and manageable security framework. The thesis covers different subsections that helped

the researcher to consolidate important pieces of valuable information. The introduction of the

paper starts with a definition of open banking and fundamental aspects that facilitates data

sharing. The architectural overview of open banking (PSD2) presented showcase interactions

between different application programming interfaces (APIs). It highlights different APIs and

technologies which support open banking. The next section presents a rationale and background

of the study. The background of the study is an important section of the thesis because it forms

the basis of the study. It is at this point where the problem of the study is explained in detail.

Technology has posed so many challenges in the banking industry and through the use of open

banking practices, security should be addressed effectively. The security concerns should focus

on android security challenges, open banking APIs, security challenges that face IOS, mobile

application banking security challenges and the use of open banking architecture and design. The

fourth section of the thesis evaluate the entire open banking case study and its application in the

financial sector. It presents a consolidated overview of open banking, its application in the

industry, benefits, and success in the market. Threat analysis section evaluate different types of

threats and threat agents, open banking architecture security threats and vulnerabilities that

should be sealed. Security requirements is a major area considering various APIs that connect to

access customers’ financial data. There should be standard security requirements that every API

should meet to start operating in open banking platforms. The next section focuses on a detailed

open banking mobile security analysis. Several aspects such as mobile security threshold and

individual customer precautions are evaluated intensively. Security controls are also analyzed to

provide recommendations to customers and third-party data users on appropriate security

measures.

on android security challenges, open banking APIs, security challenges that face IOS, mobile

application banking security challenges and the use of open banking architecture and design. The

fourth section of the thesis evaluate the entire open banking case study and its application in the

financial sector. It presents a consolidated overview of open banking, its application in the

industry, benefits, and success in the market. Threat analysis section evaluate different types of

threats and threat agents, open banking architecture security threats and vulnerabilities that

should be sealed. Security requirements is a major area considering various APIs that connect to

access customers’ financial data. There should be standard security requirements that every API

should meet to start operating in open banking platforms. The next section focuses on a detailed

open banking mobile security analysis. Several aspects such as mobile security threshold and

individual customer precautions are evaluated intensively. Security controls are also analyzed to

provide recommendations to customers and third-party data users on appropriate security

measures.

2. Study Background

The focus of the study on the security challenges in open banking applications deployed

on mobile has been of great concern in the financial sector. Notably, technology has been greatly

adopted in the banking industry to efficient access to information to customers’. In the banking

industry, data and access to the data remain a key factor because it is used to make financial

decisions. Both customers and banking institutions need to access financial data which is held by

different banking institutions (Elkhodr, Shahrestani, & Kourouche 2012, pp. 260). For banks and

other financial institutions, it has beeen difficult to determine customer creditworthiness in cases

where an individual has more than one account in different banks. On the same note, customers

with money in different accounts from more than one bank have some challenges to have a

consolidated financial overview of all the accounts. With open banking, both customers and

financial institutions are able to eliminate these challenges by having a unified view of financial

status from all individual customers' accounts. The adoption of open banking in the industry is

expected to change both business policies and operating strategies. As organizations embrace

open banking. It is important to evaluate security concerns that should be addressed.

2.1. Problem domain

Mobile application security in financial institutions remains a fundamental aspect that

requires a concerted effort from all stakeholders. To resolve mobile application challenges in the

banking industry, application users' challenges, organizational processes, and software

development security flaws should be addressed. Precisely, financial institutions make use of

different mobile banking applications that have different security vulnerabilities. To address

security flaws associated with different mobile banking applications, financial institutions should

The focus of the study on the security challenges in open banking applications deployed

on mobile has been of great concern in the financial sector. Notably, technology has been greatly

adopted in the banking industry to efficient access to information to customers’. In the banking

industry, data and access to the data remain a key factor because it is used to make financial

decisions. Both customers and banking institutions need to access financial data which is held by

different banking institutions (Elkhodr, Shahrestani, & Kourouche 2012, pp. 260). For banks and

other financial institutions, it has beeen difficult to determine customer creditworthiness in cases

where an individual has more than one account in different banks. On the same note, customers

with money in different accounts from more than one bank have some challenges to have a

consolidated financial overview of all the accounts. With open banking, both customers and

financial institutions are able to eliminate these challenges by having a unified view of financial

status from all individual customers' accounts. The adoption of open banking in the industry is

expected to change both business policies and operating strategies. As organizations embrace

open banking. It is important to evaluate security concerns that should be addressed.

2.1. Problem domain

Mobile application security in financial institutions remains a fundamental aspect that

requires a concerted effort from all stakeholders. To resolve mobile application challenges in the

banking industry, application users' challenges, organizational processes, and software

development security flaws should be addressed. Precisely, financial institutions make use of

different mobile banking applications that have different security vulnerabilities. To address

security flaws associated with different mobile banking applications, financial institutions should

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

outline some security measures that each mobile application should meet for a secure connection

to core banking solutions. On the same note, application developers should make sure mobile

applications meet the minimum security threshold before attempting any connection to banking

solutions.

to core banking solutions. On the same note, application developers should make sure mobile

applications meet the minimum security threshold before attempting any connection to banking

solutions.

3. Literature review

A review of previous studies in mobile banking application security involves the

evaluation of other scholarly articles. The study focuses mainly on security and mobile banking

applications in the banking industry (Elkhodr, Shahrestani, & Kourouche 2012, pp. 260). The use

of mobile banking applications has been on the rise and according to studies, mobile application

usage as surpassed desktop-based applications. Every business requires to reach out to its

customers conveniently and at all times. With the desktop application being unpotable, the

mobile application has dominated the market because it can be accessed conveniently. In the

case of financial institutions that want to offer their services effectively and competitively,

customer satisfaction is the key. To satisfy customers’ in the banking industry, access and use of

their funds from mobile applications should be availed. The review help banking industry

stakeholders to internalize the meaning of mobile banking application, and the meaning and use

of open banking. It also focus on the security challenges in open mobile banking applications,

analyze and design open mobile baking application architecture (He, Tian, & Shen 2015, pp.

