Case Study Dysonica Plc

VerifiedAdded on 2023/06/11

|13

|4005

|459

AI Summary

This case study on Dysonica Plc includes the classification of costs, cost reduction strategies, 12-month forecast/budget, and performance evaluation. The study recommends the use of activity-based costing approach to reduce costs and improve profitability.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Case Study Dysonica

Plc

Plc

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Classify the costs according to their nature.................................................................................3

TASK 2............................................................................................................................................6

Provide recommendation and cost reduction strategy.................................................................6

TASK 3............................................................................................................................................7

Preparation a 12 - month forecast/budget for the business up to 30 April 2023.........................7

TASK 4..........................................................................................................................................10

Based on the facts in the forecast and budgets, evaluate Dysonica's performance...................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Classify the costs according to their nature.................................................................................3

TASK 2............................................................................................................................................6

Provide recommendation and cost reduction strategy.................................................................6

TASK 3............................................................................................................................................7

Preparation a 12 - month forecast/budget for the business up to 30 April 2023.........................7

TASK 4..........................................................................................................................................10

Based on the facts in the forecast and budgets, evaluate Dysonica's performance...................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Business finance refers to the funds generated, arranged, and managed by businesses in

order to accomplish their objectives. It may also be defined as the assets obtained by

organisations in order to start a business. The capital assets and credit subsidises that are invested

into a firm are included in these assets. This money will be used to acquire resources, purchase

raw materials, and make goods for the company's operating operations. When a company first

begins operations, the funding available is insufficient to solve all of the issues that arise. As a

result, in order to meet these needs, business organisations must take care of a large number of

components in order to generate revenue. The evaluation of monetary requirements and possible

results may be cross-checked in a standard approach, allowing for the creation of a superb

monetary management plan for the smooth operation of a project (Anghelache and et.al., 2019).

The context analysis of Dysonica Plc is the subject of this research. It consists of four exercises,

the first of which covers the expenditure elements of a business and how they are separated. The

next project consists of suggestions for the administration that will aid the chiefs in lowering

their expenses and prices. The third section includes Dysonica Plc's income forecasts until April

30, 2023. Furthermore, the final project examines the organization's triumphs and achievements,

as well as how it operates in that particular industry. This decision will be made based on the

gauge values in Dysonica Plc's revenue.

TASK 1

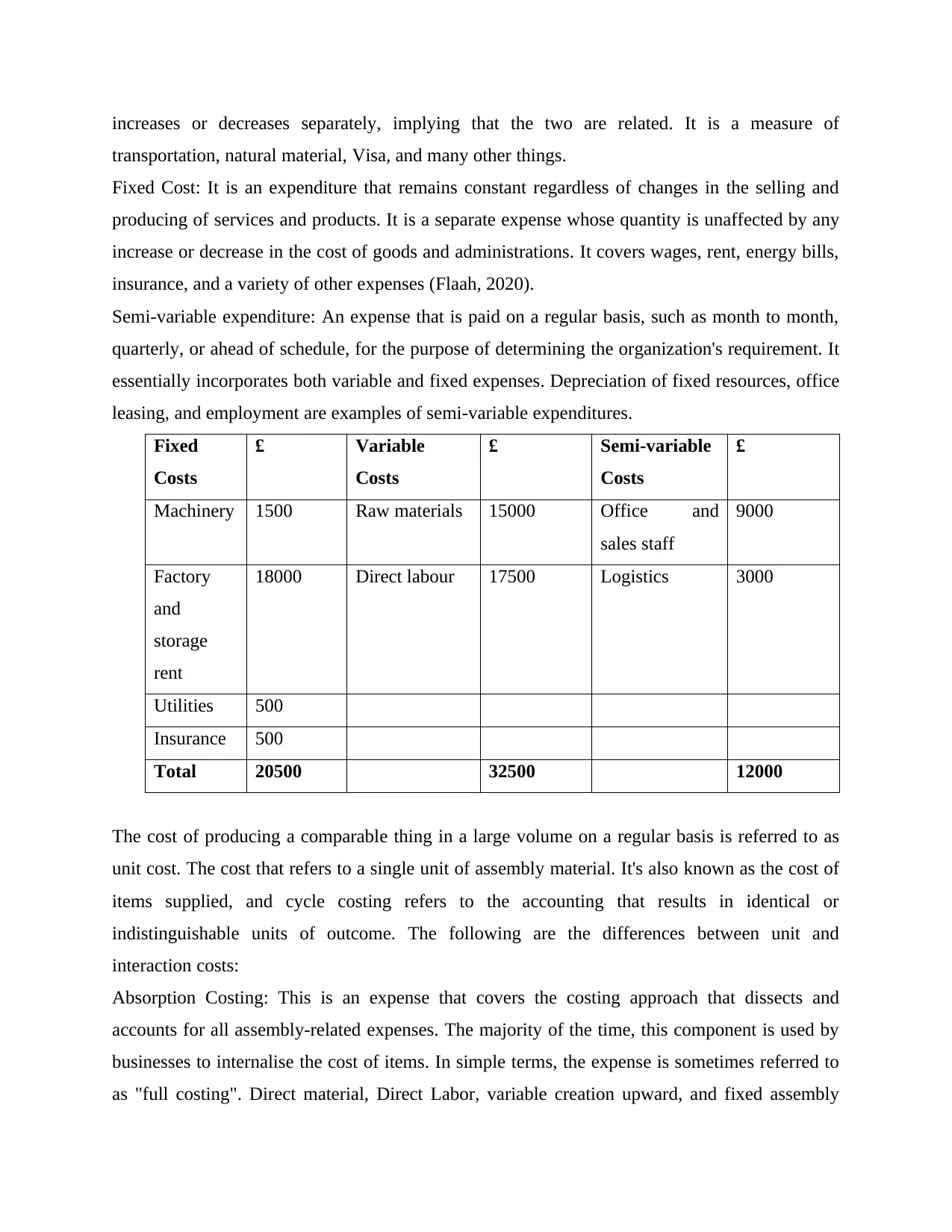

Classify the costs according to their nature

The term "cost" is used while putting together and supplying services and products. Cost is

critical at every stage of the production and manufacturing cycle, from procuring unprocessed

materials to completing an organization's finished goods. Essentially, cost is the amount of

money used to help pay the costs of production. There are several types of costs that affect an

organisation, but the most common two types of expenses that cause product problems are

variable expense and fixed cost (Feyaerts and Demarsin, 2020).

