HA3032: Developing Audit Program for Cygnus Gold Limited - Project

VerifiedAdded on 2022/09/14

|21

|4058

|12

Project

AI Summary

This project develops an audit program for Cygnus Gold Limited, a company listed on the Australian Stock Exchange (ASX). The assignment begins with an overview of Cygnus Gold's business, focusing on its exploration activities for base metals and gold. It then identifies key business risks, including liquidity, currency, and market risks. The audit risk model is applied to assess inherent and control risks, leading to the determination of detection risk. Analytical procedures, including ratio analysis, are performed to evaluate Cygnus Gold's financial performance, focusing on profitability, efficiency, and solvency. Materiality is considered in relation to account balances. The project concludes with a detailed set of audit work steps for material account balances, incorporating assertions and sampling plans to generate appropriate audit evidence. This comprehensive approach ensures a thorough audit program is developed, addressing various financial aspects of the company.

Running head: DEVELOPING AN AUDIT PROGRAM FOR SELECTED PUBLICALLY

LISTED COMPANY

Developing an audit program for a selected publically listed company

Name of the student

Name of the university

Student ID

Author note

LISTED COMPANY

Developing an audit program for a selected publically listed company

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DEVELOPING AN AUDIT PROGRAM FOR SELECTED PUBLICALLY LISTED

COMPANY

Executive summary:

The paper is prepared to develop the audit program of one of the companies listed on the

Australian stock exchange. For the purpose of analysis, the selected company is Cygnus Gold

limited for which the nature of business and different types of risks faced have been

identified. The development of audit program incorporate the adoption of the audit risk model

for determining the overall audit risk faced by the company. Development of audit program is

done by performing analytical procedures that concerns the evaluation of the financial

performance using ratio analysis tool. The materiality of the account balances have been

identified by analyzing the trend of ratio and the figures obtained therein. The later part of the

paper depicts the comprehensive set of audit work steps for each of the material account

balance that are identified. Development of such program helps in obtaining audit evidence

for all the accounts that have been tested.

COMPANY

Executive summary:

The paper is prepared to develop the audit program of one of the companies listed on the

Australian stock exchange. For the purpose of analysis, the selected company is Cygnus Gold

limited for which the nature of business and different types of risks faced have been

identified. The development of audit program incorporate the adoption of the audit risk model

for determining the overall audit risk faced by the company. Development of audit program is

done by performing analytical procedures that concerns the evaluation of the financial

performance using ratio analysis tool. The materiality of the account balances have been

identified by analyzing the trend of ratio and the figures obtained therein. The later part of the

paper depicts the comprehensive set of audit work steps for each of the material account

balance that are identified. Development of such program helps in obtaining audit evidence

for all the accounts that have been tested.

DEVELOPING AN AUDIT PROGRAM FOR SELECTED PUBLICALLY LISTED

COMPANY

Table of Contents

Introduction:...............................................................................................................................2

Discussion:.................................................................................................................................2

Understanding the nature of business entity:.............................................................................2

Identification of key business risk:............................................................................................3

Assessing risk of material misstatements:..................................................................................3

Performing analytical procedures of the financial position statement:......................................3

Identification of material accounts balances and computation of materiality for planning

purposes:....................................................................................................................................4

Conclusion:................................................................................................................................5

References list:...........................................................................................................................6

COMPANY

Table of Contents

Introduction:...............................................................................................................................2

Discussion:.................................................................................................................................2

Understanding the nature of business entity:.............................................................................2

Identification of key business risk:............................................................................................3

Assessing risk of material misstatements:..................................................................................3

Performing analytical procedures of the financial position statement:......................................3

Identification of material accounts balances and computation of materiality for planning

purposes:....................................................................................................................................4

Conclusion:................................................................................................................................5

References list:...........................................................................................................................6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DEVELOPING AN AUDIT PROGRAM FOR SELECTED PUBLICALLY LISTED

COMPANY

Introduction:

The paper demonstrates the development of an audit program for a company listed on

Australian stock exchange (ASX). The chosen company for which the audit program is

developed is Cygnus Gold limited that is engaged in the discovery of base metals deposits

and gold within the Terrane of Southwest in the Wheatbelt region of Western Australia.

