Project Evaluation Using Different Methods

VerifiedAdded on 2020/05/08

|8

|960

|125

AI Summary

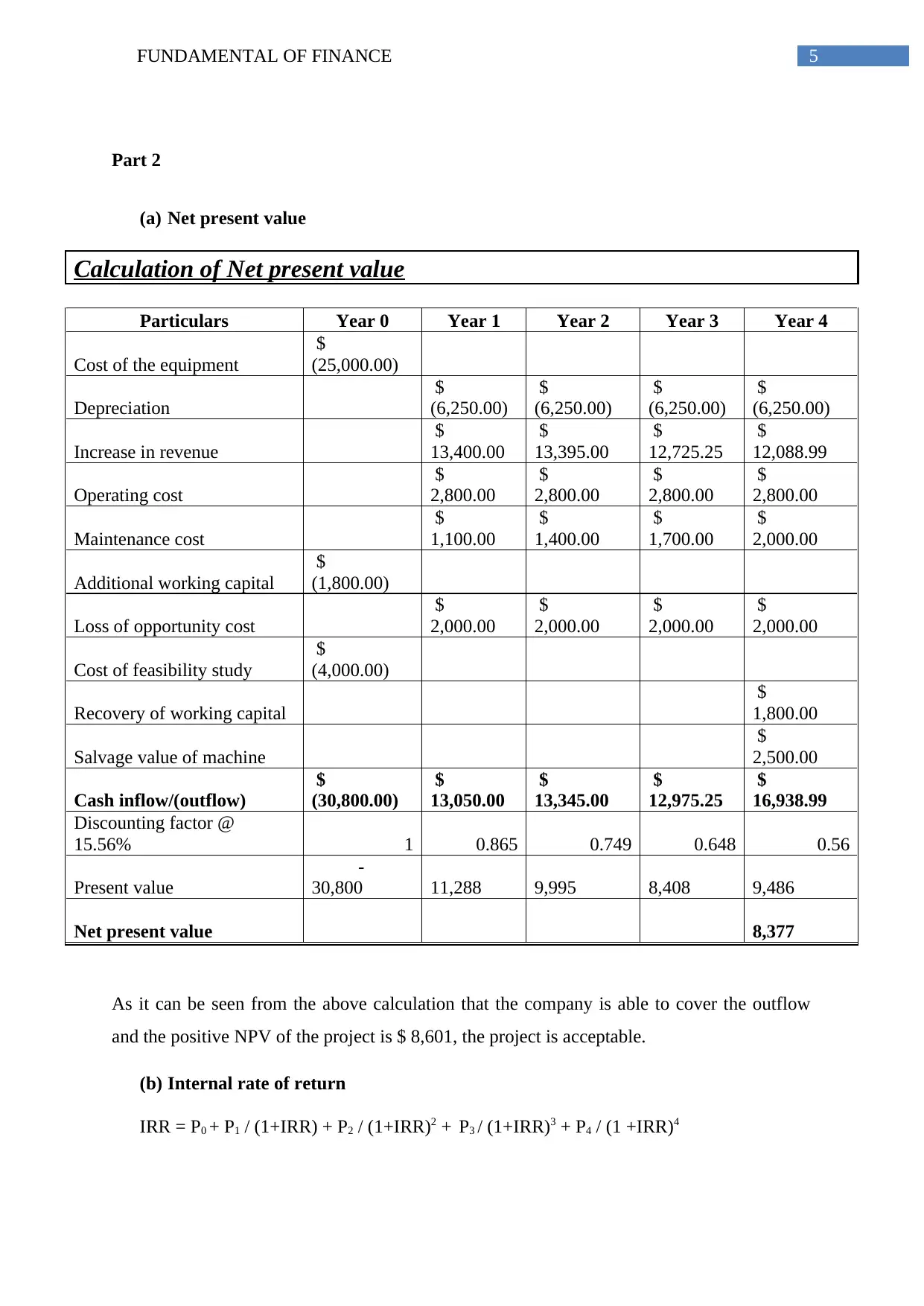

This assignment presents a case study where a company is considering investing in a new machine. The student is tasked with evaluating the project's feasibility using three common methods: Net Present Value (NPV), Internal Rate of Return (IRR), and Payback Period. The analysis involves calculating these financial metrics, comparing them to the required rate of return, and ultimately making a recommendation on whether to accept or reject the project. The assignment emphasizes understanding the strengths and limitations of each method in decision-making.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.