Final Research Proposal: Dividend Policy & Firm Performance in Nepal

VerifiedAdded on 2021/01/15

|16

|4100

|350

Project

AI Summary

This research proposal investigates the impact of dividend policy on the financial performance of Nepalese commercial banks listed on the Nepal Stock Exchange (NEPSE). The study aims to analyze the relationship between dividend policies and firm performance, focusing on Return on Assets (ROA), Earnings Per Share (EPS), and Return on Capital Employed. The proposal includes a comprehensive literature review covering agency theory, signaling theory, the bird-in-the-hand theory, residual theory, and empirical studies. It outlines the research questions, methodology involving quantitative techniques, and potential limitations. The research seeks to determine the factors affecting firm performance and their implications, contributing to a better understanding of how dividend decisions influence the financial success of commercial banks in Nepal. The proposal also includes a conceptual framework and a time schedule for the research.

FINAL RESEARCH PROPOSAL ON IMPACT OF

DIVIDEND POLICY ON FIRM PERFORMANCE IN

NEPALESE COMMERCIAL BANK

DIVIDEND POLICY ON FIRM PERFORMANCE IN

NEPALESE COMMERCIAL BANK

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

TITLE..............................................................................................................................................1

INTRODUCTION...........................................................................................................................1

I. Overview of the Research...................................................................................................1

II. Background of Research....................................................................................................1

III. Significance of Research..................................................................................................1

PROJECT OBJECTIVE..................................................................................................................2

PROJECT SCOPE...........................................................................................................................2

LITERATURE REVIEW................................................................................................................2

I. Impact of dividend policy on corporate performance.........................................................2

II. Conceptual Framework......................................................................................................3

III. Factors affecting financial performance of a firm............................................................4

IV. Empirical Studies.............................................................................................................5

V. Legal Provision regarding Dividend practice in Nepal.....................................................6

VI. Literature Gap..................................................................................................................6

RESEARCH QUESTIONS.............................................................................................................7

RESEARCH DESIGN AND METHODOLODGY........................................................................7

RESEARCH LIMITATIONS..........................................................................................................7

TIME SCHEDULE..........................................................................................................................8

CONCLUSION................................................................................................................................9

REFERENCE LIST.......................................................................................................................10

APPENDIX....................................................................................................................................12

TITLE..............................................................................................................................................1

INTRODUCTION...........................................................................................................................1

I. Overview of the Research...................................................................................................1

II. Background of Research....................................................................................................1

III. Significance of Research..................................................................................................1

PROJECT OBJECTIVE..................................................................................................................2

PROJECT SCOPE...........................................................................................................................2

LITERATURE REVIEW................................................................................................................2

I. Impact of dividend policy on corporate performance.........................................................2

II. Conceptual Framework......................................................................................................3

III. Factors affecting financial performance of a firm............................................................4

IV. Empirical Studies.............................................................................................................5

V. Legal Provision regarding Dividend practice in Nepal.....................................................6

VI. Literature Gap..................................................................................................................6

RESEARCH QUESTIONS.............................................................................................................7

RESEARCH DESIGN AND METHODOLODGY........................................................................7

RESEARCH LIMITATIONS..........................................................................................................7

TIME SCHEDULE..........................................................................................................................8

CONCLUSION................................................................................................................................9

REFERENCE LIST.......................................................................................................................10

APPENDIX....................................................................................................................................12

TITLE

“Impact of dividend policy on firm performance in Nepalese Commercial Bank”

INTRODUCTION

.I Overview of the Research

A commercial bank is a financial institution that offers services to promote trade and

industry in the country. It performs functions such as accepting deposits, aid loans, provide

agency services to individuals as well as companies, transfer of funds, capital issue and mobility

(Commercial Bank Act, 2031). Similar to a company, a commercial bank also earns profits and

records losses. These banks provide returns to their investors in form of dividends and reinvest

the surplus for operational efficiencies.

.II Background of Research

An organization operates with an objective of wealth maximization which is governed by

various policies and procedures formulated by management internally. One such policy is of

dividends that enlists in what proportion and procedures would a business distribute its surplus

earnings to its stakeholders. A good dividend policy may make or break a business. For instance,

if an organisation has a lenient dividend policy it may face working capital deficiencies. On the

other hand, if the organisation is frugal in distributing its profits, the investors may lose interest

in the business. However, in both cases, the ultimate effect is observed on the firm's

performance. In order to analyse this concept at length, this report has selected to study the

impact of dividend policy on performance of Nepalese Commercial Banks listed in NEPSE for

different financial periods.

.III Significance of Research

The given research work focuses on the analysis of firm performance in relation to the

dividend policy followed by Nepalese commercial banks listed on NEPSE. Dividends refer to a

portion of earnings that are distributed to the shareholders of a business as per their holdings or

ownership. They are a type of benefit to shareholders in return of risk taken by them. Dividend

policy guides a business to allocate these benefits among its shareholders fairly by taking into

consideration all other variables such as working capital requirements and payment of debts.

