Long term intention of studying MPA in Australia

VerifiedAdded on 2023/01/17

|43

|11339

|67

AI Summary

This dissertation explores the long term intentions of students from different cultures studying MPA in Australia. It discusses the benefits of pursuing Masters in Professional Accounting and its impact on future career prospects. The research aims to understand the concept of professional accounting, the competencies achieved through studying MPA, the job prospects after completion, and the suitable ways of accomplishing the long term intentions. The study focuses on students from Nepal, India, China, and Africa.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: DISSERTATION

Long term intention of studying MPA in Australia

Name of the Student:

Name of the University:

Author’s Note:

Long term intention of studying MPA in Australia

Name of the Student:

Name of the University:

Author’s Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1DISSERTATION

Acknowledgement

Thank you to all of those who have helped listened and encouraged me throughout this study. I

am indebted to my supervisor ……………………. whose guidance, advice and patience have

been immeasurable. My sincere thanks to all members of the…………… [Mention your

university/college name], both staff and students, whose continuous support have made this

thesis possible.

I would like to thank all of the participants in the study: students, teachers and Local Education

Authorities, for the time and help given throughout. Without their participation, this research

would not have been possible. In this context, I am also thankful to them, whose research work

helped me to execute this paper well.

Finally, I thank my family, without whom this thesis would not have been started or completed!

Your encouragement and support have never faltered; thank you.

Acknowledgement

Thank you to all of those who have helped listened and encouraged me throughout this study. I

am indebted to my supervisor ……………………. whose guidance, advice and patience have

been immeasurable. My sincere thanks to all members of the…………… [Mention your

university/college name], both staff and students, whose continuous support have made this

thesis possible.

I would like to thank all of the participants in the study: students, teachers and Local Education

Authorities, for the time and help given throughout. Without their participation, this research

would not have been possible. In this context, I am also thankful to them, whose research work

helped me to execute this paper well.

Finally, I thank my family, without whom this thesis would not have been started or completed!

Your encouragement and support have never faltered; thank you.

2DISSERTATION

Abstract

Masters in Professional Accounting is designed for the students those possess the long term

intention of obtaining specialized knowledge and research skills in accounting and related areas

of business. As a result, the students learn to implement advanced conceptual and practical

accounting knowledge for undertaking rewarding careers in accounting and related areas of

business. In addition to, the course also offers the direction for further specialized learning that

helps in applying coherent and advanced knowledge of accounting and business concepts for the

students of different cultural origin that includes India, China, Africa and Nepal. The aim of the

study is to determine what and why is the long term intention of four different culture-origin

students studying MPA (Masters in Professional Accounting) in Australia. The four different

cultures considered for this research are Nepal, India, China and Africa. Completion of the

research offers the scope of understanding the accounting job prospects in Nepal, India, China

and Africa as well as in international job platform. Studying the long term intention of the

students of different backgrounds helps in understanding the benefits the course is offering to the

students at international level. As a result, the research provides a scope of understanding what

the course has to offer for the students and how it tends to shape up their future in the long run.

Additionally, the research also provides an opportunity to investigate how completion of an

MPA degree successfully in Australia will help in allowing the students to take a career in

accounting field by developing the necessary skills and expertise required.

Abstract

Masters in Professional Accounting is designed for the students those possess the long term

intention of obtaining specialized knowledge and research skills in accounting and related areas

of business. As a result, the students learn to implement advanced conceptual and practical

accounting knowledge for undertaking rewarding careers in accounting and related areas of

business. In addition to, the course also offers the direction for further specialized learning that

helps in applying coherent and advanced knowledge of accounting and business concepts for the

students of different cultural origin that includes India, China, Africa and Nepal. The aim of the

study is to determine what and why is the long term intention of four different culture-origin

students studying MPA (Masters in Professional Accounting) in Australia. The four different

cultures considered for this research are Nepal, India, China and Africa. Completion of the

research offers the scope of understanding the accounting job prospects in Nepal, India, China

and Africa as well as in international job platform. Studying the long term intention of the

students of different backgrounds helps in understanding the benefits the course is offering to the

students at international level. As a result, the research provides a scope of understanding what

the course has to offer for the students and how it tends to shape up their future in the long run.

Additionally, the research also provides an opportunity to investigate how completion of an

MPA degree successfully in Australia will help in allowing the students to take a career in

accounting field by developing the necessary skills and expertise required.

3DISSERTATION

Table of Contents

Chapter 1: Introduction....................................................................................................................5

1.0 Overview................................................................................................................................5

1.1 Research aim..........................................................................................................................5

1.2 Research objectives...............................................................................................................6

1.3 Research questions.................................................................................................................6

1.4 Research scope.......................................................................................................................6

1.5 Structure of the dissertation...................................................................................................7

1.6 Summary................................................................................................................................7

Chapter 2: Literature review............................................................................................................8

2.0 Overview................................................................................................................................8

2.1 Professional accounting education........................................................................................8

2.2 Competencies achieved by studying professional accounting...............................................9

2.3 Demand of professional accounting jobs at global scale.....................................................10

2.4 Long-term intentions of pursuing professional accounting.................................................10

2.5 Career opportunities of studying professional accounting..................................................11

2.6 The various issues noticed in the field of Professional Accounting........................................11

2.7 Summary..............................................................................................................................21

Chapter 3: Research methodology.................................................................................................22

Table of Contents

Chapter 1: Introduction....................................................................................................................5

1.0 Overview................................................................................................................................5

1.1 Research aim..........................................................................................................................5

1.2 Research objectives...............................................................................................................6

1.3 Research questions.................................................................................................................6

1.4 Research scope.......................................................................................................................6

1.5 Structure of the dissertation...................................................................................................7

1.6 Summary................................................................................................................................7

Chapter 2: Literature review............................................................................................................8

2.0 Overview................................................................................................................................8

2.1 Professional accounting education........................................................................................8

2.2 Competencies achieved by studying professional accounting...............................................9

2.3 Demand of professional accounting jobs at global scale.....................................................10

2.4 Long-term intentions of pursuing professional accounting.................................................10

2.5 Career opportunities of studying professional accounting..................................................11

2.6 The various issues noticed in the field of Professional Accounting........................................11

2.7 Summary..............................................................................................................................21

Chapter 3: Research methodology.................................................................................................22

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4DISSERTATION

3.0 Research philosophy............................................................................................................22

3.1 Research approach...............................................................................................................22

3.2 Research design...................................................................................................................22

3.3 Research strategy.................................................................................................................23

3.4 Sampling technique and sample size...................................................................................23

3.5 Data collection process........................................................................................................24

3.6 Data analysis technique.......................................................................................................24

3.7 Ethical considerations..........................................................................................................24

