Desklib - Online Library for Study Material with Solved Assignments

VerifiedAdded on 2023/06/13

|33

|3327

|378

AI Summary

The article discusses budgeting and includes a sales budget, purchase budget, income statement, and cash budget. It also covers the evaluation of the production manager's performance and a flexible budget performance report. Additionally, it provides a budgeted income statement and cash budget for Desklib, an online library for study material with solved assignments.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: BUDGETING

BUDGETING

Name of the Student

Name of the University

Author Note

BUDGETING

Name of the Student

Name of the University

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1BUDGETING

Table of Contents

Acttivity 1........................................................................................................................................3

Task 1...........................................................................................................................................3

Task 2...........................................................................................................................................4

Task 3...........................................................................................................................................5

Task 4...........................................................................................................................................9

Task 5.........................................................................................................................................10

Task 6.........................................................................................................................................12

Activity 2.......................................................................................................................................14

Cash Budget...............................................................................................................................14

Acitivity 3......................................................................................................................................17

Budgeted Income statement.......................................................................................................17

Cash budget...............................................................................................................................20

Budgeted Balance Sheet as on June, 2015.................................................................................22

Activity 4.......................................................................................................................................26

Answer to Question 1................................................................................................................26

Answer to Question 2................................................................................................................27

Answer to Question 3................................................................................................................29

Answer to Question 4................................................................................................................31

References......................................................................................................................................33

Table of Contents

Acttivity 1........................................................................................................................................3

Task 1...........................................................................................................................................3

Task 2...........................................................................................................................................4

Task 3...........................................................................................................................................5

Task 4...........................................................................................................................................9

Task 5.........................................................................................................................................10

Task 6.........................................................................................................................................12

Activity 2.......................................................................................................................................14

Cash Budget...............................................................................................................................14

Acitivity 3......................................................................................................................................17

Budgeted Income statement.......................................................................................................17

Cash budget...............................................................................................................................20

Budgeted Balance Sheet as on June, 2015.................................................................................22

Activity 4.......................................................................................................................................26

Answer to Question 1................................................................................................................26

Answer to Question 2................................................................................................................27

Answer to Question 3................................................................................................................29

Answer to Question 4................................................................................................................31

References......................................................................................................................................33

2BUDGETING

3BUDGETING

Activity 1

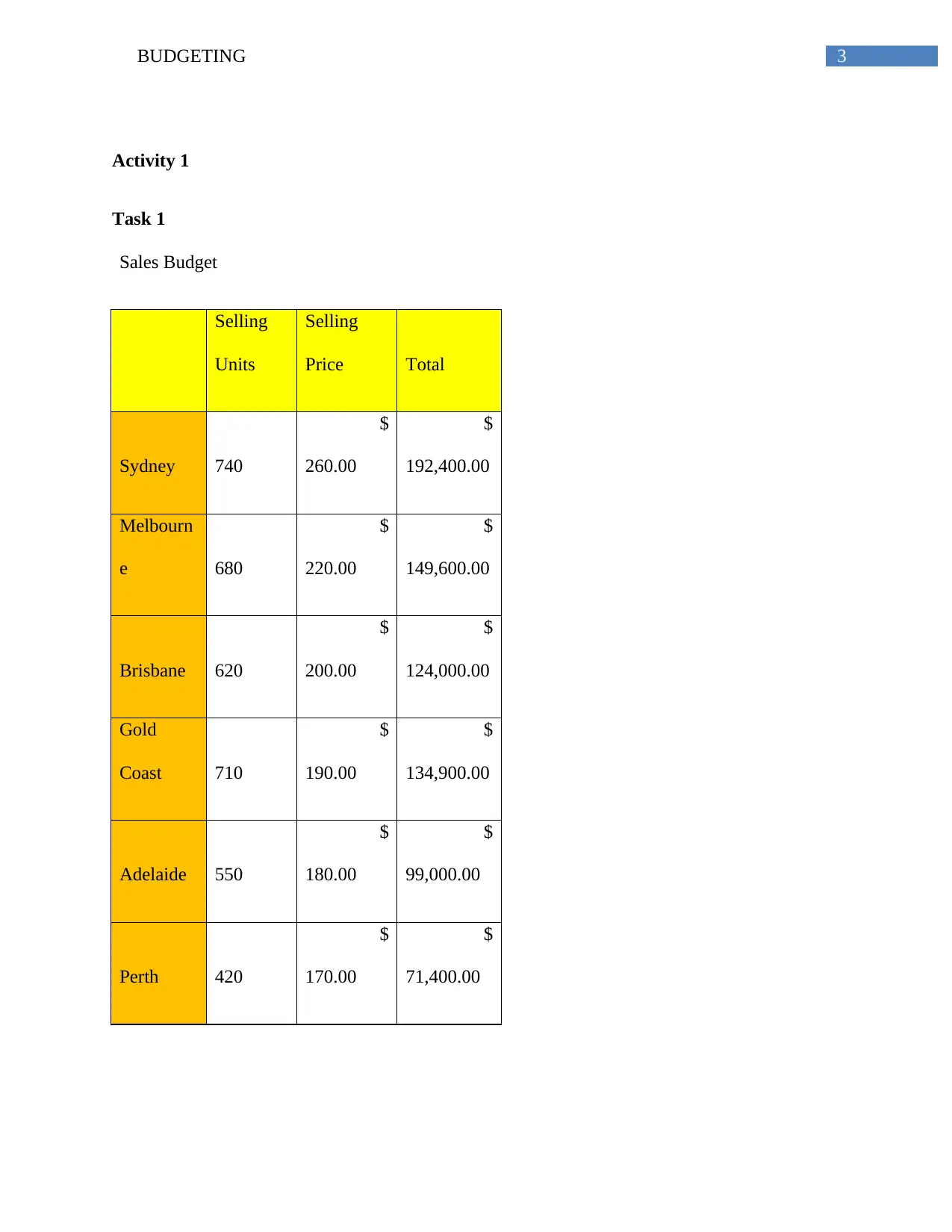

Task 1

Sales Budget

Selling

Units

Selling

Price Total

Sydney 740

$

260.00

$

192,400.00

Melbourn

e 680

$

220.00

$

149,600.00

Brisbane 620

$

200.00

$

124,000.00

Gold

Coast 710

$

190.00

$

134,900.00

Adelaide 550

$

180.00

$

99,000.00

Perth 420

$

170.00

$

71,400.00

Activity 1

Task 1

Sales Budget

Selling

Units

Selling

Price Total

Sydney 740

$

260.00

$

192,400.00

Melbourn

e 680

$

220.00

$

149,600.00

Brisbane 620

$

200.00

$

124,000.00

Gold

Coast 710

$

190.00

$

134,900.00

Adelaide 550

$

180.00

$

99,000.00

Perth 420

$

170.00

$

71,400.00

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4BUDGETING

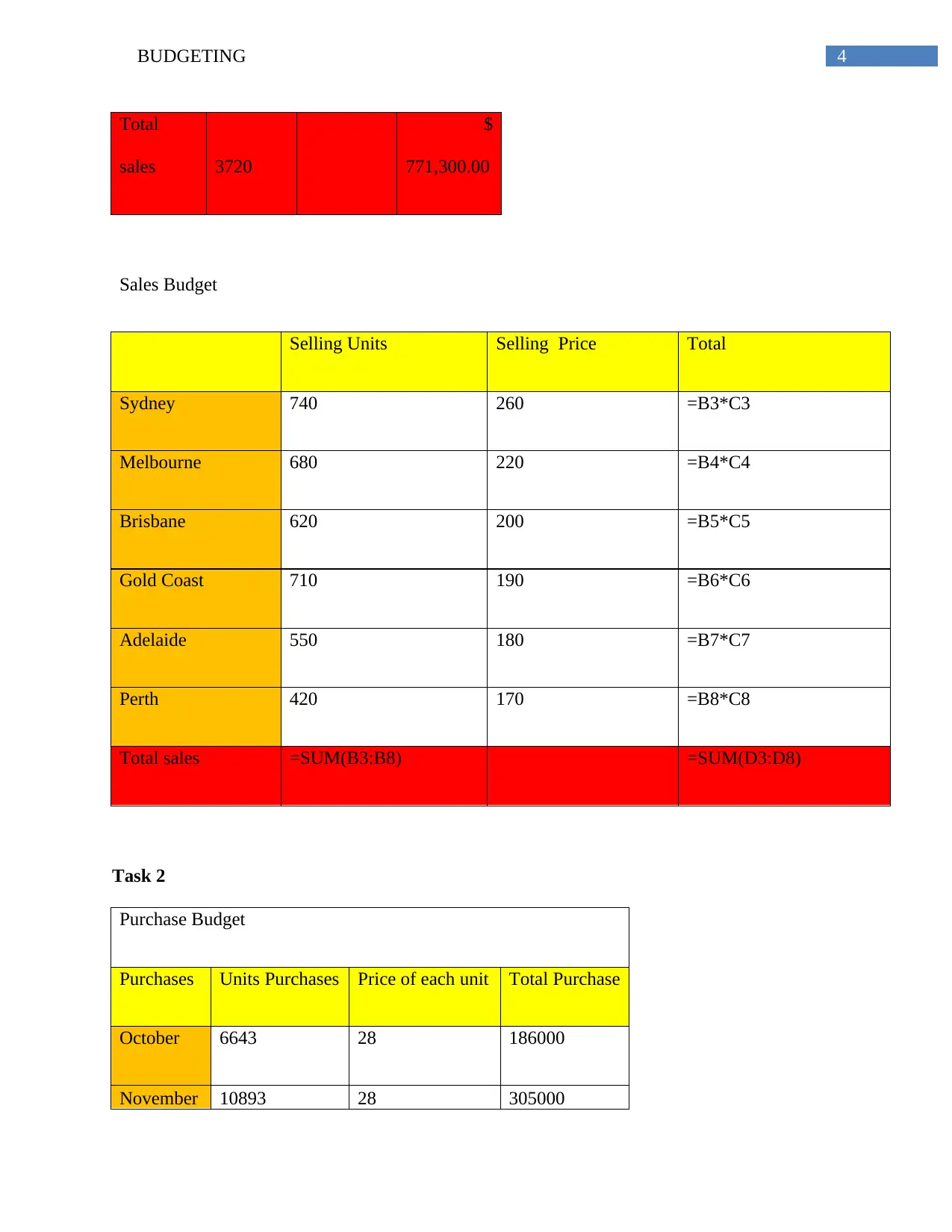

Total

sales 3720

$

771,300.00

Sales Budget

Selling Units Selling Price Total

Sydney 740 260 =B3*C3

Melbourne 680 220 =B4*C4

Brisbane 620 200 =B5*C5

Gold Coast 710 190 =B6*C6

Adelaide 550 180 =B7*C7

Perth 420 170 =B8*C8

Total sales =SUM(B3:B8) =SUM(D3:D8)

Task 2

Purchase Budget

Purchases Units Purchases Price of each unit Total Purchase

October 6643 28 186000

November 10893 28 305000

Total

sales 3720

$

771,300.00

Sales Budget

Selling Units Selling Price Total

Sydney 740 260 =B3*C3

Melbourne 680 220 =B4*C4

Brisbane 620 200 =B5*C5

Gold Coast 710 190 =B6*C6

Adelaide 550 180 =B7*C7

Perth 420 170 =B8*C8

Total sales =SUM(B3:B8) =SUM(D3:D8)

Task 2

Purchase Budget

Purchases Units Purchases Price of each unit Total Purchase

October 6643 28 186000

November 10893 28 305000

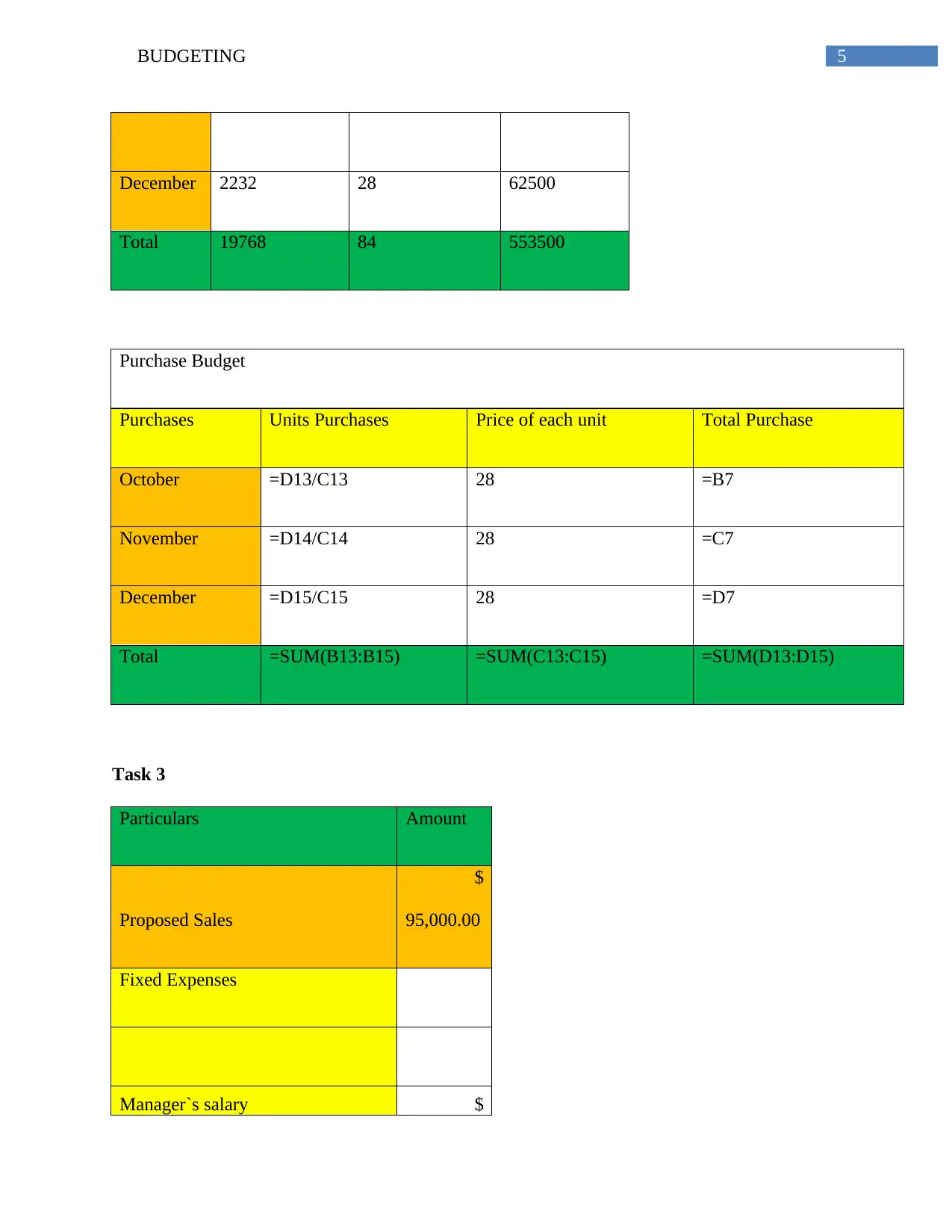

5BUDGETING

December 2232 28 62500

Total 19768 84 553500

Purchase Budget

Purchases Units Purchases Price of each unit Total Purchase

October =D13/C13 28 =B7

November =D14/C14 28 =C7

December =D15/C15 28 =D7

Total =SUM(B13:B15) =SUM(C13:C15) =SUM(D13:D15)

