Financial Regulation in China and UK

VerifiedAdded on 2020/03/16

|21

|4539

|215

AI Summary

This assignment requires a comparative analysis of financial regulation frameworks in China and the UK. It delves into the historical development, key regulatory bodies, specific policies, and their influence on market stability, firm performance, and overall economic growth. The analysis should also consider the challenges and opportunities presented by global trends in financial regulation and explore areas of convergence and divergence between the two systems.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

INTERNATIONAL TRADE, FINANCE AND INVESTMENT

International trade, finance and investment

Name of the Student:

Name of the University:

Author Note:

International trade, finance and investment

Name of the Student:

Name of the University:

Author Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

INTERNATIONAL TRADE, FINANCE AND INVESTMENT

Executive Summary:

The report is prepared for demonstrating the evaluation of allocation of capital within domestic

and international economy. Domestic economy that has been selected for analyzing the

allocation of capital is United Kingdom. On other hand, emerging economy that has been

selected for analysis of capital allocation is China. For the purpose of analysis, application of

trade theories has been explained that forms the basis for international trade. Several aspects that

have taken into account for the explanation of capital allocation are financial instruments,

borrowings, and stock exchange and government policies. Furthermore, the challenges faced by

emerging country due to industrialization and trade policies have also been demonstrated.

Executive Summary:

The report is prepared for demonstrating the evaluation of allocation of capital within domestic

and international economy. Domestic economy that has been selected for analyzing the

allocation of capital is United Kingdom. On other hand, emerging economy that has been

selected for analysis of capital allocation is China. For the purpose of analysis, application of

trade theories has been explained that forms the basis for international trade. Several aspects that

have taken into account for the explanation of capital allocation are financial instruments,

borrowings, and stock exchange and government policies. Furthermore, the challenges faced by

emerging country due to industrialization and trade policies have also been demonstrated.

INTERNATIONAL TRADE, FINANCE AND INVESTMENT

Table of Contents

Background of financial markets:....................................................................................................4

Capital allocation within domestic economy (United Kingdom):...................................................6

Capital allocation within international markets:............................................................................11

Evaluation of emerging economy (China):....................................................................................12

Critical evaluation of challenges that country faces due to industrialization and trade policies:..14

Conclusion:....................................................................................................................................15

Reference lists:...............................................................................................................................17

Table of Contents

Background of financial markets:....................................................................................................4

Capital allocation within domestic economy (United Kingdom):...................................................6

Capital allocation within international markets:............................................................................11

Evaluation of emerging economy (China):....................................................................................12

Critical evaluation of challenges that country faces due to industrialization and trade policies:..14

Conclusion:....................................................................................................................................15

Reference lists:...............................................................................................................................17

INTERNATIONAL TRADE, FINANCE AND INVESTMENT

Background of financial markets:

Financial market is a place where investors make trading of commodities, financial

securities and value at lower cost of transaction. The channel of financial market helps in brining

funding to business without investment opportunities that helps in improving economy

efficiencies. Segments of financial market comprise of direct and indirect finance. In segment of

direct financing, funds are directly borrowed from lenders by borrowers by selling financial

instruments in the financial market. In segment of indirect finance, funds are borrowed indirectly

from lenders via the financial intermediaries by issuance of financial instruments that are

claimed on future income and assets of borrowers. Large magnitude is involved in global

financial market that reflects investor’s desire for making global investment and diversification

creation (Liu et al. 2015).

Several regulators enhance financial stability in the financial market in the global

financial system. Apex bank at domestic and international level in respective economies plays a

crucial in regulating the mechanism of financial market. Supervision and regulation of banking

system in different countries are the main activities of apex banks that ensures soundness and

safety of banking system (James and Quaglia 2017). Moreover, the banking institutions protect

credit rights of investors as they play a considerable role in nation’s payment system and

depository institutions.

Mechanism of financial market:

Mechanism of financial market is the system, structure and conventions that exist for

trading of shares and facilitating the issue. International; financial market has several elements

Background of financial markets:

Financial market is a place where investors make trading of commodities, financial

securities and value at lower cost of transaction. The channel of financial market helps in brining

funding to business without investment opportunities that helps in improving economy

efficiencies. Segments of financial market comprise of direct and indirect finance. In segment of

direct financing, funds are directly borrowed from lenders by borrowers by selling financial

instruments in the financial market. In segment of indirect finance, funds are borrowed indirectly

from lenders via the financial intermediaries by issuance of financial instruments that are

claimed on future income and assets of borrowers. Large magnitude is involved in global

financial market that reflects investor’s desire for making global investment and diversification

creation (Liu et al. 2015).

Several regulators enhance financial stability in the financial market in the global

financial system. Apex bank at domestic and international level in respective economies plays a

crucial in regulating the mechanism of financial market. Supervision and regulation of banking

system in different countries are the main activities of apex banks that ensures soundness and

safety of banking system (James and Quaglia 2017). Moreover, the banking institutions protect

credit rights of investors as they play a considerable role in nation’s payment system and

depository institutions.

Mechanism of financial market:

Mechanism of financial market is the system, structure and conventions that exist for

trading of shares and facilitating the issue. International; financial market has several elements

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

INTERNATIONAL TRADE, FINANCE AND INVESTMENT

such as financial institutions, securities market, international currency market, international debt

market, department of foreign exchange and currency exchange.