Cygnus is an exploration company that focuses on the development of base metals and gold

deposits in the South west Yilgarn of Western Australia. The company is managing the

exploration of two joint ventures with Gold resources limited and significant earn in

agreements (Cygnusgold.com 2019). The application of audit risk model for assessing the

inherent risk and control is demonstrated in the paper. For the development of audit program

for Cygnus, substantive and analytical procedures have been adopted that helps in

identification of the account balances that are material. A comprehensive set of audit work

for each of the material account balances identified has been addressed in the context of

assertions so that there is a generation of appropriate audit evidences. The audit program also

incorporates the development of sampling plan for each of the identified material accounts

balances that have been tested.

Discussion:

Understanding the nature of business entity:

The discovery of base metal deposits and high grade gold has been targeted by

Cygnus within the Southwest Terrane of Western Australia. Most advanced exploration

project of Cygnus is Stanley project that comprise of an area of approximately 160 km2. The

initial diamond drilling program was followed by Cygnus by targeting the basement

extension of gold mineralization and high grade zone as well as targeting on the Stanley Hills

and Brays prospects. A detailed ground gravity survey that targeted relatively dense massive

COMPANY

Introduction:

The paper demonstrates the development of an audit program for a company listed on

Australian stock exchange (ASX). The chosen company for which the audit program is

developed is Cygnus Gold limited that is engaged in the discovery of base metals deposits

and gold within the Terrane of Southwest in the Wheatbelt region of Western Australia.

Cygnus is an exploration company that focuses on the development of base metals and gold

deposits in the South west Yilgarn of Western Australia. The company is managing the

exploration of two joint ventures with Gold resources limited and significant earn in

agreements (Cygnusgold.com 2019). The application of audit risk model for assessing the

inherent risk and control is demonstrated in the paper. For the development of audit program

for Cygnus, substantive and analytical procedures have been adopted that helps in

identification of the account balances that are material. A comprehensive set of audit work

for each of the material account balances identified has been addressed in the context of

assertions so that there is a generation of appropriate audit evidences. The audit program also

incorporates the development of sampling plan for each of the identified material accounts

balances that have been tested.

Discussion:

Understanding the nature of business entity:

The discovery of base metal deposits and high grade gold has been targeted by

Cygnus within the Southwest Terrane of Western Australia. Most advanced exploration

project of Cygnus is Stanley project that comprise of an area of approximately 160 km2. The

initial diamond drilling program was followed by Cygnus by targeting the basement

extension of gold mineralization and high grade zone as well as targeting on the Stanley Hills

and Brays prospects. A detailed ground gravity survey that targeted relatively dense massive

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DEVELOPING AN AUDIT PROGRAM FOR SELECTED PUBLICALLY LISTED

COMPANY

sulfides was completed by Cygnus. In order to identify the additional conducive targets

representing the accumulation of massive sulfides and screening the prospective gravity

anomalies, the company is engaged in the collection of Airborne Electromagnetic (AEM)

survey. In addition to this, a new tenement over the Bonnie rock prospect was applied by the

company and the exploration of Bonnie rock would be commenced after the grant of

tenement. Furthermore, a new joint venture was announced by the company in the early 2018

over the Yandina project with Gold road. Therefore, the key nature of the entity is to

systematically explore the key assets, engage in the advance exploration, managing the

projects in accordance with the relevant joint venture agreements (Cannon and Bedard 2016).

They are also engaged in the acquisition, exploration and joint venture opportunities by

implementing the growth strategy.

Identification of key business risk:

The performance of Cygnus limited is affected by some of the risks that are listed

below:

Liquidity risk- The risk of liquidity arises from the possibility of the failure of the

company to meet its obligations in relation to the financial liabilities and difficulty in settling

the debts. Liquidity risk is managed by investing in surplus cash, monitoring cash flow and

comparing the realization profile of financial assets with the maturity profile of financial

liabilities.

Currency risk- The Company is exposed to considerable currency risk on the

transactions that are not denominated in a currency other than the respective functional

currencies.

COMPANY

sulfides was completed by Cygnus. In order to identify the additional conducive targets

representing the accumulation of massive sulfides and screening the prospective gravity

anomalies, the company is engaged in the collection of Airborne Electromagnetic (AEM)

survey. In addition to this, a new tenement over the Bonnie rock prospect was applied by the

company and the exploration of Bonnie rock would be commenced after the grant of

tenement. Furthermore, a new joint venture was announced by the company in the early 2018

over the Yandina project with Gold road. Therefore, the key nature of the entity is to

systematically explore the key assets, engage in the advance exploration, managing the

projects in accordance with the relevant joint venture agreements (Cannon and Bedard 2016).

