Financial Resource Management and Decision Making Report - University

VerifiedAdded on 2020/02/05

|18

|4678

|50

Report

AI Summary

This report provides a comprehensive analysis of financial resource management and decision-making within a business context. It begins by identifying and assessing various sources of finance, including internal and external options such as personal capital, retained earnings, share issues, debentures, bank loans, venture capital, and government grants. The report evaluates the implications of each source, considering legal aspects, ownership dilution, and potential bankruptcy risks. It then analyzes the costs associated with each financing option, emphasizing the importance of financial planning, budgeting, and forecasting. The report further explores the information needs of internal and external decision-makers, including shareholders, investors, government entities, and financial institutions. It examines the impact of finance on financial statements and delves into financial ratio analysis, using J Sainsbury Plc as a case study to interpret financial statements and assess profitability, liquidity, efficiency, and investment performance. Finally, the report discusses projected budgets, unit cost calculations, pricing decisions, and the viability of a chosen contract using investment appraisal techniques, ultimately providing valuable insights into effective financial management strategies.

Managing Financial

Resources and Decisions

1

Resources and Decisions

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

TASK 1............................................................................................................................................3

AC 1.1 Identify the sources of finance available to a business ..................................................3

AC 1.2 Assess the implications of the different sources of finance identified ...........................4

AC 1.3 Evaluate appropriate sources of finance for business project ........................................5

TASK 2............................................................................................................................................6

AC 2.1 Analyse the costs of each of sources of finance which are identified ............................6

AC 2.2 Explain the importance of financial planning and give details of how this financial

planning undertaken.....................................................................................................................6

AC 2.3 Identify and assess the information needs of internal and external decision makers......7

AC 2.4 Explain the impact of finance on the financial statements..............................................8

TASK 3............................................................................................................................................8

AC 3.1 Projected budgets and appropriate decision towards the chosen contract .....................8

AC 3.2 Calculation of unit costs for the chosen contract and make pricing decisions using

relevant information.....................................................................................................................9

AC 3.3 Viability of the chosen contract using different investment appraisal techniques.......10

TASK 4..........................................................................................................................................13

AC 4.1 Main financial statements by explaining what they contain, their purposes and who

makes use of them......................................................................................................................13

AC 4.2 Compare the formats of main financial statements for different types of businesses ..14

AC 4.3 Interpret financial statements and ratio calculation of Sainsbury Plc...........................14

CONCLUSION .............................................................................................................................16

REFERENCES .............................................................................................................................17

2

INTRODUCTION ..........................................................................................................................3

TASK 1............................................................................................................................................3

AC 1.1 Identify the sources of finance available to a business ..................................................3

AC 1.2 Assess the implications of the different sources of finance identified ...........................4

AC 1.3 Evaluate appropriate sources of finance for business project ........................................5

TASK 2............................................................................................................................................6

AC 2.1 Analyse the costs of each of sources of finance which are identified ............................6

AC 2.2 Explain the importance of financial planning and give details of how this financial

planning undertaken.....................................................................................................................6

AC 2.3 Identify and assess the information needs of internal and external decision makers......7

AC 2.4 Explain the impact of finance on the financial statements..............................................8

TASK 3............................................................................................................................................8

AC 3.1 Projected budgets and appropriate decision towards the chosen contract .....................8

AC 3.2 Calculation of unit costs for the chosen contract and make pricing decisions using

relevant information.....................................................................................................................9

AC 3.3 Viability of the chosen contract using different investment appraisal techniques.......10

TASK 4..........................................................................................................................................13

AC 4.1 Main financial statements by explaining what they contain, their purposes and who

makes use of them......................................................................................................................13

AC 4.2 Compare the formats of main financial statements for different types of businesses ..14

AC 4.3 Interpret financial statements and ratio calculation of Sainsbury Plc...........................14

CONCLUSION .............................................................................................................................16

REFERENCES .............................................................................................................................17

2

INTRODUCTION

Financial decision making is pivotal for business as it directly links with the profitability

and financial performance of an organization. In order to gain success in the corporate world,

businesses focus on management of financial resources (Hill, 2007). For gaining higher profits

and maintaining a smooth financial performance, companies use various financial tools. This

manuscript is based on a case scenario in which an entrepreneur requires bidding on a business

project but there are not enough financial resources to invest into project, therefore, various

sources of finance need to be searched. The report herewith is going to discuss about different

financial sources that can be used for raising funds for investing into proposed business.

Furthermore, the report represents implication of chosen sources of finance along with their cost.

This unit also represents the importance of financial planning and impact of finance on the

financial statements. Moreover, financial ratio analysis is done for the purpose of interpreting

financial statements and assessing profitability, liquidity, efficiency and investment performance

of J Sainsbury Plc.

TASK 1

AC 1.1 Identify the sources of finance available to a business

According to the given business scenario, an entrepreneur requires total £300,000 for the

purpose of investing into a business project. However, only £20,000 is with him to invest into

business, therefore, the balance needs to be borrowed. For this purpose, entrepreneur is looking

for various sources of finance that could meet the financial needs. Internal and external are two

major sources of finance that could be used; internal sources are those which are acquired from

the business, on the other hand external sources are those sources in which business raises funds

from outside (Zoan, 2014.). Here are some sources of finance that could be used by the

entrepreneur:

Personal capital: The saving available with the business owner can be used to invest in

new project. This will be an internal source of finance for which the business is not required to

pay the financial cost. The cited source of finance is easily available and provides cost benefits.

3

Financial decision making is pivotal for business as it directly links with the profitability

and financial performance of an organization. In order to gain success in the corporate world,

businesses focus on management of financial resources (Hill, 2007). For gaining higher profits

and maintaining a smooth financial performance, companies use various financial tools. This

manuscript is based on a case scenario in which an entrepreneur requires bidding on a business

project but there are not enough financial resources to invest into project, therefore, various

sources of finance need to be searched. The report herewith is going to discuss about different

financial sources that can be used for raising funds for investing into proposed business.

Furthermore, the report represents implication of chosen sources of finance along with their cost.

This unit also represents the importance of financial planning and impact of finance on the

financial statements. Moreover, financial ratio analysis is done for the purpose of interpreting

financial statements and assessing profitability, liquidity, efficiency and investment performance

of J Sainsbury Plc.

TASK 1

AC 1.1 Identify the sources of finance available to a business

According to the given business scenario, an entrepreneur requires total £300,000 for the

purpose of investing into a business project. However, only £20,000 is with him to invest into

business, therefore, the balance needs to be borrowed. For this purpose, entrepreneur is looking

for various sources of finance that could meet the financial needs. Internal and external are two

major sources of finance that could be used; internal sources are those which are acquired from

the business, on the other hand external sources are those sources in which business raises funds

from outside (Zoan, 2014.). Here are some sources of finance that could be used by the

entrepreneur:

Personal capital: The saving available with the business owner can be used to invest in

new project. This will be an internal source of finance for which the business is not required to

pay the financial cost. The cited source of finance is easily available and provides cost benefits.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Retained earnings: Retained earnings are the part of previous year’s profits and are kept

safe by the business for the purpose of using it in the future. This source of finance can only be

used for existing business and which had earned profits in last year. This is also an internal

source of finance however; its uses are limited in the present case scenario (Wildavsky, 2006).

