Taxation of Financial Institutions

VerifiedAdded on 2020/03/23

|13

|2520

|30

AI Summary

This taxation assignment delves into the application of tax laws on financial institutions. It presents a case study of Big Bank, where students must analyze its advertising expenses to determine the allowable input tax credit. Additionally, it requires calculating Angelo's taxable income and the net income of a partnership, demonstrating an understanding of individual and partnership tax computations.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1TAXATION LAW

Answer to question 1:

Answer to Question 1.1:

Issue:

The prevailing problem introduces that whether an individual incurring the cost on

moving the machine to the new site will be able to claim deductions specified under the

“section 8-1 of the ITAA 1997”.

Rule: The rules are section 8-1 of the ITAA The rules for this study is “British Insulated and Helsby Cables v Atherton (1926)”

Applications:

From the above-defined prevailing issue of cost incurred on the movement of the

machine to a new place a person will be disallowed from making allowable deductions in tax

return. One should note that “Section 8-1 of the ITAA 1997” accordingly specifies that a

person is disallowed from claiming expense that is not related in the production of assessable

income or business proceeds having private or domestic character (Kiprotich 2016). The

problem statement provides that the cost of moving the machine is capital outlay and such

expenses are disallowed from being considered as deductions.

An evidence of such cost is put forward under the “Taxation ruling of IT 2197”

where the cost of moving the machine is observed as capital expenditure and deductions for

income tax is disallowed for such outlay or expense (Chan 2013). The important case laws of

“British Insulated and Helsby Cables Ltd v. Atherton (1926)” expenditure taking place at

Answer to question 1:

Answer to Question 1.1:

Issue:

The prevailing problem introduces that whether an individual incurring the cost on

moving the machine to the new site will be able to claim deductions specified under the

“section 8-1 of the ITAA 1997”.

Rule: The rules are section 8-1 of the ITAA The rules for this study is “British Insulated and Helsby Cables v Atherton (1926)”

Applications:

From the above-defined prevailing issue of cost incurred on the movement of the

machine to a new place a person will be disallowed from making allowable deductions in tax

return. One should note that “Section 8-1 of the ITAA 1997” accordingly specifies that a

person is disallowed from claiming expense that is not related in the production of assessable

income or business proceeds having private or domestic character (Kiprotich 2016). The

problem statement provides that the cost of moving the machine is capital outlay and such

expenses are disallowed from being considered as deductions.

An evidence of such cost is put forward under the “Taxation ruling of IT 2197”

where the cost of moving the machine is observed as capital expenditure and deductions for

income tax is disallowed for such outlay or expense (Chan 2013). The important case laws of

“British Insulated and Helsby Cables Ltd v. Atherton (1926)” expenditure taking place at

2TAXATION LAW

the time of moving the depreciable asset is portrayed as unceasing benefit to the asset (Miller

and Oats 2016).

Conclusion:

The argument can be concluded that capital cost are disallowed from being considered

as deductible expense and cost of moving the machine to the new site is prevent from

allowable income tax deductions.

Answer to question 1.2:

Issue:

The problem that has been prevalent in this context is making of claim of admissible

income tax related deductions defined in context of “section 8-1 of the ITAA 1997” about

the revaluating of asset.

Rule:

The applicable rule in this context is the “Section 8-1 of the ITAA 1997”

Application:

The problem that has been stated in the context of the situation is the asset revaluation

and claiming the deductions that has been allowed in accordance with the “section 8-1 of the

ITAA 1997”. As evident the cost that is incurred by the individual taxpayer in order to

revalue the asset to the effect of insurance cover is primarily occurred from the execution of

trade activities. The cost of revaluation is solely incurred in the deriving the business revenue

and therefore such cost can be considered as allowable deductions for the reason that they are

not carrying the nature of domestic, private or capital under the purview of first limb (Preez

2016). It is assumed that cost of revaluing the asset to effect insurance cover is cyclical

business cost and such is incurred in generating the business revenue. Furthermore, an

the time of moving the depreciable asset is portrayed as unceasing benefit to the asset (Miller

and Oats 2016).

Conclusion:

The argument can be concluded that capital cost are disallowed from being considered

as deductible expense and cost of moving the machine to the new site is prevent from

allowable income tax deductions.

Answer to question 1.2:

Issue:

The problem that has been prevalent in this context is making of claim of admissible

income tax related deductions defined in context of “section 8-1 of the ITAA 1997” about

the revaluating of asset.