They are also engaged in the acquisition, exploration and joint venture opportunities by

implementing the growth strategy.

Identification of key business risk:

The performance of Cygnus limited is affected by some of the risks that are listed

below:

Liquidity risk- The risk of liquidity arises from the possibility of the failure of the

company to meet its obligations in relation to the financial liabilities and difficulty in settling

the debts. Liquidity risk is managed by investing in surplus cash, monitoring cash flow and

comparing the realization profile of financial assets with the maturity profile of financial

liabilities.

Currency risk- The Company is exposed to considerable currency risk on the

transactions that are not denominated in a currency other than the respective functional

currencies.

DEVELOPING AN AUDIT PROGRAM FOR SELECTED PUBLICALLY LISTED

COMPANY

Market risk- The value of holdings of the financial instruments and income of the

company is impacted by the change in the market prices such as interest rate and foreign

exchange rates.

Interest rate risk- The Company is exposed to market risk for any changes in the rate

of interest and such risk is attributable to the cash of the company. Cash of the company earn

variable interest in the range between 1.05% and 2.05% and the cash comprising of cheque

accounts and term deposits.

The risk of material misstatements in the financial report of Cygnus Gold limited has

been assessed with the help of audit risk model that requires identification of control and

inherent risk. Control and inherent risk are independent of the auditor whereas detection and

audit risk are related to the auditor. The inherent and control risks is influenced by number of

factors such as the competitive environment in which the business conducts its operation and

the nature of business entity that exposes it to different risks. Inherent risk is the risk to the

assertion of material misstatements without accounting for internal control. The performance

of the company is impacted by some unknown and known risk. Some of the inherent risk

include market risk, interest risk and currency risks faced by the company. However, for the

items such as trade payables and loans, risk associated with credit, market and liquidity risk

are not considered material. Control risk is dependent upon the internal control system of

Cygnus gold limited and it has been found that the exposures to market risk within the

acceptable parameters is managed by the market risk management. In addition to this, for the

arrangements to the liabilities and assets, there is a joint control brought by the joint

arrangements. The development of internal control is considered necessary for ensuing the

true and fair preparation of the financial statements and free from any material misstatements

(Endaya and Hanefah 2016).

COMPANY

Market risk- The value of holdings of the financial instruments and income of the

company is impacted by the change in the market prices such as interest rate and foreign

exchange rates.

Interest rate risk- The Company is exposed to market risk for any changes in the rate

of interest and such risk is attributable to the cash of the company. Cash of the company earn

variable interest in the range between 1.05% and 2.05% and the cash comprising of cheque

accounts and term deposits.

The risk of material misstatements in the financial report of Cygnus Gold limited has

been assessed with the help of audit risk model that requires identification of control and

inherent risk. Control and inherent risk are independent of the auditor whereas detection and

audit risk are related to the auditor. The inherent and control risks is influenced by number of

factors such as the competitive environment in which the business conducts its operation and

the nature of business entity that exposes it to different risks. Inherent risk is the risk to the

assertion of material misstatements without accounting for internal control. The performance

of the company is impacted by some unknown and known risk. Some of the inherent risk

include market risk, interest risk and currency risks faced by the company. However, for the

items such as trade payables and loans, risk associated with credit, market and liquidity risk

are not considered material. Control risk is dependent upon the internal control system of

Cygnus gold limited and it has been found that the exposures to market risk within the

acceptable parameters is managed by the market risk management. In addition to this, for the

arrangements to the liabilities and assets, there is a joint control brought by the joint

arrangements. The development of internal control is considered necessary for ensuing the

true and fair preparation of the financial statements and free from any material misstatements

(Endaya and Hanefah 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DEVELOPING AN AUDIT PROGRAM FOR SELECTED PUBLICALLY LISTED

COMPANY

The total amount of risk measured by audit risk is determined using audit risk model

that gives an overall description of the risks faced by Cygnus gold limited. The mathematical

formula used for computing the audit risk faced by the company is given by:

Audit risk= Control risk * Inherent risk * detection risk

Cygnus gold faces some inherent risk due to the existence of some inherent factors

impacting the subjective judgment and accounting estimates used in different accounting

treatments. Some of the inherent risks include exposure to market risk, interest rate risk and

liquidity risk impacting various financial instruments of the company (Griffith et al. 2015). In

addition to this, it has been ascertained from that the internal control system of the company

is effective on handing the control activities and all the different perspective actions and risks

associated have been accounted by the auditors for forming an opinion on the financial

statements. If the overall audit risk of Cygnus Gold limited is set in the range of 10% by the

auditors of the company and the control and inherent risk is determined at 60% and 50%.