104). The security of mobile applications from the mobile operating system (OS) such as the

android and IOS perspective has been done. The review is done from the scholarly articles that

are less than 10 years old since publication. The study evaluates security challenges that are

faced in the banking industry and measures required to control the menace. It brings together

different stakeholders and highlights their respective responsibilities. Finally, threats, threat

agents, and threat control procedures wraps up the study. The study fits the research gap because

it addresses open mobile banking security challenges, which form part of current industrial

problem that need urgent intervention.

A review of previous studies in mobile banking application security involves the

evaluation of other scholarly articles. The study focuses mainly on security and mobile banking

applications in the banking industry (Elkhodr, Shahrestani, & Kourouche 2012, pp. 260). The use

of mobile banking applications has been on the rise and according to studies, mobile application

usage as surpassed desktop-based applications. Every business requires to reach out to its

customers conveniently and at all times. With the desktop application being unpotable, the

mobile application has dominated the market because it can be accessed conveniently. In the

case of financial institutions that want to offer their services effectively and competitively,

customer satisfaction is the key. To satisfy customers’ in the banking industry, access and use of

their funds from mobile applications should be availed. The review help banking industry

stakeholders to internalize the meaning of mobile banking application, and the meaning and use

of open banking. It also focus on the security challenges in open mobile banking applications,

analyze and design open mobile baking application architecture (He, Tian, & Shen 2015, pp.

104). The security of mobile applications from the mobile operating system (OS) such as the

android and IOS perspective has been done. The review is done from the scholarly articles that

are less than 10 years old since publication. The study evaluates security challenges that are

faced in the banking industry and measures required to control the menace. It brings together

different stakeholders and highlights their respective responsibilities. Finally, threats, threat

agents, and threat control procedures wraps up the study. The study fits the research gap because

it addresses open mobile banking security challenges, which form part of current industrial

problem that need urgent intervention.

3.1. What is open banking?

Open banking (PSD2) is a new and secure way through which consumers share

information to allow both new and other existing companies to provide efficient payment

methods and innovative products in the industry (Bharti 2016, pp. 13). It is also known to be

“open bank data”, and a practice used by banking institutions to provide data access to third

parties. The data exposed to third parties include transaction data, consumer banking, and

financial which is exposed through APIs. In an open banking environment, all stakeholders can

access and share data for use by other service providers, consumers, and financial institutions. To

facilitate open banking, banks are required to get customer consent to allow the sharing of

financial data. Customer consent can be in the form of a checkbox with appropriate terms of the

agreement in a mobile online banking application. In open banking, electronic sharing of

financial data should be secure and governed by terms of service approved by the consumer. In

current banking scenarios, it is not possible to manage two different accounts at the same time

from different banks due to the incompatibility of the systems (Hadad 2019, pp. 343). With the

introduction and use of open banking, consumers are able to access and manage their money

from all accounts at once. It is expected to centralize all customer's banking data for ease of

money management, lending, and payment processes. Therefore, Open banking has been

categorized as an innovation expected to change the nature and operations of the banking

industry.