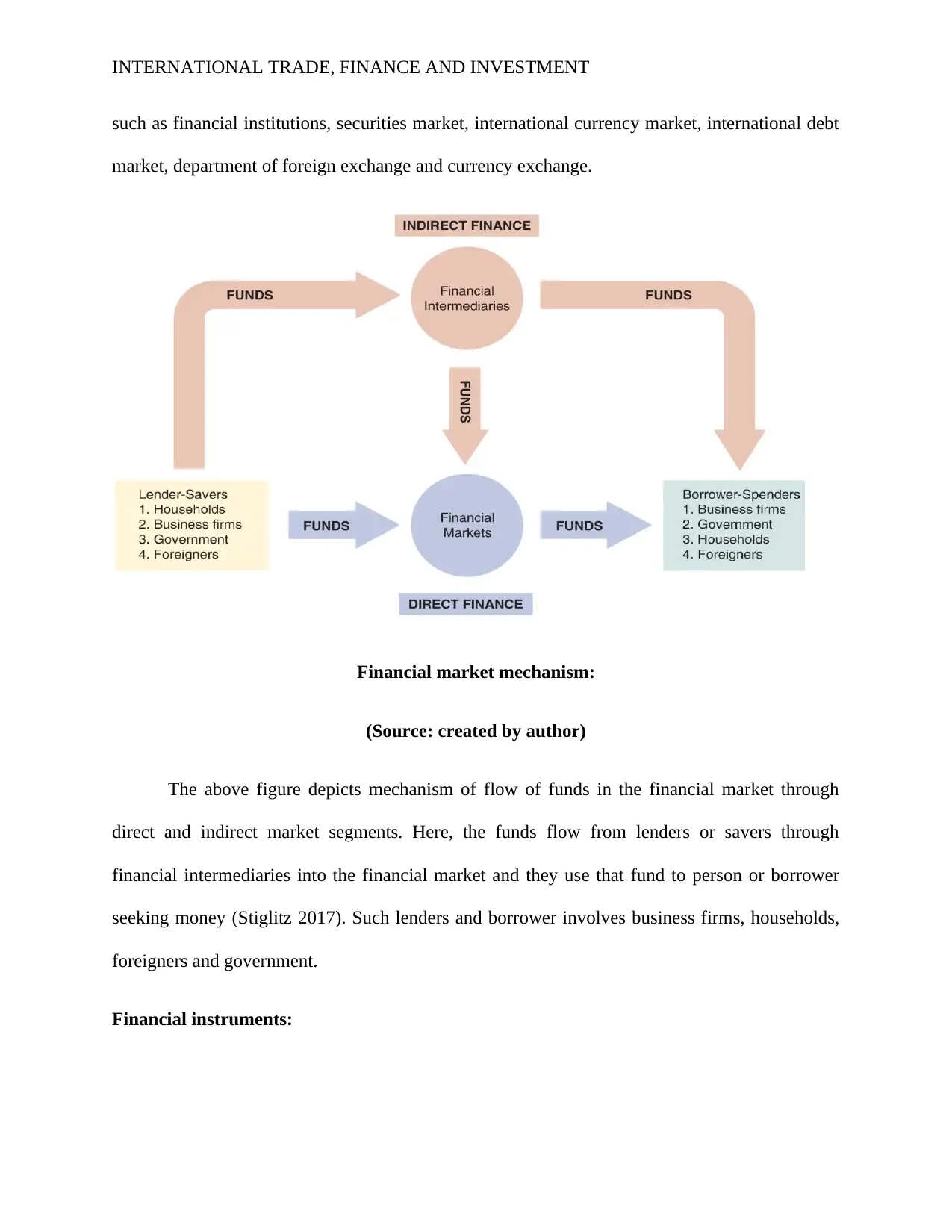

Financial market mechanism:

(Source: created by author)

The above figure depicts mechanism of flow of funds in the financial market through

direct and indirect market segments. Here, the funds flow from lenders or savers through

financial intermediaries into the financial market and they use that fund to person or borrower

seeking money (Stiglitz 2017). Such lenders and borrower involves business firms, households,

foreigners and government.

Financial instruments:

such as financial institutions, securities market, international currency market, international debt

market, department of foreign exchange and currency exchange.

Financial market mechanism:

(Source: created by author)

The above figure depicts mechanism of flow of funds in the financial market through

direct and indirect market segments. Here, the funds flow from lenders or savers through

financial intermediaries into the financial market and they use that fund to person or borrower

seeking money (Stiglitz 2017). Such lenders and borrower involves business firms, households,

foreigners and government.

Financial instruments:

INTERNATIONAL TRADE, FINANCE AND INVESTMENT

Many exchanges such as spot market, forward market and future market dominate the

international capital market. Different countries have different stock exchanges that facilitate

exchange of money and trading of securities. Some of the stock exchanges are London stock

exchange, New York stock exchange, Shanghai stock exchange and National stock exchange.

Over the counter and securities is one of the financial instruments that comprise of

treasury bills, stock and bonds. Instruments that are included in the over the counter derivatives

are interest rate swaps, forward rate agreements (Shankar 2015).

Cash instruments- Cash instruments are transferred readily and value of such

instruments are directly derive from market. Loans, receivables, financial assets, stock options

and deposits are some of the cash instruments (Perera et al. 2016).

Derivative instruments- Derivative are the financial instruments that derive value from

underlying entities such as index, interest rate and assets. Derivative contracts comprise of

future, forward, swaps, option that are regarded as arrangement of payment exchange or bilateral

contracts.

Capital allocation within domestic economy (United Kindgom):

UK financial sector is one of the largest financial service centers in London and European

Union. Financial market of country helps in facilitating capital allocation within the country.

Moreover, in the present economy situation, the extent of state ownership and capital allocation

efficiency is negatively related. On other hand, there exist positive relationship between capital

allocation efficiency and firm specific information in returns from domestic stock of country.

Thereafter, the legal protection of minority investors has positive correlation when the capital is

efficiently allocated. This in turn assist declining industries in countries to curb the over

Many exchanges such as spot market, forward market and future market dominate the

international capital market. Different countries have different stock exchanges that facilitate

exchange of money and trading of securities. Some of the stock exchanges are London stock

exchange, New York stock exchange, Shanghai stock exchange and National stock exchange.

Over the counter and securities is one of the financial instruments that comprise of

treasury bills, stock and bonds. Instruments that are included in the over the counter derivatives

are interest rate swaps, forward rate agreements (Shankar 2015).

Cash instruments- Cash instruments are transferred readily and value of such

instruments are directly derive from market. Loans, receivables, financial assets, stock options

and deposits are some of the cash instruments (Perera et al. 2016).

Derivative instruments- Derivative are the financial instruments that derive value from

underlying entities such as index, interest rate and assets. Derivative contracts comprise of

future, forward, swaps, option that are regarded as arrangement of payment exchange or bilateral

contracts.

Capital allocation within domestic economy (United Kindgom):

UK financial sector is one of the largest financial service centers in London and European

Union. Financial market of country helps in facilitating capital allocation within the country.

Moreover, in the present economy situation, the extent of state ownership and capital allocation

efficiency is negatively related. On other hand, there exist positive relationship between capital

allocation efficiency and firm specific information in returns from domestic stock of country.

Thereafter, the legal protection of minority investors has positive correlation when the capital is

efficiently allocated. This in turn assist declining industries in countries to curb the over

INTERNATIONAL TRADE, FINANCE AND INVESTMENT

investment made with the help of strong minority investors. There are three ways by which

capital allocation within the economy is improved. Firstly, capital allocation is improved by

declining ownership of state (Shen and Lei 2015). Secondly, countries have less synchronicity in

stock price if specific information are impounded into the stock price (Quitzow 2015). Lastly,

investor’s strong minority rights are associated with allocating capital in a better way.

In UK, one of the large markets for capital allocation is asset management. Asset

management industry is one of the crucial intermediaries in the country’s financial system and

such channel is facilitated because of underlying connection between investments and service of

clients. Assets managers are actively involved in efficiently pooling the savings and allocating

the capital. However, asset managers in channeling of capital for private and public companies

play fewer roles.

Several financial activities sought by majority of UK households are provided by assets

management firms and such activities involves provision of investment vehicles, diversification

of portfolio, wide range of asset class and formulation of investment strategies. Asset managers

run the investment vehicle that helps in diversification of portfolio and enabling investors to

invest in wide assets range.