Then, detection risk is determined using the audit risk model and the value comes to 0.33

(0.1= 0.6* 0.5* Detection risk). Therefore, from the figures, it can be deduced that the

occurrence of error on part of the auditors to identify the material misstatement is lower as

against control and inherent risk faced by the company. The assessment of control and

inherent risk can be applied as higher risk rating compared to overall audit risk faced.

Assessing risk of material misstatements:

One of the important concepts in auditing is materiality as it helps in the preparation

of the financial statements in a true and fair manner. Materiality is also influenced by the

perception of the users of the financial statements. For limiting the inherent risk in the

process of auditing, auditors account for judgment in the materiality. The information

produced in the financial report is not materially impacted by any new information as the

COMPANY

The total amount of risk measured by audit risk is determined using audit risk model

that gives an overall description of the risks faced by Cygnus gold limited. The mathematical

formula used for computing the audit risk faced by the company is given by:

Audit risk= Control risk * Inherent risk * detection risk

Cygnus gold faces some inherent risk due to the existence of some inherent factors

impacting the subjective judgment and accounting estimates used in different accounting

treatments. Some of the inherent risks include exposure to market risk, interest rate risk and

liquidity risk impacting various financial instruments of the company (Griffith et al. 2015). In

addition to this, it has been ascertained from that the internal control system of the company

is effective on handing the control activities and all the different perspective actions and risks

associated have been accounted by the auditors for forming an opinion on the financial

statements. If the overall audit risk of Cygnus Gold limited is set in the range of 10% by the

auditors of the company and the control and inherent risk is determined at 60% and 50%.

Then, detection risk is determined using the audit risk model and the value comes to 0.33

(0.1= 0.6* 0.5* Detection risk). Therefore, from the figures, it can be deduced that the

occurrence of error on part of the auditors to identify the material misstatement is lower as

against control and inherent risk faced by the company. The assessment of control and

inherent risk can be applied as higher risk rating compared to overall audit risk faced.

Assessing risk of material misstatements:

One of the important concepts in auditing is materiality as it helps in the preparation

of the financial statements in a true and fair manner. Materiality is also influenced by the

perception of the users of the financial statements. For limiting the inherent risk in the

process of auditing, auditors account for judgment in the materiality. The information

produced in the financial report is not materially impacted by any new information as the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DEVELOPING AN AUDIT PROGRAM FOR SELECTED PUBLICALLY LISTED

COMPANY

company is not aware of the same. The material revenue has not been derived by the

company after the implementation of new standard that is AASB 15 revenue from the

contracts with the customers and the adoption of the standard has not materially impacted the

financial instruments (Boughey and McKenna 2017). The impact of discounting is considered

immaterial and there has been omission of discounting factor. As the time value of money is

considered material, discounting of provisions are done at their present value. In addition to

this, it is observed from the financial report of Cygnus gold that the auditors have view that

the information presented in the financial report is materially consistent with the financial

statements that is there is no material misstatement of the information.

Performing analytical procedures of the financial position statement:

The financial performance of Cygnus Gold limited have been evaluated by

performing the analytical procedures using the ratio analysis tool. Using this procedures,

auditor is able to gain an understanding of the riskiness of operations of specific area and

assist in framing opinion about the financial position of the company (Appelbaum et al.

2018). Some of the financial metrics which has been used for evaluating the performance

include profitability, liquidity, efficiency and solvency. The solvency, efficiency, profitability

and liquidity position of Cygnus gold has been evaluated by computing ratios that are

presented in the table below:

(see appendix for

calculations)

2018 2017 2016

Operating profit/loss

margin

-484.36% -24056.44%

-6342.72%

Return on equity -11.34% -11.88% -9.37%

COMPANY

company is not aware of the same. The material revenue has not been derived by the

company after the implementation of new standard that is AASB 15 revenue from the

contracts with the customers and the adoption of the standard has not materially impacted the

financial instruments (Boughey and McKenna 2017). The impact of discounting is considered

immaterial and there has been omission of discounting factor. As the time value of money is

considered material, discounting of provisions are done at their present value. In addition to

this, it is observed from the financial report of Cygnus gold that the auditors have view that

the information presented in the financial report is materially consistent with the financial

statements that is there is no material misstatement of the information.