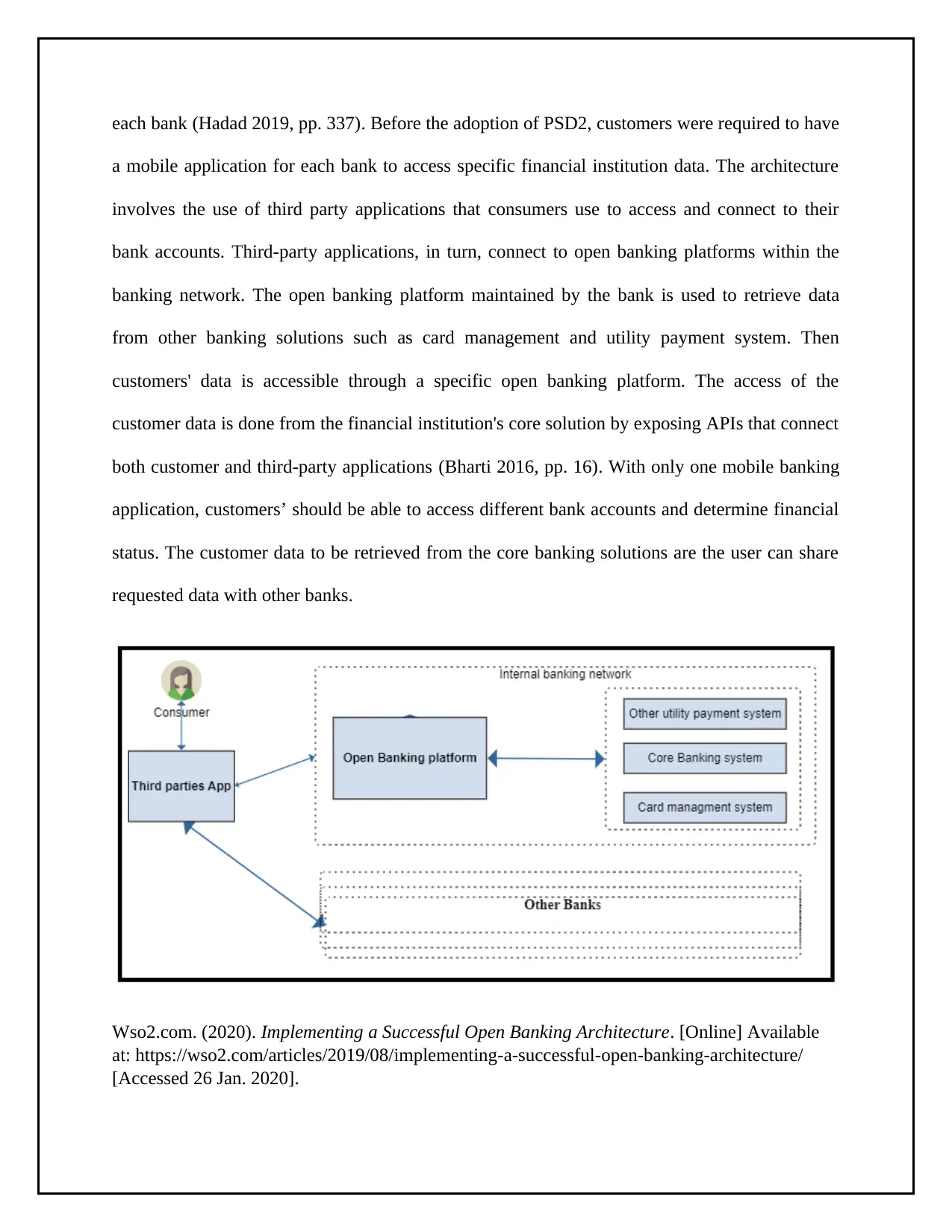

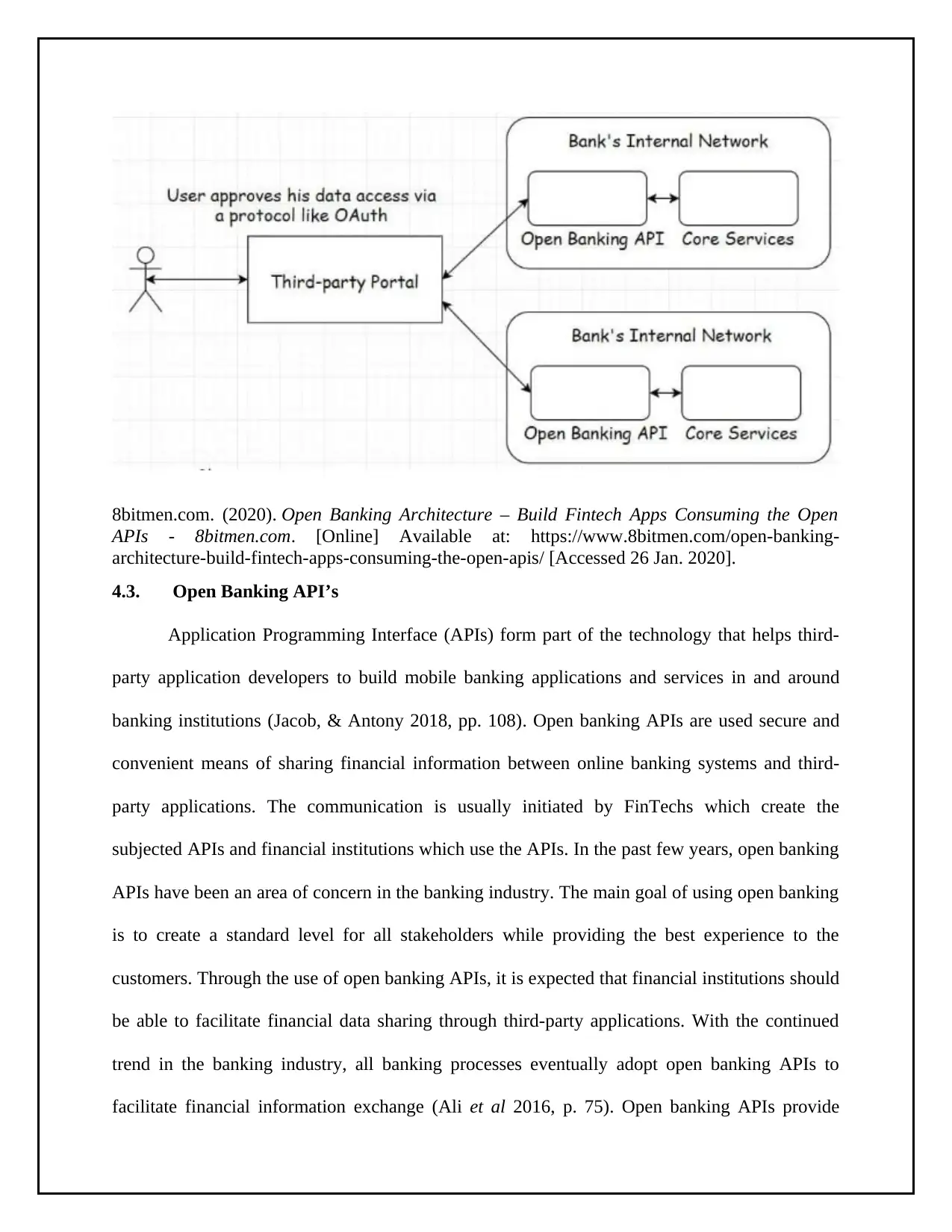

3.2. Open Banking Architecture and Mobile Banking at a Glance

Open banking architecture involves the integration of different entities and stakeholders

into a single business process. With the innovation and acceptance of PSD2 by European Union

(EU) countries, the architecture was compressed to eliminate mobile banking applications for

Open banking (PSD2) is a new and secure way through which consumers share

information to allow both new and other existing companies to provide efficient payment

methods and innovative products in the industry (Bharti 2016, pp. 13). It is also known to be

“open bank data”, and a practice used by banking institutions to provide data access to third

parties. The data exposed to third parties include transaction data, consumer banking, and

financial which is exposed through APIs. In an open banking environment, all stakeholders can

access and share data for use by other service providers, consumers, and financial institutions. To

facilitate open banking, banks are required to get customer consent to allow the sharing of

financial data. Customer consent can be in the form of a checkbox with appropriate terms of the

agreement in a mobile online banking application. In open banking, electronic sharing of

financial data should be secure and governed by terms of service approved by the consumer. In

current banking scenarios, it is not possible to manage two different accounts at the same time

from different banks due to the incompatibility of the systems (Hadad 2019, pp. 343). With the

introduction and use of open banking, consumers are able to access and manage their money

from all accounts at once. It is expected to centralize all customer's banking data for ease of

money management, lending, and payment processes. Therefore, Open banking has been

categorized as an innovation expected to change the nature and operations of the banking

industry.