Variable cost refers to an expense that is directly related to an organization's sales and

production, or an expense that controls the number of items sold and assembled in a project. If an

organization's inventory and product creation increase or decrease, the variable expenditure

Business finance refers to the funds generated, arranged, and managed by businesses in

order to accomplish their objectives. It may also be defined as the assets obtained by

organisations in order to start a business. The capital assets and credit subsidises that are invested

into a firm are included in these assets. This money will be used to acquire resources, purchase

raw materials, and make goods for the company's operating operations. When a company first

begins operations, the funding available is insufficient to solve all of the issues that arise. As a

result, in order to meet these needs, business organisations must take care of a large number of

components in order to generate revenue. The evaluation of monetary requirements and possible

results may be cross-checked in a standard approach, allowing for the creation of a superb

monetary management plan for the smooth operation of a project (Anghelache and et.al., 2019).

The context analysis of Dysonica Plc is the subject of this research. It consists of four exercises,

the first of which covers the expenditure elements of a business and how they are separated. The

next project consists of suggestions for the administration that will aid the chiefs in lowering

their expenses and prices. The third section includes Dysonica Plc's income forecasts until April

30, 2023. Furthermore, the final project examines the organization's triumphs and achievements,

as well as how it operates in that particular industry. This decision will be made based on the

gauge values in Dysonica Plc's revenue.

TASK 1

Classify the costs according to their nature

The term "cost" is used while putting together and supplying services and products. Cost is

critical at every stage of the production and manufacturing cycle, from procuring unprocessed

materials to completing an organization's finished goods. Essentially, cost is the amount of

money used to help pay the costs of production. There are several types of costs that affect an

organisation, but the most common two types of expenses that cause product problems are

variable expense and fixed cost (Feyaerts and Demarsin, 2020).

Variable cost refers to an expense that is directly related to an organization's sales and

production, or an expense that controls the number of items sold and assembled in a project. If an

organization's inventory and product creation increase or decrease, the variable expenditure

increases or decreases separately, implying that the two are related. It is a measure of

transportation, natural material, Visa, and many other things.

Fixed Cost: It is an expenditure that remains constant regardless of changes in the selling and

producing of services and products. It is a separate expense whose quantity is unaffected by any

increase or decrease in the cost of goods and administrations. It covers wages, rent, energy bills,

insurance, and a variety of other expenses (Flaah, 2020).

Semi-variable expenditure: An expense that is paid on a regular basis, such as month to month,

quarterly, or ahead of schedule, for the purpose of determining the organization's requirement. It

essentially incorporates both variable and fixed expenses. Depreciation of fixed resources, office

leasing, and employment are examples of semi-variable expenditures.

Fixed

Costs

£ Variable

Costs

£ Semi-variable

Costs

£

Machinery 1500 Raw materials 15000 Office and

sales staff

9000

Factory

and

storage

rent

18000 Direct labour 17500 Logistics 3000

Utilities 500

Insurance 500

Total 20500 32500 12000

The cost of producing a comparable thing in a large volume on a regular basis is referred to as

unit cost. The cost that refers to a single unit of assembly material. It's also known as the cost of

items supplied, and cycle costing refers to the accounting that results in identical or

indistinguishable units of outcome. The following are the differences between unit and

interaction costs:

Absorption Costing: This is an expense that covers the costing approach that dissects and

accounts for all assembly-related expenses. The majority of the time, this component is used by

businesses to internalise the cost of items. In simple terms, the expense is sometimes referred to

as "full costing". Direct material, Direct Labor, variable creation upward, and fixed assembly

transportation, natural material, Visa, and many other things.

Fixed Cost: It is an expenditure that remains constant regardless of changes in the selling and

producing of services and products. It is a separate expense whose quantity is unaffected by any

increase or decrease in the cost of goods and administrations. It covers wages, rent, energy bills,

insurance, and a variety of other expenses (Flaah, 2020).

Semi-variable expenditure: An expense that is paid on a regular basis, such as month to month,

quarterly, or ahead of schedule, for the purpose of determining the organization's requirement. It

essentially incorporates both variable and fixed expenses. Depreciation of fixed resources, office

leasing, and employment are examples of semi-variable expenditures.

Fixed

Costs

£ Variable

Costs

£ Semi-variable

Costs

£

Machinery 1500 Raw materials 15000 Office and

sales staff

9000

Factory

and

storage

rent

18000 Direct labour 17500 Logistics 3000

Utilities 500

Insurance 500

Total 20500 32500 12000

The cost of producing a comparable thing in a large volume on a regular basis is referred to as

unit cost. The cost that refers to a single unit of assembly material. It's also known as the cost of

items supplied, and cycle costing refers to the accounting that results in identical or

indistinguishable units of outcome. The following are the differences between unit and

interaction costs:

Absorption Costing: This is an expense that covers the costing approach that dissects and

accounts for all assembly-related expenses. The majority of the time, this component is used by

businesses to internalise the cost of items. In simple terms, the expense is sometimes referred to

as "full costing". Direct material, Direct Labor, variable creation upward, and fixed assembly

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

upward are the four types of retention costing components. The cost includes both direct and

indirect costs (Hilorme and et.al., 2019). The most important components of direct expenditure

are the amount of materials used and the time spent constructing the product. Office

expenditures, plant rentals, security charges, and protection are all included in the creation's

indirect costs.

Computation of Absorption costing:

Formula = (Direct work cost + Direct material expense + Variable assembling upward expense +

Fixed assembling upward) / No. of units created

It is mostly used in the field of assembling companies to aid the company in calculating the cost

of goods so that the company may examine the best expenditure approach for the amount as well

as to manage the cost of goods (Mazahrih, 2019).

For instance:

Accept that the ABC Corporation is a fan-producer. One assembly step accommodates the

relevant information. The retention costing technique will be used to determine the advantages.

The number of units produced equals 10,000. 9,000 units sold over the time = $ 50 per unit price

Direct Labour = $ 5 Direct Material = $ 20

$ 5 in other variable costs

Overheads Fixed = $ 5

$ 30,000 in fixed costs

Marginal costing is a method of accounting for inconsequential expenses in which variable costs

are charged to unit costs and fixed costs for a certain period are totally recorded according to the

commitment value. The cost indicates that a greater number of costs were incurred in the

assembly of an additional unit of object or outcome. Minor costing includes the circulation of

both variable and fixed costs, as well as detecting the value, material valuation, and benefit pace.

It's also worthwhile to look at the cost-behaving patterns that influence the organization's

productivity limit (Paulet, 2018).

Marginal Cost = Change in cost / Change in Quantity

The unit of cost is affected by the rate of change in factor costs. In a sufficient level of creation,

the organization's fixed costs remain constant (Nguyen, 2018).

