International Finance Report: Dixons Carphone Plc Performance Analysis

VerifiedAdded on 2020/01/23

|18

|3765

|81

Report

AI Summary

This report provides a comprehensive financial analysis of Dixons Carphone Plc, examining its performance through ratio analysis for the years 2015 and 2016. The analysis covers profitability (gross and net profit margins), liquidity (current and quick ratios), solvency (debt-to-equity ratio), efficiency (asset turnover and inventory turnover), and investment performance (earnings per share). The report compares Dixons Carphone Plc to its competitor, Metro AG, highlighting key differences and trends. In addition to ratio analysis, the report discusses capital structure and dividend theories relevant to the company's financial strategy. The analysis considers factors such as revenue, cost control, market competition, and the impact of financial decisions on the company's overall financial health. The report concludes with an overview of the financial performance and provides insights into the company's strengths and weaknesses.

International Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................1

RATIO ANALYSIS..............................................................................................................................1

Analysis of profitability...................................................................................................................1

Analysis of liquidity.........................................................................................................................3

Analysis of solvency........................................................................................................................5

Analysis of efficiency......................................................................................................................7

Analysis of investment performance...............................................................................................8

CAPITAL STRUCTURE THEORY....................................................................................................9

DIVIDEND THEORY........................................................................................................................10

NON-DOMESTIC FINANCE PRODUCT........................................................................................11

CONCLUSION...................................................................................................................................11

REFERENCES...................................................................................................................................12

APPENDIX........................................................................................................................................14

Dixone Carphone’s ratio analysis..................................................................................................14

Metro AG ratio analysis.................................................................................................................15

INTRODUCTION................................................................................................................................1

RATIO ANALYSIS..............................................................................................................................1

Analysis of profitability...................................................................................................................1

Analysis of liquidity.........................................................................................................................3

Analysis of solvency........................................................................................................................5

Analysis of efficiency......................................................................................................................7

Analysis of investment performance...............................................................................................8

CAPITAL STRUCTURE THEORY....................................................................................................9

DIVIDEND THEORY........................................................................................................................10

NON-DOMESTIC FINANCE PRODUCT........................................................................................11

CONCLUSION...................................................................................................................................11

REFERENCES...................................................................................................................................12

APPENDIX........................................................................................................................................14

Dixone Carphone’s ratio analysis..................................................................................................14

Metro AG ratio analysis.................................................................................................................15

Index of Figures

Figure 1 Profitability ratios of Dixone Carphone Plc...........................................................................1

Figure 2 Gross profit ratios of Dixone Carphone and Metro AG.........................................................2

Figure 3 Net profit ratios of Dixone Carphone and Metro AG............................................................3

Figure 4 Liquidity ratio of Dixone Carphone Plc.................................................................................4

Figure 5 Current ratio of Dixone Carphone Plc and Metro AG...........................................................4

Figure 6 Quick Ratio of Dixone Carphone Plc and Metro AG............................................................5

Figure 7 Debt to equity ratio of Dixone Carphone Plc.........................................................................6

Figure 8 Debt to equity ratio of Dixone Carphone Plc and Metro AG................................................6

Figure 9 Efficiency ratio of Dixone Carphone Plc...............................................................................7

Figure 10 Earnings per share of Dixone Carphone Plc and Metro AG................................................8

Figure 1 Profitability ratios of Dixone Carphone Plc...........................................................................1

Figure 2 Gross profit ratios of Dixone Carphone and Metro AG.........................................................2

Figure 3 Net profit ratios of Dixone Carphone and Metro AG............................................................3

Figure 4 Liquidity ratio of Dixone Carphone Plc.................................................................................4

Figure 5 Current ratio of Dixone Carphone Plc and Metro AG...........................................................4

Figure 6 Quick Ratio of Dixone Carphone Plc and Metro AG............................................................5

Figure 7 Debt to equity ratio of Dixone Carphone Plc.........................................................................6

Figure 8 Debt to equity ratio of Dixone Carphone Plc and Metro AG................................................6

Figure 9 Efficiency ratio of Dixone Carphone Plc...............................................................................7

Figure 10 Earnings per share of Dixone Carphone Plc and Metro AG................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

In the present times, companies carry out their operations and formal course of activities at

an international market which raise the competition level among the organization. In order to

sustain in the competitive market, establishments are required to analyse their operational

performance and financial status so as to assess that whether they are performing well or not. The

present assignment here emphasises upon financial performance evaluation of an international

electrical and telecommunication company, Dixons Carphone Plc. It was established by the merger

of Dixons Retail and Carphone Warehouse on 7th August 2014. The report will analyse the

performance of the firm by incorporating ratio analysis tool for the two recent financial years, 2015

and 2016. Along with this, capital structure theory and dividend theories will be discussed.

RATIO ANALYSIS

This technique of strategic financial analysis lay emphasises upon computing a different

kind of ratios like profitability, creditworthiness, solvency, efficiency and so on to make an in-depth

evaluation of business performance.