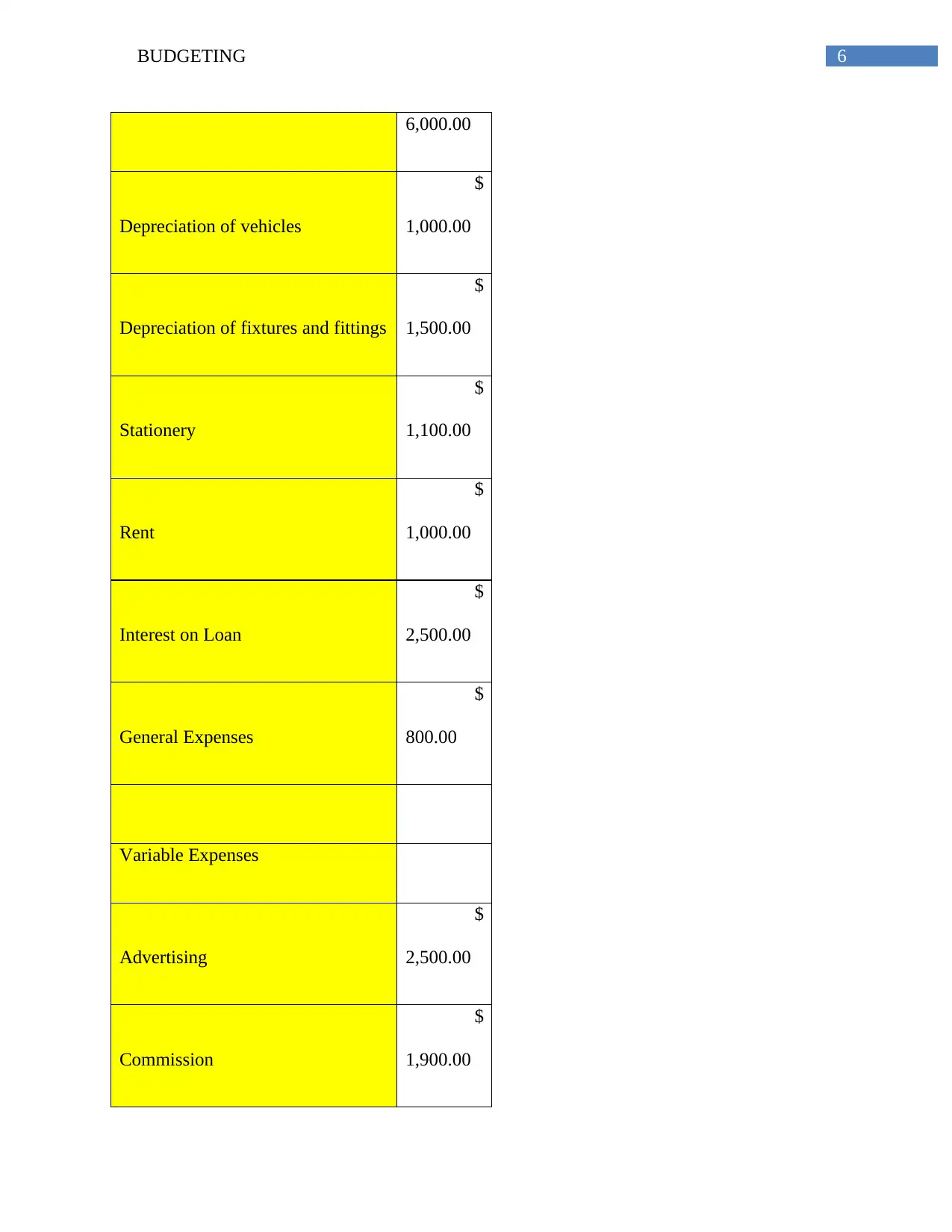

Task 3

Particulars Amount

Proposed Sales

$

95,000.00

Fixed Expenses

Manager`s salary $

December 2232 28 62500

Total 19768 84 553500

Purchase Budget

Purchases Units Purchases Price of each unit Total Purchase

October =D13/C13 28 =B7

November =D14/C14 28 =C7

December =D15/C15 28 =D7

Total =SUM(B13:B15) =SUM(C13:C15) =SUM(D13:D15)

Task 3

Particulars Amount

Proposed Sales

$

95,000.00

Fixed Expenses

Manager`s salary $

6BUDGETING

6,000.00

Depreciation of vehicles

$

1,000.00

Depreciation of fixtures and fittings

$

1,500.00

Stationery

$

1,100.00

Rent

$

1,000.00

Interest on Loan

$

2,500.00

General Expenses

$

800.00

Variable Expenses

Advertising

$

2,500.00

Commission

$

1,900.00

6,000.00

Depreciation of vehicles

$

1,000.00

Depreciation of fixtures and fittings

$

1,500.00

Stationery

$

1,100.00

Rent

$

1,000.00

Interest on Loan

$

2,500.00

General Expenses

$

800.00

Variable Expenses

Advertising

$

2,500.00

Commission

$

1,900.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

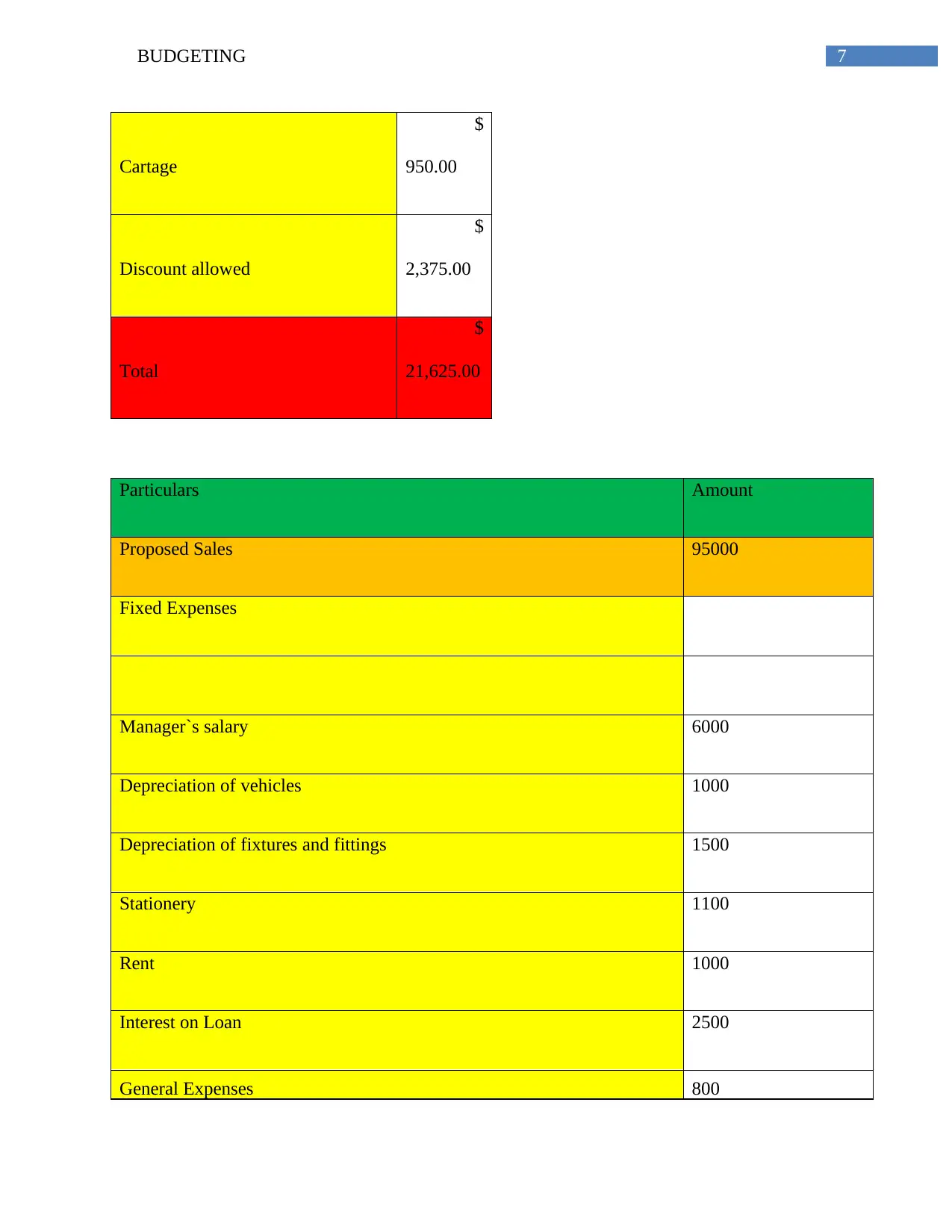

7BUDGETING

Cartage

$

950.00

Discount allowed

$

2,375.00

Total

$

21,625.00

Particulars Amount

Proposed Sales 95000

Fixed Expenses

Manager`s salary 6000

Depreciation of vehicles 1000

Depreciation of fixtures and fittings 1500

Stationery 1100

Rent 1000

Interest on Loan 2500

General Expenses 800

Cartage

$

950.00

Discount allowed

$

2,375.00

Total

$

21,625.00

Particulars Amount

Proposed Sales 95000

Fixed Expenses

Manager`s salary 6000

Depreciation of vehicles 1000

Depreciation of fixtures and fittings 1500

Stationery 1100

Rent 1000

Interest on Loan 2500

General Expenses 800

8BUDGETING

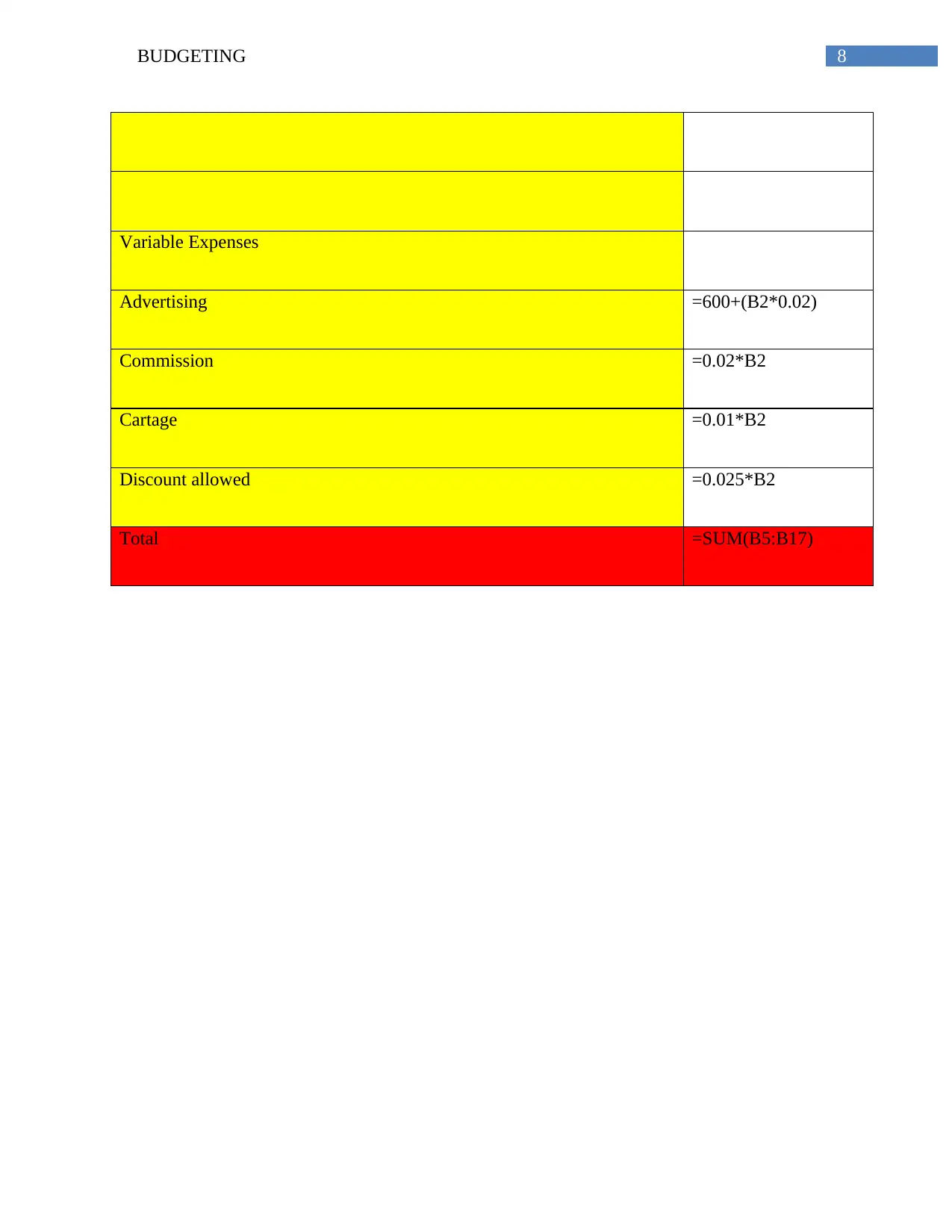

Variable Expenses

Advertising =600+(B2*0.02)

