Financial Analysis: DuPont Analysis and Budgeting for FluidOne

VerifiedAdded on 2020/10/22

|15

|4974

|232

Report

AI Summary

This report presents a comprehensive financial analysis of FluidOne, focusing on DuPont analysis and budgeting methodologies. Part 1 critically evaluates FluidOne's Return on Equity (ROE) for 2018 and 2017 using ratio analysis, examining profitability, efficiency, and liquidity through metrics like Net Profit Margin, Asset Turnover, and Equity Multiplier. Part 2 provides a critical analysis of the budgeting process and non-financial performance indicators used to improve performance management within the organization, including re-forecasting and variance analysis. The analysis reveals insights into FluidOne's financial health, highlighting the impact of operating efficiency, asset utilization, and financial leverage on its overall financial performance and strategic decision-making.

DU PONT ANALYSIS AND

BUDGETING

BUDGETING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

DuPont Analysis.....................................................................................................................1

FluidOne's DuPont Analysis:.................................................................................................5

PART 2............................................................................................................................................7

Description and Critical Analysis of Fluidone company.......................................................7

Re forecasting Process............................................................................................................9

Variance Analysis...................................................................................................................9

Non Financial Performance Indicators.................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

DuPont Analysis.....................................................................................................................1

FluidOne's DuPont Analysis:.................................................................................................5

PART 2............................................................................................................................................7

Description and Critical Analysis of Fluidone company.......................................................7

Re forecasting Process............................................................................................................9

Variance Analysis...................................................................................................................9

Non Financial Performance Indicators.................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

DuPont Analysis and Budgeting are two financial models that are used by businesses

regularly (Seddon, 2015) . While DuPont Analysis helps to understand the changes in company's

return on equity, Budgeting ensures effective apportionment of organization's available capital to

various expenditure respectively. This report has been divided into two parts viz. Part 1 and Part

2. Part 1 of this report critically evaluates the Return On Equity (ROE) of FluidOne by

comparing its profitability, efficiency and liquidity for 2018 and 2017 using Ratio Analysis. Part

2 provides a critical analysis of budgeting process and non-financial performance indicators that

are used to improve performance management system in the organization.

PART 1

DuPont Analysis

DuPont Analysis is a model that was first propounded by DuPont Corporation. This

framework involved an analysis of fundamental performance variables which covered

profitability, efficiency and liquidity. As per this model, the return on equity of a business is

decomposed to evaluate the individual strengths and weakness of financial performance metrics.

The three main components that drive a company's ROE include operating efficiency, asset-use

efficiency and financial leverage. Therefore, DuPont Analysis is calculated as follows:

DuPont Analysis = Net Profit Margin * Asst Turnover * Equity Multiplier, where

Net Profit Margin denotes as a measuring metric of operating efficiency;

Asset Turnover denotes as a metric measuring asset-use efficiency; and

Equity Multiplier denotes as the financial leverage metric.

In the context of this assessment, a financial analysis of FluidOne's accounts have been

carried out to conduct a DuPont Analysis for the business. These have been shown below:

(a) Operating Efficiency:

One of the first constituent under DuPont Analysis is operating efficiency. Operating

efficiency means profitability. It is taken as an important criteria while decomposing the ROE of

the business since profitability is one of the main objective of any business. Therefore, any

changes made in this regard will affect the Return on Equity too. For this purpose, Net Profit

Margin is calculated to measure the operational efficacy of the business. (Pissard and et.al, 2013)

Net Profit Margin:

1

DuPont Analysis and Budgeting are two financial models that are used by businesses

regularly (Seddon, 2015) . While DuPont Analysis helps to understand the changes in company's

return on equity, Budgeting ensures effective apportionment of organization's available capital to

various expenditure respectively. This report has been divided into two parts viz. Part 1 and Part

2. Part 1 of this report critically evaluates the Return On Equity (ROE) of FluidOne by

comparing its profitability, efficiency and liquidity for 2018 and 2017 using Ratio Analysis. Part

2 provides a critical analysis of budgeting process and non-financial performance indicators that

are used to improve performance management system in the organization.

PART 1

DuPont Analysis

DuPont Analysis is a model that was first propounded by DuPont Corporation. This

framework involved an analysis of fundamental performance variables which covered

profitability, efficiency and liquidity. As per this model, the return on equity of a business is

decomposed to evaluate the individual strengths and weakness of financial performance metrics.

The three main components that drive a company's ROE include operating efficiency, asset-use

efficiency and financial leverage. Therefore, DuPont Analysis is calculated as follows:

DuPont Analysis = Net Profit Margin * Asst Turnover * Equity Multiplier, where

Net Profit Margin denotes as a measuring metric of operating efficiency;

Asset Turnover denotes as a metric measuring asset-use efficiency; and

Equity Multiplier denotes as the financial leverage metric.

In the context of this assessment, a financial analysis of FluidOne's accounts have been

carried out to conduct a DuPont Analysis for the business. These have been shown below:

(a) Operating Efficiency:

One of the first constituent under DuPont Analysis is operating efficiency. Operating

efficiency means profitability. It is taken as an important criteria while decomposing the ROE of

the business since profitability is one of the main objective of any business. Therefore, any

changes made in this regard will affect the Return on Equity too. For this purpose, Net Profit

Margin is calculated to measure the operational efficacy of the business. (Pissard and et.al, 2013)