Occupational and personal pensions are the most common form of financial wealth

ownership, which comprise of direct securities ownership and defined contribution schemes.

Importance of asset managers in UK is growing over time due to prevalence of private pension

funds. Wealth distribution of society is influenced by existing variations in financial assets size.

investment made with the help of strong minority investors. There are three ways by which

capital allocation within the economy is improved. Firstly, capital allocation is improved by

declining ownership of state (Shen and Lei 2015). Secondly, countries have less synchronicity in

stock price if specific information are impounded into the stock price (Quitzow 2015). Lastly,

investor’s strong minority rights are associated with allocating capital in a better way.

In UK, one of the large markets for capital allocation is asset management. Asset

management industry is one of the crucial intermediaries in the country’s financial system and

such channel is facilitated because of underlying connection between investments and service of

clients. Assets managers are actively involved in efficiently pooling the savings and allocating

the capital. However, asset managers in channeling of capital for private and public companies

play fewer roles.

Several financial activities sought by majority of UK households are provided by assets

management firms and such activities involves provision of investment vehicles, diversification

of portfolio, wide range of asset class and formulation of investment strategies. Asset managers

run the investment vehicle that helps in diversification of portfolio and enabling investors to

invest in wide assets range.

Occupational and personal pensions are the most common form of financial wealth

ownership, which comprise of direct securities ownership and defined contribution schemes.

Importance of asset managers in UK is growing over time due to prevalence of private pension

funds. Wealth distribution of society is influenced by existing variations in financial assets size.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNATIONAL TRADE, FINANCE AND INVESTMENT

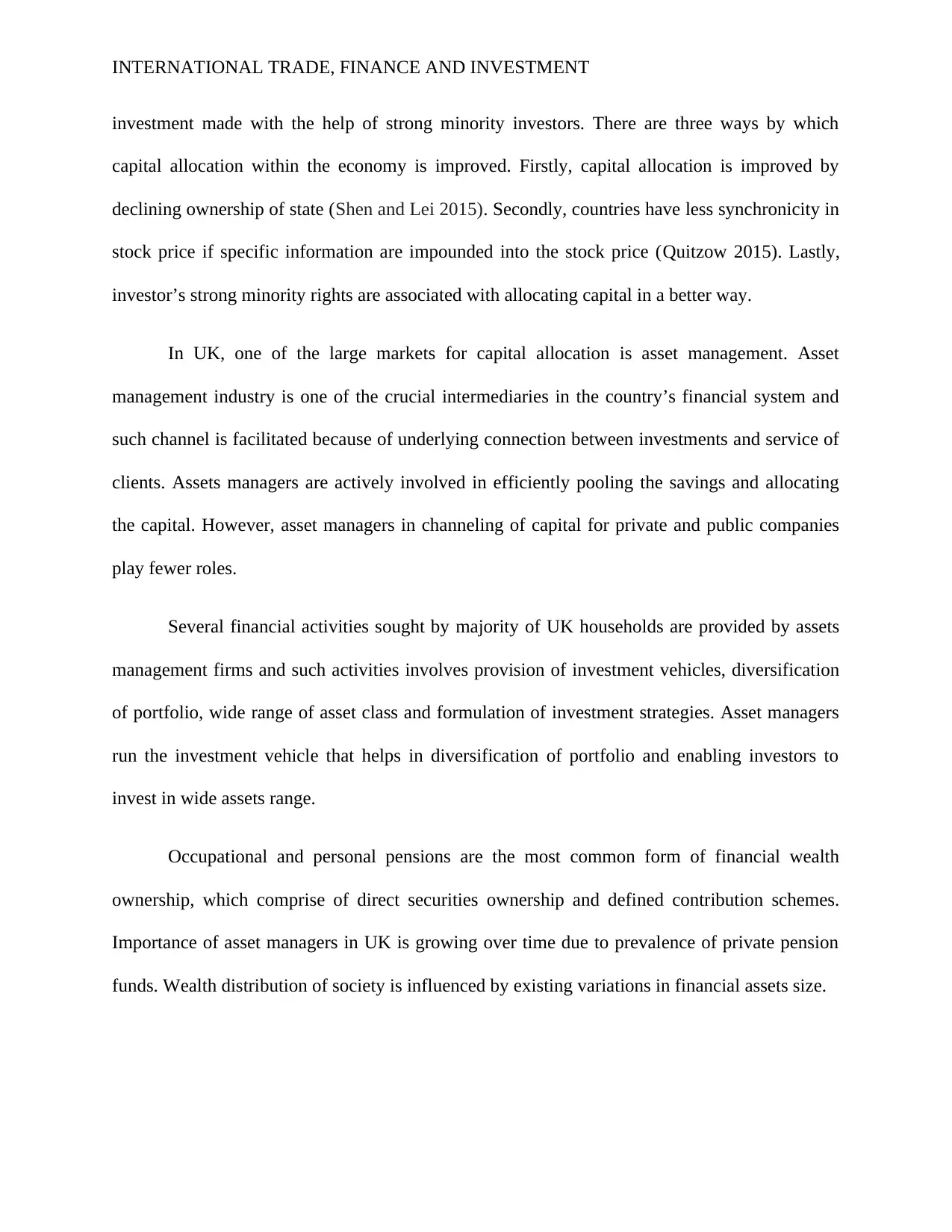

Financial assets ownership by UK households:

(Source: theinvestmentassociation.org 2018)

Profit potential players and risks- Money market activities help in distribution of

liquidity that Bank of England supplies. However, it is not required to recourse the facilities

provided by Bank of England liquidity distribution by market participants. In stressing situations,

it might be difficult to manage the trading positions because of market liquidity and unevenness

of order flows. Moreover, the management of foreign exchange market of pound sterling did not

require any sort of official intervention in recent years. In some extreme circumstances, the

channel of contagion is provided by the interbank system of money market of country. Existing

banking relationship of UK helps in enhancing management of risk settlement. UK is seeking to

resolve the issues faced by London clearinghouse due to its growing importance in the financial

market of world because the intraday risk is threatening the integrity of clearing house.

Borrowing- The apex bank of UK that is bank of England is responsible for

strengthening the financial position of all commercial banks in light of rapid growth in

borrowing from households and business such as personal loans, credit cards and car financing.

Lending conditions in the financial market of country is facilitated and consumer credits have

Financial assets ownership by UK households:

(Source: theinvestmentassociation.org 2018)

Profit potential players and risks- Money market activities help in distribution of

liquidity that Bank of England supplies. However, it is not required to recourse the facilities

provided by Bank of England liquidity distribution by market participants. In stressing situations,

it might be difficult to manage the trading positions because of market liquidity and unevenness

of order flows. Moreover, the management of foreign exchange market of pound sterling did not

require any sort of official intervention in recent years. In some extreme circumstances, the

channel of contagion is provided by the interbank system of money market of country. Existing

banking relationship of UK helps in enhancing management of risk settlement. UK is seeking to

resolve the issues faced by London clearinghouse due to its growing importance in the financial

market of world because the intraday risk is threatening the integrity of clearing house.