Commission =0.02*B2

Cartage =0.01*B2

Discount allowed =0.025*B2

Total =SUM(B5:B17)

Variable Expenses

Advertising =600+(B2*0.02)

Commission =0.02*B2

Cartage =0.01*B2

Discount allowed =0.025*B2

Total =SUM(B5:B17)

9BUDGETING

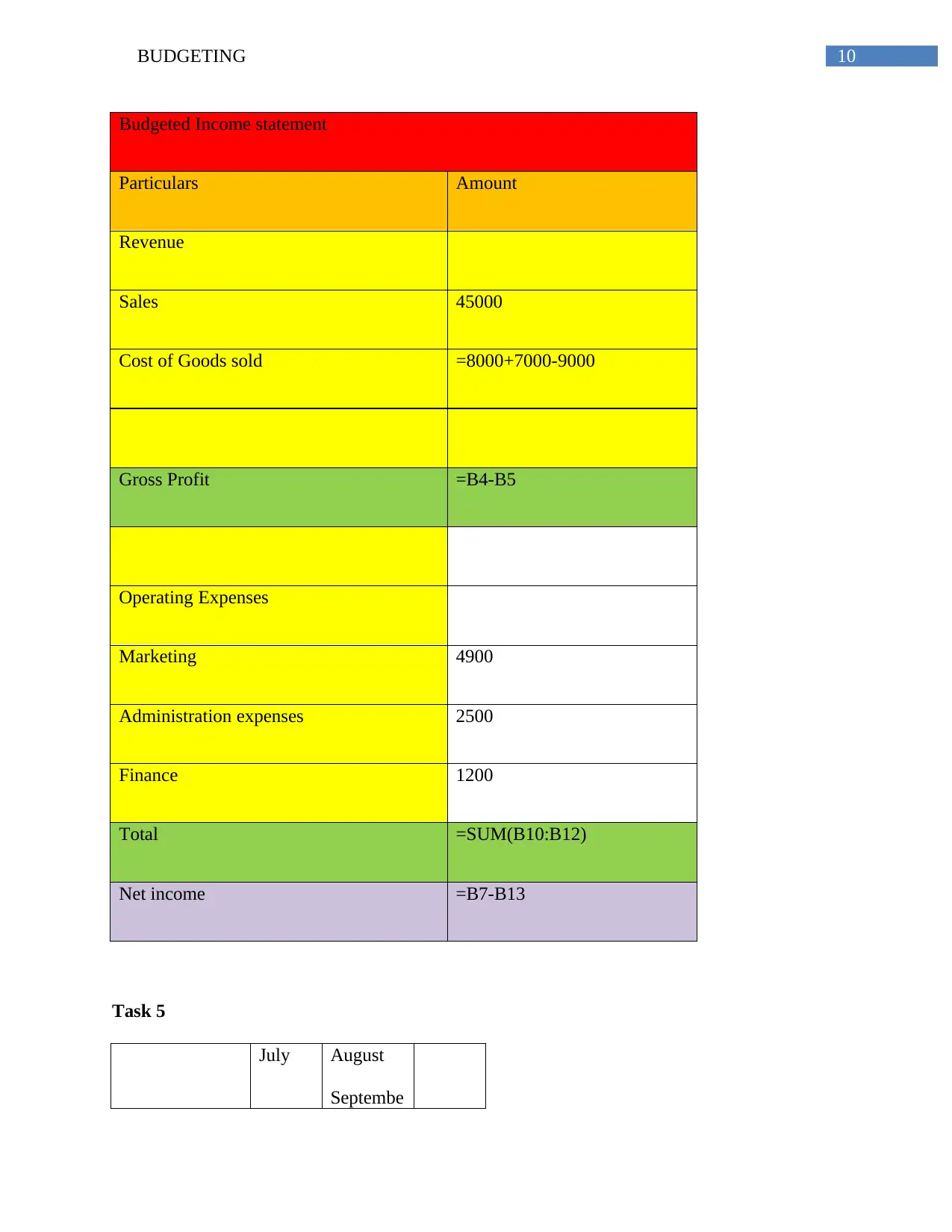

Task 4

Budgeted Income statement

Particulars

Amoun

t

Revenue

Sales 45000

Cost of Goods sold 6000

Gross Profit 39000

Operating Expenses

Marketing 4900

Administration expenses 2500

Finance 1200

Total 8600

Net income 30400

Task 4

Budgeted Income statement

Particulars

Amoun

t

Revenue

Sales 45000

Cost of Goods sold 6000

Gross Profit 39000

Operating Expenses

Marketing 4900

Administration expenses 2500

Finance 1200

Total 8600

Net income 30400

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10BUDGETING

Budgeted Income statement

Particulars Amount

Revenue

Sales 45000

Cost of Goods sold =8000+7000-9000

Gross Profit =B4-B5

Operating Expenses

Marketing 4900

Administration expenses 2500

Finance 1200

Total =SUM(B10:B12)

Net income =B7-B13

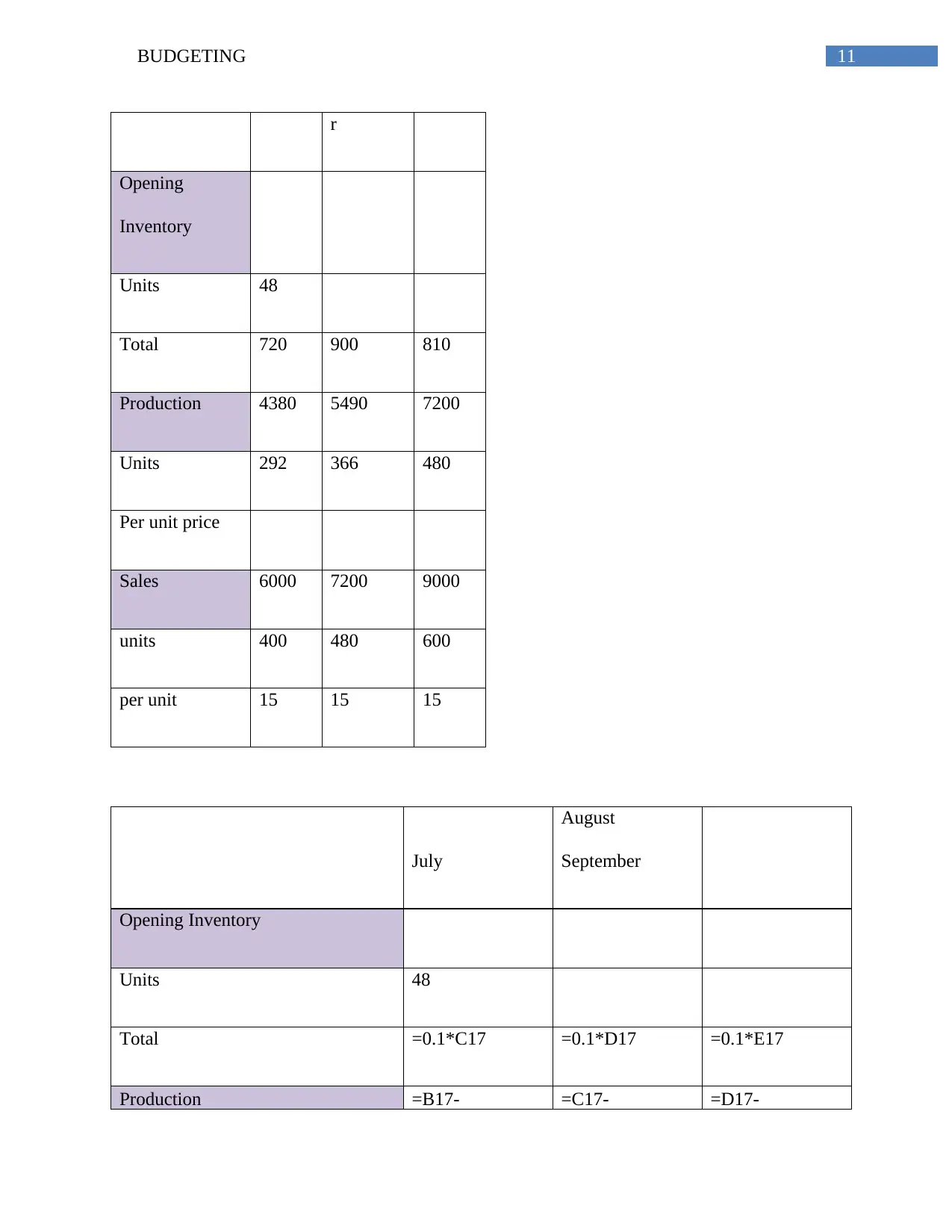

Task 5

July August

Septembe

Budgeted Income statement

Particulars Amount

Revenue

Sales 45000

Cost of Goods sold =8000+7000-9000

Gross Profit =B4-B5

Operating Expenses

Marketing 4900

Administration expenses 2500

Finance 1200

Total =SUM(B10:B12)

Net income =B7-B13

Task 5

July August

Septembe

11BUDGETING

r

Opening

Inventory

Units 48

Total 720 900 810

Production 4380 5490 7200

Units 292 366 480

Per unit price

Sales 6000 7200 9000

units 400 480 600

per unit 15 15 15

July

August

September

Opening Inventory

Units 48

Total =0.1*C17 =0.1*D17 =0.1*E17

Production =B17- =C17- =D17-

r

Opening

Inventory

Units 48

Total 720 900 810

Production 4380 5490 7200

Units 292 366 480

Per unit price

Sales 6000 7200 9000

units 400 480 600

per unit 15 15 15

July

August

September

Opening Inventory

Units 48

Total =0.1*C17 =0.1*D17 =0.1*E17

Production =B17- =C17- =D17-

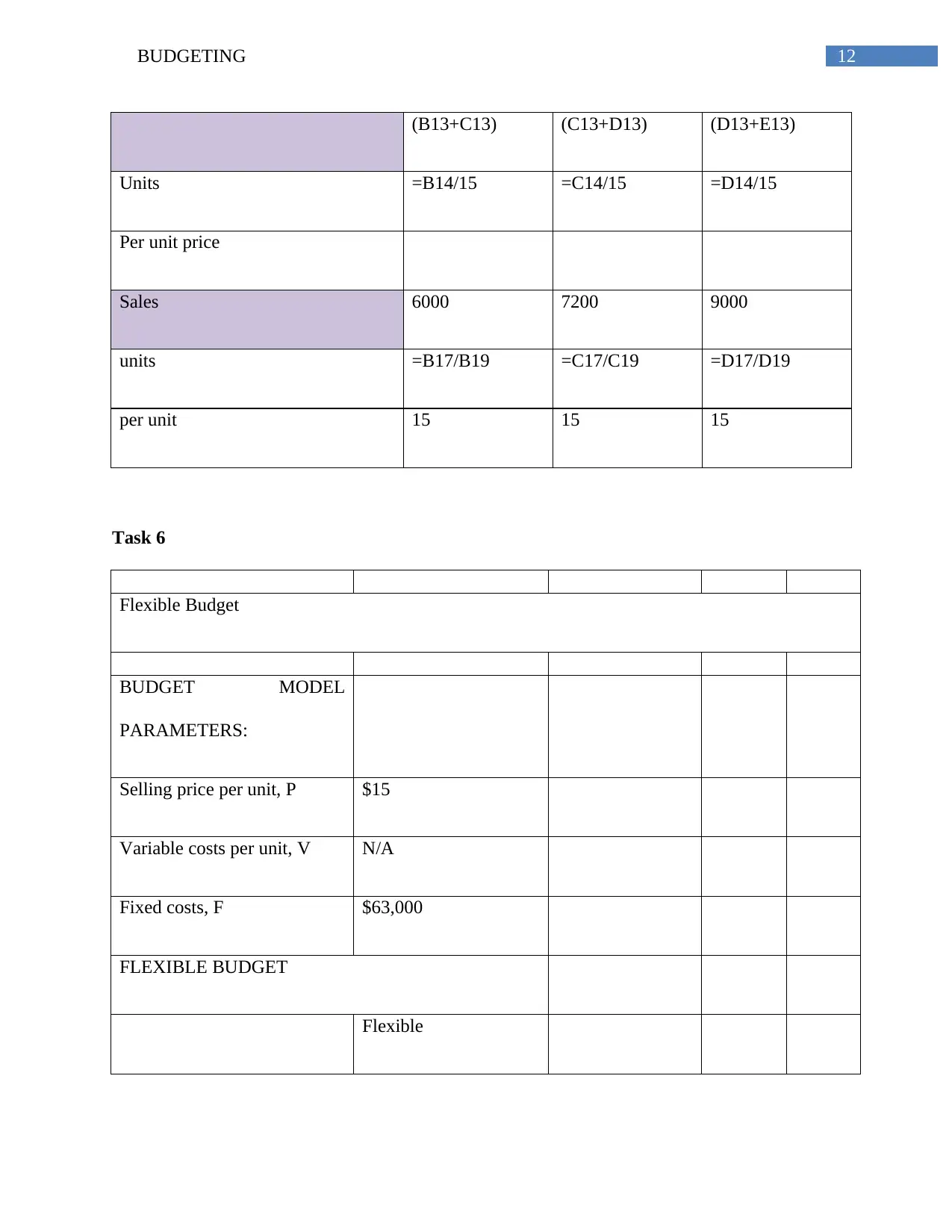

12BUDGETING

(B13+C13) (C13+D13) (D13+E13)

Units =B14/15 =C14/15 =D14/15

Per unit price

Sales 6000 7200 9000

units =B17/B19 =C17/C19 =D17/D19

per unit 15 15 15

Task 6

Flexible Budget

BUDGET MODEL

PARAMETERS:

Selling price per unit, P $15

Variable costs per unit, V N/A

Fixed costs, F $63,000

FLEXIBLE BUDGET

Flexible

(B13+C13) (C13+D13) (D13+E13)

Units =B14/15 =C14/15 =D14/15

Per unit price

Sales 6000 7200 9000

units =B17/B19 =C17/C19 =D17/D19

per unit 15 15 15

Task 6

Flexible Budget

BUDGET MODEL

PARAMETERS:

Selling price per unit, P $15

Variable costs per unit, V N/A

Fixed costs, F $63,000

FLEXIBLE BUDGET

Flexible

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13BUDGETING

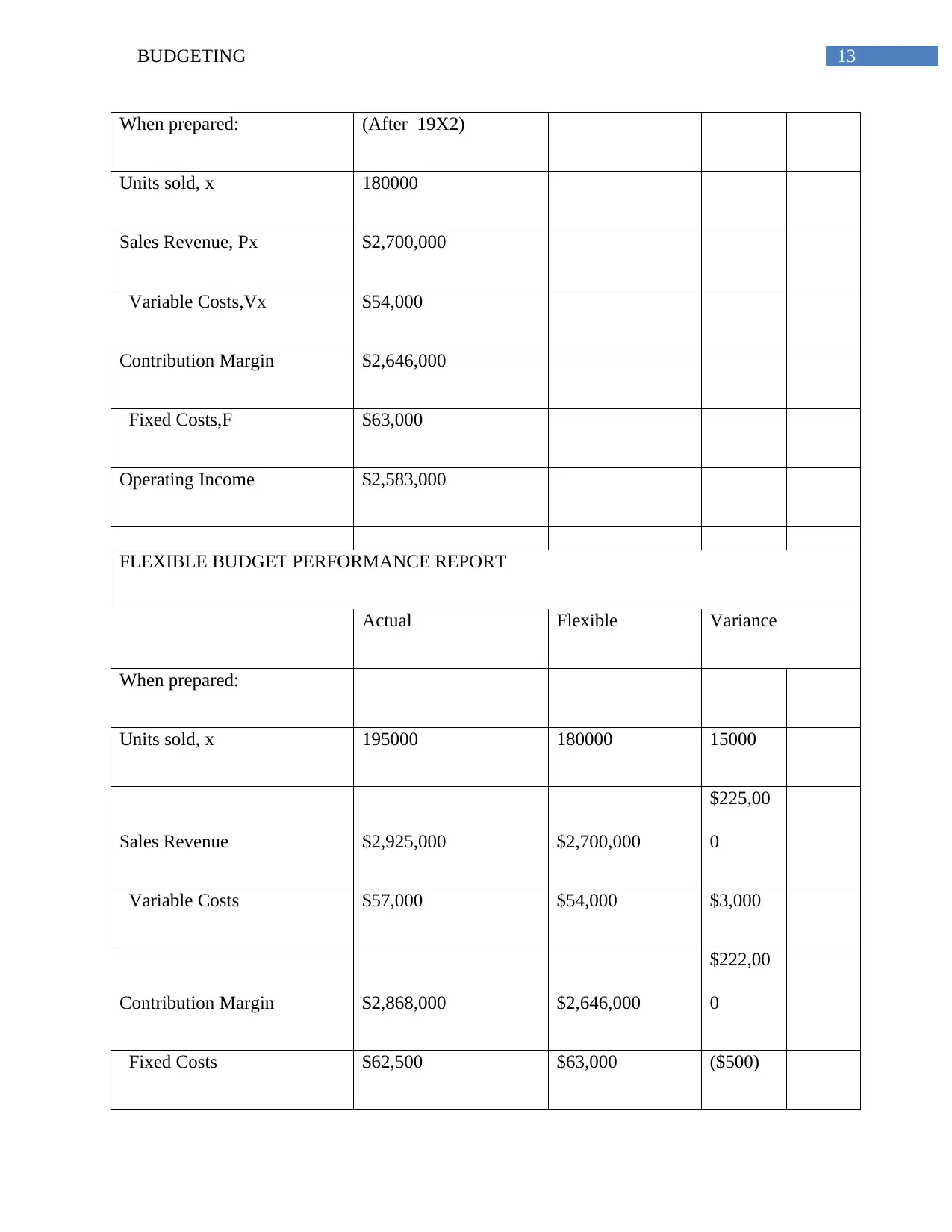

When prepared: (After 19X2)

Units sold, x 180000

Sales Revenue, Px $2,700,000

Variable Costs,Vx $54,000

Contribution Margin $2,646,000

Fixed Costs,F $63,000

Operating Income $2,583,000

FLEXIBLE BUDGET PERFORMANCE REPORT

Actual Flexible Variance

When prepared:

Units sold, x 195000 180000 15000

Sales Revenue $2,925,000 $2,700,000

$225,00

0

Variable Costs $57,000 $54,000 $3,000

Contribution Margin $2,868,000 $2,646,000

$222,00

0

Fixed Costs $62,500 $63,000 ($500)

When prepared: (After 19X2)

Units sold, x 180000

Sales Revenue, Px $2,700,000

Variable Costs,Vx $54,000

Contribution Margin $2,646,000

Fixed Costs,F $63,000

Operating Income $2,583,000

FLEXIBLE BUDGET PERFORMANCE REPORT

Actual Flexible Variance

When prepared:

Units sold, x 195000 180000 15000

Sales Revenue $2,925,000 $2,700,000

$225,00

0

Variable Costs $57,000 $54,000 $3,000

Contribution Margin $2,868,000 $2,646,000

$222,00

0

Fixed Costs $62,500 $63,000 ($500)

14BUDGETING

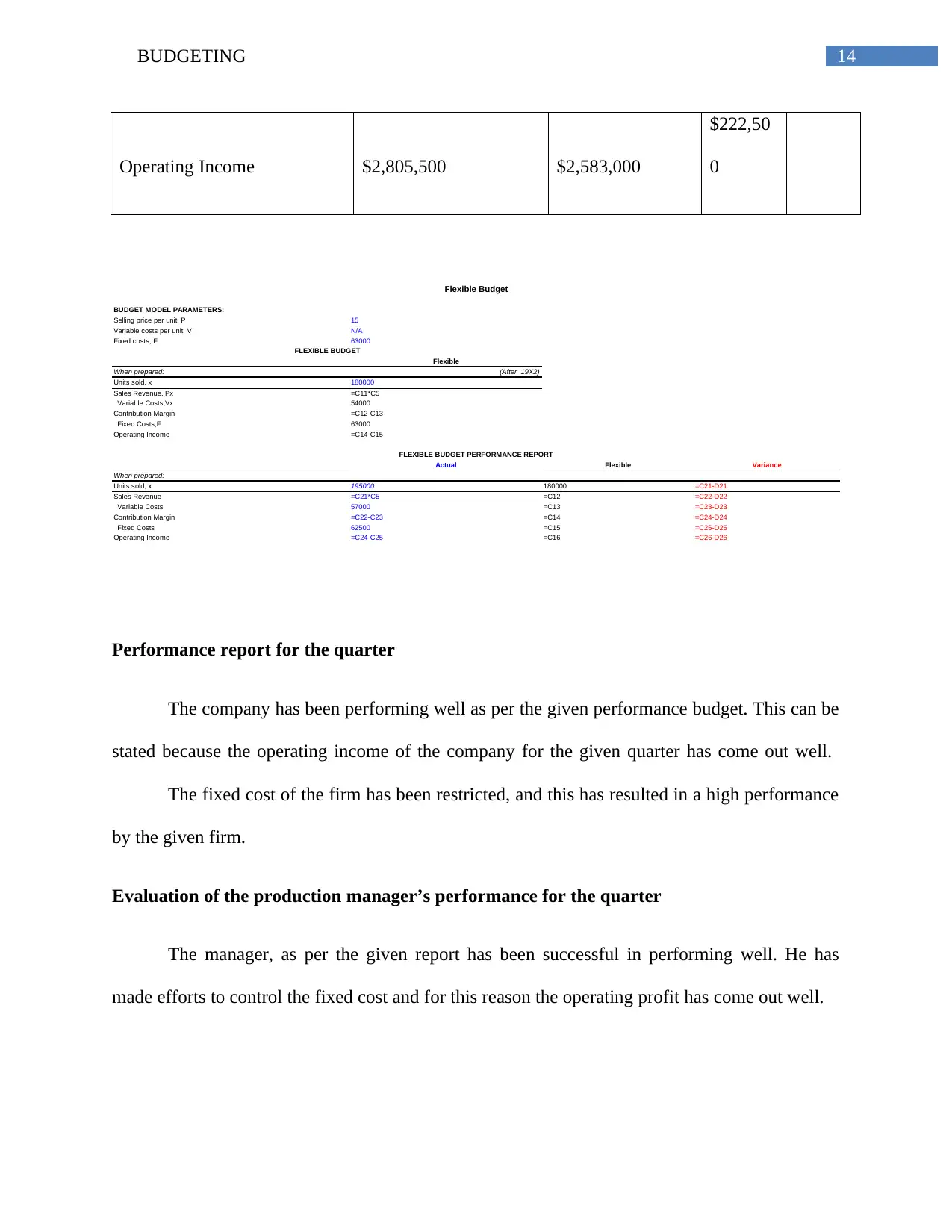

Operating Income $2,805,500 $2,583,000

$222,50

0

Flexible Budget

BUDGET MODEL PARAMETERS:

Selling price per unit, P 15

Variable costs per unit, V N/A

Fixed costs, F 63000

FLEXIBLE BUDGET

Flexible

When prepared: (After 19X2)

Units sold, x 180000

Sales Revenue, Px =C11*C5

Variable Costs,Vx 54000

Contribution Margin =C12-C13

Fixed Costs,F 63000

Operating Income =C14-C15

FLEXIBLE BUDGET PERFORMANCE REPORT

Actual Flexible Variance

When prepared:

Units sold, x 195000 180000 =C21-D21

Sales Revenue =C21*C5 =C12 =C22-D22

Variable Costs 57000 =C13 =C23-D23

Contribution Margin =C22-C23 =C14 =C24-D24

Fixed Costs 62500 =C15 =C25-D25

Operating Income =C24-C25 =C16 =C26-D26

Performance report for the quarter

The company has been performing well as per the given performance budget. This can be

stated because the operating income of the company for the given quarter has come out well.

The fixed cost of the firm has been restricted, and this has resulted in a high performance

by the given firm.

Evaluation of the production manager’s performance for the quarter

The manager, as per the given report has been successful in performing well. He has

made efforts to control the fixed cost and for this reason the operating profit has come out well.

Operating Income $2,805,500 $2,583,000

$222,50

0

Flexible Budget

BUDGET MODEL PARAMETERS:

Selling price per unit, P 15

Variable costs per unit, V N/A

Fixed costs, F 63000

FLEXIBLE BUDGET

Flexible

When prepared: (After 19X2)

Units sold, x 180000

Sales Revenue, Px =C11*C5

Variable Costs,Vx 54000

Contribution Margin =C12-C13

Fixed Costs,F 63000

Operating Income =C14-C15

FLEXIBLE BUDGET PERFORMANCE REPORT

Actual Flexible Variance

When prepared:

Units sold, x 195000 180000 =C21-D21

Sales Revenue =C21*C5 =C12 =C22-D22

Variable Costs 57000 =C13 =C23-D23

Contribution Margin =C22-C23 =C14 =C24-D24

Fixed Costs 62500 =C15 =C25-D25

Operating Income =C24-C25 =C16 =C26-D26

Performance report for the quarter

The company has been performing well as per the given performance budget. This can be

stated because the operating income of the company for the given quarter has come out well.

The fixed cost of the firm has been restricted, and this has resulted in a high performance

by the given firm.

Evaluation of the production manager’s performance for the quarter

The manager, as per the given report has been successful in performing well. He has

made efforts to control the fixed cost and for this reason the operating profit has come out well.