Model:

indirect costs (Hilorme and et.al., 2019). The most important components of direct expenditure

are the amount of materials used and the time spent constructing the product. Office

expenditures, plant rentals, security charges, and protection are all included in the creation's

indirect costs.

Computation of Absorption costing:

Formula = (Direct work cost + Direct material expense + Variable assembling upward expense +

Fixed assembling upward) / No. of units created

It is mostly used in the field of assembling companies to aid the company in calculating the cost

of goods so that the company may examine the best expenditure approach for the amount as well

as to manage the cost of goods (Mazahrih, 2019).

For instance:

Accept that the ABC Corporation is a fan-producer. One assembly step accommodates the

relevant information. The retention costing technique will be used to determine the advantages.

The number of units produced equals 10,000. 9,000 units sold over the time = $ 50 per unit price

Direct Labour = $ 5 Direct Material = $ 20

$ 5 in other variable costs

Overheads Fixed = $ 5

$ 30,000 in fixed costs

Marginal costing is a method of accounting for inconsequential expenses in which variable costs

are charged to unit costs and fixed costs for a certain period are totally recorded according to the

commitment value. The cost indicates that a greater number of costs were incurred in the

assembly of an additional unit of object or outcome. Minor costing includes the circulation of

both variable and fixed costs, as well as detecting the value, material valuation, and benefit pace.

It's also worthwhile to look at the cost-behaving patterns that influence the organization's

productivity limit (Paulet, 2018).

Marginal Cost = Change in cost / Change in Quantity

The unit of cost is affected by the rate of change in factor costs. In a sufficient level of creation,

the organization's fixed costs remain constant (Nguyen, 2018).

Model:

Accept that ABC is a partnership that makes a fan. For its assembling offices, the it is given to

follow data.

Month 1 Units Produced = 10,000 Month 2 Units Produced = 15,000 Variable Costs in Month

1= $ 50,000 Variable Costs in Month 2 = $ 80,000

Change in cost/change in quantity Equals Marginal Cost

(80,000 – 50,000)/ (15,000 – 10,000) = Marginal Cost

Therefore, the result of marginal cost per unit is $ 6 (30,000/5,000).

Activity-based costing (ABC) is a costing method that may be used to analyse the cost of

production. In view of approaches, it is broken down upward expenditure amid assembling. By

focusing on minimising the worth of rising costs, action-based costing is followed. The

following are the implications of this costing:

Investigating the expenditure rehearsals demonstrates the expense rehearsals method in light of

the organization's stance (Persson, 2019).

The ABC business examines the distribution channels that a vendor uses to market a goods or

service, such as a shop, a distributor, a person-to-person communication site, and house-to-house

services.

Product pricing is also an important part of action-based costing that has a direct influence on the

company's profit. The price of the item is determined by analysing the market and the value of

similar challenger's organisation items. If the cost of goods is higher than the lowest cost, it

creates a problem of misfortune; hence, the base valuing is important to keep track of the

situation on the watch.

TASK 2

Provide recommendation and cost reduction strategy

Based on the results of the aforesaid methods, they have come to the conclusion that they

should consolidate the activity - based costing approach as their method of calculating expenses.

The primary argument for using such a strategy is that it considers the cost of each branch of the

business and distributes the expenditure depending on previously defined drivers. The ABC

costing would assist them in empowering the expense in each of their business cycles, and they

would be able to easily check which office is valuable for them in terms of cost distribution, and

those divisions that are causing more expense would ensure that their expense should be kept up

follow data.

Month 1 Units Produced = 10,000 Month 2 Units Produced = 15,000 Variable Costs in Month

1= $ 50,000 Variable Costs in Month 2 = $ 80,000

Change in cost/change in quantity Equals Marginal Cost

(80,000 – 50,000)/ (15,000 – 10,000) = Marginal Cost

Therefore, the result of marginal cost per unit is $ 6 (30,000/5,000).

Activity-based costing (ABC) is a costing method that may be used to analyse the cost of

production. In view of approaches, it is broken down upward expenditure amid assembling. By

focusing on minimising the worth of rising costs, action-based costing is followed. The

following are the implications of this costing:

Investigating the expenditure rehearsals demonstrates the expense rehearsals method in light of

the organization's stance (Persson, 2019).

The ABC business examines the distribution channels that a vendor uses to market a goods or

service, such as a shop, a distributor, a person-to-person communication site, and house-to-house

services.

Product pricing is also an important part of action-based costing that has a direct influence on the

company's profit. The price of the item is determined by analysing the market and the value of

similar challenger's organisation items. If the cost of goods is higher than the lowest cost, it

creates a problem of misfortune; hence, the base valuing is important to keep track of the

situation on the watch.

TASK 2

Provide recommendation and cost reduction strategy

Based on the results of the aforesaid methods, they have come to the conclusion that they

should consolidate the activity - based costing approach as their method of calculating expenses.

The primary argument for using such a strategy is that it considers the cost of each branch of the

business and distributes the expenditure depending on previously defined drivers. The ABC

costing would assist them in empowering the expense in each of their business cycles, and they

would be able to easily check which office is valuable for them in terms of cost distribution, and

those divisions that are causing more expense would ensure that their expense should be kept up

with under a reasonable cut-off (Scerri, 2021). The fundamental benefit of ABC costing is that it

groups expenses according to work rather than apportioning something comparable across

functional divisionsIt aids the business in lowering the cost of the end result as a whole, as well

as assisting the business in selecting the selling with an acceptable level of valuing the item so

that the buyer is not inconvenienced. As a result of the preceding discussion, it is suggested that

Dysonica Plc use an action-based costing approach in their organisation so that they can reduce

item costs in a similar manner.

