Mortgage Broking Assignment: Financial Analysis, Risk, and Policies

VerifiedAdded on 2020/04/13

|30

|7551

|373

Homework Assignment

AI Summary

This mortgage broking assignment solution encompasses various aspects of the profession. Assignment 1 focuses on client details, including financial information, assets, liabilities, and net worth, alongside a needs analysis for a loan, covering loan purpose, facility details, security, risk assessment, and recommendations. Assignment 2 involves preparing needs analysis and proposal documents for clients, outlining loan terms and lender details. Subsequent assignments delve into complex lending requirements, information gathering, client interactions, broking solutions, and risk management. The solution also covers financial statements, including balance sheets and profit/loss statements, alongside definitions of financial instruments and risk management principles. Further, it addresses the scope of a sustainability policy, stakeholder consultation, strategy development, policy recommendations, implementation methods, and performance indicators. References are included to support the analysis and recommendations provided.

MORTGAGE BROKING

Table of Content

Table of Content

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

s

ASSIGNMENT 1......................................................................................................................................1

ASSIGNMENT 2......................................................................................................................................5

PART A THE CLIENT................................................................................................................................5

1. Prepare needs analysis and fact finding document.......................................................................5

2. Proposal Documents......................................................................................................................6

PART B THE LENDER...............................................................................................................................9

ASSIGNMENT 3....................................................................................................................................14

QUESTION 1.........................................................................................................................................14

Describe gathering of information when establishing the client’s complex lending requirements. 14

QUESTION 2.........................................................................................................................................14

Describe how you record and document your interaction with clients...........................................14

QUESTION 3.........................................................................................................................................14

Describe how you research and consider complex broking solutions based on client’s needs.......14

QUESTION 4.........................................................................................................................................15

Describe evidence of how you identify and manage risk when dealing with clients with loan

requirements...................................................................................................................................15

QUESTION 5.........................................................................................................................................16

Give example of presenting loan options to the client....................................................................16

QUESTION 6.........................................................................................................................................17

Before presentation, identify any concerns that the client may raise and what preparations was

completed to respond these concerns............................................................................................17

ASSIGNMENT 4....................................................................................................................................18

QUESTION 1.........................................................................................................................................18

PART A.................................................................................................................................................18

PART B.................................................................................................................................................19

PART C.................................................................................................................................................19

QUESTION 2.........................................................................................................................................20

A TRUST...............................................................................................................................................20

What is a Unit Trust?.......................................................................................................................20

What is a Discretionary Trust?.........................................................................................................20

What is a Hybrid Trust?...................................................................................................................20

What is a Trustee?...........................................................................................................................20

Difference between different kinds of trust....................................................................................20

ASSIGNMENT 1......................................................................................................................................1

ASSIGNMENT 2......................................................................................................................................5

PART A THE CLIENT................................................................................................................................5

1. Prepare needs analysis and fact finding document.......................................................................5

2. Proposal Documents......................................................................................................................6

PART B THE LENDER...............................................................................................................................9

ASSIGNMENT 3....................................................................................................................................14

QUESTION 1.........................................................................................................................................14

Describe gathering of information when establishing the client’s complex lending requirements. 14

QUESTION 2.........................................................................................................................................14

Describe how you record and document your interaction with clients...........................................14

QUESTION 3.........................................................................................................................................14

Describe how you research and consider complex broking solutions based on client’s needs.......14

QUESTION 4.........................................................................................................................................15

Describe evidence of how you identify and manage risk when dealing with clients with loan

requirements...................................................................................................................................15

QUESTION 5.........................................................................................................................................16

Give example of presenting loan options to the client....................................................................16

QUESTION 6.........................................................................................................................................17

Before presentation, identify any concerns that the client may raise and what preparations was

completed to respond these concerns............................................................................................17

ASSIGNMENT 4....................................................................................................................................18

QUESTION 1.........................................................................................................................................18

PART A.................................................................................................................................................18

PART B.................................................................................................................................................19

PART C.................................................................................................................................................19

QUESTION 2.........................................................................................................................................20

A TRUST...............................................................................................................................................20

What is a Unit Trust?.......................................................................................................................20

What is a Discretionary Trust?.........................................................................................................20

What is a Hybrid Trust?...................................................................................................................20

What is a Trustee?...........................................................................................................................20

Difference between different kinds of trust....................................................................................20

Provide an example of different types of Trust...............................................................................21

B COMPANY.........................................................................................................................................21

What are the legal requirements of a company?............................................................................21

What are the personal obligations of directors by law?..................................................................21

Can anyone be a director of a company?........................................................................................21

What is the minimum number of directors required?.....................................................................22

QUESTION 3.........................................................................................................................................22

What is a Balance sheet?.................................................................................................................22

What is a Profit and loss statement?...............................................................................................22

What is Depreciation?.....................................................................................................................22

What is Liquidity ratio?....................................................................................................................22

What is current ratio?......................................................................................................................22

What is Debt to equity ratio?..........................................................................................................22

What is cash flow statement?.........................................................................................................23

What is an asset?.............................................................................................................................23

What is Liability?..............................................................................................................................23

How is a Net profit determined?.....................................................................................................23

How would you define equity?........................................................................................................23

Allowable expenses under Australian taxation conditions..............................................................23

QUESTION 4.........................................................................................................................................24