3.2. Open Banking Architecture and Mobile Banking at a Glance

Open banking architecture involves the integration of different entities and stakeholders

into a single business process. With the innovation and acceptance of PSD2 by European Union

(EU) countries, the architecture was compressed to eliminate mobile banking applications for

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

each bank (Hadad 2019, pp. 337). Before the adoption of PSD2, customers were required to have

a mobile application for each bank to access specific financial institution data. The architecture

involves the use of third party applications that consumers use to access and connect to their

bank accounts. Third-party applications, in turn, connect to open banking platforms within the

banking network. The open banking platform maintained by the bank is used to retrieve data

from other banking solutions such as card management and utility payment system. Then

customers' data is accessible through a specific open banking platform. The access of the

customer data is done from the financial institution's core solution by exposing APIs that connect

both customer and third-party applications (Bharti 2016, pp. 16). With only one mobile banking

application, customers’ should be able to access different bank accounts and determine financial

status. The customer data to be retrieved from the core banking solutions are the user can share

requested data with other banks.

Wso2.com. (2020). Implementing a Successful Open Banking Architecture. [Online] Available

at: https://wso2.com/articles/2019/08/implementing-a-successful-open-banking-architecture/

[Accessed 26 Jan. 2020].

a mobile application for each bank to access specific financial institution data. The architecture

involves the use of third party applications that consumers use to access and connect to their

bank accounts. Third-party applications, in turn, connect to open banking platforms within the

banking network. The open banking platform maintained by the bank is used to retrieve data

from other banking solutions such as card management and utility payment system. Then

customers' data is accessible through a specific open banking platform. The access of the

customer data is done from the financial institution's core solution by exposing APIs that connect

both customer and third-party applications (Bharti 2016, pp. 16). With only one mobile banking

application, customers’ should be able to access different bank accounts and determine financial

status. The customer data to be retrieved from the core banking solutions are the user can share

requested data with other banks.

Wso2.com. (2020). Implementing a Successful Open Banking Architecture. [Online] Available

at: https://wso2.com/articles/2019/08/implementing-a-successful-open-banking-architecture/

[Accessed 26 Jan. 2020].

3.3. Security Challenges in Mobile Application Banking

Mobile banking is regarded as one of the most important innovations in the banking

sector. Despite its advantages, it has been linked to the number of risks. Mobile application

developers need to uphold the highest standards of security (Sharma 2016, pp. 304). Data

security in mobile banking remains complex due to; organizational employee behavior.

Application users' in the banking industry form a key component of security challenges that

financial institutions should address. The behavior of the users should be controlled by creating

specific privileges for application users within banking institutions. Next, specific organizational

business procedures have been identified as a security problem that organizations should

implement to minimize security challenges that are associated with a mobile application in the

banking sector. On the same note, flaws related to software are quite common and financial

institutions should be held mobile application developers accountable for security flaws that

associated wit code bugs. All stakeholders in the banking sector should understand that a single

security flaw cannot be corrected by other security measures (Solanki 2012, pp. 2277). In this

case, it is important to evaluate and test all security flaws in mobile application banking

frequently.

3.4. IOS security challenges

Applications are believed to have some security flaws despite the effort that system

developers implement as security measures. Apple Inc. has implemented strong security

measures but different types of security issues have been faced by IOS users. Some of the IOS

security issues that the banking industry should address are mainly categorized as Open Web

Application Security Project (OWASP). The first IOS security challenge that should be

addressed is the improper use of mobile banking applications by different stakeholders (He,

Mobile banking is regarded as one of the most important innovations in the banking

sector. Despite its advantages, it has been linked to the number of risks. Mobile application

developers need to uphold the highest standards of security (Sharma 2016, pp. 304). Data

security in mobile banking remains complex due to; organizational employee behavior.

Application users' in the banking industry form a key component of security challenges that

financial institutions should address. The behavior of the users should be controlled by creating

specific privileges for application users within banking institutions. Next, specific organizational

business procedures have been identified as a security problem that organizations should

implement to minimize security challenges that are associated with a mobile application in the

banking sector. On the same note, flaws related to software are quite common and financial

institutions should be held mobile application developers accountable for security flaws that

associated wit code bugs. All stakeholders in the banking sector should understand that a single

security flaw cannot be corrected by other security measures (Solanki 2012, pp. 2277). In this

case, it is important to evaluate and test all security flaws in mobile application banking

frequently.

3.4. IOS security challenges

Applications are believed to have some security flaws despite the effort that system

developers implement as security measures. Apple Inc. has implemented strong security

measures but different types of security issues have been faced by IOS users. Some of the IOS

security issues that the banking industry should address are mainly categorized as Open Web

Application Security Project (OWASP). The first IOS security challenge that should be

addressed is the improper use of mobile banking applications by different stakeholders (He,

Tian, & Shen 2015, pp. 104). IOS provides users with unique security parameters such as

permission systems and failure by users to make use of them is considered a security flaw. As a

development platform, IOS offers specific guidelines to be followed by developers if secure

mobile applications are to be accorded a top priority. Failing to uphold proper implementation

features by application developers can result in sensitive data being corrupted. The next IOS

security challenge that mobile application developers should be concerned about is the insecure

storage of data. Every mobile application in the banking industry stores and use data (Al-Sabri,

& Al-Saleem 2013, pp. 259). To store sensitive data required by financial institutions, data

storage solutions such as internal storage features should be very secure. In most cases, securing

internal data storage is recommended as a means of preventing data leak. Failure to protect

confidential data leads to data access by unauthorized users who can use the data for illegal

activities such as money laundering.

