Dryden Natural Springs: An Intermediate Accounting II Case Study

VerifiedAdded on 2023/05/31

|7

|2319

|236

Case Study

AI Summary

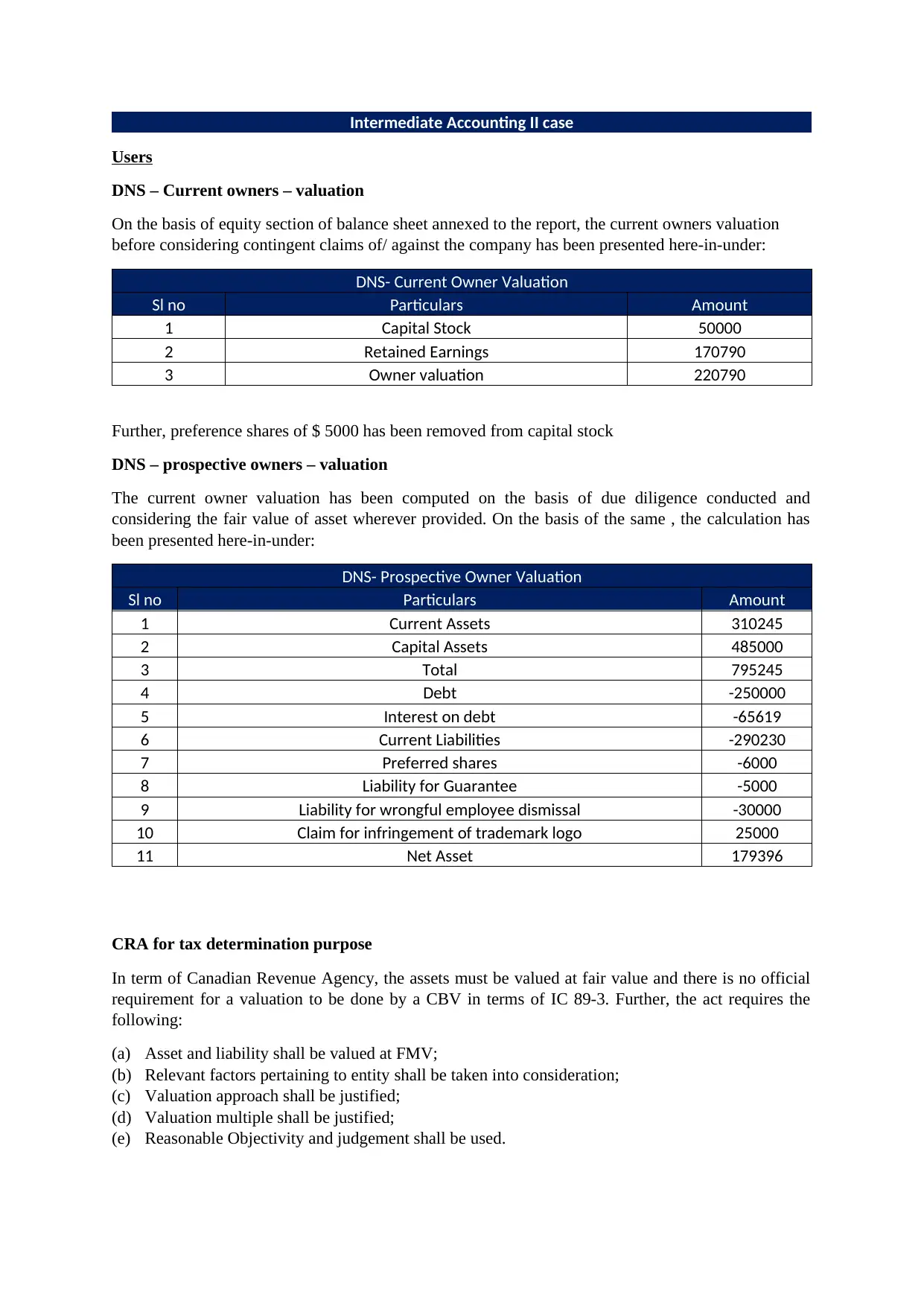

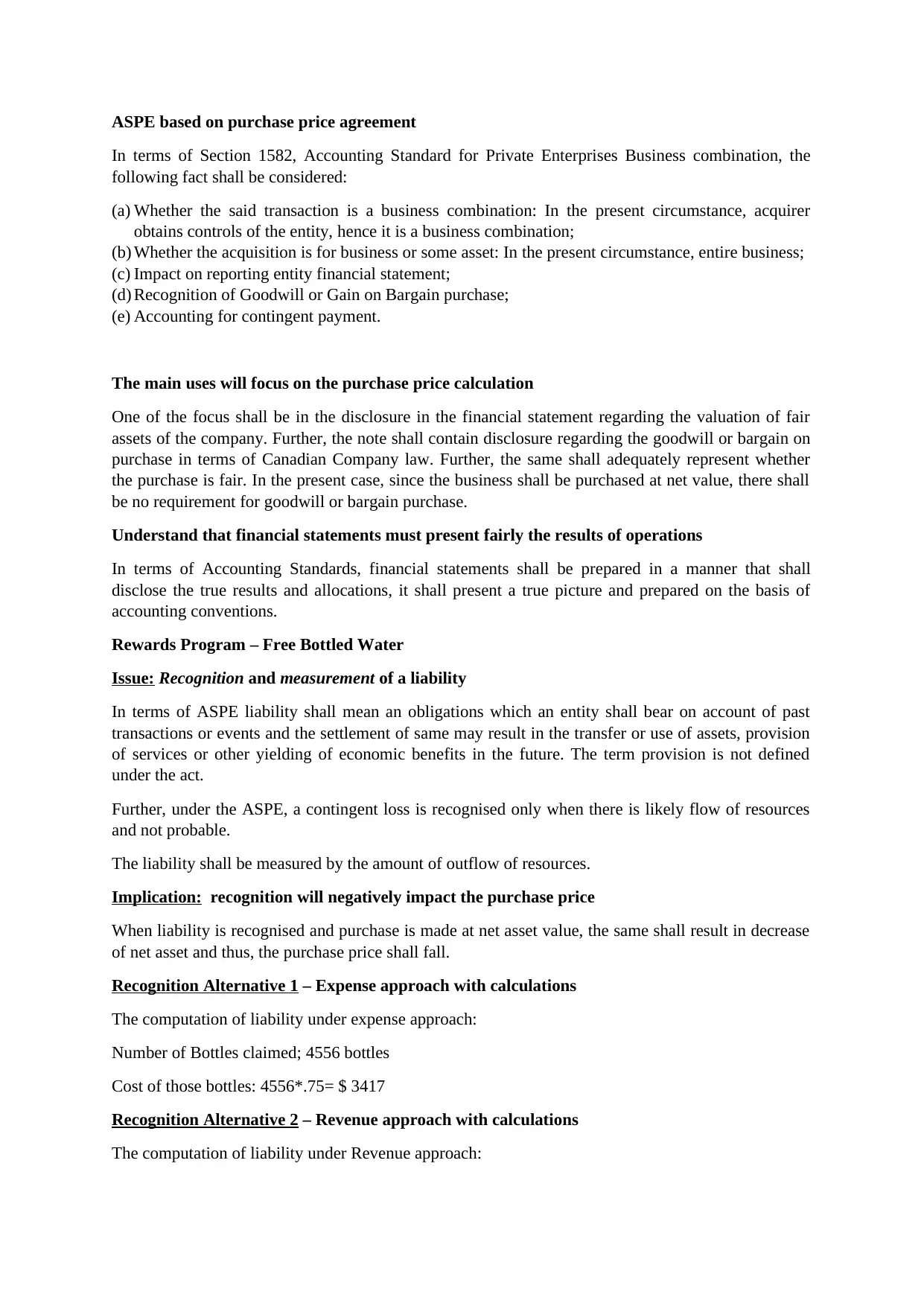

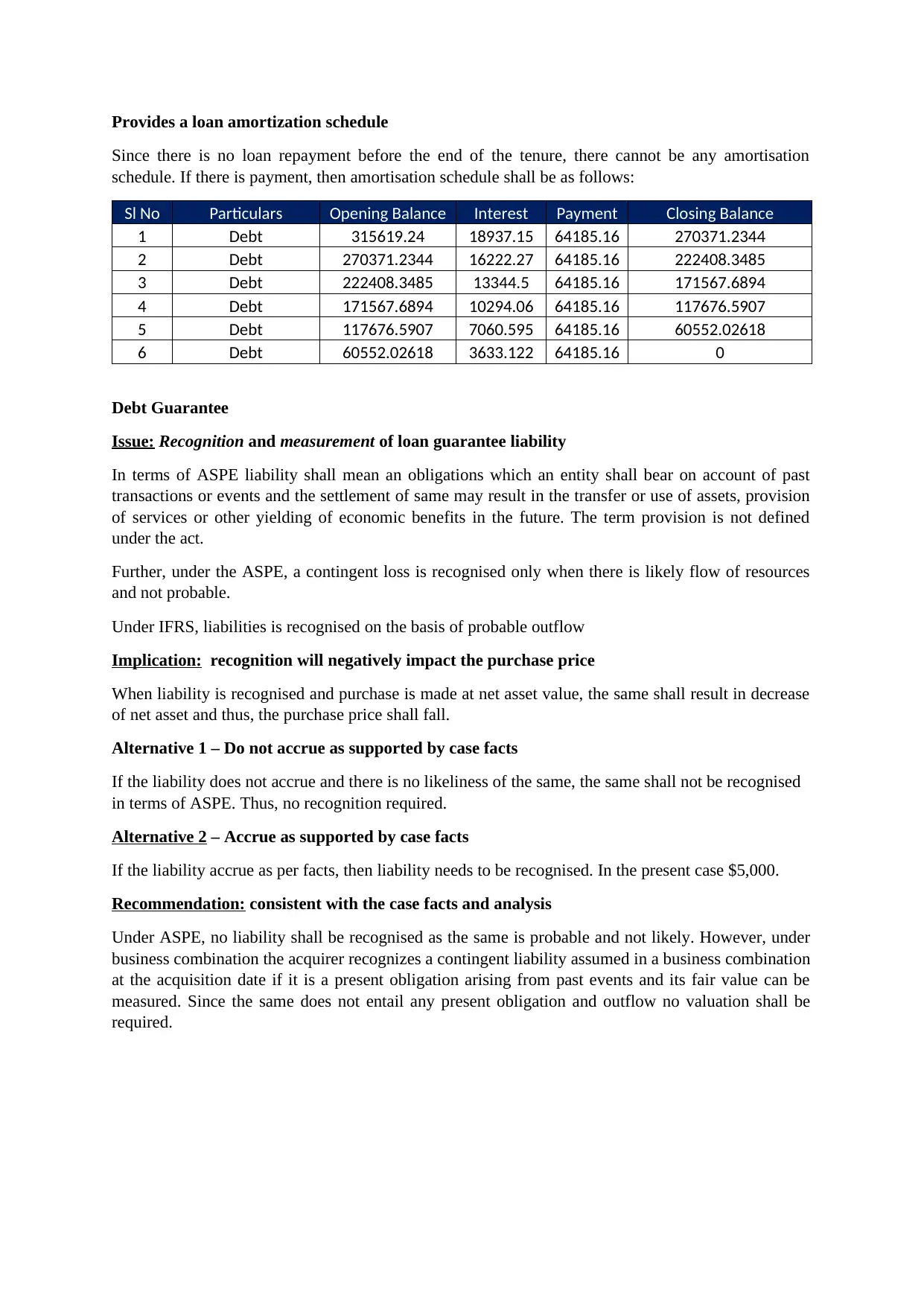

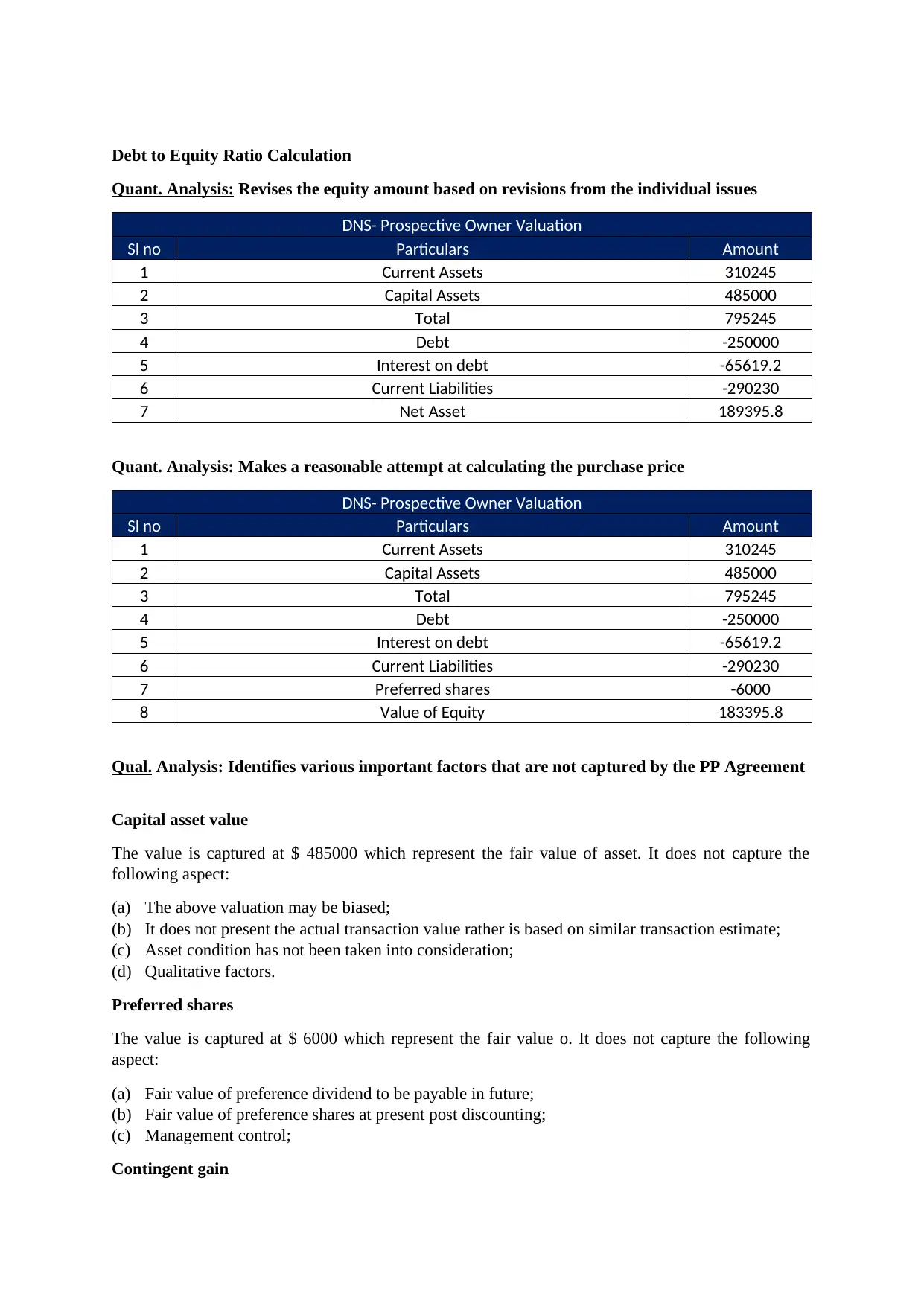

This case study solution examines the acquisition of Dryden Natural Springs, focusing on the valuation from both current and prospective owner perspectives. It delves into the application of Canadian Revenue Agency (CRA) guidelines for tax determination and Accounting Standards for Private Enterprises (ASPE) concerning business combinations, particularly purchase price agreements. The analysis addresses key issues such as the rewards program (free bottled water), contingent losses and gains, long-term debt measurement, and debt guarantees, providing recommendations consistent with ASPE. The solution includes quantitative analysis, revising equity amounts and calculating purchase price, and qualitative analysis, identifying factors not captured by the purchase price agreement, such as capital asset value, preferred shares, contingent gains and losses. The document provides calculations and amortization schedules where applicable, ultimately aiming to present a fair view of the financial implications of the acquisition.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.