Brexit and the Battle for Control of Euro Clearing: Legal Analysis

VerifiedAdded on 2020/06/04

|48

|12632

|358

Thesis and Dissertation

AI Summary

This dissertation delves into the intricate relationship between Brexit and the Euro clearing system, offering a comprehensive legal and tactical analysis of the competing regulatory powers wielded by the UK and the EU concerning central counterparties. The study begins with an introduction to the background of Brexit and its potential economic impacts, particularly within the financial sector, followed by a review of relevant literature examining the workings of clearing houses, the reasons behind Brexit, and its effects on the Euro clearing landscape. The research employs a detailed methodology, outlining the research philosophy, approach, design, and data collection methods used to gather and analyze information. Data findings and analysis explore the dominant position of London in the Euro clearing market, the consequences of Brexit on this position, and the impact of Brexit on legislation and regulatory requirements. The analysis interprets these findings, addressing issues such as the legal and tactical challenges of relocation proposals, the impact of Brexit on financial uncertainties, and the Eurosystem oversight policy framework. The dissertation concludes with recommendations for navigating the complexities of Euro clearing post-Brexit, considering the legal and regulatory dynamics between the UK and the EU.

Dissertation

(Brexit and the battle for control of euro clearing - a

legal and tactical analysis of the competing

regulatory powers of the UK and EU concerning

central counterparties)

(Brexit and the battle for control of euro clearing - a

legal and tactical analysis of the competing

regulatory powers of the UK and EU concerning

central counterparties)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

CHAPTER – 1 INTRODUCTION..................................................................................................1

1.1 Background of the study........................................................................................................1

1.2 Problem statement..................................................................................................................4

1.3 Research aims and objectives................................................................................................4

1.4 Potential contribution.............................................................................................................4

1.5 Disposition.............................................................................................................................5

CHAPTER -2 LITERATURE REVIEW.........................................................................................6

2.0 Introduction............................................................................................................................6

2.1 Understanding the working of clearing houses......................................................................6

2.2 Reasons of Brexit and its impact over legal & political uncertainties...................................8

2.3 Impact of Brexit on Euro Clearing system.............................................................................9

2.4 Legal & tactical evaluation of UK and EU’s regulatory authorities’ power concerned to

central counterparties.................................................................................................................11

CHAPTER – 3 RESEARCH METHODOLOGY.........................................................................15

3.0 Introduction..........................................................................................................................15

3.1 Research philosophy............................................................................................................15

3.2 Research approach...............................................................................................................16

3.3 Research design....................................................................................................................16

3.4 Research type.......................................................................................................................17

3.5 Data collection.....................................................................................................................18

3.6 Data analysis........................................................................................................................18

CHAPTER – 1 INTRODUCTION..................................................................................................1

1.1 Background of the study........................................................................................................1

1.2 Problem statement..................................................................................................................4

1.3 Research aims and objectives................................................................................................4

1.4 Potential contribution.............................................................................................................4

1.5 Disposition.............................................................................................................................5

CHAPTER -2 LITERATURE REVIEW.........................................................................................6

2.0 Introduction............................................................................................................................6

2.1 Understanding the working of clearing houses......................................................................6

2.2 Reasons of Brexit and its impact over legal & political uncertainties...................................8

2.3 Impact of Brexit on Euro Clearing system.............................................................................9

2.4 Legal & tactical evaluation of UK and EU’s regulatory authorities’ power concerned to

central counterparties.................................................................................................................11

CHAPTER – 3 RESEARCH METHODOLOGY.........................................................................15

3.0 Introduction..........................................................................................................................15

3.1 Research philosophy............................................................................................................15

3.2 Research approach...............................................................................................................16

3.3 Research design....................................................................................................................16

3.4 Research type.......................................................................................................................17

3.5 Data collection.....................................................................................................................18

3.6 Data analysis........................................................................................................................18

3.7 Reliability & validity...........................................................................................................19

3.8 Ethical implications..............................................................................................................19

3.9 Limitation & strategy followed to overcome obstacles.......................................................19

CHAPTER – 4 DATA FINDINGS AND ANALYSIS.................................................................21

4.0 Introduction..........................................................................................................................21

4.1 Data findings and presentation.............................................................................................21

Dominant position of London in the Euro clearing market.......................................................21

Brexit consequences on the dominant position of LCH and its trade volume...........................25

Impact of brexit over the legislation & regulatory requirement on London based clearing

houses.........................................................................................................................................25

4.2 Analysis and interpretation..................................................................................................26

Dominant position of London....................................................................................................26

Legal & tactical issues in relocation proposal...........................................................................27

Impact of brexit over uncertainties in the financial sector.........................................................28

Eurosystem oversight policy framework...................................................................................28

Critical reflection.......................................................................................................................29

CHAPTER -5 CONCLUSION & RECOMMENDATIONS........................................................31

Conclusion.................................................................................................................................31

Recommendations......................................................................................................................32

REFERENCES..............................................................................................................................35

3.8 Ethical implications..............................................................................................................19

3.9 Limitation & strategy followed to overcome obstacles.......................................................19

CHAPTER – 4 DATA FINDINGS AND ANALYSIS.................................................................21

4.0 Introduction..........................................................................................................................21

