Desklib: SEO Title, Meta Title, Meta Description, Slug, Summary, Course Code, Course Name, College/University

VerifiedAdded on 2023/06/17

|16

|3684

|100

AI Summary

This article provides SEO suggestions for Desklib, an online library for study material. It includes a title, meta title, meta description, slug, summary, course code, course name, and college/university. The article also includes sample output in JSON format.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Student Number: (enter on the line below)

Student Name: (enter on the line below)

HI5001

ACCOUNTING FOR BUSINESS DECISIONS

TRIMESTER 2, 2021

Assessment Weight: 50 total marks

Instructions:

All questions must be answered in this paper.

Completed answers must be submitted to Blackboard by the published due date

and time.

Please strictly follow the submission instructions posted in the announcement

Purpose:

This assessment consists of six (6) questions and is designed to assess your level of

knowledge of the key topics covered in this unit

Student Name: (enter on the line below)

HI5001

ACCOUNTING FOR BUSINESS DECISIONS

TRIMESTER 2, 2021

Assessment Weight: 50 total marks

Instructions:

All questions must be answered in this paper.

Completed answers must be submitted to Blackboard by the published due date

and time.

Please strictly follow the submission instructions posted in the announcement

Purpose:

This assessment consists of six (6) questions and is designed to assess your level of

knowledge of the key topics covered in this unit

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

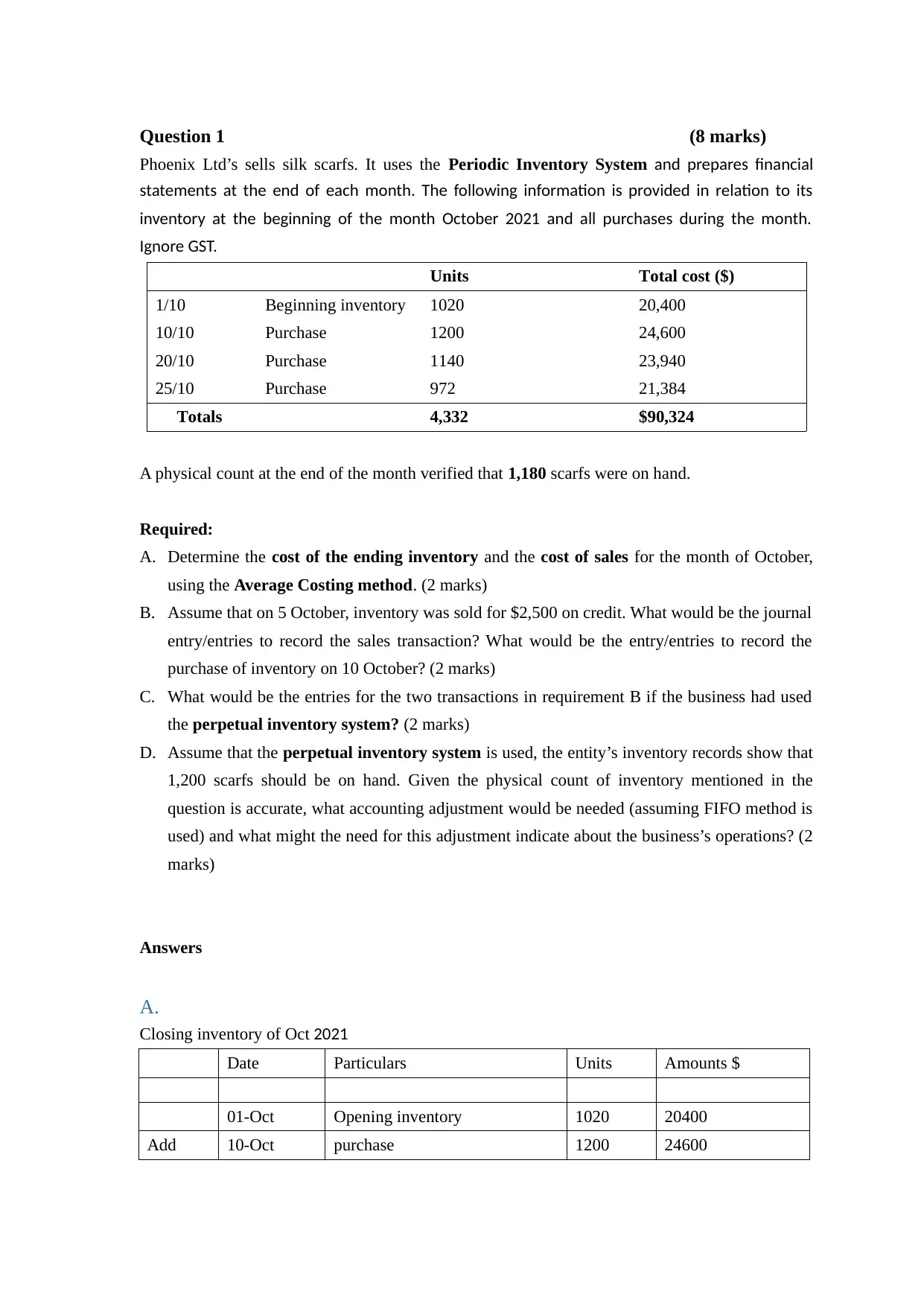

Question 1 (8 marks)

Phoenix Ltd’s sells silk scarfs. It uses the Periodic Inventory System and prepares financial

statements at the end of each month. The following information is provided in relation to its

inventory at the beginning of the month October 2021 and all purchases during the month.

Ignore GST.

Units Total cost ($)

1/10 Beginning inventory 1020 20,400

10/10 Purchase 1200 24,600

20/10 Purchase 1140 23,940

25/10 Purchase 972 21,384

Totals 4,332 $90,324

A physical count at the end of the month verified that 1,180 scarfs were on hand.

Required:

A. Determine the cost of the ending inventory and the cost of sales for the month of October,

using the Average Costing method. (2 marks)

B. Assume that on 5 October, inventory was sold for $2,500 on credit. What would be the journal

entry/entries to record the sales transaction? What would be the entry/entries to record the

purchase of inventory on 10 October? (2 marks)

C. What would be the entries for the two transactions in requirement B if the business had used

the perpetual inventory system? (2 marks)

D. Assume that the perpetual inventory system is used, the entity’s inventory records show that

1,200 scarfs should be on hand. Given the physical count of inventory mentioned in the

question is accurate, what accounting adjustment would be needed (assuming FIFO method is

used) and what might the need for this adjustment indicate about the business’s operations? (2

marks)

Answers

A.

Closing inventory of Oct 2021

Date Particulars Units Amounts $

01-Oct Opening inventory 1020 20400

Add 10-Oct purchase 1200 24600

Phoenix Ltd’s sells silk scarfs. It uses the Periodic Inventory System and prepares financial

statements at the end of each month. The following information is provided in relation to its

inventory at the beginning of the month October 2021 and all purchases during the month.

Ignore GST.

Units Total cost ($)

1/10 Beginning inventory 1020 20,400

10/10 Purchase 1200 24,600

20/10 Purchase 1140 23,940

25/10 Purchase 972 21,384

Totals 4,332 $90,324

A physical count at the end of the month verified that 1,180 scarfs were on hand.

Required:

A. Determine the cost of the ending inventory and the cost of sales for the month of October,

using the Average Costing method. (2 marks)

B. Assume that on 5 October, inventory was sold for $2,500 on credit. What would be the journal

entry/entries to record the sales transaction? What would be the entry/entries to record the

purchase of inventory on 10 October? (2 marks)

C. What would be the entries for the two transactions in requirement B if the business had used

the perpetual inventory system? (2 marks)

D. Assume that the perpetual inventory system is used, the entity’s inventory records show that

1,200 scarfs should be on hand. Given the physical count of inventory mentioned in the

question is accurate, what accounting adjustment would be needed (assuming FIFO method is

used) and what might the need for this adjustment indicate about the business’s operations? (2

marks)

Answers

A.