Rule:

The applicable rule in this context is the “Section 8-1 of the ITAA 1997”

Application:

The problem that has been stated in the context of the situation is the asset revaluation

and claiming the deductions that has been allowed in accordance with the “section 8-1 of the

ITAA 1997”. As evident the cost that is incurred by the individual taxpayer in order to

revalue the asset to the effect of insurance cover is primarily occurred from the execution of

trade activities. The cost of revaluation is solely incurred in the deriving the business revenue

and therefore such cost can be considered as allowable deductions for the reason that they are

not carrying the nature of domestic, private or capital under the purview of first limb (Preez

2016). It is assumed that cost of revaluing the asset to effect insurance cover is cyclical

business cost and such is incurred in generating the business revenue. Furthermore, an

3TAXATION LAW

assertion can be bought forward that the cost incurred possess significant association with the

taxpayers business functions and does not constitute capital or private expense.

Conclusion:

Arguably, the cost of revaluing asset in order to effect insurance cover is a recurring

business cost. Therefore, such cost forms the part of the income tax deductions.

Answer to question 1.3:

The prevailing circumstances is associated with determining the deductibility of the

legal cost a person incurs for opposing the petition of winding up.

Rule: The applicable rule in this context is the “Section 8-1 of the ITAA 1997” The applicable case laws legislation in this issue is the “Sun Newspapers Ltd v F C of

T (1938)”

Applications:

The above stated problems statement is concerned with the deductibility of the legal

cost that a person incurs for opposing the winding up petition. In order to obtain an income

tax deductions for legal expenses or outgoings, in important considerations is to paid in

understanding the nature of such cost under “Section 8-1 of the ITAA 1997” (Atkinson and

Stiglitz 2016). The character or the feature of the legal expense carries a benefit that is sought

by the taxpayers for the expenses incurred. An important consideration of the “Section 8-1 of

the ITAA 1997” is that when individual taxpayers in the process of gaining or deriving

business revenue occur a legal expenditure then such legal expense is regarded as admissible

income tax deductible expense.

assertion can be bought forward that the cost incurred possess significant association with the

taxpayers business functions and does not constitute capital or private expense.

Conclusion:

Arguably, the cost of revaluing asset in order to effect insurance cover is a recurring

business cost. Therefore, such cost forms the part of the income tax deductions.

Answer to question 1.3:

The prevailing circumstances is associated with determining the deductibility of the

legal cost a person incurs for opposing the petition of winding up.

Rule: The applicable rule in this context is the “Section 8-1 of the ITAA 1997” The applicable case laws legislation in this issue is the “Sun Newspapers Ltd v F C of

T (1938)”

Applications:

The above stated problems statement is concerned with the deductibility of the legal

cost that a person incurs for opposing the winding up petition. In order to obtain an income

tax deductions for legal expenses or outgoings, in important considerations is to paid in

understanding the nature of such cost under “Section 8-1 of the ITAA 1997” (Atkinson and

Stiglitz 2016). The character or the feature of the legal expense carries a benefit that is sought

by the taxpayers for the expenses incurred. An important consideration of the “Section 8-1 of

the ITAA 1997” is that when individual taxpayers in the process of gaining or deriving

business revenue occur a legal expenditure then such legal expense is regarded as admissible

income tax deductible expense.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4TAXATION LAW

Reciting the situation “Sun Newspapers Ltd v F C of T (1938)” when a legal

expense is primarily dedicated for deriving the operational trade functions then such expense

are considered for income tax purpose (Shome 2015). Whereas, when the expense are

structural in nature then such legal expense are disallowed from being considered as

admissible income tax deductions. The legal expense of opposing the petition of winding up

represents structural business cost rather than an operative cost therefore, such expense are

disallowed from allowable deductions.

Conclusion:

The above stated explanation provides conclusive evidence that the legal expenditure

are incurred are structural business cost rather a operative business cost. In compliance with

“Section 8-1 of the ITAA 1997”, these expenses are disallowed from being considered as

deductible expense.

Answer to question 1.4:

Issue:

The prevalent issue is focussed on determining the deductibility of the legal expense

incurred by an individual taxpayer in discharge of the business functions for taking the

service of the solicitor.

Rule: The applicable rule in this problem statement is the “Section 8-1 of the ITAA 1997” The appropriate case laws that is applicable here is “Herald and Weekly Times v.