Borrowing- The apex bank of UK that is bank of England is responsible for

strengthening the financial position of all commercial banks in light of rapid growth in

borrowing from households and business such as personal loans, credit cards and car financing.

Lending conditions in the financial market of country is facilitated and consumer credits have

INTERNATIONAL TRADE, FINANCE AND INVESTMENT

witnessed rapid growth. In the upcoming year, it is expected that total amount of borrowings will

increase and net debt of government as proportion of gross domestic product of country is

increasing.

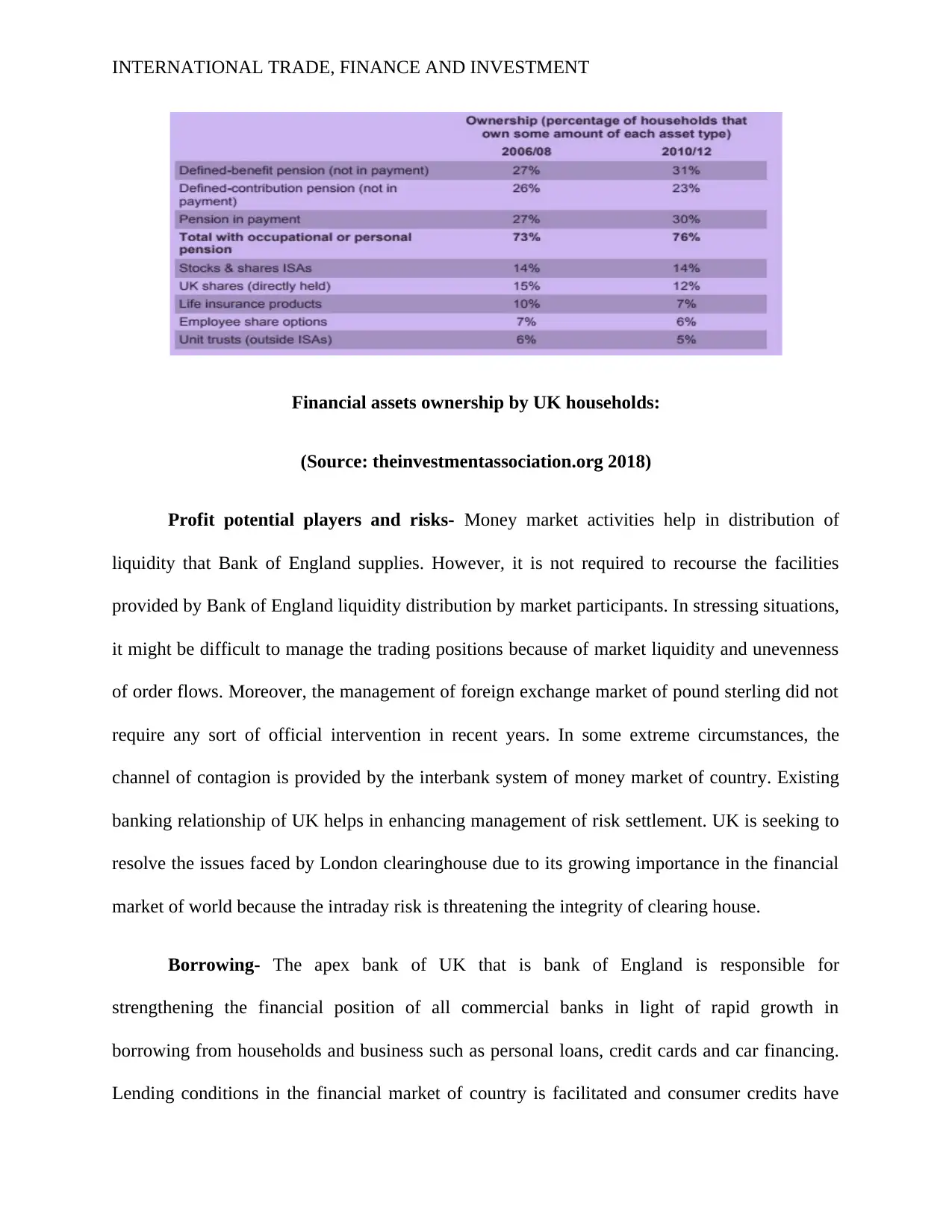

Net borrowing in UK:

(Source: Un.org 2018)

The elasticity of industrial investment to value added in developed and advanced

countries like United Kingdom is several times higher than underdeveloped countries. Despite

the pressure related to Brexit, United Kingdom has remained a hub for economic activity. The

testament to the economy of UK and resilience of sterling comes from dramatic turnaround in

the Great Britain pound fortunes. In fiscal year 2014, UK economy was best performing with a

growth rate of 3.1% and the growth slipped to 1% in year 2018 (Guidi et al. 2016). However,

there exist degrees of short-term profits in the UK despite this negative performance.

witnessed rapid growth. In the upcoming year, it is expected that total amount of borrowings will

increase and net debt of government as proportion of gross domestic product of country is

increasing.

Net borrowing in UK:

(Source: Un.org 2018)

The elasticity of industrial investment to value added in developed and advanced

countries like United Kingdom is several times higher than underdeveloped countries. Despite

the pressure related to Brexit, United Kingdom has remained a hub for economic activity. The

testament to the economy of UK and resilience of sterling comes from dramatic turnaround in

the Great Britain pound fortunes. In fiscal year 2014, UK economy was best performing with a

growth rate of 3.1% and the growth slipped to 1% in year 2018 (Guidi et al. 2016). However,

there exist degrees of short-term profits in the UK despite this negative performance.

INTERNATIONAL TRADE, FINANCE AND INVESTMENT

Fiscal policy of UK Government- Government of UK has taken several steps for

boosting economic activities and there has been a shift to fiscal policy from monetary policy.

Fiscal measures such as cutting down tax expenditure and increased spending on part of

government helps in stimulation of economic growth. Fiscal policies is the efforts taken by

government in the form of changing the aggregate demand level and altering demand

compositions that helps in achieving desirable macro and micro economic activities. Fiscal

policy intends to promote stabilization in economic growth, avoiding boom and bust in economic

cycle and checking level of inflation. Government is able to increase aggregate demand in the

economy by employing expansionary fiscal policy that is done by increasing expenditure and

cutting down of taxes. UK government employs deflationary fiscal policy on other hand by

lowering spending and increasing tax charged for decreasing overall demand in the economy.

Stock exchange- London stock exchange is one of the oldest stock exchanges that was

formed more than three hundred years ago and is situated in the city of London. Stock market

provides platform to investors for trading securities and buying and selling of stocks of listed

companies. There is primary and secondary capital market, in the former market, public does the

listing of shares for the first time. On other hand, secondary market is a platform for trading

listed companies security (Dhingra et al. 2016).