Closing inventory of Oct 2021

Date Particulars Units Amounts $

01-Oct Opening inventory 1020 20400

Add 10-Oct purchase 1200 24600

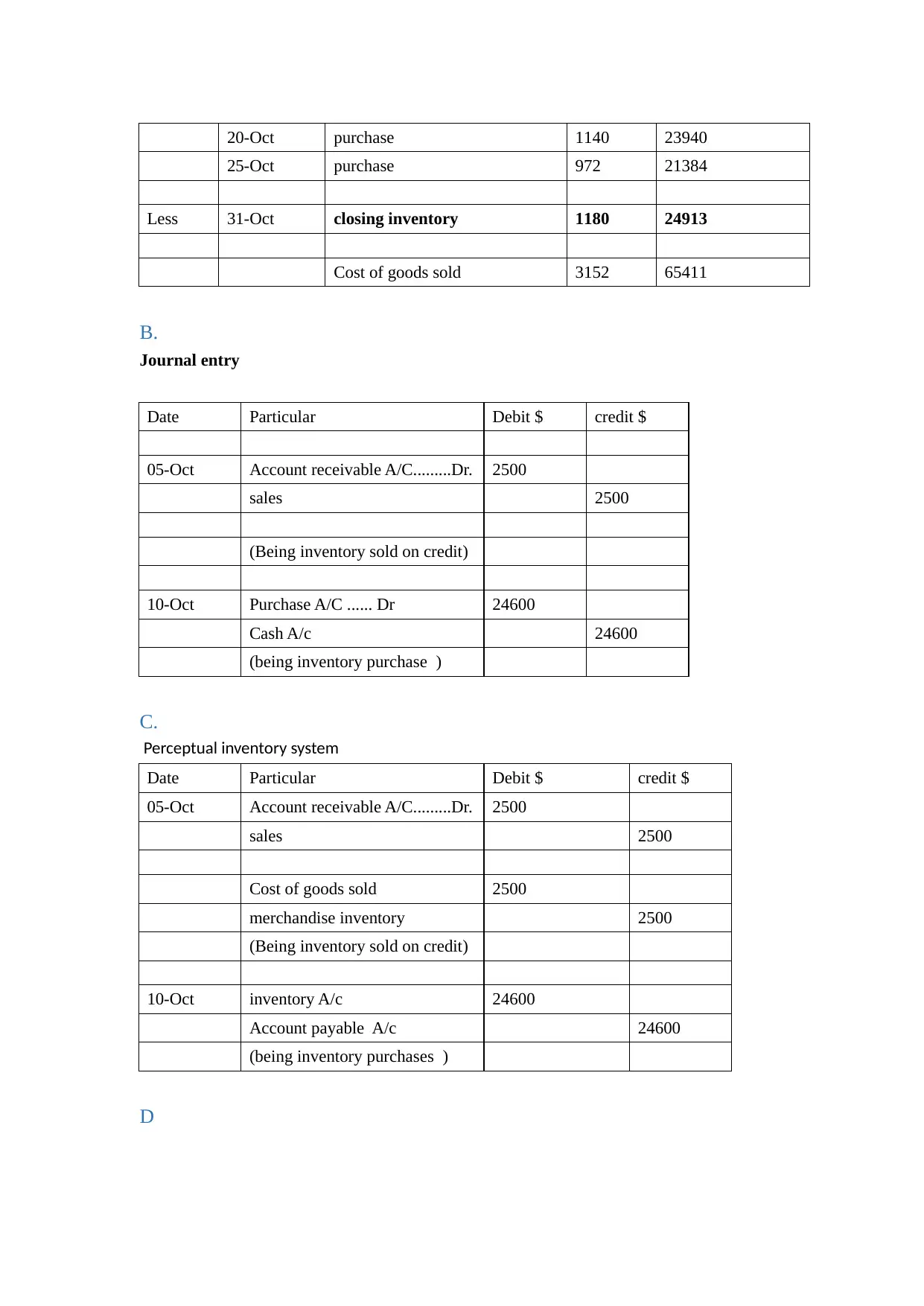

20-Oct purchase 1140 23940

25-Oct purchase 972 21384

Less 31-Oct closing inventory 1180 24913

Cost of goods sold 3152 65411

B.

Journal entry

Date Particular Debit $ credit $

05-Oct Account receivable A/C.........Dr. 2500

sales 2500

(Being inventory sold on credit)

10-Oct Purchase A/C ...... Dr 24600

Cash A/c 24600

(being inventory purchase )

C.

Perceptual inventory system

Date Particular Debit $ credit $

05-Oct Account receivable A/C.........Dr. 2500

sales 2500

Cost of goods sold 2500

merchandise inventory 2500

(Being inventory sold on credit)

10-Oct inventory A/c 24600

Account payable A/c 24600

(being inventory purchases )

D

25-Oct purchase 972 21384

Less 31-Oct closing inventory 1180 24913

Cost of goods sold 3152 65411

B.

Journal entry

Date Particular Debit $ credit $

05-Oct Account receivable A/C.........Dr. 2500

sales 2500

(Being inventory sold on credit)

10-Oct Purchase A/C ...... Dr 24600

Cash A/c 24600

(being inventory purchase )

C.

Perceptual inventory system

Date Particular Debit $ credit $

05-Oct Account receivable A/C.........Dr. 2500

sales 2500

Cost of goods sold 2500

merchandise inventory 2500

(Being inventory sold on credit)

10-Oct inventory A/c 24600

Account payable A/c 24600

(being inventory purchases )

D

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

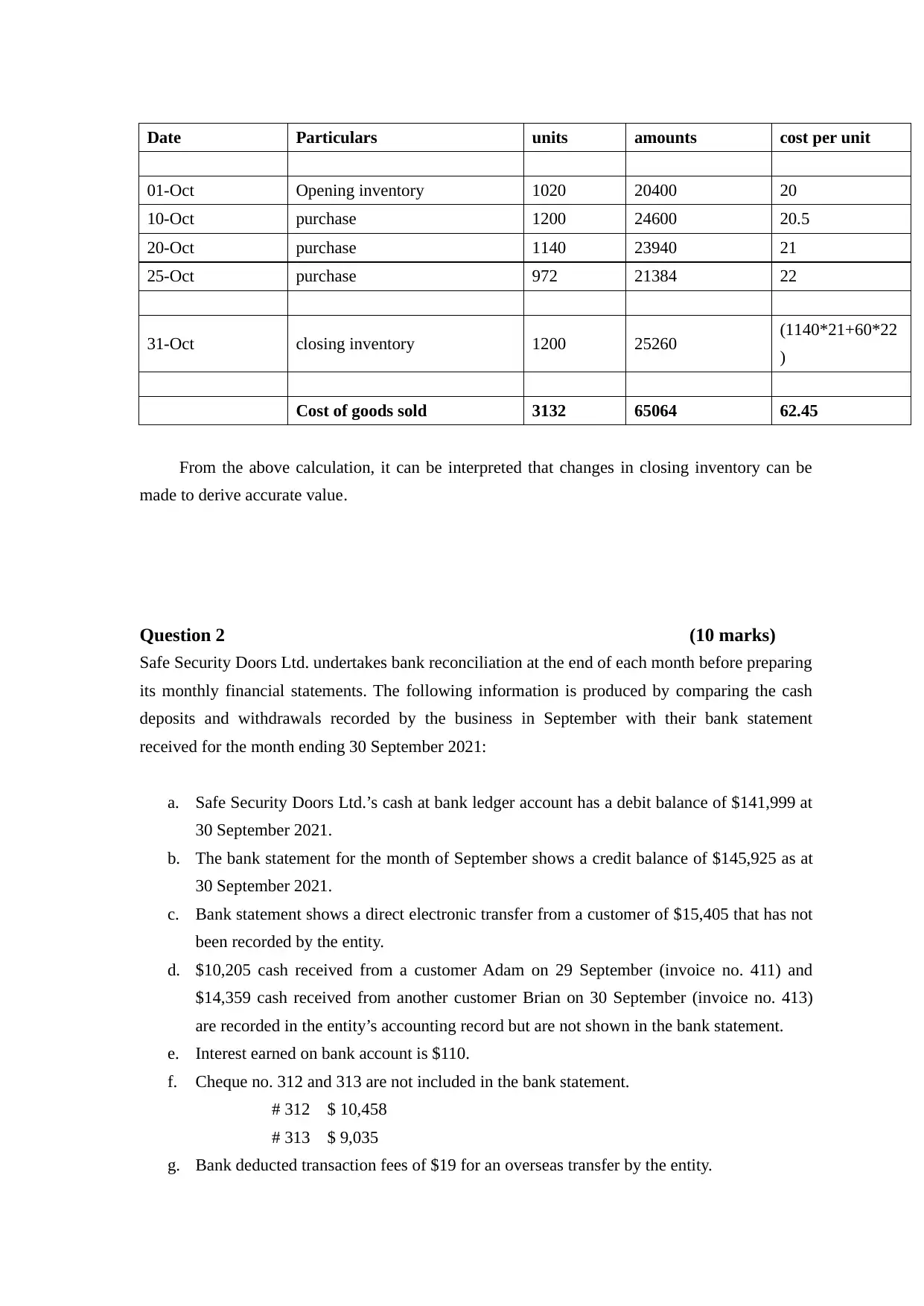

Date Particulars units amounts cost per unit

01-Oct Opening inventory 1020 20400 20

10-Oct purchase 1200 24600 20.5

20-Oct purchase 1140 23940 21

25-Oct purchase 972 21384 22

31-Oct closing inventory 1200 25260 (1140*21+60*22

)

Cost of goods sold 3132 65064 62.45

From the above calculation, it can be interpreted that changes in closing inventory can be

made to derive accurate value.