Chapter 4: Data analysis and Findings..........................................................................................25

4.0 Overview..............................................................................................................................25

4.1 Data Findings.......................................................................................................................25

4.2 Summary..............................................................................................................................28

Chapter 5: Conclusion and Recommendation...............................................................................29

Future Scope of action...............................................................................................................31

References......................................................................................................................................32

Appendix:......................................................................................................................................35

3.0 Research philosophy............................................................................................................22

3.1 Research approach...............................................................................................................22

3.2 Research design...................................................................................................................22

3.3 Research strategy.................................................................................................................23

3.4 Sampling technique and sample size...................................................................................23

3.5 Data collection process........................................................................................................24

3.6 Data analysis technique.......................................................................................................24

3.7 Ethical considerations..........................................................................................................24

Chapter 4: Data analysis and Findings..........................................................................................25

4.0 Overview..............................................................................................................................25

4.1 Data Findings.......................................................................................................................25

4.2 Summary..............................................................................................................................28

Chapter 5: Conclusion and Recommendation...............................................................................29

Future Scope of action...............................................................................................................31

References......................................................................................................................................32

Appendix:......................................................................................................................................35

5DISSERTATION

Chapter 1: Introduction

1.0 Overview

The job sector has become highly competitive due to which the students need to enroll

themselves in courses those are highly specific. According to Wen et al. (2018), taking into

account the current job market, global universities are offering highly specific courses for

students from all over the world with the aim of developing competent candidates for jobs. One

such highly specific accounting course is Masters in Professional Accounting (MPA) that is

offered in Australia. Australia is one of the highly preferred destinations for higher studies and

students from all over the globe visit Australia for undertaking various courses with the long

term intention of securing a desired career in this highly competitive job market.

Masters in Professional Accounting is designed for the students those possess the long

term intention of obtaining specialized knowledge and research skills in accounting and related

areas of business. As a result, the students learn to implement advanced conceptual and practical

accounting knowledge for undertaking rewarding careers in accounting and related areas of

business. In addition to, the course also offers the direction for further specialized learning that

helps in applying coherent and advanced knowledge of accounting and business concepts for the

students of different cultural origin that includes India, China, Africa and Nepal (Duff 2016).

1.1 Research aim

The aim of the study is to determine what and why is the long term intention of four

different culture-origin students studying MPA (Masters in Professional Accounting) in

Australia. The four different cultures considered for this research are Nepal, India, China and

Africa.

Chapter 1: Introduction

1.0 Overview

The job sector has become highly competitive due to which the students need to enroll

themselves in courses those are highly specific. According to Wen et al. (2018), taking into

account the current job market, global universities are offering highly specific courses for

students from all over the world with the aim of developing competent candidates for jobs. One

such highly specific accounting course is Masters in Professional Accounting (MPA) that is

offered in Australia. Australia is one of the highly preferred destinations for higher studies and

students from all over the globe visit Australia for undertaking various courses with the long

term intention of securing a desired career in this highly competitive job market.

Masters in Professional Accounting is designed for the students those possess the long

term intention of obtaining specialized knowledge and research skills in accounting and related

areas of business. As a result, the students learn to implement advanced conceptual and practical

accounting knowledge for undertaking rewarding careers in accounting and related areas of

business. In addition to, the course also offers the direction for further specialized learning that

helps in applying coherent and advanced knowledge of accounting and business concepts for the

students of different cultural origin that includes India, China, Africa and Nepal (Duff 2016).

1.1 Research aim

The aim of the study is to determine what and why is the long term intention of four

different culture-origin students studying MPA (Masters in Professional Accounting) in

Australia. The four different cultures considered for this research are Nepal, India, China and

Africa.

6DISSERTATION

1.2 Research objectives

The objectives of the research are:

To understand the concept of professional accounting

To critically analyze the professional competencies achieved by studying MPA

To investigate the job prospects after completion of MPAat global platform

To determine the long term intentions for pursuing MPA

To suggest ways of accomplishing the intentions of studying MPA

1.3 Research questions

The questions of the research are:

What do you understand by professional accounting?

What are the professional competencies achieved by studying MPA?

What are the job prospects after completion of MPA at global platform?

What are the long term intentions for pursuing MPA?

What are the suitable ways of accomplishing the intentions of studying MPA?

1.4 Research scope

Completion of the research offers the scope of understanding the accounting job

prospects in Nepal, India, China and Africa as well as in international job platform. Studying the

long term intention of the students of different backgrounds helps in understanding the benefits

the course is offering to the students at international level. As a result, the research provides a

scope of understanding what the course has to offer for the students and how it tends to shape up

their future in the long run. Additionally, the research also provides an opportunity to

investigatehow completion of an MPA degree successfully in Australia will help in allowing the

1.2 Research objectives

The objectives of the research are:

To understand the concept of professional accounting

To critically analyze the professional competencies achieved by studying MPA

To investigate the job prospects after completion of MPAat global platform

To determine the long term intentions for pursuing MPA

To suggest ways of accomplishing the intentions of studying MPA

1.3 Research questions

The questions of the research are:

What do you understand by professional accounting?

What are the professional competencies achieved by studying MPA?

What are the job prospects after completion of MPA at global platform?

What are the long term intentions for pursuing MPA?

What are the suitable ways of accomplishing the intentions of studying MPA?

1.4 Research scope

Completion of the research offers the scope of understanding the accounting job

prospects in Nepal, India, China and Africa as well as in international job platform. Studying the

long term intention of the students of different backgrounds helps in understanding the benefits

the course is offering to the students at international level. As a result, the research provides a

scope of understanding what the course has to offer for the students and how it tends to shape up

their future in the long run. Additionally, the research also provides an opportunity to

investigatehow completion of an MPA degree successfully in Australia will help in allowing the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7DISSERTATION

students to take a career in accounting field by developing the necessary skills and expertise

required.

1.5 Structure of the dissertation

The overall dissertation is divided five major chapters that includethe introduction

chapter followed by literature review, research methodology, data analysis, conclusion and

recommendations.

1.6 Summary

Thus, in this chapter, it can be summarized that an overview of the research background

has been provided successful that helped in developing suitable research objectives, aim and

question that provides an opportunity to determine the long-term intention of four different

culture origin students studying MPA in Australia. Current accounting job prospects of India,

Nepal, Africa and China has been evaluated in order to justify the potential reasons of how and

why the students want to accomplish those goals.

students to take a career in accounting field by developing the necessary skills and expertise

required.

1.5 Structure of the dissertation

The overall dissertation is divided five major chapters that includethe introduction

chapter followed by literature review, research methodology, data analysis, conclusion and

recommendations.