Investment- London financial exchange plays an influential role in intermediation of

funds and securities for both domestic and international investors. Debt and equity market in UK

have to cope up with several changes relating to accounting and investment rules. There have

been some development in financial market of country that has affected future regulations and

such changes involves consolidation of securities regulators and an approach of supervising

Fiscal policy of UK Government- Government of UK has taken several steps for

boosting economic activities and there has been a shift to fiscal policy from monetary policy.

Fiscal measures such as cutting down tax expenditure and increased spending on part of

government helps in stimulation of economic growth. Fiscal policies is the efforts taken by

government in the form of changing the aggregate demand level and altering demand

compositions that helps in achieving desirable macro and micro economic activities. Fiscal

policy intends to promote stabilization in economic growth, avoiding boom and bust in economic

cycle and checking level of inflation. Government is able to increase aggregate demand in the

economy by employing expansionary fiscal policy that is done by increasing expenditure and

cutting down of taxes. UK government employs deflationary fiscal policy on other hand by

lowering spending and increasing tax charged for decreasing overall demand in the economy.

Stock exchange- London stock exchange is one of the oldest stock exchanges that was

formed more than three hundred years ago and is situated in the city of London. Stock market

provides platform to investors for trading securities and buying and selling of stocks of listed

companies. There is primary and secondary capital market, in the former market, public does the

listing of shares for the first time. On other hand, secondary market is a platform for trading

listed companies security (Dhingra et al. 2016).

Investment- London financial exchange plays an influential role in intermediation of

funds and securities for both domestic and international investors. Debt and equity market in UK

have to cope up with several changes relating to accounting and investment rules. There have

been some development in financial market of country that has affected future regulations and

such changes involves consolidation of securities regulators and an approach of supervising

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

INTERNATIONAL TRADE, FINANCE AND INVESTMENT

based on risks. Global financial marketing activities ongoing in London do not affect the stability

of financial market of UK (Elliott et al. 2015).

Capital allocation within international markets:

Several trade theories exists for explaining the allocation of capital in the international

economies and the main reason attributable for countries engaging in trade is that economic

disadvantage in prediction and goods and service. Engaging in trade for sourcing such products

from other countries will incur lower cost on part of exporting countries. International trade

theories comes with the nation that when transactions can be done at lower costs, then companies

intend to develop their own internal market. Some of international theories that can be explained

in this regard involve theory of comparative advantage, factor proportion theory and classical

trade theory. As per the theory of comparative advantage, countries focus on industry that has

largest comparative advantage for boosting economic growth. This theory forms the rationale

free trade agreements among nations and addresses the reasons why trade protectionism should

not be given importance. As per classical theory, the trading nations form the basis of extent of

importing and exporting and countries produce goods and services in which they have

competitive advantage. Products having economic disadvantage should be imported by countries

and the basis of international trade basis is difference in resource endowment and production

characteristics. However, this theory does not explain causes of difference in relative advantage.

Factor proportion theory helps in explaining the difference that is exhibited between trading

countries. Countries import goods that require scare factor of production and export goods that

harness large amount of goods and services.

In recent years, cross border flow of capital between countries have witnessed

considerable increase. Developed as well as developed countries have increasing dependence

based on risks. Global financial marketing activities ongoing in London do not affect the stability

of financial market of UK (Elliott et al. 2015).

Capital allocation within international markets:

Several trade theories exists for explaining the allocation of capital in the international

economies and the main reason attributable for countries engaging in trade is that economic

disadvantage in prediction and goods and service. Engaging in trade for sourcing such products

from other countries will incur lower cost on part of exporting countries. International trade

theories comes with the nation that when transactions can be done at lower costs, then companies

intend to develop their own internal market. Some of international theories that can be explained

in this regard involve theory of comparative advantage, factor proportion theory and classical

trade theory. As per the theory of comparative advantage, countries focus on industry that has

largest comparative advantage for boosting economic growth. This theory forms the rationale

free trade agreements among nations and addresses the reasons why trade protectionism should

not be given importance. As per classical theory, the trading nations form the basis of extent of

importing and exporting and countries produce goods and services in which they have

competitive advantage. Products having economic disadvantage should be imported by countries

and the basis of international trade basis is difference in resource endowment and production

characteristics. However, this theory does not explain causes of difference in relative advantage.

Factor proportion theory helps in explaining the difference that is exhibited between trading

countries. Countries import goods that require scare factor of production and export goods that

harness large amount of goods and services.

In recent years, cross border flow of capital between countries have witnessed

considerable increase. Developed as well as developed countries have increasing dependence

INTERNATIONAL TRADE, FINANCE AND INVESTMENT

upon international investors for receiving finance. Developed countries investors have

inclination of making investment in emerging companies bonds. Proportion of investors basing

capital allocation on the financial returns generated comprises of 47% after it takes into account

risk and synergies (Zhou et al. 2015).

Evaluation of emerging economy (China):

SWOT analysis of China’s financial market:

Strength-

Overall efficiency of financial system can be enhanced due to proper allocation of capital.

Financial system performs an outstanding job for mobilization of savings.

Shifting of funding to production private enterprise has helped in improving operations

for attracting source of finance.

Economy of China is witnessing booming period that would assist in development of

overall financial system (Du and Lai 2018).

Weakness-

The banking system of China is responsible for poor allocation of capital and they have a

number of weaknesses in their operations.

High financial intermediation cost and existence of large volume of nonperforming loans

(Sun and Davidson 2015).

Underdeveloped bond and equity market of China.

Opportunities-

upon international investors for receiving finance. Developed countries investors have

inclination of making investment in emerging companies bonds. Proportion of investors basing

capital allocation on the financial returns generated comprises of 47% after it takes into account

risk and synergies (Zhou et al. 2015).

Evaluation of emerging economy (China):

SWOT analysis of China’s financial market:

Strength-

Overall efficiency of financial system can be enhanced due to proper allocation of capital.

Financial system performs an outstanding job for mobilization of savings.

Shifting of funding to production private enterprise has helped in improving operations

for attracting source of finance.

Economy of China is witnessing booming period that would assist in development of

overall financial system (Du and Lai 2018).

Weakness-

The banking system of China is responsible for poor allocation of capital and they have a

number of weaknesses in their operations.

High financial intermediation cost and existence of large volume of nonperforming loans

(Sun and Davidson 2015).

Underdeveloped bond and equity market of China.

Opportunities-

INTERNATIONAL TRADE, FINANCE AND INVESTMENT

There can be better choice of funding vehicles due resulting from development of bond

and equity market.

Implementation of system wide and coordinated programs has the scope of strengthening

financial system.

Threats-

Banks are likely to lose corporate customers due to increasing competitiveness of

financial system of different economies and countries.

Inappropriate regulations existence would not lead to development of corporate equity

and bond market.

