Impact of Interest Rate Fluctuation on Commercial Banks in Tajikistan

VerifiedAdded on 2023/01/23

|78

|33590

|89

AI Summary

This dissertation focuses on analyzing the impact of interest rate fluctuation on commercial banks in Tajikistan after accession to the WTO. It examines the relationship between interest rate and commercial banks, analyzes the impact of interest rate liberalization in the financial system of Tajikistan, and compares Tajikistan's interest rate with its neighboring countries. The research aims to fill the research gap in understanding the fluctuation of interest rates and its effects on the banking industry in Tajikistan.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Dissertation (Chapter 1,2, 3

Modification)

Modification)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

CHAPTER 1 - INTRODUCTION...................................................................................................5

INTRODUCTION ..........................................................................................................................5

Background .................................................................................................................................5

Research Problem........................................................................................................................8

Aim& Objectives of the Research...............................................................................................8

Research Questions......................................................................................................................9

Research Hypothesis....................................................................................................................9

Justification for the Research.......................................................................................................9

Brief Description of the Research Methodology.........................................................................9

Outline of the Thesis..................................................................................................................10

terms...........................................................................................................................................10

Scope of the Research................................................................................................................12

Limitation of study.....................................................................................................................13

Theoretical background ............................................................................................................13

Chapter summary ......................................................................................................................14

CHAPTER 2: LITERATURE REVIEW.......................................................................................15

2.0 Introduction..........................................................................................................................15

2.1 Current condition of interest rate and associated theories with interest rate.......................15

2.1.1 Overview...........................................................................................................................15

2.1.2 Theory related to interest rate fluctuation.........................................................................15

2.1.3 International theory related to Interest rate fluctuation.....................................................16

2.1.4 Comparison of both theories.............................................................................................16

2.1.5 Condition of interest rate in commercial banks................................................................16

2.1.6 Impact of Interest rate fluctuation in Tajikistan................................................................19

2.2 Theory behind fluctuation of Interest Rates ........................................................................21

2.2.1 Background.......................................................................................................................21

2.2.2 Interest Rate Parity............................................................................................................21

2.2.2 Classical theory.................................................................................................................22

2.2.3 How both theory affect country........................................................................................23

2.2.4 Model behind used in order to know fluctuation of Interest Rates...................................25

CHAPTER 1 - INTRODUCTION...................................................................................................5

INTRODUCTION ..........................................................................................................................5

Background .................................................................................................................................5

Research Problem........................................................................................................................8

Aim& Objectives of the Research...............................................................................................8

Research Questions......................................................................................................................9

Research Hypothesis....................................................................................................................9

Justification for the Research.......................................................................................................9

Brief Description of the Research Methodology.........................................................................9

Outline of the Thesis..................................................................................................................10

terms...........................................................................................................................................10

Scope of the Research................................................................................................................12

Limitation of study.....................................................................................................................13

Theoretical background ............................................................................................................13

Chapter summary ......................................................................................................................14

CHAPTER 2: LITERATURE REVIEW.......................................................................................15

2.0 Introduction..........................................................................................................................15

2.1 Current condition of interest rate and associated theories with interest rate.......................15

2.1.1 Overview...........................................................................................................................15

2.1.2 Theory related to interest rate fluctuation.........................................................................15

2.1.3 International theory related to Interest rate fluctuation.....................................................16

2.1.4 Comparison of both theories.............................................................................................16

2.1.5 Condition of interest rate in commercial banks................................................................16

2.1.6 Impact of Interest rate fluctuation in Tajikistan................................................................19

2.2 Theory behind fluctuation of Interest Rates ........................................................................21

2.2.1 Background.......................................................................................................................21

2.2.2 Interest Rate Parity............................................................................................................21

2.2.2 Classical theory.................................................................................................................22

2.2.3 How both theory affect country........................................................................................23

2.2.4 Model behind used in order to know fluctuation of Interest Rates...................................25

2.2.5 Analysis of how fluctuation of interest rates took place...................................................26

2.2.6 Impact of Negative Interest Rates on implementation in different banks or financial

institutions in Tajikistan.............................................................................................................27

2.3 To analyse the impact of interest rate liberalisation in the financial system of Tajikistan..31

2.3.1 Briefing.............................................................................................................................31

2.3.2 Interest rate relaxation relationship with the financial system..........................................31

2.3.3 Relative factors behind the cause of fluctuation of interest rate.......................................38

2.4 Comparing the interest rate liberalization of Tajikistan with the neighbourhood countries42

2.4.1 Prelude..............................................................................................................................42