15BUDGETING

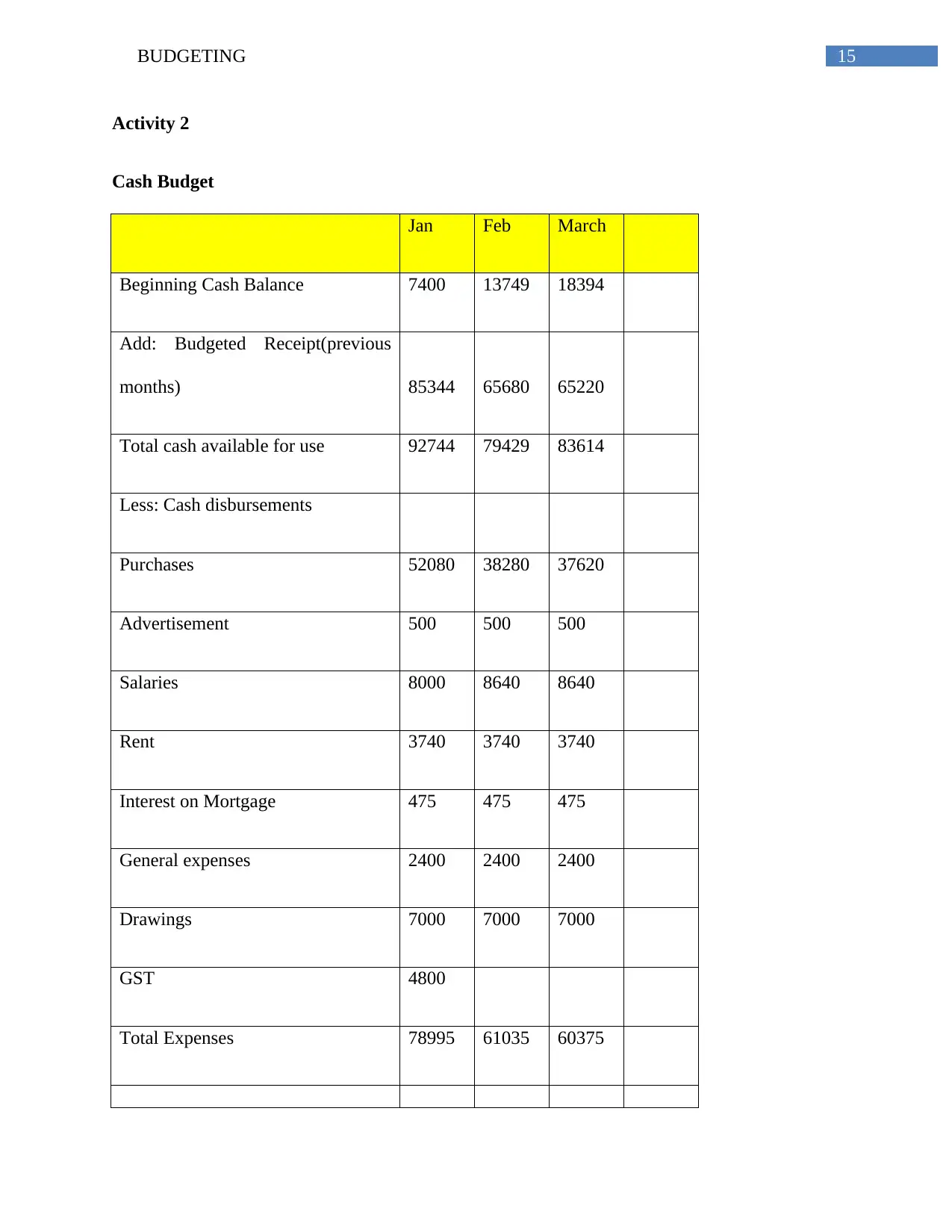

Activity 2

Cash Budget

Jan Feb March

Beginning Cash Balance 7400 13749 18394

Add: Budgeted Receipt(previous

months) 85344 65680 65220

Total cash available for use 92744 79429 83614

Less: Cash disbursements

Purchases 52080 38280 37620

Advertisement 500 500 500

Salaries 8000 8640 8640

Rent 3740 3740 3740

Interest on Mortgage 475 475 475

General expenses 2400 2400 2400

Drawings 7000 7000 7000

GST 4800

Total Expenses 78995 61035 60375

Activity 2

Cash Budget

Jan Feb March

Beginning Cash Balance 7400 13749 18394

Add: Budgeted Receipt(previous

months) 85344 65680 65220

Total cash available for use 92744 79429 83614

Less: Cash disbursements

Purchases 52080 38280 37620

Advertisement 500 500 500

Salaries 8000 8640 8640

Rent 3740 3740 3740

Interest on Mortgage 475 475 475

General expenses 2400 2400 2400

Drawings 7000 7000 7000

GST 4800

Total Expenses 78995 61035 60375

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

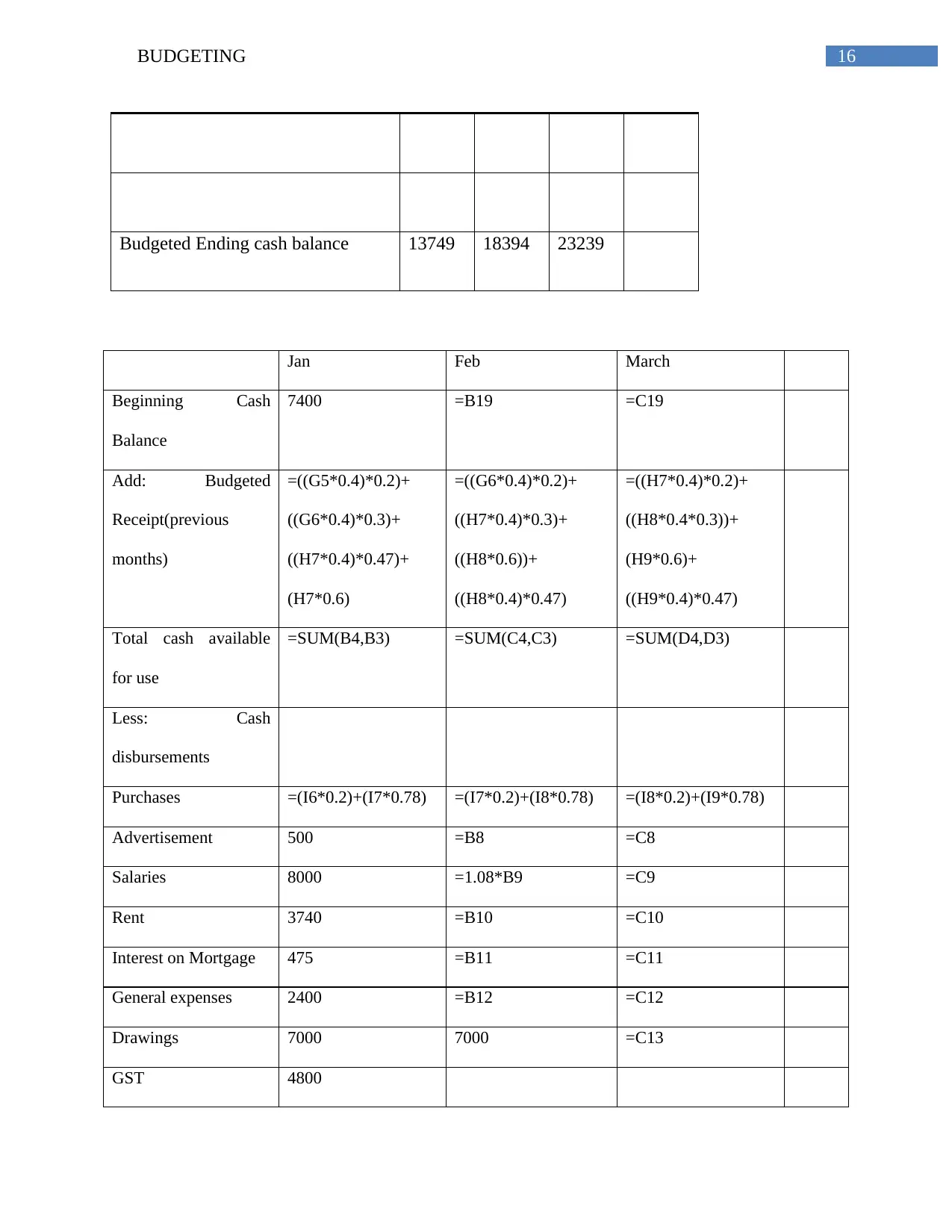

16BUDGETING

Budgeted Ending cash balance 13749 18394 23239

Jan Feb March

Beginning Cash

Balance

7400 =B19 =C19

Add: Budgeted

Receipt(previous

months)

=((G5*0.4)*0.2)+

((G6*0.4)*0.3)+

((H7*0.4)*0.47)+

(H7*0.6)

=((G6*0.4)*0.2)+

((H7*0.4)*0.3)+

((H8*0.6))+

((H8*0.4)*0.47)

=((H7*0.4)*0.2)+

((H8*0.4*0.3))+

(H9*0.6)+

((H9*0.4)*0.47)

Total cash available

for use

=SUM(B4,B3) =SUM(C4,C3) =SUM(D4,D3)

Less: Cash

disbursements

Purchases =(I6*0.2)+(I7*0.78) =(I7*0.2)+(I8*0.78) =(I8*0.2)+(I9*0.78)

Advertisement 500 =B8 =C8

Salaries 8000 =1.08*B9 =C9

Rent 3740 =B10 =C10

Interest on Mortgage 475 =B11 =C11

General expenses 2400 =B12 =C12

Drawings 7000 7000 =C13

GST 4800

Budgeted Ending cash balance 13749 18394 23239

Jan Feb March

Beginning Cash

Balance

7400 =B19 =C19

Add: Budgeted

Receipt(previous

months)

=((G5*0.4)*0.2)+

((G6*0.4)*0.3)+

((H7*0.4)*0.47)+

(H7*0.6)

=((G6*0.4)*0.2)+

((H7*0.4)*0.3)+

((H8*0.6))+

((H8*0.4)*0.47)

=((H7*0.4)*0.2)+

((H8*0.4*0.3))+

(H9*0.6)+

((H9*0.4)*0.47)

Total cash available

for use

=SUM(B4,B3) =SUM(C4,C3) =SUM(D4,D3)

Less: Cash

disbursements

Purchases =(I6*0.2)+(I7*0.78) =(I7*0.2)+(I8*0.78) =(I8*0.2)+(I9*0.78)

Advertisement 500 =B8 =C8

Salaries 8000 =1.08*B9 =C9

Rent 3740 =B10 =C10

Interest on Mortgage 475 =B11 =C11

General expenses 2400 =B12 =C12

Drawings 7000 7000 =C13

GST 4800

17BUDGETING

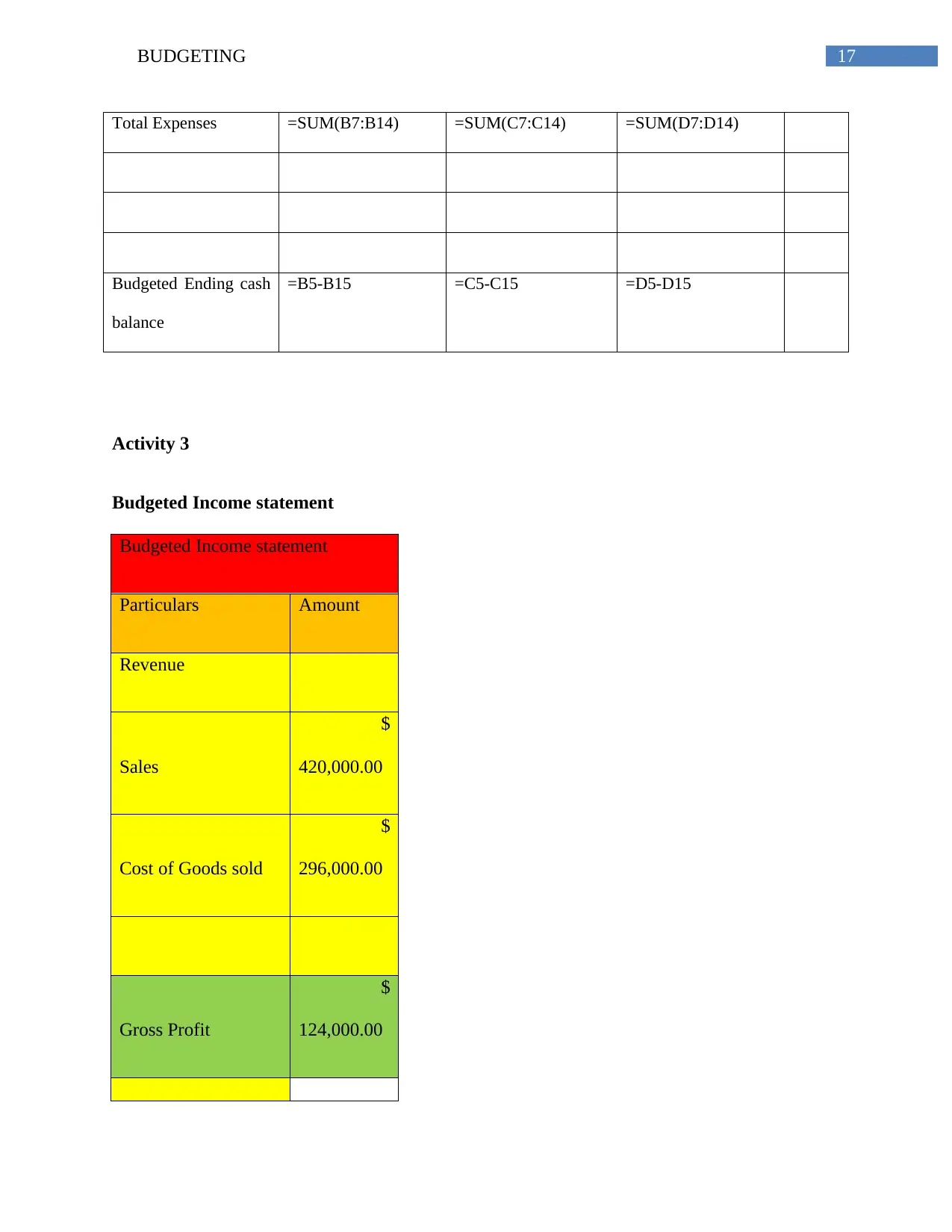

Total Expenses =SUM(B7:B14) =SUM(C7:C14) =SUM(D7:D14)

Budgeted Ending cash

balance

=B5-B15 =C5-C15 =D5-D15

Activity 3

Budgeted Income statement

Budgeted Income statement

Particulars Amount

Revenue

Sales

$

420,000.00

Cost of Goods sold

$

296,000.00

Gross Profit

$

124,000.00

Total Expenses =SUM(B7:B14) =SUM(C7:C14) =SUM(D7:D14)