4.1 Data findings and presentation.............................................................................................21

Dominant position of London in the Euro clearing market.......................................................21

Brexit consequences on the dominant position of LCH and its trade volume...........................25

Impact of brexit over the legislation & regulatory requirement on London based clearing

houses.........................................................................................................................................25

4.2 Analysis and interpretation..................................................................................................26

Dominant position of London....................................................................................................26

Legal & tactical issues in relocation proposal...........................................................................27

Impact of brexit over uncertainties in the financial sector.........................................................28

Eurosystem oversight policy framework...................................................................................28

Critical reflection.......................................................................................................................29

CHAPTER -5 CONCLUSION & RECOMMENDATIONS........................................................31

Conclusion.................................................................................................................................31

Recommendations......................................................................................................................32

REFERENCES..............................................................................................................................35

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CHAPTER – 1 INTRODUCTION

Research title: Brexit and the battle for control of Euro clearing: a legal & tactical

analysis of the competing regulatory powers of UK & EU with respect to central counterparties

1.1 Background of the study

Britain exit from European Union (Brexit) took place on 23rd June 2016 after 43 years of

their joint membership. The leave decision won by having majority of 51.9% votes, whilst 48.1%

people voted in favour of remaining the part of EU. England voted for the refendum by 53.4%,

Wales by 52.5%, whilst in Scotland & Northern Ireland, 62% and 55.8% people supported

remain decisions1. The debate mostly revolves around free movement of goods across EU

nations without any custom tariffs and economic benefits of EU membership. Before refendum,

Cameron, George Osborne and other senior authorities have predicted that if UK voted to leave

Union than it will lead to sudden economic crisis. Evidencing it, on the day after the brexit, the

value of pound slumped down by 15% and 10% against dollar and euro2.

However, critics argued that predictions are wrong because UK economy is expecting a

growth of 1.8% in 2016 and Germany alone has been expected to grow @ 1.9% among all

leading G7 countries3. ONS (Office of National Statistics) reported that undoubtedly, the growth

of the country has been slowed still, the economy is expanding4.

Clearing houses offer various services covers risk mitigation, capital efficiency, price

transparency, delivery facilitation and operational efficiencies for various liquid derivatives i.e.

1 'Brexit: All You Need To Know About The UK Leaving The EU - BBC News'. 2017.

Available through: <http://www.bbc.com/news/uk-politics-32810887> [Accessed on 11

August 2017].

2 Ibid

3 Ibid

4 What Is London’S Euro Clearing Market And Why Is Brussels Worried?'. 2017.

Available through: <https://webcache.googleusercontent.com/search?

q=cache:oWsR_mL3RCQJ:https://www.ft.com/content/18dcf566-5025-11e7-bfb8-

997009366969%3Fmhq5j%3De4+&cd=1&hl=en&ct=clnk&gl=in> [Accessed on 11

August 2017].

1

Research title: Brexit and the battle for control of Euro clearing: a legal & tactical

analysis of the competing regulatory powers of UK & EU with respect to central counterparties

1.1 Background of the study

Britain exit from European Union (Brexit) took place on 23rd June 2016 after 43 years of

their joint membership. The leave decision won by having majority of 51.9% votes, whilst 48.1%

people voted in favour of remaining the part of EU. England voted for the refendum by 53.4%,

Wales by 52.5%, whilst in Scotland & Northern Ireland, 62% and 55.8% people supported

remain decisions1. The debate mostly revolves around free movement of goods across EU

nations without any custom tariffs and economic benefits of EU membership. Before refendum,

Cameron, George Osborne and other senior authorities have predicted that if UK voted to leave

Union than it will lead to sudden economic crisis. Evidencing it, on the day after the brexit, the

value of pound slumped down by 15% and 10% against dollar and euro2.

However, critics argued that predictions are wrong because UK economy is expecting a

growth of 1.8% in 2016 and Germany alone has been expected to grow @ 1.9% among all

leading G7 countries3. ONS (Office of National Statistics) reported that undoubtedly, the growth

of the country has been slowed still, the economy is expanding4.

Clearing houses offer various services covers risk mitigation, capital efficiency, price

transparency, delivery facilitation and operational efficiencies for various liquid derivatives i.e.

1 'Brexit: All You Need To Know About The UK Leaving The EU - BBC News'. 2017.

Available through: <http://www.bbc.com/news/uk-politics-32810887> [Accessed on 11

August 2017].

2 Ibid

3 Ibid

4 What Is London’S Euro Clearing Market And Why Is Brussels Worried?'. 2017.

Available through: <https://webcache.googleusercontent.com/search?

q=cache:oWsR_mL3RCQJ:https://www.ft.com/content/18dcf566-5025-11e7-bfb8-

997009366969%3Fmhq5j%3De4+&cd=1&hl=en&ct=clnk&gl=in> [Accessed on 11

August 2017].

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

bond, equity, interest rate and others. Clearing houses maintains high level of market integrity by

playing an intermediary role between buyer and sellers5. They discount various instrument in

return for certain margin and becomes the central counterparty for clearing and settling trades.