TASK 3

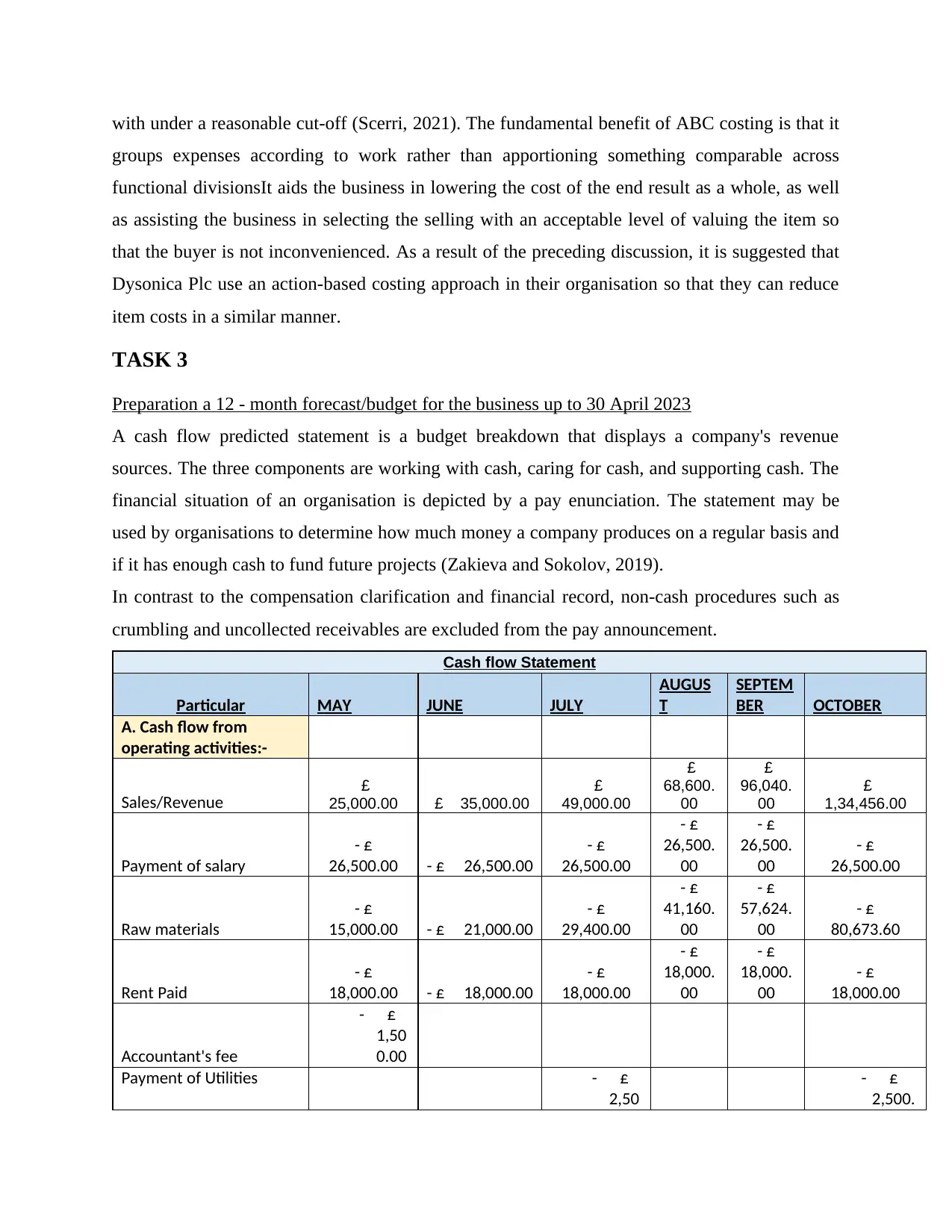

Preparation a 12 - month forecast/budget for the business up to 30 April 2023

A cash flow predicted statement is a budget breakdown that displays a company's revenue

sources. The three components are working with cash, caring for cash, and supporting cash. The

financial situation of an organisation is depicted by a pay enunciation. The statement may be

used by organisations to determine how much money a company produces on a regular basis and

if it has enough cash to fund future projects (Zakieva and Sokolov, 2019).

In contrast to the compensation clarification and financial record, non-cash procedures such as

crumbling and uncollected receivables are excluded from the pay announcement.

Cash flow Statement

Particular MAY JUNE JULY

AUGUS

T

SEPTEM

BER OCTOBER

A. Cash flow from

operating activities:-

Sales/Revenue £

25,000.00 £ 35,000.00

£

49,000.00

£

68,600.

00

£

96,040.

00

£

1,34,456.00

Payment of salary

- £

26,500.00 - £ 26,500.00

- £

26,500.00

- £

26,500.

00

- £

26,500.

00

- £

26,500.00

Raw materials

- £

15,000.00 - £ 21,000.00

- £

29,400.00

- £

41,160.

00

- £

57,624.

00

- £

80,673.60

Rent Paid

- £

18,000.00 - £ 18,000.00

- £

18,000.00

- £

18,000.

00

- £

18,000.

00

- £

18,000.00

Accountant's fee

- £

1,50

0.00

Payment of Utilities - £

2,50

- £

2,500.

groups expenses according to work rather than apportioning something comparable across

functional divisionsIt aids the business in lowering the cost of the end result as a whole, as well

as assisting the business in selecting the selling with an acceptable level of valuing the item so

that the buyer is not inconvenienced. As a result of the preceding discussion, it is suggested that

Dysonica Plc use an action-based costing approach in their organisation so that they can reduce

item costs in a similar manner.

TASK 3

Preparation a 12 - month forecast/budget for the business up to 30 April 2023

A cash flow predicted statement is a budget breakdown that displays a company's revenue

sources. The three components are working with cash, caring for cash, and supporting cash. The

financial situation of an organisation is depicted by a pay enunciation. The statement may be

used by organisations to determine how much money a company produces on a regular basis and

if it has enough cash to fund future projects (Zakieva and Sokolov, 2019).

In contrast to the compensation clarification and financial record, non-cash procedures such as

crumbling and uncollected receivables are excluded from the pay announcement.

Cash flow Statement

Particular MAY JUNE JULY

AUGUS

T

SEPTEM

BER OCTOBER

A. Cash flow from

operating activities:-

Sales/Revenue £

25,000.00 £ 35,000.00

£

49,000.00

£

68,600.

00

£

96,040.

00

£

1,34,456.00

Payment of salary

- £

26,500.00 - £ 26,500.00

- £

26,500.00

- £

26,500.

00

- £

26,500.

00

- £

26,500.00

Raw materials

- £

15,000.00 - £ 21,000.00

- £

29,400.00

- £

41,160.

00

- £

57,624.

00

- £

80,673.60

Rent Paid

- £

18,000.00 - £ 18,000.00

- £

18,000.00

- £

18,000.

00

- £

18,000.

00

- £

18,000.00

Accountant's fee

- £

1,50

0.00

Payment of Utilities - £

2,50

- £

2,500.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

0.00 00

Telephones

-£

1,000.00

- £

1,000.

00

Vehicles

- £

20,000.00 - £ 200.00

- £

200.00

- £

200.00

- £

200.00

- £

200.00

marketing costs

- £

1,250.00 - £ 1,750.00

- £

2,450.00

- £

3,430.0

0

- £

4,802.0

0

- £

6,722.80

water

- £

100.

