Cost Accounting - Direct cost and Indirect cost

VerifiedAdded on 2022/09/02

|30

|7186

|23

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

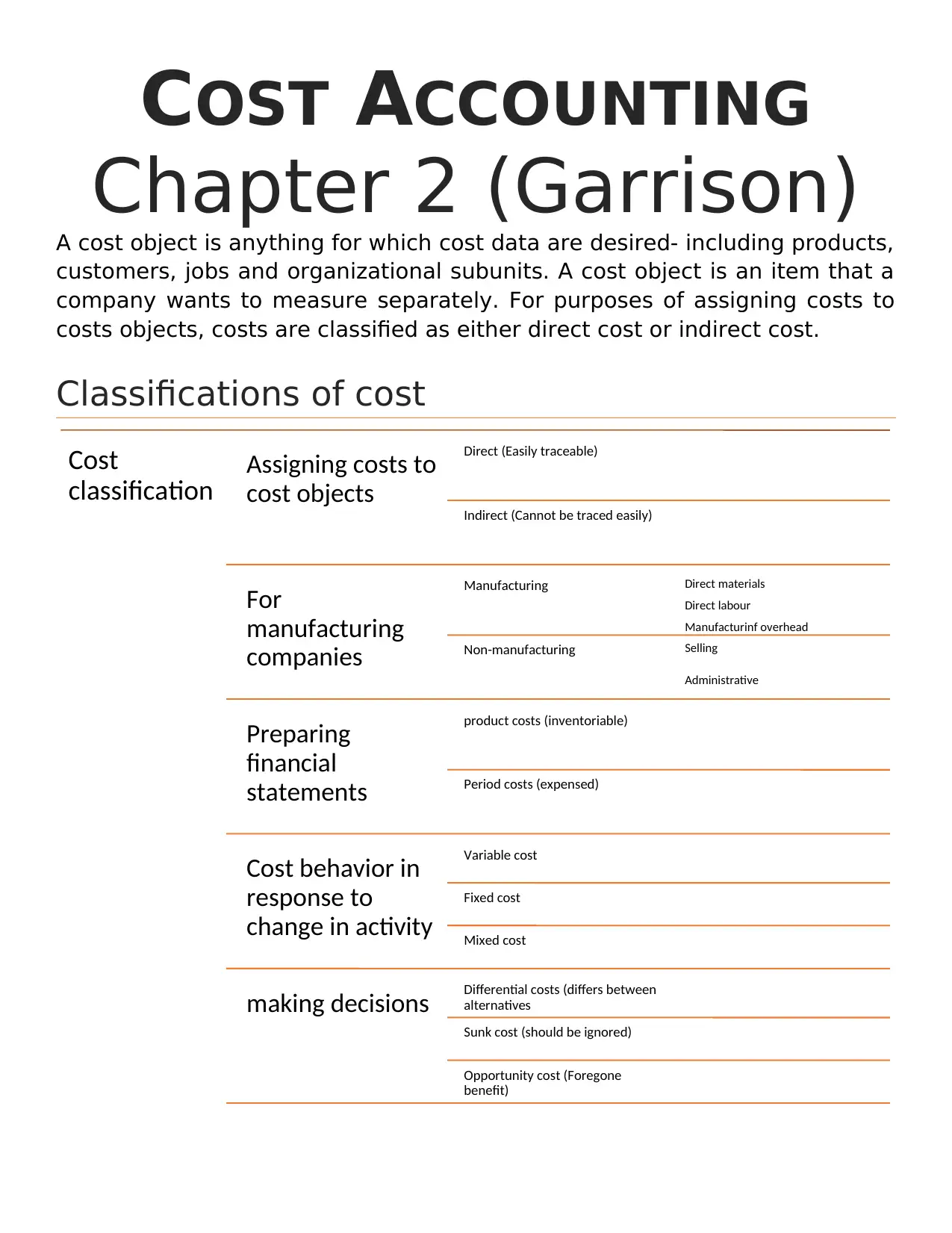

COST ACCOUNTING

Chapter 2 (Garrison)

A cost object is anything for which cost data are desired- including products,

customers, jobs and organizational subunits. A cost object is an item that a

company wants to measure separately. For purposes of assigning costs to

costs objects, costs are classified as either direct cost or indirect cost.

Classifications of cost

Cost

classification Assigning costs to

cost objects

Direct (Easily traceable)

Indirect (Cannot be traced easily)

For

manufacturing

companies

Manufacturing Direct materials

Direct labour

Manufacturinf overhead

Non-manufacturing Selling

Administrative

Preparing

financial

statements

product costs (inventoriable)

Period costs (expensed)

Cost behavior in

response to

change in activity

Variable cost

Fixed cost

Mixed cost

making decisions Differential costs (differs between

alternatives

Sunk cost (should be ignored)

Opportunity cost (Foregone

benefit)

Chapter 2 (Garrison)

A cost object is anything for which cost data are desired- including products,

customers, jobs and organizational subunits. A cost object is an item that a

company wants to measure separately. For purposes of assigning costs to

costs objects, costs are classified as either direct cost or indirect cost.

Classifications of cost

Cost

classification Assigning costs to

cost objects

Direct (Easily traceable)

Indirect (Cannot be traced easily)

For

manufacturing

companies

Manufacturing Direct materials

Direct labour

Manufacturinf overhead

Non-manufacturing Selling

Administrative

Preparing

financial

statements

product costs (inventoriable)

Period costs (expensed)

Cost behavior in

response to

change in activity

Variable cost

Fixed cost

Mixed cost

making decisions Differential costs (differs between

alternatives

Sunk cost (should be ignored)

Opportunity cost (Foregone

benefit)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Assigning costs to cost objects

Direct cost: A direct cost is a cost that can be easily and conveniently

traced to a specified cost object. A direct cost is a price that is directly

related to the production of a certain good or service. A direct cost can be

linked to a cost object such as a service, product, or department. The two

basic categories of expenses or prices that businesses might incur are direct

and indirect charges. Direct expenses are frequently variable costs, which

means they change with production levels like inventory.

Direct costs are expenses that your business can completely

attribute to the production of a product. The costs are easily

connected to only one project. Direct costs are not allocated, which

means they are not divided among many departments or projects.

A direct cost can be a fixed cost or variable cost.

An example of a direct cost are the supplies used to make the product. For

example, if you own a printing company, the paper for each project is a

direct cost. The employees who work on the production line are considered

direct labor. Their wages can also be attributed as a direct cost of the

projects.

Indirect cost: Indirect costs are expenses that cannot be traced back to a

single cost object or cost source. During the manufacturing process, items

like products, departments, and customers create costs. These are

considered cost objects because the original manufacturing costs stem from

them. The factory manager’s salary is called a common cost.

Now, consider the sales staff at the company. The sales staff is not

connected to one project. Therefore, their wages are not direct

costs because they cannot be attributed to any one project. Their

wages must be allocated to multiple projects.

Direct cost: A direct cost is a cost that can be easily and conveniently

traced to a specified cost object. A direct cost is a price that is directly

related to the production of a certain good or service. A direct cost can be

linked to a cost object such as a service, product, or department. The two

basic categories of expenses or prices that businesses might incur are direct

and indirect charges. Direct expenses are frequently variable costs, which

means they change with production levels like inventory.

Direct costs are expenses that your business can completely

attribute to the production of a product. The costs are easily

connected to only one project. Direct costs are not allocated, which

means they are not divided among many departments or projects.

A direct cost can be a fixed cost or variable cost.

An example of a direct cost are the supplies used to make the product. For

example, if you own a printing company, the paper for each project is a

direct cost. The employees who work on the production line are considered

direct labor. Their wages can also be attributed as a direct cost of the

projects.

Indirect cost: Indirect costs are expenses that cannot be traced back to a

single cost object or cost source. During the manufacturing process, items

like products, departments, and customers create costs. These are

considered cost objects because the original manufacturing costs stem from

them. The factory manager’s salary is called a common cost.

Now, consider the sales staff at the company. The sales staff is not

connected to one project. Therefore, their wages are not direct

costs because they cannot be attributed to any one project. Their

wages must be allocated to multiple projects.

Cost classification for manufacturing companies

Costs may be classified as manufacturing costs and non-manufacturing

costs. This classification is usually used by manufacturing companies.

Manufacturing costs

Most manufacturing companies separate their manufacturing costs into two

direct cost categories, direct-materials and direct labor and in one indirect

cost categories, manufacturing overhead.

Direct materials

Direct labor

Manufacturing overhead

Direct materials: Direct material is the physical items built into a product.

For example, the direct materials for a baker include flour, eggs,

yeast, sugar, oil, and water. The direct materials concept is used in cost

accounting, where this cost is separately classified in several types of

financial analysis. Direct materials are rolled into the total cost of goods

produced, which is then subdivided into the cost of goods sold (which

appears in the income statement) and ending inventory (which appears in

the balance sheet). The finished product of a company may become raw

material of another company. For example, cement is a finished product for

manufacturers of cement and raw materials for companies involved in

construction business.

Direct labor: Direct labor refers to the salaries and wages paid to workers

directly involved in the manufacture of a specific product or in performing a

service. The work performed must be related to the specific task. For a

business that provides services to its customers, direct labor is the work

performed by the workers who provide the service directly to the

customers, such as auditors, lawyers, and consultants. Examples of direct

labor cost include labor cost of machine operators and painters in a

manufacturing company. Like direct materials, it comprises of a

significant portion of total manufacturing cost.

The sum of direct materials cost and direct labor cost is known as

prime cost. Prime cost = Direct materials cost + Direct labor cost

Manufacturing overhead: Manufacturing costs other than direct materials

and direct labor are categorized as manufacturing overhead cost (also

known as factory overhead costs). They usually include indirect materials,

Costs may be classified as manufacturing costs and non-manufacturing

costs. This classification is usually used by manufacturing companies.

Manufacturing costs

Most manufacturing companies separate their manufacturing costs into two

direct cost categories, direct-materials and direct labor and in one indirect

cost categories, manufacturing overhead.

Direct materials

Direct labor

Manufacturing overhead

Direct materials: Direct material is the physical items built into a product.

For example, the direct materials for a baker include flour, eggs,

yeast, sugar, oil, and water. The direct materials concept is used in cost

accounting, where this cost is separately classified in several types of

financial analysis. Direct materials are rolled into the total cost of goods

produced, which is then subdivided into the cost of goods sold (which

appears in the income statement) and ending inventory (which appears in

the balance sheet). The finished product of a company may become raw

material of another company. For example, cement is a finished product for

manufacturers of cement and raw materials for companies involved in

construction business.

Direct labor: Direct labor refers to the salaries and wages paid to workers

directly involved in the manufacture of a specific product or in performing a

service. The work performed must be related to the specific task. For a

business that provides services to its customers, direct labor is the work

performed by the workers who provide the service directly to the

customers, such as auditors, lawyers, and consultants. Examples of direct

labor cost include labor cost of machine operators and painters in a

manufacturing company. Like direct materials, it comprises of a

significant portion of total manufacturing cost.

The sum of direct materials cost and direct labor cost is known as

prime cost. Prime cost = Direct materials cost + Direct labor cost

Manufacturing overhead: Manufacturing costs other than direct materials

and direct labor are categorized as manufacturing overhead cost (also

known as factory overhead costs). They usually include indirect materials,

indirect labor, salary of supervisor, lighting, heat and insurance cost of

factory etc. Mostly, manufacturing overhead costs cannot be easily traced

to individual units of finished products. The three types of overhead costs

are:

Fixed: These costs do not change each month. Also, business activity

does not cause these costs to change. Fixed overhead costs include

rent, mortgage, government fees and property taxes.

Variable: These are costs that can change with production output.

These items include some operational utilities such as electric, gas and

trash service. Output can also impact shipping costs, maintenance

situations, legal fees and advertising.

Semi-variable: These items might change over time with increased or

decreased business activity. Business activities may determine the

initial costs but over time, as activity changes, these costs may

increase or decrease. Some examples of semi-variable costs may

include operational utilities, rent or leasing and insurance.

The sum of direct labor cost and manufacturing overhead cost is

known as conversion cost. Conversion cost = Direct labor cost +

Manufacturing overhead cost.

Non-manufacturing costs

Non-manufacturing costs are further divided into the following categories:

Marketing and selling costs

Administrative costs

Examples of marketing and selling costs include advertising costs, order

taking costs and salaries of sales persons etc. Examples of administrative

costs include salaries of executives, accounting costs, and general

administration costs etc.

Selling costs include all costs that are incurred to secure customer orders

and get the finished product to the customer. These costs are sometimes

called as order-getting and order-filling costs.

Administrative costs include all costs associated with the general

management of an organization rather than with manufacturing or selling.

Examples of administrative costs include executive compensation, general

accounting, pubic relations and similar costs.

factory etc. Mostly, manufacturing overhead costs cannot be easily traced

to individual units of finished products. The three types of overhead costs

are:

Fixed: These costs do not change each month. Also, business activity

does not cause these costs to change. Fixed overhead costs include

rent, mortgage, government fees and property taxes.

Variable: These are costs that can change with production output.

These items include some operational utilities such as electric, gas and

trash service. Output can also impact shipping costs, maintenance

situations, legal fees and advertising.

Semi-variable: These items might change over time with increased or

decreased business activity. Business activities may determine the

initial costs but over time, as activity changes, these costs may

increase or decrease. Some examples of semi-variable costs may

include operational utilities, rent or leasing and insurance.

The sum of direct labor cost and manufacturing overhead cost is

known as conversion cost. Conversion cost = Direct labor cost +

Manufacturing overhead cost.

Non-manufacturing costs

Non-manufacturing costs are further divided into the following categories:

Marketing and selling costs

Administrative costs

Examples of marketing and selling costs include advertising costs, order

taking costs and salaries of sales persons etc. Examples of administrative

costs include salaries of executives, accounting costs, and general

administration costs etc.

Selling costs include all costs that are incurred to secure customer orders

and get the finished product to the customer. These costs are sometimes

called as order-getting and order-filling costs.

Administrative costs include all costs associated with the general

management of an organization rather than with manufacturing or selling.