Budgeted Ending cash

balance

=B5-B15 =C5-C15 =D5-D15

Activity 3

Budgeted Income statement

Budgeted Income statement

Particulars Amount

Revenue

Sales

$

420,000.00

Cost of Goods sold

$

296,000.00

Gross Profit

$

124,000.00

18BUDGETING

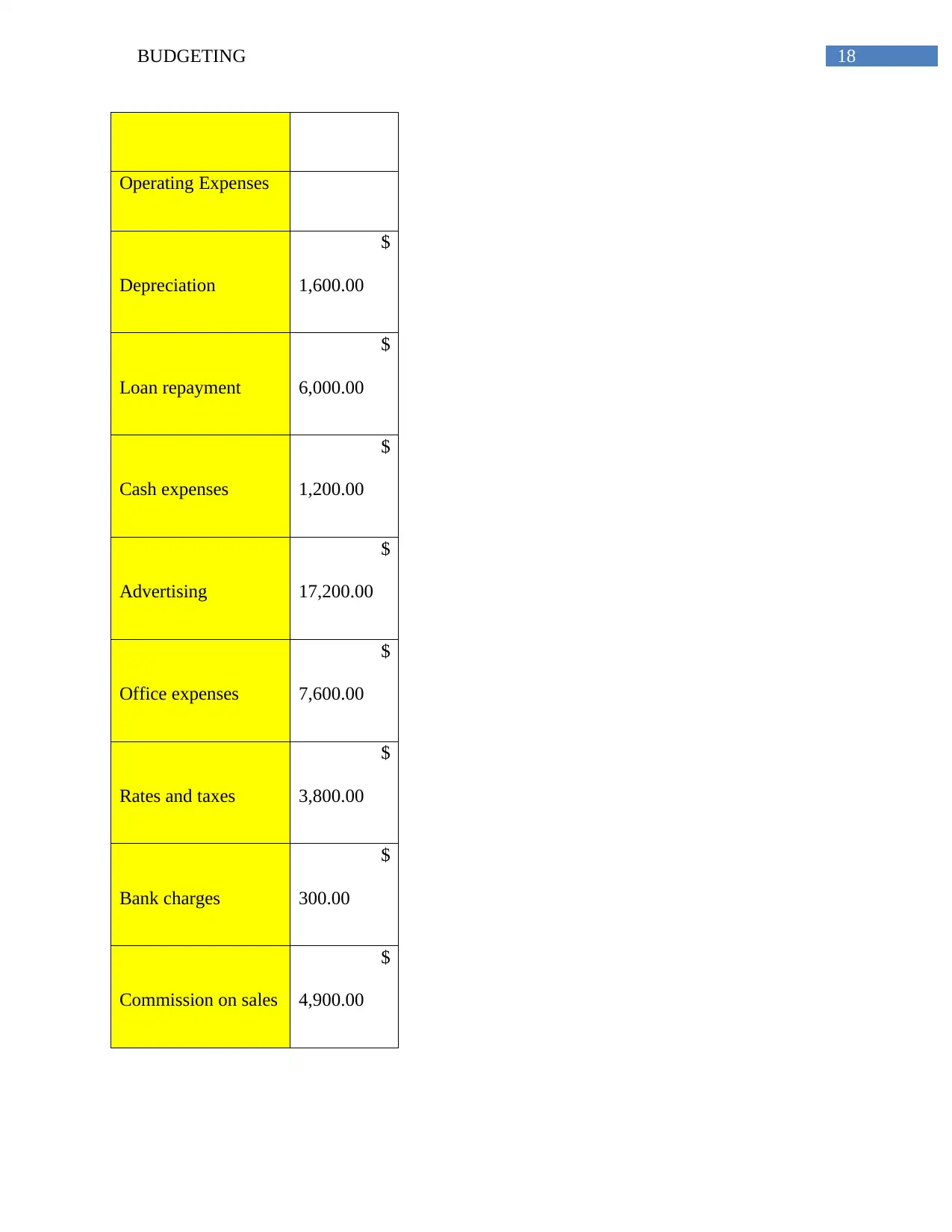

Operating Expenses

Depreciation

$

1,600.00

Loan repayment

$

6,000.00

Cash expenses

$

1,200.00

Advertising

$

17,200.00

Office expenses

$

7,600.00

Rates and taxes

$

3,800.00

Bank charges

$

300.00

Commission on sales

$

4,900.00

Operating Expenses

Depreciation

$

1,600.00

Loan repayment

$

6,000.00

Cash expenses

$

1,200.00

Advertising

$

17,200.00

Office expenses

$

7,600.00

Rates and taxes

$

3,800.00

Bank charges

$

300.00

Commission on sales

$

4,900.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19BUDGETING

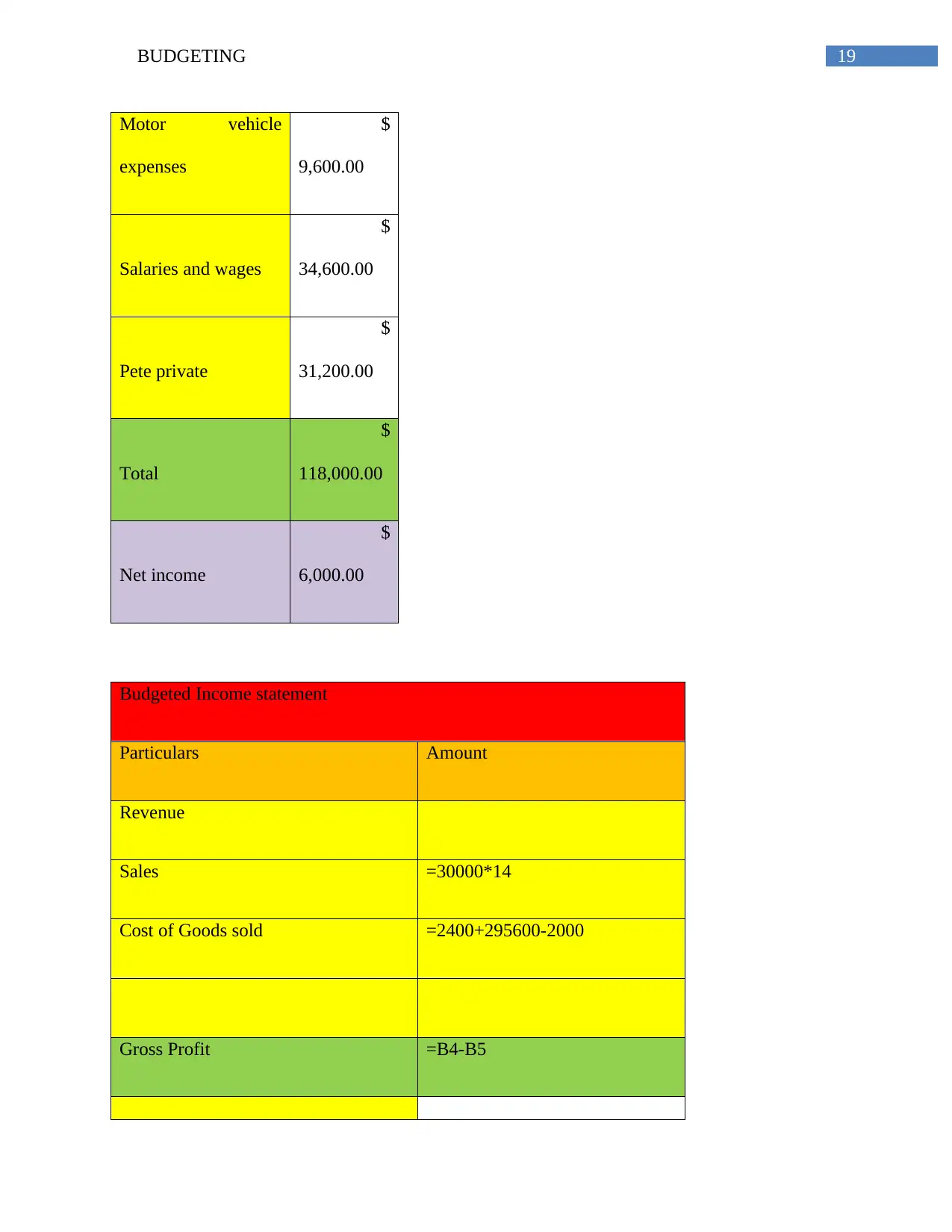

Motor vehicle

expenses

$

9,600.00

Salaries and wages

$

34,600.00

Pete private

$

31,200.00

Total

$

118,000.00

Net income

$

6,000.00

Budgeted Income statement

Particulars Amount

Revenue

Sales =30000*14

Cost of Goods sold =2400+295600-2000

Gross Profit =B4-B5

Motor vehicle

expenses

$

9,600.00

Salaries and wages

$

34,600.00

Pete private

$

31,200.00

Total

$

118,000.00

Net income

$

6,000.00

Budgeted Income statement

Particulars Amount

Revenue

Sales =30000*14

Cost of Goods sold =2400+295600-2000

Gross Profit =B4-B5

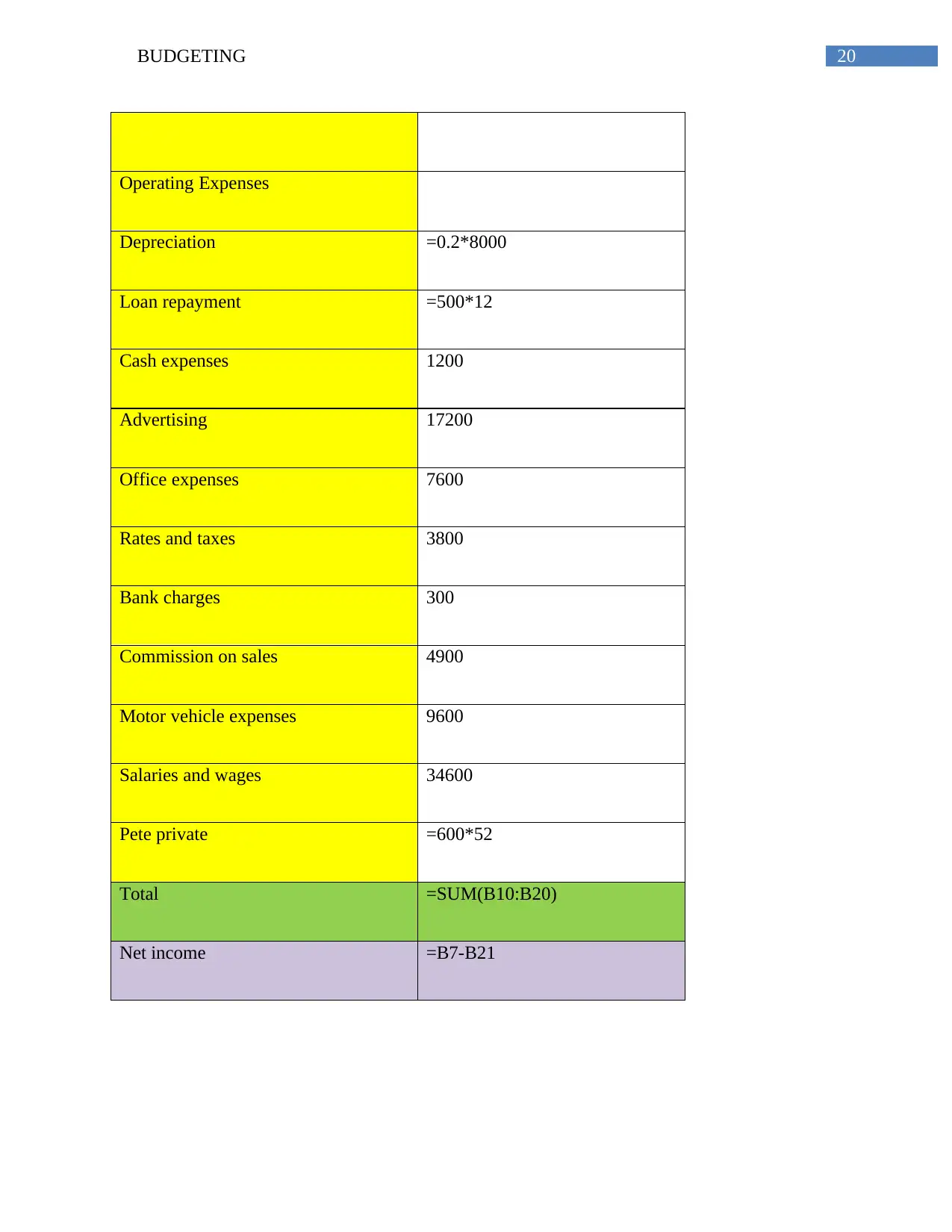

20BUDGETING

Operating Expenses

Depreciation =0.2*8000

Loan repayment =500*12

Cash expenses 1200

Advertising 17200

Office expenses 7600

Rates and taxes 3800

Bank charges 300

Commission on sales 4900

Motor vehicle expenses 9600

Salaries and wages 34600

Pete private =600*52

Total =SUM(B10:B20)

Net income =B7-B21

Operating Expenses

Depreciation =0.2*8000

Loan repayment =500*12

Cash expenses 1200

Advertising 17200

Office expenses 7600

Rates and taxes 3800

Bank charges 300

Commission on sales 4900

Motor vehicle expenses 9600

Salaries and wages 34600

Pete private =600*52

Total =SUM(B10:B20)