2.4.2 Interest rate liberalisation of Tajikistan with neighbouring countries..............................42

2.4.3 Benefits and challenges of accession to WTO in the banking sector of Tajikistan..........46

2.5 Limitation of the review framework address by the study..................................................53

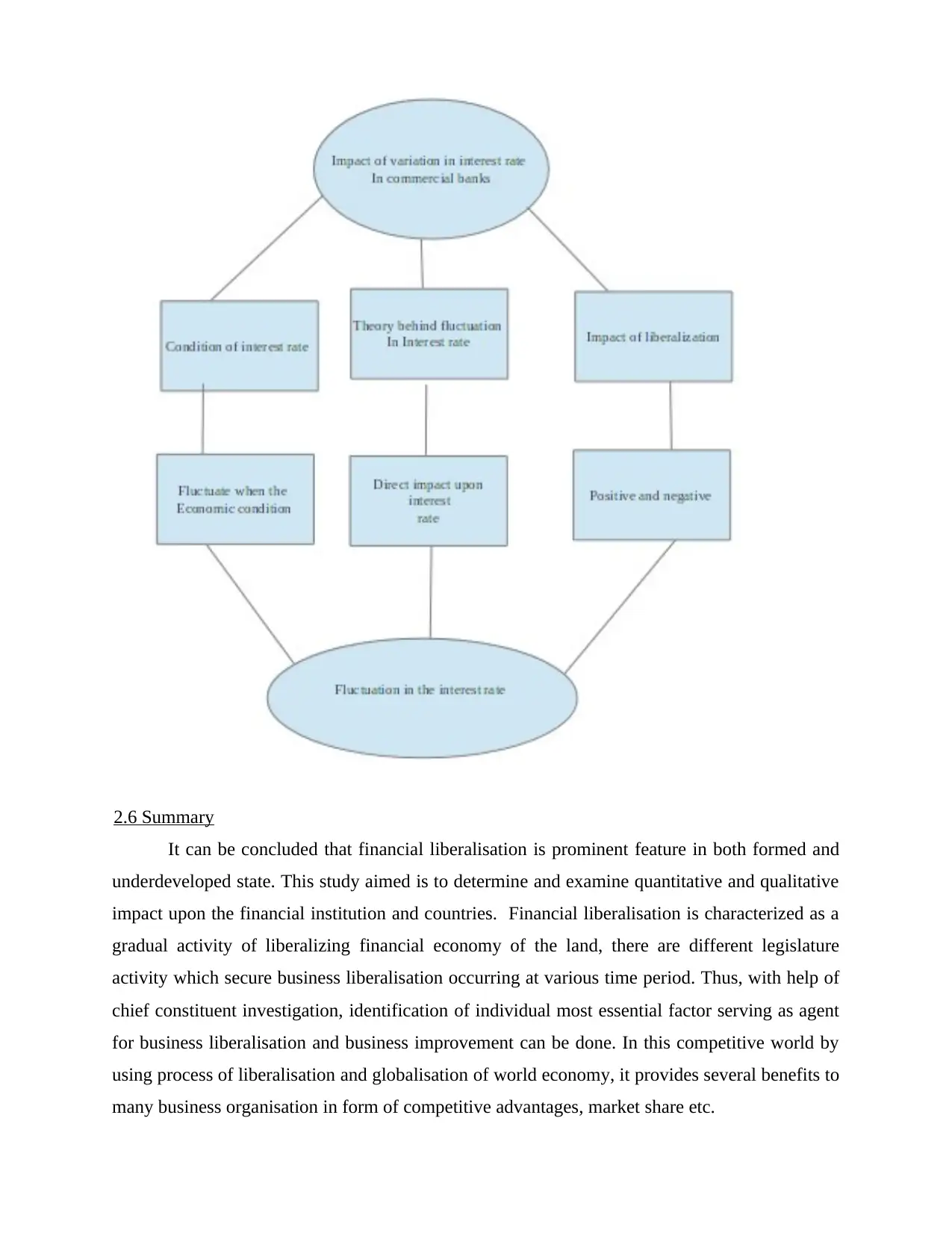

2.6 Summary..............................................................................................................................53

CHAPTER 3: RESEARCH METHODOLOGY...........................................................................55

3.1 Theoretical paradigm and assumptions................................................................................55

3.1.1 Epistemology....................................................................................................................55

3.1.2 Ontology...........................................................................................................................55

3.1.3 Methodology.....................................................................................................................56

3.2 Selection of research methods.............................................................................................56

3.3 Research Philosophy............................................................................................................56

3.4 Research approach...............................................................................................................59

3.5 Pilot Study............................................................................................................................60

3.6 Research design, Strategy and Procedures...........................................................................61

3.7 Data Collection....................................................................................................................61

3.7.1 Primary Data Collection...................................................................................................62

3.7.1.1 Quantitative Questionnaire............................................................................................63

3.7.1.2 Qualitative Structure......................................................................................................63

3.7.2 Secondary Data.................................................................................................................64

3.8 Sampling..............................................................................................................................64

3.9 Ethical Considerations.........................................................................................................65

3.9.1 Informed consent..............................................................................................................65

2.2.6 Impact of Negative Interest Rates on implementation in different banks or financial

institutions in Tajikistan.............................................................................................................27

2.3 To analyse the impact of interest rate liberalisation in the financial system of Tajikistan..31

2.3.1 Briefing.............................................................................................................................31

2.3.2 Interest rate relaxation relationship with the financial system..........................................31

2.3.3 Relative factors behind the cause of fluctuation of interest rate.......................................38

2.4 Comparing the interest rate liberalization of Tajikistan with the neighbourhood countries42

2.4.1 Prelude..............................................................................................................................42

2.4.2 Interest rate liberalisation of Tajikistan with neighbouring countries..............................42

2.4.3 Benefits and challenges of accession to WTO in the banking sector of Tajikistan..........46

2.5 Limitation of the review framework address by the study..................................................53

2.6 Summary..............................................................................................................................53

CHAPTER 3: RESEARCH METHODOLOGY...........................................................................55

3.1 Theoretical paradigm and assumptions................................................................................55

3.1.1 Epistemology....................................................................................................................55

3.1.2 Ontology...........................................................................................................................55

3.1.3 Methodology.....................................................................................................................56

3.2 Selection of research methods.............................................................................................56

3.3 Research Philosophy............................................................................................................56

3.4 Research approach...............................................................................................................59

3.5 Pilot Study............................................................................................................................60

3.6 Research design, Strategy and Procedures...........................................................................61

3.7 Data Collection....................................................................................................................61

3.7.1 Primary Data Collection...................................................................................................62

3.7.1.1 Quantitative Questionnaire............................................................................................63

3.7.1.2 Qualitative Structure......................................................................................................63

3.7.2 Secondary Data.................................................................................................................64

3.8 Sampling..............................................................................................................................64

3.9 Ethical Considerations.........................................................................................................65

3.9.1 Informed consent..............................................................................................................65

3.9.2 Privacy and confidentiality...............................................................................................65

3.10 Methodological Limitations..............................................................................................65

3.10.1 Reliability........................................................................................................................65

3.10.2 Validity...........................................................................................................................65

3.11 Limitations and Delimitation of Study..............................................................................66

3.12 Summary............................................................................................................................66

REFERENCES..............................................................................................................................68

3.10 Methodological Limitations..............................................................................................65

3.10.1 Reliability........................................................................................................................65

3.10.2 Validity...........................................................................................................................65

3.11 Limitations and Delimitation of Study..............................................................................66

3.12 Summary............................................................................................................................66

REFERENCES..............................................................................................................................68

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CHAPTER 1 - INTRODUCTION

INTRODUCTION

Financial liberalisation is essential for the financial activities of the organisation.

Introduction chapter provides the background and rationale of the study so that relevant aims and

objectives can be developed. It also describes research hypotheses and brief analysis of research

methods will be done.

Background

Financial liberalisation should be understood as the removal of restrictions in the

activities of banks in provision of financial services, for example, in the provision of loans,

deposit registration, etc. This enables the financial institutions to decide independently on whom

and by what criteria to allocate loans, allows them to set the price (interest rate) for loans and

interests on received deposits, and determine where to (aside from lending) allocate the funds at

their disposal (Bogdan & Biklen, 2003). There is a close connection between liberalisation and

banking crisis, which deserves close attention.

In the 1990s, beneath the impact of economic complications a number of countries started

fundamental changes in monetary policy, institutional structure and overall performance of the

economy as well as in ways to accomplish the goals (Harrod, 2008). Due to the gradual

economic backlog, many countries in Latin America and Asia, as well as countries with

centralised planning, relatively quickly abandoned government intervention in the economy and

liberalised economic activity. The process of liberalisation also spread to the financial sector, and

first of all to banks that for a long time belonged to the most regulated spheres of

entrepreneurship, not only in developing countries but also in many developed countries.

Furthermost specialists settle that financial liberalisation in itself is a progressive change since it

allows you to direct the investments to the place where they can be used most effectively. Thus,

liberalisation helps to accelerate economic progression (Sneider & Larner, 2009). Nevertheless,

the knowledge of numerous countries illustrates that under certain circumstances it can produce a

growth in rates and risks for some period of time.