Examples of administrative costs include executive compensation, general

accounting, pubic relations and similar costs.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Cost classifications for preparing financial statements

When preparing a balance sheet and an income statement, companies need

to classify their costs as product cost and period cost. To understand the

differences between product cost and period costs, we must first discuss the

matching principle from financial accounting. The matching principle is

based on the accrual concept the costs incurred to generate a particular

revenue should be recognized as expenses in the same period that the

revenue is recognized. Matching Principle is a common accounting concept.

Under this, a company should report an expense in the income statement in

the same period when it earns the revenue.

Product costs

Product cost refers to the costs incurred to create a product. These costs

include direct labor, direct materials, consumable production supplies, and

factory overhead. Product cost can also be considered the cost of the labor

required to deliver a service to a customer. The cost of a product on a unit

basis is typically derived by compiling the costs associated with a batch of

units that were produced as a group, and dividing by the number of units

manufactured. The calculation is:

(Total direct labor + Total direct materials + Consumable supplies

+ Total allocated overhead) ÷ Total number of units = Product unit

cost

These costs are also known as inventoriable costs.

Period costs

Period costs are costs that cannot be capitalized on a company’s balance

sheet. In other words, they are expensed in the period incurred and appear

on the income statement. Period costs are also called period expenses. In

managerial and cost accounting, period costs refer to costs that are not tied

to or related to the production of inventory. Examples include selling,

general and administrative (SG&A) expenses, marketing expenses, CEO

salary, and rent expense relating to a corporate office. The costs are not

related to the production of inventory and are therefore expensed in the

period incurred. In short, all costs that are not involved in the production of

a product (product costs) are period costs.

Prime cost and conversion cost

When preparing a balance sheet and an income statement, companies need

to classify their costs as product cost and period cost. To understand the

differences between product cost and period costs, we must first discuss the

matching principle from financial accounting. The matching principle is

based on the accrual concept the costs incurred to generate a particular

revenue should be recognized as expenses in the same period that the

revenue is recognized. Matching Principle is a common accounting concept.

Under this, a company should report an expense in the income statement in

the same period when it earns the revenue.

Product costs

Product cost refers to the costs incurred to create a product. These costs

include direct labor, direct materials, consumable production supplies, and

factory overhead. Product cost can also be considered the cost of the labor

required to deliver a service to a customer. The cost of a product on a unit

basis is typically derived by compiling the costs associated with a batch of

units that were produced as a group, and dividing by the number of units

manufactured. The calculation is:

(Total direct labor + Total direct materials + Consumable supplies

+ Total allocated overhead) ÷ Total number of units = Product unit

cost

These costs are also known as inventoriable costs.

Period costs

Period costs are costs that cannot be capitalized on a company’s balance

sheet. In other words, they are expensed in the period incurred and appear

on the income statement. Period costs are also called period expenses. In

managerial and cost accounting, period costs refer to costs that are not tied

to or related to the production of inventory. Examples include selling,

general and administrative (SG&A) expenses, marketing expenses, CEO

salary, and rent expense relating to a corporate office. The costs are not

related to the production of inventory and are therefore expensed in the

period incurred. In short, all costs that are not involved in the production of

a product (product costs) are period costs.

Prime cost and conversion cost

Prime costs are the sum of direct material costs and

direct labor costs. Conversion cost is the sum of direct

labor costs and manufacturing overhead.

Cost classifications for predicting cost behavior

Variable cost

Variable costs are expenses that vary in proportion to the volume of goods

or services that a business produces. In other words, they are costs that

vary depending on the volume of activity. The costs increase as the volume

of activities increases and decrease as the volume of activities decreases.

For a cost to be variable, it must be variable with respect to something. That

something is its activity based. An activity base is a measure of whatever

causes the incurrence of a variable cost. A activity base is sometimes

referred to as a cost driver.

Fixed cost

The term fixed cost refers to a cost that does not change with an increase or

decrease in the number of goods or services produced or sold. Fixed costs

are expenses that have to be paid by a company, independent of any

specific business activities. This means fixed costs are generally indirect, in

that they don't apply to a company's production of any goods or services.

Let us say, in a milk factory, the monthly payments for the

phone lines and security system and the monthly rent for the

facilities are fixed costs as they do not change according to

how much milk the factory produces. On the other hand, the

factory’s wage costs are variable as it will need to hire more

workers if the production increases. An analytical formula can

track the relationship between fixed cost and variable cost in

management accounting. It is important to know how total

costs are divided between the two types of costs. The division

of the costs is critical, and forecasting the earnings generated

by various changes in unit sales affects future planned

marketing campaigns. Discretionary fixed costs usually come

about from decisions made by management to spend on

certain fixed cost items. Examples of discretionary costs

include advertising, machinery maintenance, and research and

development (R&D) expenditures.

Committed fixed costs represent organizational investments with a

multiyear planning horizon that cannot be significantly reduced

direct labor costs. Conversion cost is the sum of direct

labor costs and manufacturing overhead.

Cost classifications for predicting cost behavior

Variable cost

Variable costs are expenses that vary in proportion to the volume of goods

or services that a business produces. In other words, they are costs that

vary depending on the volume of activity. The costs increase as the volume

of activities increases and decrease as the volume of activities decreases.

For a cost to be variable, it must be variable with respect to something. That

something is its activity based. An activity base is a measure of whatever

causes the incurrence of a variable cost. A activity base is sometimes

referred to as a cost driver.

Fixed cost

The term fixed cost refers to a cost that does not change with an increase or

decrease in the number of goods or services produced or sold. Fixed costs

are expenses that have to be paid by a company, independent of any

specific business activities. This means fixed costs are generally indirect, in

that they don't apply to a company's production of any goods or services.

Let us say, in a milk factory, the monthly payments for the

phone lines and security system and the monthly rent for the

facilities are fixed costs as they do not change according to

how much milk the factory produces. On the other hand, the

factory’s wage costs are variable as it will need to hire more

workers if the production increases. An analytical formula can

track the relationship between fixed cost and variable cost in

management accounting. It is important to know how total

costs are divided between the two types of costs. The division

of the costs is critical, and forecasting the earnings generated

by various changes in unit sales affects future planned

marketing campaigns. Discretionary fixed costs usually come

about from decisions made by management to spend on

certain fixed cost items. Examples of discretionary costs

include advertising, machinery maintenance, and research and

development (R&D) expenditures.

Committed fixed costs represent organizational investments with a

multiyear planning horizon that cannot be significantly reduced

ever for short period of time without making fundamental changes.

Discretionary fixed costs usually arise from annual decisions by

management to spend on certain fixed cost items.

Mixed costs

A mixed cost is an expense that has attributes of both fixed and variable

costs. In other words, it’s a cost that changes with the volume of production

like a variable cost and can’t be completely eliminated like a fixed cost.

Wage costs for employees who are paid a monthly salary plus commissions

are a good example of mixed costs. This is a common compensation

package for salesmen and sales reps. They usually receive a small base

salary and commissions based on how many sales they make during the

period.

The monthly salary is a fixed cost because it can’t be eliminated. Even if the

salesperson doesn’t sell anything during the month, the company still has to

pay the base salary.

The commission, on the other hand, acts more like a variable cost because

it’s based on the productivity of the employee. The more the employee sells

the greater the sales commission expense becomes. The company can

eliminate this expense altogether if it doesn’t sell anything for the month.

Cost classifications for decision making

Differential cost and revenue

A difference in costs between two alternatives is known as a differential

cost. A difference in revenues between two alternatives is known as

differential revenue.

A differential cost is also known as an incremental cost, although technically

an incremental cost should refer only to an increase in cost from one

alternative to another; decreases in costs should be referred to as

decremental cost. Differential cost is a broader term, encompassing both

cost increases and cost decreases between alternatives.

Opportunity cost and sunk cost

Opportunity cost is the potential benefit that is given up when one

alternative is selected over another. A sunk cost is a cost that has already

been incurred and that cannot be changed by any decision made now or in

the future. Because sunk costs cannot be changed by any decision made

Discretionary fixed costs usually arise from annual decisions by

management to spend on certain fixed cost items.

Mixed costs

A mixed cost is an expense that has attributes of both fixed and variable

costs. In other words, it’s a cost that changes with the volume of production

like a variable cost and can’t be completely eliminated like a fixed cost.

Wage costs for employees who are paid a monthly salary plus commissions

are a good example of mixed costs. This is a common compensation

package for salesmen and sales reps. They usually receive a small base

salary and commissions based on how many sales they make during the

period.

The monthly salary is a fixed cost because it can’t be eliminated. Even if the

salesperson doesn’t sell anything during the month, the company still has to

pay the base salary.

The commission, on the other hand, acts more like a variable cost because

it’s based on the productivity of the employee. The more the employee sells

the greater the sales commission expense becomes. The company can

eliminate this expense altogether if it doesn’t sell anything for the month.

Cost classifications for decision making

Differential cost and revenue

A difference in costs between two alternatives is known as a differential

cost. A difference in revenues between two alternatives is known as

differential revenue.

A differential cost is also known as an incremental cost, although technically

an incremental cost should refer only to an increase in cost from one

alternative to another; decreases in costs should be referred to as

decremental cost. Differential cost is a broader term, encompassing both

cost increases and cost decreases between alternatives.

Opportunity cost and sunk cost

Opportunity cost is the potential benefit that is given up when one

alternative is selected over another. A sunk cost is a cost that has already

been incurred and that cannot be changed by any decision made now or in

the future. Because sunk costs cannot be changed by any decision made

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

now or in the future. And because only differential costs are relevant in a

decision, sunk costs always be ignored.

The analysis of mixed cost

Mixed costs contain elements of both fixed and variable cost behavior. As

with step costs, the fixed elements are determined by the planned range of

activity level. We know of three methods for separating mixed costs into

their fixed and variable cost components:

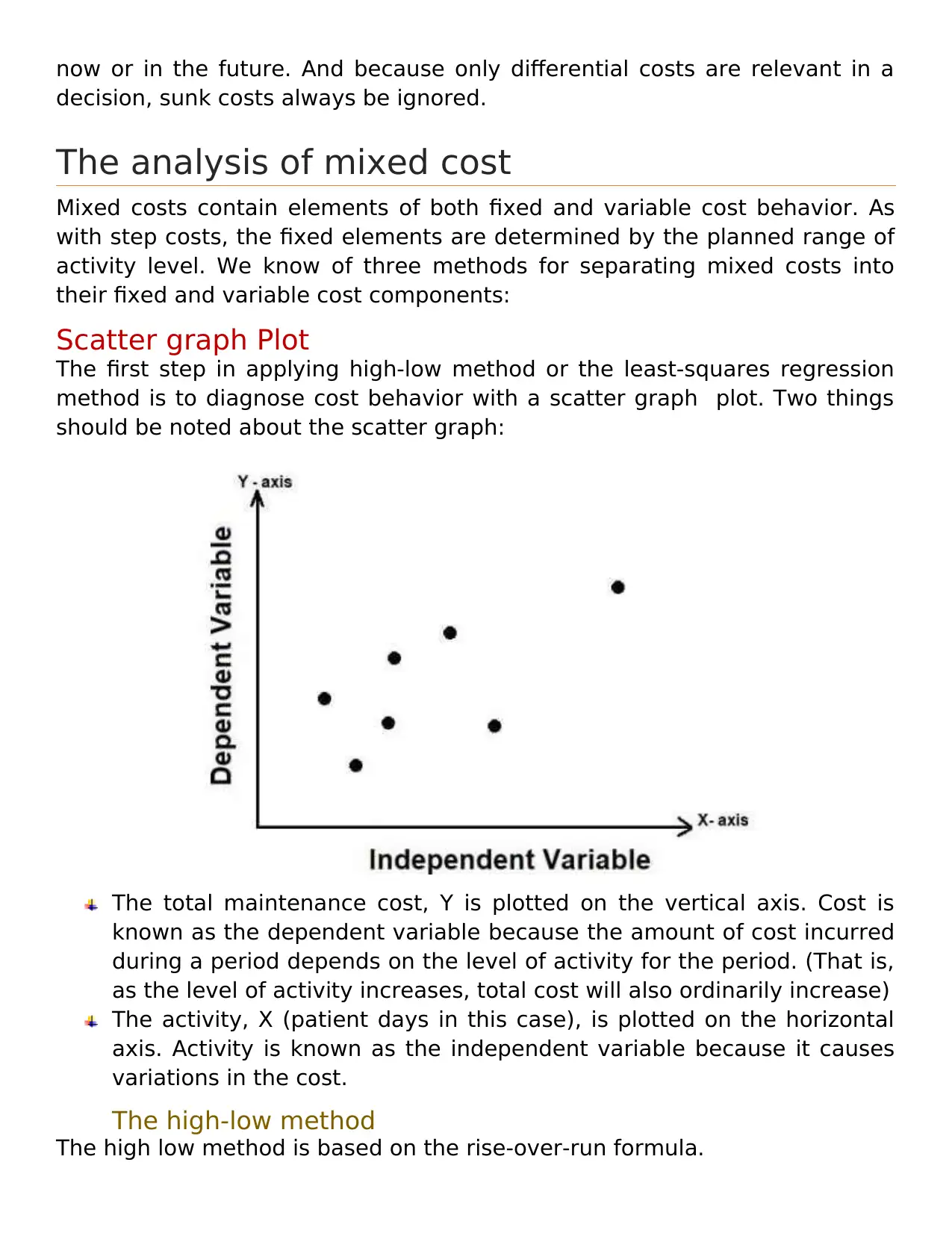

Scatter graph Plot

The first step in applying high-low method or the least-squares regression

method is to diagnose cost behavior with a scatter graph plot. Two things

should be noted about the scatter graph:

The total maintenance cost, Y is plotted on the vertical axis. Cost is

known as the dependent variable because the amount of cost incurred

during a period depends on the level of activity for the period. (That is,

as the level of activity increases, total cost will also ordinarily increase)

The activity, X (patient days in this case), is plotted on the horizontal

axis. Activity is known as the independent variable because it causes

variations in the cost.

The high-low method

The high low method is based on the rise-over-run formula.

decision, sunk costs always be ignored.