Net Profit Margin:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

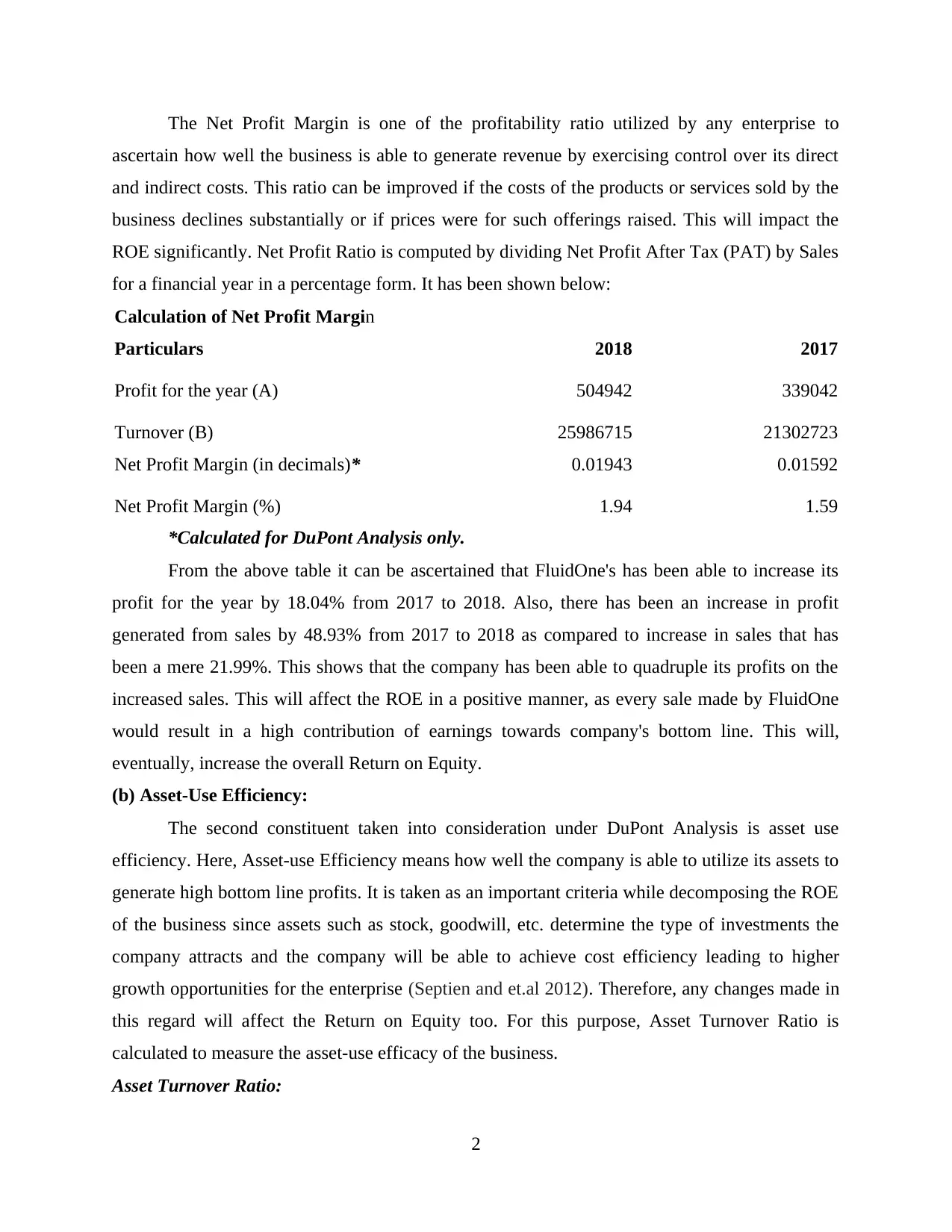

The Net Profit Margin is one of the profitability ratio utilized by any enterprise to

ascertain how well the business is able to generate revenue by exercising control over its direct

and indirect costs. This ratio can be improved if the costs of the products or services sold by the

business declines substantially or if prices were for such offerings raised. This will impact the

ROE significantly. Net Profit Ratio is computed by dividing Net Profit After Tax (PAT) by Sales

for a financial year in a percentage form. It has been shown below:

Calculation of Net Profit Margin

Particulars 2018 2017

Profit for the year (A) 504942 339042

Turnover (B) 25986715 21302723

Net Profit Margin (in decimals)* 0.01943 0.01592

Net Profit Margin (%) 1.94 1.59

*Calculated for DuPont Analysis only.

From the above table it can be ascertained that FluidOne's has been able to increase its

profit for the year by 18.04% from 2017 to 2018. Also, there has been an increase in profit

generated from sales by 48.93% from 2017 to 2018 as compared to increase in sales that has

been a mere 21.99%. This shows that the company has been able to quadruple its profits on the

increased sales. This will affect the ROE in a positive manner, as every sale made by FluidOne

would result in a high contribution of earnings towards company's bottom line. This will,

eventually, increase the overall Return on Equity.

(b) Asset-Use Efficiency:

The second constituent taken into consideration under DuPont Analysis is asset use

efficiency. Here, Asset-use Efficiency means how well the company is able to utilize its assets to

generate high bottom line profits. It is taken as an important criteria while decomposing the ROE

of the business since assets such as stock, goodwill, etc. determine the type of investments the

company attracts and the company will be able to achieve cost efficiency leading to higher

growth opportunities for the enterprise (Septien and et.al 2012). Therefore, any changes made in

this regard will affect the Return on Equity too. For this purpose, Asset Turnover Ratio is

calculated to measure the asset-use efficacy of the business.

Asset Turnover Ratio:

2

ascertain how well the business is able to generate revenue by exercising control over its direct

and indirect costs. This ratio can be improved if the costs of the products or services sold by the

business declines substantially or if prices were for such offerings raised. This will impact the

ROE significantly. Net Profit Ratio is computed by dividing Net Profit After Tax (PAT) by Sales

for a financial year in a percentage form. It has been shown below:

Calculation of Net Profit Margin

Particulars 2018 2017

Profit for the year (A) 504942 339042

Turnover (B) 25986715 21302723

Net Profit Margin (in decimals)* 0.01943 0.01592

Net Profit Margin (%) 1.94 1.59

*Calculated for DuPont Analysis only.

From the above table it can be ascertained that FluidOne's has been able to increase its

profit for the year by 18.04% from 2017 to 2018. Also, there has been an increase in profit

generated from sales by 48.93% from 2017 to 2018 as compared to increase in sales that has

been a mere 21.99%. This shows that the company has been able to quadruple its profits on the

increased sales. This will affect the ROE in a positive manner, as every sale made by FluidOne

would result in a high contribution of earnings towards company's bottom line. This will,

eventually, increase the overall Return on Equity.

(b) Asset-Use Efficiency:

The second constituent taken into consideration under DuPont Analysis is asset use

efficiency. Here, Asset-use Efficiency means how well the company is able to utilize its assets to

generate high bottom line profits. It is taken as an important criteria while decomposing the ROE

of the business since assets such as stock, goodwill, etc. determine the type of investments the

company attracts and the company will be able to achieve cost efficiency leading to higher

growth opportunities for the enterprise (Septien and et.al 2012). Therefore, any changes made in

this regard will affect the Return on Equity too. For this purpose, Asset Turnover Ratio is

calculated to measure the asset-use efficacy of the business.