The financial system of China performs an outstanding task of mobilizing savings, and at

the same time, there is a considerable room for improvement and increasing overall efficiency of

capital allocation. Reforms in the financial system of China have helped in raising value of gross

domestic product by $ 320 billion a year and spreading wealth throughout the country (Allen and

Gu 2015). A shift in funding by regulators of China towards more productive process could help

in accelerating lay off from state owned enterprise that are less productive. This shift will help in

creation of strong job opportunities and increasing revenue generated from taxation. The overall

lower productivity in China has resulted from the lending pattern that is attributable to explaining

large volume of loans that are non-performing in the banking system of China. It has resulted in

declining efficiency of investment in country (Dermody et al. 2015).

Stock market- Allocation of capital in the stock market is poor and the efficiency of

stock market is reflected by function of capital allocation. The dominance of banking sector in

the financial system of China helps in amplifying by the poor capital allocation. China witness

There can be better choice of funding vehicles due resulting from development of bond

and equity market.

Implementation of system wide and coordinated programs has the scope of strengthening

financial system.

Threats-

Banks are likely to lose corporate customers due to increasing competitiveness of

financial system of different economies and countries.

Inappropriate regulations existence would not lead to development of corporate equity

and bond market.

The financial system of China performs an outstanding task of mobilizing savings, and at

the same time, there is a considerable room for improvement and increasing overall efficiency of

capital allocation. Reforms in the financial system of China have helped in raising value of gross

domestic product by $ 320 billion a year and spreading wealth throughout the country (Allen and

Gu 2015). A shift in funding by regulators of China towards more productive process could help

in accelerating lay off from state owned enterprise that are less productive. This shift will help in

creation of strong job opportunities and increasing revenue generated from taxation. The overall

lower productivity in China has resulted from the lending pattern that is attributable to explaining

large volume of loans that are non-performing in the banking system of China. It has resulted in

declining efficiency of investment in country (Dermody et al. 2015).

Stock market- Allocation of capital in the stock market is poor and the efficiency of

stock market is reflected by function of capital allocation. The dominance of banking sector in

the financial system of China helps in amplifying by the poor capital allocation. China witness

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNATIONAL TRADE, FINANCE AND INVESTMENT

mismatch and considerable wastage of capital that led to inefficient capital allocation. The stock

market is not efficient in allocating the functioning of capital that has consequence of capital

inefficiency. If the allocation of funds were done to more productive private enterprises, this

would help in boosting the productivity. In order to attract the finance, operations of less

productive enterprise should be improved. This effort would help in closing the productivity gap

between private and state owned companies. Better capital allocation will help in benefitting the

household of China by generating higher return on savings (Cowling et al. 2015).

Poor allocation of capital by banks and high cost of financial intermediation has resulted

in dismissing of return of bank deposits. Compared to other countries, the earnings on financial

assets of China have been declining. Country would be provided with ample benefits in the light

of efficient allocation of capital and despite this fact; changes have been resistance on part of

Chinese regulators for job preserving and stability maintenance. The factor that is detrimental to

the financial system of country is underdeveloped equity and debt market along with inefficient

banking system operations. Bond, debt and equity market in China is smallest at global level and

corporate market bond represents only 1% of total value of gross domestic product when

compared to other emerging economies (Arouri et al. 2015). An improvement in efficiency of

equity market of China would help in reducing issuance cost of company. Moreover, capital

markets of China are fewer for financing larger private enterprise and are suitable only for small

enterprises. Slow development of corporate bond market in China is because of existence of

inappropriate regulations. Restricted flow of capital and excessive regulations of country has

been the reason attributable to holding back the growth of institutional investor’s growth

(Carpenter et al. 2015). Therefore, it is required by China to fully develop their equity and bond

market.

mismatch and considerable wastage of capital that led to inefficient capital allocation. The stock

market is not efficient in allocating the functioning of capital that has consequence of capital

inefficiency. If the allocation of funds were done to more productive private enterprises, this

would help in boosting the productivity. In order to attract the finance, operations of less

productive enterprise should be improved. This effort would help in closing the productivity gap

between private and state owned companies. Better capital allocation will help in benefitting the

household of China by generating higher return on savings (Cowling et al. 2015).

Poor allocation of capital by banks and high cost of financial intermediation has resulted

in dismissing of return of bank deposits. Compared to other countries, the earnings on financial

assets of China have been declining. Country would be provided with ample benefits in the light

of efficient allocation of capital and despite this fact; changes have been resistance on part of

Chinese regulators for job preserving and stability maintenance. The factor that is detrimental to

the financial system of country is underdeveloped equity and debt market along with inefficient

banking system operations. Bond, debt and equity market in China is smallest at global level and

corporate market bond represents only 1% of total value of gross domestic product when

compared to other emerging economies (Arouri et al. 2015). An improvement in efficiency of

equity market of China would help in reducing issuance cost of company. Moreover, capital

markets of China are fewer for financing larger private enterprise and are suitable only for small

enterprises. Slow development of corporate bond market in China is because of existence of

inappropriate regulations. Restricted flow of capital and excessive regulations of country has

been the reason attributable to holding back the growth of institutional investor’s growth

(Carpenter et al. 2015). Therefore, it is required by China to fully develop their equity and bond

market.

INTERNATIONAL TRADE, FINANCE AND INVESTMENT

Development of country and planning and managing of national economy is the explicit

responsibility of Chinese government. Various direct and indirect mechanisms are used by

government for implementation of economic policies and plan. Allocating supply of goods and

services and physical output designation is the direct control that is exercised by government.

While indirect mechanism involves undertaking of marketing initiatives and settlement process

such as monitoring and controlling of financial transactions, levying taxes, controlling allocation

of scare resources such as chemical fertilizers, skilled labors, steel and electronic power (Deng

and Macve 2017).

GDP growth rate of China:

(Source: Deng and Macve 2017)

In China, foreign trade supervision is the responsibility trade bank of China, ministry of

foreign economic relations, banking system and general administration of custom.

Development of country and planning and managing of national economy is the explicit

responsibility of Chinese government. Various direct and indirect mechanisms are used by

government for implementation of economic policies and plan. Allocating supply of goods and

services and physical output designation is the direct control that is exercised by government.

While indirect mechanism involves undertaking of marketing initiatives and settlement process

such as monitoring and controlling of financial transactions, levying taxes, controlling allocation

of scare resources such as chemical fertilizers, skilled labors, steel and electronic power (Deng

and Macve 2017).

GDP growth rate of China:

(Source: Deng and Macve 2017)

In China, foreign trade supervision is the responsibility trade bank of China, ministry of

foreign economic relations, banking system and general administration of custom.