Thus, by this way, they plays a substantial role in maintaining financial stability. Henderson

defined derivatives as a financial product or instrument which value depends upon underlying

assets i.e. currency, security or commodity. It includes future, options and others. Central bank is

the leading authority that owes accountability to maintain financial stability through control over

money supply. The authority designs laws and economic rules and regulation for efficient

financial regulative framework6.

In London, Financial services and business volume goes beyond $900bn a day and the

most important thing is that it centered on Euro-dominated contracts of derivatives by LSE’s

(London Stock Exchange) Clearing Houses (LCH). Brussel’s proposal stated that in order to

maintain economic stability, EU regulatory authority must be given power to look overseas

clearing houses which can threaten systematic risk on financial stability in Europe. After the

economic crisis in 2008, clearing becomes a key pillar for boosting stability in the global

financial market. There are number of clearing houses i.e. LCH, Dutsche Borse’s Eurex who

plays an intermediary role between sellers and buyers of the financial instruments as they

exchange cheques, bills and other instrument for certain margin. They are also accountable for

looking the future exchanges for the trading account settlement.

The city stands in the dominant position for the clearing of derivative instruments

denominated in euro even though UK never intended to join eurozone. After the Brexit, the key

issue is that how UK located clearing houses will be regulated and policed because current rules

of EU will be no longer required to be follow7. However, its failure may bring serious issues and

5 Wood, P. R., 2007. Set off and Netting, Derivatives, Clearing Systems. Sweet &

Maxwell. UK. pp.92-101.

6 Handerson, S. K., 2010. Henderson on Derivatives. LexisNexis UK. pp.42-68.

7 What Is London’S Euro Clearing Market And Why Is Brussels Worried?'. 2017.

Available through: <https://webcache.googleusercontent.com/search?

q=cache:oWsR_mL3RCQJ:https://www.ft.com/content/18dcf566-5025-11e7-bfb8-

2

playing an intermediary role between buyer and sellers5. They discount various instrument in

return for certain margin and becomes the central counterparty for clearing and settling trades.

Thus, by this way, they plays a substantial role in maintaining financial stability. Henderson

defined derivatives as a financial product or instrument which value depends upon underlying

assets i.e. currency, security or commodity. It includes future, options and others. Central bank is

the leading authority that owes accountability to maintain financial stability through control over

money supply. The authority designs laws and economic rules and regulation for efficient

financial regulative framework6.

In London, Financial services and business volume goes beyond $900bn a day and the

most important thing is that it centered on Euro-dominated contracts of derivatives by LSE’s

(London Stock Exchange) Clearing Houses (LCH). Brussel’s proposal stated that in order to

maintain economic stability, EU regulatory authority must be given power to look overseas

clearing houses which can threaten systematic risk on financial stability in Europe. After the

economic crisis in 2008, clearing becomes a key pillar for boosting stability in the global

financial market. There are number of clearing houses i.e. LCH, Dutsche Borse’s Eurex who

plays an intermediary role between sellers and buyers of the financial instruments as they

exchange cheques, bills and other instrument for certain margin. They are also accountable for

looking the future exchanges for the trading account settlement.

The city stands in the dominant position for the clearing of derivative instruments

denominated in euro even though UK never intended to join eurozone. After the Brexit, the key

issue is that how UK located clearing houses will be regulated and policed because current rules

of EU will be no longer required to be follow7. However, its failure may bring serious issues and

5 Wood, P. R., 2007. Set off and Netting, Derivatives, Clearing Systems. Sweet &

Maxwell. UK. pp.92-101.

6 Handerson, S. K., 2010. Henderson on Derivatives. LexisNexis UK. pp.42-68.

7 What Is London’S Euro Clearing Market And Why Is Brussels Worried?'. 2017.

Available through: <https://webcache.googleusercontent.com/search?

q=cache:oWsR_mL3RCQJ:https://www.ft.com/content/18dcf566-5025-11e7-bfb8-

2

huge ramifications to the EU. It is often complaint that LCH had increased its margin which

means that participants have to keep high collateral for the debt which leads to aggravated debt

crisis in Eurozone. Thus, in this regard, the main target of the EU is to give sufficient power to

European Security & Market Authority (ESMA) to examine the systematic risks that can be

posed by clearing houses located overseas. The body examine their businesses and its proportion

which is denominated in Euro currencies for ensuring financial stability.

Euro Clearing (EC) has been emerged as a key battleground in the negotiation process of

Brexit. European Central Bank (ECB) has made significant efforts to gain insight of lucrative

euro clearing market after refendum. Currently, the Euro denominated currencies which are

cleared in London, BOE (Bank of England) owes accountability to look oversight &

supervision8. However, now, after Brexit, settlement of such financial instrument that are traded

outside EU exposed to the risk of financial stability due to emergence of more than one currency.

Politicians believes that Eurozone must control all the Euro clearing covering control over

margin, collateral and managing the risk of credit default by the party. So, that, outside clearing

agents will not be able to charge additional margin which they intended to arise from the credit

in Euro. Therefore, ECB announced that there is a need of necessary amendments that will allow

regulators to examine and monitor such risk that are linked with the clearing houses and lead to

affect the monetary policy and currency stability.