Financial liberalisation significantly changes the environment banking sector. With

liberalisation, there is a risk of a disruption in the normal operation of the banking sector due to a

combination of the consequences of banks' behaviour in a regulated environment accumulated

but not solved problems and incentives acting in a new liberal environment (Ponterotto, 2005).

INTRODUCTION

Financial liberalisation is essential for the financial activities of the organisation.

Introduction chapter provides the background and rationale of the study so that relevant aims and

objectives can be developed. It also describes research hypotheses and brief analysis of research

methods will be done.

Background

Financial liberalisation should be understood as the removal of restrictions in the

activities of banks in provision of financial services, for example, in the provision of loans,

deposit registration, etc. This enables the financial institutions to decide independently on whom

and by what criteria to allocate loans, allows them to set the price (interest rate) for loans and

interests on received deposits, and determine where to (aside from lending) allocate the funds at

their disposal (Bogdan & Biklen, 2003). There is a close connection between liberalisation and

banking crisis, which deserves close attention.

In the 1990s, beneath the impact of economic complications a number of countries started

fundamental changes in monetary policy, institutional structure and overall performance of the

economy as well as in ways to accomplish the goals (Harrod, 2008). Due to the gradual

economic backlog, many countries in Latin America and Asia, as well as countries with

centralised planning, relatively quickly abandoned government intervention in the economy and

liberalised economic activity. The process of liberalisation also spread to the financial sector, and

first of all to banks that for a long time belonged to the most regulated spheres of

entrepreneurship, not only in developing countries but also in many developed countries.

Furthermost specialists settle that financial liberalisation in itself is a progressive change since it

allows you to direct the investments to the place where they can be used most effectively. Thus,

liberalisation helps to accelerate economic progression (Sneider & Larner, 2009). Nevertheless,

the knowledge of numerous countries illustrates that under certain circumstances it can produce a

growth in rates and risks for some period of time.

Financial liberalisation significantly changes the environment banking sector. With

liberalisation, there is a risk of a disruption in the normal operation of the banking sector due to a

combination of the consequences of banks' behaviour in a regulated environment accumulated

but not solved problems and incentives acting in a new liberal environment (Ponterotto, 2005).

The environment, previously protected from external influences, together with strict regulation

of financial and credit activities, contributed to the development of negative phenomena in the

work of banks. In general, this means that decisions to place assets were made without taking

into account the market criteria for maximising profits. Often banks provided loans on the basis

of political requirements or subjective desire of owners, sometimes simultaneously acting as

customers of banking services. In such a situation, the banks were not formed, and the skills

necessary for successful functioning in an unprotected and poorly regulated environment created

as a result of financial liberalisation could not be formed.

The previous practice of granting loans created a threat of decreasing the quality of the

loan portfolio and, at the same time, did not allow bankers to monitor debtors promptly and

assess the degree of risk in lending (Harrod, 2008). Usually financial liberalisation is conceded

out within the framework of the global approach of macroeconomic balance, financial

liberalisation and structural modifications (Senhadji, 2000). As a result of overall liberalisation

the economic situation of many enterprises deteriorates and the total of resources used to repay

bank loans is reduced. In the course of reforms and the implementation of stabilisation plans

which are often related with financial liberalisation banks change the way monetary policy is

implemented. These policy changes significantly affect the rate of interest change. Also, the role

of direct delivery of credits among banks decreases and the meaning of indirect tools of

influence on fluidity in the economy such as operations in the open money market, accounting of

bills increases. Thus, in order to achieve the profitable targets banks often varies interest rate.

In the progression of macroeconomic stabilisation further restrictions on economic policy

are also introduced (Berg and Krueger, 2002). These modifications in turn decrease the

possibility for banks to appeal other resources, such as primarily loans from the central bank and

short term financial resources purchased in e-market. The costs of obtaining these assets are

increasing. These factors are primarily associated with the changing interest rates and thus

influences the profits and financing functions of the economy.

At the same time situation is complicated by the fact that debtor companies themselves

are feeling the needs of limiting economic and financial policies. As an outcome, the liquidity

crisis can provoke a wave of non-payments, as debtors lose the ability to fulfil their obligations.

(Cojocaru and et.al., 2016).

A side effect of successful stabilisation programs is a high level of market interest rates,

of financial and credit activities, contributed to the development of negative phenomena in the

work of banks. In general, this means that decisions to place assets were made without taking

into account the market criteria for maximising profits. Often banks provided loans on the basis

of political requirements or subjective desire of owners, sometimes simultaneously acting as

customers of banking services. In such a situation, the banks were not formed, and the skills

necessary for successful functioning in an unprotected and poorly regulated environment created

as a result of financial liberalisation could not be formed.

The previous practice of granting loans created a threat of decreasing the quality of the

loan portfolio and, at the same time, did not allow bankers to monitor debtors promptly and

assess the degree of risk in lending (Harrod, 2008). Usually financial liberalisation is conceded

out within the framework of the global approach of macroeconomic balance, financial

liberalisation and structural modifications (Senhadji, 2000). As a result of overall liberalisation

the economic situation of many enterprises deteriorates and the total of resources used to repay

bank loans is reduced. In the course of reforms and the implementation of stabilisation plans

which are often related with financial liberalisation banks change the way monetary policy is

implemented. These policy changes significantly affect the rate of interest change. Also, the role

of direct delivery of credits among banks decreases and the meaning of indirect tools of

influence on fluidity in the economy such as operations in the open money market, accounting of

bills increases. Thus, in order to achieve the profitable targets banks often varies interest rate.

In the progression of macroeconomic stabilisation further restrictions on economic policy

are also introduced (Berg and Krueger, 2002). These modifications in turn decrease the

possibility for banks to appeal other resources, such as primarily loans from the central bank and

short term financial resources purchased in e-market. The costs of obtaining these assets are

increasing. These factors are primarily associated with the changing interest rates and thus

influences the profits and financing functions of the economy.

At the same time situation is complicated by the fact that debtor companies themselves

are feeling the needs of limiting economic and financial policies. As an outcome, the liquidity

crisis can provoke a wave of non-payments, as debtors lose the ability to fulfil their obligations.

(Cojocaru and et.al., 2016).

A side effect of successful stabilisation programs is a high level of market interest rates,

which is established, in particular, due to the accelerated inflation rate as compared to the

expected decrease, as well as the appreciation of the exchange rate. In the latter case, the

situation of enterprises that produce goods destined for export deteriorates, as their

competitiveness in the world market falls. Exporting enterprises in Tajikistan are forced to adjust

to the new condition increase efficiency, sales growth of products inside the country. Else, they

can face financial problems, which rises the risk for banks’ lending to these enterprises (Elsherif,

2016).

