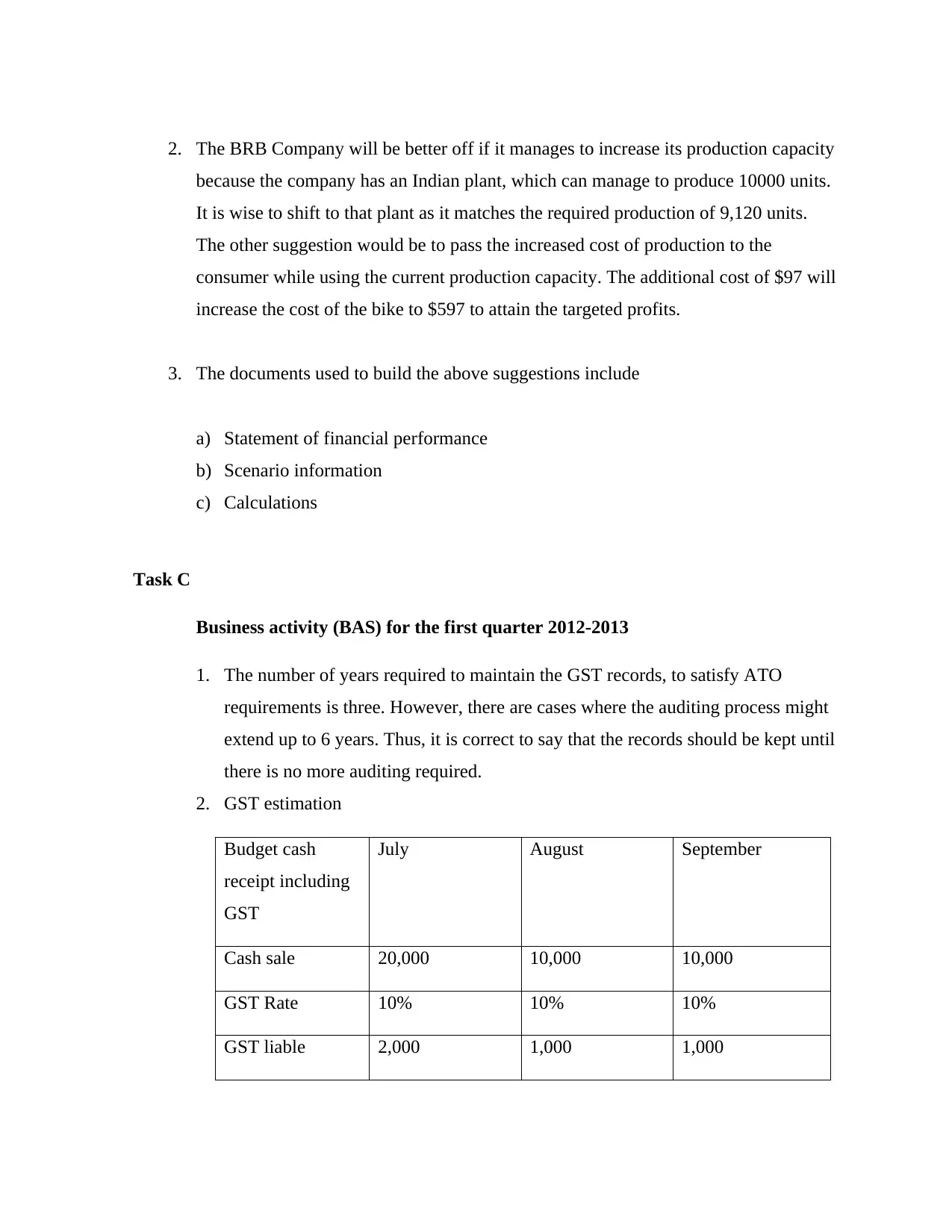

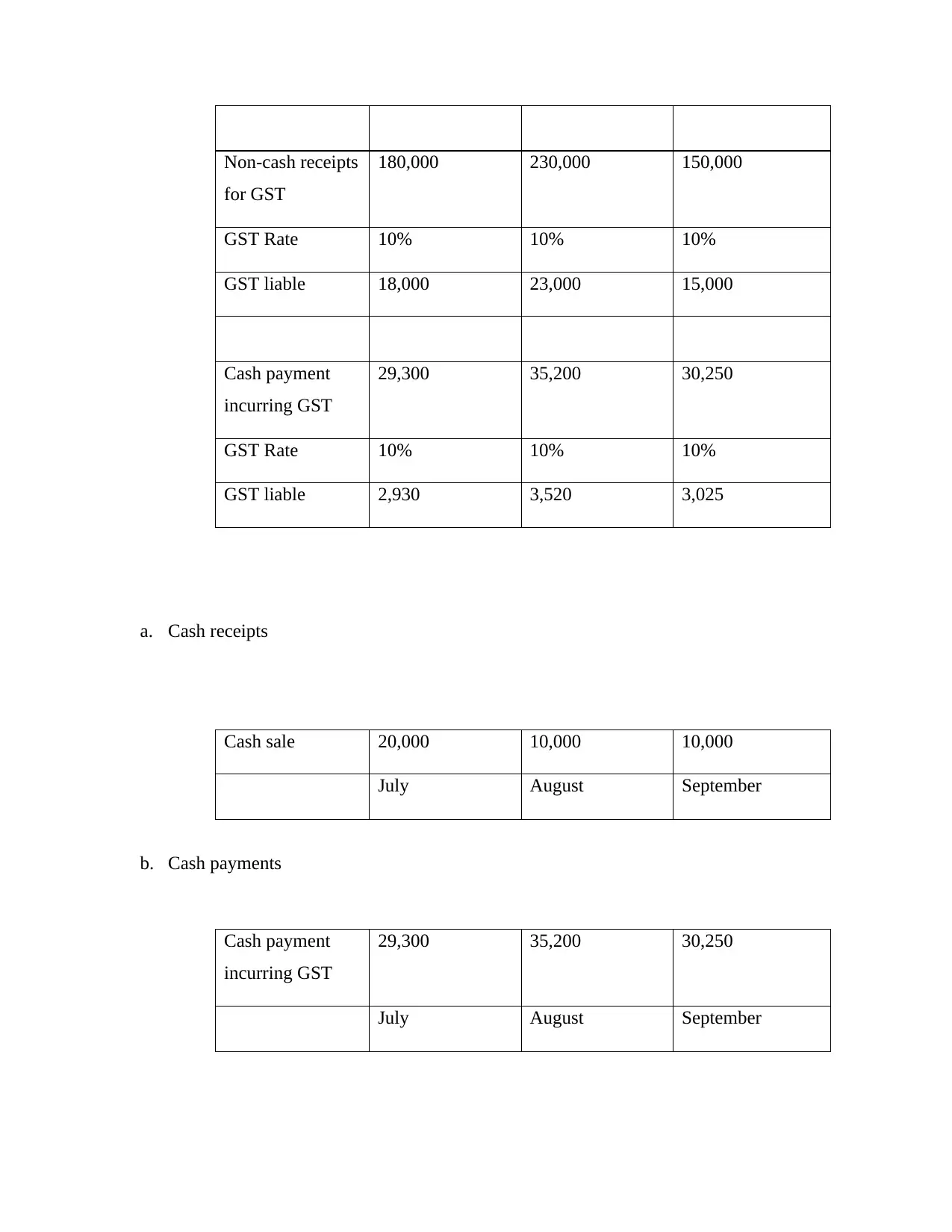

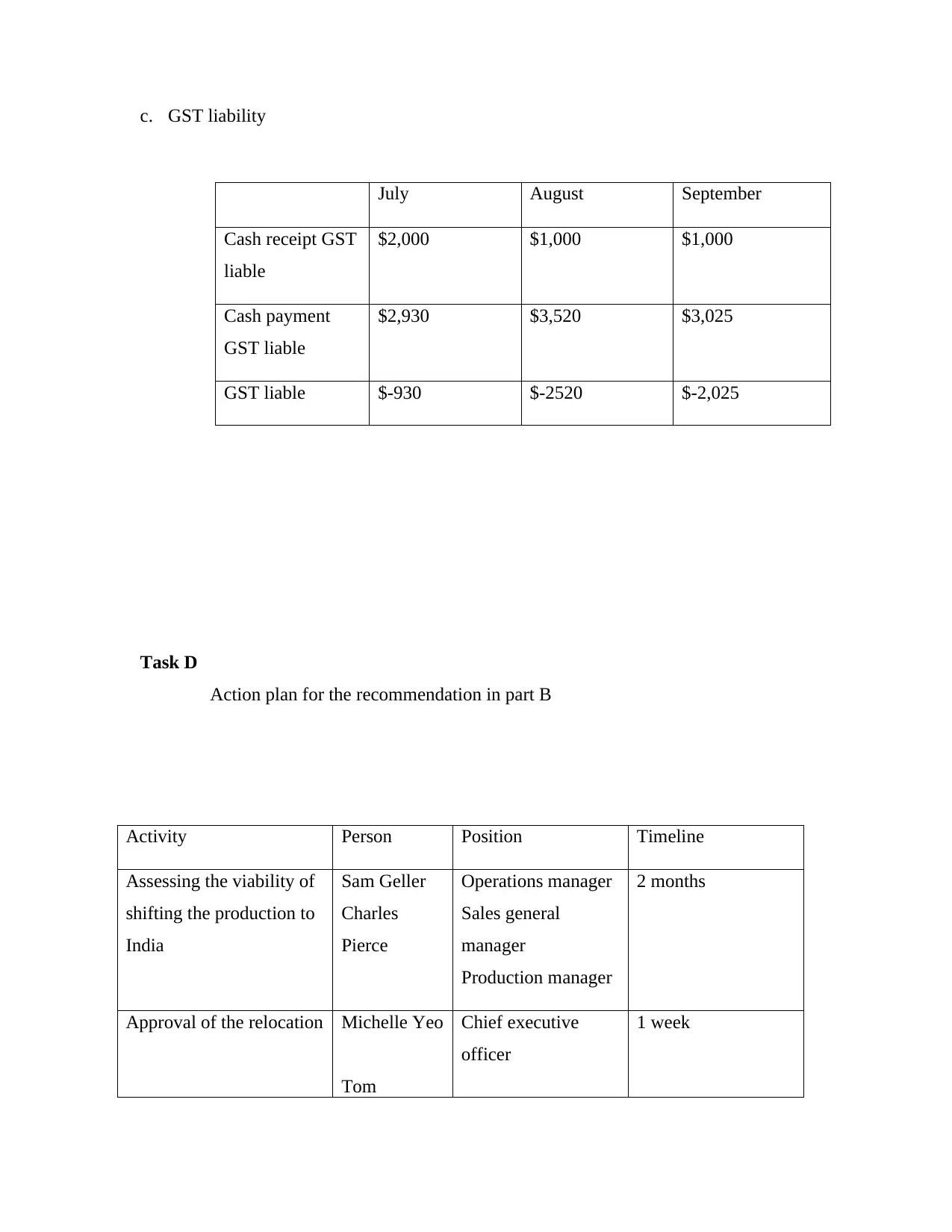

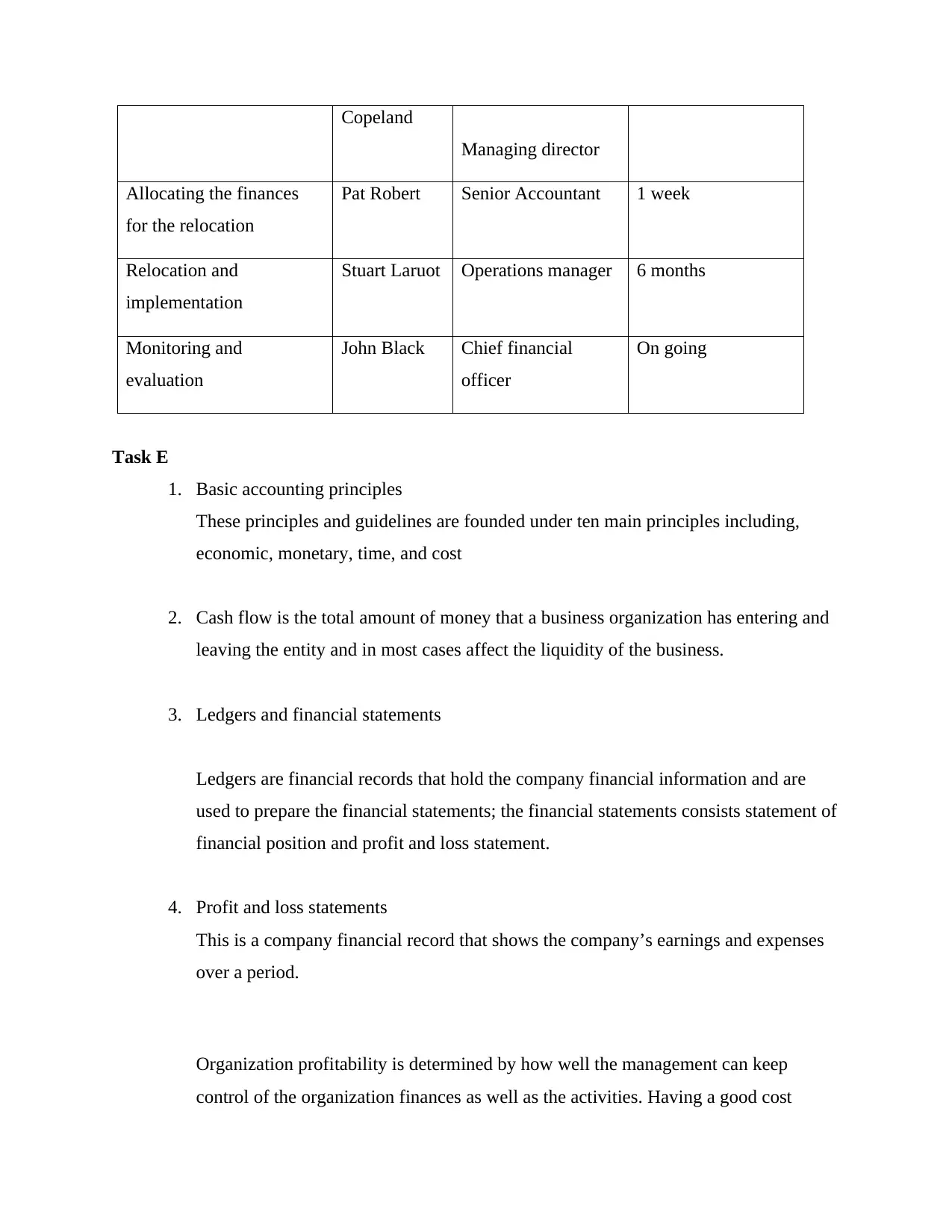

The assignment content discusses various accounting and financial concepts related to Goods and Services Tax (GST) estimation, budget cash receipt including GST, and basic accounting principles. It involves calculating GST liability for cash sales, non-cash receipts, and cash payments incurring GST for the months of July, August, and September. The content also touches on task D, which recommends shifting production to India and outlines an action plan for approval, allocation of finances, relocation, and monitoring. Additionally, it discusses basic accounting principles such as ledgers and financial statements, including profit and loss statements, and the importance of organization profitability.

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)