Define the following........................................................................................................................24

Commercial Bank Bill.......................................................................................................................24

Invoice or Factoring finance............................................................................................................24

Chattel Mortgage.............................................................................................................................24

Asset finance product or Equipment Finance..................................................................................24

QUESTION 5.........................................................................................................................................24

List 6 risk management principles and state brief about the principle............................................24

QUESTION 6.........................................................................................................................................25

Explain the importance of categorizing all the risks........................................................................25

ASSIGNMENT 5....................................................................................................................................25

Define scope of sustainability policy................................................................................................25

Gather information from different sources to develop the policy...................................................25

Identify and consult stakeholders for the development of policy...................................................26

3

B COMPANY.........................................................................................................................................21

What are the legal requirements of a company?............................................................................21

What are the personal obligations of directors by law?..................................................................21

Can anyone be a director of a company?........................................................................................21

What is the minimum number of directors required?.....................................................................22

QUESTION 3.........................................................................................................................................22

What is a Balance sheet?.................................................................................................................22

What is a Profit and loss statement?...............................................................................................22

What is Depreciation?.....................................................................................................................22

What is Liquidity ratio?....................................................................................................................22

What is current ratio?......................................................................................................................22

What is Debt to equity ratio?..........................................................................................................22

What is cash flow statement?.........................................................................................................23

What is an asset?.............................................................................................................................23

What is Liability?..............................................................................................................................23

How is a Net profit determined?.....................................................................................................23

How would you define equity?........................................................................................................23

Allowable expenses under Australian taxation conditions..............................................................23

QUESTION 4.........................................................................................................................................24

Define the following........................................................................................................................24

Commercial Bank Bill.......................................................................................................................24

Invoice or Factoring finance............................................................................................................24

Chattel Mortgage.............................................................................................................................24

Asset finance product or Equipment Finance..................................................................................24

QUESTION 5.........................................................................................................................................24

List 6 risk management principles and state brief about the principle............................................24

QUESTION 6.........................................................................................................................................25

Explain the importance of categorizing all the risks........................................................................25

ASSIGNMENT 5....................................................................................................................................25

Define scope of sustainability policy................................................................................................25

Gather information from different sources to develop the policy...................................................25

Identify and consult stakeholders for the development of policy...................................................26

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Craft strategies for decreasing use of reducing toxic material and hazardous chemical use and

employing life cycle management approaches................................................................................26

Make recommendations for policy options based on likely effectiveness, time and cost...............26

Develop policy that reflects the organisation’s commitment to sustainability as an integral aspect

.........................................................................................................................................................26

Methods of implementation and performance indicators..............................................................27

Promote workplace sustainability policy.........................................................................................27

Inform those involved in implementing the policy about the expected outcome...........................27

Develop and communicate procedures to implement workplace sustainable policy......................27

Execute strategies for continuous improvement.............................................................................27

Establish and assign responsibility for recording systems...............................................................27

Document Outcomes and provide feedback to key personnel and stakeholders...........................27

Monitor records to identify trends that may require remedial action and promote continuous

improvement of performance.........................................................................................................28

Modify policy or procedures as required to ensure improvements are made................................28

REFERENCES........................................................................................................................................29

4

employing life cycle management approaches................................................................................26

Make recommendations for policy options based on likely effectiveness, time and cost...............26

Develop policy that reflects the organisation’s commitment to sustainability as an integral aspect

.........................................................................................................................................................26

Methods of implementation and performance indicators..............................................................27

Promote workplace sustainability policy.........................................................................................27

Inform those involved in implementing the policy about the expected outcome...........................27

Develop and communicate procedures to implement workplace sustainable policy......................27

Execute strategies for continuous improvement.............................................................................27

Establish and assign responsibility for recording systems...............................................................27

Document Outcomes and provide feedback to key personnel and stakeholders...........................27

Monitor records to identify trends that may require remedial action and promote continuous

improvement of performance.........................................................................................................28

Modify policy or procedures as required to ensure improvements are made................................28

REFERENCES........................................................................................................................................29