The interest rate has been one of the critical factor in encouraging the liberalisation

process within financial sector. When interest rates are increased it leads to increase refinancing

rate and thus banks have to pay higher cost to manage their resources. The increased interest

rates also affect debtors in negative manner. When such situations occurs in Tajikistan then,

investment projects promising high income despite increasing interest rates resort to commercial

banks (Fletcher, 2017)

Negative impact due to fluctuating economic policies and refinancing rate in Tajikistan is

changing the value of interest rates reliant on the loan reimbursement stage. In the course of

liberalisation, the differentiation among the interest rates short term and long term loans which is

of great meaning for banks usually decreases. In Tajikistan interest rates are differentiated on the

basis of loan terms. Hence, commercial banks of the country are able to generate profits by

transferring short-term liabilities (deposits) to long-term assets (loans) (Lane, 2018). Interest on

deposits mainly short-term through administrative limits was set at a much lower level than

interest rates on loans granted which usually issued for a long period. In a number of countries

such as UK and USA as a result of interest rate liberalisation, possibility of easy profit-making in

this way has diminished, as the cost of seeking financial resources has increased and it has suited

more problematic to establish high interest rates for the use of credit (Macit, 2017)

Banks are difficult to resist the negative impact on interest rates. Typically, bank liabilities

are sufficiently liquid, because they represent deposits that are not limited to a certain period, and

banks can quickly lose them. In contrast, assets have significantly less liquidity. Credit

obligations of borrowers, as a rule, can be sold to other entities only with large losses. The

severance of contractual credit relations, in turn, is associated with additional costs in the form of

penalties (Turk, 2016)

Financial liberalisation leads to increased competition between the banks. Therefore, they are

expected decrease, as well as the appreciation of the exchange rate. In the latter case, the

situation of enterprises that produce goods destined for export deteriorates, as their

competitiveness in the world market falls. Exporting enterprises in Tajikistan are forced to adjust

to the new condition increase efficiency, sales growth of products inside the country. Else, they

can face financial problems, which rises the risk for banks’ lending to these enterprises (Elsherif,

2016).

The interest rate has been one of the critical factor in encouraging the liberalisation

process within financial sector. When interest rates are increased it leads to increase refinancing

rate and thus banks have to pay higher cost to manage their resources. The increased interest

rates also affect debtors in negative manner. When such situations occurs in Tajikistan then,

investment projects promising high income despite increasing interest rates resort to commercial

banks (Fletcher, 2017)

Negative impact due to fluctuating economic policies and refinancing rate in Tajikistan is

changing the value of interest rates reliant on the loan reimbursement stage. In the course of

liberalisation, the differentiation among the interest rates short term and long term loans which is

of great meaning for banks usually decreases. In Tajikistan interest rates are differentiated on the

basis of loan terms. Hence, commercial banks of the country are able to generate profits by

transferring short-term liabilities (deposits) to long-term assets (loans) (Lane, 2018). Interest on

deposits mainly short-term through administrative limits was set at a much lower level than

interest rates on loans granted which usually issued for a long period. In a number of countries

such as UK and USA as a result of interest rate liberalisation, possibility of easy profit-making in

this way has diminished, as the cost of seeking financial resources has increased and it has suited

more problematic to establish high interest rates for the use of credit (Macit, 2017)

Banks are difficult to resist the negative impact on interest rates. Typically, bank liabilities

are sufficiently liquid, because they represent deposits that are not limited to a certain period, and

banks can quickly lose them. In contrast, assets have significantly less liquidity. Credit

obligations of borrowers, as a rule, can be sold to other entities only with large losses. The

severance of contractual credit relations, in turn, is associated with additional costs in the form of

penalties (Turk, 2016)

Financial liberalisation leads to increased competition between the banks. Therefore, they are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

forced to both reduce the cost of finding resources, and to resist competitors in their use. As a

result, the profit decreases. liabilities of banks are affected by competition from other financial

institutions domestic and foreign that have access to the banking market. The situation of banks

is complicated by the fact that enterprises themselves can quickly inform about their financial

situation, which allows them to directly establish links with the owners of financial resources

without resorting to the help of banks. As a rule, enterprises that are able to seek non-bank

financing sources are the best customers and their loss means for banks increasing the level of

credit portfolio risk.

Research Problem

The main research gap that exists is the impact of interest rate on bank is highly impacting in

banking sector. But it has become difficult to identify that whether interest rate has changed due

to liberalization or not. So, this is the gap that exists. However, research done on it is not

sufficient to find out fluctuation in interest rate. Financial liberalisation is very difficult to

measure because economic fluctuations are beyond the control of any financial institutes. Hence

this has become the major issue in banking industry hence fluctuations of interest rate can not be

monitored and measured. (McKinnon and Shaw, 1973). Government of nation or finance

department of country has to keep close eye over interest rate fluctuations but it is very difficult

task that is affecting entire banking industry to great extent.

Aim& Objectives of the Research

Aim

To analyze impact of variation in interest rate in commercial banks in Tajikistan after

accession to the WTO. A case study on commercial banks of Tajikistan

Objectives

To determine relationship between interest rate and commercial banks in Tajikistan.

To examine with theory, models and analysis in order to investigate the fluctuation of

interest rate.

To analyse impact of interest rate liberalisation in financial system of Tajikistan.

To compare the interest rate and liberalisation of Tajikistan with its neighbouring nations.

result, the profit decreases. liabilities of banks are affected by competition from other financial

institutions domestic and foreign that have access to the banking market. The situation of banks

is complicated by the fact that enterprises themselves can quickly inform about their financial

situation, which allows them to directly establish links with the owners of financial resources

without resorting to the help of banks. As a rule, enterprises that are able to seek non-bank

financing sources are the best customers and their loss means for banks increasing the level of

credit portfolio risk.

Research Problem

The main research gap that exists is the impact of interest rate on bank is highly impacting in

banking sector. But it has become difficult to identify that whether interest rate has changed due

to liberalization or not. So, this is the gap that exists. However, research done on it is not

sufficient to find out fluctuation in interest rate. Financial liberalisation is very difficult to

measure because economic fluctuations are beyond the control of any financial institutes. Hence

this has become the major issue in banking industry hence fluctuations of interest rate can not be

monitored and measured. (McKinnon and Shaw, 1973). Government of nation or finance

department of country has to keep close eye over interest rate fluctuations but it is very difficult

task that is affecting entire banking industry to great extent.

Aim& Objectives of the Research

Aim

To analyze impact of variation in interest rate in commercial banks in Tajikistan after

accession to the WTO. A case study on commercial banks of Tajikistan

Objectives

To determine relationship between interest rate and commercial banks in Tajikistan.

To examine with theory, models and analysis in order to investigate the fluctuation of

interest rate.

To analyse impact of interest rate liberalisation in financial system of Tajikistan.