Asset Turnover Ratio:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

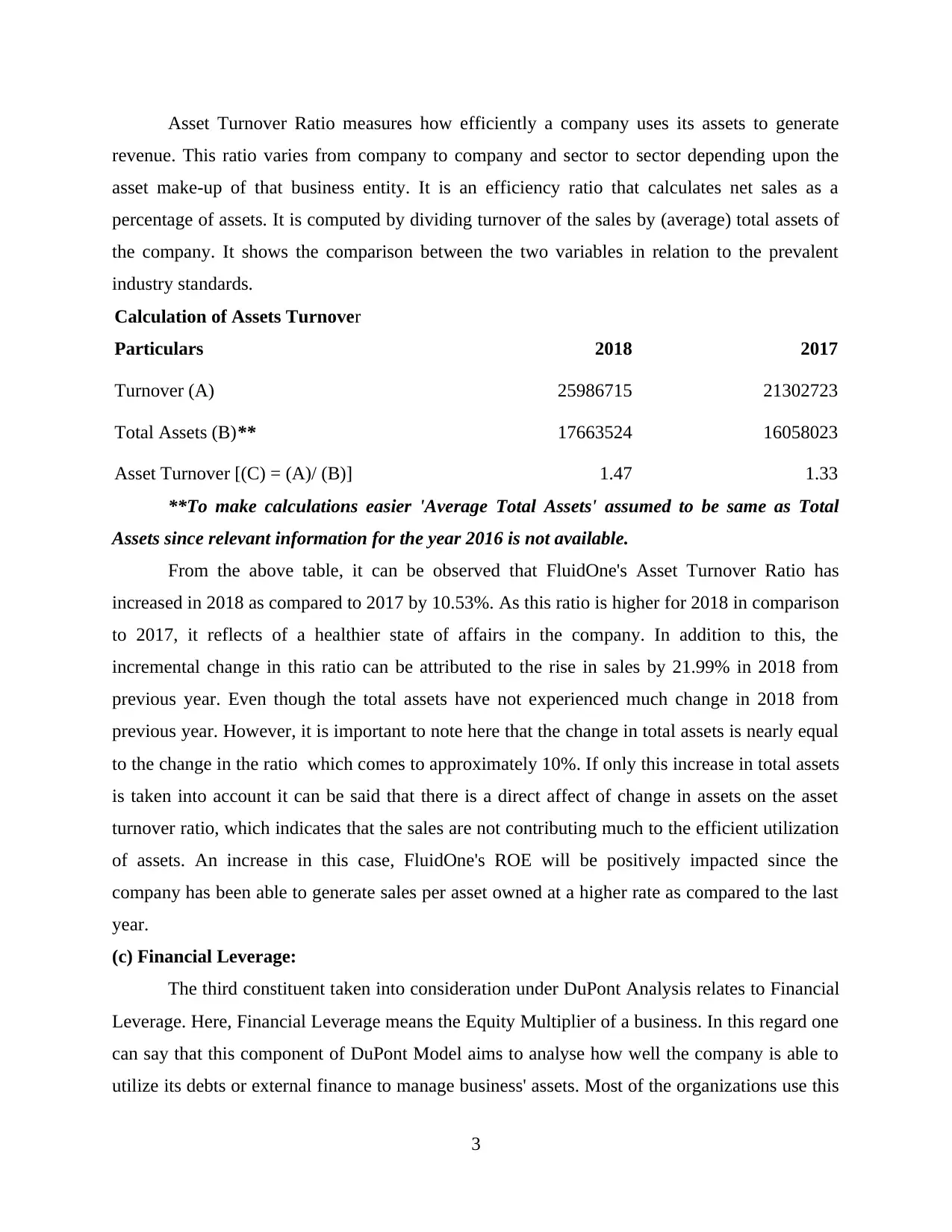

Asset Turnover Ratio measures how efficiently a company uses its assets to generate

revenue. This ratio varies from company to company and sector to sector depending upon the

asset make-up of that business entity. It is an efficiency ratio that calculates net sales as a

percentage of assets. It is computed by dividing turnover of the sales by (average) total assets of

the company. It shows the comparison between the two variables in relation to the prevalent

industry standards.

Calculation of Assets Turnover

Particulars 2018 2017

Turnover (A) 25986715 21302723

Total Assets (B)** 17663524 16058023

Asset Turnover [(C) = (A)/ (B)] 1.47 1.33

**To make calculations easier 'Average Total Assets' assumed to be same as Total

Assets since relevant information for the year 2016 is not available.

From the above table, it can be observed that FluidOne's Asset Turnover Ratio has

increased in 2018 as compared to 2017 by 10.53%. As this ratio is higher for 2018 in comparison

to 2017, it reflects of a healthier state of affairs in the company. In addition to this, the

incremental change in this ratio can be attributed to the rise in sales by 21.99% in 2018 from

previous year. Even though the total assets have not experienced much change in 2018 from

previous year. However, it is important to note here that the change in total assets is nearly equal

to the change in the ratio which comes to approximately 10%. If only this increase in total assets

is taken into account it can be said that there is a direct affect of change in assets on the asset

turnover ratio, which indicates that the sales are not contributing much to the efficient utilization

of assets. An increase in this case, FluidOne's ROE will be positively impacted since the

company has been able to generate sales per asset owned at a higher rate as compared to the last

year.

(c) Financial Leverage:

The third constituent taken into consideration under DuPont Analysis relates to Financial

Leverage. Here, Financial Leverage means the Equity Multiplier of a business. In this regard one

can say that this component of DuPont Model aims to analyse how well the company is able to

utilize its debts or external finance to manage business' assets. Most of the organizations use this

3

revenue. This ratio varies from company to company and sector to sector depending upon the

asset make-up of that business entity. It is an efficiency ratio that calculates net sales as a

percentage of assets. It is computed by dividing turnover of the sales by (average) total assets of

the company. It shows the comparison between the two variables in relation to the prevalent

industry standards.

Calculation of Assets Turnover

Particulars 2018 2017

Turnover (A) 25986715 21302723

Total Assets (B)** 17663524 16058023

Asset Turnover [(C) = (A)/ (B)] 1.47 1.33

**To make calculations easier 'Average Total Assets' assumed to be same as Total

Assets since relevant information for the year 2016 is not available.

From the above table, it can be observed that FluidOne's Asset Turnover Ratio has

increased in 2018 as compared to 2017 by 10.53%. As this ratio is higher for 2018 in comparison

to 2017, it reflects of a healthier state of affairs in the company. In addition to this, the

incremental change in this ratio can be attributed to the rise in sales by 21.99% in 2018 from

previous year. Even though the total assets have not experienced much change in 2018 from

previous year. However, it is important to note here that the change in total assets is nearly equal

to the change in the ratio which comes to approximately 10%. If only this increase in total assets

is taken into account it can be said that there is a direct affect of change in assets on the asset

turnover ratio, which indicates that the sales are not contributing much to the efficient utilization

of assets. An increase in this case, FluidOne's ROE will be positively impacted since the

company has been able to generate sales per asset owned at a higher rate as compared to the last

year.

(c) Financial Leverage:

The third constituent taken into consideration under DuPont Analysis relates to Financial

Leverage. Here, Financial Leverage means the Equity Multiplier of a business. In this regard one

can say that this component of DuPont Model aims to analyse how well the company is able to

utilize its debts or external finance to manage business' assets. Most of the organizations use this