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

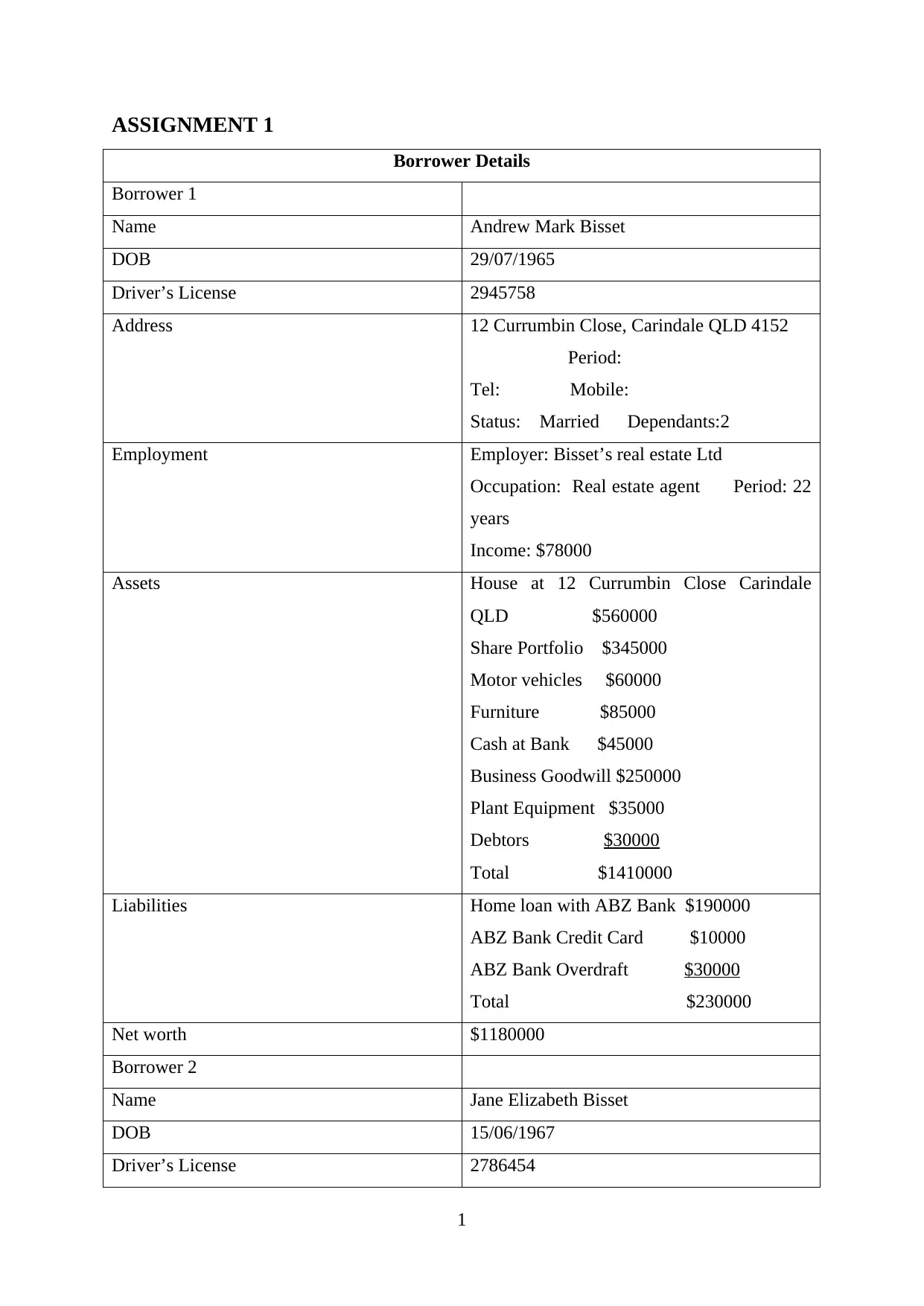

ASSIGNMENT 1

Borrower Details

Borrower 1

Name Andrew Mark Bisset

DOB 29/07/1965

Driver’s License 2945758

Address 12 Currumbin Close, Carindale QLD 4152

Period:

Tel: Mobile:

Status: Married Dependants:2

Employment Employer: Bisset’s real estate Ltd

Occupation: Real estate agent Period: 22

years

Income: $78000

Assets House at 12 Currumbin Close Carindale

QLD $560000

Share Portfolio $345000

Motor vehicles $60000

Furniture $85000

Cash at Bank $45000

Business Goodwill $250000

Plant Equipment $35000

Debtors $30000

Total $1410000

Liabilities Home loan with ABZ Bank $190000

ABZ Bank Credit Card $10000

ABZ Bank Overdraft $30000

Total $230000

Net worth $1180000

Borrower 2

Name Jane Elizabeth Bisset

DOB 15/06/1967

Driver’s License 2786454

1

Borrower Details

Borrower 1

Name Andrew Mark Bisset

DOB 29/07/1965

Driver’s License 2945758

Address 12 Currumbin Close, Carindale QLD 4152

Period:

Tel: Mobile:

Status: Married Dependants:2

Employment Employer: Bisset’s real estate Ltd

Occupation: Real estate agent Period: 22

years

Income: $78000

Assets House at 12 Currumbin Close Carindale

QLD $560000

Share Portfolio $345000

Motor vehicles $60000

Furniture $85000

Cash at Bank $45000

Business Goodwill $250000

Plant Equipment $35000

Debtors $30000

Total $1410000

Liabilities Home loan with ABZ Bank $190000

ABZ Bank Credit Card $10000

ABZ Bank Overdraft $30000

Total $230000

Net worth $1180000

Borrower 2

Name Jane Elizabeth Bisset

DOB 15/06/1967

Driver’s License 2786454

1

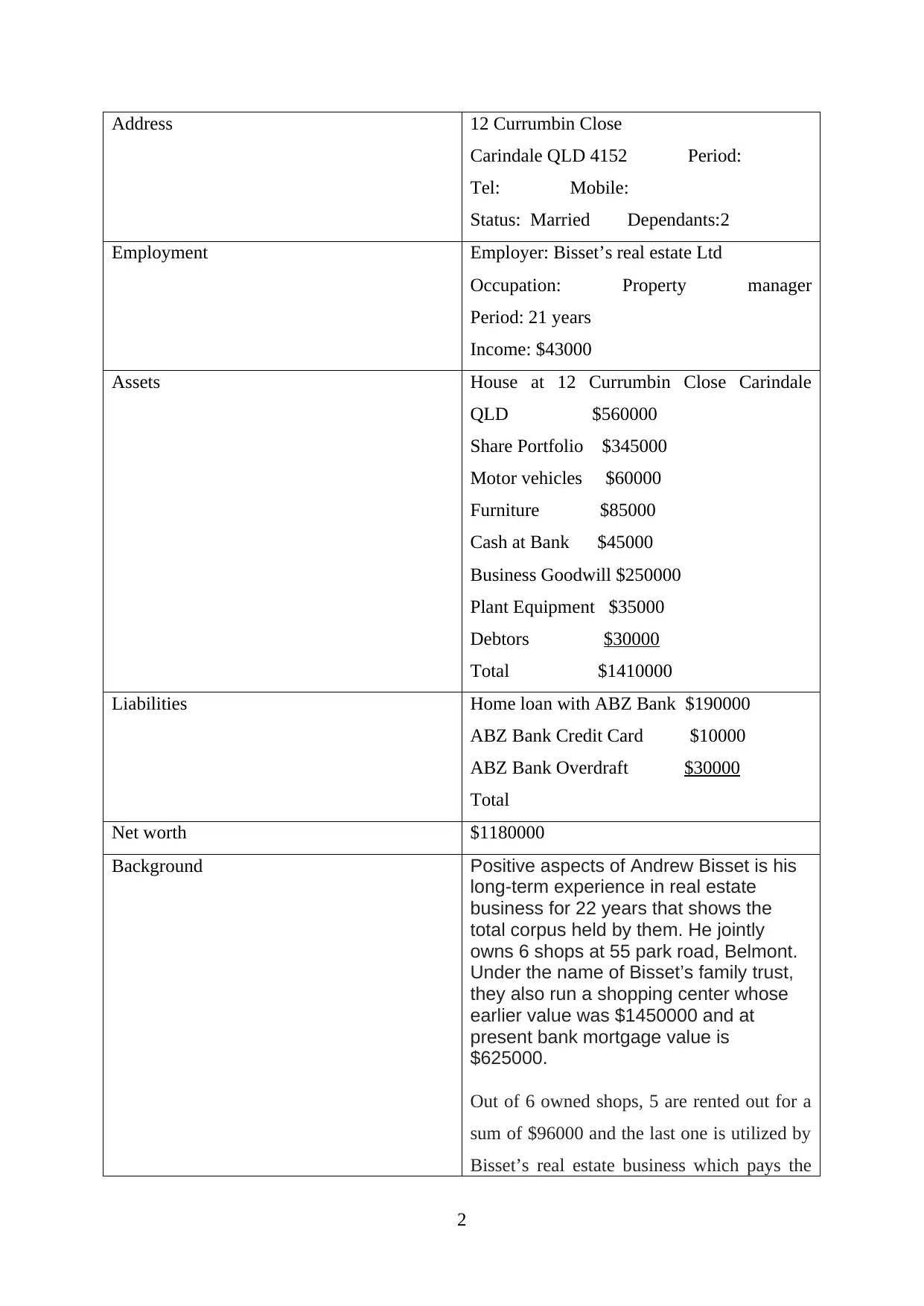

Address 12 Currumbin Close

Carindale QLD 4152 Period:

Tel: Mobile:

Status: Married Dependants:2

Employment Employer: Bisset’s real estate Ltd

Occupation: Property manager

Period: 21 years

Income: $43000

Assets House at 12 Currumbin Close Carindale

QLD $560000

Share Portfolio $345000

Motor vehicles $60000

Furniture $85000

Cash at Bank $45000

Business Goodwill $250000

Plant Equipment $35000

Debtors $30000

Total $1410000

Liabilities Home loan with ABZ Bank $190000

ABZ Bank Credit Card $10000

ABZ Bank Overdraft $30000

Total

Net worth $1180000

Background Positive aspects of Andrew Bisset is his

long-term experience in real estate

business for 22 years that shows the

total corpus held by them. He jointly

owns 6 shops at 55 park road, Belmont.

Under the name of Bisset’s family trust,

they also run a shopping center whose

earlier value was $1450000 and at

present bank mortgage value is

$625000.

Out of 6 owned shops, 5 are rented out for a

sum of $96000 and the last one is utilized by

Bisset’s real estate business which pays the

2

Carindale QLD 4152 Period:

Tel: Mobile:

Status: Married Dependants:2

Employment Employer: Bisset’s real estate Ltd

Occupation: Property manager

Period: 21 years

Income: $43000

Assets House at 12 Currumbin Close Carindale

QLD $560000

Share Portfolio $345000

Motor vehicles $60000

Furniture $85000

Cash at Bank $45000

Business Goodwill $250000

Plant Equipment $35000

Debtors $30000

Total $1410000

Liabilities Home loan with ABZ Bank $190000

ABZ Bank Credit Card $10000

ABZ Bank Overdraft $30000

Total

Net worth $1180000

Background Positive aspects of Andrew Bisset is his

long-term experience in real estate

business for 22 years that shows the

total corpus held by them. He jointly

owns 6 shops at 55 park road, Belmont.

Under the name of Bisset’s family trust,

they also run a shopping center whose

earlier value was $1450000 and at

present bank mortgage value is

$625000.