ECB recommends several amendments in article 22 of the statue which provides legal

base to the eurosystem to perform role as of central bank under currently European Market

Infrastructure Regulations (EMIR) proposed so as to stabilize the euro currency. According to

the amendments, ECB can make regulations to promote sound clearing system for all the

financial instruments. EU created a centrally controlled system for the credit rating agencies, put

997009366969%3Fmhq5j%3De4+&cd=1&hl=en&ct=clnk&gl=in> [Accessed on 11

August 2017].

8 'ECB In Drive To Control Post-Brexit Euro Clearing'. 2017. Available through:

<https://webcache.googleusercontent.com/search?q=cache:UIMkjUwUQWkJ:https://

www.ft.com/content/8888e560-57e5-11e7-9fed-c19e2700005f%3Fmhq5j

%3De4+&cd=1&hl=en&ct=clnk&gl=in> [Accessed on 11 August 2017]

3

means that participants have to keep high collateral for the debt which leads to aggravated debt

crisis in Eurozone. Thus, in this regard, the main target of the EU is to give sufficient power to

European Security & Market Authority (ESMA) to examine the systematic risks that can be

posed by clearing houses located overseas. The body examine their businesses and its proportion

which is denominated in Euro currencies for ensuring financial stability.

Euro Clearing (EC) has been emerged as a key battleground in the negotiation process of

Brexit. European Central Bank (ECB) has made significant efforts to gain insight of lucrative

euro clearing market after refendum. Currently, the Euro denominated currencies which are

cleared in London, BOE (Bank of England) owes accountability to look oversight &

supervision8. However, now, after Brexit, settlement of such financial instrument that are traded

outside EU exposed to the risk of financial stability due to emergence of more than one currency.

Politicians believes that Eurozone must control all the Euro clearing covering control over

margin, collateral and managing the risk of credit default by the party. So, that, outside clearing

agents will not be able to charge additional margin which they intended to arise from the credit

in Euro. Therefore, ECB announced that there is a need of necessary amendments that will allow

regulators to examine and monitor such risk that are linked with the clearing houses and lead to

affect the monetary policy and currency stability.

ECB recommends several amendments in article 22 of the statue which provides legal

base to the eurosystem to perform role as of central bank under currently European Market

Infrastructure Regulations (EMIR) proposed so as to stabilize the euro currency. According to

the amendments, ECB can make regulations to promote sound clearing system for all the

financial instruments. EU created a centrally controlled system for the credit rating agencies, put

997009366969%3Fmhq5j%3De4+&cd=1&hl=en&ct=clnk&gl=in> [Accessed on 11

August 2017].

8 'ECB In Drive To Control Post-Brexit Euro Clearing'. 2017. Available through:

<https://webcache.googleusercontent.com/search?q=cache:UIMkjUwUQWkJ:https://

www.ft.com/content/8888e560-57e5-11e7-9fed-c19e2700005f%3Fmhq5j

%3De4+&cd=1&hl=en&ct=clnk&gl=in> [Accessed on 11 August 2017]

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

restrictions on short selling of EU debt and put brake on speculation & hedging9. Authorities

have been permitted to look over the creditworthiness of euro-denominated instruments. EC

(European Commission) also recently planned to investigate EMIR including the examination of

clearers. If ECB provides clear authority to the central bank for creating sound and efficient

clearing operations within EU and with others nations than it will be a clear signal to London.

These powers present an improved role for central bank with regards to the supervisory system

of CCPs, specifically, to supervise third party for the clearing of euro-denominated instruments.

Besides this, relocation of huge clearing agents like LCH will be followed only if EU

regulators will be unable to closely supervise the CH located in London. It is just like to that of

America in which US dollar is mostly cleared outside US; still regulators have enough direct

oversight of UK located clearing houses. Till the time, EU legislations do not allow ECB to have

a direct oversight to supervise outsight clearing houses that are clearing euro dominated

instruments; the EU authority will have power to make policies for liquidity management for the

economic stability. Currently, euro-sterling swaps are used to cope up with such prevailing issue,

still, BOE (Bank of England) is committed to convey necessary information with the ECB that is

regulated by EU law and after Brexit, it needs to renegotiate. Thus, more power has been given

to EU regulators such as ECB, ESMA and others for managing possible crisis risk. Thus, the key

concern of the paper is to investigate euro clearing control issues and purposes at examining the

legal and regulatory power of both the UK & EU with respect to central counterparties10.

9 EU-Managed Control Of Euro Clearing Is Not Viable'. 2017. Available through:

<https://webcache.googleusercontent.com/search?q=cache:o1tU8P_Dm-YJ:https://

www.ft.com/content/64f5d320-3403-11e7-99bd-13beb0903fa3%3Fmhq5j

%3De4+&cd=2&hl=en&ct=clnk&gl=in> [Accessed on 11 August 2017]

10 Cremades, M. T., 2017. Brexit and the European Union: General Institutional and Legal

Consideration. [PDF]. Available through: <

http://www.europarl.europa.eu/RegData/etudes/STUD/2017/571404/IPOL_STU(2017)57

1404_EN.pdf>. [Accessed on 11th August 2017].

4

have been permitted to look over the creditworthiness of euro-denominated instruments. EC

(European Commission) also recently planned to investigate EMIR including the examination of

clearers. If ECB provides clear authority to the central bank for creating sound and efficient

clearing operations within EU and with others nations than it will be a clear signal to London.