To compare the interest rate and liberalisation of Tajikistan with its neighbouring nations.

In addition, any combination of a market portfolio with a risk-free asset also provides an

efficient portfolio with less risk and less expected income. This approach is macroeconomic,

since in it the main object of study. Next difference between the Markowits and Tobin theory is

that Markowits emphasised the mathematical analysis of the consequences of the initial data and

the development of algorithms for solving optimisation problems. Tobin also took as a basis the

analysis of the factors that compel investors to form a portfolio of securities rather than keep

them in one form.

Research Questions

Q.1 What is the ongoing concern regarding interest rate on the commercial banks in Tajikistan?

Q.2 What are the relative factors behind the cause of fluctuation of interest rate?

Q.3 How does the interest rate liberalisation impact on its financial system?

Q.4 What are the recommendations to guide the banks on achieving interest rate stability?

Research Hypothesis

H0- The research hypothesis significant relationship between interest rate liberalisation and

banks ‘s performance in Tajikistan.

H1- The research hypothesis is there is no significant relationship between interest rate

liberalisation and banks ‘s performance in Tajikistan.

Justification for the Research

Study will concentrate on different prudential regulations in financial sector. It will pay

emphases on level of interest rate fluctuations and its impact on entire financial sector.

Furthermore, what are factors that impact on developing country financial systems. Beside this,

how interest rates are determined and how it impact on banking sector. Along with it, the study

will explain about how interest rate is controlled and how it results in improving economic

growth. Along with it, the research will help in analysing various kinds of liberalisation

component that can help in monetary control.

Brief Description of the Research Methodology

It is necessary to apply different research methods to gather data. This is because it helps in

gathering relevant and precise data. In this research, econometric methodology is been used.

Also, some statistical tests are applied to find out mean, mode, median, etc. besides this,

researcher has taken assistance of primary data in which questionnaire and interview are taken.

Furthermore, Mckinnon and Shaw hypothesis research methodology is applied. However, data is

efficient portfolio with less risk and less expected income. This approach is macroeconomic,

since in it the main object of study. Next difference between the Markowits and Tobin theory is

that Markowits emphasised the mathematical analysis of the consequences of the initial data and

the development of algorithms for solving optimisation problems. Tobin also took as a basis the

analysis of the factors that compel investors to form a portfolio of securities rather than keep

them in one form.

Research Questions

Q.1 What is the ongoing concern regarding interest rate on the commercial banks in Tajikistan?

Q.2 What are the relative factors behind the cause of fluctuation of interest rate?

Q.3 How does the interest rate liberalisation impact on its financial system?

Q.4 What are the recommendations to guide the banks on achieving interest rate stability?

Research Hypothesis

H0- The research hypothesis significant relationship between interest rate liberalisation and

banks ‘s performance in Tajikistan.

H1- The research hypothesis is there is no significant relationship between interest rate

liberalisation and banks ‘s performance in Tajikistan.

Justification for the Research

Study will concentrate on different prudential regulations in financial sector. It will pay

emphases on level of interest rate fluctuations and its impact on entire financial sector.

Furthermore, what are factors that impact on developing country financial systems. Beside this,

how interest rates are determined and how it impact on banking sector. Along with it, the study

will explain about how interest rate is controlled and how it results in improving economic

growth. Along with it, the research will help in analysing various kinds of liberalisation

component that can help in monetary control.

Brief Description of the Research Methodology

It is necessary to apply different research methods to gather data. This is because it helps in

gathering relevant and precise data. In this research, econometric methodology is been used.

Also, some statistical tests are applied to find out mean, mode, median, etc. besides this,

researcher has taken assistance of primary data in which questionnaire and interview are taken.

Furthermore, Mckinnon and Shaw hypothesis research methodology is applied. However, data is

analysed with SPSS. Hypotheses is framed and test are applied.

Outline of the Thesis

This thesis will be divided into several sectors: As first chapter will be introduction in which

researcher will explain the topic, background will be discussed. Apart from this, aim objectives

will be framed and problem statement s will be framed. In the second chapter researcher will use

literatures of other scholars in order to develop understanding about the subject matter. It will

emphases more on financial liberalisation and regulations of government will be reviews by

getting support of different authors views. Chapter third will be research methodology in which

scholar will explain and justify various methods that can be used in any kind of dissertation and

will specify the chosen method in the current research. It will explain the type of study it is and

will defines the data collection sources that are used to answer the research questions. Chapter

fourth will be analyses chapter in which scholar will gather all details and will analyses it in

qualitative manner. All the details will be presented in systemic manner so that valid conclusion

can be drawn. Chapter 5 will be discussion in which literature review and data analyses chapters

will be combined to discuss the topic. At last conclusion chapter will come in which necessary

findings will be drawn and necessary recommendations will be given.

terms

Interest rate: It is defined as the amount paid per period which is the proportion of principal

amount or the amount which is borrowed, lent or deposited. (Shaofeng, 2017)

Commercial banks: These are the financial institutions which performs and regulate the

financial operations and accepts deposits, manage loan services, accounting services and other

transactional operations. Commercial banks also assign certificates of deposit and savings to

individuals as well as organisations. (Alotaibi, 2015)

Financial liberalisation: It refers to the removal or elimination of government ceiling or

regulation on interest rates and all other attributes of financial intermediaries. (Zhang, 2018)

Refinancing rate: minimum bid rate and can be defined as the interest rate which is paid

by commercial banks when they borrow money from European central bank. (Kothari, 2018)

Liquidity: It can be described as the extent up to which an asset can be sold or purchased

in the market at its intrinsic value. Thus, liquidity refers to the ease in the converting an asset into

cash. (Bun, 2018)

Outline of the Thesis

This thesis will be divided into several sectors: As first chapter will be introduction in which

researcher will explain the topic, background will be discussed. Apart from this, aim objectives

will be framed and problem statement s will be framed. In the second chapter researcher will use

literatures of other scholars in order to develop understanding about the subject matter. It will

emphases more on financial liberalisation and regulations of government will be reviews by

getting support of different authors views. Chapter third will be research methodology in which

scholar will explain and justify various methods that can be used in any kind of dissertation and

will specify the chosen method in the current research. It will explain the type of study it is and

will defines the data collection sources that are used to answer the research questions. Chapter

fourth will be analyses chapter in which scholar will gather all details and will analyses it in

qualitative manner. All the details will be presented in systemic manner so that valid conclusion

can be drawn. Chapter 5 will be discussion in which literature review and data analyses chapters

will be combined to discuss the topic. At last conclusion chapter will come in which necessary

findings will be drawn and necessary recommendations will be given.

terms

Interest rate: It is defined as the amount paid per period which is the proportion of principal

amount or the amount which is borrowed, lent or deposited. (Shaofeng, 2017)

Commercial banks: These are the financial institutions which performs and regulate the

financial operations and accepts deposits, manage loan services, accounting services and other

transactional operations. Commercial banks also assign certificates of deposit and savings to

individuals as well as organisations. (Alotaibi, 2015)

Financial liberalisation: It refers to the removal or elimination of government ceiling or

regulation on interest rates and all other attributes of financial intermediaries. (Zhang, 2018)

Refinancing rate: minimum bid rate and can be defined as the interest rate which is paid

by commercial banks when they borrow money from European central bank. (Kothari, 2018)

Liquidity: It can be described as the extent up to which an asset can be sold or purchased

in the market at its intrinsic value. Thus, liquidity refers to the ease in the converting an asset into

cash. (Bun, 2018)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Fluctuations in interest rate: The quick changes in the interest rates are known as

fluctuations. These fluctuations are the result of inflation, supply and demand variation and

economic stability. (Aid, 2019).