F.C. of T (1932)”

Reciting the situation “Sun Newspapers Ltd v F C of T (1938)” when a legal

expense is primarily dedicated for deriving the operational trade functions then such expense

are considered for income tax purpose (Shome 2015). Whereas, when the expense are

structural in nature then such legal expense are disallowed from being considered as

admissible income tax deductions. The legal expense of opposing the petition of winding up

represents structural business cost rather than an operative cost therefore, such expense are

disallowed from allowable deductions.

Conclusion:

The above stated explanation provides conclusive evidence that the legal expenditure

are incurred are structural business cost rather a operative business cost. In compliance with

“Section 8-1 of the ITAA 1997”, these expenses are disallowed from being considered as

deductible expense.

Answer to question 1.4:

Issue:

The prevalent issue is focussed on determining the deductibility of the legal expense

incurred by an individual taxpayer in discharge of the business functions for taking the

service of the solicitor.

Rule: The applicable rule in this problem statement is the “Section 8-1 of the ITAA 1997” The appropriate case laws that is applicable here is “Herald and Weekly Times v.

F.C. of T (1932)”

5TAXATION LAW

Applications:

Denoting the prevalent of determining the deductibility of legal expense that is

incurred by the taxpayer for discharge of varied business functions with the help of solicitor

should be considered as admissible income tax deductible expense (Lang 2014). A significant

considerations of “Section 8-1 of the ITAA 1997” is that legal expense incurred by the

taxpayers carrying the nature of the operative business functions are regarded for income tax

deductions except for capital, domestic or private expense (Kaldor 2014). Referring the

instance of “Herald & Weekly Times v F C of T (1932)” expenses incurred in the discharge

of regular business functions are treated for deductions since they form the part of the

revenue deriving actions. Moreover, if the legal expense has more than outlying connection

with the business actions then such expense qualifies for income tax deductions (Bankman et

al. 2017). As noted in the prevailing case that legal expense was incurred for taking the

service of solicitor in order to discharge numerous business functions and those functions

formed the operative part of the business. Therefore, the taxpayer in this scenario can claim

for income tax allowable deductions.

Conclusion:

Under the reference of “Section 8-1 of the ITAA 1997” legal expense that originated

in the present scenario formed the part of the business functions and the taxpayer for such

expense can claim an allowable income tax deduction.

Answer to question 2:

Issue:

The following case study of Big Bank Ltd deals with the determination of the input

tax credit that can be claimed by the company for the financial supplies made by them under

the purview of the “GST Act 1999”.

Applications:

Denoting the prevalent of determining the deductibility of legal expense that is

incurred by the taxpayer for discharge of varied business functions with the help of solicitor

should be considered as admissible income tax deductible expense (Lang 2014). A significant

considerations of “Section 8-1 of the ITAA 1997” is that legal expense incurred by the

taxpayers carrying the nature of the operative business functions are regarded for income tax

deductions except for capital, domestic or private expense (Kaldor 2014). Referring the

instance of “Herald & Weekly Times v F C of T (1932)” expenses incurred in the discharge

of regular business functions are treated for deductions since they form the part of the

revenue deriving actions. Moreover, if the legal expense has more than outlying connection

with the business actions then such expense qualifies for income tax deductions (Bankman et

al. 2017). As noted in the prevailing case that legal expense was incurred for taking the

service of solicitor in order to discharge numerous business functions and those functions

formed the operative part of the business. Therefore, the taxpayer in this scenario can claim

for income tax allowable deductions.

Conclusion:

Under the reference of “Section 8-1 of the ITAA 1997” legal expense that originated

in the present scenario formed the part of the business functions and the taxpayer for such

expense can claim an allowable income tax deduction.

Answer to question 2:

Issue:

The following case study of Big Bank Ltd deals with the determination of the input

tax credit that can be claimed by the company for the financial supplies made by them under

the purview of the “GST Act 1999”.

6TAXATION LAW

Rule:

I. The applicable rule in this present context is the “GST Act 1999”

II. Another applicable rulings that is has been concerned is the “Goods and Service

Taxation Ruling of GSTR 2006/3”

III. The appropriate case laws legislation is the “Ronpibon Tin NL v FC of T”

Applications:

The problem statement brings forward the scenario of Big Bank Ltd providing

financial supplies to its customers and the advertisement expenditure incurred by the

company. The bank provided service in more than 50 branches across the state of Australia

and had large number of customers to access the service of the home content and insurance

products. Apart from this, Big Bank also provided the services of loans and deposits to its

customers. As evident from the “Taxation ruling of GSTR 2006/3” it provides process of

computing and determining the amount of input tax credit that can be availed by the

commercial entities making financial supplies (Schmalbeck, Zelenak and Lawsky 2015). An

important considerations has been laid down under the second chapter of the “GST Act

1999” that effectively puts forward that an commercial entities making financial supplies

would be entitled for claiming input tax credit concerning the expenditure occurred by the

business in their ordinary course.