These powers present an improved role for central bank with regards to the supervisory system

of CCPs, specifically, to supervise third party for the clearing of euro-denominated instruments.

Besides this, relocation of huge clearing agents like LCH will be followed only if EU

regulators will be unable to closely supervise the CH located in London. It is just like to that of

America in which US dollar is mostly cleared outside US; still regulators have enough direct

oversight of UK located clearing houses. Till the time, EU legislations do not allow ECB to have

a direct oversight to supervise outsight clearing houses that are clearing euro dominated

instruments; the EU authority will have power to make policies for liquidity management for the

economic stability. Currently, euro-sterling swaps are used to cope up with such prevailing issue,

still, BOE (Bank of England) is committed to convey necessary information with the ECB that is

regulated by EU law and after Brexit, it needs to renegotiate. Thus, more power has been given

to EU regulators such as ECB, ESMA and others for managing possible crisis risk. Thus, the key

concern of the paper is to investigate euro clearing control issues and purposes at examining the

legal and regulatory power of both the UK & EU with respect to central counterparties10.

9 EU-Managed Control Of Euro Clearing Is Not Viable'. 2017. Available through:

<https://webcache.googleusercontent.com/search?q=cache:o1tU8P_Dm-YJ:https://

www.ft.com/content/64f5d320-3403-11e7-99bd-13beb0903fa3%3Fmhq5j

%3De4+&cd=2&hl=en&ct=clnk&gl=in> [Accessed on 11 August 2017]

10 Cremades, M. T., 2017. Brexit and the European Union: General Institutional and Legal

Consideration. [PDF]. Available through: <

http://www.europarl.europa.eu/RegData/etudes/STUD/2017/571404/IPOL_STU(2017)57

1404_EN.pdf>. [Accessed on 11th August 2017].

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.2 Problem statement

Eurozone is not controlled by a single sovereign and LCH is one of the biggest clearing

houses that alone clear huge amount of euro-denominated financial instruments. They are

adjusting their margin on the transactions cleared which created doubt on the credit viability.

Divergent national interest for the euro clearing indulged huge risk into the system. Therefore,

EU implemented a centrally controlled system so as to create the system on fair basis in views of

eurozone authorities. Thus, this is the key concern for which the study will provide useful insight

for examining legislative framework and competing regulatory authorities power of both the UK

& EU. It is a current prevailing issue which gains scholar attention & interest to conduct a new

investigation in respective field.

1.3 Research aims and objectives

Aim: To explore legal and tactical analysis of the competing regulatory powers of UK & EU

with respect to central counterparties for euro clearing system

Objectives:

To explore the concept of Euro clearing controlled framework

To examine the impact of Brexit over political uncertainty & legal complexities

To make legal and tactical evaluation of UK and EU’s regulatory authorities power with

respect to central counterparties

1.4 Potential contribution

UK recently voted to left EU membership on 23rd June 2016, this recent refendum brings

significant uncertainties in the legal & political environment. As Brexit took place recently,

therefore, there are only few studies conducted therefore, the current study will provide a

conceptual framework to the scholars who are likely to investigate the issue in future. In

addition, governing authorities of both UK and EU can also get important insight towards

examining their competing regulatory powers with reference to the central counterparties in the

currency clearing system.

1.5 Disposition

Chapter 1: Introduction: It is the commencing chapter which details out in-depth

overview of the research issue along with its rationale and key aims & objectives. Moreover, it

will discuss the significance and potential contribution of the study.

5

Eurozone is not controlled by a single sovereign and LCH is one of the biggest clearing

houses that alone clear huge amount of euro-denominated financial instruments. They are

adjusting their margin on the transactions cleared which created doubt on the credit viability.

Divergent national interest for the euro clearing indulged huge risk into the system. Therefore,

EU implemented a centrally controlled system so as to create the system on fair basis in views of

eurozone authorities. Thus, this is the key concern for which the study will provide useful insight

for examining legislative framework and competing regulatory authorities power of both the UK

& EU. It is a current prevailing issue which gains scholar attention & interest to conduct a new

investigation in respective field.

1.3 Research aims and objectives

Aim: To explore legal and tactical analysis of the competing regulatory powers of UK & EU

with respect to central counterparties for euro clearing system

Objectives:

To explore the concept of Euro clearing controlled framework

To examine the impact of Brexit over political uncertainty & legal complexities

To make legal and tactical evaluation of UK and EU’s regulatory authorities power with

respect to central counterparties

1.4 Potential contribution

UK recently voted to left EU membership on 23rd June 2016, this recent refendum brings

significant uncertainties in the legal & political environment. As Brexit took place recently,

therefore, there are only few studies conducted therefore, the current study will provide a

conceptual framework to the scholars who are likely to investigate the issue in future. In

addition, governing authorities of both UK and EU can also get important insight towards

examining their competing regulatory powers with reference to the central counterparties in the

currency clearing system.

1.5 Disposition

Chapter 1: Introduction: It is the commencing chapter which details out in-depth

overview of the research issue along with its rationale and key aims & objectives. Moreover, it

will discuss the significance and potential contribution of the study.

