Stock Price Simulation and Option Pricing

Comment on whether the chosen specification captures FX dynamics properly.

7 Pages1286 Words142 Views

Added on 2023-04-23

About This Document

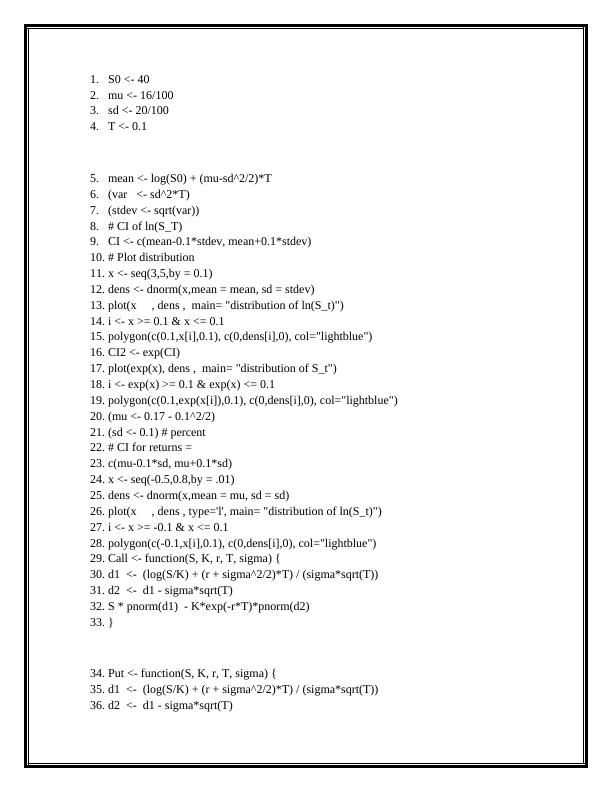

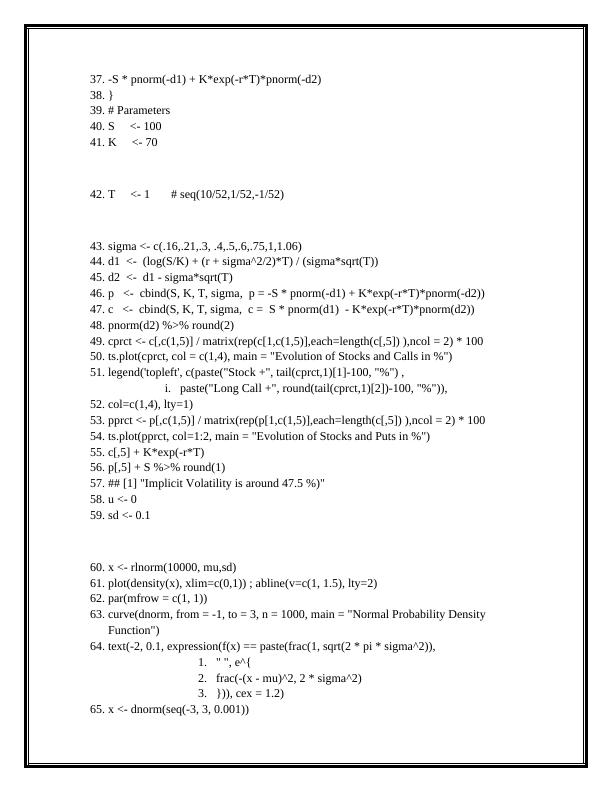

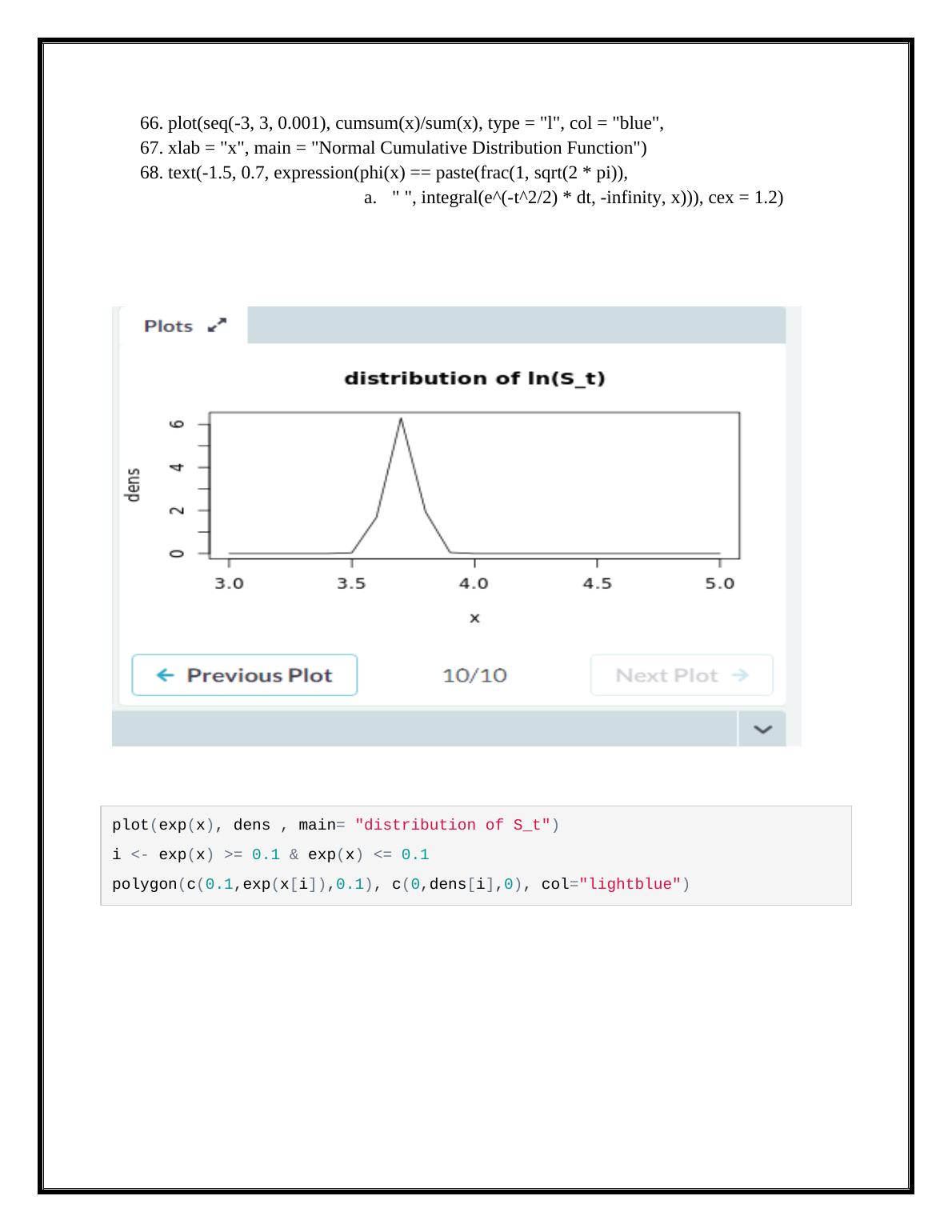

This code simulates stock price and calculates option prices using Black-Scholes model. It also plots the distribution of stock prices and option prices.

Stock Price Simulation and Option Pricing

Comment on whether the chosen specification captures FX dynamics properly.

Added on 2023-04-23

ShareRelated Documents

End of preview

Want to access all the pages? Upload your documents or become a member.