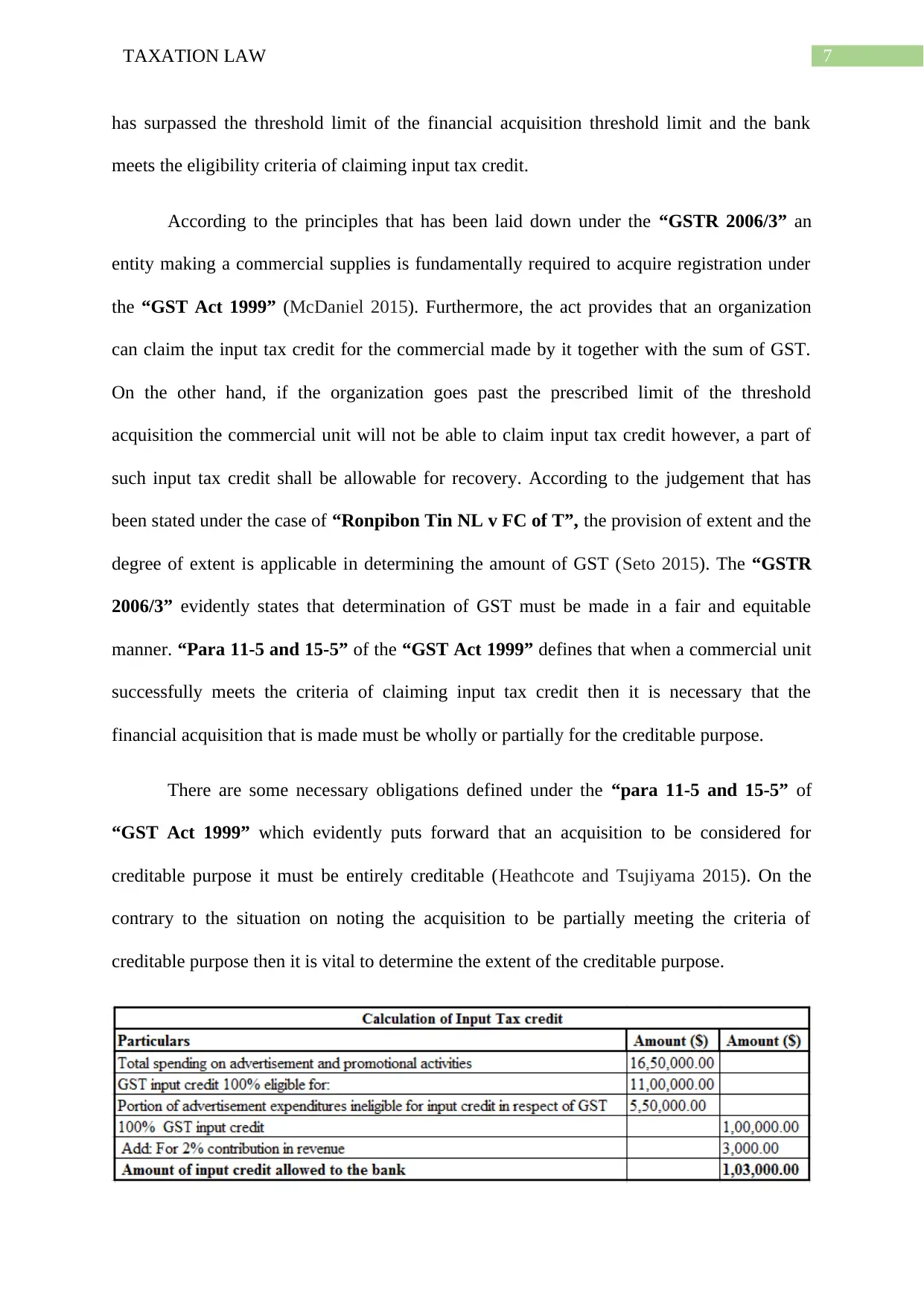

More significantly, to claim an input tax credit an organization must be the price of

the financial supplies must include the amount of the GST (Beard and Lucas 2017). The