5

Chapter: 2: Literature review: The given section discuss the key issue in detailed manner

by extracting useful information from various secondary sources, more importantly, journal

articles, recent news published on Brexit and others to pay emphasizes upon various legislations

to examine competing regulatory powers of EU & UK concerned with central counterparties.

Chapter: 3: Research methodology: Under this section, research methods, approach,

design, paradigm, data collection & analysis methods has been provided. It is necessary to apply

suitable & appropriate methodology because it affects the quality of results.

Chapter: 4: Data Findings and analysis: The particular section has gather data set and

analyzes & interprets the results to reflect key findings with the chosen area of the research. It is

the most crucial chapter on which the justifiable conclusion is made after deeply & thoroughly

investing the issue.

Chapter 5: Conclusion & Recommendation: The dissertation ends with this chapter which

presents summarized results of the whole study and provides a justifiable conclusion along with

some excellent recommendations to overcome the issue.

6

by extracting useful information from various secondary sources, more importantly, journal

articles, recent news published on Brexit and others to pay emphasizes upon various legislations

to examine competing regulatory powers of EU & UK concerned with central counterparties.

Chapter: 3: Research methodology: Under this section, research methods, approach,

design, paradigm, data collection & analysis methods has been provided. It is necessary to apply

suitable & appropriate methodology because it affects the quality of results.

Chapter: 4: Data Findings and analysis: The particular section has gather data set and

analyzes & interprets the results to reflect key findings with the chosen area of the research. It is

the most crucial chapter on which the justifiable conclusion is made after deeply & thoroughly

investing the issue.

Chapter 5: Conclusion & Recommendation: The dissertation ends with this chapter which

presents summarized results of the whole study and provides a justifiable conclusion along with

some excellent recommendations to overcome the issue.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CHAPTER -2 LITERATURE REVIEW

2.0 Introduction

Review of literature is the process in which earlier studies results are provided to gain

broad knowledge of the concept. In this section, previous studies that are conducted with respect

to similar area of the field have been presented. It is a two-folded approach which discusses the

findings & discussion of number of scholarly articles to create a conceptual base for the chosen

research issue.

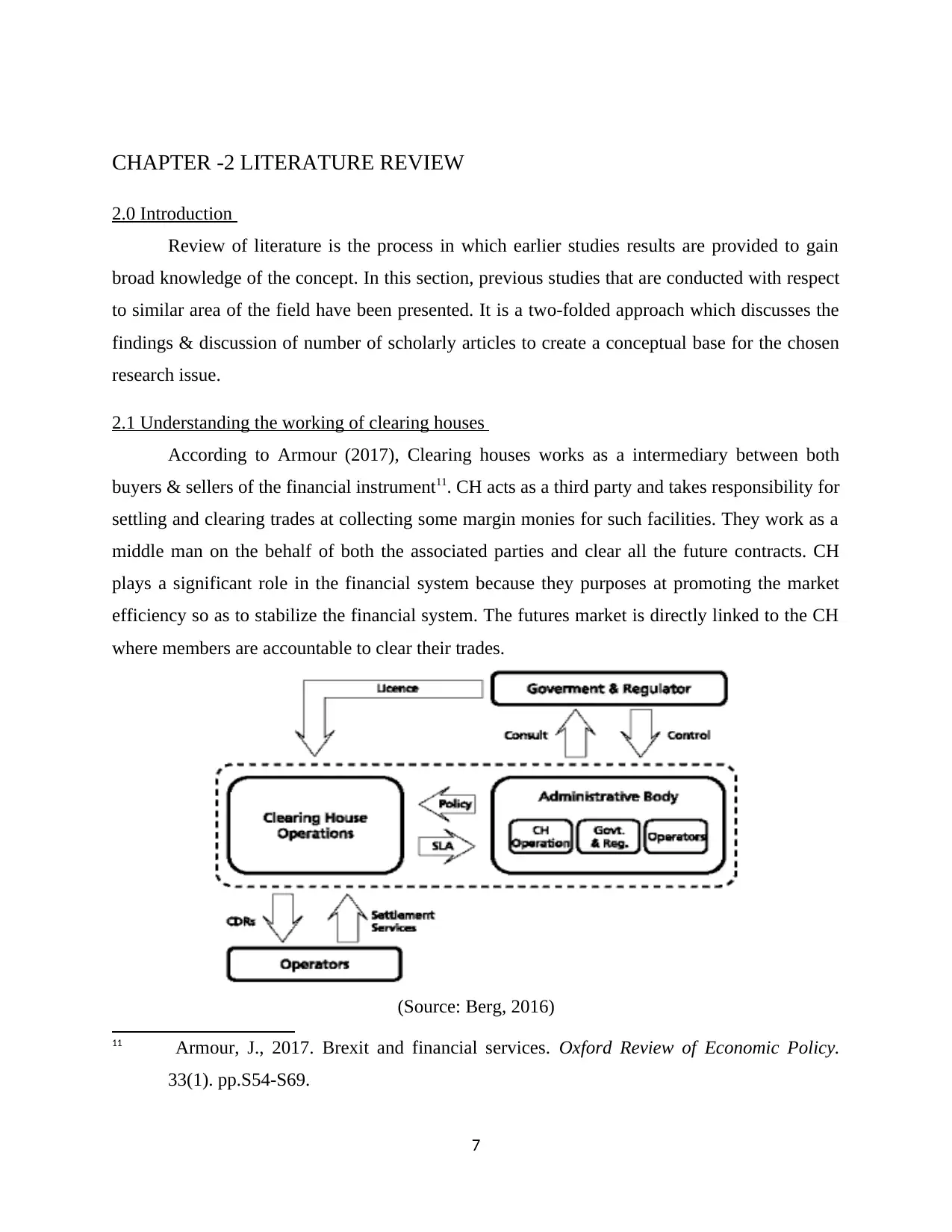

2.1 Understanding the working of clearing houses

According to Armour (2017), Clearing houses works as a intermediary between both

buyers & sellers of the financial instrument11. CH acts as a third party and takes responsibility for