00

- £

100.00

logistics

- £

3,000.00 - £ 3,000.00

- £

3,000.00

- £

4,500.0

0

- £

3,000.0

0

- £

3,000.00

Machinery

- £

1,500.00 - £ 1,500.00

- £

1,500.00

- £

1,500.0

0

- £

1,500.0

0

- £

1,500.00

Insurance

- £

500.00 - £ 500.00

- £

500.00

- £

500.00

- £

500.00

- £

500.00

Mixc Expense

- £

50.00 - £ 50.00

- £

50.00

- £

50.00

- £

50.00

- £

50.00

Net cash flow from

operating activites:-

- £

62,300.00 - £ 37,500.00

- £

36,200.00

- £

27,240.

00

- £

16,136.

00

- £

6,290.40

B. Cash flow from

financaing activities:- £ - £ - £ -

£

-

£

- £ -

Net Cash flow from

financing activities:- £ - £ - £ -

£

-

£

- £ -

C. Cash flow from

Investing activities:-

Initial investment made

£

20,000.00 £ - £ -

£

-

£

- £ -

Net cash flow from

investing activities:-

£

20,000.00 £ - £ -

£

-

£

- £ -

Tatal cash

inflwo/outflows(A+B+C)

- £

42,300.00 - £ 37,500.00

- £

36,200.00

- £

27,240.

00

- £

16,136.

00

- £

6,290.40

Cash flow Statement

Particular NOVEMBE DECEMBE JANUARY FEBURAR MARCH APRIL Total

Telephones

-£

1,000.00

- £

1,000.

00

Vehicles

- £

20,000.00 - £ 200.00

- £

200.00

- £

200.00

- £

200.00

- £

200.00

marketing costs

- £

1,250.00 - £ 1,750.00

- £

2,450.00

- £

3,430.0

0

- £

4,802.0

0

- £

6,722.80

water

- £

100.

00

- £

100.00

logistics

- £

3,000.00 - £ 3,000.00

- £

3,000.00

- £

4,500.0

0

- £

3,000.0

0

- £

3,000.00

Machinery

- £

1,500.00 - £ 1,500.00

- £

1,500.00

- £

1,500.0

0

- £

1,500.0

0

- £

1,500.00

Insurance

- £

500.00 - £ 500.00

- £

500.00

- £

500.00

- £

500.00

- £

500.00

Mixc Expense

- £

50.00 - £ 50.00

- £

50.00

- £

50.00

- £

50.00

- £

50.00

Net cash flow from

operating activites:-

- £

62,300.00 - £ 37,500.00

- £

36,200.00

- £

27,240.

00

- £

16,136.

00

- £

6,290.40

B. Cash flow from

financaing activities:- £ - £ - £ -

£

-

£

- £ -

Net Cash flow from

financing activities:- £ - £ - £ -

£

-

£

- £ -

C. Cash flow from

Investing activities:-

Initial investment made

£

20,000.00 £ - £ -

£

-

£

- £ -

Net cash flow from

investing activities:-

£

20,000.00 £ - £ -

£

-

£

- £ -

Tatal cash

inflwo/outflows(A+B+C)

- £

42,300.00 - £ 37,500.00

- £

36,200.00

- £

27,240.

00

- £

16,136.

00

- £

6,290.40

Cash flow Statement

Particular NOVEMBE DECEMBE JANUARY FEBURAR MARCH APRIL Total

R R Y (Year 1)

A. Cash flow from

operating activities:-

Sales/Revenue £1,88,238.

40

£2,63,53

3.76

£3,68,947.

26

£5,16,52

6.17

£7,23,136.

64

£10,12,3

91.29

£34,80,8

69.52

Payment of salary

- £

31,800.00

- £

31,800.00

- £

31,800.00

- £

31,800.00

- £

31,800.00

- £

31,800.00

- £

3,49,800.

00

Raw materials

- £

1,12,943.04

- £

1,58,120.

26

- £

2,21,368.36

- £

3,09,915.

70

- £

4,33,881.98

- £

6,07,434.

78

Rent Paid

- £

25,000.00

- £

25,000.00

- £

25,000.00

- £

25,000.00

- £

25,000.00

- £

25,000.00

- £

2,58,000.

00

Accountant's fee

- £

1,500.00

Payment of Utilities

- £

2,5

00.

00

- £

2,500.00

- £

10,000.00

Telephones

- £

1,0

00.

00

- £

1,000.00

- £

4,000.00

Vehicles

- £

200.00

- £

200.00

- £

200.00

- £

200.00

- £

200.00

- £

200.00

- £

22,200.00

marketing costs

- £

18,823.84

- £

26,353.38

- £

36,894.73

- £

51,652.62

- £

72,313.66

- £

1,01,239.

13

- £

3,27,682.

15

water

- £

100

.00

- £

100.00

- £

400.00

logistics

- £

3,000.00

- £

3,000.00

- £

3,000.00

- £

3,000.00

- £

3,000.00

- £

3,000.00

- £

37,500.00

Machinery

- £

1,500.00

- £

1,500.00

- £

1,500.00

- £

1,500.00

- £

1,500.00

- £

1,500.00

- £

18,000.00

Insurance

- £

500.00

- £

500.00

- £

500.00

- £

500.00

- £

500.00

- £

500.00

- £

6,000.00

Mixc Expense

- £

50.00

- £

50.00

- £

50.00

- £

50.00

- £

50.00

- £

50.00

- £

600.00

Net cash flow from

operating activites:-

- £

5,5

78.

48

£

17,010.13

£

45,034.18

£

92,907.85

£

1,54,890.9

9

£

2,38,067.

39

£

24,45,187

.37

A. Cash flow from

operating activities:-

Sales/Revenue £1,88,238.

40

£2,63,53

3.76

£3,68,947.

26

£5,16,52

6.17

£7,23,136.

64

£10,12,3

91.29

£34,80,8

69.52

Payment of salary

- £

31,800.00

- £

31,800.00

- £

31,800.00

- £

31,800.00

- £

31,800.00

- £

31,800.00

- £

3,49,800.

00

Raw materials

- £

1,12,943.04

- £

1,58,120.

26

- £

2,21,368.36

- £

3,09,915.

70

- £

4,33,881.98

- £

6,07,434.

78

Rent Paid

- £

25,000.00

- £

25,000.00

- £

25,000.00

- £

25,000.00

- £

25,000.00

- £

25,000.00

- £

2,58,000.

00

Accountant's fee

- £

1,500.00

Payment of Utilities

- £

2,5

00.

00

- £

2,500.00

- £

10,000.00

Telephones

- £

1,0

00.