Performing analytical procedures of the financial position statement:

The financial performance of Cygnus Gold limited have been evaluated by

performing the analytical procedures using the ratio analysis tool. Using this procedures,

auditor is able to gain an understanding of the riskiness of operations of specific area and

assist in framing opinion about the financial position of the company (Appelbaum et al.

2018). Some of the financial metrics which has been used for evaluating the performance

include profitability, liquidity, efficiency and solvency. The solvency, efficiency, profitability

and liquidity position of Cygnus gold has been evaluated by computing ratios that are

presented in the table below:

(see appendix for

calculations)

2018 2017 2016

Operating profit/loss

margin

-484.36% -24056.44%

-6342.72%

Return on equity -11.34% -11.88% -9.37%

DEVELOPING AN AUDIT PROGRAM FOR SELECTED PUBLICALLY LISTED

COMPANY

Gross profit/loss

margin

-484.36% -24056.44% -6342.72%

The profitability position of Cygnus gold has been evaluated by using the analytical

procedure of computing operating profit margin, gross profit margin and return on equity. It

can be observed from the table that operating loss margin increased in year 2017 and

decreased in 2018 and this decrease in loss generated is due to increase in revenue in the

current year. Return on equity on other hand has declined year on year indicating that the

employment of capital has resulted in creation of loss. Looking at the figures of gross loss, it

is observed that the gross loss has increased in year 2017 and it fell in year 2018 implying

that company is not left to cover for financing, operating and other costs. However, the

condition has improved in year 2018 due to increase in amount of revenue.

(see appendix for calculations) 2018 2017 2016

Total Asset turnover 0.02 0.0005 0.0014

Debtor turnover 1.82 0.01 0.17

Working capital ratio 5.92 13.30 13.20

The above table presents the efficiency figures of the company by computing debtor

turnover, total asset turnover and working capital ratio. Total asset turnover of Cygnus Gold

has increased indicating that the company has been efficient in utilizing its assets for

generating sales. Debtor turnover has increased in year 2018 and this has implication of the

fact that the company has better cash position as they are collecting cash more frequently

COMPANY

Gross profit/loss

margin

-484.36% -24056.44% -6342.72%

The profitability position of Cygnus gold has been evaluated by using the analytical

procedure of computing operating profit margin, gross profit margin and return on equity. It

can be observed from the table that operating loss margin increased in year 2017 and

decreased in 2018 and this decrease in loss generated is due to increase in revenue in the

current year. Return on equity on other hand has declined year on year indicating that the

employment of capital has resulted in creation of loss. Looking at the figures of gross loss, it

is observed that the gross loss has increased in year 2017 and it fell in year 2018 implying

that company is not left to cover for financing, operating and other costs. However, the

condition has improved in year 2018 due to increase in amount of revenue.

(see appendix for calculations) 2018 2017 2016

Total Asset turnover 0.02 0.0005 0.0014

Debtor turnover 1.82 0.01 0.17

Working capital ratio 5.92 13.30 13.20

The above table presents the efficiency figures of the company by computing debtor

turnover, total asset turnover and working capital ratio. Total asset turnover of Cygnus Gold

has increased indicating that the company has been efficient in utilizing its assets for

generating sales. Debtor turnover has increased in year 2018 and this has implication of the

fact that the company has better cash position as they are collecting cash more frequently