settling and clearing trades at collecting some margin monies for such facilities. They work as a

middle man on the behalf of both the associated parties and clear all the future contracts. CH

plays a significant role in the financial system because they purposes at promoting the market

efficiency so as to stabilize the financial system. The futures market is directly linked to the CH

where members are accountable to clear their trades.

(Source: Berg, 2016)

11 Armour, J., 2017. Brexit and financial services. Oxford Review of Economic Policy.

33(1). pp.S54-S69.

7

2.0 Introduction

Review of literature is the process in which earlier studies results are provided to gain

broad knowledge of the concept. In this section, previous studies that are conducted with respect

to similar area of the field have been presented. It is a two-folded approach which discusses the

findings & discussion of number of scholarly articles to create a conceptual base for the chosen

research issue.

2.1 Understanding the working of clearing houses

According to Armour (2017), Clearing houses works as a intermediary between both

buyers & sellers of the financial instrument11. CH acts as a third party and takes responsibility for

settling and clearing trades at collecting some margin monies for such facilities. They work as a

middle man on the behalf of both the associated parties and clear all the future contracts. CH

plays a significant role in the financial system because they purposes at promoting the market

efficiency so as to stabilize the financial system. The futures market is directly linked to the CH

where members are accountable to clear their trades.

(Source: Berg, 2016)