3

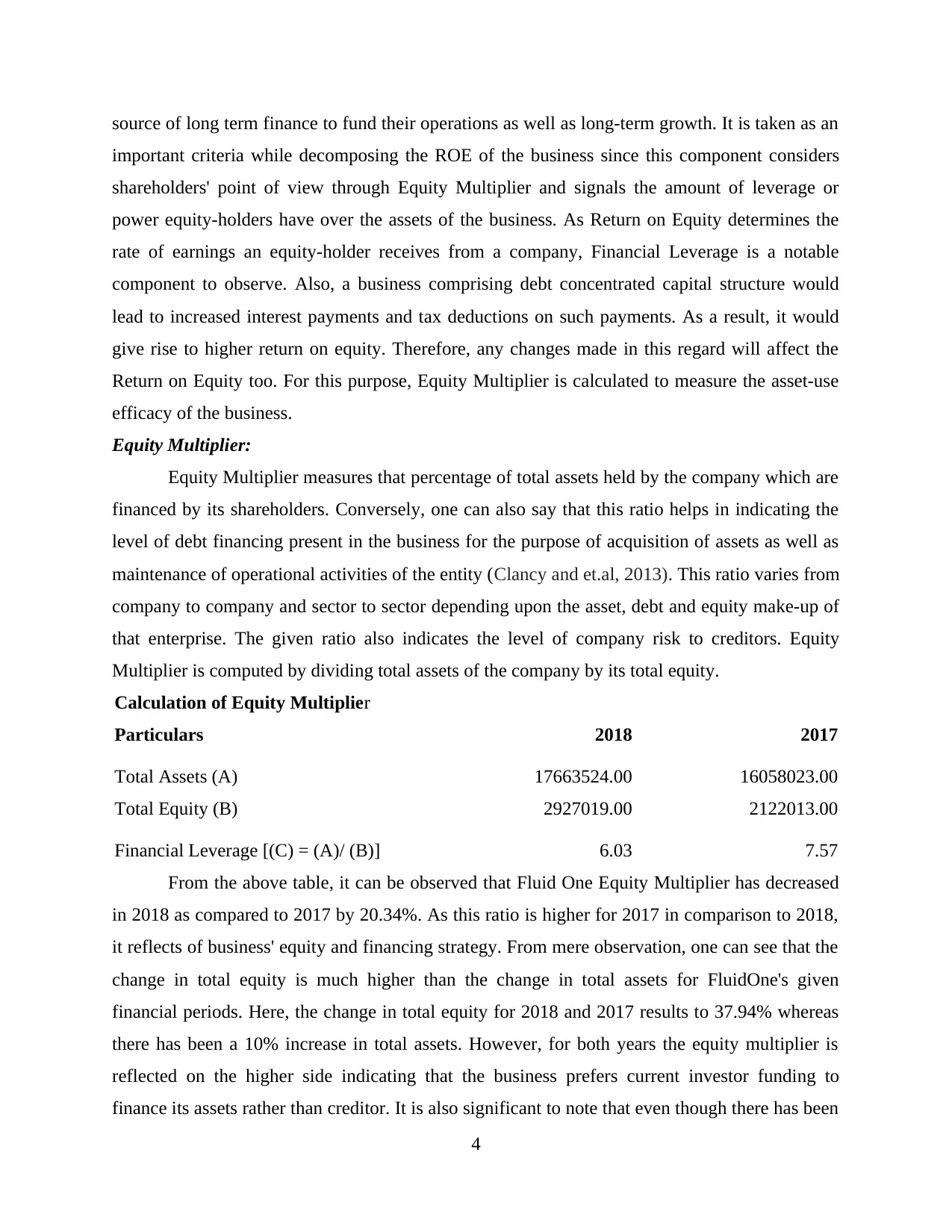

source of long term finance to fund their operations as well as long-term growth. It is taken as an

important criteria while decomposing the ROE of the business since this component considers

shareholders' point of view through Equity Multiplier and signals the amount of leverage or

power equity-holders have over the assets of the business. As Return on Equity determines the

rate of earnings an equity-holder receives from a company, Financial Leverage is a notable

component to observe. Also, a business comprising debt concentrated capital structure would

lead to increased interest payments and tax deductions on such payments. As a result, it would

give rise to higher return on equity. Therefore, any changes made in this regard will affect the

Return on Equity too. For this purpose, Equity Multiplier is calculated to measure the asset-use

efficacy of the business.

Equity Multiplier:

Equity Multiplier measures that percentage of total assets held by the company which are

financed by its shareholders. Conversely, one can also say that this ratio helps in indicating the

level of debt financing present in the business for the purpose of acquisition of assets as well as

maintenance of operational activities of the entity (Clancy and et.al, 2013). This ratio varies from

company to company and sector to sector depending upon the asset, debt and equity make-up of

that enterprise. The given ratio also indicates the level of company risk to creditors. Equity

Multiplier is computed by dividing total assets of the company by its total equity.

Calculation of Equity Multiplier

Particulars 2018 2017

Total Assets (A) 17663524.00 16058023.00

Total Equity (B) 2927019.00 2122013.00

Financial Leverage [(C) = (A)/ (B)] 6.03 7.57

From the above table, it can be observed that Fluid One Equity Multiplier has decreased

in 2018 as compared to 2017 by 20.34%. As this ratio is higher for 2017 in comparison to 2018,

it reflects of business' equity and financing strategy. From mere observation, one can see that the

change in total equity is much higher than the change in total assets for FluidOne's given

financial periods. Here, the change in total equity for 2018 and 2017 results to 37.94% whereas

there has been a 10% increase in total assets. However, for both years the equity multiplier is

reflected on the higher side indicating that the business prefers current investor funding to

finance its assets rather than creditor. It is also significant to note that even though there has been

4

important criteria while decomposing the ROE of the business since this component considers

shareholders' point of view through Equity Multiplier and signals the amount of leverage or

power equity-holders have over the assets of the business. As Return on Equity determines the

rate of earnings an equity-holder receives from a company, Financial Leverage is a notable

component to observe. Also, a business comprising debt concentrated capital structure would

lead to increased interest payments and tax deductions on such payments. As a result, it would

give rise to higher return on equity. Therefore, any changes made in this regard will affect the

Return on Equity too. For this purpose, Equity Multiplier is calculated to measure the asset-use

efficacy of the business.

Equity Multiplier:

Equity Multiplier measures that percentage of total assets held by the company which are

financed by its shareholders. Conversely, one can also say that this ratio helps in indicating the

level of debt financing present in the business for the purpose of acquisition of assets as well as

maintenance of operational activities of the entity (Clancy and et.al, 2013). This ratio varies from

company to company and sector to sector depending upon the asset, debt and equity make-up of

that enterprise. The given ratio also indicates the level of company risk to creditors. Equity

Multiplier is computed by dividing total assets of the company by its total equity.

Calculation of Equity Multiplier

Particulars 2018 2017

Total Assets (A) 17663524.00 16058023.00

Total Equity (B) 2927019.00 2122013.00

Financial Leverage [(C) = (A)/ (B)] 6.03 7.57

From the above table, it can be observed that Fluid One Equity Multiplier has decreased

in 2018 as compared to 2017 by 20.34%. As this ratio is higher for 2017 in comparison to 2018,

it reflects of business' equity and financing strategy. From mere observation, one can see that the

change in total equity is much higher than the change in total assets for FluidOne's given

financial periods. Here, the change in total equity for 2018 and 2017 results to 37.94% whereas

there has been a 10% increase in total assets. However, for both years the equity multiplier is

reflected on the higher side indicating that the business prefers current investor funding to

finance its assets rather than creditor. It is also significant to note that even though there has been

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

an increase in both variables constituting the Equity Multiplier, the company has still

experienced a decrease. A lower multiplier ratio can be attributed to the conservative behaviour

exhibited on the part of FluidOne. Also, it can mean that there has been a substantial decrease in

company's debt servicing costs as well as the overall dependency on debt financing. A decline, in

this case, will negatively impact FluidOne's Return On Equity since the company has not been

able to generate higher financing from its debt and is more reliable towards equity-holder's

funding as compared to the last year.