Out of 6 owned shops, 5 are rented out for a

sum of $96000 and the last one is utilized by

Bisset’s real estate business which pays the

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

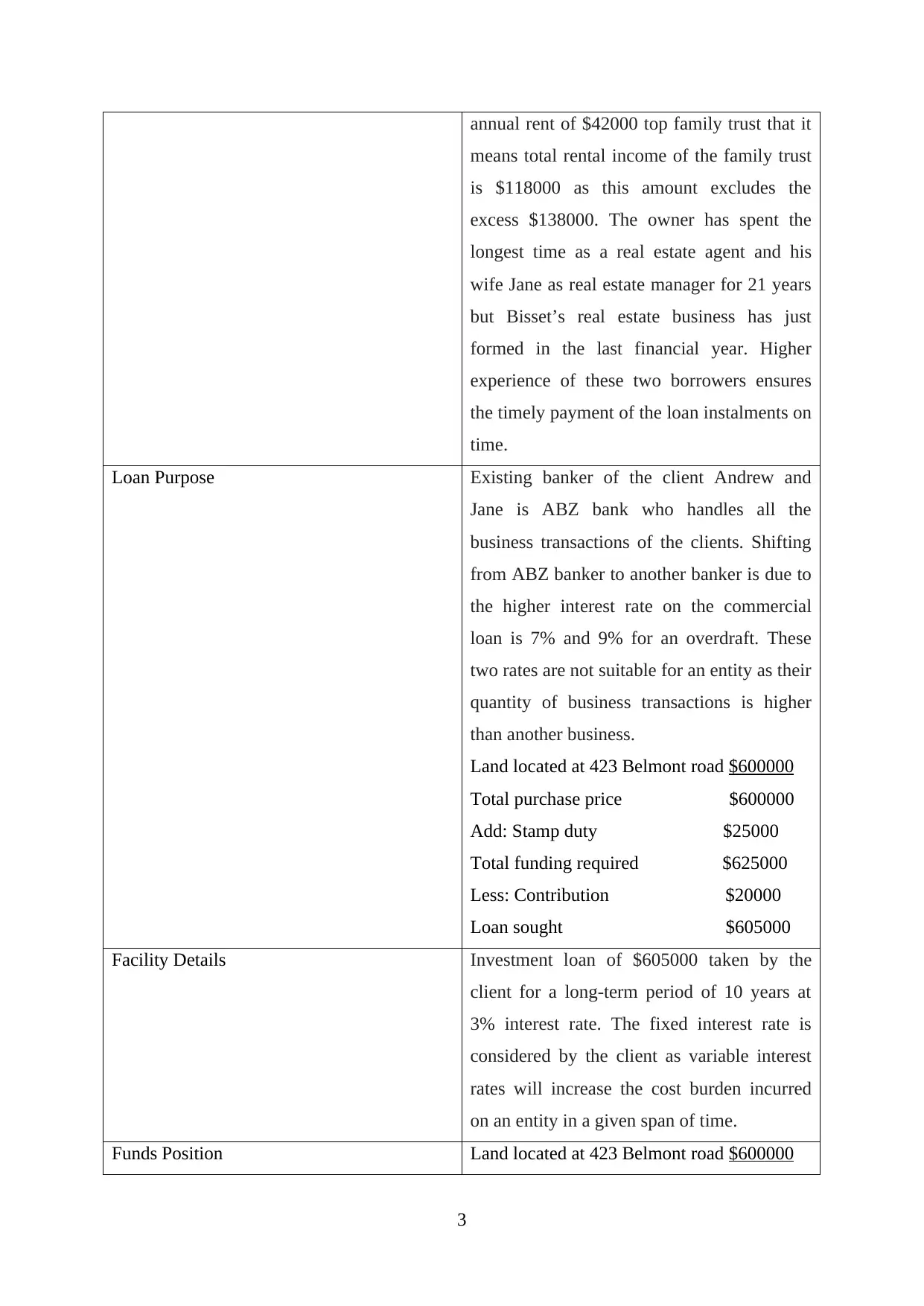

annual rent of $42000 top family trust that it

means total rental income of the family trust

is $118000 as this amount excludes the

excess $138000. The owner has spent the

longest time as a real estate agent and his

wife Jane as real estate manager for 21 years

but Bisset’s real estate business has just

formed in the last financial year. Higher

experience of these two borrowers ensures

the timely payment of the loan instalments on

time.

Loan Purpose Existing banker of the client Andrew and

Jane is ABZ bank who handles all the

business transactions of the clients. Shifting

from ABZ banker to another banker is due to

the higher interest rate on the commercial

loan is 7% and 9% for an overdraft. These

two rates are not suitable for an entity as their

quantity of business transactions is higher

than another business.

Land located at 423 Belmont road $600000

Total purchase price $600000

Add: Stamp duty $25000

Total funding required $625000

Less: Contribution $20000

Loan sought $605000

Facility Details Investment loan of $605000 taken by the

client for a long-term period of 10 years at

3% interest rate. The fixed interest rate is

considered by the client as variable interest

rates will increase the cost burden incurred

on an entity in a given span of time.

Funds Position Land located at 423 Belmont road $600000

3

means total rental income of the family trust

is $118000 as this amount excludes the

excess $138000. The owner has spent the

longest time as a real estate agent and his

wife Jane as real estate manager for 21 years

but Bisset’s real estate business has just

formed in the last financial year. Higher

experience of these two borrowers ensures

the timely payment of the loan instalments on

time.