Question 2 (10 marks)

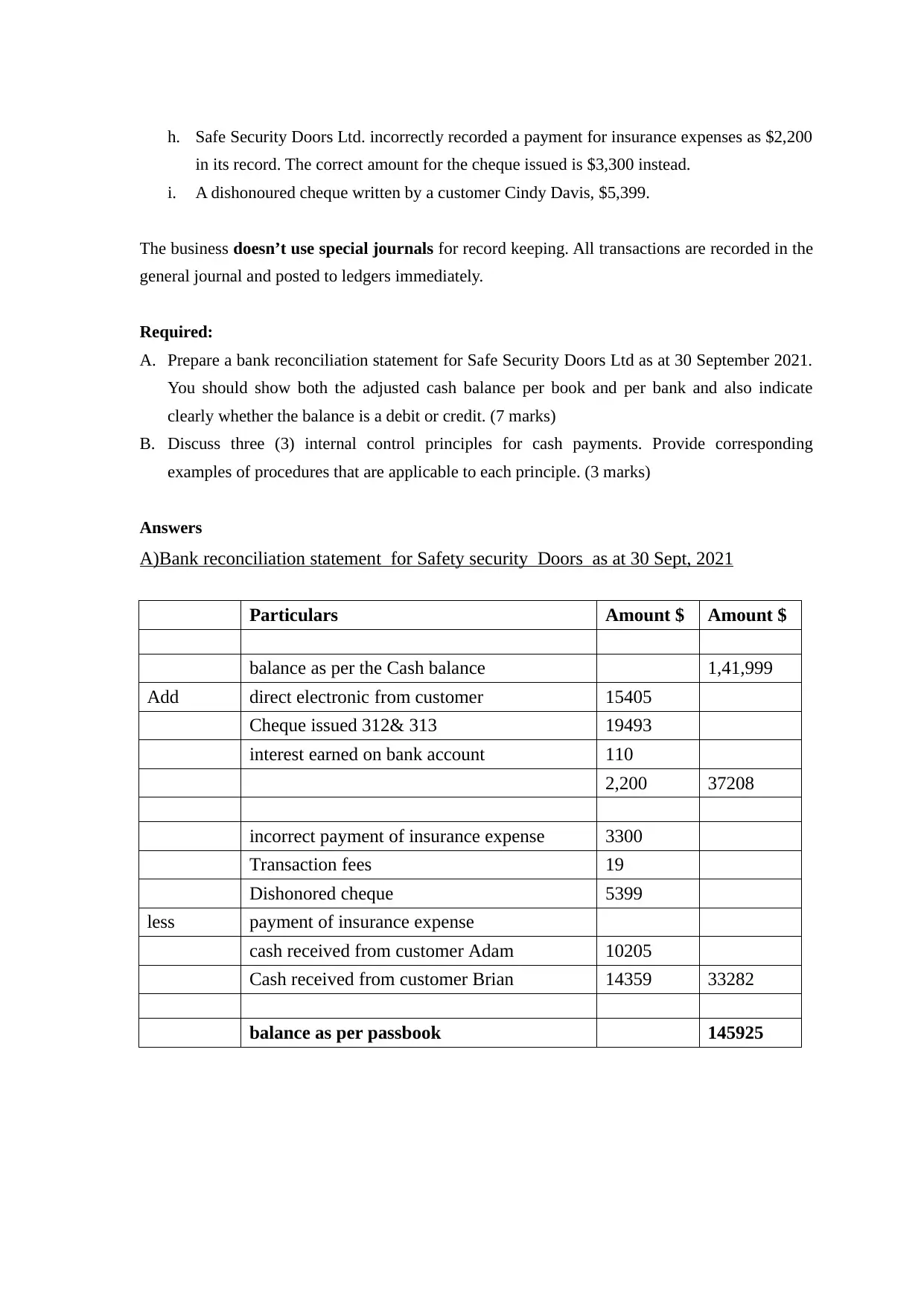

Safe Security Doors Ltd. undertakes bank reconciliation at the end of each month before preparing

its monthly financial statements. The following information is produced by comparing the cash

deposits and withdrawals recorded by the business in September with their bank statement

received for the month ending 30 September 2021:

a. Safe Security Doors Ltd.’s cash at bank ledger account has a debit balance of $141,999 at

30 September 2021.

b. The bank statement for the month of September shows a credit balance of $145,925 as at

30 September 2021.

c. Bank statement shows a direct electronic transfer from a customer of $15,405 that has not

been recorded by the entity.

d. $10,205 cash received from a customer Adam on 29 September (invoice no. 411) and

$14,359 cash received from another customer Brian on 30 September (invoice no. 413)

are recorded in the entity’s accounting record but are not shown in the bank statement.

e. Interest earned on bank account is $110.

f. Cheque no. 312 and 313 are not included in the bank statement.

# 312 $ 10,458

# 313 $ 9,035

g. Bank deducted transaction fees of $19 for an overseas transfer by the entity.

01-Oct Opening inventory 1020 20400 20

10-Oct purchase 1200 24600 20.5

20-Oct purchase 1140 23940 21

25-Oct purchase 972 21384 22

31-Oct closing inventory 1200 25260 (1140*21+60*22

)

Cost of goods sold 3132 65064 62.45

From the above calculation, it can be interpreted that changes in closing inventory can be

made to derive accurate value.

Question 2 (10 marks)

Safe Security Doors Ltd. undertakes bank reconciliation at the end of each month before preparing

its monthly financial statements. The following information is produced by comparing the cash

deposits and withdrawals recorded by the business in September with their bank statement

received for the month ending 30 September 2021:

a. Safe Security Doors Ltd.’s cash at bank ledger account has a debit balance of $141,999 at

30 September 2021.

b. The bank statement for the month of September shows a credit balance of $145,925 as at

30 September 2021.

c. Bank statement shows a direct electronic transfer from a customer of $15,405 that has not

been recorded by the entity.

d. $10,205 cash received from a customer Adam on 29 September (invoice no. 411) and

$14,359 cash received from another customer Brian on 30 September (invoice no. 413)

are recorded in the entity’s accounting record but are not shown in the bank statement.

e. Interest earned on bank account is $110.

f. Cheque no. 312 and 313 are not included in the bank statement.

# 312 $ 10,458

# 313 $ 9,035

g. Bank deducted transaction fees of $19 for an overseas transfer by the entity.

h. Safe Security Doors Ltd. incorrectly recorded a payment for insurance expenses as $2,200

in its record. The correct amount for the cheque issued is $3,300 instead.

i. A dishonoured cheque written by a customer Cindy Davis, $5,399.

The business doesn’t use special journals for record keeping. All transactions are recorded in the

general journal and posted to ledgers immediately.

Required:

A. Prepare a bank reconciliation statement for Safe Security Doors Ltd as at 30 September 2021.

You should show both the adjusted cash balance per book and per bank and also indicate

clearly whether the balance is a debit or credit. (7 marks)

B. Discuss three (3) internal control principles for cash payments. Provide corresponding

examples of procedures that are applicable to each principle. (3 marks)

Answers

A)Bank reconciliation statement for Safety security Doors as at 30 Sept, 2021

Particulars Amount $ Amount $

balance as per the Cash balance 1,41,999

Add direct electronic from customer 15405

Cheque issued 312& 313 19493

interest earned on bank account 110

2,200 37208

incorrect payment of insurance expense 3300

Transaction fees 19

Dishonored cheque 5399

less payment of insurance expense

cash received from customer Adam 10205

Cash received from customer Brian 14359 33282

balance as per passbook 145925

in its record. The correct amount for the cheque issued is $3,300 instead.

i. A dishonoured cheque written by a customer Cindy Davis, $5,399.

The business doesn’t use special journals for record keeping. All transactions are recorded in the

general journal and posted to ledgers immediately.