“taxation ruling of GSTR 2006/3” is generally applicable to the commercial entities making

financial supplies that goes past the financial acquisition threshold limit. The prevalent study

of Big Bank has evidently puts forward that the bank has made the spending on

advertisement that was inclusive of the sum of GST (Scholes 2015). The applicable rulings in

the case study of Big Bank that can be applied is the GSTR of 2006/3. Arguably, Big Bank

Rule:

I. The applicable rule in this present context is the “GST Act 1999”

II. Another applicable rulings that is has been concerned is the “Goods and Service

Taxation Ruling of GSTR 2006/3”

III. The appropriate case laws legislation is the “Ronpibon Tin NL v FC of T”

Applications:

The problem statement brings forward the scenario of Big Bank Ltd providing

financial supplies to its customers and the advertisement expenditure incurred by the

company. The bank provided service in more than 50 branches across the state of Australia

and had large number of customers to access the service of the home content and insurance

products. Apart from this, Big Bank also provided the services of loans and deposits to its

customers. As evident from the “Taxation ruling of GSTR 2006/3” it provides process of

computing and determining the amount of input tax credit that can be availed by the

commercial entities making financial supplies (Schmalbeck, Zelenak and Lawsky 2015). An

important considerations has been laid down under the second chapter of the “GST Act

1999” that effectively puts forward that an commercial entities making financial supplies

would be entitled for claiming input tax credit concerning the expenditure occurred by the

business in their ordinary course.

More significantly, to claim an input tax credit an organization must be the price of

the financial supplies must include the amount of the GST (Beard and Lucas 2017). The

“taxation ruling of GSTR 2006/3” is generally applicable to the commercial entities making

financial supplies that goes past the financial acquisition threshold limit. The prevalent study

of Big Bank has evidently puts forward that the bank has made the spending on

advertisement that was inclusive of the sum of GST (Scholes 2015). The applicable rulings in

the case study of Big Bank that can be applied is the GSTR of 2006/3. Arguably, Big Bank

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

has surpassed the threshold limit of the financial acquisition threshold limit and the bank

meets the eligibility criteria of claiming input tax credit.

According to the principles that has been laid down under the “GSTR 2006/3” an

entity making a commercial supplies is fundamentally required to acquire registration under

the “GST Act 1999” (McDaniel 2015). Furthermore, the act provides that an organization

can claim the input tax credit for the commercial made by it together with the sum of GST.

On the other hand, if the organization goes past the prescribed limit of the threshold

acquisition the commercial unit will not be able to claim input tax credit however, a part of

such input tax credit shall be allowable for recovery. According to the judgement that has

been stated under the case of “Ronpibon Tin NL v FC of T”, the provision of extent and the

degree of extent is applicable in determining the amount of GST (Seto 2015). The “GSTR

2006/3” evidently states that determination of GST must be made in a fair and equitable

manner. “Para 11-5 and 15-5” of the “GST Act 1999” defines that when a commercial unit

successfully meets the criteria of claiming input tax credit then it is necessary that the

financial acquisition that is made must be wholly or partially for the creditable purpose.

There are some necessary obligations defined under the “para 11-5 and 15-5” of

“GST Act 1999” which evidently puts forward that an acquisition to be considered for

creditable purpose it must be entirely creditable (Heathcote and Tsujiyama 2015). On the

contrary to the situation on noting the acquisition to be partially meeting the criteria of

creditable purpose then it is vital to determine the extent of the creditable purpose.

has surpassed the threshold limit of the financial acquisition threshold limit and the bank

meets the eligibility criteria of claiming input tax credit.

According to the principles that has been laid down under the “GSTR 2006/3” an

entity making a commercial supplies is fundamentally required to acquire registration under

the “GST Act 1999” (McDaniel 2015). Furthermore, the act provides that an organization

can claim the input tax credit for the commercial made by it together with the sum of GST.

On the other hand, if the organization goes past the prescribed limit of the threshold

acquisition the commercial unit will not be able to claim input tax credit however, a part of

such input tax credit shall be allowable for recovery. According to the judgement that has

been stated under the case of “Ronpibon Tin NL v FC of T”, the provision of extent and the

degree of extent is applicable in determining the amount of GST (Seto 2015). The “GSTR

2006/3” evidently states that determination of GST must be made in a fair and equitable

manner. “Para 11-5 and 15-5” of the “GST Act 1999” defines that when a commercial unit

successfully meets the criteria of claiming input tax credit then it is necessary that the

financial acquisition that is made must be wholly or partially for the creditable purpose.