The analysis of mixed cost

Mixed costs contain elements of both fixed and variable cost behavior. As

with step costs, the fixed elements are determined by the planned range of

activity level. We know of three methods for separating mixed costs into

their fixed and variable cost components:

Scatter graph Plot

The first step in applying high-low method or the least-squares regression

method is to diagnose cost behavior with a scatter graph plot. Two things

should be noted about the scatter graph:

The total maintenance cost, Y is plotted on the vertical axis. Cost is

known as the dependent variable because the amount of cost incurred

during a period depends on the level of activity for the period. (That is,

as the level of activity increases, total cost will also ordinarily increase)

The activity, X (patient days in this case), is plotted on the horizontal

axis. Activity is known as the independent variable because it causes

variations in the cost.

The high-low method

The high low method is based on the rise-over-run formula.

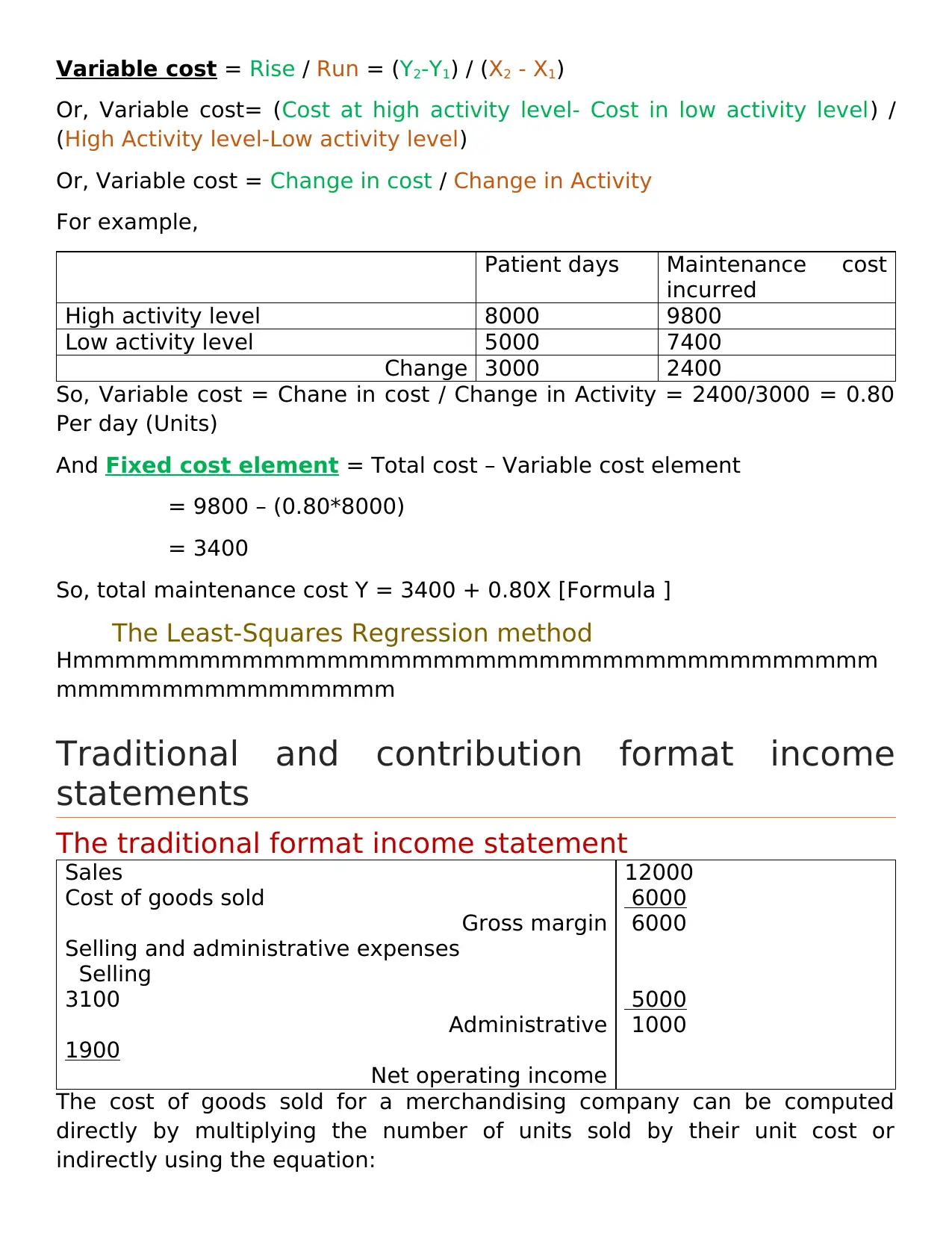

Variable cost = Rise / Run = (Y2-Y1) / (X2 - X1)

Or, Variable cost= (Cost at high activity level- Cost in low activity level) /

(High Activity level-Low activity level)

Or, Variable cost = Change in cost / Change in Activity

For example,

Patient days Maintenance cost

incurred

High activity level 8000 9800

Low activity level 5000 7400

Change 3000 2400

So, Variable cost = Chane in cost / Change in Activity = 2400/3000 = 0.80

Per day (Units)

And Fixed cost element = Total cost – Variable cost element

= 9800 – (0.80*8000)

= 3400

So, total maintenance cost Y = 3400 + 0.80X [Formula ]

The Least-Squares Regression method

Hmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmm

mmmmmmmmmmmmmmmm

Traditional and contribution format income

statements

The traditional format income statement

Sales

Cost of goods sold

Gross margin

Selling and administrative expenses

Selling

3100

Administrative

1900

Net operating income

12000

6000

6000

5000

1000

The cost of goods sold for a merchandising company can be computed

directly by multiplying the number of units sold by their unit cost or

indirectly using the equation:

Or, Variable cost= (Cost at high activity level- Cost in low activity level) /

(High Activity level-Low activity level)

Or, Variable cost = Change in cost / Change in Activity

For example,

Patient days Maintenance cost

incurred

High activity level 8000 9800

Low activity level 5000 7400

Change 3000 2400

So, Variable cost = Chane in cost / Change in Activity = 2400/3000 = 0.80

Per day (Units)

And Fixed cost element = Total cost – Variable cost element

= 9800 – (0.80*8000)

= 3400

So, total maintenance cost Y = 3400 + 0.80X [Formula ]

The Least-Squares Regression method

Hmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmm

mmmmmmmmmmmmmmmm

Traditional and contribution format income

statements

The traditional format income statement

Sales

Cost of goods sold

Gross margin

Selling and administrative expenses

Selling

3100

Administrative

1900

Net operating income

12000

6000

6000

5000

1000

The cost of goods sold for a merchandising company can be computed

directly by multiplying the number of units sold by their unit cost or

indirectly using the equation:

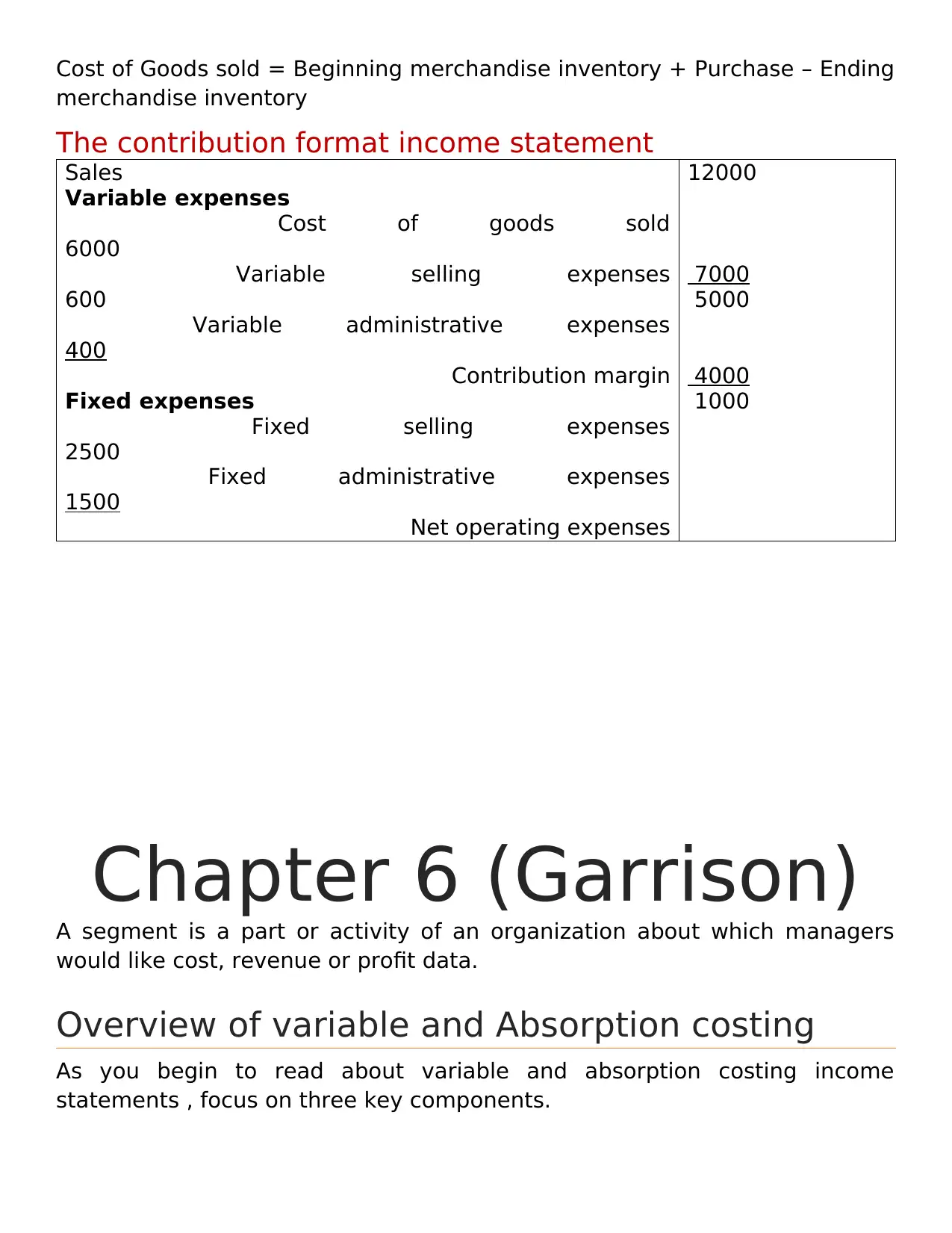

Cost of Goods sold = Beginning merchandise inventory + Purchase – Ending

merchandise inventory

The contribution format income statement

Sales

Variable expenses

Cost of goods sold

6000

Variable selling expenses

600

Variable administrative expenses

400

Contribution margin

Fixed expenses

Fixed selling expenses

2500

Fixed administrative expenses

1500

Net operating expenses

12000

7000

5000

4000

1000

Chapter 6 (Garrison)

A segment is a part or activity of an organization about which managers

would like cost, revenue or profit data.

Overview of variable and Absorption costing

As you begin to read about variable and absorption costing income

statements , focus on three key components.

merchandise inventory

The contribution format income statement

Sales

Variable expenses

Cost of goods sold

6000

Variable selling expenses

600

Variable administrative expenses

400

Contribution margin

Fixed expenses

Fixed selling expenses

2500

Fixed administrative expenses

1500

Net operating expenses

12000

7000

5000

4000

1000

Chapter 6 (Garrison)

A segment is a part or activity of an organization about which managers

would like cost, revenue or profit data.

Overview of variable and Absorption costing

As you begin to read about variable and absorption costing income

statements , focus on three key components.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

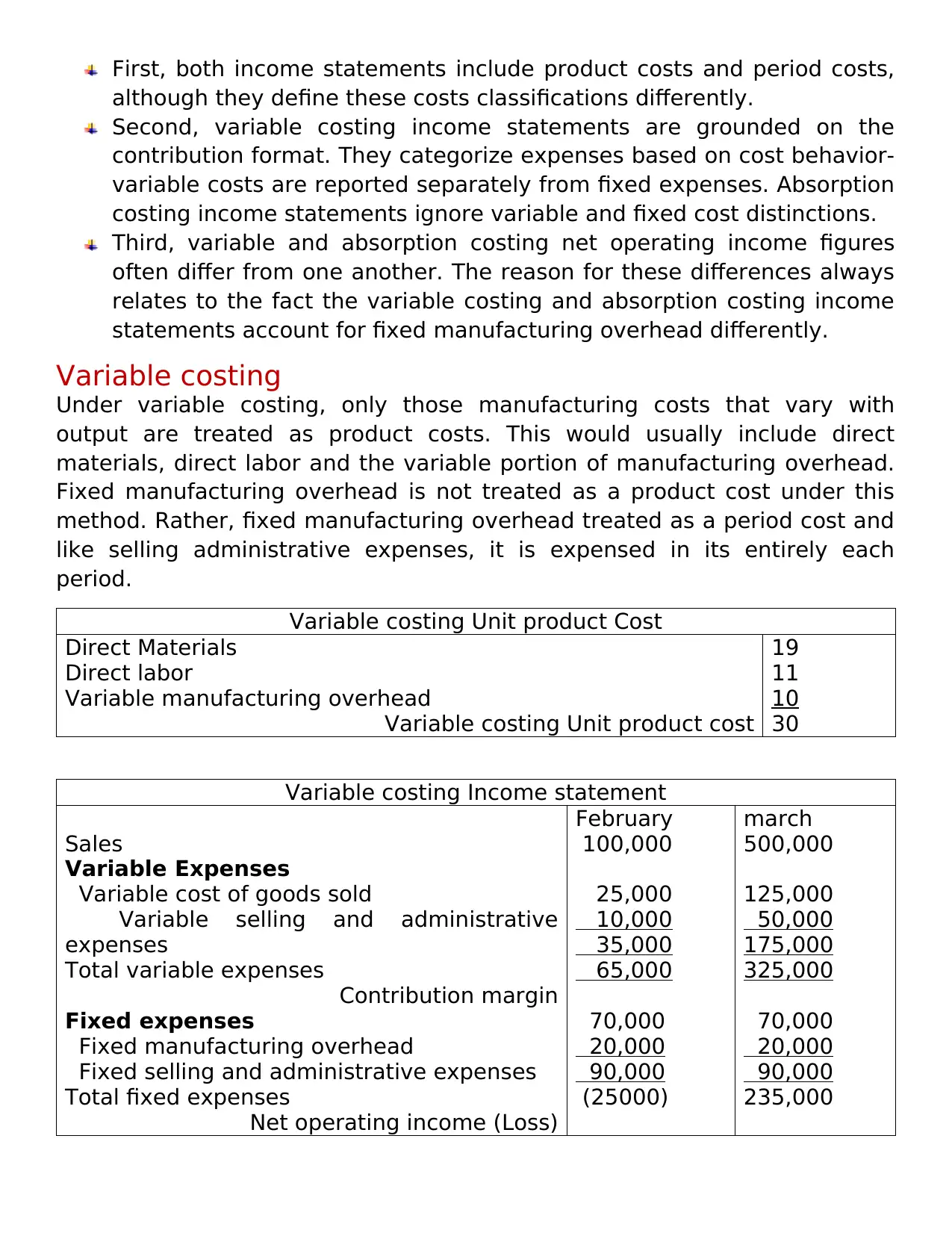

First, both income statements include product costs and period costs,

although they define these costs classifications differently.