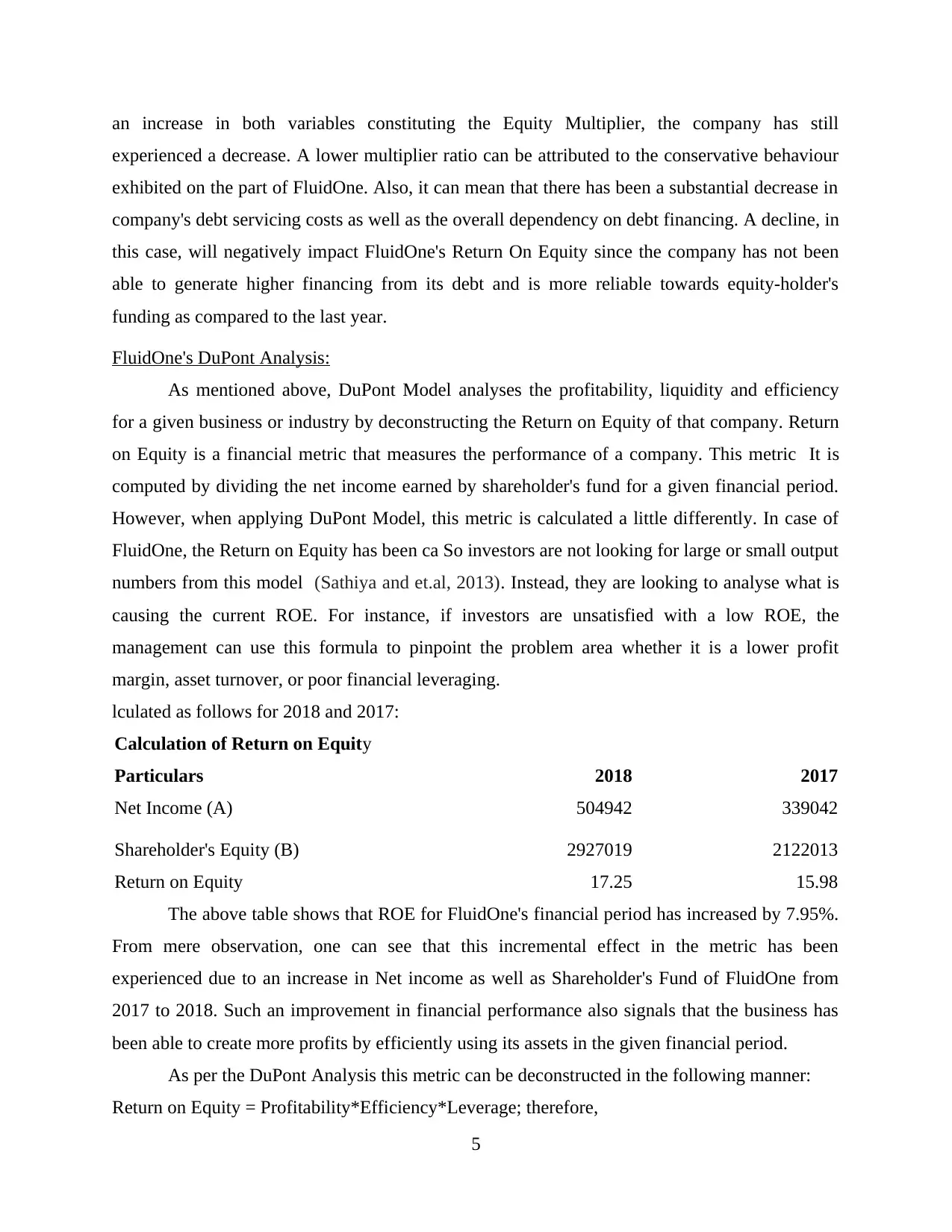

FluidOne's DuPont Analysis:

As mentioned above, DuPont Model analyses the profitability, liquidity and efficiency

for a given business or industry by deconstructing the Return on Equity of that company. Return

on Equity is a financial metric that measures the performance of a company. This metric It is

computed by dividing the net income earned by shareholder's fund for a given financial period.

However, when applying DuPont Model, this metric is calculated a little differently. In case of

FluidOne, the Return on Equity has been ca So investors are not looking for large or small output

numbers from this model (Sathiya and et.al, 2013). Instead, they are looking to analyse what is

causing the current ROE. For instance, if investors are unsatisfied with a low ROE, the

management can use this formula to pinpoint the problem area whether it is a lower profit

margin, asset turnover, or poor financial leveraging.

lculated as follows for 2018 and 2017:

Calculation of Return on Equity

Particulars 2018 2017

Net Income (A) 504942 339042

Shareholder's Equity (B) 2927019 2122013

Return on Equity 17.25 15.98

The above table shows that ROE for FluidOne's financial period has increased by 7.95%.

From mere observation, one can see that this incremental effect in the metric has been

experienced due to an increase in Net income as well as Shareholder's Fund of FluidOne from

2017 to 2018. Such an improvement in financial performance also signals that the business has

been able to create more profits by efficiently using its assets in the given financial period.

As per the DuPont Analysis this metric can be deconstructed in the following manner:

Return on Equity = Profitability*Efficiency*Leverage; therefore,

5

experienced a decrease. A lower multiplier ratio can be attributed to the conservative behaviour

exhibited on the part of FluidOne. Also, it can mean that there has been a substantial decrease in

company's debt servicing costs as well as the overall dependency on debt financing. A decline, in

this case, will negatively impact FluidOne's Return On Equity since the company has not been

able to generate higher financing from its debt and is more reliable towards equity-holder's

funding as compared to the last year.

FluidOne's DuPont Analysis:

As mentioned above, DuPont Model analyses the profitability, liquidity and efficiency

for a given business or industry by deconstructing the Return on Equity of that company. Return

on Equity is a financial metric that measures the performance of a company. This metric It is

computed by dividing the net income earned by shareholder's fund for a given financial period.

However, when applying DuPont Model, this metric is calculated a little differently. In case of

FluidOne, the Return on Equity has been ca So investors are not looking for large or small output

numbers from this model (Sathiya and et.al, 2013). Instead, they are looking to analyse what is

causing the current ROE. For instance, if investors are unsatisfied with a low ROE, the

management can use this formula to pinpoint the problem area whether it is a lower profit

margin, asset turnover, or poor financial leveraging.

lculated as follows for 2018 and 2017:

Calculation of Return on Equity

Particulars 2018 2017

Net Income (A) 504942 339042

Shareholder's Equity (B) 2927019 2122013

Return on Equity 17.25 15.98

The above table shows that ROE for FluidOne's financial period has increased by 7.95%.

From mere observation, one can see that this incremental effect in the metric has been

experienced due to an increase in Net income as well as Shareholder's Fund of FluidOne from

2017 to 2018. Such an improvement in financial performance also signals that the business has

been able to create more profits by efficiently using its assets in the given financial period.

As per the DuPont Analysis this metric can be deconstructed in the following manner:

Return on Equity = Profitability*Efficiency*Leverage; therefore,

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

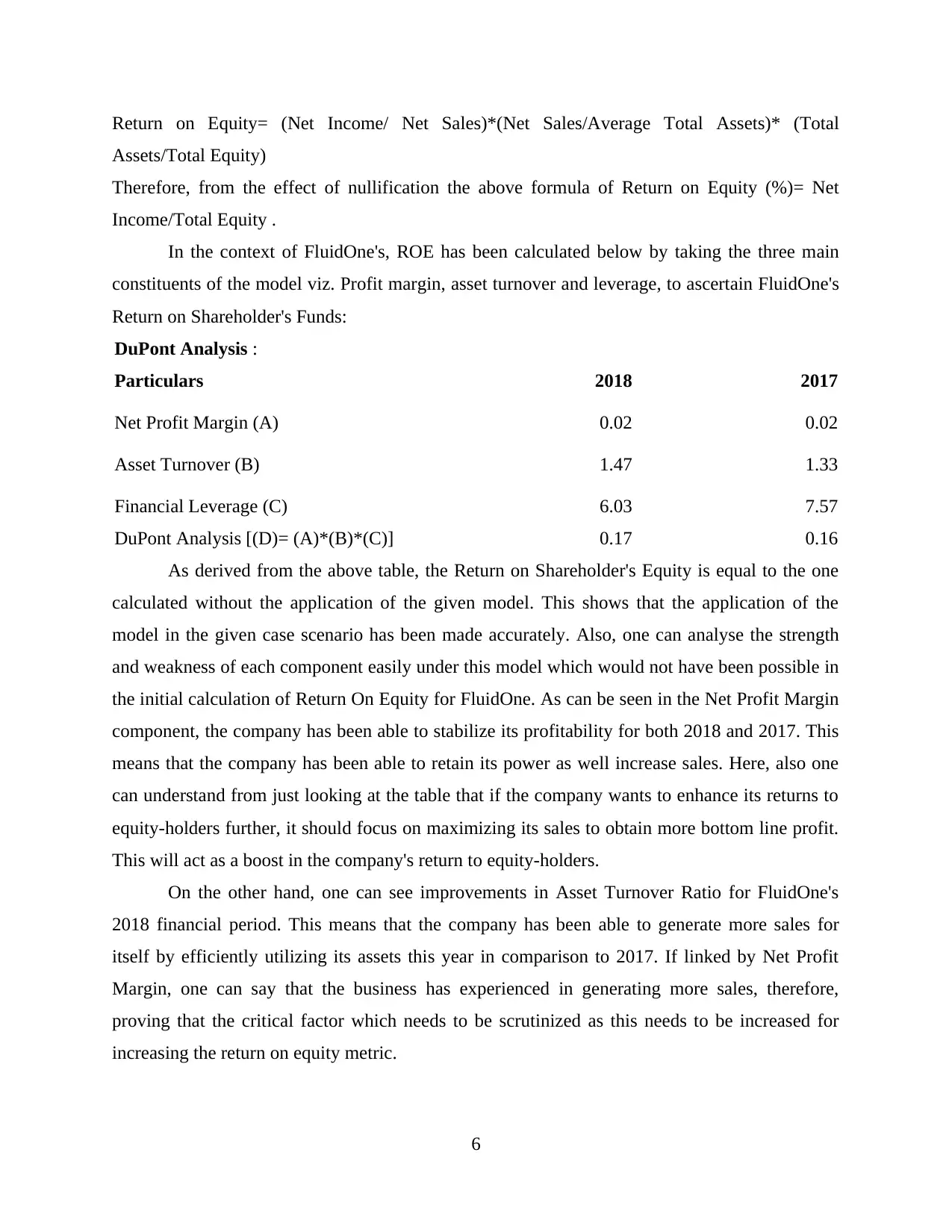

Return on Equity= (Net Income/ Net Sales)*(Net Sales/Average Total Assets)* (Total

Assets/Total Equity)

Therefore, from the effect of nullification the above formula of Return on Equity (%)= Net

Income/Total Equity .

In the context of FluidOne's, ROE has been calculated below by taking the three main

constituents of the model viz. Profit margin, asset turnover and leverage, to ascertain FluidOne's

Return on Shareholder's Funds:

DuPont Analysis :

Particulars 2018 2017

Net Profit Margin (A) 0.02 0.02

Asset Turnover (B) 1.47 1.33

Financial Leverage (C) 6.03 7.57

DuPont Analysis [(D)= (A)*(B)*(C)] 0.17 0.16

As derived from the above table, the Return on Shareholder's Equity is equal to the one

calculated without the application of the given model. This shows that the application of the

model in the given case scenario has been made accurately. Also, one can analyse the strength

and weakness of each component easily under this model which would not have been possible in

the initial calculation of Return On Equity for FluidOne. As can be seen in the Net Profit Margin

component, the company has been able to stabilize its profitability for both 2018 and 2017. This

means that the company has been able to retain its power as well increase sales. Here, also one

can understand from just looking at the table that if the company wants to enhance its returns to

equity-holders further, it should focus on maximizing its sales to obtain more bottom line profit.

This will act as a boost in the company's return to equity-holders.

On the other hand, one can see improvements in Asset Turnover Ratio for FluidOne's

2018 financial period. This means that the company has been able to generate more sales for

itself by efficiently utilizing its assets this year in comparison to 2017. If linked by Net Profit

Margin, one can say that the business has experienced in generating more sales, therefore,

proving that the critical factor which needs to be scrutinized as this needs to be increased for

increasing the return on equity metric.

6

Assets/Total Equity)

Therefore, from the effect of nullification the above formula of Return on Equity (%)= Net

Income/Total Equity .

In the context of FluidOne's, ROE has been calculated below by taking the three main

constituents of the model viz. Profit margin, asset turnover and leverage, to ascertain FluidOne's

Return on Shareholder's Funds:

DuPont Analysis :

Particulars 2018 2017

Net Profit Margin (A) 0.02 0.02

Asset Turnover (B) 1.47 1.33

Financial Leverage (C) 6.03 7.57

DuPont Analysis [(D)= (A)*(B)*(C)] 0.17 0.16

As derived from the above table, the Return on Shareholder's Equity is equal to the one

calculated without the application of the given model. This shows that the application of the

model in the given case scenario has been made accurately. Also, one can analyse the strength

and weakness of each component easily under this model which would not have been possible in

the initial calculation of Return On Equity for FluidOne. As can be seen in the Net Profit Margin

component, the company has been able to stabilize its profitability for both 2018 and 2017. This

means that the company has been able to retain its power as well increase sales. Here, also one

can understand from just looking at the table that if the company wants to enhance its returns to

equity-holders further, it should focus on maximizing its sales to obtain more bottom line profit.

This will act as a boost in the company's return to equity-holders.

On the other hand, one can see improvements in Asset Turnover Ratio for FluidOne's

2018 financial period. This means that the company has been able to generate more sales for

itself by efficiently utilizing its assets this year in comparison to 2017. If linked by Net Profit

Margin, one can say that the business has experienced in generating more sales, therefore,

proving that the critical factor which needs to be scrutinized as this needs to be increased for

increasing the return on equity metric.

6

Lastly, this model has been able to point out that the financial leverage, specifically

Equity Multiplier, has decreased for FluidOne's 2018 financial period in comparison to 2017.

Also a deeper look into this multiplier shows that the company has been able to increase its

shareholder's equity substantially and requires to increase the efficiency of its total assets by

increasing its debt financing to enjoy more tax benefits available on interest payments as well as

provide more returns to their equity-holder.

Thus, this model has been successful in analysing the reasons behind changes in return on

equity for 2018 and 2017 of FluidOne Network pointing out those criterion which require most

attention of top management.

PART 2

Description and Critical Analysis of Fluidone company

A budget is a formal statement of predication of incomes and expenses which is based on

future plans and objectives. It is a one of the most important administrative tool which is

evaluated revenues, costs and resources in particular specific period for reflecting on upcoming

financial conditions and goals. The company perform their business under two core products -

Data

Mobile

For the growth of business company has estimated revenues, EBITDA after then

compares result on the basis of 2017. They grew revenue by £5m to £26m which is £21m in

2017 and EBITDA also increased which was £1.8m and now in 2018 in £0.7m to £2.4m.

Data – When analysis of income and expenses of Data business after then getting gross

profit which is compared with previous year of 2017, in 2018 it is improved by 6% to £8.7m.

Revenue continue grow and substantial investments in our acquisition operations has delivered

substance gross margin improvements (Nedelec and et.al 2014) .

Mobile – The company has working with all leading networks and in the year it will

become EE's biggest wholesale business partner and shifting from a dealer model to own billing

platform. The team of mobile can supply inventory growth in mobile connections which has

increased by 25% to 26k from 21k last year.

Budgetary Control Process

7

Equity Multiplier, has decreased for FluidOne's 2018 financial period in comparison to 2017.

Also a deeper look into this multiplier shows that the company has been able to increase its

shareholder's equity substantially and requires to increase the efficiency of its total assets by

increasing its debt financing to enjoy more tax benefits available on interest payments as well as

provide more returns to their equity-holder.

Thus, this model has been successful in analysing the reasons behind changes in return on

equity for 2018 and 2017 of FluidOne Network pointing out those criterion which require most

attention of top management.

PART 2

Description and Critical Analysis of Fluidone company

A budget is a formal statement of predication of incomes and expenses which is based on

future plans and objectives. It is a one of the most important administrative tool which is

evaluated revenues, costs and resources in particular specific period for reflecting on upcoming

financial conditions and goals. The company perform their business under two core products -

Data

Mobile

For the growth of business company has estimated revenues, EBITDA after then

compares result on the basis of 2017. They grew revenue by £5m to £26m which is £21m in

2017 and EBITDA also increased which was £1.8m and now in 2018 in £0.7m to £2.4m.

Data – When analysis of income and expenses of Data business after then getting gross

profit which is compared with previous year of 2017, in 2018 it is improved by 6% to £8.7m.