Interest rate stability: For the stability and better functioning of interest rates it is

required that changes in interest rates are smooth so that financial stability can be promoted. The

reduced volatility of interest rate has direct impact on the insolvency of the commercial banks.

(Lu, 2018).

Fiscal policies: These are known as the policies which describes the utilisation of

government expenditure and revenue collection so that economy can be improved.

(GONZALEZ, 2017)

WTO: World trade organisation (WTO) is intergovernmental institute which regulates the

international trades between countries. (Smart, 2017)

Financial repression: It is known as the policies through which government and

regulatory bodies can enhance domestically held debt and tax income. (Siddiqui, 2019)

Foreign exchange trade: This trade is global decentralised market for the trading of

currencies. Thus, through this procedure currencies are bought, exchanged and sold at the

determined prices. (Verdiyeva, 2018)

Redistributive economy: It is defined as the economy system in which substantial share of

wealth is mobilised into the centralised administrative control and out from the common

population. (Shaofeng, 2017)

Gross domestic product (GDP): it is monetary measurement that describes value of goods

that are produced in a fixed time period in country. (Alotaibi, 2015)

Marginal efficiency of capital: The discount rate which equates the price or monetary

value of the fixed capital asset with the present discounted price of expected income is known as

marginal efficiency of capital. (Kothari, 2018)

Depreciation: Depreciation refers to the reduction or decline in the monetary value of an asset

over time period. The cost of the assets is allocated to the time period through which they were

in use (Aid, 2019).

Amortisation: It is known as the process or method of paying off the debts or loans

through regular payments. It is also used for both loans and assets. (Bun, 2018)

Accumulated capital: Accumulated capital is defined as the increment in the value of assets by

fluctuations. These fluctuations are the result of inflation, supply and demand variation and

economic stability. (Aid, 2019).

Interest rate stability: For the stability and better functioning of interest rates it is

required that changes in interest rates are smooth so that financial stability can be promoted. The

reduced volatility of interest rate has direct impact on the insolvency of the commercial banks.

(Lu, 2018).

Fiscal policies: These are known as the policies which describes the utilisation of

government expenditure and revenue collection so that economy can be improved.

(GONZALEZ, 2017)

WTO: World trade organisation (WTO) is intergovernmental institute which regulates the

international trades between countries. (Smart, 2017)

Financial repression: It is known as the policies through which government and

regulatory bodies can enhance domestically held debt and tax income. (Siddiqui, 2019)

Foreign exchange trade: This trade is global decentralised market for the trading of

currencies. Thus, through this procedure currencies are bought, exchanged and sold at the

determined prices. (Verdiyeva, 2018)

Redistributive economy: It is defined as the economy system in which substantial share of

wealth is mobilised into the centralised administrative control and out from the common

population. (Shaofeng, 2017)

Gross domestic product (GDP): it is monetary measurement that describes value of goods

that are produced in a fixed time period in country. (Alotaibi, 2015)

Marginal efficiency of capital: The discount rate which equates the price or monetary

value of the fixed capital asset with the present discounted price of expected income is known as

marginal efficiency of capital. (Kothari, 2018)

Depreciation: Depreciation refers to the reduction or decline in the monetary value of an asset

over time period. The cost of the assets is allocated to the time period through which they were

in use (Aid, 2019).

Amortisation: It is known as the process or method of paying off the debts or loans

through regular payments. It is also used for both loans and assets. (Bun, 2018)

Accumulated capital: Accumulated capital is defined as the increment in the value of assets by

the means of profits or investments. It motivates the profit so that initial monetary value can be

increased. (Zhang, 2018)

Scope of the Research

The research scope’s to analyse financial market from regional or the national

perspective instead it evaluates financial market of the Republic of Tajikistan after accession to

the WTO. Also how financial reforms effected in economically similar countries. Also a set of

significant internal and external relationships of financial market segments that determine the

direction of impact aimed at reducing the deformation of the economic role of the financial

market.

Scope of the research devoted to the analysis of interest rate liberalisation that can be

divided into four areas:

(1) A quantitative assessment of income from interest rate liberalisation;

(2) The political and economic reasons for using interest rate liberalisation;

(3) Financial repression’s impact on growth of economy

(4) Optimality of interest rate liberalisation.

The study will describe about Quantitative estimates of income from financial institutions

and its significance for public finances. For example, Reinhart (2008) notes that even with

moderate inflation, interest rate liberalisation often leads to maintaining a real interest rate at a

negative level for a long period of time. De Melo (2002) also cited that the transition to financial

liberalisation leads to significant losses in budget revenues and requires budgetary reforms. As

for modern developed countries, such measures as the nationalisation of the funded part of the

pension system and the increase in the share of government bonds on the balance of commercial

banks have allowed to avoid defaulting on public debt.

The most extensive area of research on banking interest rate liberalisation affects the

ways of tightening financial regulation on economic growth. The works of such scientists as Fry

(1996) note that such a policy allows ensuring financial stability and avoiding the negative

financial shocks’s impact on growth of country and its economic condition.

The main contribution of this work will be directed to the optimal policy of financial

liberalisation. This problem is considered in the literature in the context of the government

getting inflationary tax and optimising budget revenues in conditions of evasion from paying

income tax. The subject of research is developing countries characterised by a low level of

increased. (Zhang, 2018)

Scope of the Research

The research scope’s to analyse financial market from regional or the national

perspective instead it evaluates financial market of the Republic of Tajikistan after accession to

the WTO. Also how financial reforms effected in economically similar countries. Also a set of

significant internal and external relationships of financial market segments that determine the

direction of impact aimed at reducing the deformation of the economic role of the financial

market.

Scope of the research devoted to the analysis of interest rate liberalisation that can be

divided into four areas:

(1) A quantitative assessment of income from interest rate liberalisation;

(2) The political and economic reasons for using interest rate liberalisation;

(3) Financial repression’s impact on growth of economy

(4) Optimality of interest rate liberalisation.