INTERNATIONAL TRADE, FINANCE AND INVESTMENT

Critical evaluation of challenges that country faces due to industrialization and trade

policies:

Poor allocation of capital in the stock market of China is one of the challenges that

would be faced by country. Returns of bank deposit are dismal due to higher cost of financial

intermediation and poor allocation of capital by banks. Lending practice in country is influenced

by political pressures rudimentary financial system. Underdeveloped state of debt and equity

market and inefficient operation of banking system some other challenges. Banks incur higher

operation cost in light of inefficiencies. It is required by banks to raise their operational

efficiency to the benchmark that would help in annual reduction of operation cost. For providing

competitions to bank, Chinese companies are required to develop bond and equity market so that

they are provide with funding vehicles in a better way (Broadstock and Filis 2014). Moreover,

Chinese government is required to strengthen dialogue and cooperation in this area for healthy

intellectual property development. Restricted controlling of capital, usage of restricted measures

and trade development model transition is another challenge faced by trading industry in China.

It is required to dismantle discretionary regulatory reforms in association with several services of

cross border supply. Another demanding challenge is witnessed in foreign interest such as

institutionalized world and international collective actions (Beltratti et al. 2016).

Conclusion:

The report prepared above demonstrates the financial markets of developed country,

United Kingdom and developing countries such as China. From the analysis several facts

discussed above, it can be inferred that capital allocation of China is poor as against efficient

capital allocation of United Kingdom. Better allocation of capital provides investor with several

benefits such as capable of making investment in wide range of assets and wide diversification of

Critical evaluation of challenges that country faces due to industrialization and trade

policies:

Poor allocation of capital in the stock market of China is one of the challenges that

would be faced by country. Returns of bank deposit are dismal due to higher cost of financial

intermediation and poor allocation of capital by banks. Lending practice in country is influenced

by political pressures rudimentary financial system. Underdeveloped state of debt and equity

market and inefficient operation of banking system some other challenges. Banks incur higher

operation cost in light of inefficiencies. It is required by banks to raise their operational

efficiency to the benchmark that would help in annual reduction of operation cost. For providing

competitions to bank, Chinese companies are required to develop bond and equity market so that

they are provide with funding vehicles in a better way (Broadstock and Filis 2014). Moreover,

Chinese government is required to strengthen dialogue and cooperation in this area for healthy

intellectual property development. Restricted controlling of capital, usage of restricted measures

and trade development model transition is another challenge faced by trading industry in China.

It is required to dismantle discretionary regulatory reforms in association with several services of

cross border supply. Another demanding challenge is witnessed in foreign interest such as

institutionalized world and international collective actions (Beltratti et al. 2016).

Conclusion:

The report prepared above demonstrates the financial markets of developed country,

United Kingdom and developing countries such as China. From the analysis several facts

discussed above, it can be inferred that capital allocation of China is poor as against efficient

capital allocation of United Kingdom. Better allocation of capital provides investor with several

benefits such as capable of making investment in wide range of assets and wide diversification of

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

INTERNATIONAL TRADE, FINANCE AND INVESTMENT

portfolio. It is deduced from evaluation of financial market of respective countries that allocation

of capital in the stock market of China is poor and the capital is not changed by stock market

although stocks provide higher return. Nevertheless, in terms of capital allocation, several

challenges are faced by Chinese economy. In this regard, Chinese government is required to

enhance bond and capital market through development of policy and strict control of capital.

Therefore, the overall financial system of China should be strengthening for facilitating the

allocation of capital and elevating domestic investor’s growth.

portfolio. It is deduced from evaluation of financial market of respective countries that allocation

of capital in the stock market of China is poor and the capital is not changed by stock market

although stocks provide higher return. Nevertheless, in terms of capital allocation, several

challenges are faced by Chinese economy. In this regard, Chinese government is required to

enhance bond and capital market through development of policy and strict control of capital.

Therefore, the overall financial system of China should be strengthening for facilitating the

allocation of capital and elevating domestic investor’s growth.

INTERNATIONAL TRADE, FINANCE AND INVESTMENT

Reference lists:

Allen, F. and Gu, X., 2015. China's financial system: growth and risk. Foundations and Trends®

in Finance, 9(3–4), pp.197-319.

Arouri, M.E.H., Lahiani, A. and Nguyen, D.K., 2015. World gold prices and stock returns in

China: insights for hedging and diversification strategies. Economic Modelling, 44, pp.273-282.

Beltratti, A., Bortolotti, B. and Caccavaio, M., 2016. Stock market efficiency in China: evidence

from the split-share reform. The Quarterly Review of Economics and Finance, 60, pp.125-137.

Blanchard, O. and Giavazzi, F., 2016. Rebalancing growth in China: A three-handed approach.

In SEEKING CHANGES: The Economic Development in Contemporary China (pp. 49-84).

Broadstock, D.C. and Filis, G., 2014. Oil price shocks and stock market returns: New evidence

from the United States and China. Journal of International Financial Markets, Institutions and

Money, 33, pp.417-433.

Carpenter, J.N., Lu, F. and Whitelaw, R.F., 2015. The real value of China's stock market (No.

w20957). National Bureau of Economic Research.

Cowling, M., Liu, W., Ledger, A. and Zhang, N., 2015. What really happens to small and

medium-sized enterprises in a global economic recession? UK evidence on sales and job

dynamics. International Small Business Journal, 33(5), pp.488-513.

Deng, S. and Macve, R.H., 2017. Perspectives from Mainland China, Hong Kong and the UK on

the Potential Future Roles of China's Auditing Firms in the Global Profession.

Reference lists:

Allen, F. and Gu, X., 2015. China's financial system: growth and risk. Foundations and Trends®

in Finance, 9(3–4), pp.197-319.

Arouri, M.E.H., Lahiani, A. and Nguyen, D.K., 2015. World gold prices and stock returns in

China: insights for hedging and diversification strategies. Economic Modelling, 44, pp.273-282.

Beltratti, A., Bortolotti, B. and Caccavaio, M., 2016. Stock market efficiency in China: evidence

from the split-share reform. The Quarterly Review of Economics and Finance, 60, pp.125-137.

Blanchard, O. and Giavazzi, F., 2016. Rebalancing growth in China: A three-handed approach.

In SEEKING CHANGES: The Economic Development in Contemporary China (pp. 49-84).

Broadstock, D.C. and Filis, G., 2014. Oil price shocks and stock market returns: New evidence

from the United States and China. Journal of International Financial Markets, Institutions and

Money, 33, pp.417-433.

Carpenter, J.N., Lu, F. and Whitelaw, R.F., 2015. The real value of China's stock market (No.

w20957). National Bureau of Economic Research.

Cowling, M., Liu, W., Ledger, A. and Zhang, N., 2015. What really happens to small and

medium-sized enterprises in a global economic recession? UK evidence on sales and job

dynamics. International Small Business Journal, 33(5), pp.488-513.

Deng, S. and Macve, R.H., 2017. Perspectives from Mainland China, Hong Kong and the UK on

the Potential Future Roles of China's Auditing Firms in the Global Profession.

INTERNATIONAL TRADE, FINANCE AND INVESTMENT

Dermody, J., Hanmer-Lloyd, S., Koenig-Lewis, N. and Zhao, A.L., 2015. Advancing sustainable

consumption in the UK and China: the mediating effect of pro-environmental self-identity.