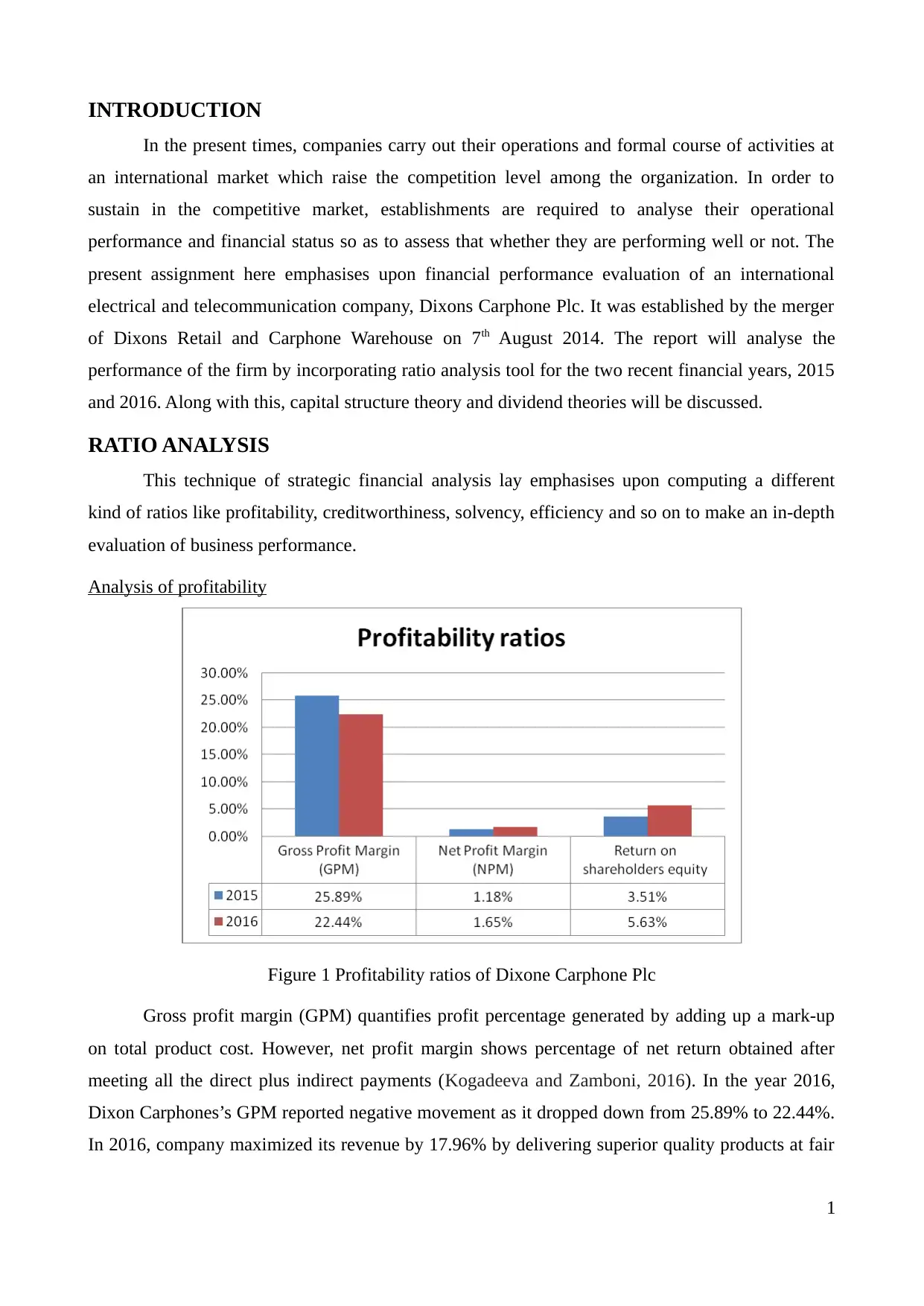

Analysis of profitability

Figure 1 Profitability ratios of Dixone Carphone Plc

Gross profit margin (GPM) quantifies profit percentage generated by adding up a mark-up

on total product cost. However, net profit margin shows percentage of net return obtained after

meeting all the direct plus indirect payments (Kogadeeva and Zamboni, 2016). In the year 2016,

Dixon Carphones’s GPM reported negative movement as it dropped down from 25.89% to 22.44%.

In 2016, company maximized its revenue by 17.96% by delivering superior quality products at fair

1

In the present times, companies carry out their operations and formal course of activities at

an international market which raise the competition level among the organization. In order to

sustain in the competitive market, establishments are required to analyse their operational

performance and financial status so as to assess that whether they are performing well or not. The

present assignment here emphasises upon financial performance evaluation of an international

electrical and telecommunication company, Dixons Carphone Plc. It was established by the merger

of Dixons Retail and Carphone Warehouse on 7th August 2014. The report will analyse the

performance of the firm by incorporating ratio analysis tool for the two recent financial years, 2015

and 2016. Along with this, capital structure theory and dividend theories will be discussed.

RATIO ANALYSIS

This technique of strategic financial analysis lay emphasises upon computing a different

kind of ratios like profitability, creditworthiness, solvency, efficiency and so on to make an in-depth

evaluation of business performance.

Analysis of profitability

Figure 1 Profitability ratios of Dixone Carphone Plc

Gross profit margin (GPM) quantifies profit percentage generated by adding up a mark-up

on total product cost. However, net profit margin shows percentage of net return obtained after

meeting all the direct plus indirect payments (Kogadeeva and Zamboni, 2016). In the year 2016,

Dixon Carphones’s GPM reported negative movement as it dropped down from 25.89% to 22.44%.

In 2016, company maximized its revenue by 17.96% by delivering superior quality products at fair

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

prices which helps to increase market demand (Dehnavi and et.al., 2015). In this year, DC’s

maximized its product sales from £5641m to £7018m whereas revenues from sale of services

comprises commission, delivery, installation, consumer support, repairing and others got increased

from £2614m to £2720m. DC struggled for the growth in revenues but its innovative, stylish and

top-quality products enable firm to enlarge their like for like sales in both the terms of electrical and

mobile trading. But still, ineffective control on direct expenditures and inflation resulted in

excessive cost of sale as it got enhanced by 23.46%, which in turn, decreased gross profit margin. It

indicates that in this year, DC’s profitability goes declined.

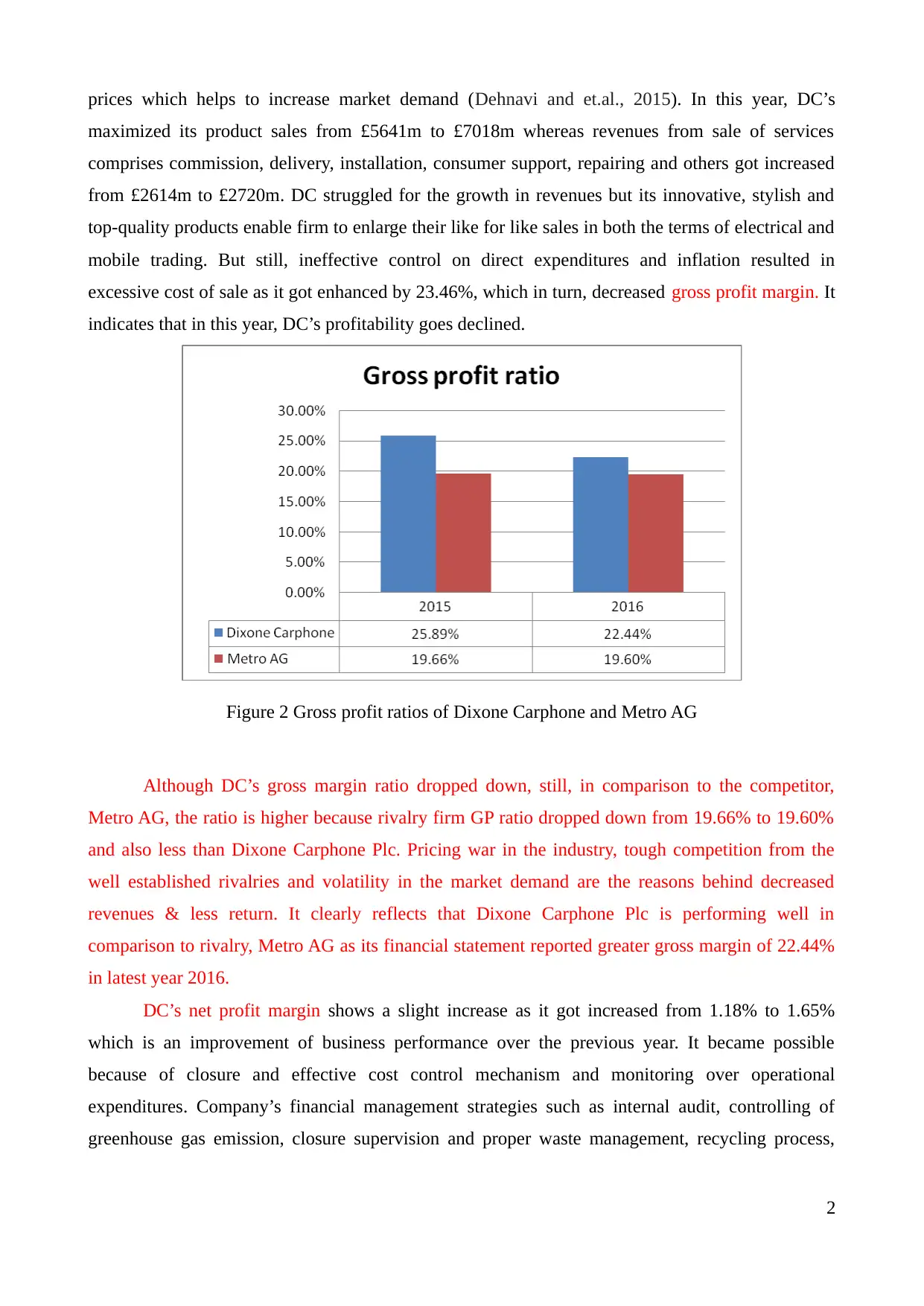

Figure 2 Gross profit ratios of Dixone Carphone and Metro AG

Although DC’s gross margin ratio dropped down, still, in comparison to the competitor,

Metro AG, the ratio is higher because rivalry firm GP ratio dropped down from 19.66% to 19.60%

and also less than Dixone Carphone Plc. Pricing war in the industry, tough competition from the

well established rivalries and volatility in the market demand are the reasons behind decreased

revenues & less return. It clearly reflects that Dixone Carphone Plc is performing well in

comparison to rivalry, Metro AG as its financial statement reported greater gross margin of 22.44%

in latest year 2016.