Additionally, insecure communication between data applications and other data sources

including servers and Bluetooth enabled devices is a security challenge in IOS devices. It is

inevitable for mobile applications to communicate and share data because they majorly work

through data sharing. Considering each mobile application has its security flaws, adequate data

protection measures while on the transmission is important to prevent potential data leaks

(Handa, & Singh 2015, pp. 786). With readily available tools to access external data while on

transmission, insecure data sharing results in data breaches such as identity theft. The next IOS

security challenge is insecure authentication when accessing the internal functionality of mobile

banking applications (Hanafizadeh et al 2014, pp. 62). Applications provide users with various

authentication measures such as PINs, specific user ids, strong passwords, and fingerprint

scanning. It is important to note that strong authentication measures allow mobile application

permission systems and failure by users to make use of them is considered a security flaw. As a

development platform, IOS offers specific guidelines to be followed by developers if secure

mobile applications are to be accorded a top priority. Failing to uphold proper implementation

features by application developers can result in sensitive data being corrupted. The next IOS

security challenge that mobile application developers should be concerned about is the insecure

storage of data. Every mobile application in the banking industry stores and use data (Al-Sabri,

& Al-Saleem 2013, pp. 259). To store sensitive data required by financial institutions, data

storage solutions such as internal storage features should be very secure. In most cases, securing

internal data storage is recommended as a means of preventing data leak. Failure to protect

confidential data leads to data access by unauthorized users who can use the data for illegal

activities such as money laundering.

Additionally, insecure communication between data applications and other data sources

including servers and Bluetooth enabled devices is a security challenge in IOS devices. It is

inevitable for mobile applications to communicate and share data because they majorly work

through data sharing. Considering each mobile application has its security flaws, adequate data

protection measures while on the transmission is important to prevent potential data leaks

(Handa, & Singh 2015, pp. 786). With readily available tools to access external data while on

transmission, insecure data sharing results in data breaches such as identity theft. The next IOS

security challenge is insecure authentication when accessing the internal functionality of mobile

banking applications (Hanafizadeh et al 2014, pp. 62). Applications provide users with various

authentication measures such as PINs, specific user ids, strong passwords, and fingerprint

scanning. It is important to note that strong authentication measures allow mobile application

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

users to secure manage all assets within the application. Mobile application developers and users

should make sure strong authentication and validation measures are implemented in applications.

Weak authentication security measures are easier to bypass and expose sensitive data to

unauthorized users (Goyal, Pandey, & Batra 2012, pp. 87). It is the responsibility of the

developers to enforce the use of strong authentication measures such as the use of strong

passwords and change of passwords expiry dates. On the other hand, mobile application users are

expected to adhere to secure authentication measures provided by mobile application developers.

Similarly, insufficient data cryptography has proved to be a great challenge in mobile

banking applications. Cryptography with a strong transformation algorithm is required to

transform mobile application raw data into secure data packages (Islam 2014, pp. 114).

Encryption is regarded as a secure means of protecting data because it is impossible to either

read the data. Encrypted data is useless as it requires high processing power and too much time

to break encrypted data. Despite encryption being a secure means of protecting data, weak

encryption algorithms expose sensitive data to attackers (Das, & Debbarma 2011, pp. 162). Code

quality is an important aspect that should be observed by mobile application developers. It is not

simple to measure code quality, but some coding quality parameters such as proper code layering

and consistency in coding style must be enforced. The use of poor coding techniques makes it

difficult to use and maintain an application for a long period. Change in a block of code when

adding new features may introduce the subjected application to vulnerabilities. In most cases,

attackers make use of complex code analysis tools to evaluate code vulnerabilities and extract

required data without knowledge of the application user (Xavier, & Pati 2012, pp. 219). Finally,

code tempering is believed to be a complex security challenge in mobile application banking.

Hackers with code development skills can change some blocks of code or replicate some binary

should make sure strong authentication and validation measures are implemented in applications.

Weak authentication security measures are easier to bypass and expose sensitive data to

unauthorized users (Goyal, Pandey, & Batra 2012, pp. 87). It is the responsibility of the

developers to enforce the use of strong authentication measures such as the use of strong

passwords and change of passwords expiry dates. On the other hand, mobile application users are

expected to adhere to secure authentication measures provided by mobile application developers.

Similarly, insufficient data cryptography has proved to be a great challenge in mobile

banking applications. Cryptography with a strong transformation algorithm is required to

transform mobile application raw data into secure data packages (Islam 2014, pp. 114).

Encryption is regarded as a secure means of protecting data because it is impossible to either

read the data. Encrypted data is useless as it requires high processing power and too much time

to break encrypted data. Despite encryption being a secure means of protecting data, weak

encryption algorithms expose sensitive data to attackers (Das, & Debbarma 2011, pp. 162). Code

quality is an important aspect that should be observed by mobile application developers. It is not

simple to measure code quality, but some coding quality parameters such as proper code layering

and consistency in coding style must be enforced. The use of poor coding techniques makes it

difficult to use and maintain an application for a long period. Change in a block of code when

adding new features may introduce the subjected application to vulnerabilities. In most cases,

attackers make use of complex code analysis tools to evaluate code vulnerabilities and extract

required data without knowledge of the application user (Xavier, & Pati 2012, pp. 219). Finally,

code tempering is believed to be a complex security challenge in mobile application banking.

Hackers with code development skills can change some blocks of code or replicate some binary

codes. Once the code is changed, attackers can execute code and affect application programming

interfaces (API) calls and affect application functionality by running some malicious codes

(Devadevan 2013, pp. 518). In most cases, attackers are known to distribute malicious codes

through phishing. By tampering with the code, attackers can intercept any form of

communication between IOS applications and steal data. It is also possible to gain authorized

access to either part of an entire mobile application such as internal data storage.

3.5. Android Security Challenges

Most of the devices such as smartphones and tablets are running on the Android

Operating System (OS). Cybercriminals have been targeting devices that run on Android because

their users use them to conduct online transactions from their bank accounts. With an increase in

online purchases from Android devices, security challenges should be of great concern to both

user and application developers (Handa, & Singh 2015, pp. 787). The first security concern with

Android devices is application-focused due to an increase in instant messaging and music mobile

applications. Considering one Android device can support several applications, attackers do not

focus on financial related applications. To gain access to mobile banking applications without

knowledge of the user, attackers gain access to the Android device through less suspicious

Applications. Once backdoor access is available, it is possible to extract logs related to mobile

banking applications and analyze them to get its related authentication sensitive data. It is a

common problem with application users to allow other mobile applications to access data within

the device. The vulnerable mobile application allows some data to be collected by malicious

actors and use it for social engineering attacks (Singh 2013, pp. 97). As a result, mobile

application users are convinced to provide sensitive data to untrusted entities. On the same note,

interfaces (API) calls and affect application functionality by running some malicious codes

(Devadevan 2013, pp. 518). In most cases, attackers are known to distribute malicious codes

through phishing. By tampering with the code, attackers can intercept any form of

communication between IOS applications and steal data. It is also possible to gain authorized

access to either part of an entire mobile application such as internal data storage.