1.6 Summary

Thus, in this chapter, it can be summarized that an overview of the research background

has been provided successful that helped in developing suitable research objectives, aim and

question that provides an opportunity to determine the long-term intention of four different

culture origin students studying MPA in Australia. Current accounting job prospects of India,

Nepal, Africa and China has been evaluated in order to justify the potential reasons of how and

why the students want to accomplish those goals.

8DISSERTATION

Chapter 2: Literature review

2.0 Overview

In this section, past researches is studied with the aim of understanding the concept of

professional accounting. This section compares and contrasts the views and opinions of different

authors in terms of professional accounting and the competencies it offers to the individuals

those intend to study the course. The long term intentions of the students for studying

professional accounting is analyzed by shedding light on the concept of the subject,

competencies it has to offer, the demands of professional accounting in the global job sector and

the methods that can be used for achieving the long-term intentions. Below mentioned

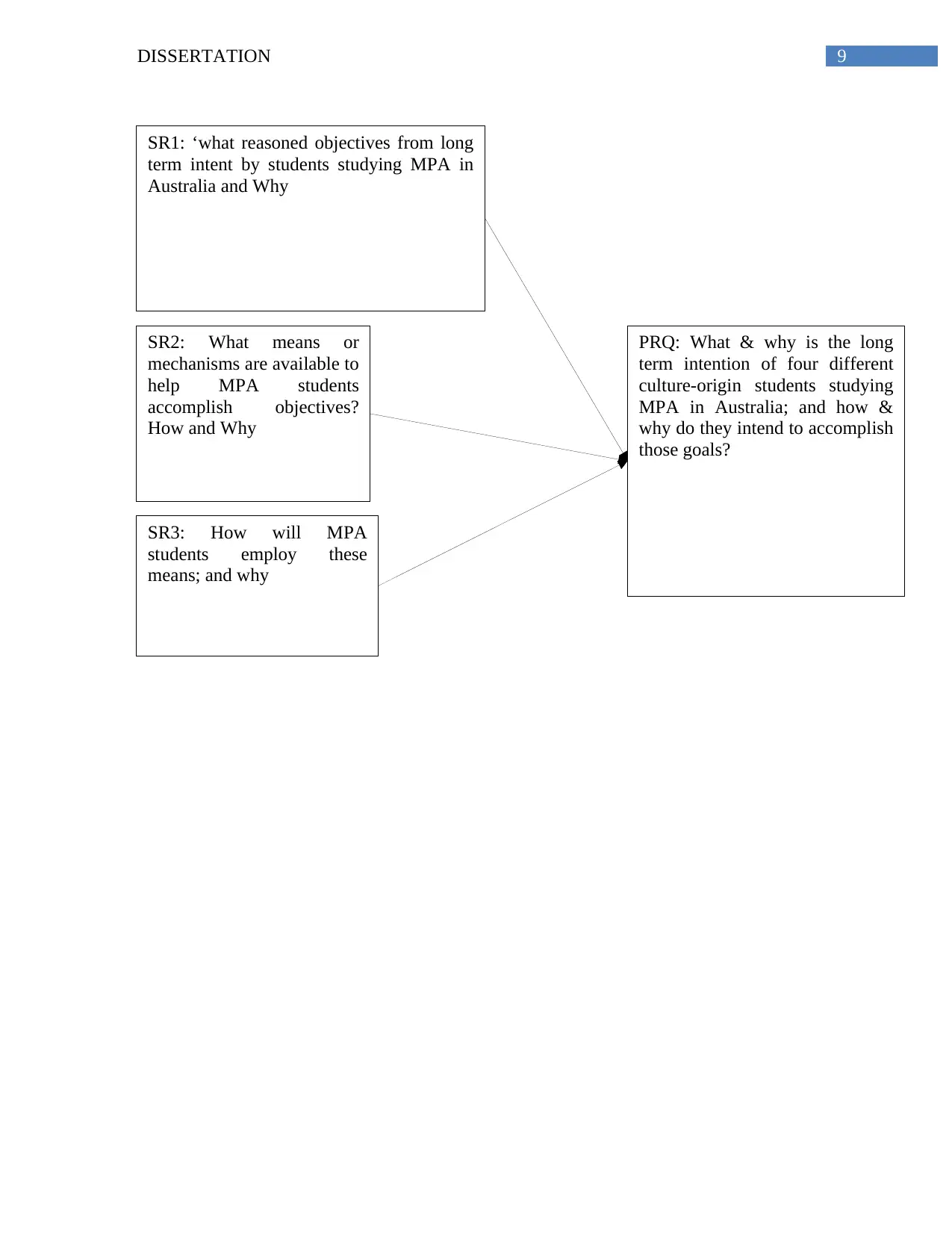

framework shows primary research question and secondary research question to evaluate the

extant literature. This framework identifies the key relationship of each factor identified in the

literature review.

Chapter 2: Literature review

2.0 Overview

In this section, past researches is studied with the aim of understanding the concept of

professional accounting. This section compares and contrasts the views and opinions of different

authors in terms of professional accounting and the competencies it offers to the individuals

those intend to study the course. The long term intentions of the students for studying

professional accounting is analyzed by shedding light on the concept of the subject,

competencies it has to offer, the demands of professional accounting in the global job sector and

the methods that can be used for achieving the long-term intentions. Below mentioned

framework shows primary research question and secondary research question to evaluate the

extant literature. This framework identifies the key relationship of each factor identified in the

literature review.

9DISSERTATION

SR1: ‘what reasoned objectives from long

term intent by students studying MPA in

Australia and Why

SR2: What means or

mechanisms are available to

help MPA students

accomplish objectives?

How and Why

SR3: How will MPA

students employ these

means; and why

PRQ: What & why is the long

term intention of four different

culture-origin students studying

MPA in Australia; and how &

why do they intend to accomplish

those goals?

SR1: ‘what reasoned objectives from long

term intent by students studying MPA in

Australia and Why

SR2: What means or

mechanisms are available to

help MPA students

accomplish objectives?

How and Why

SR3: How will MPA

students employ these

means; and why

PRQ: What & why is the long

term intention of four different

culture-origin students studying

MPA in Australia; and how &

why do they intend to accomplish

those goals?

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10DISSERTATION

2.1 Theme 1: Nature of Professional Accounting in Australia

SR1: what reasoned objectives from long term intent by students studying MPA in

Australia and Why

The idea gathered from this section highlights the long term intentions of the students of

four different cultures of Nepal, India, China and Africa to pursue the course of Masters in

Professional Accounting (MPA) in Australia. Undertaking this highly specific accounting course

allows the students to apply coherent and advanced knowledge of accounting and business and

strengthen the global economies. The students of four different cultures of Nepal, India, China

and Africa have long term intentions of pursuing MPA in Australia due to the various advantages

it has to offer to the individuals once they have the competencies. According to Daly et al.