Thus, if there is a change in dividend policy it would show in the bank's performance too. This

1

“Impact of dividend policy on firm performance in Nepalese Commercial Bank”

INTRODUCTION

.I Overview of the Research

A commercial bank is a financial institution that offers services to promote trade and

industry in the country. It performs functions such as accepting deposits, aid loans, provide

agency services to individuals as well as companies, transfer of funds, capital issue and mobility

(Commercial Bank Act, 2031). Similar to a company, a commercial bank also earns profits and

records losses. These banks provide returns to their investors in form of dividends and reinvest

the surplus for operational efficiencies.

.II Background of Research

An organization operates with an objective of wealth maximization which is governed by

various policies and procedures formulated by management internally. One such policy is of

dividends that enlists in what proportion and procedures would a business distribute its surplus

earnings to its stakeholders. A good dividend policy may make or break a business. For instance,

if an organisation has a lenient dividend policy it may face working capital deficiencies. On the

other hand, if the organisation is frugal in distributing its profits, the investors may lose interest

in the business. However, in both cases, the ultimate effect is observed on the firm's

performance. In order to analyse this concept at length, this report has selected to study the

impact of dividend policy on performance of Nepalese Commercial Banks listed in NEPSE for

different financial periods.

.III Significance of Research

The given research work focuses on the analysis of firm performance in relation to the

dividend policy followed by Nepalese commercial banks listed on NEPSE. Dividends refer to a

portion of earnings that are distributed to the shareholders of a business as per their holdings or

ownership. They are a type of benefit to shareholders in return of risk taken by them. Dividend

policy guides a business to allocate these benefits among its shareholders fairly by taking into

consideration all other variables such as working capital requirements and payment of debts.

Thus, if there is a change in dividend policy it would show in the bank's performance too. This

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

research shows the extent to which the impact of these policies are related to a commercial

bank's performance using quantitative techniques of data analysis.

PROJECT OBJECTIVE

Primarily, this research aims to discover the impact of dividend policy on financial

performance of Nepalese commercial banks listed on Nepal Stock Exchange through empirical

observation. In addition, it also attempts to analyse current dividend policies followed by such

banks, whether they are similar or different, frequency as well as rate at which dividends are paid

to the investors and determine the factors affecting firm performance and their implications.

PROJECT SCOPE

To achieve the aforementioned objectives, this project will consist of using quantitative

to study the relationship between Return on Assets (ROA), Earning Per Share (EPS), Return on

Capital Employed and Dividend with performance of commercial banks of Nepal through

regression analysis.

LITERATURE REVIEW

.I Impact of dividend policy on corporate performance

According to Walter (1966), a business entity is required to ponder over the fact that

whether it would retain all its earnings for future operations or it will pay its shareholders in a

definite amount and retain the balance or provide a non-cash alternative through Scrip dividends.

If the business decides to opt for the second alternative, such payments made to the shareholders

are called Dividends. These payments are based on some predefined policies or regulations that

provide guidelines to the internal management to ensure that its paid in a fair and logical manner.

Such guidelines are known as Dividend Policy. It is important to formulate the dividend policies

carefully as they help in providing the picture of organisation's success or failure over the years.

This ultimately acts as an indicator for corporate performance of an organisation,whether a

company or a bank.

Dividend has been a debatable topic for decades and many researchers have tried to come

up with theories to better explain the relationship between dividend policies and firm

performance. They have been explained below:

Agency Theory:

2

bank's performance using quantitative techniques of data analysis.

PROJECT OBJECTIVE

Primarily, this research aims to discover the impact of dividend policy on financial

performance of Nepalese commercial banks listed on Nepal Stock Exchange through empirical

observation. In addition, it also attempts to analyse current dividend policies followed by such

banks, whether they are similar or different, frequency as well as rate at which dividends are paid

to the investors and determine the factors affecting firm performance and their implications.

PROJECT SCOPE

To achieve the aforementioned objectives, this project will consist of using quantitative

to study the relationship between Return on Assets (ROA), Earning Per Share (EPS), Return on

Capital Employed and Dividend with performance of commercial banks of Nepal through

regression analysis.

LITERATURE REVIEW

.I Impact of dividend policy on corporate performance

According to Walter (1966), a business entity is required to ponder over the fact that

whether it would retain all its earnings for future operations or it will pay its shareholders in a

definite amount and retain the balance or provide a non-cash alternative through Scrip dividends.

If the business decides to opt for the second alternative, such payments made to the shareholders

are called Dividends. These payments are based on some predefined policies or regulations that

provide guidelines to the internal management to ensure that its paid in a fair and logical manner.

Such guidelines are known as Dividend Policy. It is important to formulate the dividend policies

carefully as they help in providing the picture of organisation's success or failure over the years.

This ultimately acts as an indicator for corporate performance of an organisation,whether a

company or a bank.