Journal of Marketing Management, 31(13-14), pp.1472-1502.

Dhingra, S., Ottaviano, G., Sampson, T. and Van Reenen, J., 2016. The impact of Brexit on

foreign investment in the UK. BREXIT 2016, 24.

Du, X. and Lai, S., 2018. Financial distress, investment opportunity, and the contagion effect of

low audit quality: Evidence from china. Journal of Business Ethics, 147(3), pp.565-593.

Elliott, D., Kroeber, A. and Qiao, Y., 2015. Shadow banking in China: A primer. Brookings

Institution, 13.

Guidi, F., Savva, C.S. and Ugur, M., 2016. Dynamic co-movements and diversification benefits:

The case of the Greater China region, the UK and the US equity markets. Journal of

Multinational Financial Management, 35, pp.59-78.

Huang, S., An, H., Gao, X. and Huang, X., 2015. Identifying the multiscale impacts of crude oil

price shocks on the stock market in China at the sector level. Physica A: Statistical Mechanics

and its Applications, 434, pp.13-24.

James, S. and Quaglia, L., 2017. Why does the United Kingdom (UK) have inconsistent

preferences on financial regulation? The case of banking and capital markets. Journal of Public

Policy, pp.1-24.

Liu, Y., Miletkov, M.K., Wei, Z. and Yang, T., 2015. Board independence and firm performance

in China. Journal of Corporate Finance, 30, pp.223-244.

Dermody, J., Hanmer-Lloyd, S., Koenig-Lewis, N. and Zhao, A.L., 2015. Advancing sustainable

consumption in the UK and China: the mediating effect of pro-environmental self-identity.

Journal of Marketing Management, 31(13-14), pp.1472-1502.

Dhingra, S., Ottaviano, G., Sampson, T. and Van Reenen, J., 2016. The impact of Brexit on

foreign investment in the UK. BREXIT 2016, 24.

Du, X. and Lai, S., 2018. Financial distress, investment opportunity, and the contagion effect of

low audit quality: Evidence from china. Journal of Business Ethics, 147(3), pp.565-593.

Elliott, D., Kroeber, A. and Qiao, Y., 2015. Shadow banking in China: A primer. Brookings

Institution, 13.

Guidi, F., Savva, C.S. and Ugur, M., 2016. Dynamic co-movements and diversification benefits:

The case of the Greater China region, the UK and the US equity markets. Journal of

Multinational Financial Management, 35, pp.59-78.

Huang, S., An, H., Gao, X. and Huang, X., 2015. Identifying the multiscale impacts of crude oil

price shocks on the stock market in China at the sector level. Physica A: Statistical Mechanics

and its Applications, 434, pp.13-24.

James, S. and Quaglia, L., 2017. Why does the United Kingdom (UK) have inconsistent

preferences on financial regulation? The case of banking and capital markets. Journal of Public

Policy, pp.1-24.

Liu, Y., Miletkov, M.K., Wei, Z. and Yang, T., 2015. Board independence and firm performance

in China. Journal of Corporate Finance, 30, pp.223-244.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNATIONAL TRADE, FINANCE AND INVESTMENT

Perera, S., Zhou, L. and Victoria, M.F., 2016. Construction cost and commercial management

system in the UK and China: professional body and business comparison.

Quitzow, R., 2015. Dynamics of a policy-driven market: The co-evolution of technological

innovation systems for solar photovoltaics in China and Germany. Environmental Innovation

and Societal Transitions, 17, pp.126-148.

Shankar, S., 2015. Globalisation, the Global Financial Crisis and the State by John H. Farrar and

David G. Mayes (eds.) 2013. Cheltenham, UK: Edward Elgar Publishing, 304 pages. $135.00,

hardcover.

Shen, G.U. and Lei, C.E.N., 2015. The Construction of Rural Financial Regulation System under

the Concept of Inclusive Regulation. Credit Reference, 12, p.018.

Stiglitz, J.E., 2017. The overselling of globalization. Business Economics, 52(3), pp.129-137.

Sun, Y. and Davidson, I., 2015. Influential factors of online fraud occurrence in retailing banking

sectors from a global prospective: An empirical study of individual customers in the UK and

China. Information & Computer Security, 23(1), pp.3-19.

Theinvestmentassociation.org. (2018). Retrieved 16 March 2018, from

https://www.theinvestmentassociation.org/assets/files/press/2016/The%20contribution%20of

%20asset%20management%20to%20the%20UK%20economy.pdf

Un.org. (2018). [online] Available at:

http://www.un.org/esa/sustdev/publications/industrial_development/full_report.pdf [Accessed 16

March. 2018].

Perera, S., Zhou, L. and Victoria, M.F., 2016. Construction cost and commercial management

system in the UK and China: professional body and business comparison.

Quitzow, R., 2015. Dynamics of a policy-driven market: The co-evolution of technological

innovation systems for solar photovoltaics in China and Germany. Environmental Innovation

and Societal Transitions, 17, pp.126-148.

Shankar, S., 2015. Globalisation, the Global Financial Crisis and the State by John H. Farrar and

David G. Mayes (eds.) 2013. Cheltenham, UK: Edward Elgar Publishing, 304 pages. $135.00,

hardcover.

Shen, G.U. and Lei, C.E.N., 2015. The Construction of Rural Financial Regulation System under

the Concept of Inclusive Regulation. Credit Reference, 12, p.018.

Stiglitz, J.E., 2017. The overselling of globalization. Business Economics, 52(3), pp.129-137.

Sun, Y. and Davidson, I., 2015. Influential factors of online fraud occurrence in retailing banking

sectors from a global prospective: An empirical study of individual customers in the UK and

China. Information & Computer Security, 23(1), pp.3-19.

Theinvestmentassociation.org. (2018). Retrieved 16 March 2018, from

https://www.theinvestmentassociation.org/assets/files/press/2016/The%20contribution%20of

%20asset%20management%20to%20the%20UK%20economy.pdf

Un.org. (2018). [online] Available at:

http://www.un.org/esa/sustdev/publications/industrial_development/full_report.pdf [Accessed 16

March. 2018].

INTERNATIONAL TRADE, FINANCE AND INVESTMENT

Xiong, W., 2018. Risks in China’s financial system (No. 1/2018). Bank of Finland, Institute for

Economies in Transition.

Zhou, B., Guo, J.M., Hua, J. and Doukas, A.J., 2015. Does state ownership drive M&A

performance? Evidence from China. European Financial Management, 21(1), pp.79-105.

Xiong, W., 2018. Risks in China’s financial system (No. 1/2018). Bank of Finland, Institute for

Economies in Transition.

Zhou, B., Guo, J.M., Hua, J. and Doukas, A.J., 2015. Does state ownership drive M&A

performance? Evidence from China. European Financial Management, 21(1), pp.79-105.

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.