(2015), having a professional accounting degree provides an opportunity for the individuals to

use their coherent and advanced knowledge of accounting and business concepts diversely. As a

result, the individuals develop the ability of solving problems, designs and making decisions

methodically that helps in identifying and proving innovative solutions to complex problems

with intellectual independence. However, as argued by Adapa, Rindfleish and Sheridan (2016),

the competence that individuals develop after having a professional accounting degree is the

ability to communicate proficiently in professional practice to a variety of audiences in

professional accountability. As a result, the individuals are able to gather deep awareness about

professional accounting practices. Therefore, the long term intentions of the students of four

different cultures of Nepal, India, China and Africa to pursue the course of Masters in

Professional Accounting (MPA) in Australia is to develop the competence to apply accounting

2.1 Theme 1: Nature of Professional Accounting in Australia

SR1: what reasoned objectives from long term intent by students studying MPA in

Australia and Why

The idea gathered from this section highlights the long term intentions of the students of

four different cultures of Nepal, India, China and Africa to pursue the course of Masters in

Professional Accounting (MPA) in Australia. Undertaking this highly specific accounting course

allows the students to apply coherent and advanced knowledge of accounting and business and

strengthen the global economies. The students of four different cultures of Nepal, India, China

and Africa have long term intentions of pursuing MPA in Australia due to the various advantages

it has to offer to the individuals once they have the competencies. According to Daly et al.

(2015), having a professional accounting degree provides an opportunity for the individuals to

use their coherent and advanced knowledge of accounting and business concepts diversely. As a

result, the individuals develop the ability of solving problems, designs and making decisions

methodically that helps in identifying and proving innovative solutions to complex problems

with intellectual independence. However, as argued by Adapa, Rindfleish and Sheridan (2016),

the competence that individuals develop after having a professional accounting degree is the

ability to communicate proficiently in professional practice to a variety of audiences in

professional accountability. As a result, the individuals are able to gather deep awareness about

professional accounting practices. Therefore, the long term intentions of the students of four

different cultures of Nepal, India, China and Africa to pursue the course of Masters in

Professional Accounting (MPA) in Australia is to develop the competence to apply accounting

11DISSERTATION

and business fundamentals for analyzing, designing and operating business models using suitable

accounting tools and methods.

However, in the opinion of Abayadeera and Watty (2014) it is believed that there exists a

significant gap between the expectation from the graduate students in their performance in the

accounting skills and their real life performance in the field. In this article, the data was gathered

with the help of survey and analyzed with non-parametric tests. It was founded out that the main

reason behind the existence of this gap was the low self-confidence of the professors of the

universities to teach the required subject to the students in an effective manner. The field of

professional accounting has undergone enormous changes in the recent times as a result of its

dynamic nature. The necessary skill set of the employees have also changed over the times to

suit the needs of the work place. In the opinion of Spence and Carter (2014), there is a need to

imbibe different logics within the framework of a hierarchical organization. The findings of the

article shows that habitus is important for the development of professional self-determination.In

other words, it can be noticed that often times there exists a gap in the required skills of the

professional accountants and in the skills that is possessed by such individuals. This makes it

quite difficult on the part of the different business organizations to ensure the effective working

of the business organizations as they have to recruit only those professional accounts who are

adept in their work. However, due to their unavailability this becomes a problematic on the part

of the different business organizations to choose from the available pool of professional

graduates.

According to Asonitou (2015), the activity of globalization and liberalization has brought

about many significant changes in the way the professional accountants perform their task. This

has also been impacted as a result of the technological advancements in the field. The field of

and business fundamentals for analyzing, designing and operating business models using suitable

accounting tools and methods.

However, in the opinion of Abayadeera and Watty (2014) it is believed that there exists a

significant gap between the expectation from the graduate students in their performance in the

accounting skills and their real life performance in the field. In this article, the data was gathered

with the help of survey and analyzed with non-parametric tests. It was founded out that the main

reason behind the existence of this gap was the low self-confidence of the professors of the

universities to teach the required subject to the students in an effective manner. The field of

professional accounting has undergone enormous changes in the recent times as a result of its

dynamic nature. The necessary skill set of the employees have also changed over the times to

suit the needs of the work place. In the opinion of Spence and Carter (2014), there is a need to

imbibe different logics within the framework of a hierarchical organization. The findings of the

article shows that habitus is important for the development of professional self-determination.In

other words, it can be noticed that often times there exists a gap in the required skills of the

professional accountants and in the skills that is possessed by such individuals. This makes it

quite difficult on the part of the different business organizations to ensure the effective working

of the business organizations as they have to recruit only those professional accounts who are

adept in their work. However, due to their unavailability this becomes a problematic on the part

of the different business organizations to choose from the available pool of professional

graduates.

According to Asonitou (2015), the activity of globalization and liberalization has brought

about many significant changes in the way the professional accountants perform their task. This

has also been impacted as a result of the technological advancements in the field. The field of

12DISSERTATION

professional accounting is quite challenging in itself. In the study conducted by Asonitou (2015),

the dimensions of the skill and the reforms brought about in this field have been talked about in a

detailed manner. Furthermore, the research study analyzes the various criticisms against the field

of accountancy, particularly in the Anglo-Saxon countries of the European continent.

According to Hayes, Freudenberg and Delaney (2018), most of the graduate students in

Australia are recruited in to the small and medium sized enterprises. Often times, people are of

the idea that a person working in the small and medium enterprises do not need any particular

skill set. However, in the article written by Hayes, Freudenberg and Delaney (2018), it is stated

that every single individual that is engaged with accountancy, require the similar skill set that is

needed for effectively executing their work.

Moreover, the need for every employee, no matter their place of work, is job satisfaction.

In the words of Sejjaaka and Kaawaase (2014), it is the system of rewards and recognition that

motivates the employees in a proper manner to work efficiently within their work place. This is

also true in respect of the professional accountants. The professional accountants have a lot of

work pressure due to which they are often stresses. In the event that they receive motivation in

the form of rewards, they would be able to work in a more efficient manner (Yap, Ryan and

Yong 2014).

According to Shan (2015), the establishment of neo-liberalism has introduced the concept

of entrepreneurial self. In this regard, almost every self-fulfilling individual wants to build a

career for him or herself so that they can achieve the recognition that they have always wanted.

In this respect, Shan (2015) analyzes the case study of a Chinese woman who had migrated to

Canada in search for an opportunity to further her career growth. In this respect, there is a need

professional accounting is quite challenging in itself. In the study conducted by Asonitou (2015),

the dimensions of the skill and the reforms brought about in this field have been talked about in a

detailed manner. Furthermore, the research study analyzes the various criticisms against the field

of accountancy, particularly in the Anglo-Saxon countries of the European continent.