Second, variable costing income statements are grounded on the

contribution format. They categorize expenses based on cost behavior-

variable costs are reported separately from fixed expenses. Absorption

costing income statements ignore variable and fixed cost distinctions.

Third, variable and absorption costing net operating income figures

often differ from one another. The reason for these differences always

relates to the fact the variable costing and absorption costing income

statements account for fixed manufacturing overhead differently.

Variable costing

Under variable costing, only those manufacturing costs that vary with

output are treated as product costs. This would usually include direct

materials, direct labor and the variable portion of manufacturing overhead.

Fixed manufacturing overhead is not treated as a product cost under this

method. Rather, fixed manufacturing overhead treated as a period cost and

like selling administrative expenses, it is expensed in its entirely each

period.

Variable costing Unit product Cost

Direct Materials

Direct labor

Variable manufacturing overhead

Variable costing Unit product cost

19

11

10

30

Variable costing Income statement

Sales

Variable Expenses

Variable cost of goods sold

Variable selling and administrative

expenses

Total variable expenses

Contribution margin

Fixed expenses

Fixed manufacturing overhead

Fixed selling and administrative expenses

Total fixed expenses

Net operating income (Loss)

February

100,000

25,000

10,000

35,000

65,000

70,000

20,000

90,000

(25000)

march

500,000

125,000

50,000

175,000

325,000

70,000

20,000

90,000

235,000

although they define these costs classifications differently.

Second, variable costing income statements are grounded on the

contribution format. They categorize expenses based on cost behavior-

variable costs are reported separately from fixed expenses. Absorption

costing income statements ignore variable and fixed cost distinctions.

Third, variable and absorption costing net operating income figures

often differ from one another. The reason for these differences always

relates to the fact the variable costing and absorption costing income

statements account for fixed manufacturing overhead differently.

Variable costing

Under variable costing, only those manufacturing costs that vary with

output are treated as product costs. This would usually include direct

materials, direct labor and the variable portion of manufacturing overhead.

Fixed manufacturing overhead is not treated as a product cost under this

method. Rather, fixed manufacturing overhead treated as a period cost and

like selling administrative expenses, it is expensed in its entirely each

period.

Variable costing Unit product Cost

Direct Materials

Direct labor

Variable manufacturing overhead

Variable costing Unit product cost

19

11

10

30

Variable costing Income statement

Sales

Variable Expenses

Variable cost of goods sold

Variable selling and administrative

expenses

Total variable expenses

Contribution margin

Fixed expenses

Fixed manufacturing overhead

Fixed selling and administrative expenses

Total fixed expenses

Net operating income (Loss)

February

100,000

25,000

10,000

35,000

65,000

70,000

20,000

90,000

(25000)

march

500,000

125,000

50,000

175,000

325,000

70,000

20,000

90,000

235,000

Absorption costing

Absorption costing treats all manufacturing costs as product costs,

regardless of whether they are variable or fixed. The cost of a unit of

product under the absorption costing method consist of direct materials,

direct labor and both variable and fixed manufacturing overhead. Thus,

absorption costing allocates a portion of fixed manufacturing overhead cost

to each unit of product, along with the variable manufacturing costs.

Because absorption costing includes all manufacturing costs in product

costs, it is frequently referred as the full cost method.

Absorption costing Unit product Cost

Direct Materials

Direct labor

Variable manufacturing overhead

Fixed manufacturing overhead

Variable costing Unit product cost

19

11

10

30

60

Absorption costing Income statement

Sales

Cost of goods sold (Unit product cost * total units)

Gross margin

Selling and administrative expenses

Net operating margin

Reconciliation of Variable costing with

absorption costing income

Step 1: The net operating incomes are reconciled as follows:

Year 1 Year 2

Units in beginning inventory

+ Units produced

- Units sold

= Units in ending inventory

0

50,000

40,000

10,000

10,000

40,000

50,000

0

Step 2:

Year 1 Year 2

Fixed manufacturing overhead in ending inventory

- fixed manufacturing overhead in beginning

inventory

= Manufacturing overhead differed in (released from)

inventory

50000

0

50000

0

50000

(50000)

Absorption costing treats all manufacturing costs as product costs,

regardless of whether they are variable or fixed. The cost of a unit of

product under the absorption costing method consist of direct materials,

direct labor and both variable and fixed manufacturing overhead. Thus,

absorption costing allocates a portion of fixed manufacturing overhead cost

to each unit of product, along with the variable manufacturing costs.

Because absorption costing includes all manufacturing costs in product

costs, it is frequently referred as the full cost method.

Absorption costing Unit product Cost

Direct Materials

Direct labor

Variable manufacturing overhead

Fixed manufacturing overhead

Variable costing Unit product cost

19

11

10

30

60

Absorption costing Income statement

Sales

Cost of goods sold (Unit product cost * total units)

Gross margin

Selling and administrative expenses

Net operating margin

Reconciliation of Variable costing with

absorption costing income

Step 1: The net operating incomes are reconciled as follows:

Year 1 Year 2

Units in beginning inventory

+ Units produced

- Units sold

= Units in ending inventory

0

50,000

40,000

10,000

10,000

40,000

50,000

0

Step 2:

Year 1 Year 2

Fixed manufacturing overhead in ending inventory

- fixed manufacturing overhead in beginning

inventory

= Manufacturing overhead differed in (released from)

inventory

50000

0

50000

0

50000

(50000)

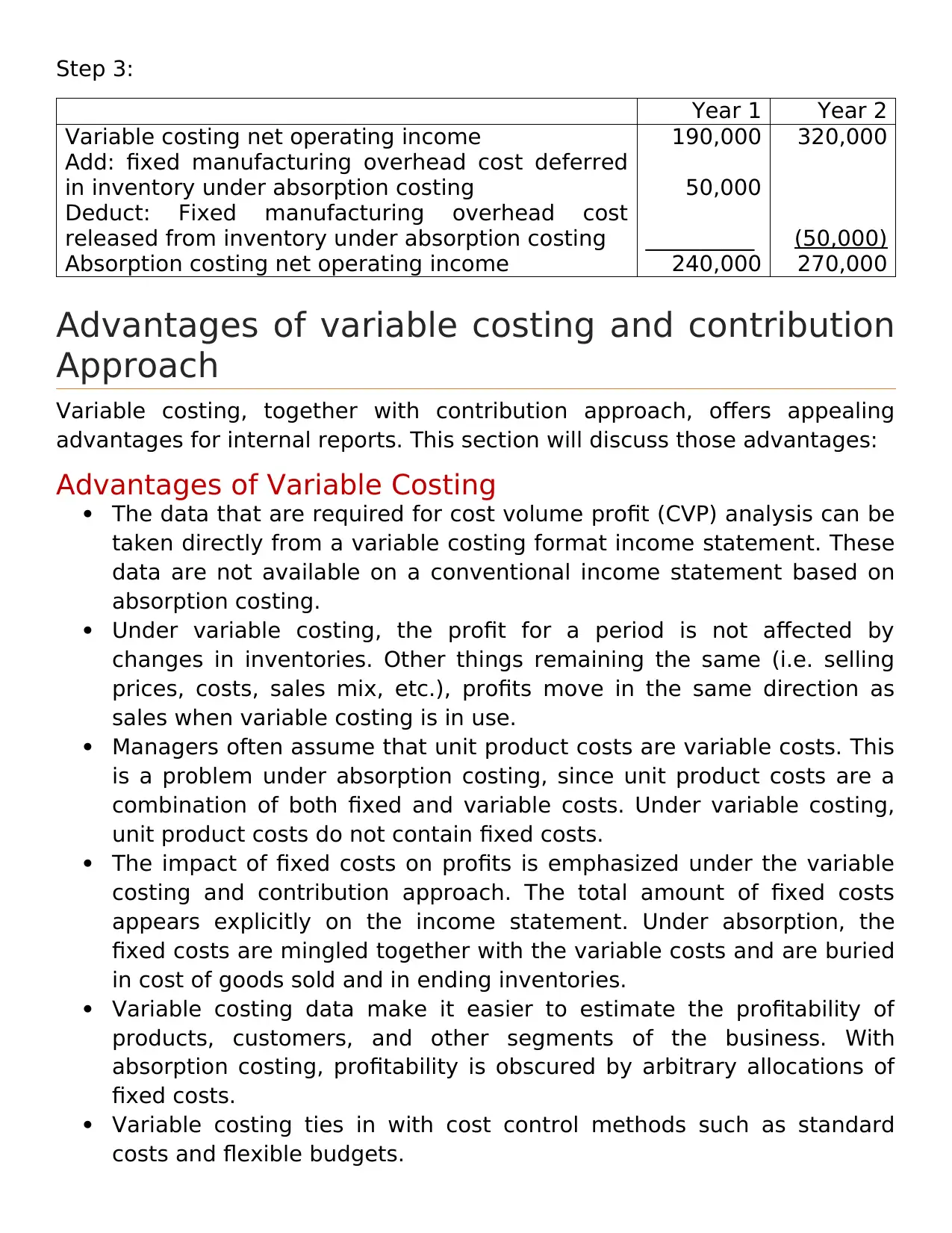

Step 3:

Year 1 Year 2

Variable costing net operating income

Add: fixed manufacturing overhead cost deferred

in inventory under absorption costing

Deduct: Fixed manufacturing overhead cost

released from inventory under absorption costing

Absorption costing net operating income

190,000

50,000

__________

240,000

320,000

(50,000)

270,000

Advantages of variable costing and contribution

Approach

Variable costing, together with contribution approach, offers appealing

advantages for internal reports. This section will discuss those advantages:

Advantages of Variable Costing

The data that are required for cost volume profit (CVP) analysis can be

taken directly from a variable costing format income statement. These

data are not available on a conventional income statement based on

absorption costing.

Under variable costing, the profit for a period is not affected by

changes in inventories. Other things remaining the same (i.e. selling

prices, costs, sales mix, etc.), profits move in the same direction as

sales when variable costing is in use.

Managers often assume that unit product costs are variable costs. This

is a problem under absorption costing, since unit product costs are a

combination of both fixed and variable costs. Under variable costing,

unit product costs do not contain fixed costs.

The impact of fixed costs on profits is emphasized under the variable

costing and contribution approach. The total amount of fixed costs

appears explicitly on the income statement. Under absorption, the

fixed costs are mingled together with the variable costs and are buried

in cost of goods sold and in ending inventories.

Variable costing data make it easier to estimate the profitability of

products, customers, and other segments of the business. With

absorption costing, profitability is obscured by arbitrary allocations of

fixed costs.

Variable costing ties in with cost control methods such as standard

costs and flexible budgets.

Year 1 Year 2

Variable costing net operating income

Add: fixed manufacturing overhead cost deferred

in inventory under absorption costing

Deduct: Fixed manufacturing overhead cost

released from inventory under absorption costing

Absorption costing net operating income

190,000

50,000

__________

240,000

320,000

(50,000)

270,000

Advantages of variable costing and contribution

Approach

Variable costing, together with contribution approach, offers appealing

advantages for internal reports. This section will discuss those advantages:

Advantages of Variable Costing

The data that are required for cost volume profit (CVP) analysis can be

taken directly from a variable costing format income statement. These

data are not available on a conventional income statement based on

absorption costing.

Under variable costing, the profit for a period is not affected by

changes in inventories. Other things remaining the same (i.e. selling

prices, costs, sales mix, etc.), profits move in the same direction as

sales when variable costing is in use.

Managers often assume that unit product costs are variable costs. This

is a problem under absorption costing, since unit product costs are a

combination of both fixed and variable costs. Under variable costing,

unit product costs do not contain fixed costs.

The impact of fixed costs on profits is emphasized under the variable

costing and contribution approach. The total amount of fixed costs

appears explicitly on the income statement. Under absorption, the

fixed costs are mingled together with the variable costs and are buried

in cost of goods sold and in ending inventories.

Variable costing data make it easier to estimate the profitability of

products, customers, and other segments of the business. With

absorption costing, profitability is obscured by arbitrary allocations of

fixed costs.

Variable costing ties in with cost control methods such as standard

costs and flexible budgets.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Variable costing net operating income is closer to net cash flow than

absorption costing net operating income. This is particularly important

for companies having cash flow problems.

Advantages of contribution approach

More useful for CVP analysis. Variable costing statements provide data

that are immediately useful for CVP analysis since they categorize

costs on the basis of their behavior. In contrast, itis often difficult to

rework absorption costing data so that they can be used in CVP

analysis and in decisions.

Income is not affected by changes in production volume. Under

absorption costing, reported net operating income is affected by

changes in production since fixed costs are spread across more or

fewer units. This can distort income and may even result in income

moving in an opposite direction from sales. This does not occur under

variable costing.

Avoids misunderstandings concerning unit product costs. Absorption

costing unit product costs can be easily misinterpreted as variable

costs since they are stated on a per unit basis. Such a misperception

can lead to serious errors in making decisions. Variable costing avoids

this problem since unit costs include only variable costs.

Fixed costs are more visible. The impact of fixed costs on profits is

emphasized because the total amount of such costs for the period

appears separately and is highlighted in the income statement rather

than being buried in cost of goods sold and ending inventory.

Understandability. Managers should find it easier to understand

variable costing reports because data are organized by behavior and

because variable costing is much closer to cash flow.