Net income =B7-B21

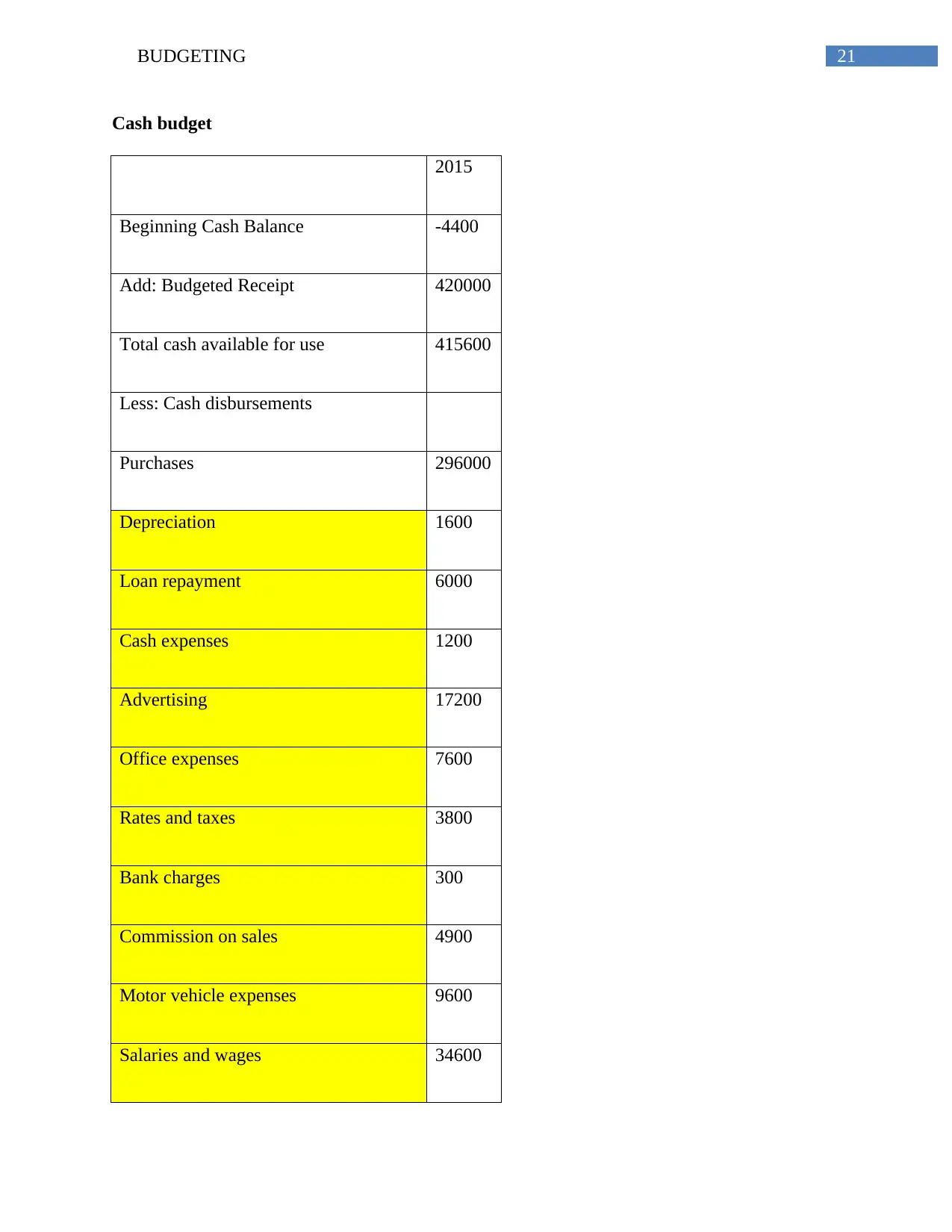

21BUDGETING

Cash budget

2015

Beginning Cash Balance -4400

Add: Budgeted Receipt 420000

Total cash available for use 415600

Less: Cash disbursements

Purchases 296000

Depreciation 1600

Loan repayment 6000

Cash expenses 1200

Advertising 17200

Office expenses 7600

Rates and taxes 3800

Bank charges 300

Commission on sales 4900

Motor vehicle expenses 9600

Salaries and wages 34600

Cash budget

2015

Beginning Cash Balance -4400

Add: Budgeted Receipt 420000

Total cash available for use 415600

Less: Cash disbursements

Purchases 296000

Depreciation 1600

Loan repayment 6000

Cash expenses 1200

Advertising 17200

Office expenses 7600

Rates and taxes 3800

Bank charges 300

Commission on sales 4900

Motor vehicle expenses 9600

Salaries and wages 34600

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

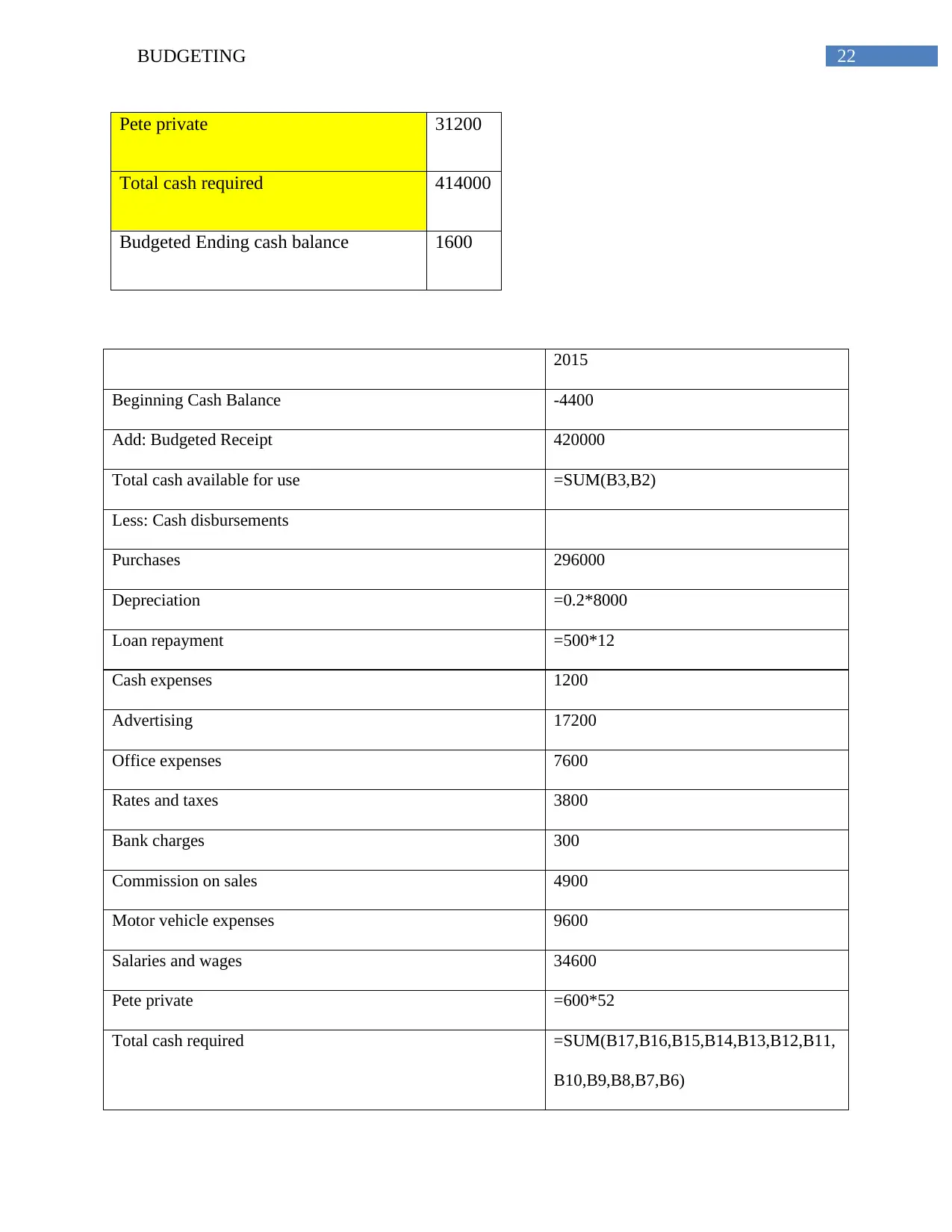

22BUDGETING

Pete private 31200

Total cash required 414000

Budgeted Ending cash balance 1600

2015

Beginning Cash Balance -4400

Add: Budgeted Receipt 420000

Total cash available for use =SUM(B3,B2)

Less: Cash disbursements

Purchases 296000

Depreciation =0.2*8000

Loan repayment =500*12

Cash expenses 1200

Advertising 17200

Office expenses 7600

Rates and taxes 3800

Bank charges 300

Commission on sales 4900

Motor vehicle expenses 9600

Salaries and wages 34600

Pete private =600*52

Total cash required =SUM(B17,B16,B15,B14,B13,B12,B11,

B10,B9,B8,B7,B6)

Pete private 31200

Total cash required 414000

Budgeted Ending cash balance 1600

2015

Beginning Cash Balance -4400

Add: Budgeted Receipt 420000

Total cash available for use =SUM(B3,B2)

Less: Cash disbursements

Purchases 296000

Depreciation =0.2*8000

Loan repayment =500*12

Cash expenses 1200

Advertising 17200

Office expenses 7600

Rates and taxes 3800

Bank charges 300

Commission on sales 4900

Motor vehicle expenses 9600

Salaries and wages 34600

Pete private =600*52

Total cash required =SUM(B17,B16,B15,B14,B13,B12,B11,

B10,B9,B8,B7,B6)

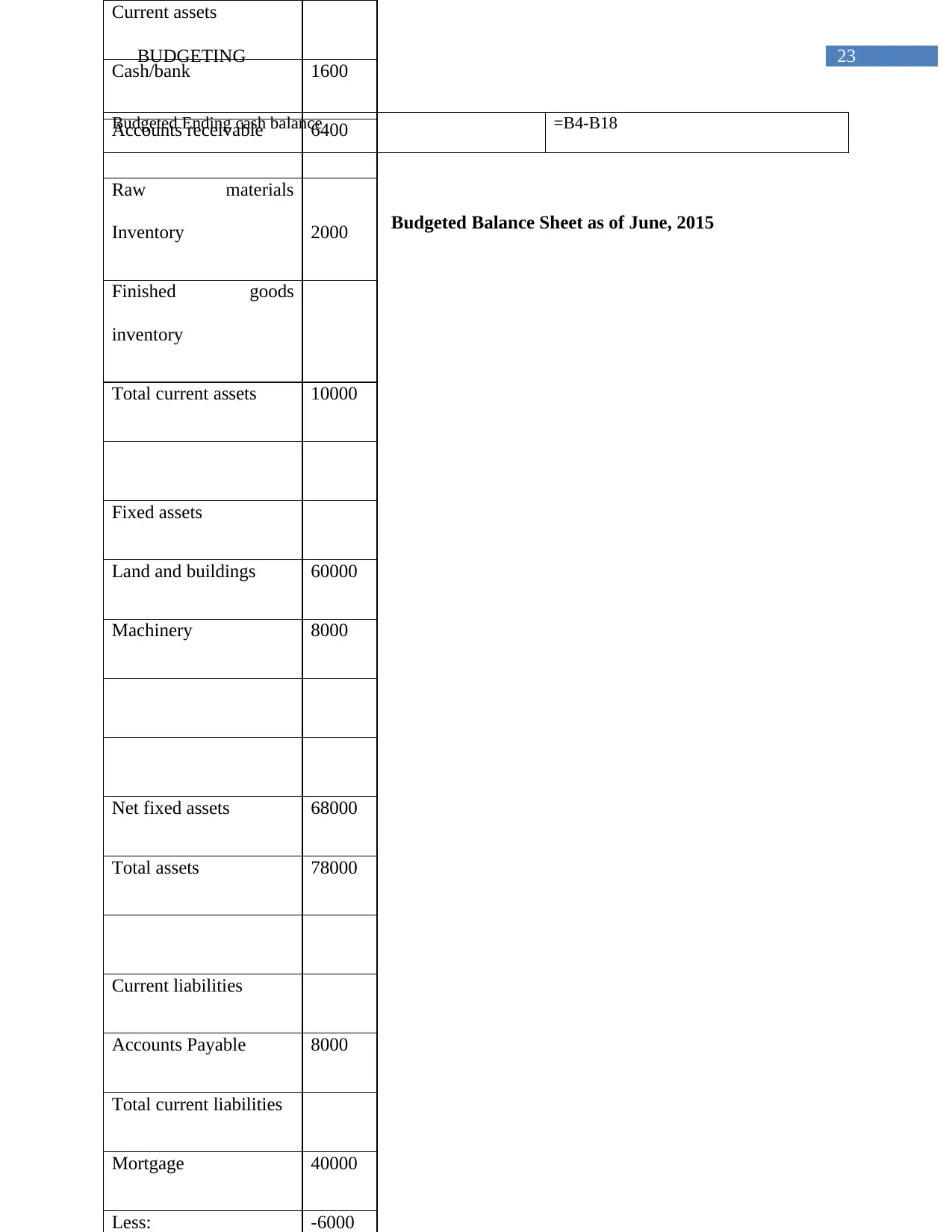

23BUDGETING

Budgeted Ending cash balance =B4-B18

Budgeted Balance Sheet as of June, 2015

Current assets

Cash/bank 1600

Accounts receivable 6400

Raw materials

Inventory 2000

Finished goods

inventory

Total current assets 10000

Fixed assets

Land and buildings 60000

Machinery 8000

Net fixed assets 68000

Total assets 78000

Current liabilities

Accounts Payable 8000

Total current liabilities

Mortgage 40000

Less: -6000

Budgeted Ending cash balance =B4-B18

Budgeted Balance Sheet as of June, 2015

Current assets

Cash/bank 1600

Accounts receivable 6400

Raw materials

Inventory 2000

Finished goods

inventory

Total current assets 10000

Fixed assets

Land and buildings 60000

Machinery 8000

Net fixed assets 68000

Total assets 78000

Current liabilities

Accounts Payable 8000

Total current liabilities

Mortgage 40000

Less: -6000

24BUDGETING

Current assets

Cash/bank 1600

Accounts receivable 6400

Raw materials Inventory 2000

Finished goods inventory

Total current assets =SUM(B4:B7)

Fixed assets

Land and buildings 60000

Machinery 8000

Net fixed assets =SUM(B11,B12,B13)

Total assets =SUM(B15,B8)

Current liabilities

Accounts Payable 8000

Current assets

Cash/bank 1600

Accounts receivable 6400

Raw materials Inventory 2000

Finished goods inventory

Total current assets =SUM(B4:B7)

Fixed assets

Land and buildings 60000

Machinery 8000

Net fixed assets =SUM(B11,B12,B13)

Total assets =SUM(B15,B8)

Current liabilities

Accounts Payable 8000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

25BUDGETING

Total current liabilities

Mortgage 40000

Less: -6000

Reserves and Surplus 6000

Shareholders’ equity 24000

Total equity and liabilities

=SUM(B19,B21,B23,B

24)

Activity 4

Answer to Question 1

Budgets can be described as an essential component of the organization which helps in

effective management of the various functions in an organization (Brigham et al. 2016).However

there exists certain advantages and disadvantages of the budgeting process.

The advantages of budgets are:

The budget forms an essential aspect of the management as they help the organization to

think about the future. The given budgeting procedure with specific guidelines for the

managers helps them to divert their attention from the different mundane activities and

concentrate on the strategic obligations of the organization.

Total current liabilities

Mortgage 40000

Less: -6000

Reserves and Surplus 6000

Shareholders’ equity 24000

Total equity and liabilities

=SUM(B19,B21,B23,B

24)

Activity 4

Answer to Question 1

Budgets can be described as an essential component of the organization which helps in

effective management of the various functions in an organization (Brigham et al. 2016).However

there exists certain advantages and disadvantages of the budgeting process.

The advantages of budgets are:

The budget forms an essential aspect of the management as they help the organization to

think about the future. The given budgeting procedure with specific guidelines for the

managers helps them to divert their attention from the different mundane activities and

concentrate on the strategic obligations of the organization.

26BUDGETING

It helps in communication and coordination. It brings together the various departments in

an organization and goes a long way in building team rapport.

The budgets also tend to act as guidance for action.

Budgets go a long way in evaluating the performance of the organization. It forms an

integral part of control and review in a firm and the actual performance may be

monitored against it.

Budgets go a long way in helping to identify considerable savings and maintain overhead

costs. The company helps the organization to maintain a control system (Titman, Keown

and Martin 2017).

The disadvantages of a budget are as follows:

Budgets are bureaucratic in nature.

They involve time and funds. Budgeting procedure can be described as a tedious one and

therefore, it requires investment from the organization.

The organization has to indulge in various efforts to form a budget. This effort could

instead be invested in some other productive matter (Barr 2018).

Experts argue that if the organization has already identified the Key Volume and Activity

then why should the organization investing in the exercise of budgeting.

The budgets are coercive and it is important for a firm to engage in good management

and motivate the workforce.

Answer to Question 2

The different kinds of budgets have been discussed as follows;

1. Plant Utilization Budget:

It helps in communication and coordination. It brings together the various departments in

an organization and goes a long way in building team rapport.

The budgets also tend to act as guidance for action.

Budgets go a long way in evaluating the performance of the organization. It forms an

integral part of control and review in a firm and the actual performance may be

monitored against it.

Budgets go a long way in helping to identify considerable savings and maintain overhead

costs. The company helps the organization to maintain a control system (Titman, Keown

and Martin 2017).

The disadvantages of a budget are as follows:

Budgets are bureaucratic in nature.