DC’s net profit margin shows a slight increase as it got increased from 1.18% to 1.65%

which is an improvement of business performance over the previous year. It became possible

because of closure and effective cost control mechanism and monitoring over operational

expenditures. Company’s financial management strategies such as internal audit, controlling of

greenhouse gas emission, closure supervision and proper waste management, recycling process,

2

maximized its product sales from £5641m to £7018m whereas revenues from sale of services

comprises commission, delivery, installation, consumer support, repairing and others got increased

from £2614m to £2720m. DC struggled for the growth in revenues but its innovative, stylish and

top-quality products enable firm to enlarge their like for like sales in both the terms of electrical and

mobile trading. But still, ineffective control on direct expenditures and inflation resulted in

excessive cost of sale as it got enhanced by 23.46%, which in turn, decreased gross profit margin. It

indicates that in this year, DC’s profitability goes declined.

Figure 2 Gross profit ratios of Dixone Carphone and Metro AG

Although DC’s gross margin ratio dropped down, still, in comparison to the competitor,

Metro AG, the ratio is higher because rivalry firm GP ratio dropped down from 19.66% to 19.60%

and also less than Dixone Carphone Plc. Pricing war in the industry, tough competition from the

well established rivalries and volatility in the market demand are the reasons behind decreased

revenues & less return. It clearly reflects that Dixone Carphone Plc is performing well in

comparison to rivalry, Metro AG as its financial statement reported greater gross margin of 22.44%

in latest year 2016.

DC’s net profit margin shows a slight increase as it got increased from 1.18% to 1.65%

which is an improvement of business performance over the previous year. It became possible

because of closure and effective cost control mechanism and monitoring over operational

expenditures. Company’s financial management strategies such as internal audit, controlling of

greenhouse gas emission, closure supervision and proper waste management, recycling process,

2

carbon management, efficient use of energy, expansion strategy are the reasons for control over cost

(Uechi and et.al., 2015). It can be evident from the annual financial reports, as in 2016, it shows a

little bit increase from £1813m to £1877 by 3.57%. However, high taxation obligations worth £84m

and finance cost of £41m give rises to the interest and tax payments.

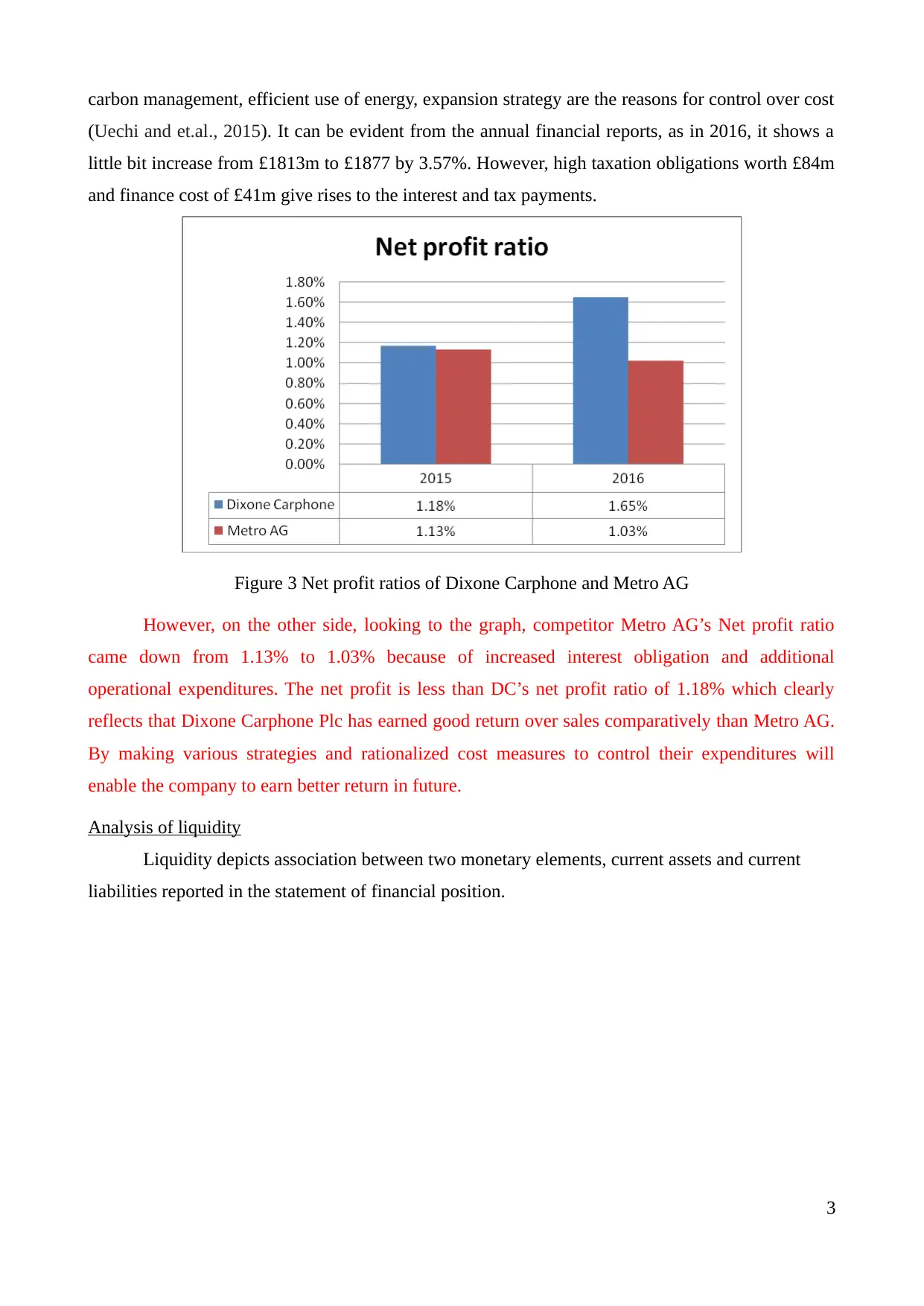

Figure 3 Net profit ratios of Dixone Carphone and Metro AG

However, on the other side, looking to the graph, competitor Metro AG’s Net profit ratio

came down from 1.13% to 1.03% because of increased interest obligation and additional

operational expenditures. The net profit is less than DC’s net profit ratio of 1.18% which clearly

reflects that Dixone Carphone Plc has earned good return over sales comparatively than Metro AG.

By making various strategies and rationalized cost measures to control their expenditures will

enable the company to earn better return in future.

Analysis of liquidity

Liquidity depicts association between two monetary elements, current assets and current

liabilities reported in the statement of financial position.