According to Hayes, Freudenberg and Delaney (2018), most of the graduate students in

Australia are recruited in to the small and medium sized enterprises. Often times, people are of

the idea that a person working in the small and medium enterprises do not need any particular

skill set. However, in the article written by Hayes, Freudenberg and Delaney (2018), it is stated

that every single individual that is engaged with accountancy, require the similar skill set that is

needed for effectively executing their work.

Moreover, the need for every employee, no matter their place of work, is job satisfaction.

In the words of Sejjaaka and Kaawaase (2014), it is the system of rewards and recognition that

motivates the employees in a proper manner to work efficiently within their work place. This is

also true in respect of the professional accountants. The professional accountants have a lot of

work pressure due to which they are often stresses. In the event that they receive motivation in

the form of rewards, they would be able to work in a more efficient manner (Yap, Ryan and

Yong 2014).

According to Shan (2015), the establishment of neo-liberalism has introduced the concept

of entrepreneurial self. In this regard, almost every self-fulfilling individual wants to build a

career for him or herself so that they can achieve the recognition that they have always wanted.

In this respect, Shan (2015) analyzes the case study of a Chinese woman who had migrated to

Canada in search for an opportunity to further her career growth. In this respect, there is a need

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13DISSERTATION

for certified accountants in this age of globalization and liberalization. According to Ramadhan

(2015), it can be observed that the demands of the consumer market have increased to a

considerable extent which necessitates the increase in the number of certified accountants who

are available within the labor work force. A study was conducted in the region of Bahrain where

it was found that a group of eighty respondents affirmed that there would be a rise in the demand

for forensic accountants in the future. As a result, there is a need on the part of the students all

across the world to train them in professional accounting so that they can better serve the needs

of the society (Jackling and Natoli 2015).

According to Kraten (2014), the multinational company of the United States of America

has invested in a lot of projects all around the world, such as the energy sector and the generation

of the hydroelectric power. However, most of the times it is observed that such projects poses a

serious problem to the environment in the sense that it negatively impacts the health of the

people through the generation of many pollutants. In this context, the professional accountants

have a major role to play in the sense that they can keep a track of the health of the environment

and warn the state leaders in the event that it reaches a serious level. The impact of globalization

became effective in the global market from the latter half of the twentieth century. In this respect,

in the words of Pacter (2014), the field of professional accounting gained significance in several

countries of the world such as that of the United States of America. To better manage the

accounting standards in the globe, the International Accounting Standards Committee was

established which sought to provide a basic standard for the presentation of the financial annual

statements of any organizations.The aim of the study is to determine what and why is the long

term intention of four different culture-origin students studying MPA (Masters in Professional

Accounting) in Australia. The four different cultures considered for this research are Nepal,

for certified accountants in this age of globalization and liberalization. According to Ramadhan

(2015), it can be observed that the demands of the consumer market have increased to a

considerable extent which necessitates the increase in the number of certified accountants who

are available within the labor work force. A study was conducted in the region of Bahrain where

it was found that a group of eighty respondents affirmed that there would be a rise in the demand

for forensic accountants in the future. As a result, there is a need on the part of the students all

across the world to train them in professional accounting so that they can better serve the needs

of the society (Jackling and Natoli 2015).

According to Kraten (2014), the multinational company of the United States of America

has invested in a lot of projects all around the world, such as the energy sector and the generation

of the hydroelectric power. However, most of the times it is observed that such projects poses a

serious problem to the environment in the sense that it negatively impacts the health of the

people through the generation of many pollutants. In this context, the professional accountants

have a major role to play in the sense that they can keep a track of the health of the environment

and warn the state leaders in the event that it reaches a serious level. The impact of globalization

became effective in the global market from the latter half of the twentieth century. In this respect,

in the words of Pacter (2014), the field of professional accounting gained significance in several

countries of the world such as that of the United States of America. To better manage the

accounting standards in the globe, the International Accounting Standards Committee was

established which sought to provide a basic standard for the presentation of the financial annual

statements of any organizations.The aim of the study is to determine what and why is the long

term intention of four different culture-origin students studying MPA (Masters in Professional

Accounting) in Australia. The four different cultures considered for this research are Nepal,

14DISSERTATION

India, China and Africa. As a result, this section helps in the understanding of how the field came

in to existence and its spread to the different corners of the world. This will help to understand

the role played by the different cultures in the spread of the subject of professional accounting in

the different parts of the world.

According to Stoner and Milner (2010), there is a need of certain skills on the part of the

accounting graduates which determines if they can be employed or not. These are known as

employability skills. The research under study aimed to provide a broad list of such skills which

are needed for building a bright future in business management. According to the authors, there

are three skills which are most essential, such as those of time management, learning to learn and

that of modeling. As a result, an educator of accounting needs to emphasis on the development of

these skills. According to Sin, Jones and Wang (2015), there is a need for critical thinking among

the field of professional accounting. Professional accounting involves the activities of complex

mathematical calculations and thinking in an analytical manner in order to make sense of the

data that is presented in front of the individual. Moreover, a professional accountant is required

to provide an objective analysis of the data which requires them to be critical in their approach

(Carnegie and O’Connell 2014). The beliefs and the opinions held by the different individuals

have a significant impact on their career decision. According to Samsuri, Arifin and Hussin

(2016), the decision regarding their career is significant as this aids in the further development of

their future prospects. In the field of professional accounting within the context of Malaysia, it is

found out that there are relatively less number of students who are desirous to pursue the field of

professional accounting while the rest are more interested in non-accounting jobs.

India, China and Africa. As a result, this section helps in the understanding of how the field came

in to existence and its spread to the different corners of the world. This will help to understand

the role played by the different cultures in the spread of the subject of professional accounting in

the different parts of the world.

According to Stoner and Milner (2010), there is a need of certain skills on the part of the

accounting graduates which determines if they can be employed or not. These are known as

employability skills. The research under study aimed to provide a broad list of such skills which

are needed for building a bright future in business management. According to the authors, there

are three skills which are most essential, such as those of time management, learning to learn and

that of modeling. As a result, an educator of accounting needs to emphasis on the development of

these skills. According to Sin, Jones and Wang (2015), there is a need for critical thinking among

the field of professional accounting. Professional accounting involves the activities of complex

mathematical calculations and thinking in an analytical manner in order to make sense of the

data that is presented in front of the individual. Moreover, a professional accountant is required

to provide an objective analysis of the data which requires them to be critical in their approach

(Carnegie and O’Connell 2014). The beliefs and the opinions held by the different individuals

have a significant impact on their career decision. According to Samsuri, Arifin and Hussin

(2016), the decision regarding their career is significant as this aids in the further development of

their future prospects. In the field of professional accounting within the context of Malaysia, it is

found out that there are relatively less number of students who are desirous to pursue the field of

professional accounting while the rest are more interested in non-accounting jobs.