Dividend has been a debatable topic for decades and many researchers have tried to come

up with theories to better explain the relationship between dividend policies and firm

performance. They have been explained below:

Agency Theory:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Jensen and Mackling (1986) explain agency relationship as an agreement between

principal and and agent where principal can be one or more person and an agent is obliged to

perform services on behalf of the former, including decision making. Agency theory states that

dividend payments can prove to be beneficial for the shareholders to control over-investment

problem even if the firm does not have free cash flows. According to Ho (2003), agency

relationships tend to face many conflicts and can increase agency costs. This can result in

management taking actions that are not entirely in the best interest of their investors.

Signalling Theory:

According to Miller and Rock (1985), signalling theory explains that a declaration of

increase in dividend payout ratio of a firm acts as an indicator of future growth for a company.

Thus, if there is an increase in dividend profit or payments, a positive reaction is observed among

the investors for such news and vice versa. This theory essentially works on the information

asymmetry present in the market among the investors and managers.

On the other hand, Miller and Modigliani (1961) state that investors consider dividend

history of a firm irrelevant as the dividend payments are based on the ongoing investment policy

that is followed by the Bank. This results in dividend policy having no effect on price of shares

of firm in a world with no tax levy.

Bird-in-the-hand Theory:

According to Gordon (1962) the bird in the hand theory explains that dividend is a

relevant factor to determine the firm’s value, that is to say, the external users prefer higher

dividend policy over uncertain capital gains in order to earn higher returns on their investments

and vice-versa. Here, the term “a bird-in-the-hand” refers to cash dividends. However, this

theory proves to be unsuccessful where there is no uncertainty and perfect market exists as this

would amount to complete information available in regards to a bank with both investors and

management.

Black, Fisher and Scholes, Myron (1974) observes that dividend policies have been

essentially developed to protect and prioritize shareholder's interest to receive annual returns on

their stock-holdings rather than capital gains. Thus, an investor tends to opt for a high-priced

share yielding current dividends in the market. Amidu (2006) agrees that current dividends or

bird in hand help in minimizing uncertainty of an investor and increasing valuation of an

organisation such as banks.

3

principal and and agent where principal can be one or more person and an agent is obliged to

perform services on behalf of the former, including decision making. Agency theory states that

dividend payments can prove to be beneficial for the shareholders to control over-investment

problem even if the firm does not have free cash flows. According to Ho (2003), agency

relationships tend to face many conflicts and can increase agency costs. This can result in

management taking actions that are not entirely in the best interest of their investors.

Signalling Theory:

According to Miller and Rock (1985), signalling theory explains that a declaration of

increase in dividend payout ratio of a firm acts as an indicator of future growth for a company.

Thus, if there is an increase in dividend profit or payments, a positive reaction is observed among

the investors for such news and vice versa. This theory essentially works on the information

asymmetry present in the market among the investors and managers.

On the other hand, Miller and Modigliani (1961) state that investors consider dividend

history of a firm irrelevant as the dividend payments are based on the ongoing investment policy

that is followed by the Bank. This results in dividend policy having no effect on price of shares

of firm in a world with no tax levy.

Bird-in-the-hand Theory:

According to Gordon (1962) the bird in the hand theory explains that dividend is a

relevant factor to determine the firm’s value, that is to say, the external users prefer higher

dividend policy over uncertain capital gains in order to earn higher returns on their investments

and vice-versa. Here, the term “a bird-in-the-hand” refers to cash dividends. However, this

theory proves to be unsuccessful where there is no uncertainty and perfect market exists as this

would amount to complete information available in regards to a bank with both investors and

management.

Black, Fisher and Scholes, Myron (1974) observes that dividend policies have been

essentially developed to protect and prioritize shareholder's interest to receive annual returns on

their stock-holdings rather than capital gains. Thus, an investor tends to opt for a high-priced

share yielding current dividends in the market. Amidu (2006) agrees that current dividends or

bird in hand help in minimizing uncertainty of an investor and increasing valuation of an

organisation such as banks.