Required:

A. Prepare a bank reconciliation statement for Safe Security Doors Ltd as at 30 September 2021.

You should show both the adjusted cash balance per book and per bank and also indicate

clearly whether the balance is a debit or credit. (7 marks)

B. Discuss three (3) internal control principles for cash payments. Provide corresponding

examples of procedures that are applicable to each principle. (3 marks)

Answers

A)Bank reconciliation statement for Safety security Doors as at 30 Sept, 2021

Particulars Amount $ Amount $

balance as per the Cash balance 1,41,999

Add direct electronic from customer 15405

Cheque issued 312& 313 19493

interest earned on bank account 110

2,200 37208

incorrect payment of insurance expense 3300

Transaction fees 19

Dishonored cheque 5399

less payment of insurance expense

cash received from customer Adam 10205

Cash received from customer Brian 14359 33282

balance as per passbook 145925

B)

In order to establish proper control in internal processes so that cash payments can be

conducted effectively. This basically includes control environment, risk assessment,

control activities , sharing information and communication and communication. To get

proper cash payment system, having physical audits, standardized documentation,

period reconciliation can provide assistance in getting appropriate conducting regarding

cash payments.

One of the basic activity that can be conducted in order to have proper cash

disbursement includes significant establishment of proper segregation of duties among

employees. This can be done by assessing the possessed skills within employees so that

corrective data can be achieved. It will allow payment department to allocate, utilize, etc

availability cash. In addition to this, significant checking of employees background in turn

proper trustworthiness and internal control system environment can be effectively.

Sharing accurate information within finance department regarding payment activities so

that re investigation of optimum utilization of cash can be ensured.

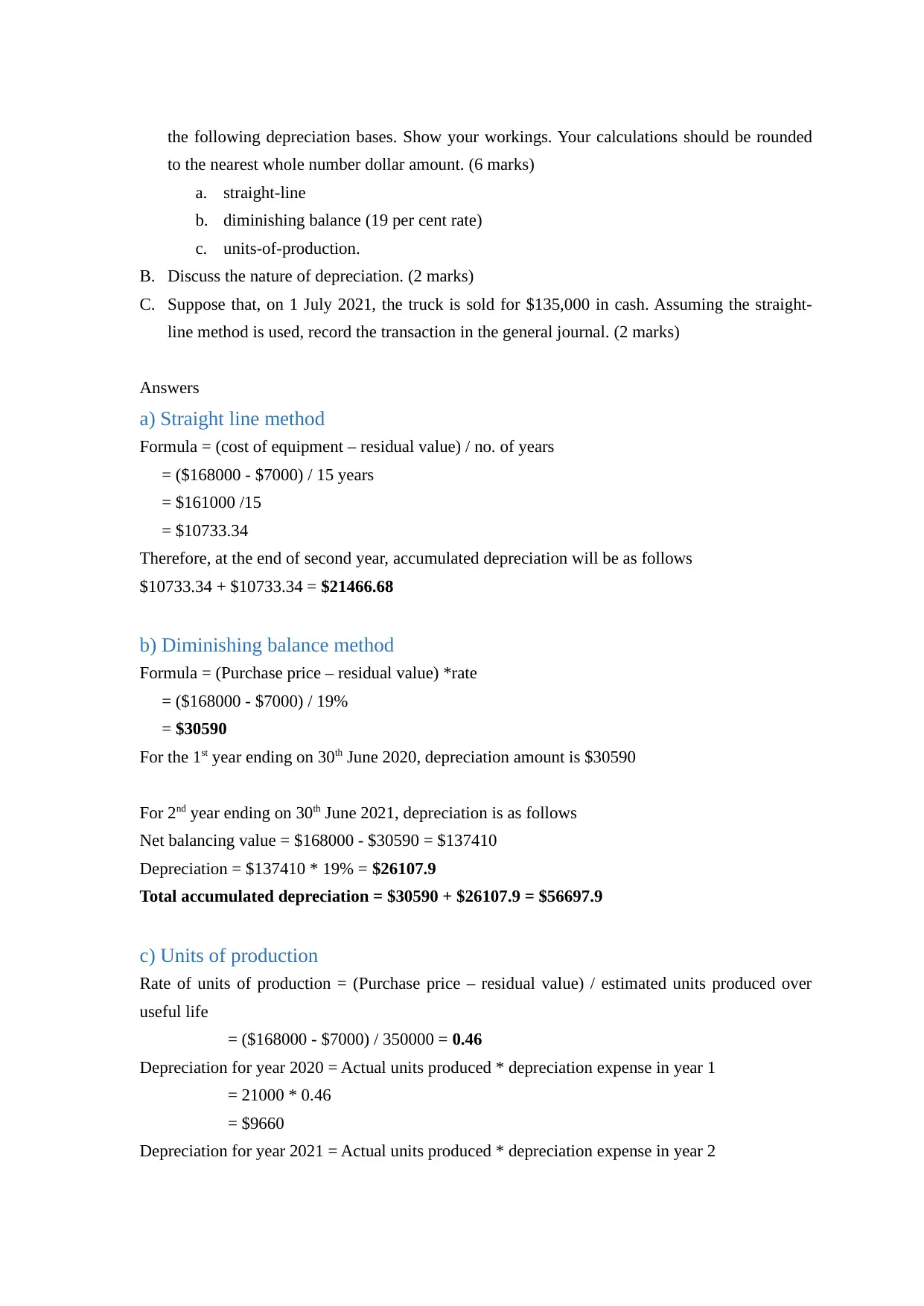

Question 3 (10 marks)

AU Removals’ financial year ends on 30 June each year. On 1 July 2019, AU Removals

purchased a truck for $168,000. You are the accountant of the business and you have estimated

that the truck is to last 15 years and to have $7,000 residual value at that point. As per the

business plan, the truck can be used to drive 350,000 kilometres over the 15 years, with per-year

projections of 21,000 km, 28,000 km, 25,200 km, respectively over the first three years.

Required:

A. Calculate the accumulated depreciation balance at the end of the second year using each of

In order to establish proper control in internal processes so that cash payments can be

conducted effectively. This basically includes control environment, risk assessment,

control activities , sharing information and communication and communication. To get

proper cash payment system, having physical audits, standardized documentation,

period reconciliation can provide assistance in getting appropriate conducting regarding

cash payments.

One of the basic activity that can be conducted in order to have proper cash

disbursement includes significant establishment of proper segregation of duties among

employees. This can be done by assessing the possessed skills within employees so that

corrective data can be achieved. It will allow payment department to allocate, utilize, etc

availability cash. In addition to this, significant checking of employees background in turn

proper trustworthiness and internal control system environment can be effectively.

Sharing accurate information within finance department regarding payment activities so

that re investigation of optimum utilization of cash can be ensured.

Question 3 (10 marks)

AU Removals’ financial year ends on 30 June each year. On 1 July 2019, AU Removals

purchased a truck for $168,000. You are the accountant of the business and you have estimated

that the truck is to last 15 years and to have $7,000 residual value at that point. As per the

business plan, the truck can be used to drive 350,000 kilometres over the 15 years, with per-year

projections of 21,000 km, 28,000 km, 25,200 km, respectively over the first three years.

Required:

A. Calculate the accumulated depreciation balance at the end of the second year using each of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the following depreciation bases. Show your workings. Your calculations should be rounded

to the nearest whole number dollar amount. (6 marks)

a. straight-line

b. diminishing balance (19 per cent rate)

c. units-of-production.

B. Discuss the nature of depreciation. (2 marks)

C. Suppose that, on 1 July 2021, the truck is sold for $135,000 in cash. Assuming the straight-

line method is used, record the transaction in the general journal. (2 marks)

Answers

a) Straight line method

Formula = (cost of equipment – residual value) / no. of years

= ($168000 - $7000) / 15 years

= $161000 /15

= $10733.34

Therefore, at the end of second year, accumulated depreciation will be as follows