Issues of shares : Equity financing or issue of share is the external sources of finance in

which company offers shares to public and raises funds to invest in business activities. Through

such sources, large funds can be accessed; however, company has to share ownership with

shareholders (Sources of finance, 2013).

Issues of debenture: Debt issuing is a kind of loan for the company in which debenture

holders are to be paid with interest against their amount. However, business has to do many

formalities to raise funds from such sources.

Bank loan: The organizations or business owners can take loan from financial institutes

however; they have to put securities against loan taken and have to pay the interest.

Venture capital: Venture capitalistic firms provide finance to the business holders

against their unique business idea or a profitable business deal. But, from these sources limited

amount of fund can be raised.

Government grants: The business entities can also raise funds in the form of

government grants, however, there are huge competition in market for acquiring government

grants is the limitation of this source (Cox and Fardon, 2003).

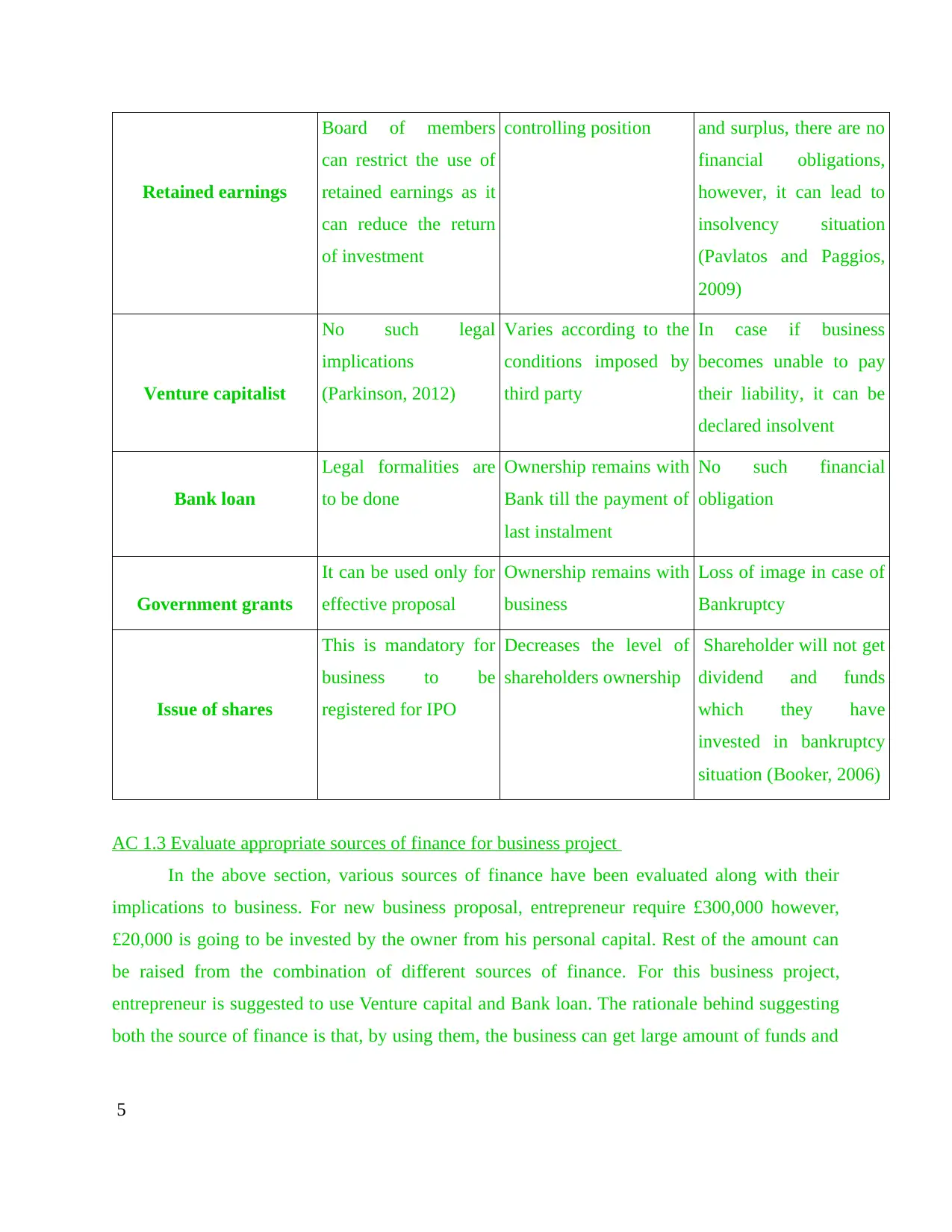

AC 1.2 Assess the implications of the different sources of finance identified

Sources Legal Dilution of Ownership Bankruptcy

Owner's capital

No legal restriction of

fund generation

The power of

controlling will be

diluted.

The business entity will

be financial obliged for

using such sources for

not getting in the

situation of insolvency

Shareholders and No change in Being a part of reserve

4

safe by the business for the purpose of using it in the future. This source of finance can only be

used for existing business and which had earned profits in last year. This is also an internal

source of finance however; its uses are limited in the present case scenario (Wildavsky, 2006).

Issues of shares : Equity financing or issue of share is the external sources of finance in

which company offers shares to public and raises funds to invest in business activities. Through

such sources, large funds can be accessed; however, company has to share ownership with

shareholders (Sources of finance, 2013).

Issues of debenture: Debt issuing is a kind of loan for the company in which debenture

holders are to be paid with interest against their amount. However, business has to do many

formalities to raise funds from such sources.

Bank loan: The organizations or business owners can take loan from financial institutes

however; they have to put securities against loan taken and have to pay the interest.

Venture capital: Venture capitalistic firms provide finance to the business holders

against their unique business idea or a profitable business deal. But, from these sources limited

amount of fund can be raised.

Government grants: The business entities can also raise funds in the form of

government grants, however, there are huge competition in market for acquiring government

grants is the limitation of this source (Cox and Fardon, 2003).

AC 1.2 Assess the implications of the different sources of finance identified

Sources Legal Dilution of Ownership Bankruptcy

Owner's capital

No legal restriction of

fund generation

The power of

controlling will be

diluted.