3

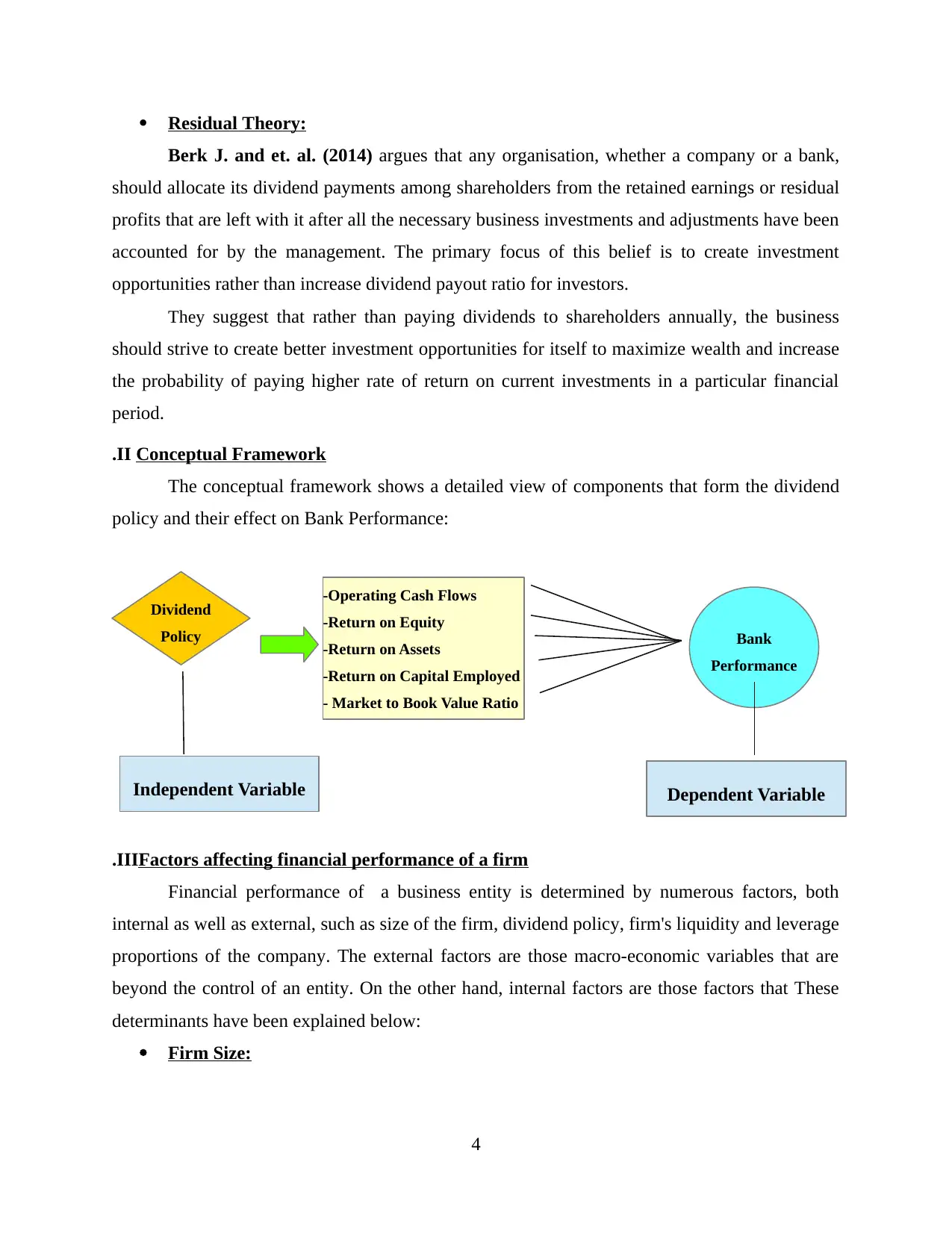

-Operating Cash Flows

-Return on Equity

-Return on Assets

-Return on Capital Employed

- Market to Book Value Ratio

Residual Theory:

Berk J. and et. al. (2014) argues that any organisation, whether a company or a bank,

should allocate its dividend payments among shareholders from the retained earnings or residual

profits that are left with it after all the necessary business investments and adjustments have been

accounted for by the management. The primary focus of this belief is to create investment

opportunities rather than increase dividend payout ratio for investors.

They suggest that rather than paying dividends to shareholders annually, the business

should strive to create better investment opportunities for itself to maximize wealth and increase

the probability of paying higher rate of return on current investments in a particular financial

period.

.II Conceptual Framework

The conceptual framework shows a detailed view of components that form the dividend

policy and their effect on Bank Performance:

.IIIFactors affecting financial performance of a firm

Financial performance of a business entity is determined by numerous factors, both

internal as well as external, such as size of the firm, dividend policy, firm's liquidity and leverage

proportions of the company. The external factors are those macro-economic variables that are

beyond the control of an entity. On the other hand, internal factors are those factors that These

determinants have been explained below:

Firm Size:

4

Dividend

Policy Bank

Performance

Independent Variable Dependent Variable

-Return on Equity

-Return on Assets

-Return on Capital Employed

- Market to Book Value Ratio

Residual Theory:

Berk J. and et. al. (2014) argues that any organisation, whether a company or a bank,

should allocate its dividend payments among shareholders from the retained earnings or residual

profits that are left with it after all the necessary business investments and adjustments have been

accounted for by the management. The primary focus of this belief is to create investment

opportunities rather than increase dividend payout ratio for investors.

They suggest that rather than paying dividends to shareholders annually, the business

should strive to create better investment opportunities for itself to maximize wealth and increase

the probability of paying higher rate of return on current investments in a particular financial

period.

.II Conceptual Framework

The conceptual framework shows a detailed view of components that form the dividend

policy and their effect on Bank Performance:

.IIIFactors affecting financial performance of a firm

Financial performance of a business entity is determined by numerous factors, both

internal as well as external, such as size of the firm, dividend policy, firm's liquidity and leverage

proportions of the company. The external factors are those macro-economic variables that are

beyond the control of an entity. On the other hand, internal factors are those factors that These

determinants have been explained below:

Firm Size:

4

Dividend

Policy Bank

Performance

Independent Variable Dependent Variable

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Love and Rachinsky (2007) say that the larger a firm is, the better it tends to perform.