$10733.34 + $10733.34 = $21466.68

b) Diminishing balance method

Formula = (Purchase price – residual value) *rate

= ($168000 - $7000) / 19%

= $30590

For the 1st year ending on 30th June 2020, depreciation amount is $30590

For 2nd year ending on 30th June 2021, depreciation is as follows

Net balancing value = $168000 - $30590 = $137410

Depreciation = $137410 * 19% = $26107.9

Total accumulated depreciation = $30590 + $26107.9 = $56697.9

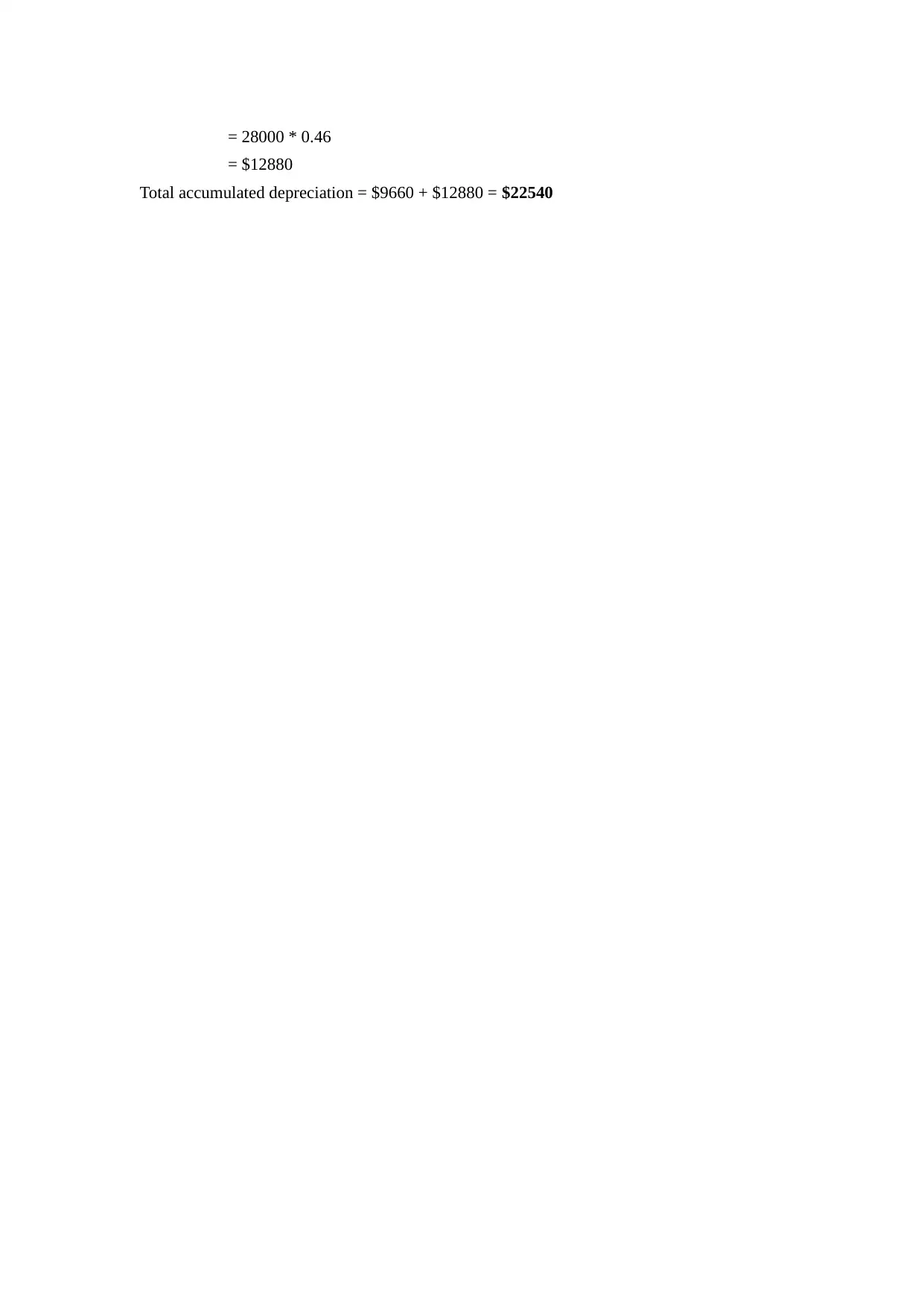

c) Units of production

Rate of units of production = (Purchase price – residual value) / estimated units produced over

useful life

= ($168000 - $7000) / 350000 = 0.46

Depreciation for year 2020 = Actual units produced * depreciation expense in year 1

= 21000 * 0.46

= $9660

Depreciation for year 2021 = Actual units produced * depreciation expense in year 2

to the nearest whole number dollar amount. (6 marks)

a. straight-line

b. diminishing balance (19 per cent rate)

c. units-of-production.

B. Discuss the nature of depreciation. (2 marks)

C. Suppose that, on 1 July 2021, the truck is sold for $135,000 in cash. Assuming the straight-

line method is used, record the transaction in the general journal. (2 marks)

Answers

a) Straight line method

Formula = (cost of equipment – residual value) / no. of years

= ($168000 - $7000) / 15 years

= $161000 /15

= $10733.34

Therefore, at the end of second year, accumulated depreciation will be as follows

$10733.34 + $10733.34 = $21466.68

b) Diminishing balance method

Formula = (Purchase price – residual value) *rate

= ($168000 - $7000) / 19%

= $30590

For the 1st year ending on 30th June 2020, depreciation amount is $30590

For 2nd year ending on 30th June 2021, depreciation is as follows

Net balancing value = $168000 - $30590 = $137410

Depreciation = $137410 * 19% = $26107.9

Total accumulated depreciation = $30590 + $26107.9 = $56697.9

c) Units of production

Rate of units of production = (Purchase price – residual value) / estimated units produced over

useful life

= ($168000 - $7000) / 350000 = 0.46

Depreciation for year 2020 = Actual units produced * depreciation expense in year 1

= 21000 * 0.46

= $9660

Depreciation for year 2021 = Actual units produced * depreciation expense in year 2

= 28000 * 0.46

= $12880

Total accumulated depreciation = $9660 + $12880 = $22540

= $12880

Total accumulated depreciation = $9660 + $12880 = $22540

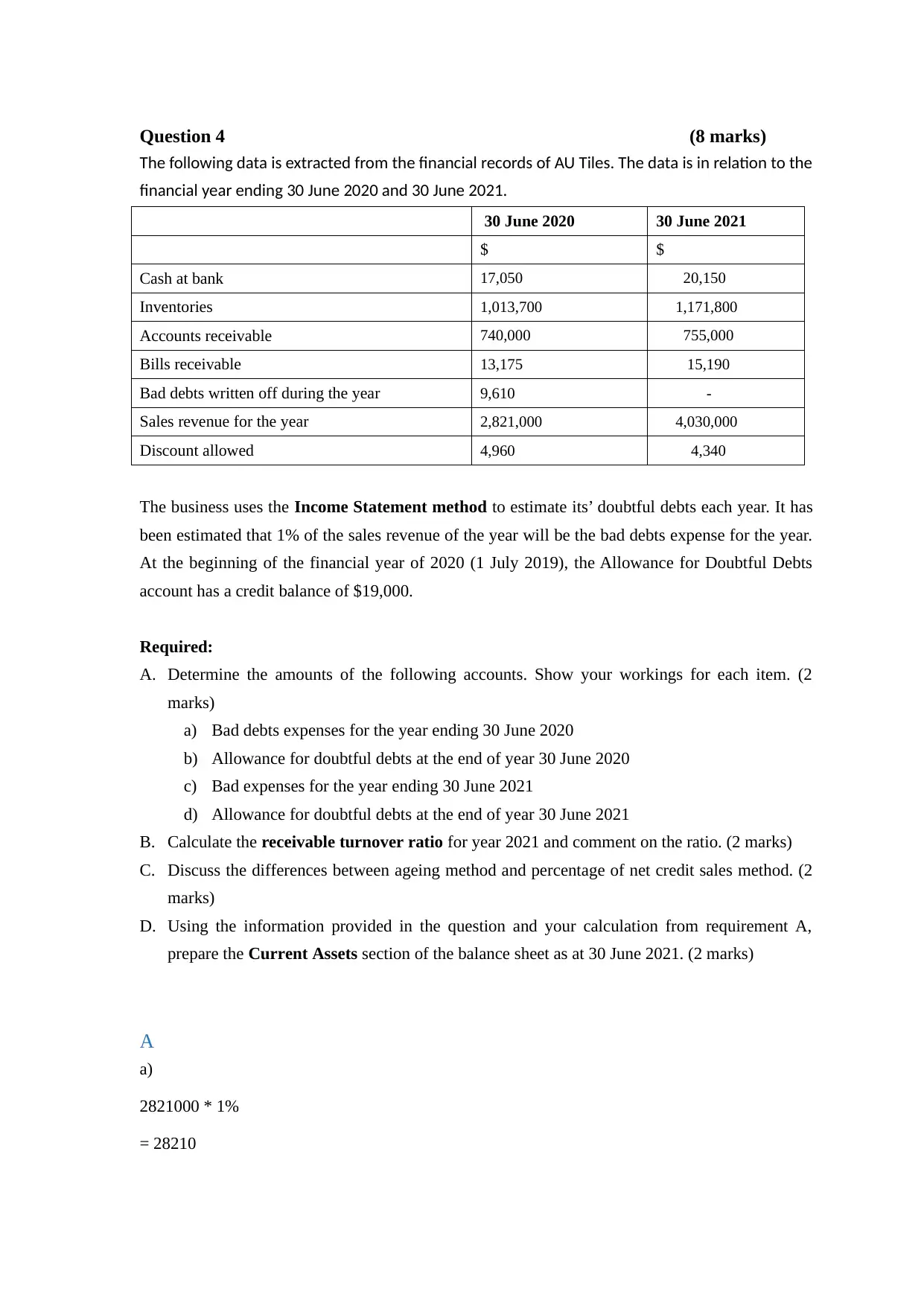

Question 4 (8 marks)

The following data is extracted from the financial records of AU Tiles. The data is in relation to the

financial year ending 30 June 2020 and 30 June 2021.