The study will describe about Quantitative estimates of income from financial institutions

and its significance for public finances. For example, Reinhart (2008) notes that even with

moderate inflation, interest rate liberalisation often leads to maintaining a real interest rate at a

negative level for a long period of time. De Melo (2002) also cited that the transition to financial

liberalisation leads to significant losses in budget revenues and requires budgetary reforms. As

for modern developed countries, such measures as the nationalisation of the funded part of the

pension system and the increase in the share of government bonds on the balance of commercial

banks have allowed to avoid defaulting on public debt.

The most extensive area of research on banking interest rate liberalisation affects the

ways of tightening financial regulation on economic growth. The works of such scientists as Fry

(1996) note that such a policy allows ensuring financial stability and avoiding the negative

financial shocks’s impact on growth of country and its economic condition.

The main contribution of this work will be directed to the optimal policy of financial

liberalisation. This problem is considered in the literature in the context of the government

getting inflationary tax and optimising budget revenues in conditions of evasion from paying

income tax. The subject of research is developing countries characterised by a low level of

financial development, tax evasion and monetisation of budget deficits. It is not assumed that

financial liberalisation is associated with inflationary financing of the budget deficit or a

decrease in the efficiency of the financial system. The redistribution of financial resources

between the private and public sectors does not make the work of financial intermediaries less

effective. Thus, the model is more in line with the situation typical for developed countries,

which have shifted from the financial crisis of 2007-2009 to fiscal stress. If we consider financial

reform as an implicit tax on the financial sector, then the problem of optimal taxation arises.

Among other things, this study answers two questions. First, is financial liberalisation an element

of optimal taxation. Second, whether financial liberalisation and explicit taxes are the perfect

substitutes.

It is also be necessary to consider the currency market of Tajikistan, the interrelations and

interdependencies arising in the process of its functioning taking into account interest rate

liberalisation. Therefore, is the process of regulating the aggregate of economic relations

regarding the formation and implementation of the monetary policy of Tajikistan, taking into

account financial liberalisation and strengthening the functional interrelationships of the currency

sector of the financial market with its other sectors.

Limitation of study

The study has been effective towards role of fluctuations in the interest rates on financial

systems. However, The most significant limitation of study is within data collection. Different

commercial banks have different interest rates and thus it is very challenging and complex to

interpret the impact of varying interest rates. Banking stability is considered as major factors

which affect their ability to manage the interest rates. primary and secondary sources are used to

analyses the research area. Several limitations of the study are associated with this.

However, interest rate variations are very quick and unpredictable thus the use of sources

from past few years can affect the relevancy of the findings. primary data is collected through

questionnaires and interviews are also conducted. Thus, due to budget limitations the sample size

was kept low. The data is gathered from different organisations. Thus, variations can occur in

data collection. However, accuracy and integrity of data can also be affected. Beside this, as

interview is taken so it becomes difficult to interpret finding from it.

Theoretical background

The study focus on identifying whether financial liberalization impact on banking sector or not.

financial liberalisation is associated with inflationary financing of the budget deficit or a

decrease in the efficiency of the financial system. The redistribution of financial resources

between the private and public sectors does not make the work of financial intermediaries less

effective. Thus, the model is more in line with the situation typical for developed countries,

which have shifted from the financial crisis of 2007-2009 to fiscal stress. If we consider financial

reform as an implicit tax on the financial sector, then the problem of optimal taxation arises.

Among other things, this study answers two questions. First, is financial liberalisation an element

of optimal taxation. Second, whether financial liberalisation and explicit taxes are the perfect

substitutes.

It is also be necessary to consider the currency market of Tajikistan, the interrelations and

interdependencies arising in the process of its functioning taking into account interest rate

liberalisation. Therefore, is the process of regulating the aggregate of economic relations

regarding the formation and implementation of the monetary policy of Tajikistan, taking into

account financial liberalisation and strengthening the functional interrelationships of the currency

sector of the financial market with its other sectors.

Limitation of study

The study has been effective towards role of fluctuations in the interest rates on financial

systems. However, The most significant limitation of study is within data collection. Different

commercial banks have different interest rates and thus it is very challenging and complex to

interpret the impact of varying interest rates. Banking stability is considered as major factors

which affect their ability to manage the interest rates. primary and secondary sources are used to

analyses the research area. Several limitations of the study are associated with this.

However, interest rate variations are very quick and unpredictable thus the use of sources

from past few years can affect the relevancy of the findings. primary data is collected through

questionnaires and interviews are also conducted. Thus, due to budget limitations the sample size

was kept low. The data is gathered from different organisations. Thus, variations can occur in

data collection. However, accuracy and integrity of data can also be affected. Beside this, as

interview is taken so it becomes difficult to interpret finding from it.

Theoretical background

The study focus on identifying whether financial liberalization impact on banking sector or not.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Also, it analysis economic condition of country and other economies. Here, many authors have

worked on finding out relation between financial liberalization and economy.

The theoretical basis of the research was the scientific works foreign authors in the field of

studying the financial and banking system, its structure, functions and role in the economic

system. Also studies on the regulation of the interest rate, as well as the effective work of the

successful implementation and reform of the financial system in the world.

However, the beginning of the modern portfolio theory was laid by Markowitz (), whose theory,

the problem of portfolio optimization is to minimize the risk at a given average profitability.

Tobin also showed that the market portfolio, where there is a set of all available at the moment

investor securities is effective. In addition, any combination of a market portfolio with a risk-free

asset also provides an efficient portfolio with less risk and less expected income. This approach

is macroeconomic, since it is considered as major aspect

Chapter summary

From above it is concluded that there are many patters due to which financial sector is

influenced. They are :

Financial liberalisation and open economy that protect against the risks associated with the

shock effect of cross-border short-term capital flows; an effective mechanism to prevent the

adoption of undercapitalised financial institutions (primarily banks) excessive risk can be created

only through a system of control by the stock market. Moreover, financial liberalisation decide

independently on whom to allocate loans, and determine where to the impact of economic

complications as well as in ways to accomplish the goals with centralised planning, and

liberalised economic activity. Different commercial banks have impact of varying interest rates

both primary and secondary sources interest rate variations unpredictable can affect the

relevancy. Optimal policy of financial liberalisation considered inflationary tax associated with

decrease in the efficiency between the private and public sectors intermediaries less effective.

Also, it is summarized that problem of financial liberalisation occurs due to the government and

optimising budget revenues in conditions of evasion from paying income tax. It is also be

necessary to consider the currency market of Tajikistan, the interrelations and interdependencies

arising in the process of its functioning taking into account interest rate liberalisation.

worked on finding out relation between financial liberalization and economy.

The theoretical basis of the research was the scientific works foreign authors in the field of

studying the financial and banking system, its structure, functions and role in the economic

system. Also studies on the regulation of the interest rate, as well as the effective work of the

successful implementation and reform of the financial system in the world.