Hence, a firm size largely affects it performance making large scale enterprises more competitive

undertaking higher risks and enjoying higher returns as compared to small and medium-sized

enterprises. Akhigbe & Mcnulty (2005) found a statistically significant difference in the

average profitability among the small banks with the lowest profitability and the largest with the

highest profitability.

Dividend policy:

Lintner (1956) explains that there is a positive relationship between dividend policy of a

firm and its market value. This idea has been additionally supported by the bird in hand theory

(Gordon, 1962). Walter (1966) observes that business entities which are more driven towards

paying regular dividends are more likely to attract potential investors due to the belief among

investors that current cash dividend are less risky as compared to future capital gains.

Liquidity:

Liquidity refers to how easily can an asset or a security of an organization is convertible

to cash without affecting the price of asset or security in question. This cash-flow provides a

means for an organisation to meet its obligations, especially when they are having scarcity of

cash or earnings in a year.

According to Amal et al. (2012) liquidity is a significant factor that affects firm’s

performance. Therefore, it is important for the firm to focus on increasing its current assets and

minimizing its present obligation to improve liquidity. This would make the daily operations of

the business more efficient thus enhancing performance in the end.

Leverage:

According to Pandey (1995) both debt and equity capital affect the cost of capital and

value of the firm. The capital structure portrays the financial security of a business among its

stakeholders which is easily understandable by analysing the amount of debt and equity a firm

possesses. Jensen (1986) states that debt financing puts pressure on managers to improve

performance by minimizing moral behavioural hazard and cash flows thus increasing the

efficiency of operating a business.

Therefore, high leverage firms tend to perform better financially, thus, denoting a

positive relationship between leveraging and performance.

5

Hence, a firm size largely affects it performance making large scale enterprises more competitive

undertaking higher risks and enjoying higher returns as compared to small and medium-sized

enterprises. Akhigbe & Mcnulty (2005) found a statistically significant difference in the

average profitability among the small banks with the lowest profitability and the largest with the

highest profitability.

Dividend policy:

Lintner (1956) explains that there is a positive relationship between dividend policy of a

firm and its market value. This idea has been additionally supported by the bird in hand theory

(Gordon, 1962). Walter (1966) observes that business entities which are more driven towards

paying regular dividends are more likely to attract potential investors due to the belief among

investors that current cash dividend are less risky as compared to future capital gains.

Liquidity:

Liquidity refers to how easily can an asset or a security of an organization is convertible

to cash without affecting the price of asset or security in question. This cash-flow provides a

means for an organisation to meet its obligations, especially when they are having scarcity of

cash or earnings in a year.

According to Amal et al. (2012) liquidity is a significant factor that affects firm’s

performance. Therefore, it is important for the firm to focus on increasing its current assets and

minimizing its present obligation to improve liquidity. This would make the daily operations of

the business more efficient thus enhancing performance in the end.

Leverage:

According to Pandey (1995) both debt and equity capital affect the cost of capital and

value of the firm. The capital structure portrays the financial security of a business among its

stakeholders which is easily understandable by analysing the amount of debt and equity a firm

possesses. Jensen (1986) states that debt financing puts pressure on managers to improve

performance by minimizing moral behavioural hazard and cash flows thus increasing the

efficiency of operating a business.

Therefore, high leverage firms tend to perform better financially, thus, denoting a

positive relationship between leveraging and performance.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

.IV Empirical Studies

La Porta, R. et al. (2000) conducted a survey to test agency cost hypotheses by taking a

sample size of 4000 companies from 33 countries that were broadly classified into two groups-

countries providing proper legal protection to shareholders and countries providing poor legal

security. This approach adopted two models- an outcome model and substitute model. The

outcome model derived that dividend is a direct product of proper provisioning of legal

protection to a firm's investors which enabled firms to have a high dividend payout ratio

incorporated in their dividend policies. On the other hand, the substitute model derived that

dividends are used to gain good reputation among shareholders present in an environment where

poor legal protection framework is observed. Thus, La Porta, R. et al. (2000) concluded that

agency approach is highly relevant to understand corporate dividend policy across the world.

Nissim and Ziv (2001) carried out a study to gauge relational aspect between change in

dividend and firm's profitability conditions between 1963 and 1968 with the help of regression

analysis where earnings and dividend were considered as dependent and independent variables

respectively. The duo concluded that any change in dividend signalled at a firm's future

profitability level at a given point of time.

Parsian, Koloukhi and Abdolnejad (2013) attempted to ascertain relation between

dividend payout ratio and future earnings by analysing 102 companies and financial institutions

between 2004 and 2010 taking growth as dependent variable and leverage, dividend payout ratio,

size, EPS and RoA as independent variables. They inferred that growth is largely affected by

dividend payout ratio of a firm.

Baker, Veit & Powell (2001) conducted a research to find out the relationship between

dividend policy and firm value on firms listed in NASDAQ, American security exchange that

pays cash dividend to its shareholders. 188 firms were used as a sample and through the research

they found that dividend policy has effect in the firm’s value.