30 June 2020 30 June 2021

$ $

Cash at bank 17,050 20,150

Inventories 1,013,700 1,171,800

Accounts receivable 740,000 755,000

Bills receivable 13,175 15,190

Bad debts written off during the year 9,610 -

Sales revenue for the year 2,821,000 4,030,000

Discount allowed 4,960 4,340

The business uses the Income Statement method to estimate its’ doubtful debts each year. It has

been estimated that 1% of the sales revenue of the year will be the bad debts expense for the year.

At the beginning of the financial year of 2020 (1 July 2019), the Allowance for Doubtful Debts

account has a credit balance of $19,000.

Required:

A. Determine the amounts of the following accounts. Show your workings for each item. (2

marks)

a) Bad debts expenses for the year ending 30 June 2020

b) Allowance for doubtful debts at the end of year 30 June 2020

c) Bad expenses for the year ending 30 June 2021

d) Allowance for doubtful debts at the end of year 30 June 2021

B. Calculate the receivable turnover ratio for year 2021 and comment on the ratio. (2 marks)

C. Discuss the differences between ageing method and percentage of net credit sales method. (2

marks)

D. Using the information provided in the question and your calculation from requirement A,

prepare the Current Assets section of the balance sheet as at 30 June 2021. (2 marks)

A

a)

2821000 * 1%

= 28210

The following data is extracted from the financial records of AU Tiles. The data is in relation to the

financial year ending 30 June 2020 and 30 June 2021.

30 June 2020 30 June 2021

$ $

Cash at bank 17,050 20,150

Inventories 1,013,700 1,171,800

Accounts receivable 740,000 755,000

Bills receivable 13,175 15,190

Bad debts written off during the year 9,610 -

Sales revenue for the year 2,821,000 4,030,000

Discount allowed 4,960 4,340

The business uses the Income Statement method to estimate its’ doubtful debts each year. It has

been estimated that 1% of the sales revenue of the year will be the bad debts expense for the year.

At the beginning of the financial year of 2020 (1 July 2019), the Allowance for Doubtful Debts

account has a credit balance of $19,000.

Required:

A. Determine the amounts of the following accounts. Show your workings for each item. (2

marks)

a) Bad debts expenses for the year ending 30 June 2020

b) Allowance for doubtful debts at the end of year 30 June 2020

c) Bad expenses for the year ending 30 June 2021

d) Allowance for doubtful debts at the end of year 30 June 2021

B. Calculate the receivable turnover ratio for year 2021 and comment on the ratio. (2 marks)

C. Discuss the differences between ageing method and percentage of net credit sales method. (2

marks)

D. Using the information provided in the question and your calculation from requirement A,

prepare the Current Assets section of the balance sheet as at 30 June 2021. (2 marks)

A

a)

2821000 * 1%

= 28210

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

b)

19000 + 28210 – 9610

= 37600

c)

4030000 * 1%

= 40300

d)

37600 + 40300

= 77900

B

Net credit sale / average account receivable

= 4030000 / 57750 (77900 + 37600 / 2)

= 69.78

The ratio demonstrates about the proportion of the account receivable involve in the sales of

company. This is a key ratio that demonstrate and indicate in respect to the liquidity situation of

business venture (Cynthia, 2020). The role of this ratio is under to demonstrate about the fact in

context to the net credit sale and the debtor account balance. In simple term this ratio talk about

the proportionate time debtors will be of net credit sales.

C

The basic difference is such that in case of percentage of sales method residual amount do not

get to a part of the whole calculation related to the bad-debt allowance whereas, in case of ageing

technique this is considered as part of the current ageing (Singh, 2019). Both the method contains

one basic difference that further create a different result at the time of evaluation.

D

Cash at bank 20150

Inventories 1171800

Account receivable 755000

Bill receivable 15190

1962140

19000 + 28210 – 9610

= 37600

c)

4030000 * 1%

= 40300

d)

37600 + 40300

= 77900

B

Net credit sale / average account receivable

= 4030000 / 57750 (77900 + 37600 / 2)

= 69.78

The ratio demonstrates about the proportion of the account receivable involve in the sales of

company. This is a key ratio that demonstrate and indicate in respect to the liquidity situation of

business venture (Cynthia, 2020). The role of this ratio is under to demonstrate about the fact in

context to the net credit sale and the debtor account balance. In simple term this ratio talk about

the proportionate time debtors will be of net credit sales.

C

The basic difference is such that in case of percentage of sales method residual amount do not

get to a part of the whole calculation related to the bad-debt allowance whereas, in case of ageing

technique this is considered as part of the current ageing (Singh, 2019). Both the method contains

one basic difference that further create a different result at the time of evaluation.

D

Cash at bank 20150

Inventories 1171800

Account receivable 755000

Bill receivable 15190

1962140

Question 5 (4 marks)

Apply the definition and recognition criteria of liabilities, discuss why, or why not, each of the

following items is recognised as a liability in the financial statement.

a) GST outlays

b) GST collection

c) Provision for warranty

d) Unearned revenue

e) An agreement to act as guarantor for another firm’s borrowings.

f) Dividend payable

g) Allowance for doubtful debts

h) Accrued interest

a) GST outlays

It is a current asset account which is used to accrue GST on purchases, that is, when a purchase

is made and asset or expense is debited, GST outlays current asset account is also debited (Smith,

2020). It shows GST paid to firms for goods and services which is offset against GST collections.

It is not treated as liability because it is a current asset account.

b) GST collections

GST is an indirect federal sales tax which is applicable on goods and services and collected by

the businesses and paid to government (Mukherjee, 2019). It is treated as liability because it is a

burden on company's part to collect stated tax from customers and pay it back to government.

c) Provision for warranty

The company makes a provision when an item is sold on warranty. It is like a promise made by

company to its customers which states that there will be no issue or problems in product, and if it

is there, then company will replace or repair it with a new piece without charging any additional

money (Tang and et.al., 2020). This provision cannot be treated as liability because it is not

considered as an expense of company. Business usually keeps aside money that may become an

expense if the event occurred.

d) Unearned revenue

It is that income or money received by company for goods or services which is not yet

provided by company to its customers (Richman, Richman and Richman, 2021). In case of such

prepaid income, liability has arisen on part of company to deliver items to their customers.

e) An agreement to act as guarantor for another firm's borrowings

Apply the definition and recognition criteria of liabilities, discuss why, or why not, each of the

following items is recognised as a liability in the financial statement.

a) GST outlays

b) GST collection

c) Provision for warranty

d) Unearned revenue

e) An agreement to act as guarantor for another firm’s borrowings.

f) Dividend payable

g) Allowance for doubtful debts

h) Accrued interest

a) GST outlays

It is a current asset account which is used to accrue GST on purchases, that is, when a purchase

is made and asset or expense is debited, GST outlays current asset account is also debited (Smith,

2020). It shows GST paid to firms for goods and services which is offset against GST collections.

It is not treated as liability because it is a current asset account.

b) GST collections

GST is an indirect federal sales tax which is applicable on goods and services and collected by

the businesses and paid to government (Mukherjee, 2019). It is treated as liability because it is a

burden on company's part to collect stated tax from customers and pay it back to government.

c) Provision for warranty

The company makes a provision when an item is sold on warranty. It is like a promise made by

company to its customers which states that there will be no issue or problems in product, and if it

is there, then company will replace or repair it with a new piece without charging any additional

money (Tang and et.al., 2020). This provision cannot be treated as liability because it is not

considered as an expense of company. Business usually keeps aside money that may become an

expense if the event occurred.

d) Unearned revenue

It is that income or money received by company for goods or services which is not yet

provided by company to its customers (Richman, Richman and Richman, 2021). In case of such

prepaid income, liability has arisen on part of company to deliver items to their customers.

e) An agreement to act as guarantor for another firm's borrowings

The agreement is known as cross guarantee which is an agreement between 2 or more related

companies for providing guarantee to each other's payment obligation. Such agreements protect

company that incurred a liability from the chances of losing assets in case non-payment (Okon

and Okon, 2021). Cross guarantee results in liability because there is an obligation to settle funds

to debtor if company fails to pay.

f) Dividend payable

The amount which is authorized to be paid to shareholders after all deductions are made from

profit but has not yet paid to them in cash (Cheung and Zhang, 2019). It is definitely a liability

because it decreases firm's assets by total dividend paid.

g) Allowance for doubtful debts

It is a contra asset because it decreases amount of asset which shows management's estimation

of accounts receivables that will not be paid by customers. It is provision that will happen in

future but the exact amount of it is not known (Christodoulou-Volos, 2020). Bad debts have

already occurred and it is a liability but an allowance made for it is an estimate of doubtful debts

in the future.

h) Accrued Interest

The interest that been incurred by company on behalf of any loan or financial obligation but

which is not yet paid by company (Cowling, Ughetto and Lee, 2018). It depends on whether

company is lending or borrowing because in case of lending accrued interest is asset. On the other

hand, in case of borrowing, it is a current asset.