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DEVELOPING AN AUDIT PROGRAM FOR SELECTED PUBLICALLY LISTED

COMPANY

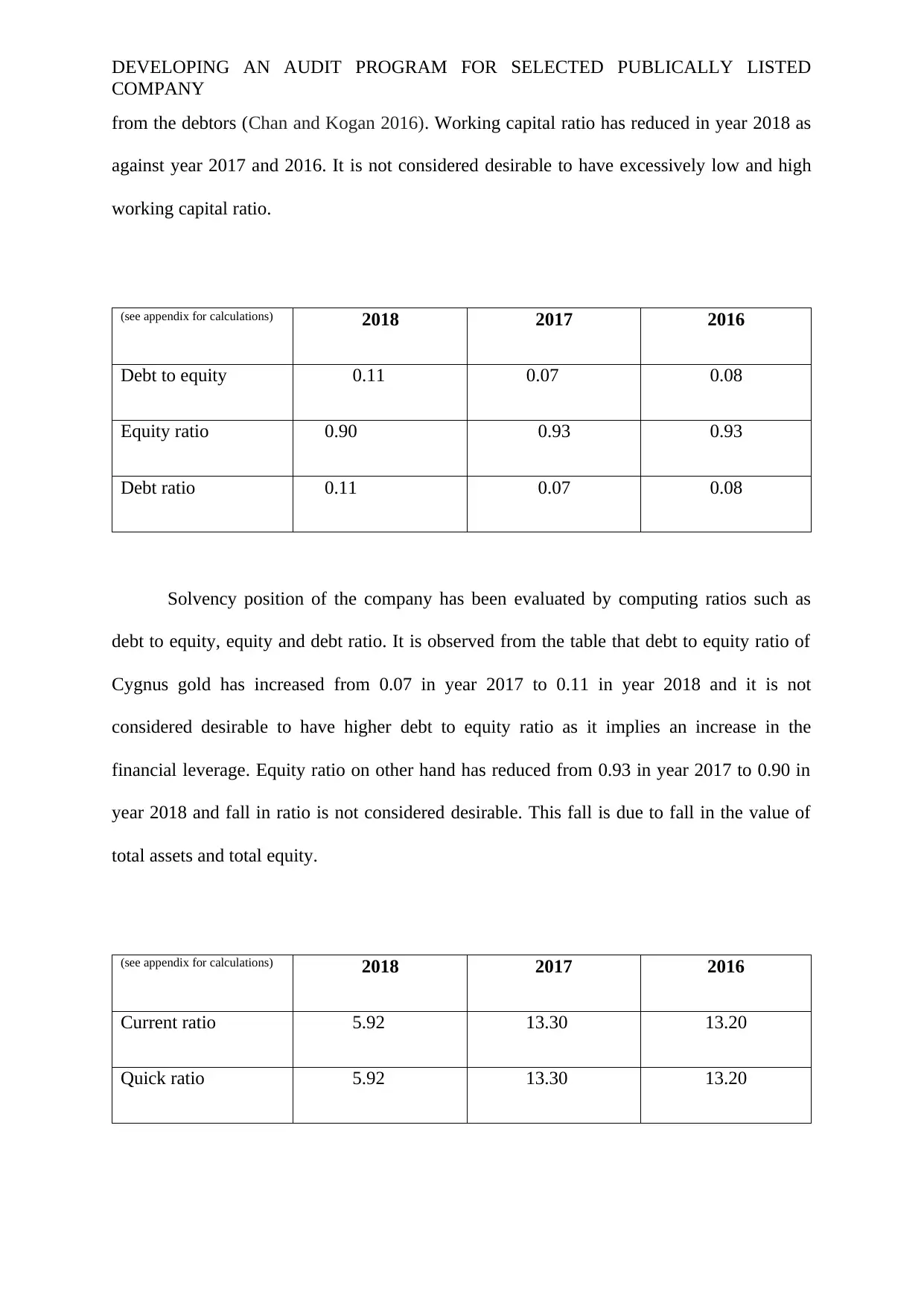

from the debtors (Chan and Kogan 2016). Working capital ratio has reduced in year 2018 as

against year 2017 and 2016. It is not considered desirable to have excessively low and high

working capital ratio.

(see appendix for calculations) 2018 2017 2016

Debt to equity 0.11 0.07 0.08

Equity ratio 0.90 0.93 0.93

Debt ratio 0.11 0.07 0.08

Solvency position of the company has been evaluated by computing ratios such as

debt to equity, equity and debt ratio. It is observed from the table that debt to equity ratio of

Cygnus gold has increased from 0.07 in year 2017 to 0.11 in year 2018 and it is not

considered desirable to have higher debt to equity ratio as it implies an increase in the

financial leverage. Equity ratio on other hand has reduced from 0.93 in year 2017 to 0.90 in

year 2018 and fall in ratio is not considered desirable. This fall is due to fall in the value of

total assets and total equity.

(see appendix for calculations) 2018 2017 2016

Current ratio 5.92 13.30 13.20

Quick ratio 5.92 13.30 13.20

COMPANY

from the debtors (Chan and Kogan 2016). Working capital ratio has reduced in year 2018 as

against year 2017 and 2016. It is not considered desirable to have excessively low and high

working capital ratio.