Revenue continue grow and substantial investments in our acquisition operations has delivered

substance gross margin improvements (Nedelec and et.al 2014) .

Mobile – The company has working with all leading networks and in the year it will

become EE's biggest wholesale business partner and shifting from a dealer model to own billing

platform. The team of mobile can supply inventory growth in mobile connections which has

increased by 25% to 26k from 21k last year.

Budgetary Control Process

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Budgetary control is the process of evaluating several outcomes with budgeted figures for

the company for the upcoming period. It can set standard after then compare results actual

performance with budgeting figures to calculate variance. In the analysis of budgetary control

include initial budget preparation process which is related to strategic objectives. The company

has prepared there budget process according to strategic objectives.

Strategic objectives is a term of the company which is related to goals of an organization.

It is used in strategic management to set targets in proper way and there are mainly related to

mission or vision of the company. The objective are of the company- Increase customers,

improve profit of data business and mobile. Net assets improved by 40% compare to 2017 and it

is affected to balance sheet.

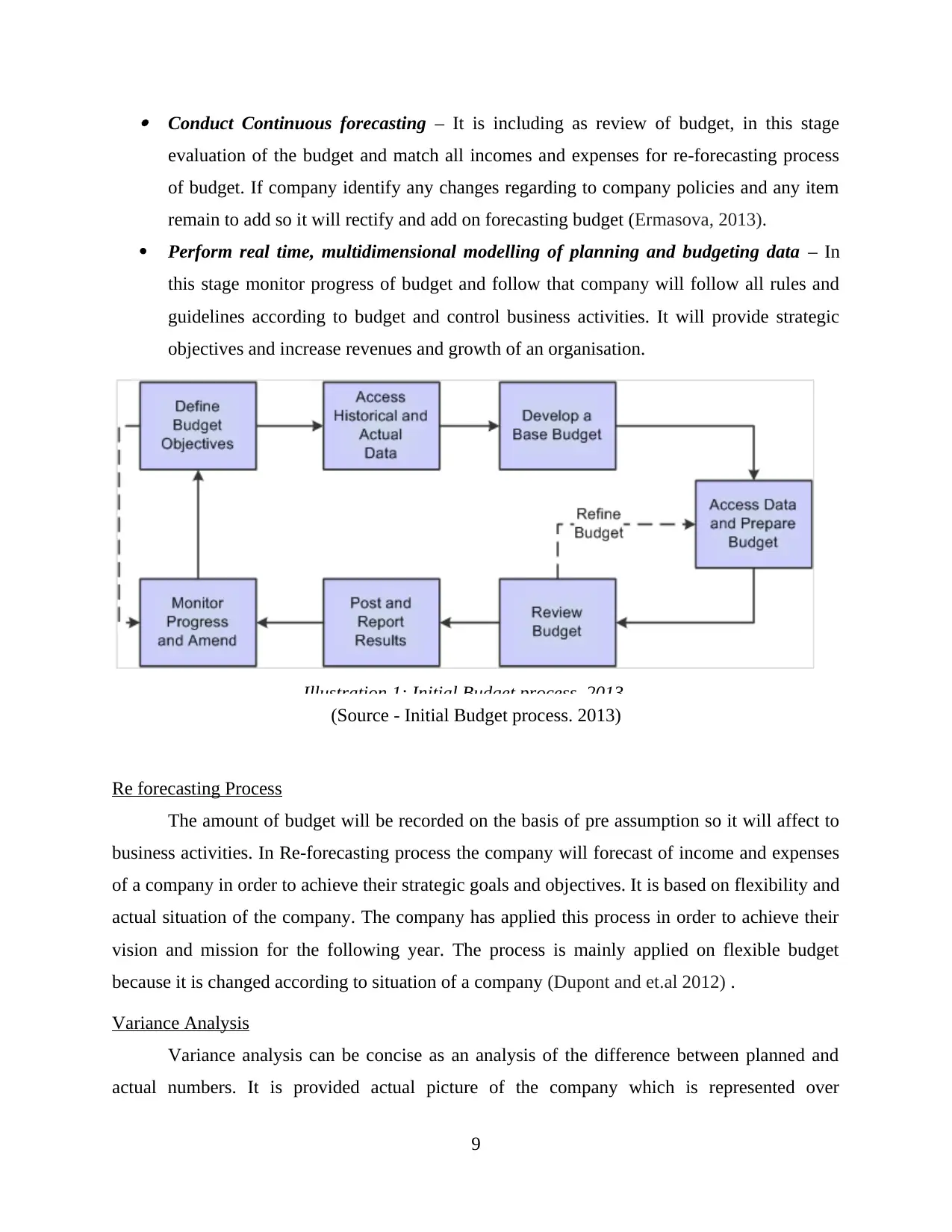

The initial budget process given below - Developing planning objectives – Firstly in initial budget process can develop planning

targets which is achieved by company in following years through budget. When prepare

budget of the company so it will relate to goals and objectives of a company (Giobbe and

et.al 2015) . Access and analyse historical and Actual data – It is a second stage of budget process

and in this stage can access all historical data as well as actual data which can help to

prepare current year budget. These data help to understand different situation and

overcome risk in future time period. Produce base budget – After all estimation there is prepare base budget and it will relate

to strategic objectives which is pre decided by company for following year. The base

budget is base plan of the company which can help to determine different situation of

company as well as risk. Link top down targets with bottom up budgets – In the base budget all items are

interrelated and provide all explanation regarding to company. These items are related to

targets of a company because the company structure divided into different division like

upper, middle and lower division. The manager can set targets for every section and it

will also mention in bottom up targets. Integrate and update financial statements as business condition change – If any

financial condition or market condition will change so it will update in budget. This

process is helpful in achieving strategic objectives of a company.

8

the company for the upcoming period. It can set standard after then compare results actual

performance with budgeting figures to calculate variance. In the analysis of budgetary control

include initial budget preparation process which is related to strategic objectives. The company

has prepared there budget process according to strategic objectives.

Strategic objectives is a term of the company which is related to goals of an organization.

It is used in strategic management to set targets in proper way and there are mainly related to

mission or vision of the company. The objective are of the company- Increase customers,

improve profit of data business and mobile. Net assets improved by 40% compare to 2017 and it

is affected to balance sheet.

The initial budget process given below - Developing planning objectives – Firstly in initial budget process can develop planning

targets which is achieved by company in following years through budget. When prepare

budget of the company so it will relate to goals and objectives of a company (Giobbe and

et.al 2015) . Access and analyse historical and Actual data – It is a second stage of budget process

and in this stage can access all historical data as well as actual data which can help to

prepare current year budget. These data help to understand different situation and

overcome risk in future time period. Produce base budget – After all estimation there is prepare base budget and it will relate

to strategic objectives which is pre decided by company for following year. The base

budget is base plan of the company which can help to determine different situation of

company as well as risk. Link top down targets with bottom up budgets – In the base budget all items are

interrelated and provide all explanation regarding to company. These items are related to

targets of a company because the company structure divided into different division like

upper, middle and lower division. The manager can set targets for every section and it

will also mention in bottom up targets. Integrate and update financial statements as business condition change – If any

financial condition or market condition will change so it will update in budget. This

process is helpful in achieving strategic objectives of a company.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Conduct Continuous forecasting – It is including as review of budget, in this stage

evaluation of the budget and match all incomes and expenses for re-forecasting process

of budget. If company identify any changes regarding to company policies and any item

remain to add so it will rectify and add on forecasting budget (Ermasova, 2013).