However, the beginning of the modern portfolio theory was laid by Markowitz (), whose theory,

the problem of portfolio optimization is to minimize the risk at a given average profitability.

Tobin also showed that the market portfolio, where there is a set of all available at the moment

investor securities is effective. In addition, any combination of a market portfolio with a risk-free

asset also provides an efficient portfolio with less risk and less expected income. This approach

is macroeconomic, since it is considered as major aspect

Chapter summary

From above it is concluded that there are many patters due to which financial sector is

influenced. They are :

Financial liberalisation and open economy that protect against the risks associated with the

shock effect of cross-border short-term capital flows; an effective mechanism to prevent the

adoption of undercapitalised financial institutions (primarily banks) excessive risk can be created

only through a system of control by the stock market. Moreover, financial liberalisation decide

independently on whom to allocate loans, and determine where to the impact of economic

complications as well as in ways to accomplish the goals with centralised planning, and

liberalised economic activity. Different commercial banks have impact of varying interest rates

both primary and secondary sources interest rate variations unpredictable can affect the

relevancy. Optimal policy of financial liberalisation considered inflationary tax associated with

decrease in the efficiency between the private and public sectors intermediaries less effective.

Also, it is summarized that problem of financial liberalisation occurs due to the government and

optimising budget revenues in conditions of evasion from paying income tax. It is also be

necessary to consider the currency market of Tajikistan, the interrelations and interdependencies

arising in the process of its functioning taking into account interest rate liberalisation.

CHAPTER 2: LITERATURE REVIEW

2.0 Introduction

This section furnish a critical assessment of the major theoretical approaches which are

used to describe different theme in the literature review section. Therefore, this section, provides

a deep knowledge related to current condition of interest rate in commercial banks in Tajikistan

and then define different theories behind the fluctuation if interest rates in Tajikistan. Moreover,

it also analyse the outcome of involvement rate liberalisation in the financial system and then

define different factors behind the cause of fluctuation of interest rates. Lastly, by supporting

different author point of views, researcher describe the benefits and challenges of accession to

WTO in the banking sector of Tajikistan.

2.1 Current condition of interest rate and associated theories with interest rate

2.1.1 Overview

As per the viewpoints of Barrell, Karim and Ventouri, (2017), the term interest rate has

been defined as the proportion of the debt or loan amount which has been charged in form of

interest to the borrower. Author also state that there is a affirmative kinship between economic

growth and fiscal market and it is so because when the financial market is high, the economy of

country also rises and author also state the relationship between an ability of financial market in

order to redistribute capital and degree of development of the commercial enterprise, in turns, it

increases economic growth of country. As financial development of the country is actually a

ratio of size of securities market and credit market to Gross Domestic Product.

2.1.2 Theory related to interest rate fluctuation

As per the view of Holston (2017) interest rate parity is the approach which works behind

interest rate. It is a no – investing situation which represents an balance state in which the

capitalist will be different to interest rates. This theory is also work on two assumption i.e.

Capital mobility and perfect substitutability from both home and abroad assets. On the other side,

The mechanism of profit making by such commercial banks is explained by the Martin and et.al.,

(2018) in its studies that commercial banks holds the balances of their customers at which they

some amount of interest which is evidently lower than the interest rate they charge from their

customers while lending the money. Addition in the rate of interest rates widens this gap due to

which banks becomes more able to enhance their profitability.

2.0 Introduction

This section furnish a critical assessment of the major theoretical approaches which are

used to describe different theme in the literature review section. Therefore, this section, provides

a deep knowledge related to current condition of interest rate in commercial banks in Tajikistan

and then define different theories behind the fluctuation if interest rates in Tajikistan. Moreover,

it also analyse the outcome of involvement rate liberalisation in the financial system and then

define different factors behind the cause of fluctuation of interest rates. Lastly, by supporting

different author point of views, researcher describe the benefits and challenges of accession to

WTO in the banking sector of Tajikistan.

2.1 Current condition of interest rate and associated theories with interest rate

2.1.1 Overview

As per the viewpoints of Barrell, Karim and Ventouri, (2017), the term interest rate has

been defined as the proportion of the debt or loan amount which has been charged in form of

interest to the borrower. Author also state that there is a affirmative kinship between economic

growth and fiscal market and it is so because when the financial market is high, the economy of

country also rises and author also state the relationship between an ability of financial market in

order to redistribute capital and degree of development of the commercial enterprise, in turns, it

increases economic growth of country. As financial development of the country is actually a

ratio of size of securities market and credit market to Gross Domestic Product.

2.1.2 Theory related to interest rate fluctuation

As per the view of Holston (2017) interest rate parity is the approach which works behind

interest rate. It is a no – investing situation which represents an balance state in which the

capitalist will be different to interest rates. This theory is also work on two assumption i.e.

Capital mobility and perfect substitutability from both home and abroad assets. On the other side,

The mechanism of profit making by such commercial banks is explained by the Martin and et.al.,

(2018) in its studies that commercial banks holds the balances of their customers at which they

some amount of interest which is evidently lower than the interest rate they charge from their

customers while lending the money. Addition in the rate of interest rates widens this gap due to

which banks becomes more able to enhance their profitability.

2.1.3 International theory related to Interest rate fluctuation

Shokirov and Backhaus (2020) stated that Neo classical theory is the international theory

in which the interest rate is stated through legislation of decreasing minimal inferior. This theory

also explain two laws such that intake of a good in high amount which create a affirmative profit,

but on the other side, contentment of extra ingestion is not good as compared to previous

consumption. On the other side, another law state that best status where the ratio of dealing of

products is equal to ratio of minimum substitute of products The ultimate effect of such low

interest rate results into higher productivity through which the total output of the economy

increases.

2.1.4 Comparison of both theories

According to Durdyev and Ismail (2017) Interest rate parity theory is that approach

which differentiate the interest rate between two state is equal to the difference between the

progressive dealing rate and spot dealing rate. This theory show an important character in the

international dealing markets and also copulative the interest rates, spot exchange rate. While on

contrary, Neo classical theory mainly depend upon the classical demand for supply and demand

of capital theory of interest. This rate of interest is also concludes all the monetary and non-

monetary aspect of interest. The ultimate effect of such low interest rate is reflected on the

higher output of the nation which in turn accelerates the profitable growth.

Xie and Han (2019) argued that the IRP model only anticipate that there are endless

finances accessibility which may be further used for monetary system investment that is further

not practical. As a result, this theory also state that when the future and forward contracts are not

available to protection then it did not hold in the real world. On comparing it with Neo- classical

theory, It has also been observed that if interest rates remains high for too many months than it

leads to slow growth rate of business present in economy. In this above mentioned manner,

interest rates does not only affects economy but it also affects individual present in an economy.

2.1.5 Condition of interest rate in commercial banks

In the view of Mehrotra and Yetman (2015), the system of banking of Tajikistan is