Loan Purpose Existing banker of the client Andrew and

Jane is ABZ bank who handles all the

business transactions of the clients. Shifting

from ABZ banker to another banker is due to

the higher interest rate on the commercial

loan is 7% and 9% for an overdraft. These

two rates are not suitable for an entity as their

quantity of business transactions is higher

than another business.

Land located at 423 Belmont road $600000

Total purchase price $600000

Add: Stamp duty $25000

Total funding required $625000

Less: Contribution $20000

Loan sought $605000

Facility Details Investment loan of $605000 taken by the

client for a long-term period of 10 years at

3% interest rate. The fixed interest rate is

considered by the client as variable interest

rates will increase the cost burden incurred

on an entity in a given span of time.

Funds Position Land located at 423 Belmont road $600000

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total purchase price $600000

Proposed Loan $605000

Borrower’s equity $5000

LVR= 99.17%

Servicing capability Debt service coverage ratio

Profit after tax

Net profit* (1-30%)

$50000*(1-30%)

= $35000

Interest $52000

Depreciation $25000

DSCR= PAT+Depreciation+Interest/ Interest

= $35000+52000+25000/52000

= $112000/$52000

= 2.15

Higher debt service coverage shows the

caliber of an entity in paying off all their

debts with the available income held by an

entity.

Security Existing property held by Andrew and Jane

utilize as a collateral security in meeting

higher debt incurred by the business concern.

The shopping centre, 55 park road, Belmont

QLD 4171, Lot 43 on RP 9542, Zoning

commercial and Area of 1850 are existing

property held by the client used as a

collateral security.

Risk assessment and management The clients have good credit history as they

have taken home loan from ABZ bank and

bank overdraft secured by their residence for

$40000. The capacity of Andrew and Jane is

higher as they have salary income, rental

income, and partnership income to meet their

4

Proposed Loan $605000

Borrower’s equity $5000

LVR= 99.17%

Servicing capability Debt service coverage ratio

Profit after tax

Net profit* (1-30%)

$50000*(1-30%)

= $35000

Interest $52000

Depreciation $25000

DSCR= PAT+Depreciation+Interest/ Interest

= $35000+52000+25000/52000

= $112000/$52000

= 2.15

Higher debt service coverage shows the

caliber of an entity in paying off all their

debts with the available income held by an

entity.

Security Existing property held by Andrew and Jane

utilize as a collateral security in meeting

higher debt incurred by the business concern.

The shopping centre, 55 park road, Belmont

QLD 4171, Lot 43 on RP 9542, Zoning

commercial and Area of 1850 are existing

property held by the client used as a

collateral security.

Risk assessment and management The clients have good credit history as they

have taken home loan from ABZ bank and

bank overdraft secured by their residence for

$40000. The capacity of Andrew and Jane is

higher as they have salary income, rental

income, and partnership income to meet their

4

future obligations. Ownership of residence

and shops will act as a collateral security.

Recommendations Joint ownership of shops to ensure

higher earnings

Good credit history of the borrowers

Net surplus of the borrower is

$1180000.

Available cash at bank of $45000

Higher Debt service coverage ratio of

2.15

Higher rental receipts of $138000

Existing properties held by all the

individuals Represents good source of

income

Attachments Serviceability assessment

Identity card of the client

Bank Statements of Andrew and Jane

Property papers of Bisset’s real estate,

and family trust

Copy of home loan statements

Copy of borrower’s income

Copy of credit card statements

Copy of bank overdraft

Partnership deed

Rental income copy

ASSIGNMENT 2

PART A THE CLIENT

1. Prepare needs analysis and fact finding document

What type of loan you want to take?

What is the maximum period of loan you want to take?

Do you choose variable or fixed interest rate and why?

From which sources, do you earn income?

5

and shops will act as a collateral security.

Recommendations Joint ownership of shops to ensure

higher earnings

Good credit history of the borrowers

Net surplus of the borrower is

$1180000.

Available cash at bank of $45000

Higher Debt service coverage ratio of

2.15

Higher rental receipts of $138000

Existing properties held by all the

individuals Represents good source of

income

Attachments Serviceability assessment

Identity card of the client

Bank Statements of Andrew and Jane

Property papers of Bisset’s real estate,

and family trust

Copy of home loan statements

Copy of borrower’s income

Copy of credit card statements

Copy of bank overdraft

Partnership deed

Rental income copy

ASSIGNMENT 2

PART A THE CLIENT

1. Prepare needs analysis and fact finding document

What type of loan you want to take?

What is the maximum period of loan you want to take?

Do you choose variable or fixed interest rate and why?

From which sources, do you earn income?

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Do you find stable or decreasing financial position of your firm?

What is the current interest rate of your loan and how you compare the current interest

rate with the earlier loan?

Do you think your current loan is better than your previous loan?

What additional fees you need to pay for the current loan?

Are you confident about the decreasing of debt over the years or not?

2. Proposal Documents

Submission for the client

To- Ray Henley and Steve Manning

Subject- Commercial Equipment Finance

From- XYZ broker

Date- 29-11-2017

Hi Ray and Steve,

This is to inform that your loan application has assessed after analyzing your firm’s

financial position to ensure the future cost compensation by you people. You run a successful

business of transportation with wide client’s base located in a conscious management

strategy. Payment terms and contract deadline is set as 30 days term period. They have

trading experience in this sector for 34 months with the solid business plan.