Question 6 (10 marks)

Tidy & Cleaning Services provides cleaning and housekeeping services to both households and

businesses. The entity prepares financial statements at the end of each month. The following

information is provided in relation to the business’s operations in the month of July 2021.

1. On 1 July 2021, the business signed an advertising agreement, that costs $10,800 for six (6)

months plus $1 per each click on their advertisements, with an online website to promote its

business for the next six months. The agreement stated $1,800 per month will need to be paid

in advance at the beginning of each month, $1 per each click on their ads will be paid at the

end of the 6th month agreement. A $1,800 advance was paid on 1 July.

2. On 2 July, rent of $39,000 is paid for a 6-months period from 1 July to 31 December 2021.

companies for providing guarantee to each other's payment obligation. Such agreements protect

company that incurred a liability from the chances of losing assets in case non-payment (Okon

and Okon, 2021). Cross guarantee results in liability because there is an obligation to settle funds

to debtor if company fails to pay.

f) Dividend payable

The amount which is authorized to be paid to shareholders after all deductions are made from

profit but has not yet paid to them in cash (Cheung and Zhang, 2019). It is definitely a liability

because it decreases firm's assets by total dividend paid.

g) Allowance for doubtful debts

It is a contra asset because it decreases amount of asset which shows management's estimation

of accounts receivables that will not be paid by customers. It is provision that will happen in

future but the exact amount of it is not known (Christodoulou-Volos, 2020). Bad debts have

already occurred and it is a liability but an allowance made for it is an estimate of doubtful debts

in the future.

h) Accrued Interest

The interest that been incurred by company on behalf of any loan or financial obligation but

which is not yet paid by company (Cowling, Ughetto and Lee, 2018). It depends on whether

company is lending or borrowing because in case of lending accrued interest is asset. On the other

hand, in case of borrowing, it is a current asset.

Question 6 (10 marks)

Tidy & Cleaning Services provides cleaning and housekeeping services to both households and

businesses. The entity prepares financial statements at the end of each month. The following

information is provided in relation to the business’s operations in the month of July 2021.

1. On 1 July 2021, the business signed an advertising agreement, that costs $10,800 for six (6)

months plus $1 per each click on their advertisements, with an online website to promote its

business for the next six months. The agreement stated $1,800 per month will need to be paid

in advance at the beginning of each month, $1 per each click on their ads will be paid at the

end of the 6th month agreement. A $1,800 advance was paid on 1 July.

2. On 2 July, rent of $39,000 is paid for a 6-months period from 1 July to 31 December 2021.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

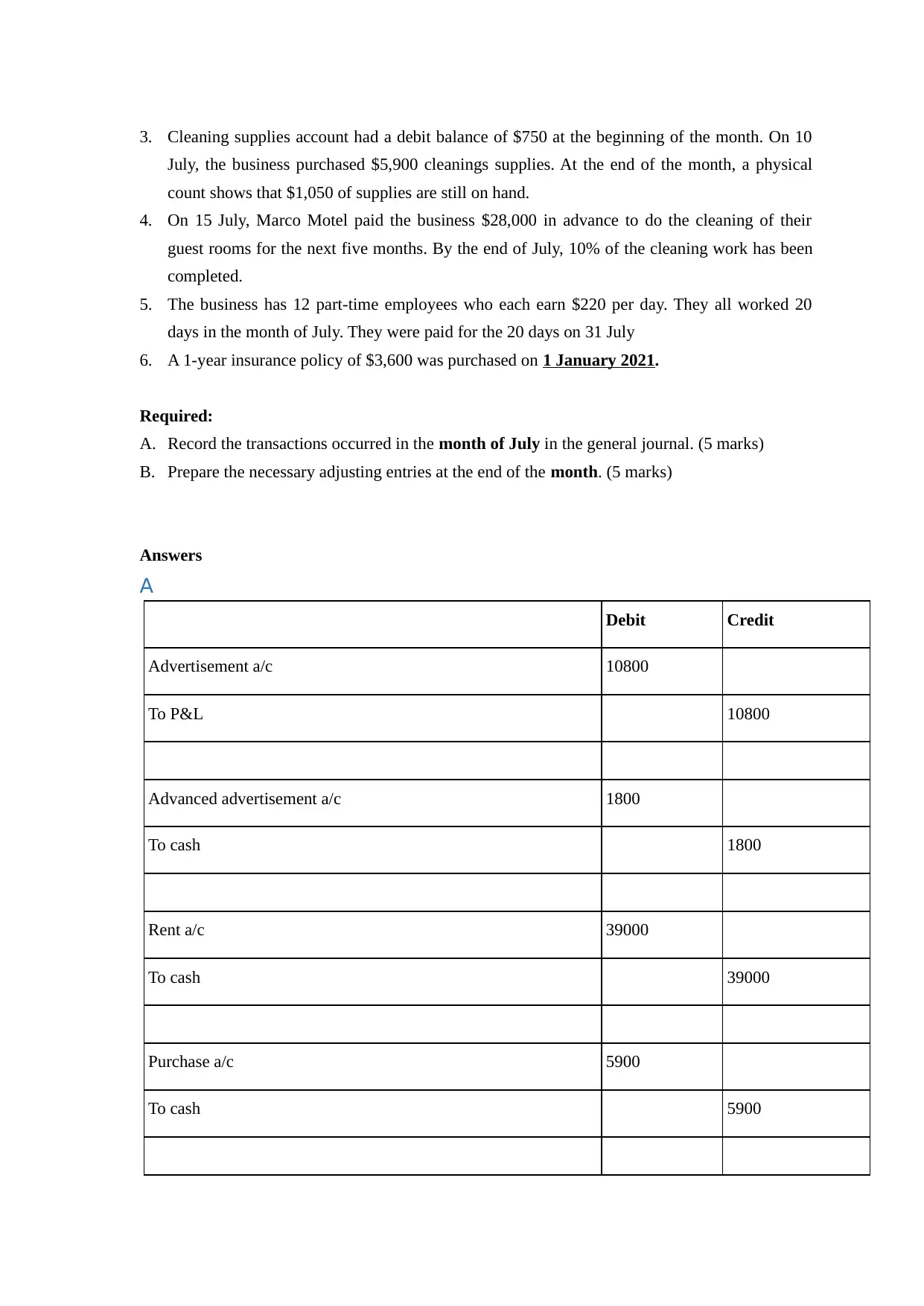

3. Cleaning supplies account had a debit balance of $750 at the beginning of the month. On 10

July, the business purchased $5,900 cleanings supplies. At the end of the month, a physical

count shows that $1,050 of supplies are still on hand.

4. On 15 July, Marco Motel paid the business $28,000 in advance to do the cleaning of their

guest rooms for the next five months. By the end of July, 10% of the cleaning work has been

completed.

5. The business has 12 part-time employees who each earn $220 per day. They all worked 20

days in the month of July. They were paid for the 20 days on 31 July

6. A 1-year insurance policy of $3,600 was purchased on 1 January 2021.

Required:

A. Record the transactions occurred in the month of July in the general journal. (5 marks)

B. Prepare the necessary adjusting entries at the end of the month. (5 marks)

Answers

A

Debit Credit

Advertisement a/c 10800

To P&L 10800

Advanced advertisement a/c 1800

To cash 1800

Rent a/c 39000

To cash 39000

Purchase a/c 5900

To cash 5900

July, the business purchased $5,900 cleanings supplies. At the end of the month, a physical

count shows that $1,050 of supplies are still on hand.

4. On 15 July, Marco Motel paid the business $28,000 in advance to do the cleaning of their

guest rooms for the next five months. By the end of July, 10% of the cleaning work has been

completed.

