Comparative Study of IFRS and IAS Standards in Financial Reporting

VerifiedAdded on 2021/02/19

|5

|492

|30

Report

AI Summary

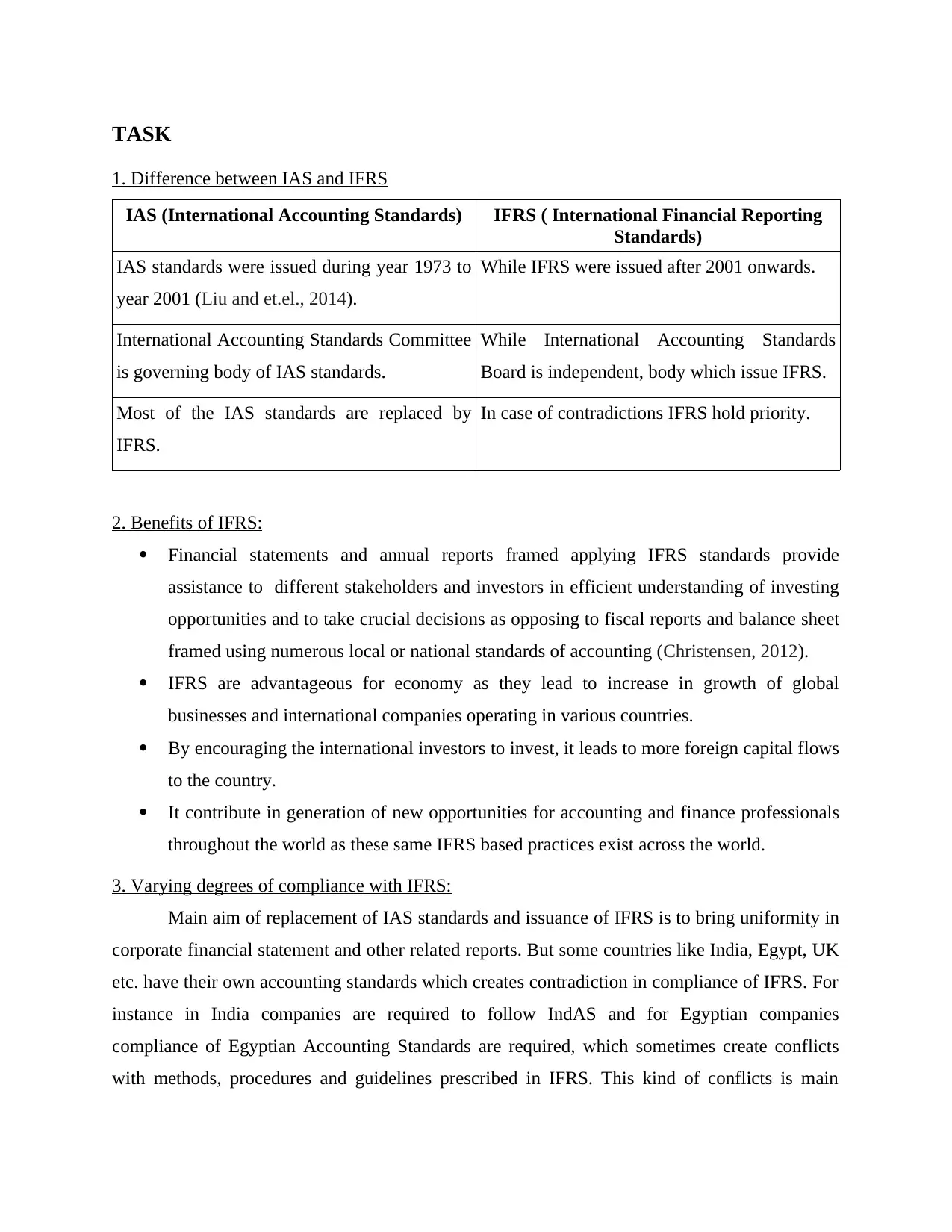

This report provides a comprehensive comparison between International Financial Reporting Standards (IFRS) and International Accounting Standards (IAS). It begins by outlining the key differences between the two sets of standards, including their governing bodies and the evolution from IAS to IFRS. The report then delves into the benefits of IFRS, such as improved financial statement comparability and enhanced opportunities for international business. The report also addresses the varying degrees of compliance with IFRS across different countries, highlighting conflicts between IFRS and local accounting standards, such as those in India and Egypt. The report concludes with a list of references that support the analysis of the IFRS and IAS standards, providing a detailed overview of the subject matter.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.