Control is facilitated. Variable costing ties in with cost control methods

such as flexible budgets.

Incremental analysis is more straight-forward. Variable cost

corresponds closely with the current out-of-pocket expenditure

necessary to produce and sell products and services and can therefore

be used more readily in incremental analysis than absorption costing

data. And since variable costing net operating income is closer to net

cash flow than absorption costing net operating income, it is likely to

be more useful to companies that have cash flow problems.

absorption costing net operating income. This is particularly important

for companies having cash flow problems.

Advantages of contribution approach

More useful for CVP analysis. Variable costing statements provide data

that are immediately useful for CVP analysis since they categorize

costs on the basis of their behavior. In contrast, itis often difficult to

rework absorption costing data so that they can be used in CVP

analysis and in decisions.

Income is not affected by changes in production volume. Under

absorption costing, reported net operating income is affected by

changes in production since fixed costs are spread across more or

fewer units. This can distort income and may even result in income

moving in an opposite direction from sales. This does not occur under

variable costing.

Avoids misunderstandings concerning unit product costs. Absorption

costing unit product costs can be easily misinterpreted as variable

costs since they are stated on a per unit basis. Such a misperception

can lead to serious errors in making decisions. Variable costing avoids

this problem since unit costs include only variable costs.

Fixed costs are more visible. The impact of fixed costs on profits is

emphasized because the total amount of such costs for the period

appears separately and is highlighted in the income statement rather

than being buried in cost of goods sold and ending inventory.

Understandability. Managers should find it easier to understand

variable costing reports because data are organized by behavior and

because variable costing is much closer to cash flow.

Control is facilitated. Variable costing ties in with cost control methods

such as flexible budgets.

Incremental analysis is more straight-forward. Variable cost

corresponds closely with the current out-of-pocket expenditure

necessary to produce and sell products and services and can therefore

be used more readily in incremental analysis than absorption costing

data. And since variable costing net operating income is closer to net

cash flow than absorption costing net operating income, it is likely to

be more useful to companies that have cash flow problems.

Traceable and common fixed costs and segment

margin

A traceable fixed cost of a segment is a fixed cost that is incurred because

of the existence of the segment- if the segment had never existed, the fixed

cost would not have been incurred; and if the segment were eliminated, the

fixed cost would disappear. For example, salary of the manager of a

segment.

A common fixed cost is a fixed cost that supports the operation of more

than one segment, but not traceable in whole or in part to any segment.

Even if a segment were entirely eliminated, there would be no change in a

true common fixed cost. For example, salary of the CEO.

A segment margin is obtained by deducting the traceable fixed costs of a

segment from the segment’s contribution margin. It represents the margin

available after a segment has covered all of its own costs.

Segment income statements-Decision making

and break-even analysis

Break-even analysis

Dollar sales for company to break even= (Traceable fixed expenses +

Common fixed expenses)/ overall CM ratio

Dollar sales for a segment to break-even= segment traceable fixed

expenses / Segment CM ratio

Chapter 8 (Garrison)

This chapter describes the details about preparing a master budget. The

master budget is an essential management tool that communicates

management’s plans throughout the organization, allocates resources, and

coordinates activities. A budget is a detailed plan for the future that is

usually expressed in formal quantitative terms. Once a budget is prepared,

actual spending is compared to the budget to make sure the plan is being

followed.

Budget is prepared for two distinct purposes- planning and controlling.

Planning involves developing goals and preparing various budgets to

margin

A traceable fixed cost of a segment is a fixed cost that is incurred because

of the existence of the segment- if the segment had never existed, the fixed

cost would not have been incurred; and if the segment were eliminated, the

fixed cost would disappear. For example, salary of the manager of a

segment.

A common fixed cost is a fixed cost that supports the operation of more

than one segment, but not traceable in whole or in part to any segment.

Even if a segment were entirely eliminated, there would be no change in a

true common fixed cost. For example, salary of the CEO.

A segment margin is obtained by deducting the traceable fixed costs of a

segment from the segment’s contribution margin. It represents the margin

available after a segment has covered all of its own costs.

Segment income statements-Decision making

and break-even analysis

Break-even analysis

Dollar sales for company to break even= (Traceable fixed expenses +

Common fixed expenses)/ overall CM ratio

Dollar sales for a segment to break-even= segment traceable fixed

expenses / Segment CM ratio

Chapter 8 (Garrison)

This chapter describes the details about preparing a master budget. The

master budget is an essential management tool that communicates

management’s plans throughout the organization, allocates resources, and

coordinates activities. A budget is a detailed plan for the future that is

usually expressed in formal quantitative terms. Once a budget is prepared,

actual spending is compared to the budget to make sure the plan is being

followed.

Budget is prepared for two distinct purposes- planning and controlling.

Planning involves developing goals and preparing various budgets to

achieve the goals. Control involves gathering feedback to ensure that plan

is being properly executed or modified as circumstances changed.

The basic idea underlying responsibility accounting is that a manager

should be held responsible for those items- and only those items- that the

manager can actually control to a significant extent.

The self-imposed budget

A self-imposed budget or participative budget is a budget that is prepared

with the full cooperation and participation of managers at all levels.

Imposed budgeting, also known as top-down budgeting, is the process

wherein the top management of a company prepares a budget and then

imposes it on lower-level managers for implementation. It starts at the top,

where the budget is prepared by senior management according to the goals

that the company wants to achieve in the next financial period.

Advantages: Below are some of the benefits of using the imposed

budgeting process over other forms of budgeting:

1. Greater efficiency

One of the benefits of using imposed budgeting is the efficiency that an

organization achieves. When a department is given an allocation by the

finance department, it must figure out how it will use that budget to achieve

the set targets and objectives of that department. The departmental heads

will be prudent in how they use the money. The prudent approach will help

reduce wastages and allocations to unnecessary expenditures.

2. Faster and less costly process

Imposed budgeting takes less time than bottom-up budgeting because it

only allows the input of key decision-makers. In the case of bottom-up

budgeting, the lower-level staff is required to contribute towards the budget

preparation at the department level. It will take a lot of time and effort

before the final budget is ready.

Imposed budgeting only allows input from a few people who have access to

key information on the company’s performance and, therefore, are better

placed to make suggestions.

3. Better financial control

is being properly executed or modified as circumstances changed.

The basic idea underlying responsibility accounting is that a manager

should be held responsible for those items- and only those items- that the

manager can actually control to a significant extent.

The self-imposed budget

A self-imposed budget or participative budget is a budget that is prepared

with the full cooperation and participation of managers at all levels.

Imposed budgeting, also known as top-down budgeting, is the process

wherein the top management of a company prepares a budget and then

imposes it on lower-level managers for implementation. It starts at the top,

where the budget is prepared by senior management according to the goals

that the company wants to achieve in the next financial period.

Advantages: Below are some of the benefits of using the imposed

budgeting process over other forms of budgeting:

1. Greater efficiency

One of the benefits of using imposed budgeting is the efficiency that an

organization achieves. When a department is given an allocation by the

finance department, it must figure out how it will use that budget to achieve

the set targets and objectives of that department. The departmental heads

will be prudent in how they use the money. The prudent approach will help

reduce wastages and allocations to unnecessary expenditures.

2. Faster and less costly process

Imposed budgeting takes less time than bottom-up budgeting because it

only allows the input of key decision-makers. In the case of bottom-up

budgeting, the lower-level staff is required to contribute towards the budget

preparation at the department level. It will take a lot of time and effort

before the final budget is ready.

Imposed budgeting only allows input from a few people who have access to

key information on the company’s performance and, therefore, are better

placed to make suggestions.

3. Better financial control

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Imposed budgeting gives management better control over the company’s

financials. Management starts by evaluating the company’s financial needs

and the expense budget required to meet its needs and generate revenues.

It gives them better control in determining how much of the total budget

goes to specific departments, depending on past performance and revenue

projections.

Limitations: The following are some of the limitations of using imposed

budgeting:

1. Lack of motivation

When lower-level staff is not involved in the budget preparation process,

they will feel demotivated because their input is not required. This may

result in tension and loss of productivity.

2. Decline in performance

Imposed budgeting requires departments to prepare their budgets within

the limits of the amounts allocated to them. This means that a department

that requires additional funding to finance its activities will need to work

with the funds allocated from the top management. Lower-level managers

may even use it as an excuse for failing to meet the revenue targets

imposed by the management.

The Master Budgeting

A master budget can be defined as the aggregation of all the lower level

budgets, which are calculated by various functional areas of the business

and is a strategy that documents the financial statements, cash flow

forecast, financial plans, and capital investments.

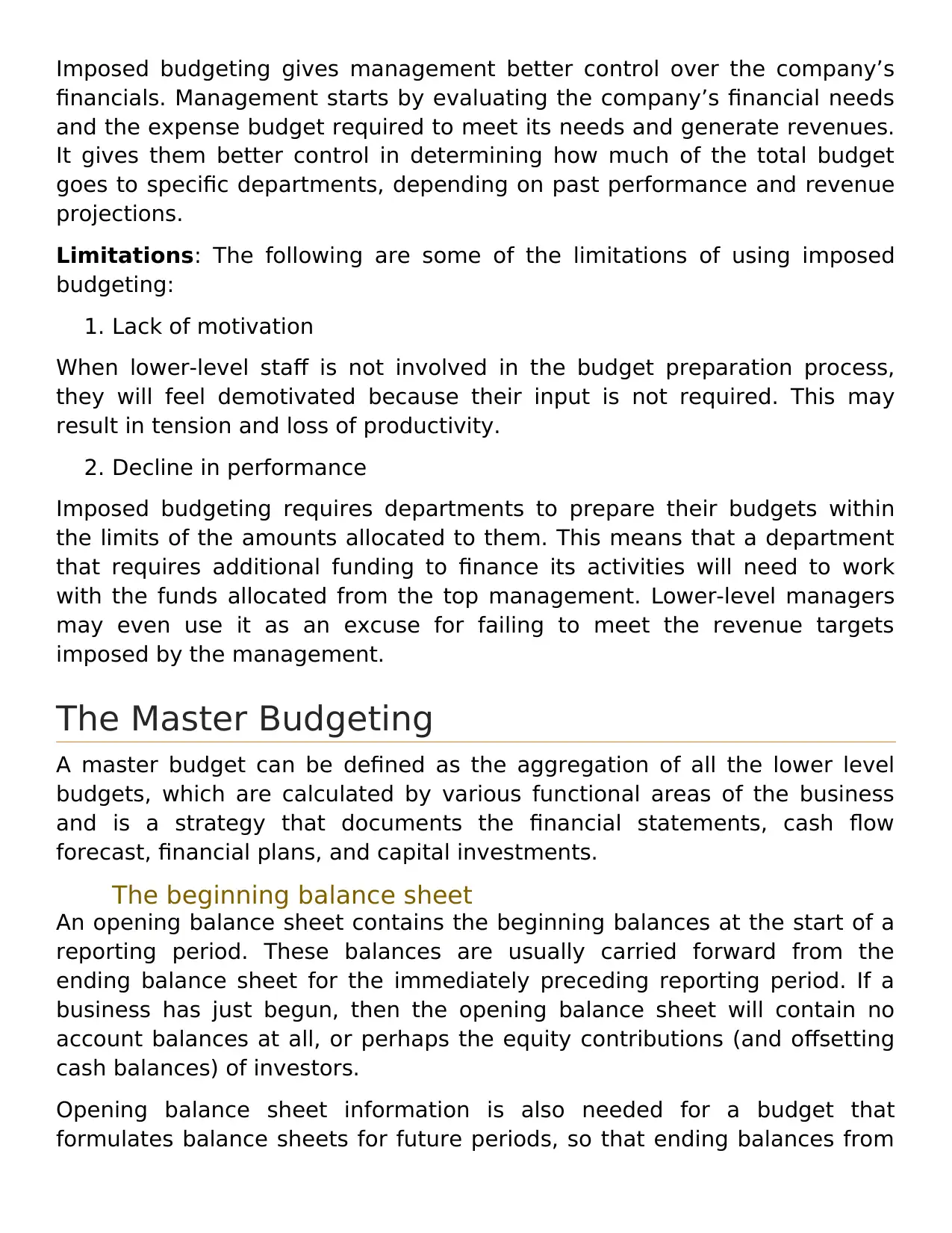

The beginning balance sheet

An opening balance sheet contains the beginning balances at the start of a

reporting period. These balances are usually carried forward from the

ending balance sheet for the immediately preceding reporting period. If a

business has just begun, then the opening balance sheet will contain no

account balances at all, or perhaps the equity contributions (and offsetting

cash balances) of investors.

Opening balance sheet information is also needed for a budget that

formulates balance sheets for future periods, so that ending balances from

financials. Management starts by evaluating the company’s financial needs

and the expense budget required to meet its needs and generate revenues.

It gives them better control in determining how much of the total budget

goes to specific departments, depending on past performance and revenue

projections.

Limitations: The following are some of the limitations of using imposed

budgeting:

1. Lack of motivation

When lower-level staff is not involved in the budget preparation process,

they will feel demotivated because their input is not required. This may

result in tension and loss of productivity.

2. Decline in performance

Imposed budgeting requires departments to prepare their budgets within

the limits of the amounts allocated to them. This means that a department

that requires additional funding to finance its activities will need to work

with the funds allocated from the top management. Lower-level managers

may even use it as an excuse for failing to meet the revenue targets

imposed by the management.

The Master Budgeting

A master budget can be defined as the aggregation of all the lower level

budgets, which are calculated by various functional areas of the business

and is a strategy that documents the financial statements, cash flow

forecast, financial plans, and capital investments.

The beginning balance sheet

An opening balance sheet contains the beginning balances at the start of a

reporting period. These balances are usually carried forward from the

ending balance sheet for the immediately preceding reporting period. If a

business has just begun, then the opening balance sheet will contain no

account balances at all, or perhaps the equity contributions (and offsetting

cash balances) of investors.

Opening balance sheet information is also needed for a budget that

formulates balance sheets for future periods, so that ending balances from

the last actual period are incorporated into the ongoing balance sheet

calculations.

The budgeting Assumption

For both business and personal budgeting purposes, budget assumptions

are expectations -- usually expected or presumed income and expenses.