15DISSERTATION

Professional accounting is a field of study which requires careful analysis of the content

related to the business sector. Every firm has a particular financial sector which needs to be

looked after. It is the finances of the firms which are deemed to be the most important

component of its functioning as without the necessary financial resources, there cannot be

effective functioning of the said business organization. It falls under the purview of the

professional accountants to ensure that there is no discrepancy made on the issue of such

finances that belongs to the business organizations. In this manner, this section aims to

understand the nature of professional accounting and what it seeks to do in the field of business

organizations and private sector.The aim of the study is to determine what and why is the long

term intention of four different culture-origin students studying MPA (Masters in Professional

Accounting) in Australia. The four different cultures considered for this research are Nepal,

India, China and Africa. As a result, this section helps in the understanding of how the field came

in to existence and its spread to the different corners of the world.

The academics of accounting is perceived to be severely challenging in nature. According

to Samkin and Schneider (2014), this course has increased in its scope in the different parts of

the world such as in Hong Kong, the United Kingdom and Australia among other countries of

the world. In the paper, the authors have opined that in spite of the challenges and obstacles

present in the course of professional accounting, the need for this subject is only increasing in the

recent times (Utami, Priantara and Manshur 2017). As a result, the future of professional

accounting will be a ‘fertile area’ in the future. This is important to understand because many of

the people are of the view that the field has nothing concrete to give. It is often believed that

professional accounting is an extremely difficult field due to its nature of logical reasoning and

Professional accounting is a field of study which requires careful analysis of the content

related to the business sector. Every firm has a particular financial sector which needs to be

looked after. It is the finances of the firms which are deemed to be the most important

component of its functioning as without the necessary financial resources, there cannot be

effective functioning of the said business organization. It falls under the purview of the

professional accountants to ensure that there is no discrepancy made on the issue of such

finances that belongs to the business organizations. In this manner, this section aims to

understand the nature of professional accounting and what it seeks to do in the field of business

organizations and private sector.The aim of the study is to determine what and why is the long

term intention of four different culture-origin students studying MPA (Masters in Professional

Accounting) in Australia. The four different cultures considered for this research are Nepal,

India, China and Africa. As a result, this section helps in the understanding of how the field came

in to existence and its spread to the different corners of the world.

The academics of accounting is perceived to be severely challenging in nature. According

to Samkin and Schneider (2014), this course has increased in its scope in the different parts of

the world such as in Hong Kong, the United Kingdom and Australia among other countries of

the world. In the paper, the authors have opined that in spite of the challenges and obstacles

present in the course of professional accounting, the need for this subject is only increasing in the

recent times (Utami, Priantara and Manshur 2017). As a result, the future of professional

accounting will be a ‘fertile area’ in the future. This is important to understand because many of

the people are of the view that the field has nothing concrete to give. It is often believed that

professional accounting is an extremely difficult field due to its nature of logical reasoning and

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16DISSERTATION

other calculations which are involved in this field of professional accounting. However, in the

words of Utami, Priantara and Manshur(2017), it can be observed that the importance of this

sector is only increasing in the recent times. This is due to the fact that the field is very lucrative

in nature. Due to the fact that there is a lot of difficulty in this particular field, the expenses paid

to the professional accountant is quite high.

According to Bromwich and Scapens (2016) the subject of management accounting

research was founded in the year of 1990. As a result, it can be noted that the subject is relatively

new in this field of study. Due to its newness, there are a lot of research yet left to be done in this

field. As a result, the authors are of the opinion that various other research studies which are

related to this field, should be carried out by different researchers. They should then compare the

findings with one another so that a concrete conclusion can be reached with respect to the

domain of management accounting research. According to Ahmad, Khan and Ahmad (2018), the

field of commerce has a long historical significance. Since the ancient times, the establishment of

the commercial institutions can be observed which were involved in the activities of finances and

monetary activities. This required the helpof different people who would manage such financial

services which led to the inception of the concept of professional accounting. In the region of

Pakistan, the education in commerce started in the year of 1991 as the educators were convinced

of the importance and significance of professional accounting as a subject to be learned. The

article written by Sokolo (2015) discusses about the historical context of the public accounting

movement in the region of St. Petersburg in Russia. The strength of this article lies in the fact

that it takes in to consideration the various working of the professional institutions and their

significant contribution that aided in the development of this subject as an academic subject. In

the context of Russia, it can be observed that there is no prevalence of any group accounting

other calculations which are involved in this field of professional accounting. However, in the

words of Utami, Priantara and Manshur(2017), it can be observed that the importance of this

sector is only increasing in the recent times. This is due to the fact that the field is very lucrative

in nature. Due to the fact that there is a lot of difficulty in this particular field, the expenses paid

to the professional accountant is quite high.

According to Bromwich and Scapens (2016) the subject of management accounting

research was founded in the year of 1990. As a result, it can be noted that the subject is relatively

new in this field of study. Due to its newness, there are a lot of research yet left to be done in this

field. As a result, the authors are of the opinion that various other research studies which are

related to this field, should be carried out by different researchers. They should then compare the

findings with one another so that a concrete conclusion can be reached with respect to the

domain of management accounting research. According to Ahmad, Khan and Ahmad (2018), the

field of commerce has a long historical significance. Since the ancient times, the establishment of

the commercial institutions can be observed which were involved in the activities of finances and

monetary activities. This required the helpof different people who would manage such financial

services which led to the inception of the concept of professional accounting. In the region of

Pakistan, the education in commerce started in the year of 1991 as the educators were convinced

of the importance and significance of professional accounting as a subject to be learned. The

article written by Sokolo (2015) discusses about the historical context of the public accounting

movement in the region of St. Petersburg in Russia. The strength of this article lies in the fact

that it takes in to consideration the various working of the professional institutions and their

significant contribution that aided in the development of this subject as an academic subject. In

the context of Russia, it can be observed that there is no prevalence of any group accounting

17DISSERTATION

group as a professional group. All the different groups that has been formed are usually of the

character of interest group.This section helps to understand how the field of professional

accounting came to in to being. Moreover, from here, it is observed that the stream is a relatively

new field of study and therefore, has a lot of scope hidden in it for further future developments.