3.5. Android Security Challenges

Most of the devices such as smartphones and tablets are running on the Android

Operating System (OS). Cybercriminals have been targeting devices that run on Android because

their users use them to conduct online transactions from their bank accounts. With an increase in

online purchases from Android devices, security challenges should be of great concern to both

user and application developers (Handa, & Singh 2015, pp. 787). The first security concern with

Android devices is application-focused due to an increase in instant messaging and music mobile

applications. Considering one Android device can support several applications, attackers do not

focus on financial related applications. To gain access to mobile banking applications without

knowledge of the user, attackers gain access to the Android device through less suspicious

Applications. Once backdoor access is available, it is possible to extract logs related to mobile

banking applications and analyze them to get its related authentication sensitive data. It is a

common problem with application users to allow other mobile applications to access data within

the device. The vulnerable mobile application allows some data to be collected by malicious

actors and use it for social engineering attacks (Singh 2013, pp. 97). As a result, mobile

application users are convinced to provide sensitive data to untrusted entities. On the same note,

mobile application users running on Android should be very careful with application installation

because viruses and worms can be hidden from some mobile applications.

The next Android security challenge is component-based threats that focus on both

hardware and software components with the android device. Some of the components that

attackers have been focusing on include Wi-Fi and Bluetooth which can be used to exploit

devices without user’s knowledge (Islam 2014, pp. 109). Both Wi-Fi and Bluetooth enabled

devices can provide an attacker with remote access to the specific mobile device and use it to

perform unauthorized activities. Attackers can also use such devices to install malware and

viruses on such devices. The installed malware can be used to extract sensitive data and monitor

specific transactions that can be used against the target user. Threats from cheap and old Android

versions of phones pose major security threats because most of the versions are not upgradable.

Old versions of technology both in hardware and software are vulnerable to security threats such

as malware and hackers (Bamoriya, & Singh P., 2011, pp. 116). New technologies are usually

incorporated into the newer versions of Android phones making it more secure. As developers

design and come up with new versions of Android, new security threats are considered and the

existing loopholes are sealed. Finally, Android instant application security has been a great

challenge in mobile banking applications. The effects of instant Applications on Android phones

are not clear and it can cause serious security challenges to financial institutions.

3.6. Mobile Application Banking Security Challenges

The banking industry remains a robust and sensitive sector in today's business and there

is a need to embrace mobile technology with caution. Despite mobile banking application is very

convenient, they are believed to pose serious security threats due to some vulnerabilities

associated channels. Some of the security challenges associated with mobile applications in the

because viruses and worms can be hidden from some mobile applications.

The next Android security challenge is component-based threats that focus on both

hardware and software components with the android device. Some of the components that

attackers have been focusing on include Wi-Fi and Bluetooth which can be used to exploit

devices without user’s knowledge (Islam 2014, pp. 109). Both Wi-Fi and Bluetooth enabled

devices can provide an attacker with remote access to the specific mobile device and use it to

perform unauthorized activities. Attackers can also use such devices to install malware and

viruses on such devices. The installed malware can be used to extract sensitive data and monitor

specific transactions that can be used against the target user. Threats from cheap and old Android

versions of phones pose major security threats because most of the versions are not upgradable.

Old versions of technology both in hardware and software are vulnerable to security threats such

as malware and hackers (Bamoriya, & Singh P., 2011, pp. 116). New technologies are usually

incorporated into the newer versions of Android phones making it more secure. As developers

design and come up with new versions of Android, new security threats are considered and the

existing loopholes are sealed. Finally, Android instant application security has been a great

challenge in mobile banking applications. The effects of instant Applications on Android phones

are not clear and it can cause serious security challenges to financial institutions.

3.6. Mobile Application Banking Security Challenges

The banking industry remains a robust and sensitive sector in today's business and there

is a need to embrace mobile technology with caution. Despite mobile banking application is very

convenient, they are believed to pose serious security threats due to some vulnerabilities

associated channels. Some of the security challenges associated with mobile applications in the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

banking industry are; poor mobile application design and configurations which make stored data

vulnerable to attacks (Driga, & Isac 2014, pp. 49-50). Banking mobile applications are regarded

as safe than banking practices on a mobile browser. However, with the ever-increasing number

of data breaches in financial institutions, security lapses have been directly linked to poor coding

practices and code quality. It is important for mobile developers and particularly in the banking

industry to understand each mobile platform has its unique requirements. By understanding

specific mobile security parameters, it is possible for developers to mitigate most of the security

challenges. It is of great concern that most of the mobile application developers lack skills and

knowledge on current security risks. This leaves the security of data at risk of being

compromised by hackers and other untrusted third parties. Next, the operating system (OS)

cryptographic vulnerabilities due to lack of adequate secure socket layer (SSL) implementation.

In mobile applications, application developers need to implement certificate validation in the

transport layer of the network (Bamoriya, & Singh P., 2011, pp. 118). Cryptographic in mobile

banking applications can be implemented by the application developers in every digital security

protocol to facilitate the establishment of encrypted communication links. Secure communication

links between applications and external data sources help to validate all communicating entities

to prevent threats such as man-in-middle and phishing attacks.

Moreover, there has been an explosive rise in malware attacks on mobile devices.