Making reasonable assumptions when creating a budget for the first time

gives you starting numbers to work with for planning purposes.

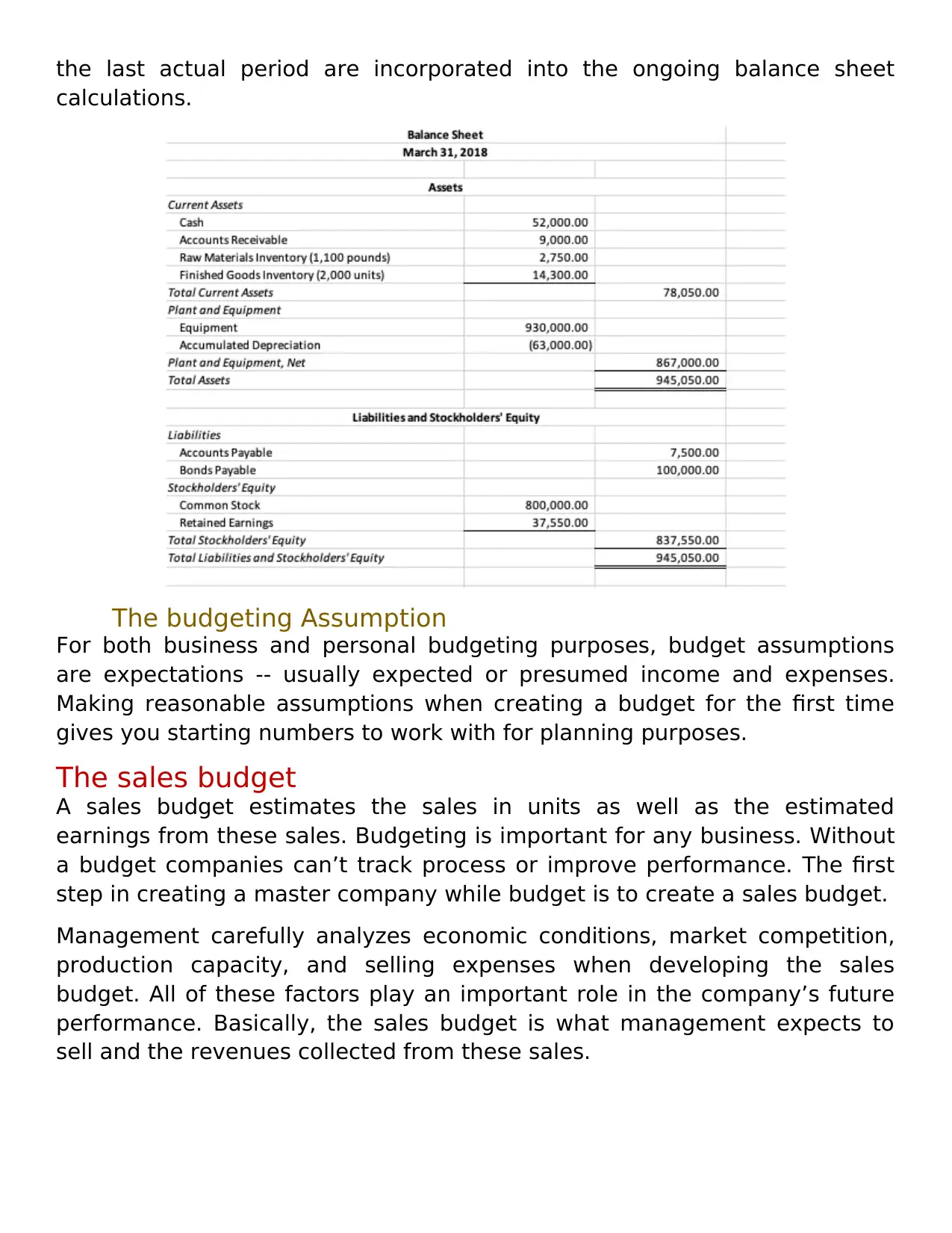

The sales budget

A sales budget estimates the sales in units as well as the estimated

earnings from these sales. Budgeting is important for any business. Without

a budget companies can’t track process or improve performance. The first

step in creating a master company while budget is to create a sales budget.

Management carefully analyzes economic conditions, market competition,

production capacity, and selling expenses when developing the sales

budget. All of these factors play an important role in the company’s future

performance. Basically, the sales budget is what management expects to

sell and the revenues collected from these sales.

calculations.

The budgeting Assumption

For both business and personal budgeting purposes, budget assumptions

are expectations -- usually expected or presumed income and expenses.

Making reasonable assumptions when creating a budget for the first time

gives you starting numbers to work with for planning purposes.

The sales budget

A sales budget estimates the sales in units as well as the estimated

earnings from these sales. Budgeting is important for any business. Without

a budget companies can’t track process or improve performance. The first

step in creating a master company while budget is to create a sales budget.

Management carefully analyzes economic conditions, market competition,

production capacity, and selling expenses when developing the sales

budget. All of these factors play an important role in the company’s future

performance. Basically, the sales budget is what management expects to

sell and the revenues collected from these sales.

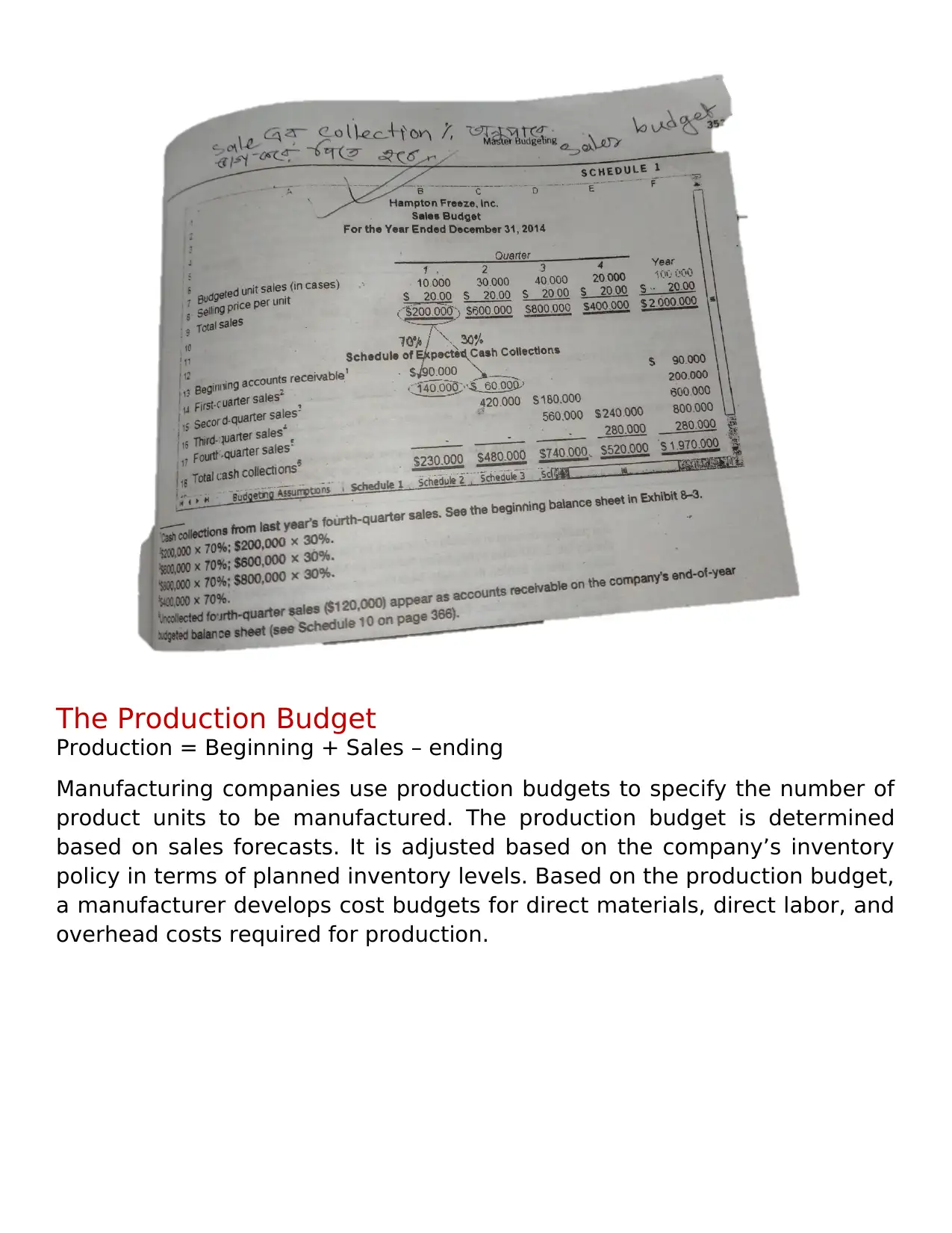

The Production Budget

Production = Beginning + Sales – ending

Manufacturing companies use production budgets to specify the number of

product units to be manufactured. The production budget is determined

based on sales forecasts. It is adjusted based on the company’s inventory

policy in terms of planned inventory levels. Based on the production budget,

a manufacturer develops cost budgets for direct materials, direct labor, and

overhead costs required for production.

Production = Beginning + Sales – ending

Manufacturing companies use production budgets to specify the number of

product units to be manufactured. The production budget is determined

based on sales forecasts. It is adjusted based on the company’s inventory

policy in terms of planned inventory levels. Based on the production budget,

a manufacturer develops cost budgets for direct materials, direct labor, and

overhead costs required for production.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