3

(Uechi and et.al., 2015). It can be evident from the annual financial reports, as in 2016, it shows a

little bit increase from £1813m to £1877 by 3.57%. However, high taxation obligations worth £84m

and finance cost of £41m give rises to the interest and tax payments.

Figure 3 Net profit ratios of Dixone Carphone and Metro AG

However, on the other side, looking to the graph, competitor Metro AG’s Net profit ratio

came down from 1.13% to 1.03% because of increased interest obligation and additional

operational expenditures. The net profit is less than DC’s net profit ratio of 1.18% which clearly

reflects that Dixone Carphone Plc has earned good return over sales comparatively than Metro AG.

By making various strategies and rationalized cost measures to control their expenditures will

enable the company to earn better return in future.

Analysis of liquidity

Liquidity depicts association between two monetary elements, current assets and current

liabilities reported in the statement of financial position.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

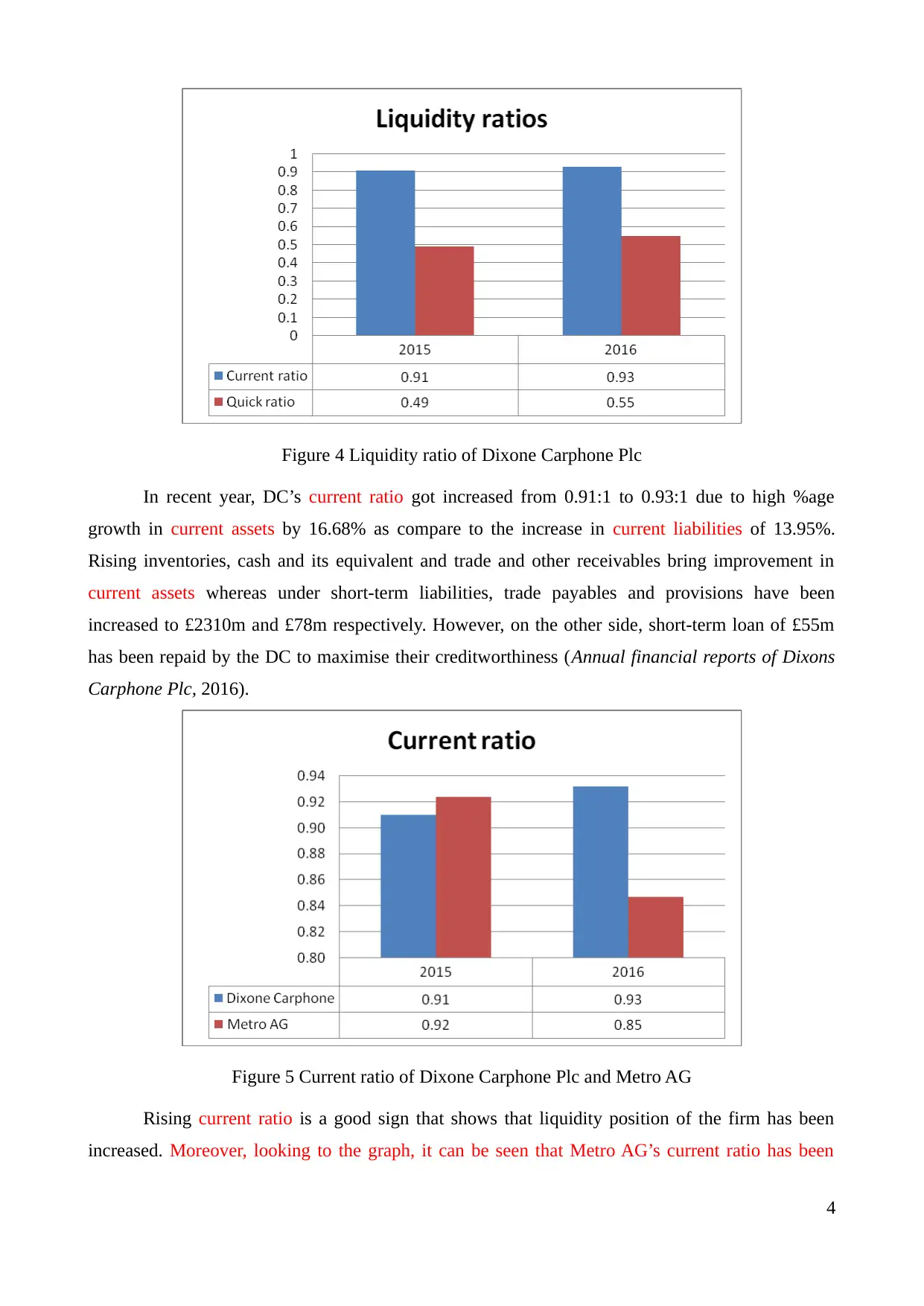

Figure 4 Liquidity ratio of Dixone Carphone Plc

In recent year, DC’s current ratio got increased from 0.91:1 to 0.93:1 due to high %age

growth in current assets by 16.68% as compare to the increase in current liabilities of 13.95%.

Rising inventories, cash and its equivalent and trade and other receivables bring improvement in

current assets whereas under short-term liabilities, trade payables and provisions have been

increased to £2310m and £78m respectively. However, on the other side, short-term loan of £55m

has been repaid by the DC to maximise their creditworthiness (Annual financial reports of Dixons

Carphone Plc, 2016).

Figure 5 Current ratio of Dixone Carphone Plc and Metro AG

Rising current ratio is a good sign that shows that liquidity position of the firm has been

increased. Moreover, looking to the graph, it can be seen that Metro AG’s current ratio has been

4

In recent year, DC’s current ratio got increased from 0.91:1 to 0.93:1 due to high %age

growth in current assets by 16.68% as compare to the increase in current liabilities of 13.95%.

Rising inventories, cash and its equivalent and trade and other receivables bring improvement in

current assets whereas under short-term liabilities, trade payables and provisions have been

increased to £2310m and £78m respectively. However, on the other side, short-term loan of £55m

has been repaid by the DC to maximise their creditworthiness (Annual financial reports of Dixons

Carphone Plc, 2016).

Figure 5 Current ratio of Dixone Carphone Plc and Metro AG

Rising current ratio is a good sign that shows that liquidity position of the firm has been

increased. Moreover, looking to the graph, it can be seen that Metro AG’s current ratio has been

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

derived to 0.92 in 2015 came down to 0.85:1 reflects less availability of short-term funds to pay off

suppliers. However, on the other side, in the industry, 2:1 is considered as an ideal ratio that

suggests both the company’s managers to make decisions in regards to enhancing their short-term

solvency position through more receivables, inventory and liquid availability to make on-time

payments to the suppliers (Bay, Chan and Walczyk, 2015).