.V Legal Provision regarding Dividend practice in Nepal

Sujata Pradhan (2009) on her research on “Dividend policies in Nepalese Commercial

Banks” has clearly outlined the legal provisions regarding dividend practices in Nepal defined by

Company Act 1997. Through her study she found that dividend should be distributed to

shareholders within 45 days from the initial decision date, except in some circumstances. She

also found that only the registered person will be entitled to receive such dividend.

6

La Porta, R. et al. (2000) conducted a survey to test agency cost hypotheses by taking a

sample size of 4000 companies from 33 countries that were broadly classified into two groups-

countries providing proper legal protection to shareholders and countries providing poor legal

security. This approach adopted two models- an outcome model and substitute model. The

outcome model derived that dividend is a direct product of proper provisioning of legal

protection to a firm's investors which enabled firms to have a high dividend payout ratio

incorporated in their dividend policies. On the other hand, the substitute model derived that

dividends are used to gain good reputation among shareholders present in an environment where

poor legal protection framework is observed. Thus, La Porta, R. et al. (2000) concluded that

agency approach is highly relevant to understand corporate dividend policy across the world.

Nissim and Ziv (2001) carried out a study to gauge relational aspect between change in

dividend and firm's profitability conditions between 1963 and 1968 with the help of regression

analysis where earnings and dividend were considered as dependent and independent variables

respectively. The duo concluded that any change in dividend signalled at a firm's future

profitability level at a given point of time.

Parsian, Koloukhi and Abdolnejad (2013) attempted to ascertain relation between

dividend payout ratio and future earnings by analysing 102 companies and financial institutions

between 2004 and 2010 taking growth as dependent variable and leverage, dividend payout ratio,

size, EPS and RoA as independent variables. They inferred that growth is largely affected by

dividend payout ratio of a firm.

Baker, Veit & Powell (2001) conducted a research to find out the relationship between

dividend policy and firm value on firms listed in NASDAQ, American security exchange that

pays cash dividend to its shareholders. 188 firms were used as a sample and through the research

they found that dividend policy has effect in the firm’s value.

.V Legal Provision regarding Dividend practice in Nepal

Sujata Pradhan (2009) on her research on “Dividend policies in Nepalese Commercial

Banks” has clearly outlined the legal provisions regarding dividend practices in Nepal defined by

Company Act 1997. Through her study she found that dividend should be distributed to

shareholders within 45 days from the initial decision date, except in some circumstances. She

also found that only the registered person will be entitled to receive such dividend.

6

.VI Literature Gap

Since this study focuses on NEPSE listed Commercial Banks of Nepal, it is very difficult

to generalize the expected outcomes of this research for Nepal's Banking sector in its entirety.

Also,in the context of Nepalese commercial banks, it has been observed that there is no definite

pattern followed by these institutions. The literature available in relation to dividend policy and

bank performance, it is important to take into account the market where tax and information

asymmetry exists along with leverage and size of the market in which the bank operates. Even in

context of research, there has been hardly any analysis carried out by researchers to find out the

effect of dividend policy in these banks. Also, instead of taking short term periods for research,

loner periods should be taken into account for better spotting of underlying trends and

behaviours of share price, dividend payouts and announcements of critical news made by the

management of an organization now and then. Most of the articles do not assume these criteria

and build their study on short term periods thus giving behavioural patterns of performance and

dividend policy that may not be eligible in larger time span. On the basis of this study latest data

from different Nepalese commercial banks will be used in later stage to analyse the impact of

dividend policies because earlier studies have become old and outdated. So, it is believed that

this study will prove different than the previous research and will be able to fulfil the research

gap in relation to dividend policy.

RESEARCH QUESTIONS

The significant questions for this expedition work are as under:

Primary Question:

What are the impact of dividend policy on firms performance in Nepalese Commercial

Banks?

Secondary Question:

Which factors affect performance of Nepalese Commercial Banks?

What type of dividend policies are followed by such banks?

Does every Nepalese Commercial Banks follow same dividend policies?

Are the banks regularly distributing dividends to its shareholders?

What are the changes observed after the implementation of dividend policy by Nepalese

Commercial Banks?

7

Since this study focuses on NEPSE listed Commercial Banks of Nepal, it is very difficult

to generalize the expected outcomes of this research for Nepal's Banking sector in its entirety.

Also,in the context of Nepalese commercial banks, it has been observed that there is no definite

pattern followed by these institutions. The literature available in relation to dividend policy and

bank performance, it is important to take into account the market where tax and information

asymmetry exists along with leverage and size of the market in which the bank operates. Even in

context of research, there has been hardly any analysis carried out by researchers to find out the

effect of dividend policy in these banks. Also, instead of taking short term periods for research,

loner periods should be taken into account for better spotting of underlying trends and

behaviours of share price, dividend payouts and announcements of critical news made by the

management of an organization now and then. Most of the articles do not assume these criteria

and build their study on short term periods thus giving behavioural patterns of performance and

dividend policy that may not be eligible in larger time span. On the basis of this study latest data

from different Nepalese commercial banks will be used in later stage to analyse the impact of

dividend policies because earlier studies have become old and outdated. So, it is believed that

this study will prove different than the previous research and will be able to fulfil the research

gap in relation to dividend policy.