00

- £

1,000.00

- £

4,000.00

Vehicles

- £

200.00

- £

200.00

- £

200.00

- £

200.00

- £

200.00

- £

200.00

- £

22,200.00

marketing costs

- £

18,823.84

- £

26,353.38

- £

36,894.73

- £

51,652.62

- £

72,313.66

- £

1,01,239.

13

- £

3,27,682.

15

water

- £

100

.00

- £

100.00

- £

400.00

logistics

- £

3,000.00

- £

3,000.00

- £

3,000.00

- £

3,000.00

- £

3,000.00

- £

3,000.00

- £

37,500.00

Machinery

- £

1,500.00

- £

1,500.00

- £

1,500.00

- £

1,500.00

- £

1,500.00

- £

1,500.00

- £

18,000.00

Insurance

- £

500.00

- £

500.00

- £

500.00

- £

500.00

- £

500.00

- £

500.00

- £

6,000.00

Mixc Expense

- £

50.00

- £

50.00

- £

50.00

- £

50.00

- £

50.00

- £

50.00

- £

600.00

Net cash flow from

operating activites:-

- £

5,5

78.

48

£

17,010.13

£

45,034.18

£

92,907.85

£

1,54,890.9

9

£

2,38,067.

39

£

24,45,187

.37

B. Cash flow from

financaing activities:-

£

-

£

-

£

-

£

-

£

-

£

-

£

-

Net Cash flow from

financing activities:-

£

-

£

-

£

-

£

-

£

-

£

-

£

-

C. Cash flow from

Investing activities:-

Initial investment

made

£

-

£

-

£

-

£

-

£

-

£

-

£

20,000.00

Net cash flow from

investing activities:-

£

-

£

-

£

-

£

-

£

-

£

-

£

20,000.00

Tatal cash

inflwo/outflows(A+B+

C)

-£

5,578.48

£

17,010.13

£

45,034.18

£

92,907.85

£

1,54,890.9

9

£

2,38,067.