The business entity will

be financial obliged for

using such sources for

not getting in the

situation of insolvency

Shareholders and No change in Being a part of reserve

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Retained earnings

Board of members

can restrict the use of

retained earnings as it

can reduce the return

of investment

controlling position and surplus, there are no

financial obligations,

however, it can lead to

insolvency situation

(Pavlatos and Paggios,

2009)

Venture capitalist

No such legal

implications

(Parkinson, 2012)

Varies according to the

conditions imposed by

third party

In case if business

becomes unable to pay

their liability, it can be

declared insolvent

Bank loan

Legal formalities are

to be done

Ownership remains with

Bank till the payment of

last instalment

No such financial

obligation

Government grants

It can be used only for

effective proposal

Ownership remains with

business

Loss of image in case of

Bankruptcy

Issue of shares

This is mandatory for

business to be

registered for IPO

Decreases the level of

shareholders ownership

Shareholder will not get

dividend and funds

which they have

invested in bankruptcy

situation (Booker, 2006)

AC 1.3 Evaluate appropriate sources of finance for business project

In the above section, various sources of finance have been evaluated along with their

implications to business. For new business proposal, entrepreneur require £300,000 however,

£20,000 is going to be invested by the owner from his personal capital. Rest of the amount can

be raised from the combination of different sources of finance. For this business project,

entrepreneur is suggested to use Venture capital and Bank loan. The rationale behind suggesting

both the source of finance is that, by using them, the business can get large amount of funds and

5

Board of members

can restrict the use of

retained earnings as it

can reduce the return

of investment

controlling position and surplus, there are no

financial obligations,

however, it can lead to

insolvency situation

(Pavlatos and Paggios,

2009)

Venture capitalist

No such legal

implications

(Parkinson, 2012)

Varies according to the

conditions imposed by

third party

In case if business

becomes unable to pay

their liability, it can be

declared insolvent

Bank loan

Legal formalities are

to be done

Ownership remains with

Bank till the payment of

last instalment

No such financial

obligation

Government grants

It can be used only for

effective proposal

Ownership remains with

business

Loss of image in case of

Bankruptcy

Issue of shares

This is mandatory for

business to be

registered for IPO

Decreases the level of

shareholders ownership

Shareholder will not get

dividend and funds

which they have

invested in bankruptcy

situation (Booker, 2006)

AC 1.3 Evaluate appropriate sources of finance for business project

In the above section, various sources of finance have been evaluated along with their

implications to business. For new business proposal, entrepreneur require £300,000 however,

£20,000 is going to be invested by the owner from his personal capital. Rest of the amount can

be raised from the combination of different sources of finance. For this business project,

entrepreneur is suggested to use Venture capital and Bank loan. The rationale behind suggesting

both the source of finance is that, by using them, the business can get large amount of funds and

5

these will be external sources of finance. For bank loan, it has to do various legal formalities.

However, business has to pay interest for using such funds and these both are less risky and

external source of finance.

TASK 2

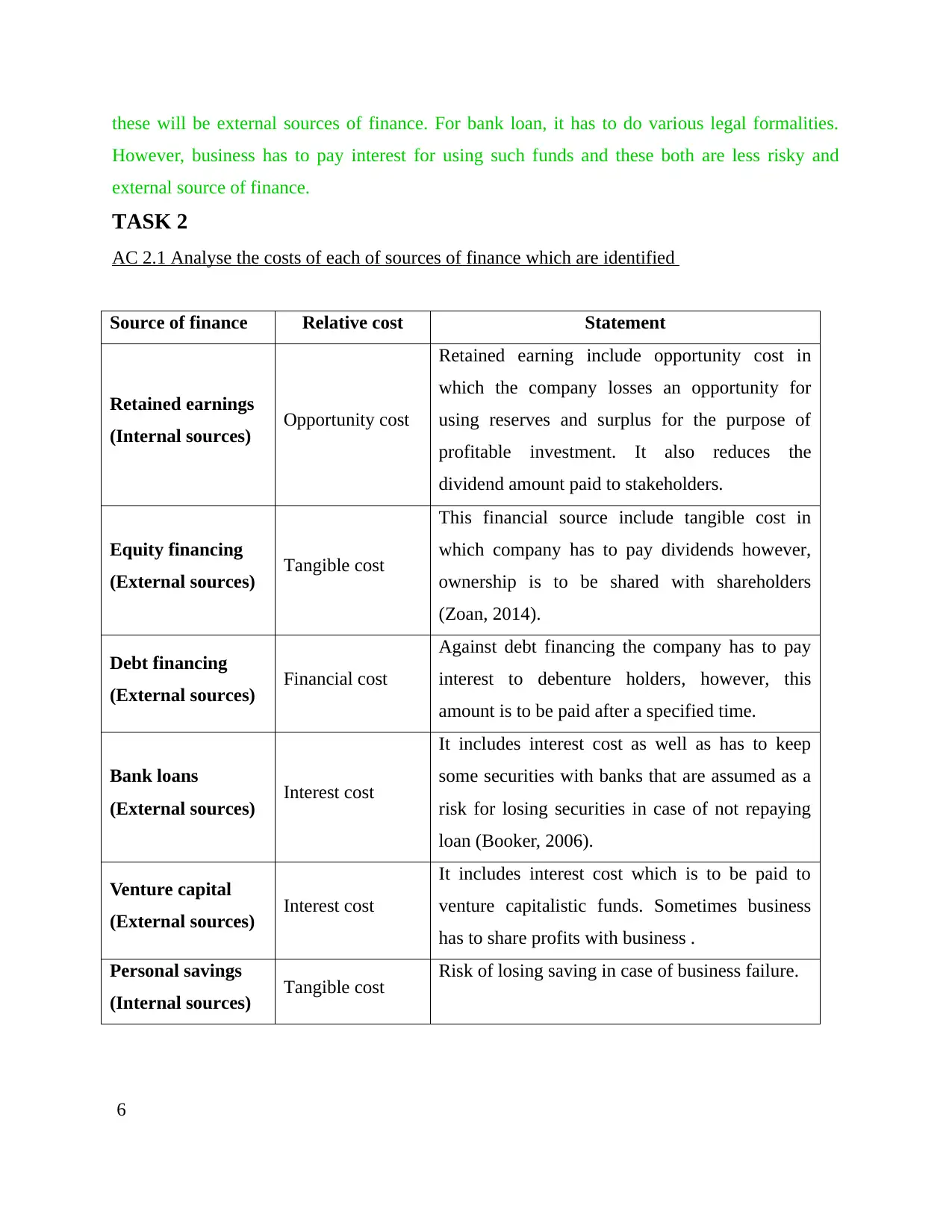

AC 2.1 Analyse the costs of each of sources of finance which are identified

Source of finance Relative cost Statement

Retained earnings

(Internal sources) Opportunity cost

Retained earning include opportunity cost in

which the company losses an opportunity for

using reserves and surplus for the purpose of

profitable investment. It also reduces the

dividend amount paid to stakeholders.

Equity financing

(External sources) Tangible cost

This financial source include tangible cost in

which company has to pay dividends however,

ownership is to be shared with shareholders

(Zoan, 2014).