(see appendix for calculations) 2018 2017 2016

Debt to equity 0.11 0.07 0.08

Equity ratio 0.90 0.93 0.93

Debt ratio 0.11 0.07 0.08

Solvency position of the company has been evaluated by computing ratios such as

debt to equity, equity and debt ratio. It is observed from the table that debt to equity ratio of

Cygnus gold has increased from 0.07 in year 2017 to 0.11 in year 2018 and it is not

considered desirable to have higher debt to equity ratio as it implies an increase in the

financial leverage. Equity ratio on other hand has reduced from 0.93 in year 2017 to 0.90 in

year 2018 and fall in ratio is not considered desirable. This fall is due to fall in the value of

total assets and total equity.

(see appendix for calculations) 2018 2017 2016

Current ratio 5.92 13.30 13.20

Quick ratio 5.92 13.30 13.20

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DEVELOPING AN AUDIT PROGRAM FOR SELECTED PUBLICALLY LISTED

COMPANY

Liquidity position of the company has been evaluated by computing current and quick

ratio. It is observed that current ratio of Cygnus gold has declined in 2018, though the ratio

has declined, it does not mean that the company is able to pay off its short term obligations

using current assets.

Identification of material accounts balances and computation of materiality for

planning purposes:

Material accounts

balance

Relevant financial

report assertion

Set of audit work

steps

Using sampling for

testing material

accounts balance

Revenue Completeness and

occurrence

Observing and

testing the revenue

accounts presented in

the income

statement. Next step

should involve

checking for the

issues of revenue

recognition and

assessing the

documentation

associated with the

revenue cycle.

The method used by

the auditor for

testing the revenue

account in the

income statement.

In the next step,

issues regarding

recognition of

revenue such as side

agreements and

channel stuffing are

looked for. The

occurrence of

revenue is evaluated

COMPANY

Liquidity position of the company has been evaluated by computing current and quick

ratio. It is observed that current ratio of Cygnus gold has declined in 2018, though the ratio

has declined, it does not mean that the company is able to pay off its short term obligations

using current assets.

Identification of material accounts balances and computation of materiality for

planning purposes:

Material accounts

balance

Relevant financial

report assertion

Set of audit work

steps

Using sampling for

testing material

accounts balance

Revenue Completeness and

occurrence

Observing and

testing the revenue

accounts presented in

the income

statement. Next step

should involve

checking for the

issues of revenue

recognition and

assessing the

documentation

associated with the

revenue cycle.

The method used by

the auditor for

testing the revenue

account in the

income statement.

In the next step,

issues regarding

recognition of

revenue such as side

agreements and

channel stuffing are

looked for. The

occurrence of

revenue is evaluated

DEVELOPING AN AUDIT PROGRAM FOR SELECTED PUBLICALLY LISTED

COMPANY

by selecting a

sample of revenue

accounts over the

period of two years.

Accounts receivable Occurrence

The reason for

occurrence assertion

in relation to

accounts receivable

is that it helps in

ascertaining that the

transactions recorded

has actually

occurred. Therefore,

auditor has

employed the

assertion of

occurrence for

testing accounts

receivables.

Any significant

difference is defined

by the auditors along

with the development

of an independent

expectation and

accordingly

conclusions are

drawn (Hoogduin et

al. 2015).

The notes of last

received goods is

recorded by the

auditor along with

tracing the invoices

of sales and

purchase. Auditor

uses systematic

sampling method for

selecting the

invoice.

Current assets Valuation and

existence

Current assets are

tested for valuation

and existence

A sample of current

assets is chosen and

they are verified for

their valuation using

and testing the

For evaluating the

current assets, non-

statistical sampling

method should be

adopted such as

COMPANY

by selecting a

sample of revenue

accounts over the

period of two years.

Accounts receivable Occurrence

The reason for

occurrence assertion

in relation to

accounts receivable

is that it helps in

ascertaining that the

transactions recorded

has actually

occurred. Therefore,

auditor has

employed the

assertion of

occurrence for

testing accounts

receivables.

Any significant

difference is defined

by the auditors along

with the development

of an independent

expectation and

accordingly

conclusions are

drawn (Hoogduin et

al. 2015).

The notes of last

received goods is

recorded by the

auditor along with

tracing the invoices

of sales and

purchase. Auditor

uses systematic

sampling method for

selecting the

invoice.

Current assets Valuation and

existence

Current assets are

tested for valuation

and existence

A sample of current

assets is chosen and

they are verified for

their valuation using

and testing the

For evaluating the

current assets, non-

statistical sampling

method should be

adopted such as

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.