In this regard, it is important to understand the working of the various organizations that

aids in the development of the field of professional accounting.The intention of the International

Federation of Accountants (IFAC) is to strengthen the accountancy profession at a global

platform that intends to help the public interest and contribute towards the development of

international economies. As commented by Utami, Priantara and Manshur (2017), the content of

professional accounting consists of accounting, finance related knowledge, organizational and

business knowledge and information technology competencies and knowledge. However, as

argued by Tucker and Schaltegger (2016), the concept of professional accounting highlights the

ability to obtain research skills and knowledge in accounting and related business areas. As a

result, the individuals having a professional accounting degree possess the ability to use critical

thinking in diverse and different business concepts. In this regard, it can be seen that there is a

need on the part of the various lecturers and the professionals to make the subject easier on the

part of the individuals. The aim of the study is to determine what and why is the long term

intention of four different culture-origin students studying MPA (Masters in Professional

Accounting) in Australia. The four different cultures considered for this research are Nepal,

India, China and Africa. As a result, this section helps in the understanding of how the field can

be developed in an effective manner by the teachers and the professors.

group as a professional group. All the different groups that has been formed are usually of the

character of interest group.This section helps to understand how the field of professional

accounting came to in to being. Moreover, from here, it is observed that the stream is a relatively

new field of study and therefore, has a lot of scope hidden in it for further future developments.

In this regard, it is important to understand the working of the various organizations that

aids in the development of the field of professional accounting.The intention of the International

Federation of Accountants (IFAC) is to strengthen the accountancy profession at a global

platform that intends to help the public interest and contribute towards the development of

international economies. As commented by Utami, Priantara and Manshur (2017), the content of

professional accounting consists of accounting, finance related knowledge, organizational and

business knowledge and information technology competencies and knowledge. However, as

argued by Tucker and Schaltegger (2016), the concept of professional accounting highlights the

ability to obtain research skills and knowledge in accounting and related business areas. As a

result, the individuals having a professional accounting degree possess the ability to use critical

thinking in diverse and different business concepts. In this regard, it can be seen that there is a

need on the part of the various lecturers and the professionals to make the subject easier on the

part of the individuals. The aim of the study is to determine what and why is the long term

intention of four different culture-origin students studying MPA (Masters in Professional

Accounting) in Australia. The four different cultures considered for this research are Nepal,

India, China and Africa. As a result, this section helps in the understanding of how the field can

be developed in an effective manner by the teachers and the professors.

18DISSERTATION

2.2 Theme 2: Ethics and mechanisms available in Professional Accounting

SR2: What means or mechanisms are available to help MPA students accomplish

objectives?

Having a professional accounting degree is highly demanded and acknowledged in

today’s job sector. As mentioned by Yap, Ryan and Yong (2014), the graduates with

professional accounting degree are able to gain professional recognition and fill up the shortage

of professionally recognized accountants at the global platform. Professional accounting degree

is highly demanded in global job scale because this provides an opportunity for the students to

obtain specialized knowledge and research skills in accounting and related areas in business. As

a result, the students, in the global job platform are able to apply practical and technical

accounting knowledge and undertake rewarding careers in accounting field. However, as

criticized by Jackling and Natoli (2015), having professional accounting degree at global job

platform is preferred because the course provides an opportunity to develop accounting skills and

knowledge in the backdrop of fast and complex growing discipline of finance and accounting.

Therefore, the long term intentions of the students of four different cultures of Nepal, India,

China and Africa to pursue the course of Masters in Professional Accounting (MPA) in Australia

is to develop their academic qualifications and securing high pay job.

There is a large in flow of cash and financial resources within any private organization,

This gives rise to the aspect of fraud and fraudulent activities within such organizations.

According to Seda and Kramer (2014), in the recent period of globalization, the activities of

fraud have increased to a considerable extent within the capitalist market. This necessitates the

need for several professional accountants who have specialized knowledge on how to tackle the

2.2 Theme 2: Ethics and mechanisms available in Professional Accounting

SR2: What means or mechanisms are available to help MPA students accomplish

objectives?

Having a professional accounting degree is highly demanded and acknowledged in

today’s job sector. As mentioned by Yap, Ryan and Yong (2014), the graduates with

professional accounting degree are able to gain professional recognition and fill up the shortage

of professionally recognized accountants at the global platform. Professional accounting degree

is highly demanded in global job scale because this provides an opportunity for the students to

obtain specialized knowledge and research skills in accounting and related areas in business. As

a result, the students, in the global job platform are able to apply practical and technical

accounting knowledge and undertake rewarding careers in accounting field. However, as

criticized by Jackling and Natoli (2015), having professional accounting degree at global job

platform is preferred because the course provides an opportunity to develop accounting skills and

knowledge in the backdrop of fast and complex growing discipline of finance and accounting.

Therefore, the long term intentions of the students of four different cultures of Nepal, India,

China and Africa to pursue the course of Masters in Professional Accounting (MPA) in Australia

is to develop their academic qualifications and securing high pay job.

There is a large in flow of cash and financial resources within any private organization,

This gives rise to the aspect of fraud and fraudulent activities within such organizations.

According to Seda and Kramer (2014), in the recent period of globalization, the activities of

fraud have increased to a considerable extent within the capitalist market. This necessitates the

need for several professional accountants who have specialized knowledge on how to tackle the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19DISSERTATION

issue of fraud and prevent the occurrence of such activities within the firm (Adapa, Rindfleish

and Sheridan 2016).

The aspect of whistle blowing has gained a considerable significance I the recent world.

According to Suryanto (2017), whistle blowing is in existence among the Javanese tribe in

Indonesia. In his article, he has tried to relate religion with accounting by opining that it is quite

difficult to perform the accounting activity for a Muslim country without making adjustments for

the ethics of governance and its responsibility. The findings of the article shows that majority of

the Javanese tribal people are not interested to become whistle blowers. It is the responsibility of

the policy makers to encourage whistle blowing. In the opinion of Everett and Tremblay (2014),

there is a link between the aspect of ethics and that of internal audit. In order to carry out an

effective research, the authors conducted an interview with some of the prominent members in

the field of accountings like that of Cynthia Cooper who was the ex-Vice President of Internal

Audit of World Com. The different documents were analyzed in order to understand the concept

of ethics in a better manner. According to the authors, there is a concerning issue with regards to

the adherence to the moralistic principles within any organization.

The field of professional activity is often seen to be one where there is minimal existence

of ethics and moral ideas. In the words of Brennan (2016), it is believed that there exists some

amount of ethics within the practice of professional accounting. It is this idea which separates the

practitioners from the professional accountants. As a consequence, this article helps to determine

what and why is the long term intention of four different culture-origin students studying MPA

(Masters in Professional Accounting) in Australia.

issue of fraud and prevent the occurrence of such activities within the firm (Adapa, Rindfleish

and Sheridan 2016).

The aspect of whistle blowing has gained a considerable significance I the recent world.