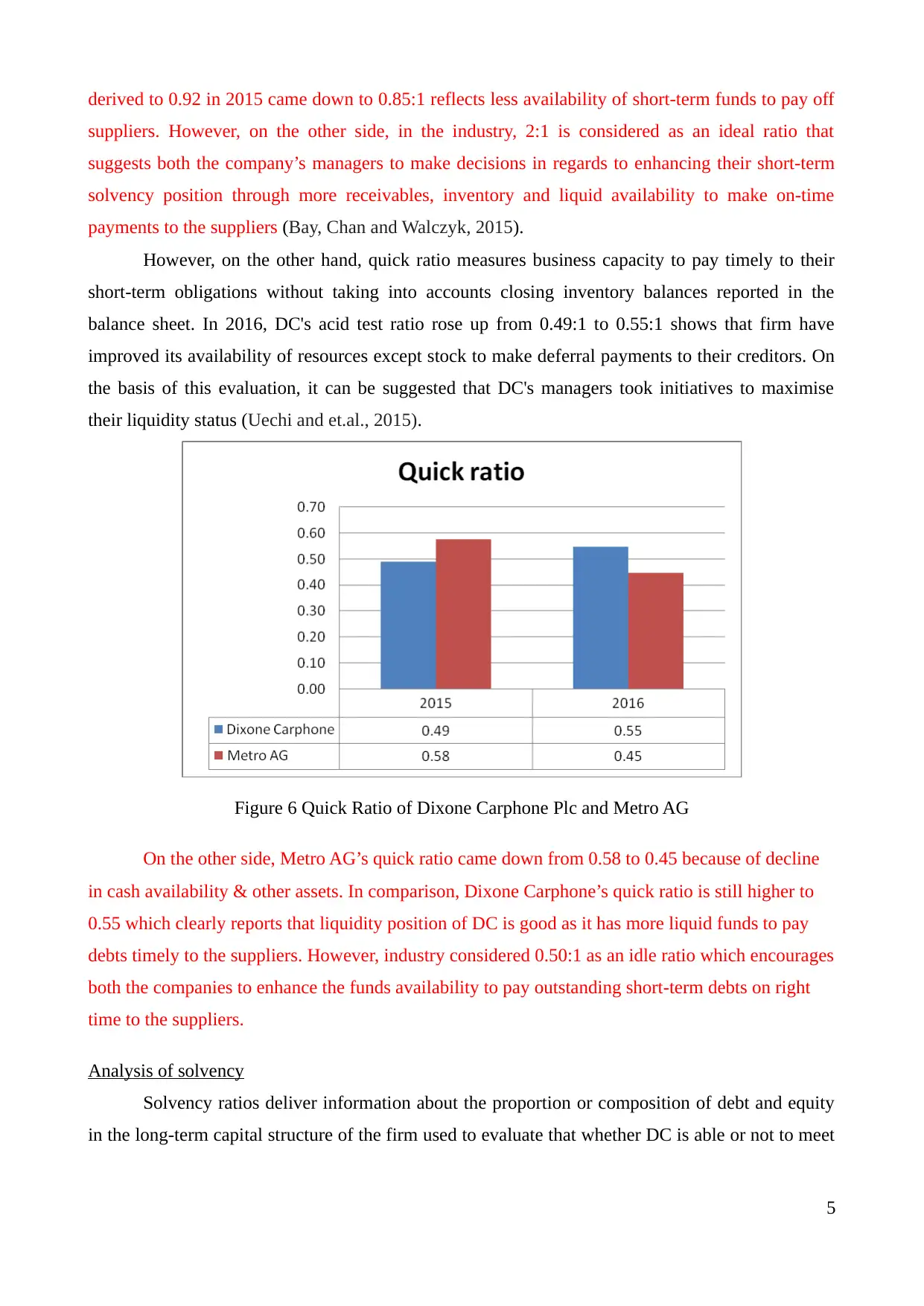

However, on the other hand, quick ratio measures business capacity to pay timely to their

short-term obligations without taking into accounts closing inventory balances reported in the

balance sheet. In 2016, DC's acid test ratio rose up from 0.49:1 to 0.55:1 shows that firm have

improved its availability of resources except stock to make deferral payments to their creditors. On

the basis of this evaluation, it can be suggested that DC's managers took initiatives to maximise

their liquidity status (Uechi and et.al., 2015).

Figure 6 Quick Ratio of Dixone Carphone Plc and Metro AG

On the other side, Metro AG’s quick ratio came down from 0.58 to 0.45 because of decline

in cash availability & other assets. In comparison, Dixone Carphone’s quick ratio is still higher to

0.55 which clearly reports that liquidity position of DC is good as it has more liquid funds to pay

debts timely to the suppliers. However, industry considered 0.50:1 as an idle ratio which encourages

both the companies to enhance the funds availability to pay outstanding short-term debts on right

time to the suppliers.

Analysis of solvency

Solvency ratios deliver information about the proportion or composition of debt and equity

in the long-term capital structure of the firm used to evaluate that whether DC is able or not to meet

5

suppliers. However, on the other side, in the industry, 2:1 is considered as an ideal ratio that

suggests both the company’s managers to make decisions in regards to enhancing their short-term

solvency position through more receivables, inventory and liquid availability to make on-time

payments to the suppliers (Bay, Chan and Walczyk, 2015).

However, on the other hand, quick ratio measures business capacity to pay timely to their

short-term obligations without taking into accounts closing inventory balances reported in the

balance sheet. In 2016, DC's acid test ratio rose up from 0.49:1 to 0.55:1 shows that firm have

improved its availability of resources except stock to make deferral payments to their creditors. On

the basis of this evaluation, it can be suggested that DC's managers took initiatives to maximise

their liquidity status (Uechi and et.al., 2015).

Figure 6 Quick Ratio of Dixone Carphone Plc and Metro AG

On the other side, Metro AG’s quick ratio came down from 0.58 to 0.45 because of decline

in cash availability & other assets. In comparison, Dixone Carphone’s quick ratio is still higher to

0.55 which clearly reports that liquidity position of DC is good as it has more liquid funds to pay

debts timely to the suppliers. However, industry considered 0.50:1 as an idle ratio which encourages

both the companies to enhance the funds availability to pay outstanding short-term debts on right

time to the suppliers.

Analysis of solvency

Solvency ratios deliver information about the proportion or composition of debt and equity

in the long-term capital structure of the firm used to evaluate that whether DC is able or not to meet