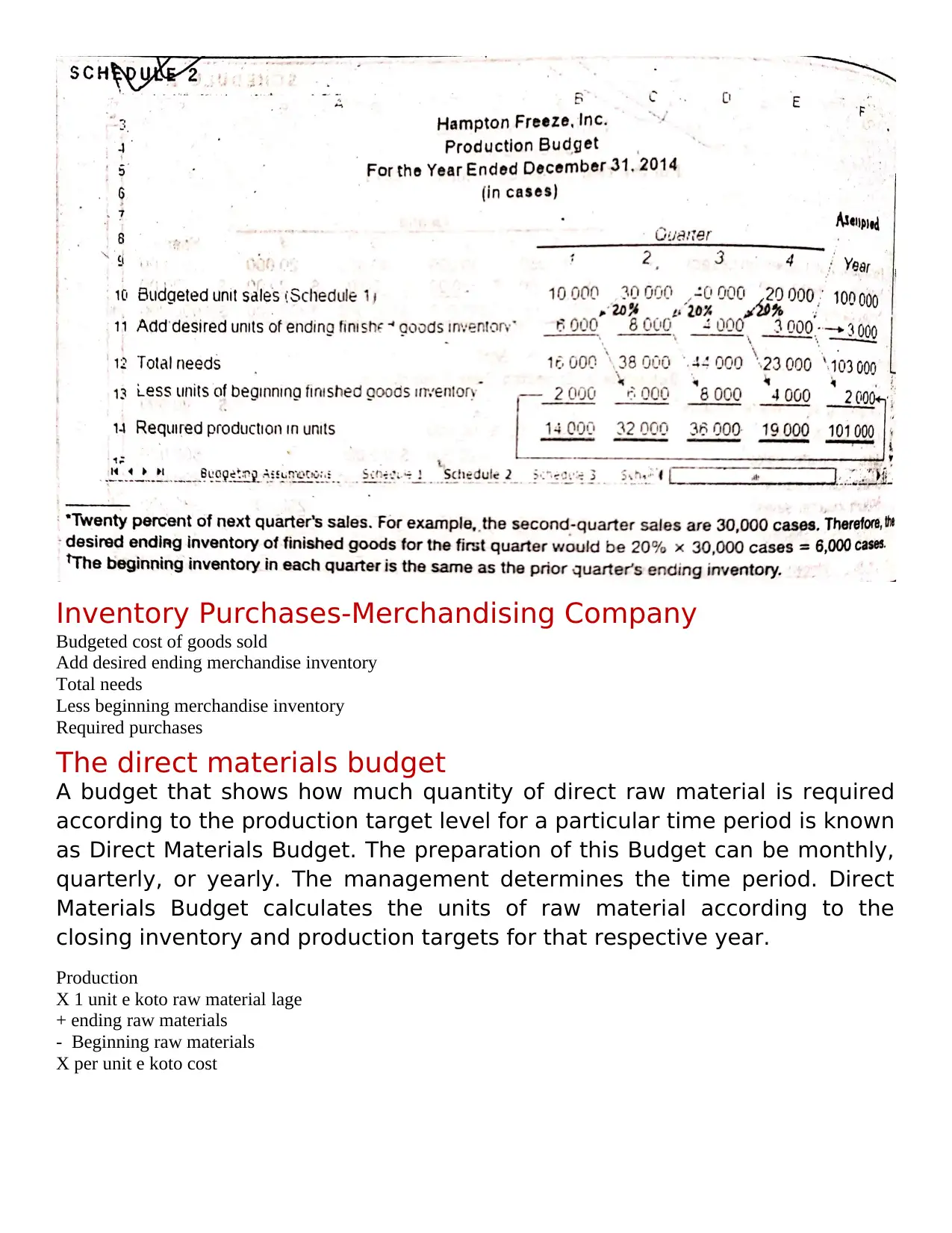

Inventory Purchases-Merchandising Company

Budgeted cost of goods sold

Add desired ending merchandise inventory

Total needs

Less beginning merchandise inventory

Required purchases

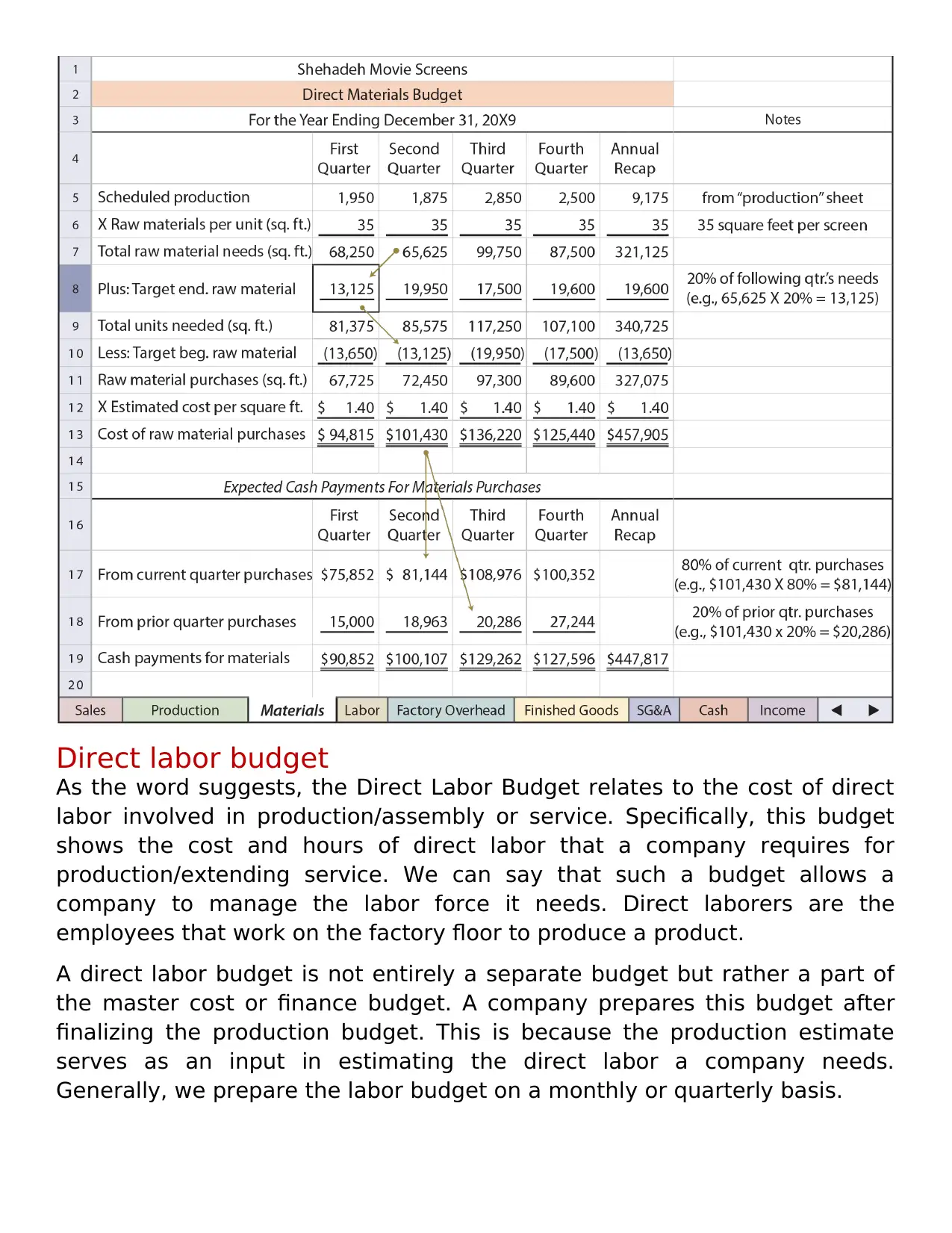

The direct materials budget

A budget that shows how much quantity of direct raw material is required

according to the production target level for a particular time period is known

as Direct Materials Budget. The preparation of this Budget can be monthly,

quarterly, or yearly. The management determines the time period. Direct

Materials Budget calculates the units of raw material according to the

closing inventory and production targets for that respective year.

Production

X 1 unit e koto raw material lage

+ ending raw materials

- Beginning raw materials

X per unit e koto cost

Budgeted cost of goods sold

Add desired ending merchandise inventory

Total needs

Less beginning merchandise inventory

Required purchases

The direct materials budget

A budget that shows how much quantity of direct raw material is required

according to the production target level for a particular time period is known

as Direct Materials Budget. The preparation of this Budget can be monthly,

quarterly, or yearly. The management determines the time period. Direct

Materials Budget calculates the units of raw material according to the

closing inventory and production targets for that respective year.

Production

X 1 unit e koto raw material lage

+ ending raw materials

- Beginning raw materials

X per unit e koto cost

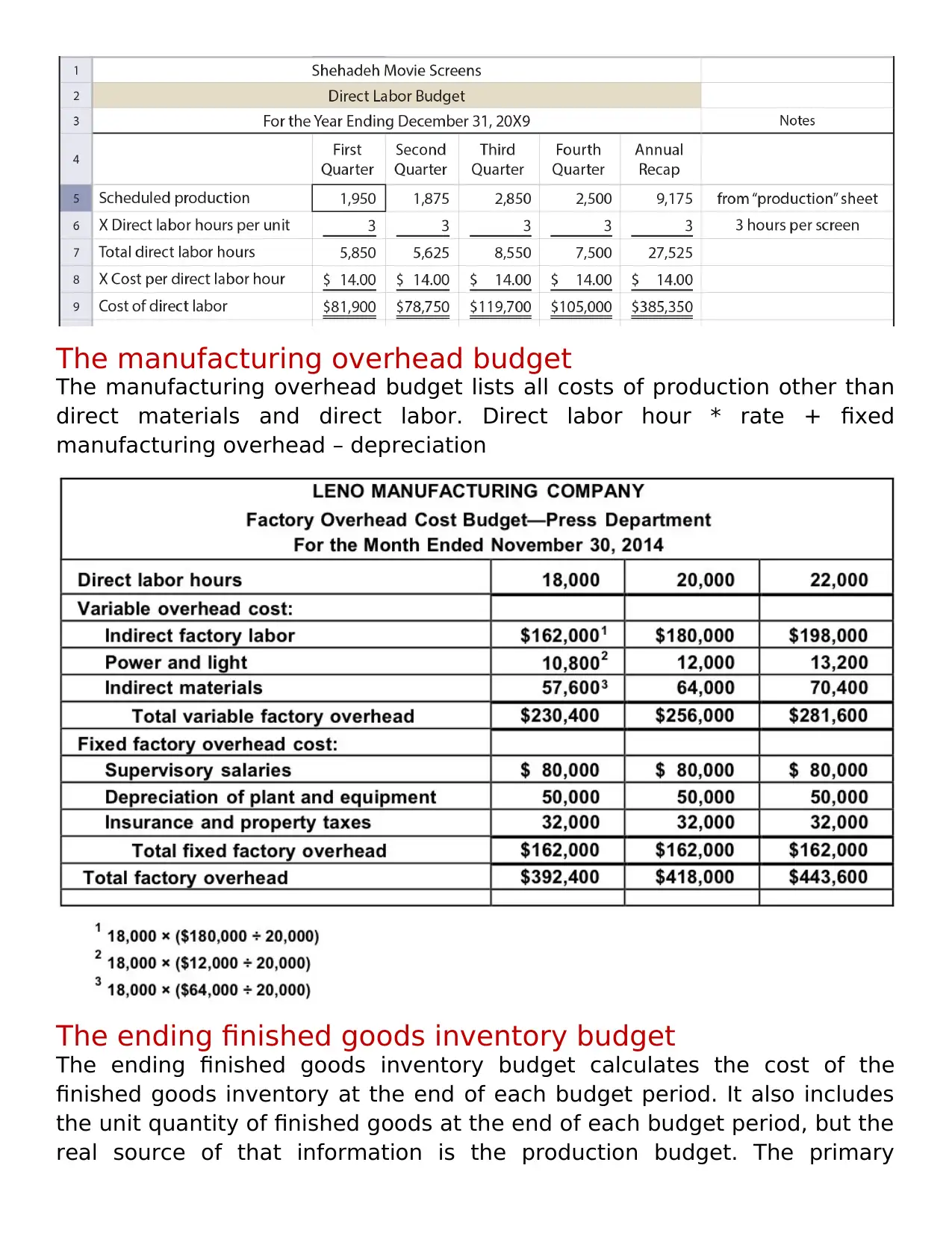

Direct labor budget

As the word suggests, the Direct Labor Budget relates to the cost of direct

labor involved in production/assembly or service. Specifically, this budget

shows the cost and hours of direct labor that a company requires for

production/extending service. We can say that such a budget allows a

company to manage the labor force it needs. Direct laborers are the

employees that work on the factory floor to produce a product.

A direct labor budget is not entirely a separate budget but rather a part of

the master cost or finance budget. A company prepares this budget after

finalizing the production budget. This is because the production estimate

serves as an input in estimating the direct labor a company needs.

Generally, we prepare the labor budget on a monthly or quarterly basis.

As the word suggests, the Direct Labor Budget relates to the cost of direct

labor involved in production/assembly or service. Specifically, this budget

shows the cost and hours of direct labor that a company requires for

production/extending service. We can say that such a budget allows a

company to manage the labor force it needs. Direct laborers are the

employees that work on the factory floor to produce a product.

A direct labor budget is not entirely a separate budget but rather a part of

the master cost or finance budget. A company prepares this budget after

finalizing the production budget. This is because the production estimate

serves as an input in estimating the direct labor a company needs.

Generally, we prepare the labor budget on a monthly or quarterly basis.

The manufacturing overhead budget

The manufacturing overhead budget lists all costs of production other than

direct materials and direct labor. Direct labor hour * rate + fixed

manufacturing overhead – depreciation

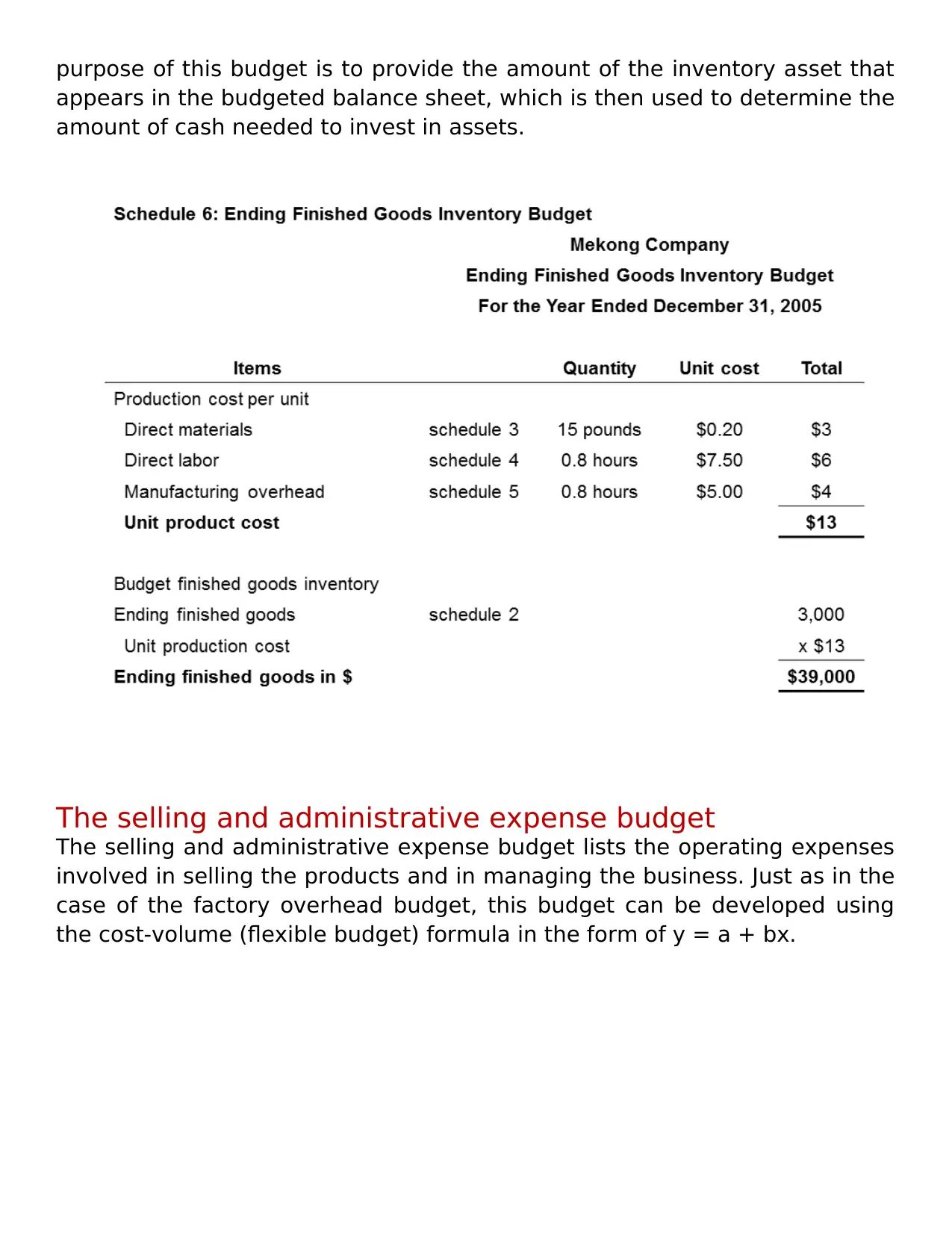

The ending finished goods inventory budget

The ending finished goods inventory budget calculates the cost of the

finished goods inventory at the end of each budget period. It also includes

the unit quantity of finished goods at the end of each budget period, but the

real source of that information is the production budget. The primary

The manufacturing overhead budget lists all costs of production other than

direct materials and direct labor. Direct labor hour * rate + fixed

manufacturing overhead – depreciation

The ending finished goods inventory budget

The ending finished goods inventory budget calculates the cost of the

finished goods inventory at the end of each budget period. It also includes

the unit quantity of finished goods at the end of each budget period, but the

real source of that information is the production budget. The primary

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

purpose of this budget is to provide the amount of the inventory asset that

appears in the budgeted balance sheet, which is then used to determine the

amount of cash needed to invest in assets.