Security

They have seed capital of 500k taken from a private investor on a guaranteed return of

45k annually for a term of 5 years. Principal instalment payment of 100k annually along with

Owner occupied the property of $850000 with credit card limit of $25000, superannuation

$550000 and a motor vehicle worth $40000. Steve manning’s occupied the property of

$500000, credit card limit of $10000, superannuation worth $1500000 and motor vehicle of

$25000. Common cash account for their business is $25000.

Facility

6

What is the current interest rate of your loan and how you compare the current interest

rate with the earlier loan?

Do you think your current loan is better than your previous loan?

What additional fees you need to pay for the current loan?

Are you confident about the decreasing of debt over the years or not?

2. Proposal Documents

Submission for the client

To- Ray Henley and Steve Manning

Subject- Commercial Equipment Finance

From- XYZ broker

Date- 29-11-2017

Hi Ray and Steve,

This is to inform that your loan application has assessed after analyzing your firm’s

financial position to ensure the future cost compensation by you people. You run a successful

business of transportation with wide client’s base located in a conscious management

strategy. Payment terms and contract deadline is set as 30 days term period. They have

trading experience in this sector for 34 months with the solid business plan.

Security

They have seed capital of 500k taken from a private investor on a guaranteed return of

45k annually for a term of 5 years. Principal instalment payment of 100k annually along with

Owner occupied the property of $850000 with credit card limit of $25000, superannuation

$550000 and a motor vehicle worth $40000. Steve manning’s occupied the property of

$500000, credit card limit of $10000, superannuation worth $1500000 and motor vehicle of

$25000. Common cash account for their business is $25000.

Facility

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Current loan application of Ray and Steve is for commercial equipment

finance raised through this loan. This equipment finance has arranged to expand it’s in the

future to increase the overall earnings. Actual limit of the equipment finance is 500k to

purchase trucks and dog trailers. This loan is requiring in funding the lease of the second

depot at cost of $6000 per month to retain the current depot.

Lender details

A future plan of the client is to acquire Henman transportation to boost the current

earnings of the business concern. It is recommended to the client to convince the lender in

investing their business to get the desired return in exchange. They have two option available

to them includes meeting the leasing costs or arranging the whole sum of 500k for the

expansion projects.

Confirmation of requirements

Approval of the overall requirements of the ray and Steve to purchase the commercial

equipment finance of 500k for the expansion project will be approved by analyzing the entire

performance of the clients. A broker will give quotations of all loan offers by different

lenders to consider the best suitable loan as per the current position of an enterprise.

Personnel

Financial advisor of the Ray and Steve play an important role in guiding the business

towards the best suitable path to get the desired return over the years. Acquisition of Henman

transport is a result of the advice of the accountants who assess the financial performance of

the business.

Process

The current process is use to arrange the finance from the lender within 5-15 working

days.

Generate reliable information and required documentation from the clients

Provide proposal documents to client along with broker’s recommendations

File completed application to the lender to seek their consent

Lender investigates credit history of the client and confirms the loan application

7

finance raised through this loan. This equipment finance has arranged to expand it’s in the

future to increase the overall earnings. Actual limit of the equipment finance is 500k to

purchase trucks and dog trailers. This loan is requiring in funding the lease of the second

depot at cost of $6000 per month to retain the current depot.

Lender details

A future plan of the client is to acquire Henman transportation to boost the current

earnings of the business concern. It is recommended to the client to convince the lender in

investing their business to get the desired return in exchange. They have two option available

to them includes meeting the leasing costs or arranging the whole sum of 500k for the

expansion projects.

Confirmation of requirements

Approval of the overall requirements of the ray and Steve to purchase the commercial

equipment finance of 500k for the expansion project will be approved by analyzing the entire

performance of the clients. A broker will give quotations of all loan offers by different

lenders to consider the best suitable loan as per the current position of an enterprise.

Personnel

Financial advisor of the Ray and Steve play an important role in guiding the business

towards the best suitable path to get the desired return over the years. Acquisition of Henman

transport is a result of the advice of the accountants who assess the financial performance of

the business.

Process

The current process is use to arrange the finance from the lender within 5-15 working

days.

Generate reliable information and required documentation from the clients

Provide proposal documents to client along with broker’s recommendations

File completed application to the lender to seek their consent

Lender investigates credit history of the client and confirms the loan application