RESEARCH QUESTIONS

The significant questions for this expedition work are as under:

Primary Question:

What are the impact of dividend policy on firms performance in Nepalese Commercial

Banks?

Secondary Question:

Which factors affect performance of Nepalese Commercial Banks?

What type of dividend policies are followed by such banks?

Does every Nepalese Commercial Banks follow same dividend policies?

Are the banks regularly distributing dividends to its shareholders?

What are the changes observed after the implementation of dividend policy by Nepalese

Commercial Banks?

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

RESEARCH DESIGN AND METHODOLODGY

This report follows Interpretivism philosophy and focuses on finding cause-effect

relationship between Dividend Policy and performance of commercial banks as well as analyses

their implications. For this purpose, the research has been divided into two broad parts viz.

Experimental and descriptive research design with quantitative data-driven study. Here,

performance is assumed as the independent variable and is initially utilised to find its effect on

Operating Cash Flows, Return on Assets, Earning per share, Return on Capital Employed,

Return on Equity and Market to Book Value Ratio. Data on 30 commercial banks has been

collected from National Stock Exchange (NEPSE) website (shown in Appendices). Out of these

30 banks, all 'A' classified commercial banks have been chosen as sample based on their

performance along with high dividend payout ratio. These include Standard Chartered Bank

Nepal Limited, NABIL Bank Limited, Nepal Investment Bank Limited and Everest Bank

Limited.

The above research has been carried out in Australia using secondary data that has been

taken through the NEPSE exchange database along with reports, financial records, and articles

from newsletters as well as related websites and books. The five year financial records including

bank's balance sheet, cash flow statements have been used to calculate ratios for each bank. After

this, they have been compared to the current CAGR growth of Banking Sector in Nepal to

understand underlying trends as to how these banks have been performing and growing in the

recent years. Also, a linear regression analysis tested at 5% significance level is carried out on

the sample for the study to establish a relationship among the variables, both dependent and

independent. On the other hand, data on performance of banks and dividend policy was

evaluated through descriptive statistics tools such as mean, standard deviation, correlation,

skewness and kurtosis.

RESEARCH LIMITATIONS

The scope of research is limited to the data available on NEPSE website in addition to

other related articles and newsletters accessible to users. Hence, this information gathered by the

researcher may not be completely reliable and the results derived thereof may not be validated

accurately. The concept of dividend policy impacting firm performance has invited varied

opinions or views among researchers and scholar which results in much ambiguity when

8

This report follows Interpretivism philosophy and focuses on finding cause-effect

relationship between Dividend Policy and performance of commercial banks as well as analyses

their implications. For this purpose, the research has been divided into two broad parts viz.

Experimental and descriptive research design with quantitative data-driven study. Here,

performance is assumed as the independent variable and is initially utilised to find its effect on

Operating Cash Flows, Return on Assets, Earning per share, Return on Capital Employed,

Return on Equity and Market to Book Value Ratio. Data on 30 commercial banks has been

collected from National Stock Exchange (NEPSE) website (shown in Appendices). Out of these

30 banks, all 'A' classified commercial banks have been chosen as sample based on their

performance along with high dividend payout ratio. These include Standard Chartered Bank

Nepal Limited, NABIL Bank Limited, Nepal Investment Bank Limited and Everest Bank

Limited.

The above research has been carried out in Australia using secondary data that has been

taken through the NEPSE exchange database along with reports, financial records, and articles

from newsletters as well as related websites and books. The five year financial records including

bank's balance sheet, cash flow statements have been used to calculate ratios for each bank. After

this, they have been compared to the current CAGR growth of Banking Sector in Nepal to

understand underlying trends as to how these banks have been performing and growing in the

recent years. Also, a linear regression analysis tested at 5% significance level is carried out on

the sample for the study to establish a relationship among the variables, both dependent and

independent. On the other hand, data on performance of banks and dividend policy was

evaluated through descriptive statistics tools such as mean, standard deviation, correlation,

skewness and kurtosis.

RESEARCH LIMITATIONS

The scope of research is limited to the data available on NEPSE website in addition to

other related articles and newsletters accessible to users. Hence, this information gathered by the

researcher may not be completely reliable and the results derived thereof may not be validated

accurately. The concept of dividend policy impacting firm performance has invited varied

opinions or views among researchers and scholar which results in much ambiguity when

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

conducting a investigation of these variables. Nepalese Commercial Bank sector is only limited

to a population size of 30 Banks which is really small for conducting a research. Also, the use of

statistical tools such as linear regression models, skewness and kurtosis have their own

limitations that also effect the results and their evaluations. Lastly, the scope and depth of

discussions in this paper are limited to the experience of the researcher in many levels as

compared to the works of experienced scholars.