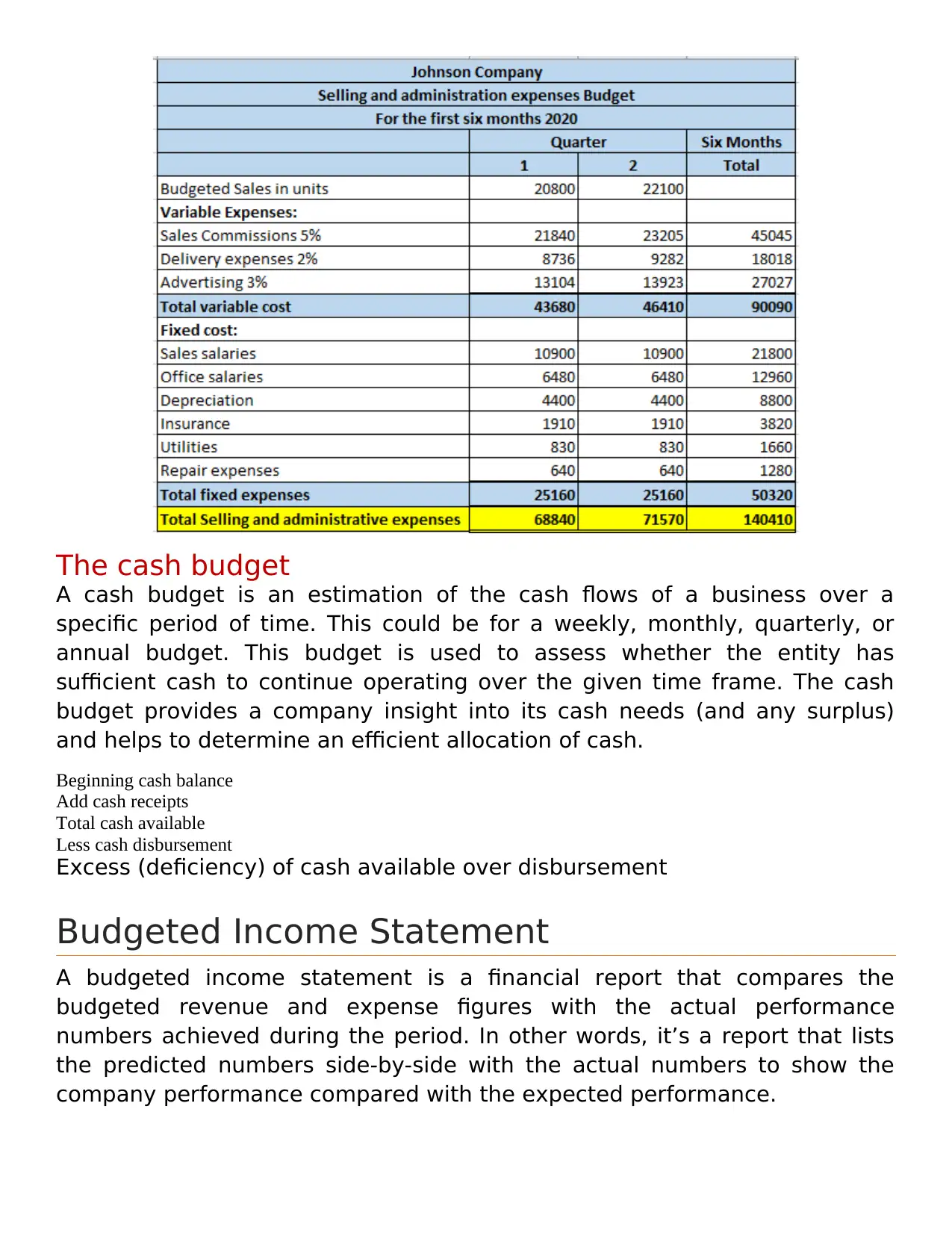

The selling and administrative expense budget

The selling and administrative expense budget lists the operating expenses

involved in selling the products and in managing the business. Just as in the

case of the factory overhead budget, this budget can be developed using

the cost-volume (flexible budget) formula in the form of y = a + bx.

appears in the budgeted balance sheet, which is then used to determine the

amount of cash needed to invest in assets.

The selling and administrative expense budget

The selling and administrative expense budget lists the operating expenses

involved in selling the products and in managing the business. Just as in the

case of the factory overhead budget, this budget can be developed using

the cost-volume (flexible budget) formula in the form of y = a + bx.

The cash budget

A cash budget is an estimation of the cash flows of a business over a

specific period of time. This could be for a weekly, monthly, quarterly, or

annual budget. This budget is used to assess whether the entity has

sufficient cash to continue operating over the given time frame. The cash

budget provides a company insight into its cash needs (and any surplus)

and helps to determine an efficient allocation of cash.

Beginning cash balance

Add cash receipts

Total cash available

Less cash disbursement

Excess (deficiency) of cash available over disbursement

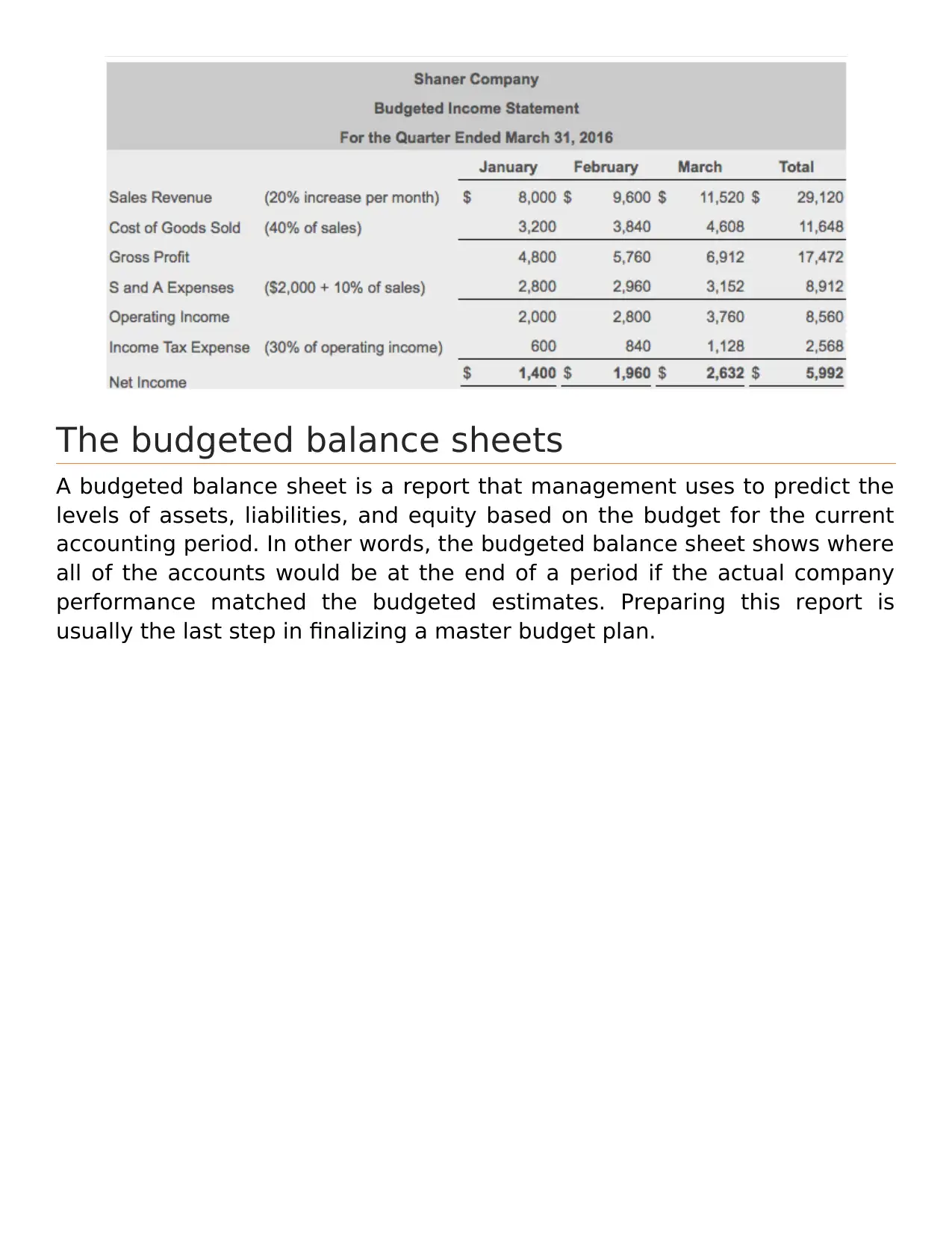

Budgeted Income Statement

A budgeted income statement is a financial report that compares the

budgeted revenue and expense figures with the actual performance

numbers achieved during the period. In other words, it’s a report that lists

the predicted numbers side-by-side with the actual numbers to show the

company performance compared with the expected performance.

A cash budget is an estimation of the cash flows of a business over a

specific period of time. This could be for a weekly, monthly, quarterly, or

annual budget. This budget is used to assess whether the entity has

sufficient cash to continue operating over the given time frame. The cash

budget provides a company insight into its cash needs (and any surplus)

and helps to determine an efficient allocation of cash.

Beginning cash balance

Add cash receipts

Total cash available

Less cash disbursement

Excess (deficiency) of cash available over disbursement

Budgeted Income Statement

A budgeted income statement is a financial report that compares the

budgeted revenue and expense figures with the actual performance

numbers achieved during the period. In other words, it’s a report that lists

the predicted numbers side-by-side with the actual numbers to show the

company performance compared with the expected performance.

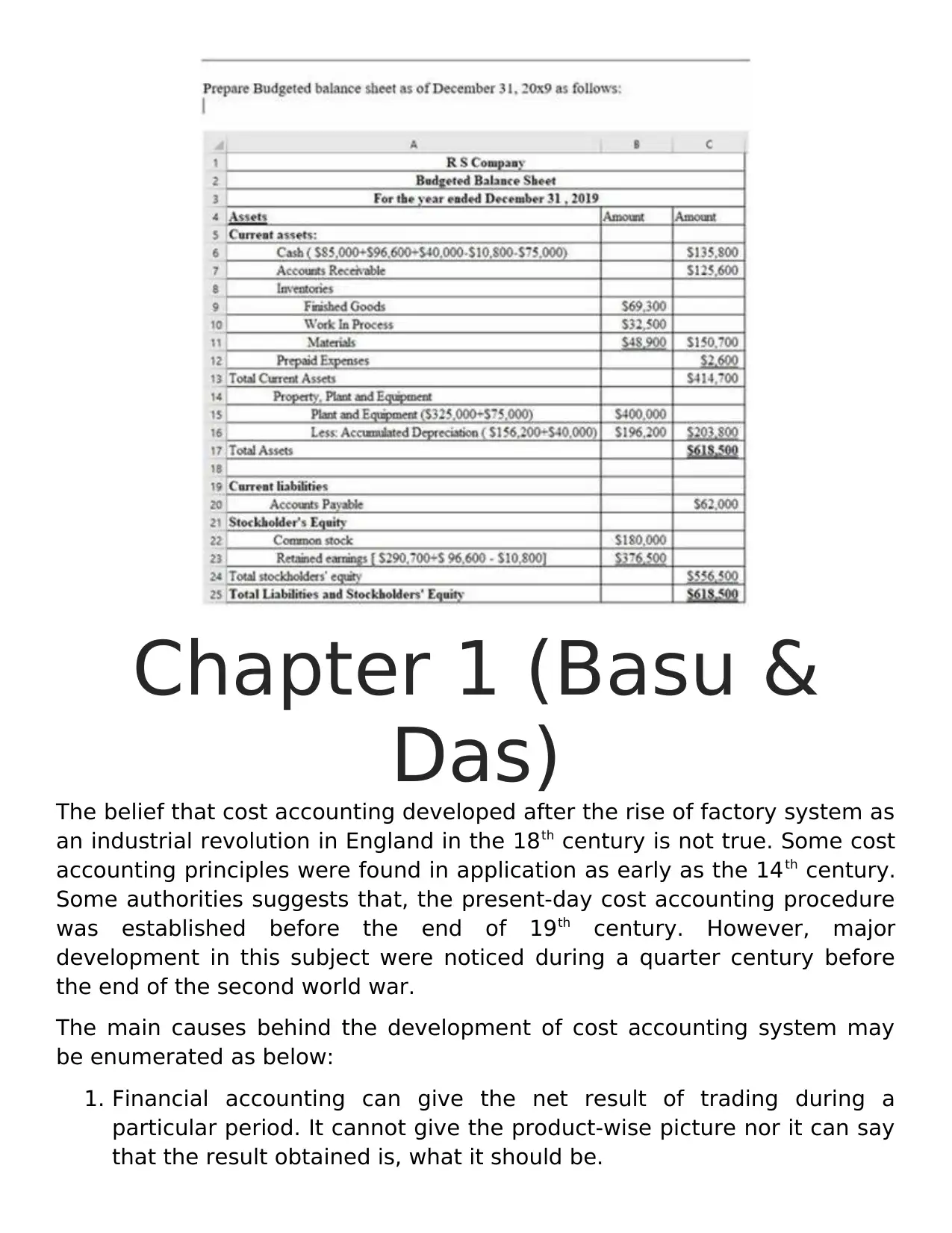

The budgeted balance sheets

A budgeted balance sheet is a report that management uses to predict the

levels of assets, liabilities, and equity based on the budget for the current

accounting period. In other words, the budgeted balance sheet shows where

all of the accounts would be at the end of a period if the actual company

performance matched the budgeted estimates. Preparing this report is

usually the last step in finalizing a master budget plan.

A budgeted balance sheet is a report that management uses to predict the

levels of assets, liabilities, and equity based on the budget for the current

accounting period. In other words, the budgeted balance sheet shows where

all of the accounts would be at the end of a period if the actual company

performance matched the budgeted estimates. Preparing this report is

usually the last step in finalizing a master budget plan.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Chapter 1 (Basu &

Das)

The belief that cost accounting developed after the rise of factory system as

an industrial revolution in England in the 18th century is not true. Some cost

accounting principles were found in application as early as the 14th century.

Some authorities suggests that, the present-day cost accounting procedure

was established before the end of 19th century. However, major

development in this subject were noticed during a quarter century before

the end of the second world war.

The main causes behind the development of cost accounting system may

be enumerated as below:

1. Financial accounting can give the net result of trading during a

particular period. It cannot give the product-wise picture nor it can say

that the result obtained is, what it should be.

Das)

The belief that cost accounting developed after the rise of factory system as

an industrial revolution in England in the 18th century is not true. Some cost

accounting principles were found in application as early as the 14th century.

Some authorities suggests that, the present-day cost accounting procedure

was established before the end of 19th century. However, major

development in this subject were noticed during a quarter century before

the end of the second world war.

The main causes behind the development of cost accounting system may

be enumerated as below:

1. Financial accounting can give the net result of trading during a