Debt financing

(External sources) Financial cost

Against debt financing the company has to pay

interest to debenture holders, however, this

amount is to be paid after a specified time.

Bank loans

(External sources) Interest cost

It includes interest cost as well as has to keep

some securities with banks that are assumed as a

risk for losing securities in case of not repaying

loan (Booker, 2006).

Venture capital

(External sources) Interest cost

It includes interest cost which is to be paid to

venture capitalistic funds. Sometimes business

has to share profits with business .

Personal savings

(Internal sources) Tangible cost Risk of losing saving in case of business failure.

6

However, business has to pay interest for using such funds and these both are less risky and

external source of finance.

TASK 2

AC 2.1 Analyse the costs of each of sources of finance which are identified

Source of finance Relative cost Statement

Retained earnings

(Internal sources) Opportunity cost

Retained earning include opportunity cost in

which the company losses an opportunity for

using reserves and surplus for the purpose of

profitable investment. It also reduces the

dividend amount paid to stakeholders.

Equity financing

(External sources) Tangible cost

This financial source include tangible cost in

which company has to pay dividends however,

ownership is to be shared with shareholders

(Zoan, 2014).

Debt financing

(External sources) Financial cost

Against debt financing the company has to pay

interest to debenture holders, however, this

amount is to be paid after a specified time.

Bank loans

(External sources) Interest cost

It includes interest cost as well as has to keep

some securities with banks that are assumed as a

risk for losing securities in case of not repaying

loan (Booker, 2006).

Venture capital

(External sources) Interest cost

It includes interest cost which is to be paid to

venture capitalistic funds. Sometimes business

has to share profits with business .

Personal savings

(Internal sources) Tangible cost Risk of losing saving in case of business failure.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AC 2.2 Explain the importance of financial planning and give details of how this financial

planning undertaken

Financial plaining has a vital role in making smooth plans to attain financial performance

of business. Making use of financial planning business entity can attain goals of profitability

and so on. This is also called as a major step of mapping out financial future of business. In

respect with the present case financial planing tools are used to assess the sources of finance as

well as effective selection of suitable one. In addition to that, financial planing helps in

identifying current and future needs of business and the ways to improve financial performance.

Budgeting and forecasting methods are the essential parts of financial planning that helps in

identifying future incomes and expenses (Cortes, 2009). With the help of financial planning tools

company can make effective use of financial resources. Investment appraisal tactics which are

related to financial planning can be used in the present case for assessing viability of business

project. The financial planning is to be done on the basis of forecasting the future profits from

the business projects for with investment appraisal tactics can be used. The importance of

financial planning is presented in the following points :

Assessment of available sources of finance

Identifying projected incomes and expenses

Preparing budgets

Making profitable investment decision

Having a proper balance between cash outflow and cash inflow (Parkinson, 2012)

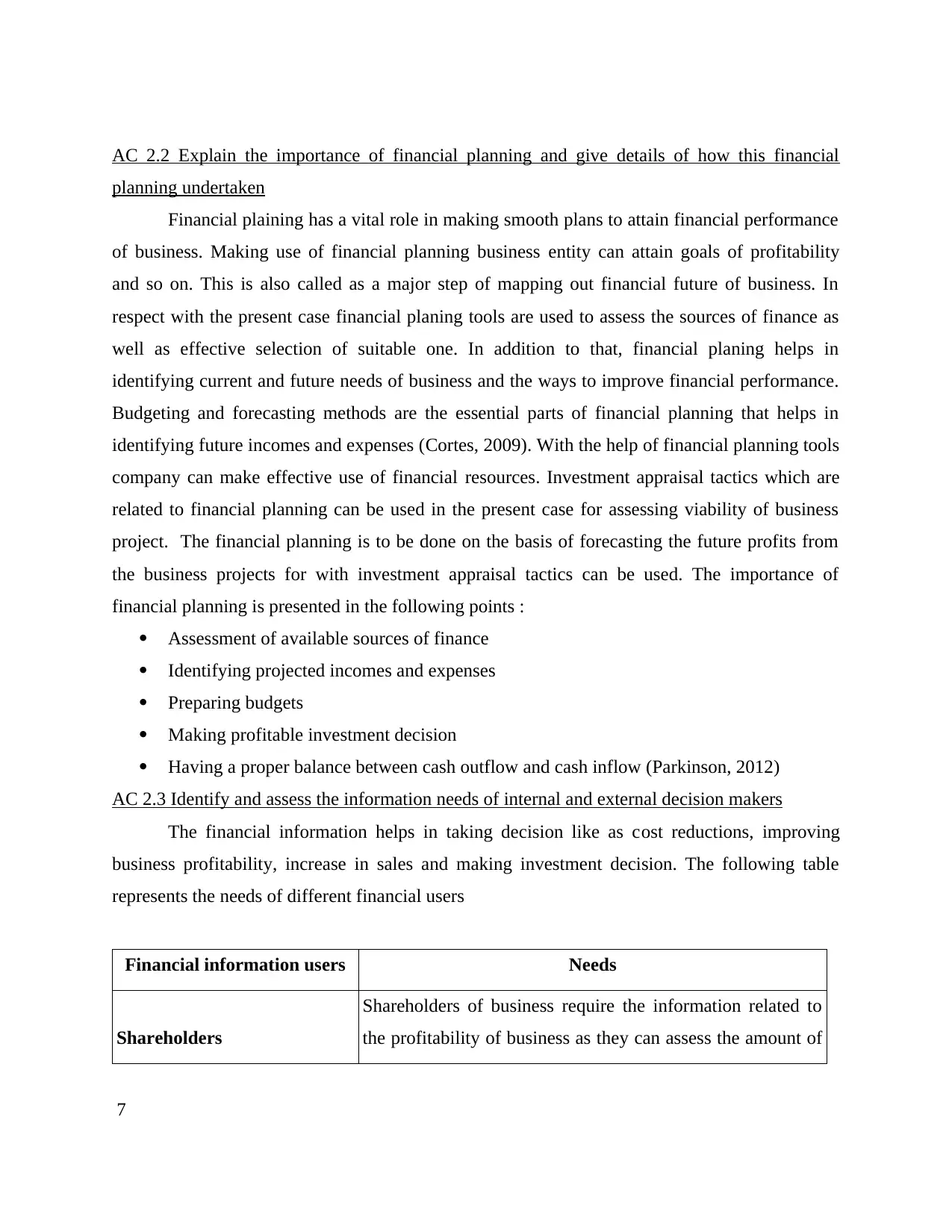

AC 2.3 Identify and assess the information needs of internal and external decision makers

The financial information helps in taking decision like as cost reductions, improving

business profitability, increase in sales and making investment decision. The following table

represents the needs of different financial users

Financial information users Needs

Shareholders

Shareholders of business require the information related to

the profitability of business as they can assess the amount of

7

planning undertaken

Financial plaining has a vital role in making smooth plans to attain financial performance

of business. Making use of financial planning business entity can attain goals of profitability

and so on. This is also called as a major step of mapping out financial future of business. In

respect with the present case financial planing tools are used to assess the sources of finance as

well as effective selection of suitable one. In addition to that, financial planing helps in

identifying current and future needs of business and the ways to improve financial performance.