They involve time and funds. Budgeting procedure can be described as a tedious one and

therefore, it requires investment from the organization.

The organization has to indulge in various efforts to form a budget. This effort could

instead be invested in some other productive matter (Barr 2018).

Experts argue that if the organization has already identified the Key Volume and Activity

then why should the organization investing in the exercise of budgeting.

The budgets are coercive and it is important for a firm to engage in good management

and motivate the workforce.

Answer to Question 2

The different kinds of budgets have been discussed as follows;

1. Plant Utilization Budget:

27BUDGETING

The plant utilization budget is prepared with respect to the working hours, convenient

units of plant facilities and other related components of the production budget. It helps in loading

on each process, costs, cost centers, dove tails other related aspects.

2. Production Cost Budget:

A prediction costs budget is a budget which is also known as a manufacturing budget and

consists of primarily materials budget, labor budget and factory overhead budget.

3. Direct Material Budget: of the

This budget consists of the cost of the direct materials purchased for the organization.

This budget assists the purchase department in preparing a schedule of their total purchases and

helps them to fix the maximum and minimum level of inventories.

4. Capital Budgeting:

Capital Budgeting can be described as the planning and development done for the

purpose of maximizing the long term profitability of the business. It lays down a plan for the

capital outlays. They are very important as it helps an organization to make effective capital

budgeting decisions. It also has an effect on the long impacts on the company`s cost structure.

5. Zero Base Budgeting:

The zero based budgeting is a budgeting process which helps the firm to prepare a new

budget for the firm from the scratch. The managers need to justify the reason behind putting each

The plant utilization budget is prepared with respect to the working hours, convenient

units of plant facilities and other related components of the production budget. It helps in loading

on each process, costs, cost centers, dove tails other related aspects.

2. Production Cost Budget:

A prediction costs budget is a budget which is also known as a manufacturing budget and

consists of primarily materials budget, labor budget and factory overhead budget.

3. Direct Material Budget: of the

This budget consists of the cost of the direct materials purchased for the organization.

This budget assists the purchase department in preparing a schedule of their total purchases and

helps them to fix the maximum and minimum level of inventories.

4. Capital Budgeting:

Capital Budgeting can be described as the planning and development done for the

purpose of maximizing the long term profitability of the business. It lays down a plan for the

capital outlays. They are very important as it helps an organization to make effective capital

budgeting decisions. It also has an effect on the long impacts on the company`s cost structure.

5. Zero Base Budgeting:

The zero based budgeting is a budgeting process which helps the firm to prepare a new

budget for the firm from the scratch. The managers need to justify the reason behind putting each

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

28BUDGETING

cost in the appropriate section (Lasher 2013). The given budget has various advantages in the

sense that it motivates the members to form cost effective ways of task performance.

6. Performance Budget:

The performance budget has been originated in USA and is based on functions, programs

and activities. It is based on a work plan which expresses the achievement of various levels of

the organization.

7. Sales Budget:

The sales budget is a functional budget which helps to forecast the sales in an

organization. It represents the total sales along with the physical quantities as well. The primary

purpose of a sales budget is to estimate the sales and developed a plan accordingly.

8. Production Budget:

A production budget consists of the total volume of production whereby the operations

has been divided by days, weeks and months (Zietlow et al. 2018). This helps the department to

estimate the correct way of identifying the production of the goods.

8. Cash Budget:

The cash budget can be described as a critical budget whereby the organization

determines what the cash requirements of the given period are.

9. Flexible Budget:

cost in the appropriate section (Lasher 2013). The given budget has various advantages in the

sense that it motivates the members to form cost effective ways of task performance.

6. Performance Budget:

The performance budget has been originated in USA and is based on functions, programs

and activities. It is based on a work plan which expresses the achievement of various levels of

the organization.

7. Sales Budget:

The sales budget is a functional budget which helps to forecast the sales in an

organization. It represents the total sales along with the physical quantities as well. The primary

purpose of a sales budget is to estimate the sales and developed a plan accordingly.

8. Production Budget:

A production budget consists of the total volume of production whereby the operations

has been divided by days, weeks and months (Zietlow et al. 2018). This helps the department to

estimate the correct way of identifying the production of the goods.

8. Cash Budget:

The cash budget can be described as a critical budget whereby the organization

determines what the cash requirements of the given period are.

9. Flexible Budget:

29BUDGETING

The flexible budget is asked on the concept of a fixed budget whereby certain changes

are made to the fixed budget in a manner such that the organization can inculcate its costs in the

budget.

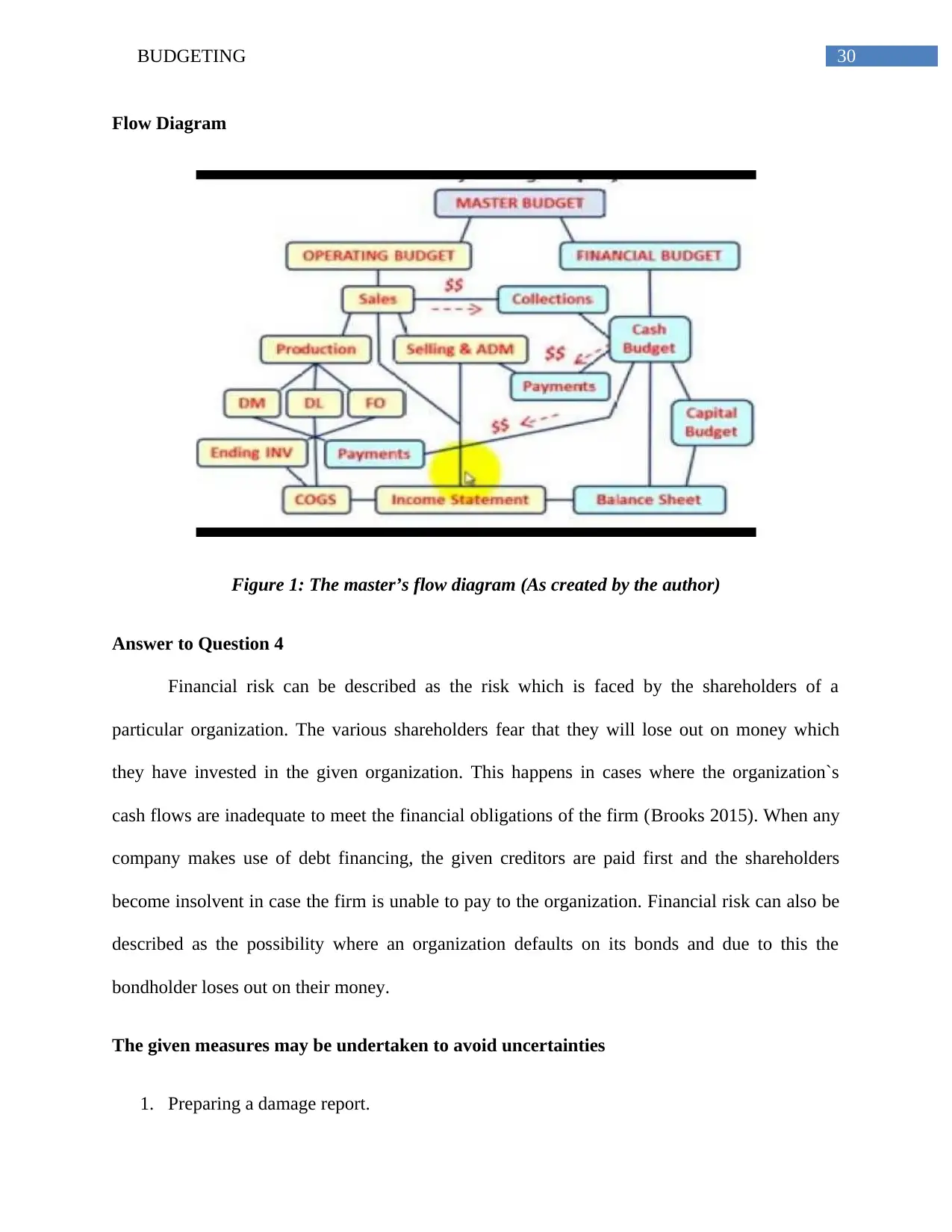

Answer to Question 3

A master budget can be described as an amalgamation of all the lower level budgets that

a company produces with respect to its various functional areas. The master budget also

comprises of the financial statements and cash forecasting. The given budget is either prepared

on a monthly basis or a quarterly basis (Saunders 2014). The primary purpose of a master budget

is to help an organization in achieving its specific goals. Various master budgets also consist of

headcount changes which are needed to be made in order to achieve the budget goals.

The budget can be described as a central planning tool which the management makes use

of in order to determine the key activities of an organization and to judge the performance in

various centers (Finkler et al. 2016). Or the formation of a master budget, the organization

should use a participative budgeting technique.

The given budgets form a part of the master budget:

Direct labor budget

Direct materials budget

Ending finished goods budget

Manufacturing overhead budget

Production budget

Sales budget

Selling and administrative expense budget

The flexible budget is asked on the concept of a fixed budget whereby certain changes

are made to the fixed budget in a manner such that the organization can inculcate its costs in the

budget.

Answer to Question 3

A master budget can be described as an amalgamation of all the lower level budgets that

a company produces with respect to its various functional areas. The master budget also

comprises of the financial statements and cash forecasting. The given budget is either prepared

on a monthly basis or a quarterly basis (Saunders 2014). The primary purpose of a master budget

is to help an organization in achieving its specific goals. Various master budgets also consist of

headcount changes which are needed to be made in order to achieve the budget goals.

The budget can be described as a central planning tool which the management makes use

of in order to determine the key activities of an organization and to judge the performance in

various centers (Finkler et al. 2016). Or the formation of a master budget, the organization

should use a participative budgeting technique.

The given budgets form a part of the master budget:

Direct labor budget

Direct materials budget

Ending finished goods budget

Manufacturing overhead budget

Production budget

Sales budget

Selling and administrative expense budget

30BUDGETING

Flow Diagram

Figure 1: The master’s flow diagram (As created by the author)

Answer to Question 4

Financial risk can be described as the risk which is faced by the shareholders of a

particular organization. The various shareholders fear that they will lose out on money which

they have invested in the given organization. This happens in cases where the organization`s

cash flows are inadequate to meet the financial obligations of the firm (Brooks 2015). When any

company makes use of debt financing, the given creditors are paid first and the shareholders

become insolvent in case the firm is unable to pay to the organization. Financial risk can also be

described as the possibility where an organization defaults on its bonds and due to this the

bondholder loses out on their money.

The given measures may be undertaken to avoid uncertainties

1. Preparing a damage report.

Flow Diagram

Figure 1: The master’s flow diagram (As created by the author)

Answer to Question 4

Financial risk can be described as the risk which is faced by the shareholders of a

particular organization. The various shareholders fear that they will lose out on money which

they have invested in the given organization. This happens in cases where the organization`s

cash flows are inadequate to meet the financial obligations of the firm (Brooks 2015). When any

company makes use of debt financing, the given creditors are paid first and the shareholders

become insolvent in case the firm is unable to pay to the organization. Financial risk can also be

described as the possibility where an organization defaults on its bonds and due to this the

bondholder loses out on their money.

The given measures may be undertaken to avoid uncertainties

1. Preparing a damage report.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

31BUDGETING

This report may help the firm to understand the how a particular happening of an event

may cause problems to an organization and what would be the degree of impact on the firm.

2. Avoiding the emotions

A business is a rational organization and for this reason, it is very important for the firm

to realize that they cannot make business decisions based on emotions.

3. Focusing on long term objectives

The long term objectives of an organization take it towards its futures and this makes it

very important for the firm to focus on the long term well being of the organization in order to

meet its goals.

4. Clarity in communication of challenge

The communication of the challenge forms an essential aspect of the organization

5. Collaboration is the key

It is very important for a firm to collaborate in the times of the need.

This report may help the firm to understand the how a particular happening of an event

may cause problems to an organization and what would be the degree of impact on the firm.

2. Avoiding the emotions

A business is a rational organization and for this reason, it is very important for the firm

to realize that they cannot make business decisions based on emotions.

3. Focusing on long term objectives

The long term objectives of an organization take it towards its futures and this makes it

very important for the firm to focus on the long term well being of the organization in order to

meet its goals.

4. Clarity in communication of challenge

The communication of the challenge forms an essential aspect of the organization

5. Collaboration is the key

It is very important for a firm to collaborate in the times of the need.

32BUDGETING

References

Barr, M.J., 2018. Budgets and financial management in higher education. John Wiley & Sons.

Brigham, E.F., Ehrhardt, M.C., Nason, R.R. and Gessaroli, J., 2016. Financial Managment:

Theory And Practice, Canadian Edition. Nelson Education.

Brooks, R., 2015. Financial management: core concepts. Pearson.

Finkler, S.A., Smith, D.L., Calabrese, T.D. and Purtell, R.M., 2016. Financial management for

public, health, and not-for-profit organizations. CQ Press.

Lasher, W.R., 2013. Practical financial management. Nelson Education.

Saunders, A., 2014. Financial markets and institutions. McGraw-Hill Higher Education.

Titman, S., Keown, A.J. and Martin, J.D., 2017. Financial management: Principles and

applications. Pearson.

Zietlow, J., Hankin, J.A., Seidner, A. and O'Brien, T., 2018. Financial management for nonprofit

organizations: Policies and practices. John Wiley & Sons.

References

Barr, M.J., 2018. Budgets and financial management in higher education. John Wiley & Sons.

Brigham, E.F., Ehrhardt, M.C., Nason, R.R. and Gessaroli, J., 2016. Financial Managment:

Theory And Practice, Canadian Edition. Nelson Education.

Brooks, R., 2015. Financial management: core concepts. Pearson.

Finkler, S.A., Smith, D.L., Calabrese, T.D. and Purtell, R.M., 2016. Financial management for

public, health, and not-for-profit organizations. CQ Press.

Lasher, W.R., 2013. Practical financial management. Nelson Education.

Saunders, A., 2014. Financial markets and institutions. McGraw-Hill Higher Education.

Titman, S., Keown, A.J. and Martin, J.D., 2017. Financial management: Principles and

applications. Pearson.

Zietlow, J., Hankin, J.A., Seidner, A. and O'Brien, T., 2018. Financial management for nonprofit

organizations: Policies and practices. John Wiley & Sons.

1 out of 33

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.