5. The business has 12 part-time employees who each earn $220 per day. They all worked 20

days in the month of July. They were paid for the 20 days on 31 July

6. A 1-year insurance policy of $3,600 was purchased on 1 January 2021.

Required:

A. Record the transactions occurred in the month of July in the general journal. (5 marks)

B. Prepare the necessary adjusting entries at the end of the month. (5 marks)

Answers

A

Debit Credit

Advertisement a/c 10800

To P&L 10800

Advanced advertisement a/c 1800

To cash 1800

Rent a/c 39000

To cash 39000

Purchase a/c 5900

To cash 5900

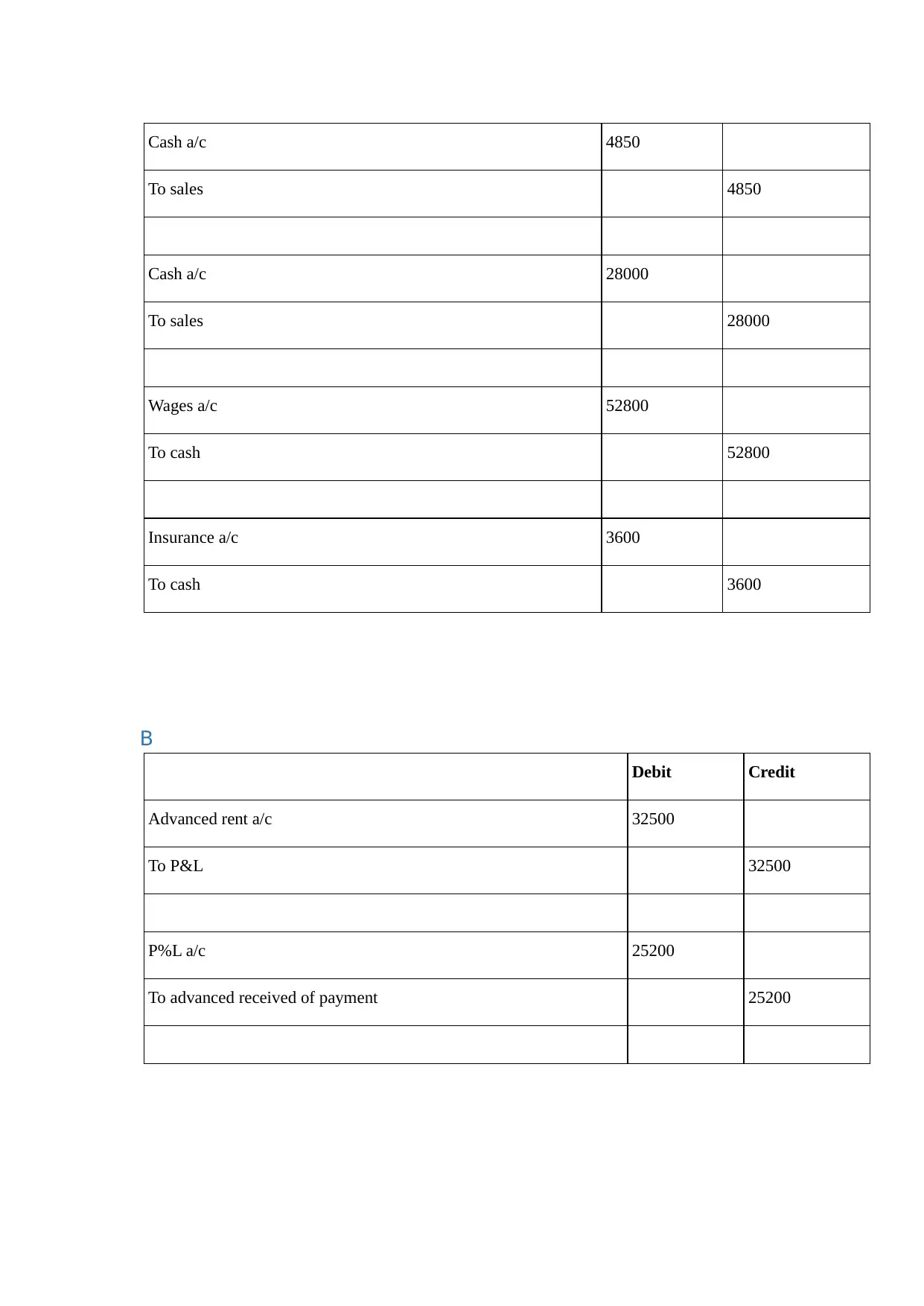

Cash a/c 4850

To sales 4850

Cash a/c 28000

To sales 28000

Wages a/c 52800

To cash 52800

Insurance a/c 3600

To cash 3600

B

Debit Credit

Advanced rent a/c 32500

To P&L 32500

P%L a/c 25200

To advanced received of payment 25200

To sales 4850

Cash a/c 28000

To sales 28000

Wages a/c 52800

To cash 52800

Insurance a/c 3600

To cash 3600

B

Debit Credit

Advanced rent a/c 32500

To P&L 32500

P%L a/c 25200

To advanced received of payment 25200

REFERENCES

Books and Journals

Cheung, E. C. and Zhang, Z., 2019. Periodic threshold-type dividend strategy in the compound

Poisson risk model. Scandinavian Actuarial Journal. 2019(1). pp.1-31

Christodoulou-Volos, C. N., 2020. Allowance for Doubtful Accounts and Earning Management:

An Empirical Study of Chinese Listed Companies. Journal of Finance and Investment

Analysis. 9(3). pp.1-4.

Cowling, M., Ughetto, E. and Lee, N., 2018. The innovation debt penalty: Cost of debt, loan

default, and the effects of a public loan guarantee on high-tech firms. Technological

Forecasting and Social Change. 127. pp.166-176.

Cynthia, C., 2020. Effect of Account Receivable Turnover, Current Ratio And Debt To Equity

Ratio On The Profitability Of Construction Companies On The Indonesia Stock

Exchange (IDX). HUMANIS (Humanities, Management and Science Proceedings). 1(1).

Mukherjee, S., 2019. Whether States Have Capacity to Sustain Projected Growth in GST

Collection During the GST Compensation Period?. Review of Market Integration. 11(1-2).

pp.30-53.

Okon, E. B. and Okon, N. S., 2021. Sources of State Revenue and State Effectiveness: The

Nigerian Experience. International Journal of Financial Research. 12(1). pp.111-122.

Richman, R. L., Richman, J. T. and Richman, H. B., 2021. Accrued Gains are not Income: An

Administratively Simple Rollover Treatment for Capital Gains Taxation. International

Journal of Economics and Finance. 12(12). pp.1-1.

Singh, A., 2019. Management of Receivables: A Study of Selected Micro and Small

Enterprises. Management.

Smith, G., 2020. GST as a secure source of revenue for the States and Territories. EJTR. 18. p.27.

Tang, J. and et.al., 2020. Pricing and warranty decisions in a two-period closed-loop supply

chain. International Journal of Production Research. 58(6). pp.1688-1704.

Books and Journals

Cheung, E. C. and Zhang, Z., 2019. Periodic threshold-type dividend strategy in the compound

Poisson risk model. Scandinavian Actuarial Journal. 2019(1). pp.1-31

Christodoulou-Volos, C. N., 2020. Allowance for Doubtful Accounts and Earning Management:

An Empirical Study of Chinese Listed Companies. Journal of Finance and Investment

Analysis. 9(3). pp.1-4.

Cowling, M., Ughetto, E. and Lee, N., 2018. The innovation debt penalty: Cost of debt, loan

default, and the effects of a public loan guarantee on high-tech firms. Technological

Forecasting and Social Change. 127. pp.166-176.

Cynthia, C., 2020. Effect of Account Receivable Turnover, Current Ratio And Debt To Equity

Ratio On The Profitability Of Construction Companies On The Indonesia Stock

Exchange (IDX). HUMANIS (Humanities, Management and Science Proceedings). 1(1).

Mukherjee, S., 2019. Whether States Have Capacity to Sustain Projected Growth in GST

Collection During the GST Compensation Period?. Review of Market Integration. 11(1-2).

pp.30-53.

Okon, E. B. and Okon, N. S., 2021. Sources of State Revenue and State Effectiveness: The

Nigerian Experience. International Journal of Financial Research. 12(1). pp.111-122.

Richman, R. L., Richman, J. T. and Richman, H. B., 2021. Accrued Gains are not Income: An

Administratively Simple Rollover Treatment for Capital Gains Taxation. International

Journal of Economics and Finance. 12(12). pp.1-1.

Singh, A., 2019. Management of Receivables: A Study of Selected Micro and Small

Enterprises. Management.

Smith, G., 2020. GST as a secure source of revenue for the States and Territories. EJTR. 18. p.27.

Tang, J. and et.al., 2020. Pricing and warranty decisions in a two-period closed-loop supply

chain. International Journal of Production Research. 58(6). pp.1688-1704.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.