39

£

24,65,187

.37

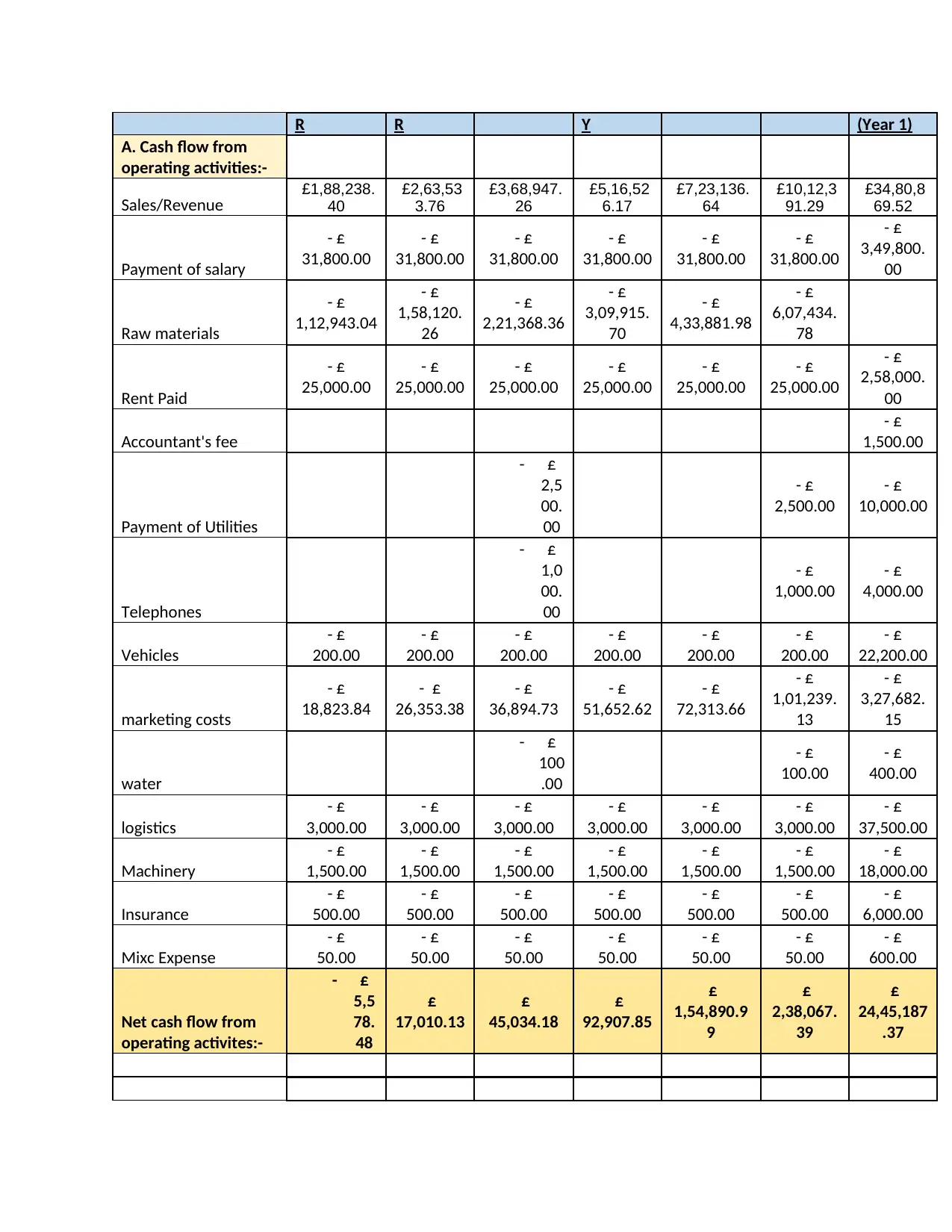

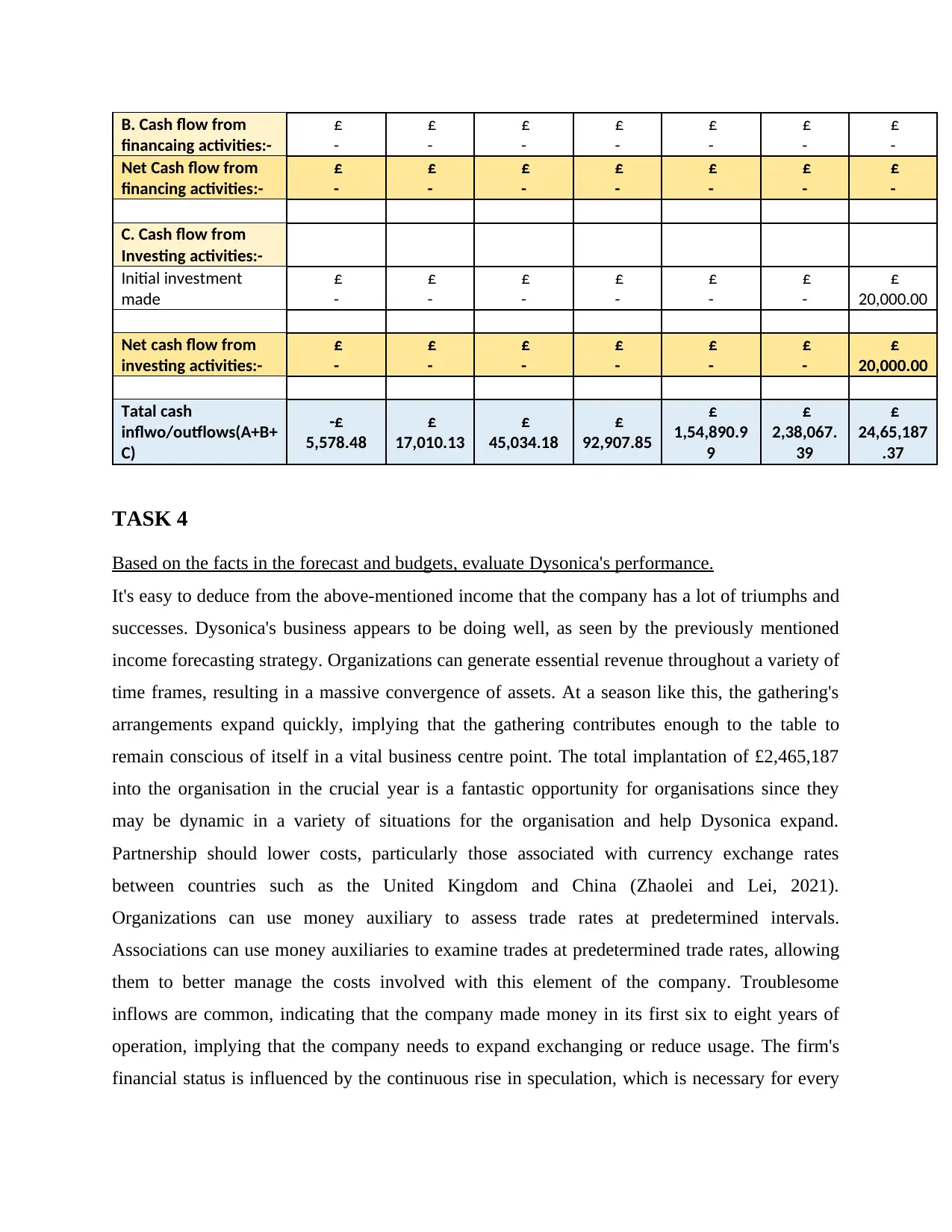

TASK 4

Based on the facts in the forecast and budgets, evaluate Dysonica's performance.

It's easy to deduce from the above-mentioned income that the company has a lot of triumphs and

successes. Dysonica's business appears to be doing well, as seen by the previously mentioned

income forecasting strategy. Organizations can generate essential revenue throughout a variety of

time frames, resulting in a massive convergence of assets. At a season like this, the gathering's

arrangements expand quickly, implying that the gathering contributes enough to the table to

remain conscious of itself in a vital business centre point. The total implantation of £2,465,187

into the organisation in the crucial year is a fantastic opportunity for organisations since they

may be dynamic in a variety of situations for the organisation and help Dysonica expand.

Partnership should lower costs, particularly those associated with currency exchange rates

between countries such as the United Kingdom and China (Zhaolei and Lei, 2021).

Organizations can use money auxiliary to assess trade rates at predetermined intervals.

Associations can use money auxiliaries to examine trades at predetermined trade rates, allowing

them to better manage the costs involved with this element of the company. Troublesome

inflows are common, indicating that the company made money in its first six to eight years of

operation, implying that the company needs to expand exchanging or reduce usage. The firm's

financial status is influenced by the continuous rise in speculation, which is necessary for every

financaing activities:-

£

-

£

-

£

-

£

-

£

-

£

-

£

-

Net Cash flow from

financing activities:-

£

-

£

-

£

-

£

-

£

-

£

-

£

-

C. Cash flow from

Investing activities:-

Initial investment

made

£

-

£

-

£

-

£

-

£

-

£

-

£

20,000.00

Net cash flow from

investing activities:-

£

-

£

-

£

-

£

-

£

-

£

-

£

20,000.00

Tatal cash

inflwo/outflows(A+B+

C)

-£

5,578.48

£

17,010.13

£

45,034.18

£

92,907.85

£

1,54,890.9

9

£

2,38,067.

39

£

24,65,187

.37

TASK 4

Based on the facts in the forecast and budgets, evaluate Dysonica's performance.

It's easy to deduce from the above-mentioned income that the company has a lot of triumphs and

successes. Dysonica's business appears to be doing well, as seen by the previously mentioned

income forecasting strategy. Organizations can generate essential revenue throughout a variety of

time frames, resulting in a massive convergence of assets. At a season like this, the gathering's

arrangements expand quickly, implying that the gathering contributes enough to the table to

remain conscious of itself in a vital business centre point. The total implantation of £2,465,187

into the organisation in the crucial year is a fantastic opportunity for organisations since they

may be dynamic in a variety of situations for the organisation and help Dysonica expand.

Partnership should lower costs, particularly those associated with currency exchange rates

between countries such as the United Kingdom and China (Zhaolei and Lei, 2021).

Organizations can use money auxiliary to assess trade rates at predetermined intervals.

Associations can use money auxiliaries to examine trades at predetermined trade rates, allowing

them to better manage the costs involved with this element of the company. Troublesome

inflows are common, indicating that the company made money in its first six to eight years of

operation, implying that the company needs to expand exchanging or reduce usage. The firm's

financial status is influenced by the continuous rise in speculation, which is necessary for every

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

organisation to succeed in complex economic sectors and throughout the world. Using elective

stock associations and determining which drives are at fault and costing the company money can

help minimise costs. They should execute their functional workouts at a consistent pace so that

their functional earnings remain positive over a longer period of time.

The absolute first portion of income from working exercises for a bookkeeping period shows

deals that begin in May and end in April, with an increase throughout the year. The

organization's expected income declarations reflect a strong and stable financial condition.