Budgeting and forecasting methods are the essential parts of financial planning that helps in

identifying future incomes and expenses (Cortes, 2009). With the help of financial planning tools

company can make effective use of financial resources. Investment appraisal tactics which are

related to financial planning can be used in the present case for assessing viability of business

project. The financial planning is to be done on the basis of forecasting the future profits from

the business projects for with investment appraisal tactics can be used. The importance of

financial planning is presented in the following points :

Assessment of available sources of finance

Identifying projected incomes and expenses

Preparing budgets

Making profitable investment decision

Having a proper balance between cash outflow and cash inflow (Parkinson, 2012)

AC 2.3 Identify and assess the information needs of internal and external decision makers

The financial information helps in taking decision like as cost reductions, improving

business profitability, increase in sales and making investment decision. The following table

represents the needs of different financial users

Financial information users Needs

Shareholders

Shareholders of business require the information related to

the profitability of business as they can assess the amount of

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

dividend. Therefore, shareholders assess income statements

of business.

Investors

Potential investors of business always look for the

information about returns earned by the company as well as

creditworthiness so that they can decide on investing in

business operations (Peterson and Fabozzi, 2004).

Government

Government entities look over the financial statement to

known whether business is paying taxes on time or not. In

addition to that annual reports of company are watched by

regulatory bodies to identity the CSR.

Financial institution

Banks and Venture capital firms always look for

creditworthiness of business to decide whether company is to

be provided credit or not.

AC 2.4 Explain the impact of finance on the financial statements

The sources of finance put a crucial impact of financial statement and affects the financial

information included in the reports. In respect with the present case, entrepreneur is going to use

personal capital, venture capital and bank loan as a source of finance hence, the amount raised

from all sources of finance put a significant impact on business. In case organization uses

personal capital will be used that the amount will be shown in balance sheet as a head of capital.

In addition to that, the use of venture capital put significant impact of income statement

as well as balance sheet. The amount raised from such sources will be included in liabilities

section of balance sheet and the interest paid to such financial institutes will reduce the profits of

business. On the other hand, Bank loan will be ho under the head of long term or short term

liability in balance sheet and interest paid will be shown I debit side of income statement.

TASK 3

AC 3.1 Projected budgets and appropriate decision towards the chosen contract

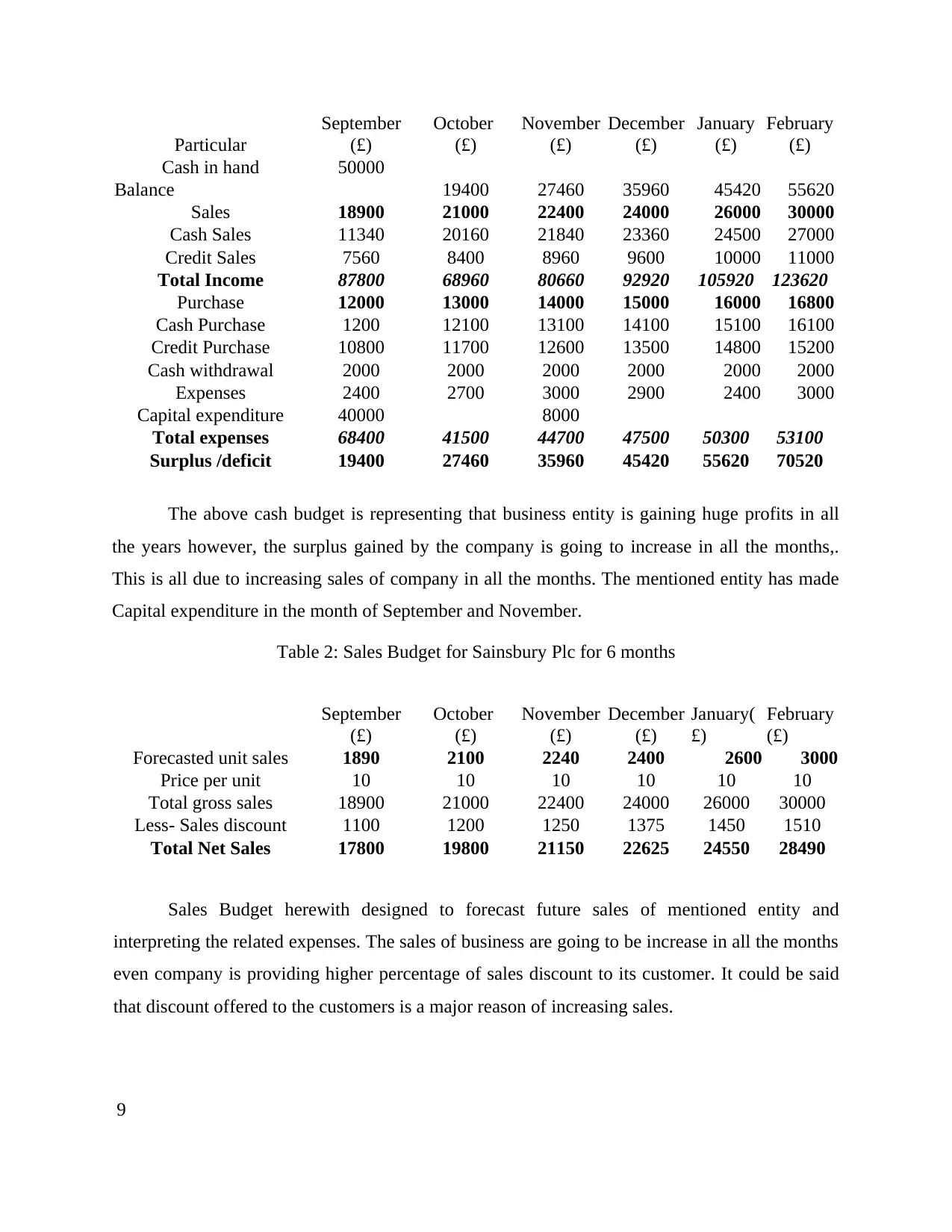

Table 1: Cash Budget for Sainsbury Plc for 6 months

8

of business.

Investors

Potential investors of business always look for the

information about returns earned by the company as well as

creditworthiness so that they can decide on investing in

business operations (Peterson and Fabozzi, 2004).

Government

Government entities look over the financial statement to

known whether business is paying taxes on time or not. In

addition to that annual reports of company are watched by

regulatory bodies to identity the CSR.