11 Armour, J., 2017. Brexit and financial services. Oxford Review of Economic Policy.

33(1). pp.S54-S69.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

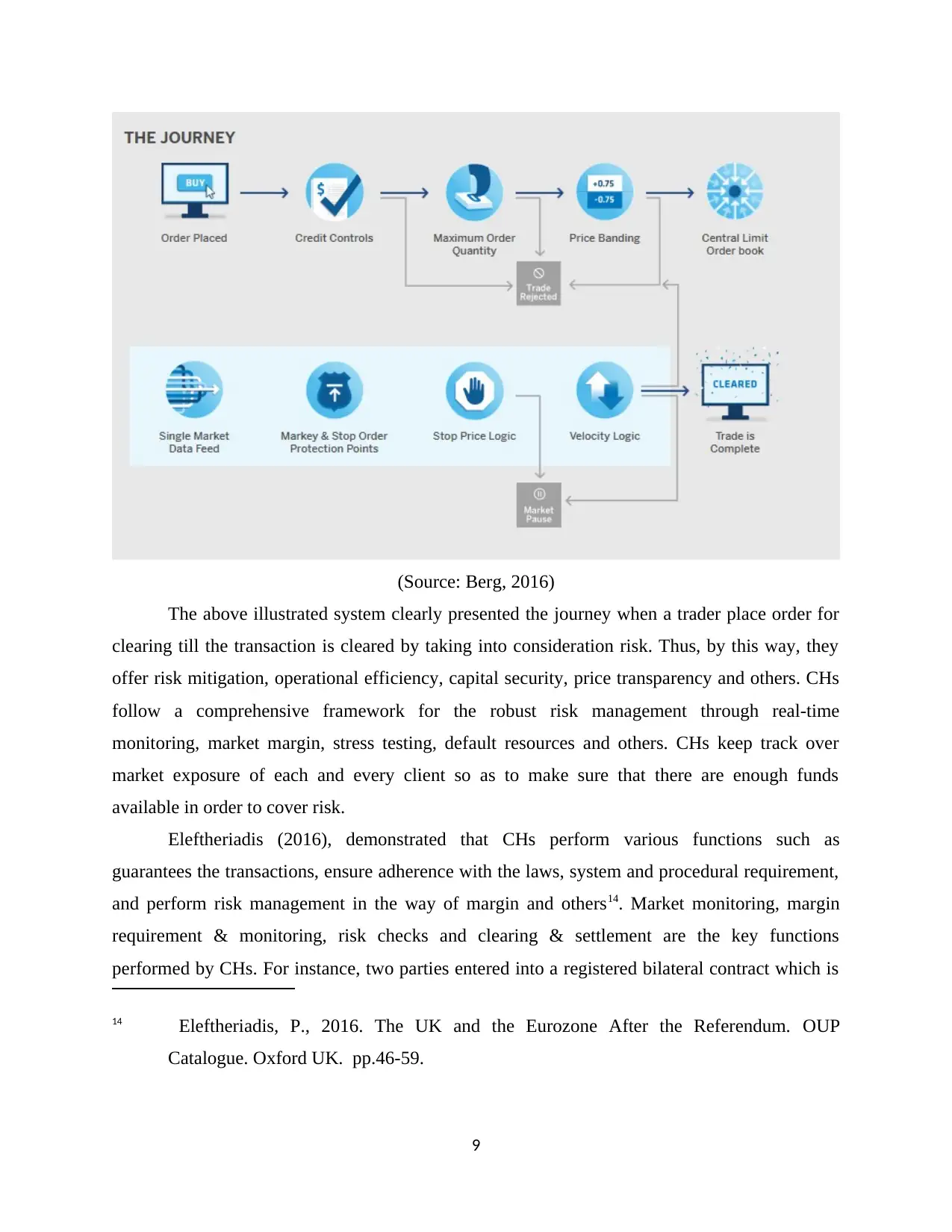

CH is a place where various financial instruments such as bills, cheques, derivatives &

securities are exchanged by the member bank so as to meet the urgent cash requirement. Duffie

(2014) stated that CH provides a platform for trading by mutual acceptance over the terms

regards to price, contract maturity period and quantity as well12. Afterwards, the contract is

cleared by offsetting the positions together, called netting. CH only provides the services of

clearing & settlements for those futures that are traded at an exchange. As they work on the

behalf of buyer and seller, therefore, it can be said that CH acts as a neutral counterparty and

assure trade integrity & soundness. Similar to CH, central counterparty clearing (CCP) also

provides clearing facilities but in different manner by taking counterparties (brokers, members

bank) risk. CHs has been established in order to facilitate transactions among various banks such

as cheque & bill clearance and others.

In accordance with the views of Dörry (2017), tthe process of clearing needs several

precautionary measures that are necessary to be applied instantaneously during the period when

order is placed & transaction is settled13. While handling & settling future trades, CHs have

number of checkpoints in the electronic trading function so as to maintain financial integrity.

12 Duffie, D., 2014. Resolution of failing central counterparties. Sweet & Maxwell. Oxford

UK. pp.28-36.

13 Dörry, S., 2017. The geo-politics of Brexit, the euro and the City of London. Geoforum.

85. pp.1-4.

8

securities are exchanged by the member bank so as to meet the urgent cash requirement. Duffie

(2014) stated that CH provides a platform for trading by mutual acceptance over the terms

regards to price, contract maturity period and quantity as well12. Afterwards, the contract is

cleared by offsetting the positions together, called netting. CH only provides the services of

clearing & settlements for those futures that are traded at an exchange. As they work on the

behalf of buyer and seller, therefore, it can be said that CH acts as a neutral counterparty and

assure trade integrity & soundness. Similar to CH, central counterparty clearing (CCP) also

provides clearing facilities but in different manner by taking counterparties (brokers, members

bank) risk. CHs has been established in order to facilitate transactions among various banks such

as cheque & bill clearance and others.

In accordance with the views of Dörry (2017), tthe process of clearing needs several

precautionary measures that are necessary to be applied instantaneously during the period when

order is placed & transaction is settled13. While handling & settling future trades, CHs have

number of checkpoints in the electronic trading function so as to maintain financial integrity.

12 Duffie, D., 2014. Resolution of failing central counterparties. Sweet & Maxwell. Oxford

UK. pp.28-36.

13 Dörry, S., 2017. The geo-politics of Brexit, the euro and the City of London. Geoforum.

85. pp.1-4.

8

(Source: Berg, 2016)

The above illustrated system clearly presented the journey when a trader place order for

clearing till the transaction is cleared by taking into consideration risk. Thus, by this way, they

offer risk mitigation, operational efficiency, capital security, price transparency and others. CHs

follow a comprehensive framework for the robust risk management through real-time

monitoring, market margin, stress testing, default resources and others. CHs keep track over

market exposure of each and every client so as to make sure that there are enough funds

available in order to cover risk.

Eleftheriadis (2016), demonstrated that CHs perform various functions such as

guarantees the transactions, ensure adherence with the laws, system and procedural requirement,

and perform risk management in the way of margin and others14. Market monitoring, margin

requirement & monitoring, risk checks and clearing & settlement are the key functions

performed by CHs. For instance, two parties entered into a registered bilateral contract which is

14 Eleftheriadis, P., 2016. The UK and the Eurozone After the Referendum. OUP

Catalogue. Oxford UK. pp.46-59.

9

The above illustrated system clearly presented the journey when a trader place order for

clearing till the transaction is cleared by taking into consideration risk. Thus, by this way, they

offer risk mitigation, operational efficiency, capital security, price transparency and others. CHs

follow a comprehensive framework for the robust risk management through real-time

monitoring, market margin, stress testing, default resources and others. CHs keep track over

market exposure of each and every client so as to make sure that there are enough funds

available in order to cover risk.

Eleftheriadis (2016), demonstrated that CHs perform various functions such as

guarantees the transactions, ensure adherence with the laws, system and procedural requirement,

and perform risk management in the way of margin and others14. Market monitoring, margin

requirement & monitoring, risk checks and clearing & settlement are the key functions

performed by CHs. For instance, two parties entered into a registered bilateral contract which is

14 Eleftheriadis, P., 2016. The UK and the Eurozone After the Referendum. OUP

Catalogue. Oxford UK. pp.46-59.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 48