There are some necessary obligations defined under the “para 11-5 and 15-5” of

“GST Act 1999” which evidently puts forward that an acquisition to be considered for

creditable purpose it must be entirely creditable (Heathcote and Tsujiyama 2015). On the

contrary to the situation on noting the acquisition to be partially meeting the criteria of

creditable purpose then it is vital to determine the extent of the creditable purpose.

8TAXATION LAW

From the applicable rulings of GSTR 2006/3, important explanations has been

provided in section 11-5 and 15-10 that is concerned with the issue of creditable acquisition.

An individual firm can make claim of the input tax credit if the monetary supplies is

including the amount of the GST (Snape and De Souza 2016). In context of the present

scenario of Big Bank, the commercial supplies of financial nature made by the bank has an

association with creditable supplies. From the given case study of Big Bank it has been

observed that it has already crossed the threshold limit that was stated in GSTR 2006/3 for

the financial acquisition so, it can claim partly for input tax credit supplies that it has made.

Conclusion:

The explanation to the case study is providing a conclusive evidence that it can claim

the input tax credit that Big Bank has incurred for its advertisement expense under the

framework of GSTR 2006/3.

Answer to question 3:

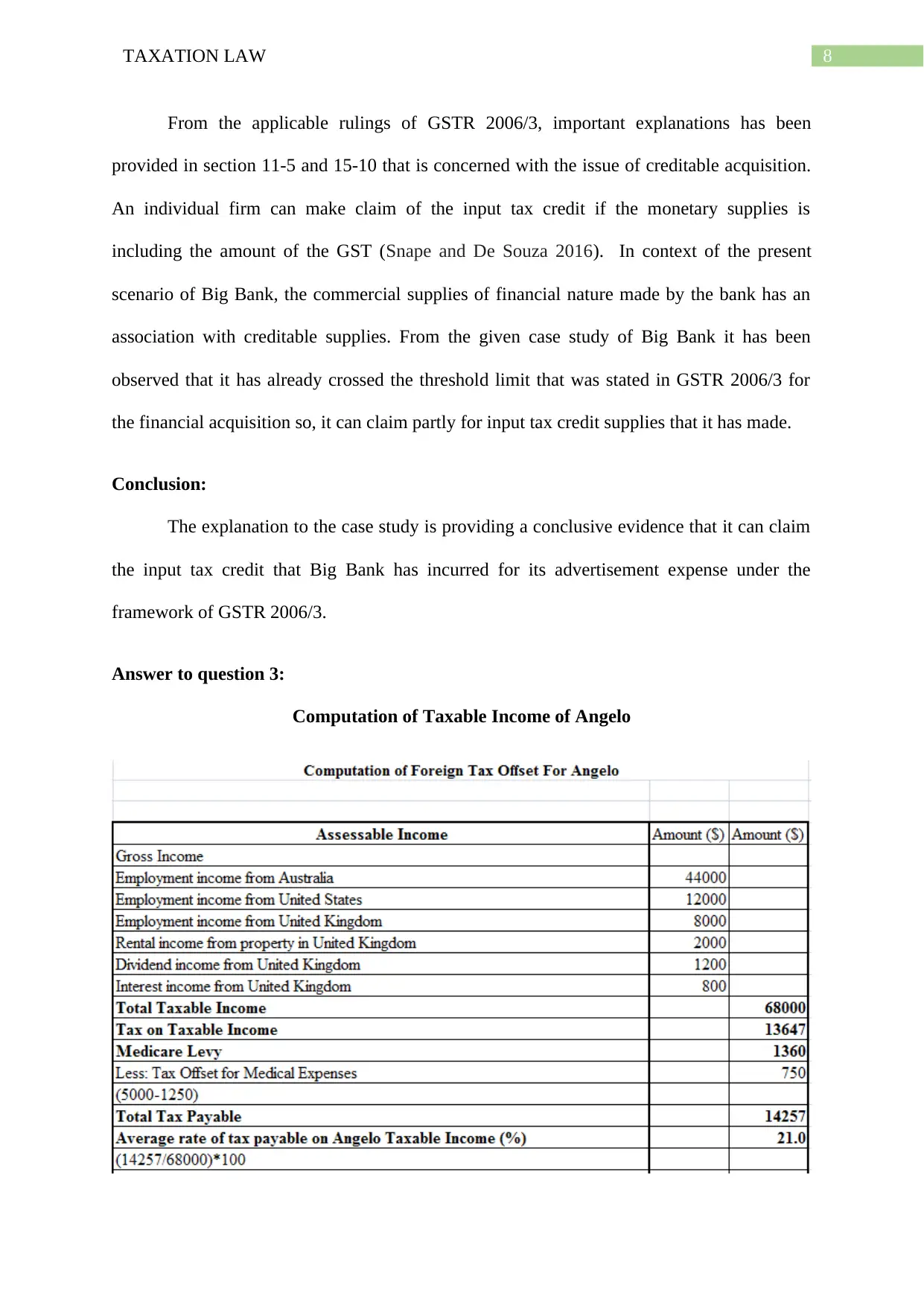

Computation of Taxable Income of Angelo

From the applicable rulings of GSTR 2006/3, important explanations has been

provided in section 11-5 and 15-10 that is concerned with the issue of creditable acquisition.

An individual firm can make claim of the input tax credit if the monetary supplies is

including the amount of the GST (Snape and De Souza 2016). In context of the present

scenario of Big Bank, the commercial supplies of financial nature made by the bank has an

association with creditable supplies. From the given case study of Big Bank it has been

observed that it has already crossed the threshold limit that was stated in GSTR 2006/3 for

the financial acquisition so, it can claim partly for input tax credit supplies that it has made.

Conclusion:

The explanation to the case study is providing a conclusive evidence that it can claim

the input tax credit that Big Bank has incurred for its advertisement expense under the

framework of GSTR 2006/3.