Financial institution

Banks and Venture capital firms always look for

creditworthiness of business to decide whether company is to

be provided credit or not.

AC 2.4 Explain the impact of finance on the financial statements

The sources of finance put a crucial impact of financial statement and affects the financial

information included in the reports. In respect with the present case, entrepreneur is going to use

personal capital, venture capital and bank loan as a source of finance hence, the amount raised

from all sources of finance put a significant impact on business. In case organization uses

personal capital will be used that the amount will be shown in balance sheet as a head of capital.

In addition to that, the use of venture capital put significant impact of income statement

as well as balance sheet. The amount raised from such sources will be included in liabilities

section of balance sheet and the interest paid to such financial institutes will reduce the profits of

business. On the other hand, Bank loan will be ho under the head of long term or short term

liability in balance sheet and interest paid will be shown I debit side of income statement.

TASK 3

AC 3.1 Projected budgets and appropriate decision towards the chosen contract

Table 1: Cash Budget for Sainsbury Plc for 6 months

8

Particular

September

(£)

October

(£)

November

(£)

December

(£)

January

(£)

February

(£)

Cash in hand 50000

Balance 19400 27460 35960 45420 55620

Sales 18900 21000 22400 24000 26000 30000

Cash Sales 11340 20160 21840 23360 24500 27000

Credit Sales 7560 8400 8960 9600 10000 11000

Total Income 87800 68960 80660 92920 105920 123620

Purchase 12000 13000 14000 15000 16000 16800

Cash Purchase 1200 12100 13100 14100 15100 16100

Credit Purchase 10800 11700 12600 13500 14800 15200

Cash withdrawal 2000 2000 2000 2000 2000 2000

Expenses 2400 2700 3000 2900 2400 3000

Capital expenditure 40000 8000

Total expenses 68400 41500 44700 47500 50300 53100

Surplus /deficit 19400 27460 35960 45420 55620 70520

The above cash budget is representing that business entity is gaining huge profits in all

the years however, the surplus gained by the company is going to increase in all the months,.

This is all due to increasing sales of company in all the months. The mentioned entity has made

Capital expenditure in the month of September and November.

Table 2: Sales Budget for Sainsbury Plc for 6 months

September

(£)

October

(£)

November

(£)

December

(£)

January(

£)

February

(£)

Forecasted unit sales 1890 2100 2240 2400 2600 3000

Price per unit 10 10 10 10 10 10

Total gross sales 18900 21000 22400 24000 26000 30000

Less- Sales discount 1100 1200 1250 1375 1450 1510

Total Net Sales 17800 19800 21150 22625 24550 28490

Sales Budget herewith designed to forecast future sales of mentioned entity and

interpreting the related expenses. The sales of business are going to be increase in all the months

even company is providing higher percentage of sales discount to its customer. It could be said

that discount offered to the customers is a major reason of increasing sales.

9

September

(£)

October

(£)

November

(£)

December

(£)

January

(£)

February

(£)

Cash in hand 50000

Balance 19400 27460 35960 45420 55620

Sales 18900 21000 22400 24000 26000 30000

Cash Sales 11340 20160 21840 23360 24500 27000

Credit Sales 7560 8400 8960 9600 10000 11000

Total Income 87800 68960 80660 92920 105920 123620

Purchase 12000 13000 14000 15000 16000 16800

Cash Purchase 1200 12100 13100 14100 15100 16100

Credit Purchase 10800 11700 12600 13500 14800 15200

Cash withdrawal 2000 2000 2000 2000 2000 2000

Expenses 2400 2700 3000 2900 2400 3000

Capital expenditure 40000 8000

Total expenses 68400 41500 44700 47500 50300 53100

Surplus /deficit 19400 27460 35960 45420 55620 70520

The above cash budget is representing that business entity is gaining huge profits in all

the years however, the surplus gained by the company is going to increase in all the months,.

This is all due to increasing sales of company in all the months. The mentioned entity has made

Capital expenditure in the month of September and November.

Table 2: Sales Budget for Sainsbury Plc for 6 months

September

(£)

October

(£)

November

(£)

December

(£)

January(

£)

February

(£)

Forecasted unit sales 1890 2100 2240 2400 2600 3000

Price per unit 10 10 10 10 10 10

Total gross sales 18900 21000 22400 24000 26000 30000

Less- Sales discount 1100 1200 1250 1375 1450 1510

Total Net Sales 17800 19800 21150 22625 24550 28490

Sales Budget herewith designed to forecast future sales of mentioned entity and

interpreting the related expenses. The sales of business are going to be increase in all the months

even company is providing higher percentage of sales discount to its customer. It could be said

that discount offered to the customers is a major reason of increasing sales.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