Malware attacks are usually propagated through software bugs and hackers are exploiting

vulnerabilities in mobile application banking for possibilities of launching attacks (Driga, & Isac

2014, pp. 49). Malicious programs are developed and executed on a target program to exploit the

possibilities of attacks. Both application developers and users should enforce security measures

due to the rise in malware and virus attacks. Flawed authentication is another security challenge

vulnerable to attacks (Driga, & Isac 2014, pp. 49-50). Banking mobile applications are regarded

as safe than banking practices on a mobile browser. However, with the ever-increasing number

of data breaches in financial institutions, security lapses have been directly linked to poor coding

practices and code quality. It is important for mobile developers and particularly in the banking

industry to understand each mobile platform has its unique requirements. By understanding

specific mobile security parameters, it is possible for developers to mitigate most of the security

challenges. It is of great concern that most of the mobile application developers lack skills and

knowledge on current security risks. This leaves the security of data at risk of being

compromised by hackers and other untrusted third parties. Next, the operating system (OS)

cryptographic vulnerabilities due to lack of adequate secure socket layer (SSL) implementation.

In mobile applications, application developers need to implement certificate validation in the

transport layer of the network (Bamoriya, & Singh P., 2011, pp. 118). Cryptographic in mobile

banking applications can be implemented by the application developers in every digital security

protocol to facilitate the establishment of encrypted communication links. Secure communication

links between applications and external data sources help to validate all communicating entities

to prevent threats such as man-in-middle and phishing attacks.

Moreover, there has been an explosive rise in malware attacks on mobile devices.

Malware attacks are usually propagated through software bugs and hackers are exploiting

vulnerabilities in mobile application banking for possibilities of launching attacks (Driga, & Isac

2014, pp. 49). Malicious programs are developed and executed on a target program to exploit the

possibilities of attacks. Both application developers and users should enforce security measures

due to the rise in malware and virus attacks. Flawed authentication is another security challenge

in mobile banking applications as fraudsters try to exploit exiting application weaknesses to

collect sensitive data. Financial institutions fail to provide mobile application users with secure

authentication measures results in security flaws. Banks have been relying on two-factor

authentication and one-time password (OTP) which has turned to be obsolete due to

technological innovation. Finally, the lack of sufficient oversight in a fast-growing technological

ecosystem by the government has created security flaws in the mobile application banking

industry. Federal Financial Institution Examination Council (FFIEC) has published some

guidelines that mobile banking applications should meet. However, the same council has failed

to address standard controls on mobile banking application regarding identification and

authentication controls (Bamoriya, & Singh P., 2011, pp. 118). The greatest challenge on

authentication and identification is that other bodies have tried to provide guidelines, but it has

not been substantive to solve financial institutions' mobile banking security challenges. Financial

institutions must establish a high level of trust on mobile channels if they have to remain

competitive.

collect sensitive data. Financial institutions fail to provide mobile application users with secure

authentication measures results in security flaws. Banks have been relying on two-factor

authentication and one-time password (OTP) which has turned to be obsolete due to

technological innovation. Finally, the lack of sufficient oversight in a fast-growing technological

ecosystem by the government has created security flaws in the mobile application banking

industry. Federal Financial Institution Examination Council (FFIEC) has published some

guidelines that mobile banking applications should meet. However, the same council has failed

to address standard controls on mobile banking application regarding identification and

authentication controls (Bamoriya, & Singh P., 2011, pp. 118). The greatest challenge on

authentication and identification is that other bodies have tried to provide guidelines, but it has

not been substantive to solve financial institutions' mobile banking security challenges. Financial

institutions must establish a high level of trust on mobile channels if they have to remain

competitive.

4. Experimental /System Design

The design of the system involves the processes of defining open banking architecture,

working interfaces, different modules, and required data to meet specific banking requirements.

System design is used by banking institutions to provide comprehensive data about open banking

and its components to facilitate architectural design consistency. The open banking institutions

have different requirements that each mobile banking application should meet before accessing

the required data (Asfaw 2015, pp. 101). The system design context can be sub-divided into

various modules which include; process, interface and working data design. The design of the

system should consider different aspects such as input requirements. In open banking, the input

requirements define the customer data used to access the mobile banking application. Once

validation and authentication of the data are performed the open banking platforms provide

access to the customers' data (Omar et al 2011, pp. 56-57). The input requirements should meet

minimum security aspects such as data encryption and character hiding during data input. The

other security parameter that open banking applications should meet is user validation through

One Time Pin (OTP). It is one of the modern data validation technique which is highly reliable

and convenient. During the system design process, output requirements should conform to the

standard banking specifications. Data retrieval and transmission should not interfere with

confidentiality and integrity (Tiwari, Agarwal, & Goyal 2014, pp. 271). To make sure security

requirements are met, the design processes should be guided by data security principles. Before

The design of the system involves the processes of defining open banking architecture,

working interfaces, different modules, and required data to meet specific banking requirements.

System design is used by banking institutions to provide comprehensive data about open banking

and its components to facilitate architectural design consistency. The open banking institutions

have different requirements that each mobile banking application should meet before accessing

the required data (Asfaw 2015, pp. 101). The system design context can be sub-divided into

various modules which include; process, interface and working data design. The design of the

system should consider different aspects such as input requirements. In open banking, the input

requirements define the customer data used to access the mobile banking application. Once

validation and authentication of the data are performed the open banking platforms provide

access to the customers' data (Omar et al 2011, pp. 56-57). The input requirements should meet

minimum security aspects such as data encryption and character hiding during data input. The

other security parameter that open banking applications should meet is user validation through

One Time Pin (OTP). It is one of the modern data validation technique which is highly reliable

and convenient. During the system design process, output requirements should conform to the

standard banking specifications. Data retrieval and transmission should not interfere with

confidentiality and integrity (Tiwari, Agarwal, & Goyal 2014, pp. 271). To make sure security

requirements are met, the design processes should be guided by data security principles. Before

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

exposing customer data to third parties, all applications should prompt the customer to grant

access to the data.

The next type of system design requirement is storage which focuses mainly on the data

storage security requirements. Data storage is very critical because it requires data to be

protected from unauthorized access by third parties. The design should be enforced to make sure

data is stored securely and only accessible to authorized users (Prasad, Gyani, & Murti 2012, pp.