5

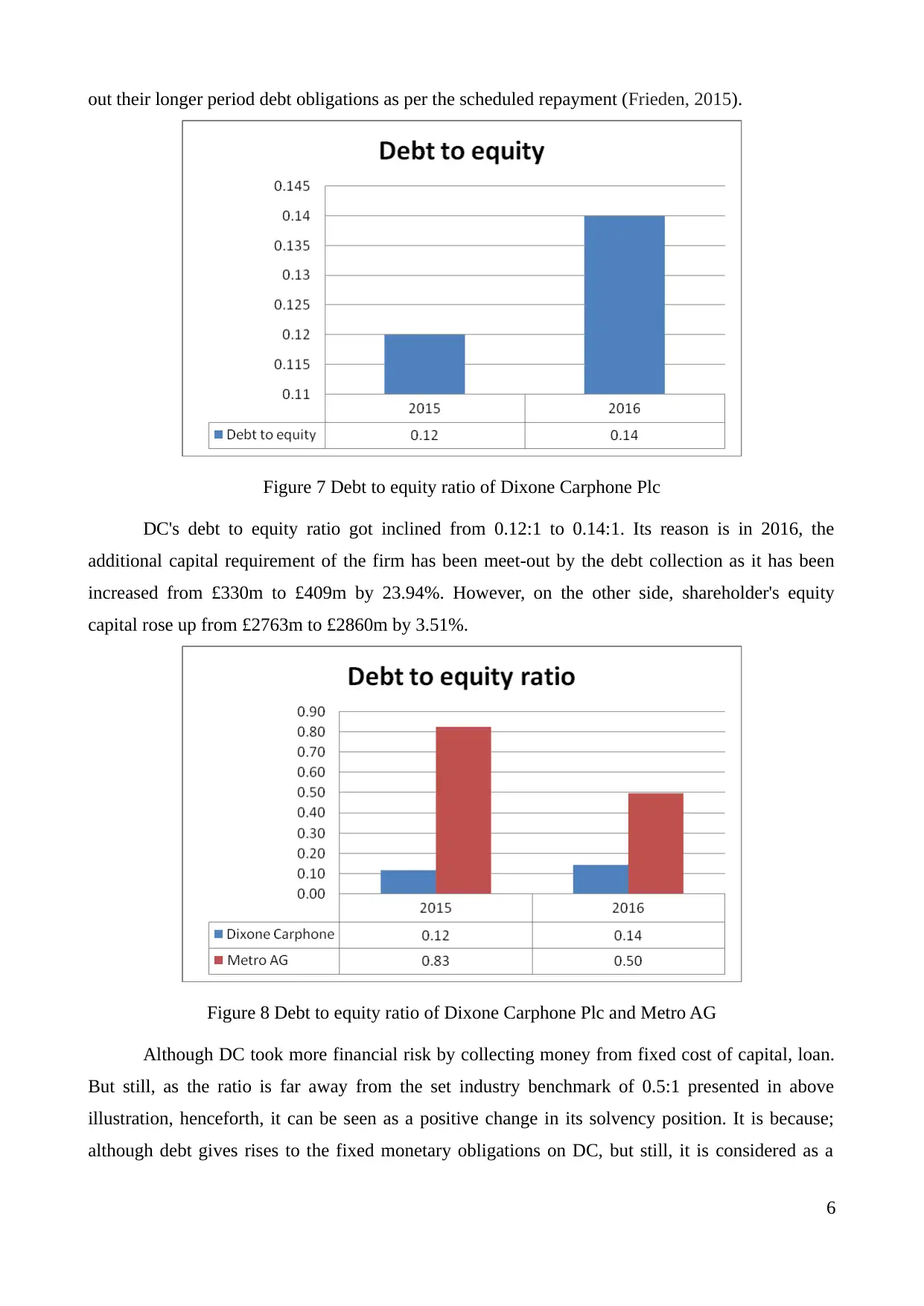

out their longer period debt obligations as per the scheduled repayment (Frieden, 2015).

Figure 7 Debt to equity ratio of Dixone Carphone Plc

DC's debt to equity ratio got inclined from 0.12:1 to 0.14:1. Its reason is in 2016, the

additional capital requirement of the firm has been meet-out by the debt collection as it has been

increased from £330m to £409m by 23.94%. However, on the other side, shareholder's equity

capital rose up from £2763m to £2860m by 3.51%.

Figure 8 Debt to equity ratio of Dixone Carphone Plc and Metro AG

Although DC took more financial risk by collecting money from fixed cost of capital, loan.

But still, as the ratio is far away from the set industry benchmark of 0.5:1 presented in above

illustration, henceforth, it can be seen as a positive change in its solvency position. It is because;

although debt gives rises to the fixed monetary obligations on DC, but still, it is considered as a

6

Figure 7 Debt to equity ratio of Dixone Carphone Plc

DC's debt to equity ratio got inclined from 0.12:1 to 0.14:1. Its reason is in 2016, the

additional capital requirement of the firm has been meet-out by the debt collection as it has been

increased from £330m to £409m by 23.94%. However, on the other side, shareholder's equity

capital rose up from £2763m to £2860m by 3.51%.

Figure 8 Debt to equity ratio of Dixone Carphone Plc and Metro AG

Although DC took more financial risk by collecting money from fixed cost of capital, loan.

But still, as the ratio is far away from the set industry benchmark of 0.5:1 presented in above

illustration, henceforth, it can be seen as a positive change in its solvency position. It is because;

although debt gives rises to the fixed monetary obligations on DC, but still, it is considered as a

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

cheaper financial source relatively to that of equity because it gives tax benefits to the company

(Dehnavi and et.al., 2015). With the help of this, the company will be able to take benefits of

trading on equity (TOI) to maximise return for investors. Apart from this, interest coverage ratio got

reduced from 8.76 to 7.41 times because of higher tax obligations and decreased earnings before

interest and tax by 6.17%. It is a clear indicator that DC's capacity to bear additional debt burden

has been fallen. Therefore, in future, it may be tough for the company to raise money through

additional external borrowings. On the basis of this, it can be suggested to the firm to maximise

their debt burden capacity to meet out their debt obligations on right time.

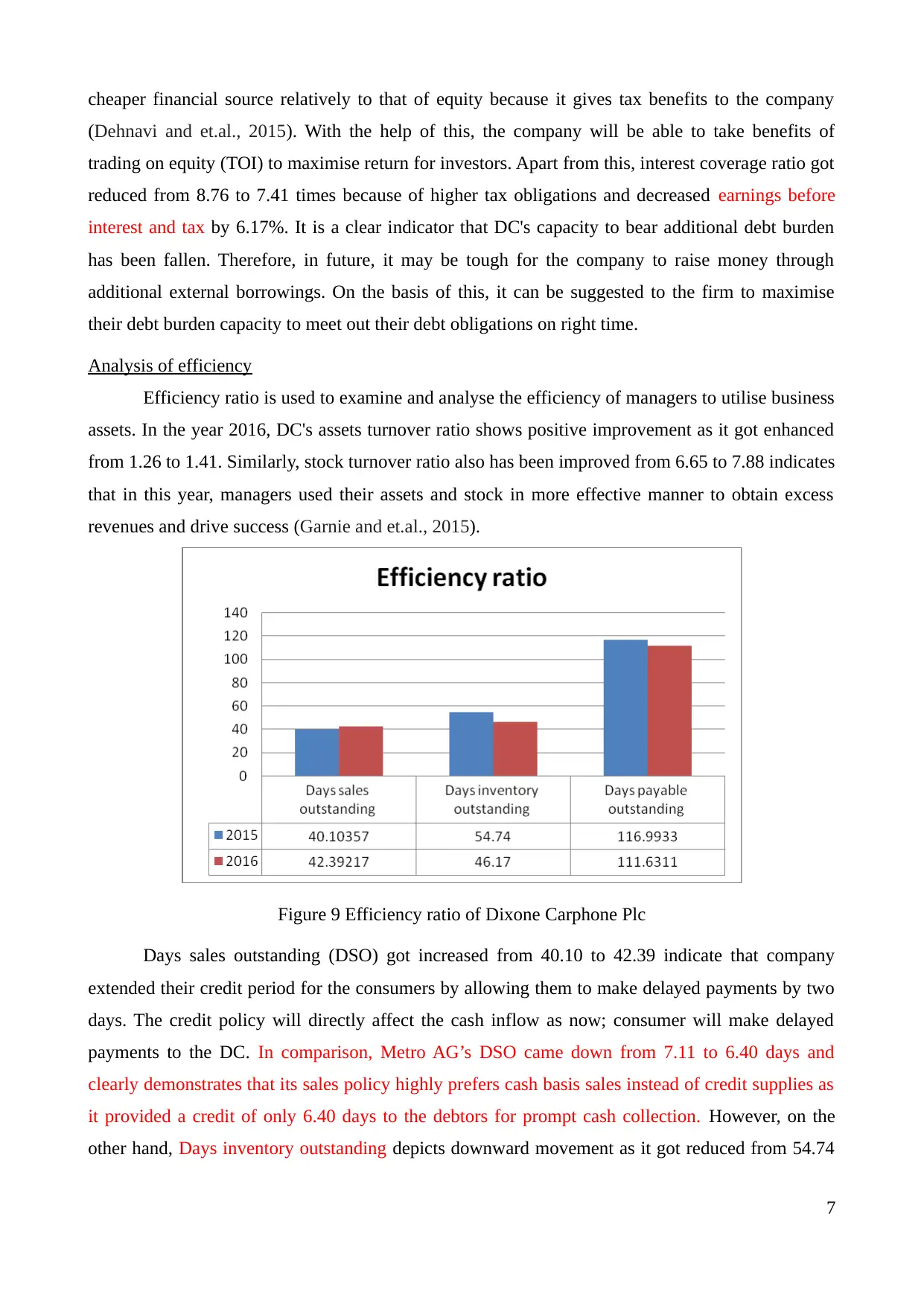

Analysis of efficiency

Efficiency ratio is used to examine and analyse the efficiency of managers to utilise business

assets. In the year 2016, DC's assets turnover ratio shows positive improvement as it got enhanced

from 1.26 to 1.41. Similarly, stock turnover ratio also has been improved from 6.65 to 7.88 indicates

that in this year, managers used their assets and stock in more effective manner to obtain excess

revenues and drive success (Garnie and et.al., 2015).