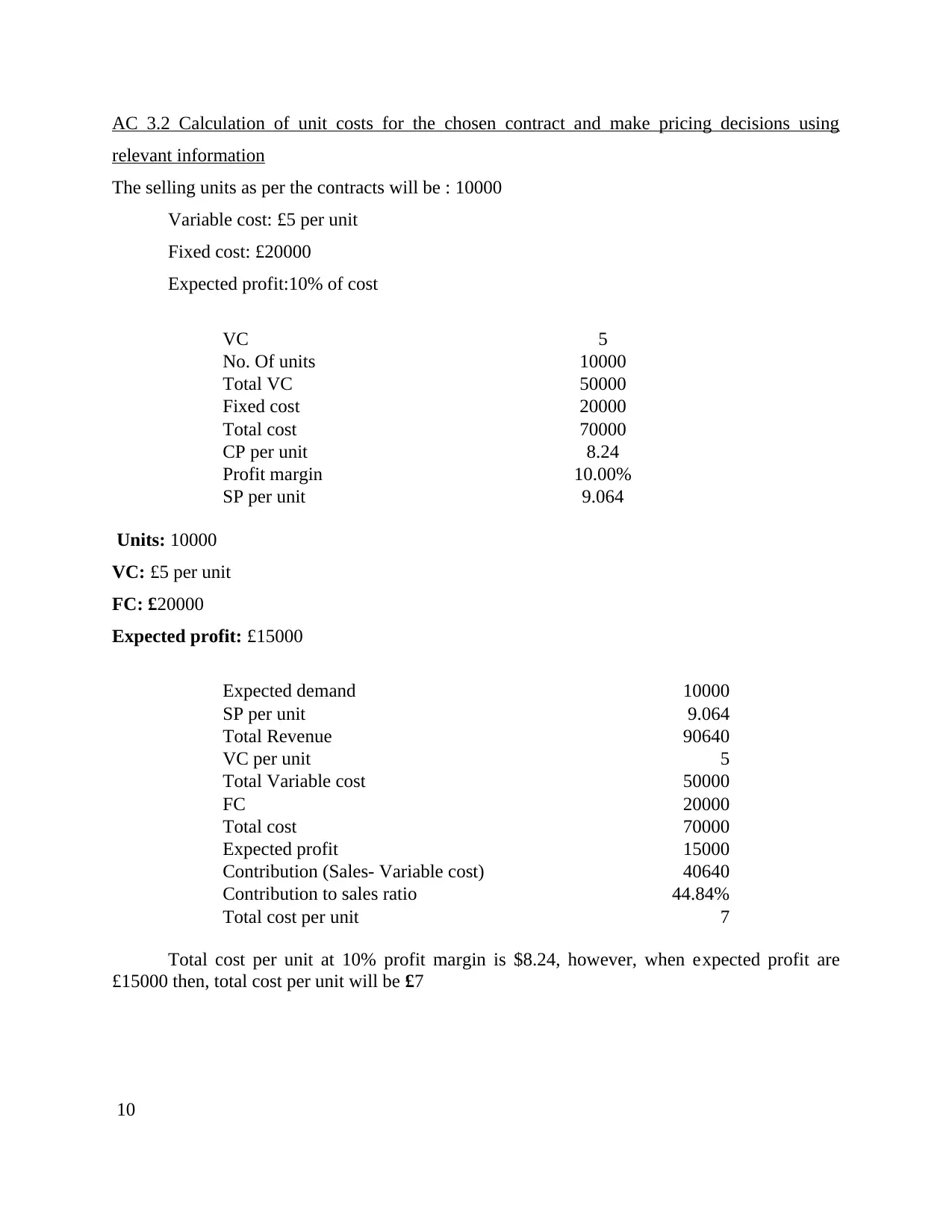

AC 3.2 Calculation of unit costs for the chosen contract and make pricing decisions using

relevant information

The selling units as per the contracts will be : 10000

Variable cost: £5 per unit

Fixed cost: £20000

Expected profit:10% of cost

VC 5

No. Of units 10000

Total VC 50000

Fixed cost 20000

Total cost 70000

CP per unit 8.24

Profit margin 10.00%

SP per unit 9.064

Units: 10000

VC: £5 per unit

FC: £20000

Expected profit: £15000

Expected demand 10000

SP per unit 9.064

Total Revenue 90640

VC per unit 5

Total Variable cost 50000

FC 20000

Total cost 70000

Expected profit 15000

Contribution (Sales- Variable cost) 40640

Contribution to sales ratio 44.84%

Total cost per unit 7

Total cost per unit at 10% profit margin is $8.24, however, when expected profit are

£15000 then, total cost per unit will be £7

10

relevant information

The selling units as per the contracts will be : 10000

Variable cost: £5 per unit

Fixed cost: £20000

Expected profit:10% of cost

VC 5

No. Of units 10000

Total VC 50000

Fixed cost 20000

Total cost 70000

CP per unit 8.24

Profit margin 10.00%

SP per unit 9.064

Units: 10000

VC: £5 per unit

FC: £20000

Expected profit: £15000

Expected demand 10000

SP per unit 9.064

Total Revenue 90640

VC per unit 5

Total Variable cost 50000

FC 20000

Total cost 70000

Expected profit 15000

Contribution (Sales- Variable cost) 40640

Contribution to sales ratio 44.84%

Total cost per unit 7

Total cost per unit at 10% profit margin is $8.24, however, when expected profit are

£15000 then, total cost per unit will be £7

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

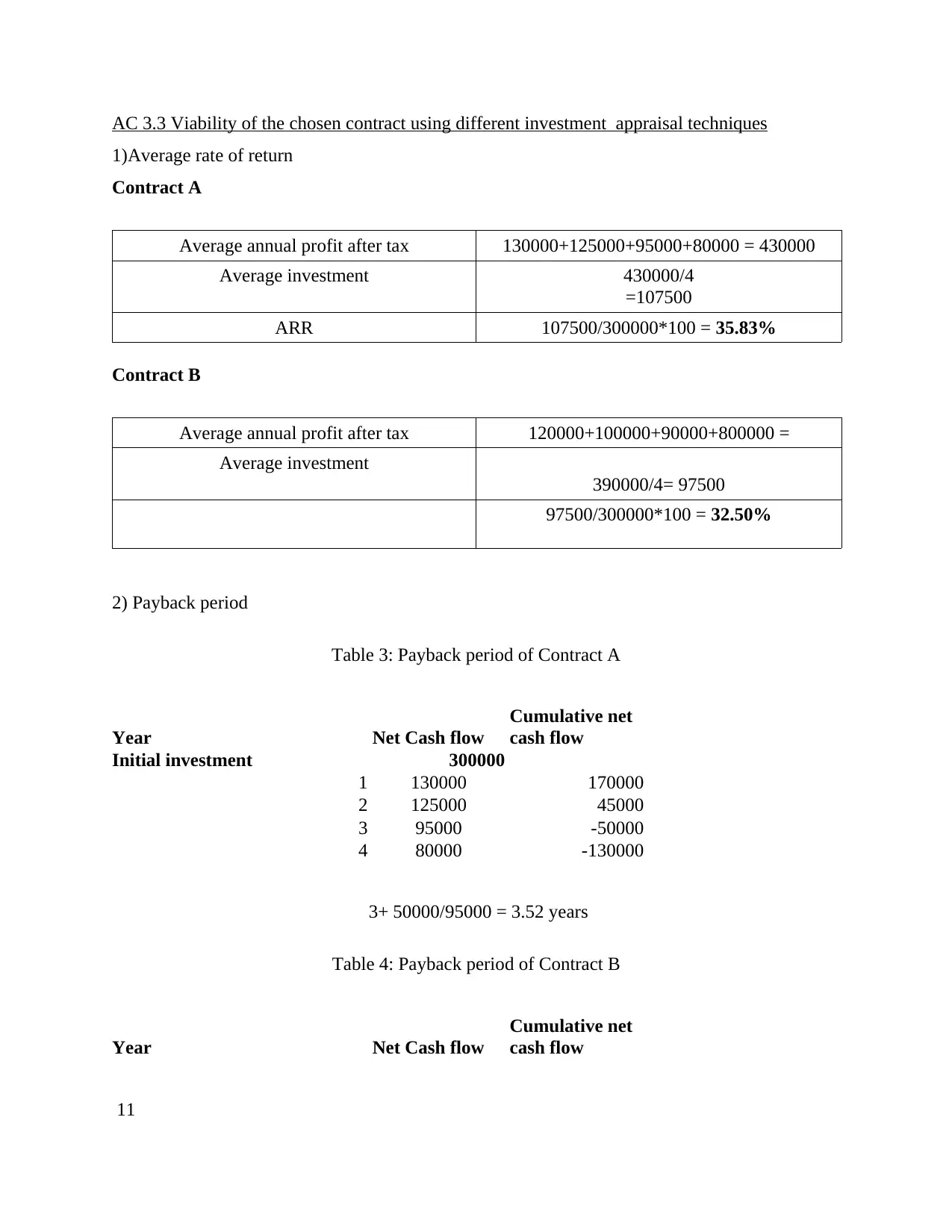

AC 3.3 Viability of the chosen contract using different investment appraisal techniques