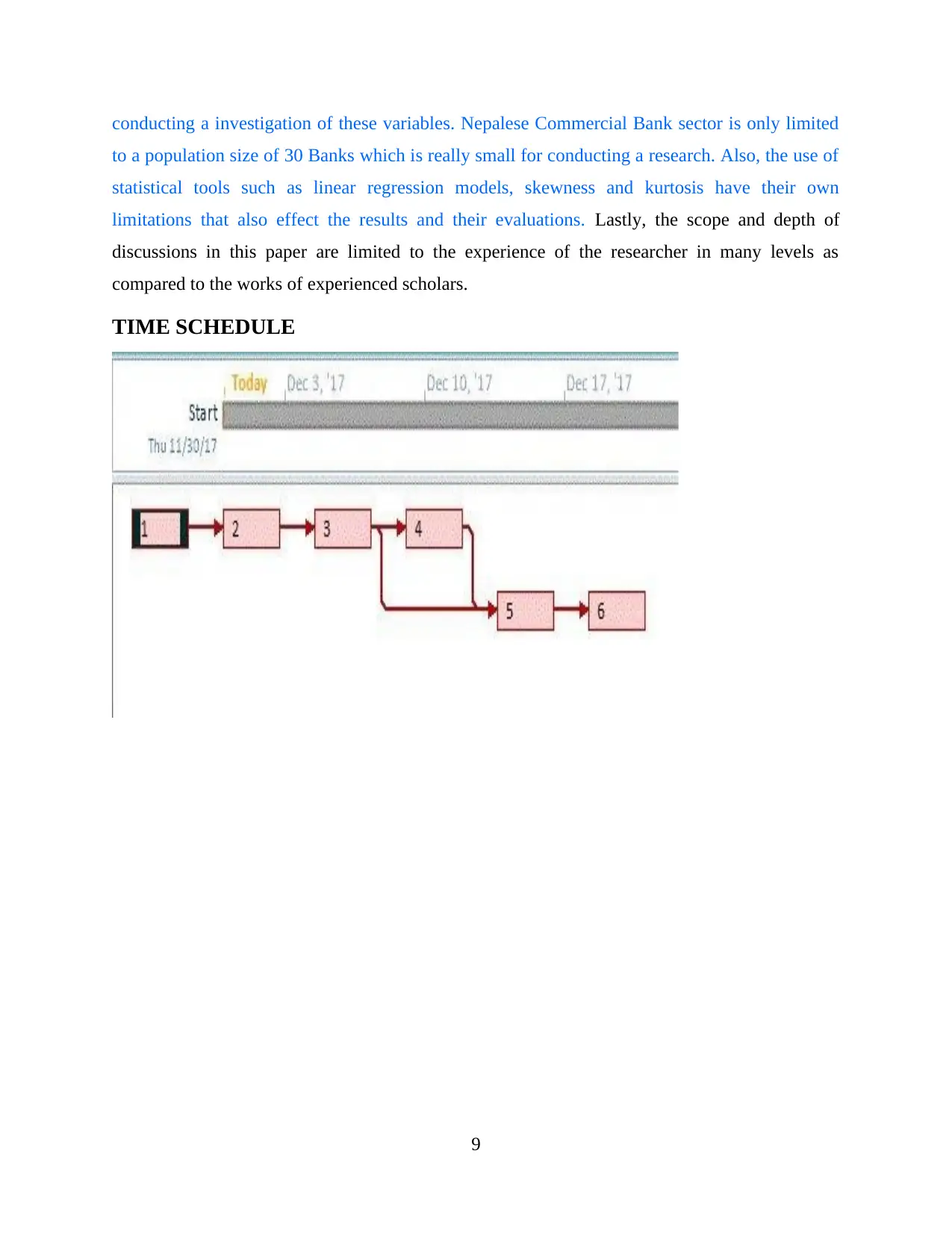

TIME SCHEDULE

9

to a population size of 30 Banks which is really small for conducting a research. Also, the use of

statistical tools such as linear regression models, skewness and kurtosis have their own

limitations that also effect the results and their evaluations. Lastly, the scope and depth of

discussions in this paper are limited to the experience of the researcher in many levels as

compared to the works of experienced scholars.

TIME SCHEDULE

9

CONCLUSION

From the above report it can be concluded that research can prove to be an effective

method to help in determining the factors that make impact on the business operation. The above

discussed research report shows the influence of dividend policy on business performance of

commercial banks listed on NEPSE. Data from 30 Nepalese commercial banks listed in NEPSE

for different financial period will be used in further stage. Return on equity (ROE) is an

important tool to measure firm performance (Garrett & Priestley, 2000) and dividend policy has

positive relation with ROE. Before making any investment on share, investor must study the

dividend policy of bank (Dickens, et al., 2002).

10

From the above report it can be concluded that research can prove to be an effective

method to help in determining the factors that make impact on the business operation. The above

discussed research report shows the influence of dividend policy on business performance of

commercial banks listed on NEPSE. Data from 30 Nepalese commercial banks listed in NEPSE

for different financial period will be used in further stage. Return on equity (ROE) is an

important tool to measure firm performance (Garrett & Priestley, 2000) and dividend policy has

positive relation with ROE. Before making any investment on share, investor must study the

dividend policy of bank (Dickens, et al., 2002).

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.