Perform real time, multidimensional modelling of planning and budgeting data – In

this stage monitor progress of budget and follow that company will follow all rules and

guidelines according to budget and control business activities. It will provide strategic

objectives and increase revenues and growth of an organisation.

Illustration 1: Initial Budget process. 2013

(Source - Initial Budget process. 2013)

Re forecasting Process

The amount of budget will be recorded on the basis of pre assumption so it will affect to

business activities. In Re-forecasting process the company will forecast of income and expenses

of a company in order to achieve their strategic goals and objectives. It is based on flexibility and

actual situation of the company. The company has applied this process in order to achieve their

vision and mission for the following year. The process is mainly applied on flexible budget

because it is changed according to situation of a company (Dupont and et.al 2012) .

Variance Analysis

Variance analysis can be concise as an analysis of the difference between planned and

actual numbers. It is provided actual picture of the company which is represented over

9

evaluation of the budget and match all incomes and expenses for re-forecasting process

of budget. If company identify any changes regarding to company policies and any item

remain to add so it will rectify and add on forecasting budget (Ermasova, 2013).

Perform real time, multidimensional modelling of planning and budgeting data – In

this stage monitor progress of budget and follow that company will follow all rules and

guidelines according to budget and control business activities. It will provide strategic

objectives and increase revenues and growth of an organisation.

Illustration 1: Initial Budget process. 2013

(Source - Initial Budget process. 2013)

Re forecasting Process

The amount of budget will be recorded on the basis of pre assumption so it will affect to

business activities. In Re-forecasting process the company will forecast of income and expenses

of a company in order to achieve their strategic goals and objectives. It is based on flexibility and

actual situation of the company. The company has applied this process in order to achieve their

vision and mission for the following year. The process is mainly applied on flexible budget

because it is changed according to situation of a company (Dupont and et.al 2012) .

Variance Analysis

Variance analysis can be concise as an analysis of the difference between planned and

actual numbers. It is provided actual picture of the company which is represented over

9

performance and underperformance for particular accounting period. The company has using this

analysis to compare standard and actual cost of raw materials.

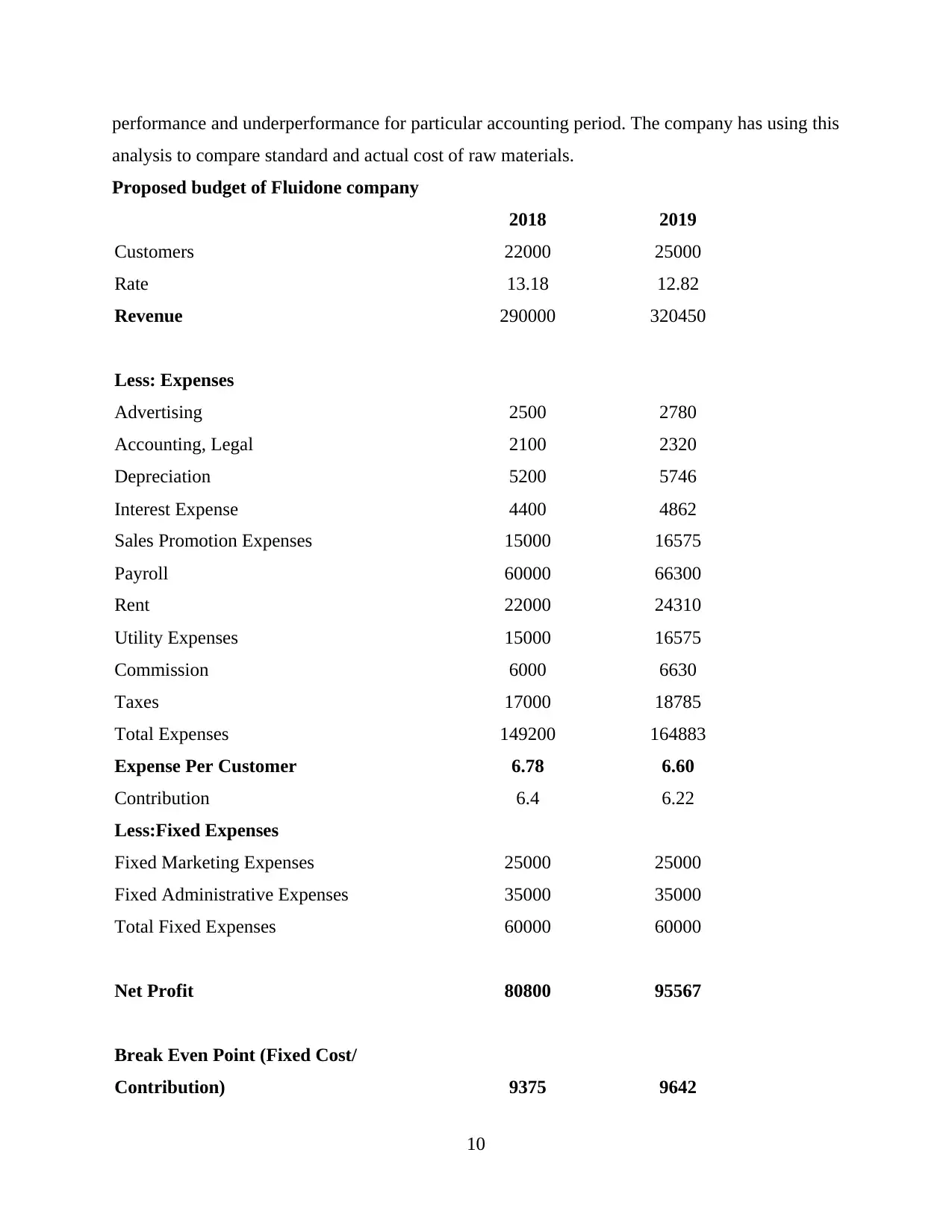

Proposed budget of Fluidone company

2018 2019

Customers 22000 25000

Rate 13.18 12.82

Revenue 290000 320450

Less: Expenses

Advertising 2500 2780

Accounting, Legal 2100 2320

Depreciation 5200 5746

Interest Expense 4400 4862

Sales Promotion Expenses 15000 16575

Payroll 60000 66300

Rent 22000 24310

Utility Expenses 15000 16575

Commission 6000 6630

Taxes 17000 18785

Total Expenses 149200 164883

Expense Per Customer 6.78 6.60

Contribution 6.4 6.22

Less:Fixed Expenses

Fixed Marketing Expenses 25000 25000

Fixed Administrative Expenses 35000 35000

Total Fixed Expenses 60000 60000

Net Profit 80800 95567

Break Even Point (Fixed Cost/

Contribution) 9375 9642

10

analysis to compare standard and actual cost of raw materials.

Proposed budget of Fluidone company

2018 2019

Customers 22000 25000

Rate 13.18 12.82

Revenue 290000 320450

Less: Expenses

Advertising 2500 2780

Accounting, Legal 2100 2320

Depreciation 5200 5746

Interest Expense 4400 4862

Sales Promotion Expenses 15000 16575

Payroll 60000 66300

Rent 22000 24310

Utility Expenses 15000 16575

Commission 6000 6630

Taxes 17000 18785

Total Expenses 149200 164883

Expense Per Customer 6.78 6.60

Contribution 6.4 6.22

Less:Fixed Expenses

Fixed Marketing Expenses 25000 25000

Fixed Administrative Expenses 35000 35000

Total Fixed Expenses 60000 60000

Net Profit 80800 95567

Break Even Point (Fixed Cost/

Contribution) 9375 9642

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.