1)Average rate of return

Contract A

Average annual profit after tax 130000+125000+95000+80000 = 430000

Average investment 430000/4

=107500

ARR 107500/300000*100 = 35.83%

Contract B

Average annual profit after tax 120000+100000+90000+800000 =

Average investment

390000/4= 97500

97500/300000*100 = 32.50%

2) Payback period

Table 3: Payback period of Contract A

Year Net Cash flow

Cumulative net

cash flow

Initial investment 300000

1 130000 170000

2 125000 45000

3 95000 -50000

4 80000 -130000

3+ 50000/95000 = 3.52 years

Table 4: Payback period of Contract B

Year Net Cash flow

Cumulative net

cash flow

11

1)Average rate of return

Contract A

Average annual profit after tax 130000+125000+95000+80000 = 430000

Average investment 430000/4

=107500

ARR 107500/300000*100 = 35.83%

Contract B

Average annual profit after tax 120000+100000+90000+800000 =

Average investment

390000/4= 97500

97500/300000*100 = 32.50%

2) Payback period

Table 3: Payback period of Contract A

Year Net Cash flow

Cumulative net

cash flow

Initial investment 300000

1 130000 170000

2 125000 45000

3 95000 -50000

4 80000 -130000

3+ 50000/95000 = 3.52 years

Table 4: Payback period of Contract B

Year Net Cash flow

Cumulative net

cash flow

11

Initial investment 300000

1 120000 180000

2 100000 80000

3 90000 -10000

4 80000 -90000

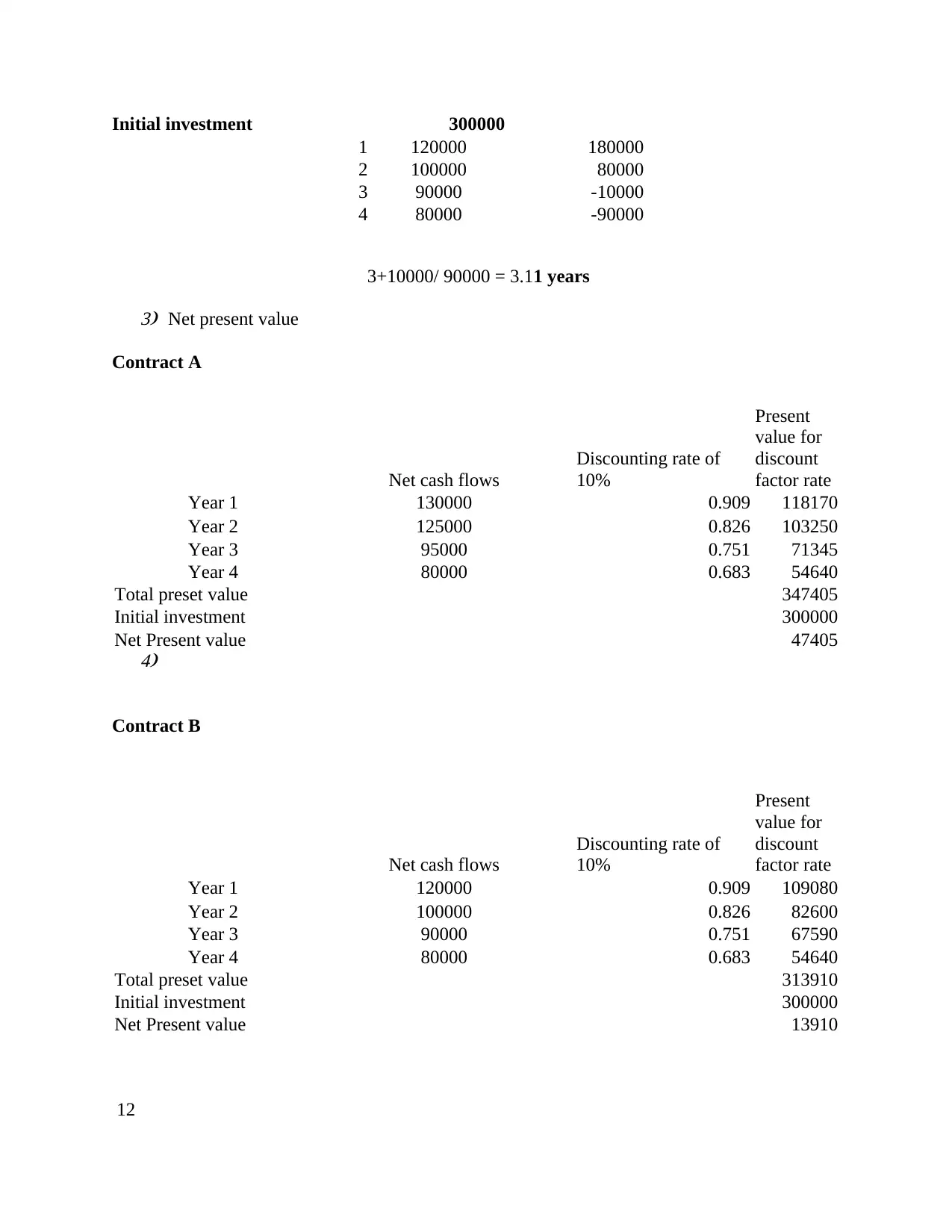

3+10000/ 90000 = 3.11 years3) Net present value

Contract A

Net cash flows

Discounting rate of

10%

Present

value for

discount

factor rate

Year 1 130000 0.909 118170

Year 2 125000 0.826 103250

Year 3 95000 0.751 71345

Year 4 80000 0.683 54640

Total preset value 347405

Initial investment 300000

Net Present value 47405

4)

Contract B

Net cash flows

Discounting rate of

10%

Present

value for

discount

factor rate

Year 1 120000 0.909 109080

Year 2 100000 0.826 82600

Year 3 90000 0.751 67590

Year 4 80000 0.683 54640

Total preset value 313910

Initial investment 300000

Net Present value 13910

12

1 120000 180000

2 100000 80000

3 90000 -10000

4 80000 -90000

3+10000/ 90000 = 3.11 years3) Net present value

Contract A

Net cash flows

Discounting rate of

10%

Present

value for

discount

factor rate

Year 1 130000 0.909 118170

Year 2 125000 0.826 103250

Year 3 95000 0.751 71345

Year 4 80000 0.683 54640

Total preset value 347405

Initial investment 300000

Net Present value 47405

4)

Contract B

Net cash flows

Discounting rate of

10%

Present

value for

discount

factor rate

Year 1 120000 0.909 109080

Year 2 100000 0.826 82600

Year 3 90000 0.751 67590

Year 4 80000 0.683 54640

Total preset value 313910

Initial investment 300000

Net Present value 13910

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.