Figure 9 Efficiency ratio of Dixone Carphone Plc

Days sales outstanding (DSO) got increased from 40.10 to 42.39 indicate that company

extended their credit period for the consumers by allowing them to make delayed payments by two

days. The credit policy will directly affect the cash inflow as now; consumer will make delayed

payments to the DC. In comparison, Metro AG’s DSO came down from 7.11 to 6.40 days and

clearly demonstrates that its sales policy highly prefers cash basis sales instead of credit supplies as

it provided a credit of only 6.40 days to the debtors for prompt cash collection. However, on the

other hand, Days inventory outstanding depicts downward movement as it got reduced from 54.74

7

(Dehnavi and et.al., 2015). With the help of this, the company will be able to take benefits of

trading on equity (TOI) to maximise return for investors. Apart from this, interest coverage ratio got

reduced from 8.76 to 7.41 times because of higher tax obligations and decreased earnings before

interest and tax by 6.17%. It is a clear indicator that DC's capacity to bear additional debt burden

has been fallen. Therefore, in future, it may be tough for the company to raise money through

additional external borrowings. On the basis of this, it can be suggested to the firm to maximise

their debt burden capacity to meet out their debt obligations on right time.

Analysis of efficiency

Efficiency ratio is used to examine and analyse the efficiency of managers to utilise business

assets. In the year 2016, DC's assets turnover ratio shows positive improvement as it got enhanced

from 1.26 to 1.41. Similarly, stock turnover ratio also has been improved from 6.65 to 7.88 indicates

that in this year, managers used their assets and stock in more effective manner to obtain excess

revenues and drive success (Garnie and et.al., 2015).

Figure 9 Efficiency ratio of Dixone Carphone Plc

Days sales outstanding (DSO) got increased from 40.10 to 42.39 indicate that company

extended their credit period for the consumers by allowing them to make delayed payments by two

days. The credit policy will directly affect the cash inflow as now; consumer will make delayed

payments to the DC. In comparison, Metro AG’s DSO came down from 7.11 to 6.40 days and

clearly demonstrates that its sales policy highly prefers cash basis sales instead of credit supplies as

it provided a credit of only 6.40 days to the debtors for prompt cash collection. However, on the

other hand, Days inventory outstanding depicts downward movement as it got reduced from 54.74

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

to 46.17 days showed the faster movement of stock into sales to generate better revenues due to

optimum and effective utilisation of stock. In comparison, Metro AG’s DIO goes up from 41.61

days to 42.28 days still it is less than DC’s inventory days which reflects quick conversion of goods

into inventory to generate sales revenues. Contrary to this, Days payable outstanding came down

from 116.99 days to 111.63 days demonstrates that DC is making quicker and earlier payments to

their suppliers as compared to previous year (Suzuki and et.al., 2015). It will have a direct impact

on DC's cash funds as quick cash outgoings and delayed receipts from the suppliers affect cash

adversely. DPO of Metro AG changed downward from 73.27 to 72.92 days because and as a result,

company had paid suppliers promptly than preceding year.

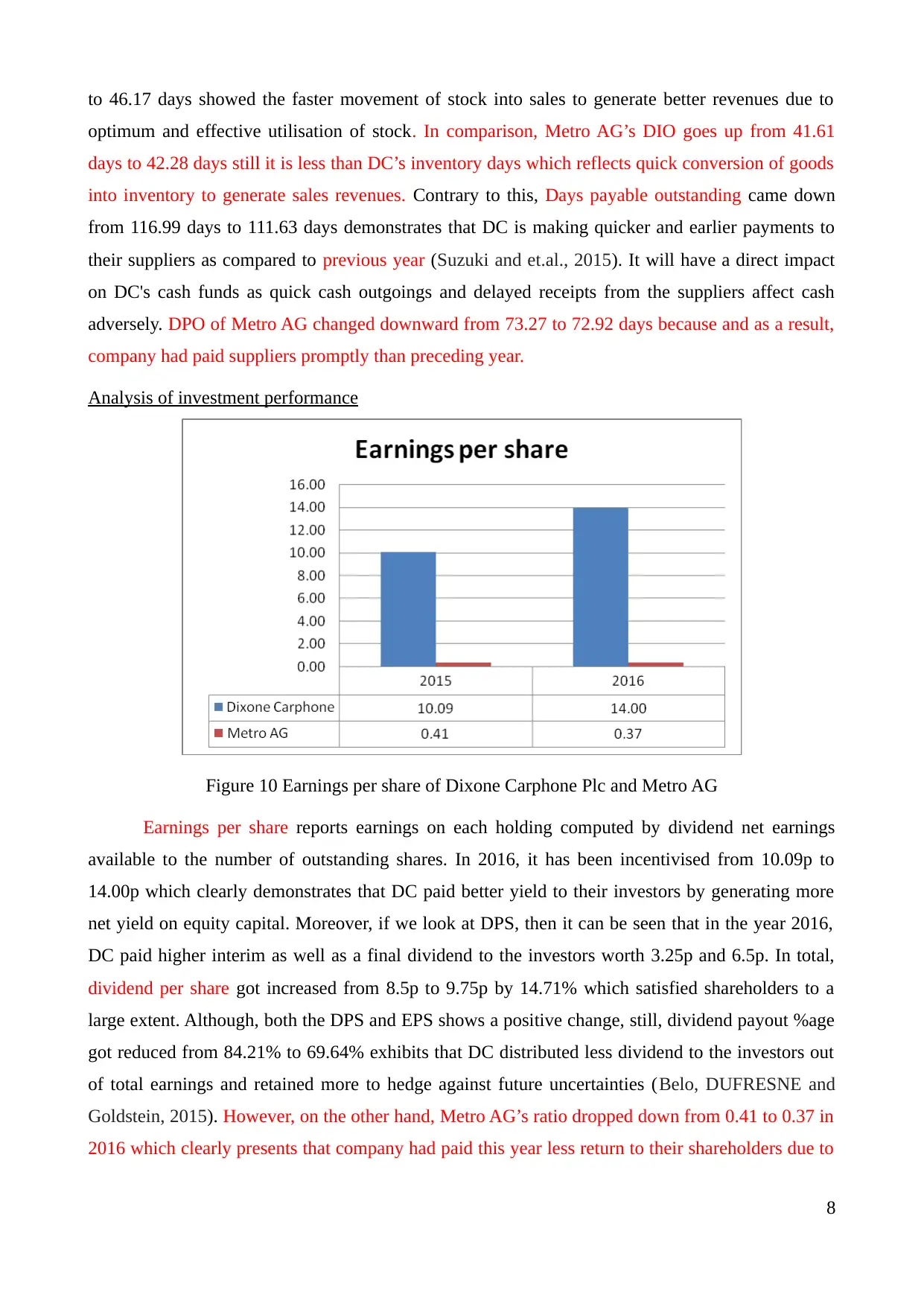

Analysis of investment performance

Figure 10 Earnings per share of Dixone Carphone Plc and Metro AG

Earnings per share reports earnings on each holding computed by dividend net earnings

available to the number of outstanding shares. In 2016, it has been incentivised from 10.09p to