7

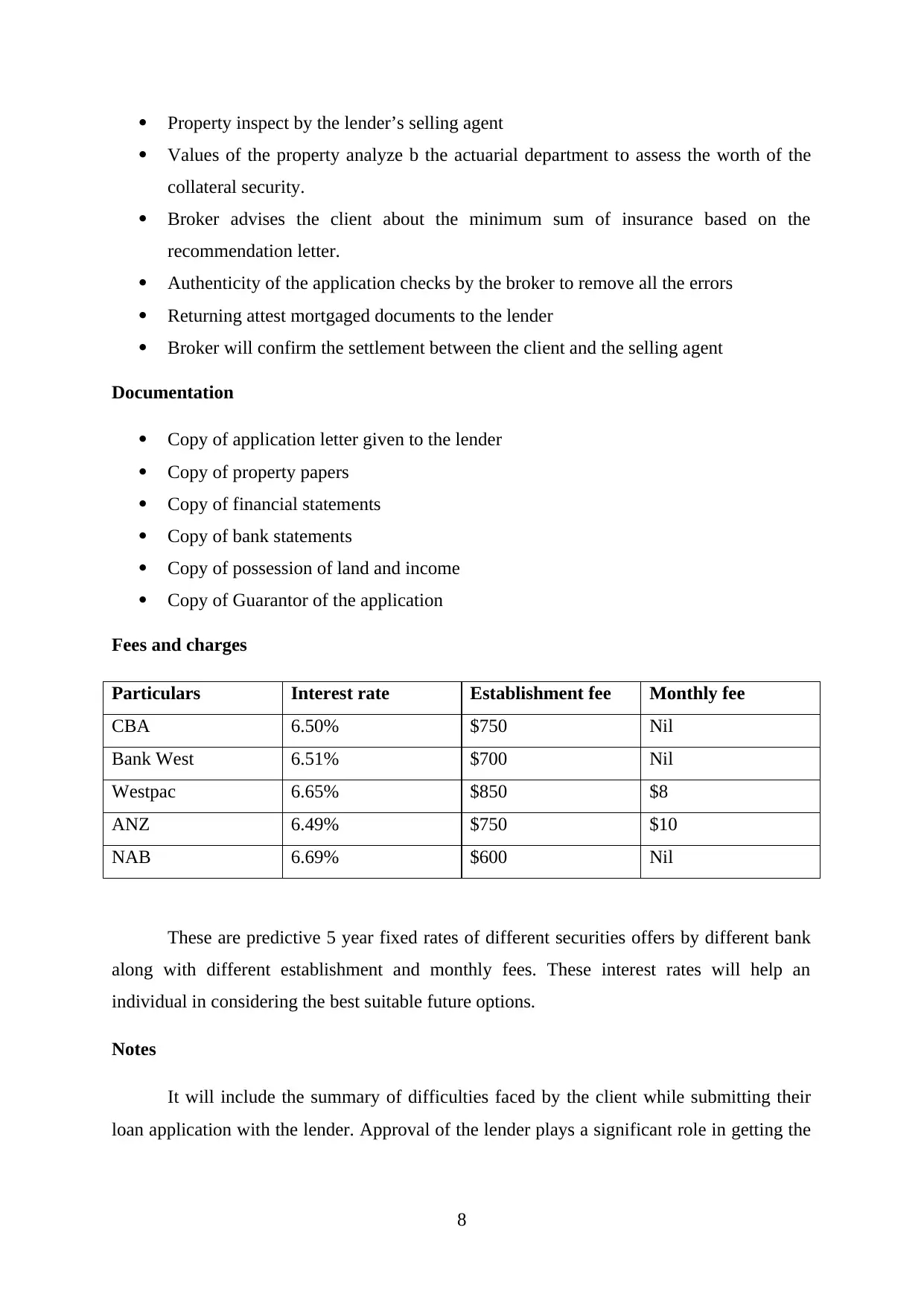

Property inspect by the lender’s selling agent

Values of the property analyze b the actuarial department to assess the worth of the

collateral security.

Broker advises the client about the minimum sum of insurance based on the

recommendation letter.

Authenticity of the application checks by the broker to remove all the errors

Returning attest mortgaged documents to the lender

Broker will confirm the settlement between the client and the selling agent

Documentation

Copy of application letter given to the lender

Copy of property papers

Copy of financial statements

Copy of bank statements

Copy of possession of land and income

Copy of Guarantor of the application

Fees and charges

Particulars Interest rate Establishment fee Monthly fee

CBA 6.50% $750 Nil

Bank West 6.51% $700 Nil

Westpac 6.65% $850 $8

ANZ 6.49% $750 $10

NAB 6.69% $600 Nil

These are predictive 5 year fixed rates of different securities offers by different bank

along with different establishment and monthly fees. These interest rates will help an

individual in considering the best suitable future options.

Notes

It will include the summary of difficulties faced by the client while submitting their

loan application with the lender. Approval of the lender plays a significant role in getting the

8

Values of the property analyze b the actuarial department to assess the worth of the

collateral security.

Broker advises the client about the minimum sum of insurance based on the

recommendation letter.

Authenticity of the application checks by the broker to remove all the errors

Returning attest mortgaged documents to the lender

Broker will confirm the settlement between the client and the selling agent

Documentation

Copy of application letter given to the lender

Copy of property papers

Copy of financial statements

Copy of bank statements

Copy of possession of land and income

Copy of Guarantor of the application

Fees and charges

Particulars Interest rate Establishment fee Monthly fee

CBA 6.50% $750 Nil

Bank West 6.51% $700 Nil

Westpac 6.65% $850 $8

ANZ 6.49% $750 $10

NAB 6.69% $600 Nil

These are predictive 5 year fixed rates of different securities offers by different bank

along with different establishment and monthly fees. These interest rates will help an

individual in considering the best suitable future options.

Notes

It will include the summary of difficulties faced by the client while submitting their

loan application with the lender. Approval of the lender plays a significant role in getting the

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 30

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.