According to Suryanto (2017), whistle blowing is in existence among the Javanese tribe in

Indonesia. In his article, he has tried to relate religion with accounting by opining that it is quite

difficult to perform the accounting activity for a Muslim country without making adjustments for

the ethics of governance and its responsibility. The findings of the article shows that majority of

the Javanese tribal people are not interested to become whistle blowers. It is the responsibility of

the policy makers to encourage whistle blowing. In the opinion of Everett and Tremblay (2014),

there is a link between the aspect of ethics and that of internal audit. In order to carry out an

effective research, the authors conducted an interview with some of the prominent members in

the field of accountings like that of Cynthia Cooper who was the ex-Vice President of Internal

Audit of World Com. The different documents were analyzed in order to understand the concept

of ethics in a better manner. According to the authors, there is a concerning issue with regards to

the adherence to the moralistic principles within any organization.

The field of professional activity is often seen to be one where there is minimal existence

of ethics and moral ideas. In the words of Brennan (2016), it is believed that there exists some

amount of ethics within the practice of professional accounting. It is this idea which separates the

practitioners from the professional accountants. As a consequence, this article helps to determine

what and why is the long term intention of four different culture-origin students studying MPA

(Masters in Professional Accounting) in Australia.

20DISSERTATION

According to Chalu and Kessy (2015), for improving the governance sector of any

country, it is necessary to improve upon the financial management of the said country or region.

The article takes the case study of Tanzania. According to the author, the strengthening of of the

governance of any region requires the careful consideration of the aspects of budgeting and

accountability. The study tries to prove that in order to install a system of good governance, it is

essential to install a new designed accounting information system which includes certain

components of good governance. According to Sithole (2015), there is an expectant skill desired

from the employees by any private organization. This expectancy flows from the starting point of

induction of the employees when the organization makes an assumption of their level of skill. In

the survey conducted by Sithole (2015), around thirty five employees were surveyed. It revealed

that the employers are desirous of the reading skill of the employees, their researching skill and

their ability to handle technology in an efficient manner. In the field of professional accounting,

such characteristics are intrinsic in nature and an employee can only function properly when he

or she has all the necessary qualities.

Ethics is one of the most important requirement for the functioning of any business

organization. This is due to the fact that in the contemporary world of today, the capitalist nature

of marketing is followed. In this system, there is very less adherence to the aspect of ethics and

morality. Rather, the different business organizations are only concerned with the attainment of a

high profit level. In this manner, there is often the overlooking of the ethics that s needed on the

part of such business firms. In this regard, it has been made essential and obligatory on the part

of the different business organizations to ensure that they adhere to the ethical considerations.

The aim of the study is to determine what and why is the long term intention of four different

culture-origin students studying MPA (Masters in Professional Accounting) in Australia. The

According to Chalu and Kessy (2015), for improving the governance sector of any

country, it is necessary to improve upon the financial management of the said country or region.

The article takes the case study of Tanzania. According to the author, the strengthening of of the

governance of any region requires the careful consideration of the aspects of budgeting and

accountability. The study tries to prove that in order to install a system of good governance, it is

essential to install a new designed accounting information system which includes certain

components of good governance. According to Sithole (2015), there is an expectant skill desired

from the employees by any private organization. This expectancy flows from the starting point of

induction of the employees when the organization makes an assumption of their level of skill. In

the survey conducted by Sithole (2015), around thirty five employees were surveyed. It revealed

that the employers are desirous of the reading skill of the employees, their researching skill and

their ability to handle technology in an efficient manner. In the field of professional accounting,

such characteristics are intrinsic in nature and an employee can only function properly when he

or she has all the necessary qualities.

Ethics is one of the most important requirement for the functioning of any business

organization. This is due to the fact that in the contemporary world of today, the capitalist nature

of marketing is followed. In this system, there is very less adherence to the aspect of ethics and

morality. Rather, the different business organizations are only concerned with the attainment of a

high profit level. In this manner, there is often the overlooking of the ethics that s needed on the

part of such business firms. In this regard, it has been made essential and obligatory on the part

of the different business organizations to ensure that they adhere to the ethical considerations.

The aim of the study is to determine what and why is the long term intention of four different

culture-origin students studying MPA (Masters in Professional Accounting) in Australia. The

21DISSERTATION

four different cultures considered for this research are Nepal, India, China and Africa. As a

result, this section helps in the understanding of how the field came in to existence and its spread

to the different corners of the world. In this manner, their role in the spreading and adhering to

the different factors of ethics is observed in this particular section.

In this manner, it has been observed that ethics can only be imbibed by an individual

during the process of learning. According to Almaan, Grosu and Circa (2015), there has been a

continuous debate on the inter relationship between the factors of research, teaching and practice

in the field of professional counting. It is believed that there exists a considerable gap between

the two factors of research and practice. In order to bridge this gap in an effective manner, there

is a need on the part of the individual to communicate the problem. This can be done with the aid

of teaching professional accounting. In the words of Kavanagh and Drennan (2008), the last

decade has been quite a challenging decade for the world. This is due to the fact that the various

private organizations all around the globe faced issues of technological changes which required

the employees and the employers both to be well-versed in it. This required immediate action by

the managers who needed to employ professional accountants who knew about such

technological changes (Blackmore, Gribble and Rahimi 2017).

2.3 Theme 3: Professional accounting and gender roles

SR3: How will MPA students employ these means; and why

In this section, the secondary research question has been considered with the help of

gender role in Australia. This section explores the gap related to gender role played by two

different genders in the field of professional accounting. This theme is related to the technique

which MPA students will employ in order achieve the goal.

four different cultures considered for this research are Nepal, India, China and Africa. As a

result, this section helps in the understanding of how the field came in to existence and its spread

to the different corners of the world. In this manner, their role in the spreading and adhering to

the different factors of ethics is observed in this particular section.

In this manner, it has been observed that ethics can only be imbibed by an individual

during the process of learning. According to Almaan, Grosu and Circa (2015), there has been a

continuous debate on the inter relationship between the factors of research, teaching and practice

in the field of professional counting. It is believed that there exists a considerable gap between

the two factors of research and practice. In order to bridge this gap in an effective manner, there

is a need on the part of the individual to communicate the problem. This can be done with the aid

of teaching professional accounting. In the words of Kavanagh and Drennan (2008), the last

decade has been quite a challenging decade for the world. This is due to the fact that the various

private organizations all around the globe faced issues of technological changes which required

the employees and the employers both to be well-versed in it. This required immediate action by

the managers who needed to employ professional accountants who knew about such

technological changes (Blackmore, Gribble and Rahimi 2017).

2.3 Theme 3: Professional accounting and gender roles

SR3: How will MPA students employ these means; and why

In this section, the secondary research question has been considered with the help of

gender role in Australia. This section explores the gap related to gender role played by two

different genders in the field of professional accounting. This theme is related to the technique