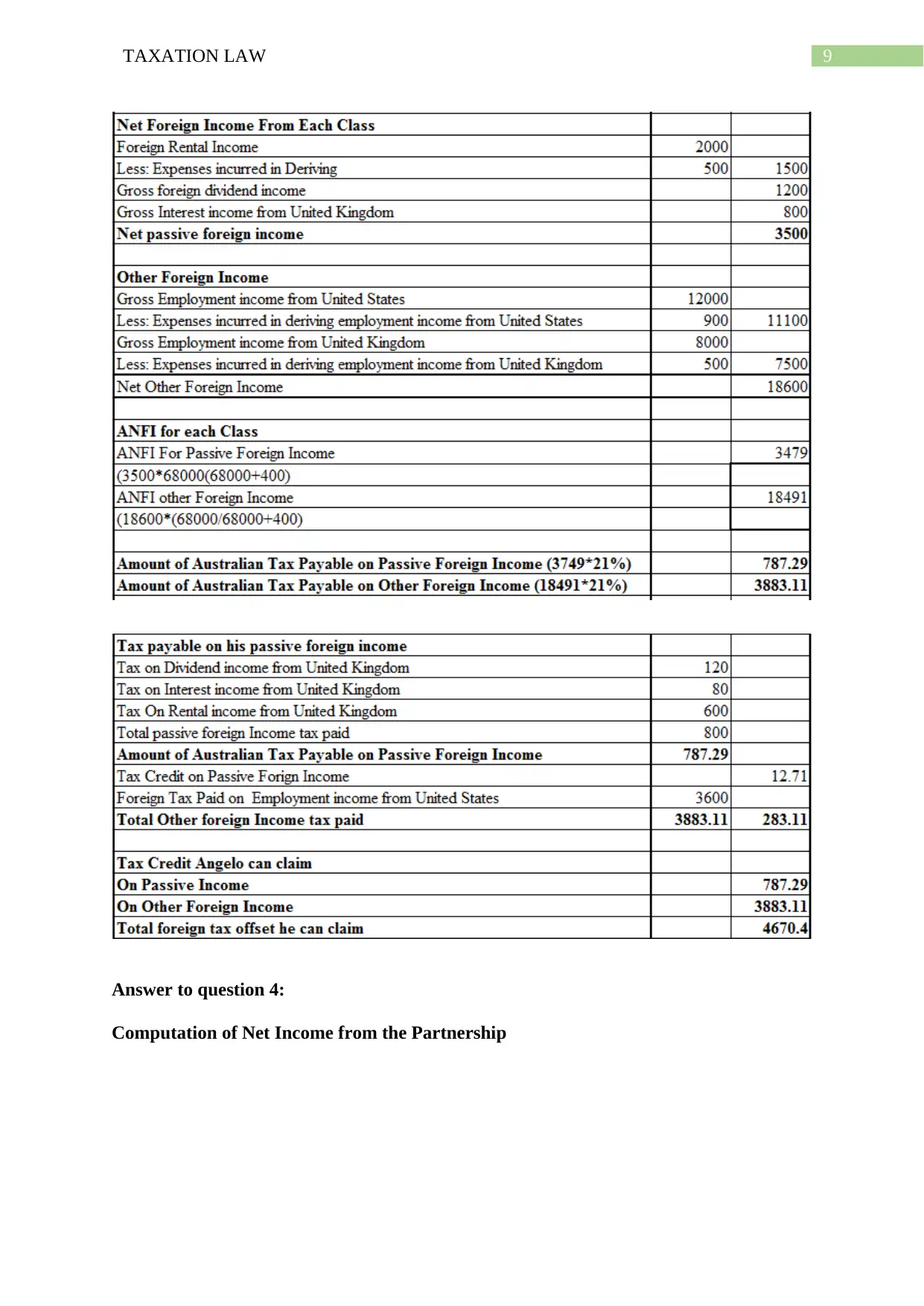

Answer to question 3:

Computation of Taxable Income of Angelo

9TAXATION LAW

Answer to question 4:

Computation of Net Income from the Partnership

Answer to question 4:

Computation of Net Income from the Partnership

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10TAXATION LAW

11TAXATION LAW

Reference List:

Atkinson, A.B. and Stiglitz, J.E., 2016. The design of tax structure: direct versus indirect

taxation. Journal of public Economics, 6(1-2), pp.55-75.

Bankman, J., Shaviro, D.N., Stark, K.J. and Kleinbard, E.D., 2017. Federal Income Taxation.

Wolters Kluwer Law & Business.

Beard, R. and Lucas, G.S., 2017. Federal Income Taxation. Mercer L. Rev., 68, pp.1041-

1161.

Chan, L.K., 2013. AAT.: Principles of Taxation. Paper 5. Pearson Education Asia Limited.

Du Preez, H., 2016. A construction of the fundamental principles of taxation (Doctoral

dissertation, University of Pretoria).

Heathcote, J. and Tsujiyama, H., 2015. Optimal income taxation: Mirrlees meets Ramsey.

Kaldor, N., 2014. Expenditure tax. Routledge.

Kiprotich, B.A., 2016. Principles of Taxation. governance.

Lang, M., 2014. Introduction to the law of double taxation conventions. Linde Verlag GmbH.

McDaniel, P.R., 2017. FEDERAL INCOME TAXATION. Foundation Press.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Schmalbeck, R., Zelenak, L. and Lawsky, S.B., 2015. Federal Income Taxation. Wolters

Kluwer Law & Business.

Scholes, M.S., 2015. Taxes and business strategy. Prentice Hall.

Seto, T., 2015. Federal Income Taxation: Cases, Problems, and Materials. West Academic

Publishing.

Reference List:

Atkinson, A.B. and Stiglitz, J.E., 2016. The design of tax structure: direct versus indirect

taxation. Journal of public Economics, 6(1-2), pp.55-75.

Bankman, J., Shaviro, D.N., Stark, K.J. and Kleinbard, E.D., 2017. Federal Income Taxation.

Wolters Kluwer Law & Business.

Beard, R. and Lucas, G.S., 2017. Federal Income Taxation. Mercer L. Rev., 68, pp.1041-

1161.

Chan, L.K., 2013. AAT.: Principles of Taxation. Paper 5. Pearson Education Asia Limited.

Du Preez, H., 2016. A construction of the fundamental principles of taxation (Doctoral

dissertation, University of Pretoria).

Heathcote, J. and Tsujiyama, H., 2015. Optimal income taxation: Mirrlees meets Ramsey.

Kaldor, N., 2014. Expenditure tax. Routledge.

Kiprotich, B.A., 2016. Principles of Taxation. governance.

Lang, M., 2014. Introduction to the law of double taxation conventions. Linde Verlag GmbH.

McDaniel, P.R., 2017. FEDERAL INCOME TAXATION. Foundation Press.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Schmalbeck, R., Zelenak, L. and Lawsky, S.B., 2015. Federal Income Taxation. Wolters

Kluwer Law & Business.

Scholes, M.S., 2015. Taxes and business strategy. Prentice Hall.

Seto, T., 2015. Federal Income Taxation: Cases, Problems, and Materials. West Academic

Publishing.

12TAXATION LAW

Shome, P. ed., 2015. Tax policy handbook. International Monetary Fund.

Snape, J. and De Souza, J., 2016. Environmental taxation law: policy, contexts and practice.

Routledge.

Shome, P. ed., 2015. Tax policy handbook. International Monetary Fund.

Snape, J. and De Souza, J., 2016. Environmental taxation law: policy, contexts and practice.

Routledge.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.