8). Mobile banking applications that access data should be designed with the highest security

requirements that conform to current banking standards. Any data storage within the mobile

banking applications should not be allowed because it can be accessed and used fraudulently by

unauthorized persons. The design should make sure that all data stored by the financial

institutions be encrypted for security purposes. Data encryption is a fundamental security

concern that every organization should use to protected data from fraudulent use even after

unauthorized data access. Encryption makes data unusable and it is the security mechanism that

guarantees the security of the data if the encryption algorithm is strong. System control and

backup for recovery during IT infrastructure disaster is very important system design aspect.

Organizations should be prepared for any eventuality because IT infrastructure is prone to failure

(Bamoriya, & Singh P., 2011, pp. 112). Data backup should be done frequently to make sure

recovery options are readily available to avoid data loss and business process interruption. To

avoid data loss, the system design should be automated to facilitate data backup without user

interventions. The final system design requirement that mobile banking applications should meet

is data processing criteria. To process data requests from any application user, open banking

platforms should be enforced to make sure the processing of data is specific to the user request.

Some mobile banking applications are designed with capabilities of accessing data from backed

access to the data.

The next type of system design requirement is storage which focuses mainly on the data

storage security requirements. Data storage is very critical because it requires data to be

protected from unauthorized access by third parties. The design should be enforced to make sure

data is stored securely and only accessible to authorized users (Prasad, Gyani, & Murti 2012, pp.

8). Mobile banking applications that access data should be designed with the highest security

requirements that conform to current banking standards. Any data storage within the mobile

banking applications should not be allowed because it can be accessed and used fraudulently by

unauthorized persons. The design should make sure that all data stored by the financial

institutions be encrypted for security purposes. Data encryption is a fundamental security

concern that every organization should use to protected data from fraudulent use even after

unauthorized data access. Encryption makes data unusable and it is the security mechanism that

guarantees the security of the data if the encryption algorithm is strong. System control and

backup for recovery during IT infrastructure disaster is very important system design aspect.

Organizations should be prepared for any eventuality because IT infrastructure is prone to failure

(Bamoriya, & Singh P., 2011, pp. 112). Data backup should be done frequently to make sure

recovery options are readily available to avoid data loss and business process interruption. To

avoid data loss, the system design should be automated to facilitate data backup without user

interventions. The final system design requirement that mobile banking applications should meet

is data processing criteria. To process data requests from any application user, open banking

platforms should be enforced to make sure the processing of data is specific to the user request.

Some mobile banking applications are designed with capabilities of accessing data from backed

without application user permissions (Gupta, Bagoria, & Bagoria 2013, pp. 4-5). Backed data

access is regarded as fraudulent activity and financial institutions should strictly define

requirements that each mobile application should meet. To avoid backed data access, financial

institutions should put in place strict measures that prohibit data protection.

4.1. Fundamentals of Open banking application design

System design is quite specific on what each stakeholder is expected to do in product

design. In the design of the system, system designers should address some concerns that are

mainly used to evaluate system quality. System reliability is a fundamental aspect that measures

system ability to withstand fault tolerance to make sure the system does not fail (Tiwari,

Agarwal, & Goyal 2014, pp. 271). System developers need to build large systems through the

use of components that are fault intolerance in nature. When systems are developed with fault

intolerance components, the subjected system is expected to be reliable because it does not fail

frequently. Open banking applications should be fault tolerance to make them reliable at all

times and when required by users. Faults can either be hardware or software but the main focus,

in this case, is software fault tolerance. Software faults can be caused by a variety of reasons

such as bug, malware and code compromise. Important to note is that a runaway system process

can over-utilize system resources and cause application failure across various nodes that are

running the Application. It is only through the understanding of the business requirements that

mobile application faults can be resiliently handled. System developers should implement

application communication features that can support user interaction to support application

monitoring (Bhuiyan, & Rahman 2013, pp. 54-55). Better application unit testing and the use of

abstraction in the design processes can be easily used to isolate faults in mobile banking

applications.

access is regarded as fraudulent activity and financial institutions should strictly define

requirements that each mobile application should meet. To avoid backed data access, financial

institutions should put in place strict measures that prohibit data protection.

4.1. Fundamentals of Open banking application design

System design is quite specific on what each stakeholder is expected to do in product

design. In the design of the system, system designers should address some concerns that are

mainly used to evaluate system quality. System reliability is a fundamental aspect that measures

system ability to withstand fault tolerance to make sure the system does not fail (Tiwari,

Agarwal, & Goyal 2014, pp. 271). System developers need to build large systems through the

use of components that are fault intolerance in nature. When systems are developed with fault

intolerance components, the subjected system is expected to be reliable because it does not fail

frequently. Open banking applications should be fault tolerance to make them reliable at all

times and when required by users. Faults can either be hardware or software but the main focus,

in this case, is software fault tolerance. Software faults can be caused by a variety of reasons

such as bug, malware and code compromise. Important to note is that a runaway system process

can over-utilize system resources and cause application failure across various nodes that are

running the Application. It is only through the understanding of the business requirements that

mobile application faults can be resiliently handled. System developers should implement

application communication features that can support user interaction to support application

monitoring (Bhuiyan, & Rahman 2013, pp. 54-55). Better application unit testing and the use of

abstraction in the design processes can be easily used to isolate faults in mobile banking

applications.

The next application development fundamental is the scalability which is the mobile

banking application ability to offer required performance. The performance of the subjected

application should remain the same despite the increase in any form of system load. The

application load is used to describe operational characteristics concerning changing application

load parameters. In open mobile applications, performance can be measured regarding its

response time (Bahl 2012, pp. 229). The time is taken for a mobile application to submit a

request or process a request presents an ideal measure of the performance. It is the responsibility

of the system developers to make sure the system is scalable and can offer the required

functionality effectively. Finally, system maintainability is meant to understand code layout

during application development. System developers need to adopt modularity in the application