14.00p which clearly demonstrates that DC paid better yield to their investors by generating more

net yield on equity capital. Moreover, if we look at DPS, then it can be seen that in the year 2016,

DC paid higher interim as well as a final dividend to the investors worth 3.25p and 6.5p. In total,

dividend per share got increased from 8.5p to 9.75p by 14.71% which satisfied shareholders to a

large extent. Although, both the DPS and EPS shows a positive change, still, dividend payout %age

got reduced from 84.21% to 69.64% exhibits that DC distributed less dividend to the investors out

of total earnings and retained more to hedge against future uncertainties (Belo, DUFRESNE and

Goldstein, 2015). However, on the other hand, Metro AG’s ratio dropped down from 0.41 to 0.37 in

2016 which clearly presents that company had paid this year less return to their shareholders due to

8

optimum and effective utilisation of stock. In comparison, Metro AG’s DIO goes up from 41.61

days to 42.28 days still it is less than DC’s inventory days which reflects quick conversion of goods

into inventory to generate sales revenues. Contrary to this, Days payable outstanding came down

from 116.99 days to 111.63 days demonstrates that DC is making quicker and earlier payments to

their suppliers as compared to previous year (Suzuki and et.al., 2015). It will have a direct impact

on DC's cash funds as quick cash outgoings and delayed receipts from the suppliers affect cash

adversely. DPO of Metro AG changed downward from 73.27 to 72.92 days because and as a result,

company had paid suppliers promptly than preceding year.

Analysis of investment performance

Figure 10 Earnings per share of Dixone Carphone Plc and Metro AG

Earnings per share reports earnings on each holding computed by dividend net earnings

available to the number of outstanding shares. In 2016, it has been incentivised from 10.09p to

14.00p which clearly demonstrates that DC paid better yield to their investors by generating more

net yield on equity capital. Moreover, if we look at DPS, then it can be seen that in the year 2016,

DC paid higher interim as well as a final dividend to the investors worth 3.25p and 6.5p. In total,

dividend per share got increased from 8.5p to 9.75p by 14.71% which satisfied shareholders to a

large extent. Although, both the DPS and EPS shows a positive change, still, dividend payout %age

got reduced from 84.21% to 69.64% exhibits that DC distributed less dividend to the investors out

of total earnings and retained more to hedge against future uncertainties (Belo, DUFRESNE and

Goldstein, 2015). However, on the other hand, Metro AG’s ratio dropped down from 0.41 to 0.37 in

2016 which clearly presents that company had paid this year less return to their shareholders due to

8

declined in net earnings.

CAPITAL STRUCTURE THEORY

Corporate finance deals with the gathering and collection of long-term capital. Dixons

Carphone Plc runs operations at multinational level, henceforth; it often needs long-term capital to

sustain in the competitive age. There are two sources of finance available to the firm that are debt

and equity capital. In such respect, on the fixed capital, DC is accountable to pay fixed cost in

return for the money collected or supplied by the debt holders such as long-term borrowings and

loans from the bank and financial institutions (Wang and Brand, 2015). However, on the other side,

on equity, also called fluctuating capital, there is no liability to pay a fixed monetary return timely.

It is because; on the money invested in the form of equity capital, although DC will need to pay a

dividend, still, the rate of dividend is not fixed. Moreover, a firm does not have any legal

compulsion to pay a specified rate of dividend as financial cost to shareholders.

There are different theories of capital structure such as a net income theory, net operating

income theory, and traditional approach and Modigliani-miller approach, discussed here as under:

Net income theory:

This theory stated that change in the composition or mix of debt and equity bring changes in

the cost of capital and corporate value. The reason behind this is debt is cheaper and less costly

source, hence, by making the use of debt; DC will be able to reduce a cost of capital through fewer

taxation obligations, which in turn, result in the higher value of the firm.

Net operating income theory:

This theory is just adverse to that of net income theory as it believes that whatever mix of

debt and equity company uses no impacts on weighted average have cost of capital and value of the

firm. It is because; it considered firm as a whole by discounting at a standard rate that is irrelevant

to the debt-equity mix (Barberis and et.al., 2015).

Traditional theory:

This theory defined optimum capital structure at where the cost of capital is minimum and

value of the firm is highest. As per the theory, companies must use debt to a specified limit so as to

reduce their overall cost of capital. However, if debt capital are raised beyond that point, then it

gives rises to the financial burden and risk, which in turn, equity investors also expects higher

dividend results in higher cost of capital. Therefore, by making use of debt capital to a certain limit,

cost of capital can be reduced by lowering tax obligations and result in enhanced value (Bodea and

Hicks, 2015).

Modigliani-Miller approach;

9

CAPITAL STRUCTURE THEORY

Corporate finance deals with the gathering and collection of long-term capital. Dixons

Carphone Plc runs operations at multinational level, henceforth; it often needs long-term capital to

sustain in the competitive age. There are two sources of finance available to the firm that are debt

and equity capital. In such respect, on the fixed capital, DC is accountable to pay fixed cost in

return for the money collected or supplied by the debt holders such as long-term borrowings and

loans from the bank and financial institutions (Wang and Brand, 2015). However, on the other side,

on equity, also called fluctuating capital, there is no liability to pay a fixed monetary return timely.

It is because; on the money invested in the form of equity capital, although DC will need to pay a

dividend, still, the rate of dividend is not fixed. Moreover, a firm does not have any legal

compulsion to pay a specified rate of dividend as financial cost to shareholders.

There are different theories of capital structure such as a net income theory, net operating

income theory, and traditional approach and Modigliani-miller approach, discussed here as under:

Net income theory:

This theory stated that change in the composition or mix of debt and equity bring changes in

the cost of capital and corporate value. The reason behind this is debt is cheaper and less costly

source, hence, by making the use of debt; DC will be able to reduce a cost of capital through fewer

taxation obligations, which in turn, result in the higher value of the firm.

Net operating income theory:

This theory is just adverse to that of net income theory as it believes that whatever mix of

debt and equity company uses no impacts on weighted average have cost of capital and value of the

firm. It is because; it considered firm as a whole by discounting at a standard rate that is irrelevant

to the debt-equity mix (Barberis and et.al., 2015).

Traditional theory:

This theory defined optimum capital structure at where the cost of capital is minimum and

value of the firm is highest. As per the theory, companies must use debt to a specified limit so as to

reduce their overall cost of capital. However, if debt capital are raised beyond that point, then it

gives rises to the financial burden and risk, which in turn, equity investors also expects higher

dividend results in higher cost of capital. Therefore, by making use of debt capital to a certain limit,

cost of capital can be reduced by lowering tax obligations and result in enhanced value (Bodea and

Hicks, 2015).

Modigliani-Miller approach;

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.