Dysonica Plc. can cover its short-term obligations without difficulty, and it has sufficient current

resources to address its long-term responsibilities. Additionally, the business plans can be seen,

indicating that the company is genuinely playing it straight when it comes to selling its products

and services and generating a significant amount of profit from transaction revenues. The total

cash inflow for the first year is estimated to be £ 2,465,187, which is the finest thing and also

allows Dysonica Plc a start and degree to open new speculating doors. Dysonica Plc. will benefit

greatly from increased interest in new resources as it expands its company and attracts a large

number of investors. It is clear from the predicted income justifications that Dysonica Plc. is

linked to unusual trade rates with countries such as China and the United Kingdom. As a result,

the expenditure incurred in this transaction is expected to reach a substantial level, which will be

limited by the business association's use of bound innovation, which will help in the evaluation

of exchange at the pre-determined rate. This will aid in the control and direction of spending for

businesses in that field. A negative inflow of real money is forecasted over the next six months,

implying that the company would focus on increasing sales while cutting costs. Because there

will be negative cash inflows, it will be undeniably difficult for an organisation to survive on the

lookout and in that industry, as it will result in disappointment in the repayment of short- and

long-term obligations, and it will be an unusual test for Dysonica Plc. to complete its operational

exercises in a powerful and smooth manner (Zhu and Jiang, 2021). There is a cash surge that

should be visible in Dysonica Plc's income articulations, which can have an impact on the

organization's operations. If this continues, it will be difficult for any business operating in a

serious industry and across the globe to meet its obligation commitments and responsibilities,

whether they are short-term or long-term. The following document or report also provides

information on the incorporation of in numerous initiatives, which is causing Dysonica Plc's

expenses to rise, as well as causing losses to the companies. Despite the fact that the organisation

stock associations and determining which drives are at fault and costing the company money can

help minimise costs. They should execute their functional workouts at a consistent pace so that

their functional earnings remain positive over a longer period of time.

The absolute first portion of income from working exercises for a bookkeeping period shows

deals that begin in May and end in April, with an increase throughout the year. The

organization's expected income declarations reflect a strong and stable financial condition.

Dysonica Plc. can cover its short-term obligations without difficulty, and it has sufficient current

resources to address its long-term responsibilities. Additionally, the business plans can be seen,

indicating that the company is genuinely playing it straight when it comes to selling its products

and services and generating a significant amount of profit from transaction revenues. The total

cash inflow for the first year is estimated to be £ 2,465,187, which is the finest thing and also

allows Dysonica Plc a start and degree to open new speculating doors. Dysonica Plc. will benefit

greatly from increased interest in new resources as it expands its company and attracts a large

number of investors. It is clear from the predicted income justifications that Dysonica Plc. is

linked to unusual trade rates with countries such as China and the United Kingdom. As a result,

the expenditure incurred in this transaction is expected to reach a substantial level, which will be

limited by the business association's use of bound innovation, which will help in the evaluation

of exchange at the pre-determined rate. This will aid in the control and direction of spending for

businesses in that field. A negative inflow of real money is forecasted over the next six months,

implying that the company would focus on increasing sales while cutting costs. Because there

will be negative cash inflows, it will be undeniably difficult for an organisation to survive on the

lookout and in that industry, as it will result in disappointment in the repayment of short- and

long-term obligations, and it will be an unusual test for Dysonica Plc. to complete its operational

exercises in a powerful and smooth manner (Zhu and Jiang, 2021). There is a cash surge that

should be visible in Dysonica Plc's income articulations, which can have an impact on the

organization's operations. If this continues, it will be difficult for any business operating in a

serious industry and across the globe to meet its obligation commitments and responsibilities,

whether they are short-term or long-term. The following document or report also provides

information on the incorporation of in numerous initiatives, which is causing Dysonica Plc's

expenses to rise, as well as causing losses to the companies. Despite the fact that the organisation

has been observed to go to great measures to limit expenses, it still has to develop its contracts to

meet future vulnerabilities.

CONCLUSION

According to the preceding research, the company should profit from its assets in order to

stay up with its market alternative in the long run. Each company will choose money from a

variety of sources. Dysonica Plc. is a multinational corporation that operates in a variety of

countries and faces fierce competition. As a result, in order to counter its claims, it must present

each of its operations in a persuasive manner. Such businesses will use a variety of tools to save

costs and employ a large number of systems to increase revenue from sales activities. In

addition, the various types of costs, such as variable, fixed, and small expenses, are clearly

defined. This study has also provided an unmistakable demonstration of the most effective

approach for predicting a business concern's future monetary potential and ability to satisfy its

upcoming needs and requirements. Minor costing and movement-based costing are two

incredibly unique approaches for Dysonica Plc to save unnecessary expenses and capitalise on an

of cost that is associated or connected with various types of activities in distinct offices.

meet future vulnerabilities.

CONCLUSION

According to the preceding research, the company should profit from its assets in order to

stay up with its market alternative in the long run. Each company will choose money from a

variety of sources. Dysonica Plc. is a multinational corporation that operates in a variety of

countries and faces fierce competition. As a result, in order to counter its claims, it must present

each of its operations in a persuasive manner. Such businesses will use a variety of tools to save

costs and employ a large number of systems to increase revenue from sales activities. In

addition, the various types of costs, such as variable, fixed, and small expenses, are clearly

defined. This study has also provided an unmistakable demonstration of the most effective

approach for predicting a business concern's future monetary potential and ability to satisfy its

upcoming needs and requirements. Minor costing and movement-based costing are two

incredibly unique approaches for Dysonica Plc to save unnecessary expenses and capitalise on an

of cost that is associated or connected with various types of activities in distinct offices.

REFERENCES

Books and Journals

Anghelache, C. and et.al., 2019. Target Costing and Its Impact on Business Strategy: Computer

Program for Cost Accounting and Administration. In Network Security and Its Impact

on Business Strategy (pp. 20-43). IGI Global.

Feyaerts, D. and Demarsin, S., 2020. Development of a management cost accounting tool for the

benelux market leader in the door manufacturing industry.

Flaah, H.J., 2020. A suggested model for the application of resource consumption accounting

approach in the oil refining industry Applied study in south refineries

company. Managerial Studies Journal, 13(27).

Hilorme, T. and et.al., 2019. Human capital cost accounting in the company management

system. Academy of Accounting and Financial Studies Journal, 23, pp.1-6.

Mazahrih, B., 2019. Integration of environmental costs into accounting information

system. Academy of Accounting and Financial Studies Journal, 23(4), pp.1-20.

Nguyen, D.T.T., 2018. Is Japanese Material Flow Cost Accounting useful to Vietnam? A case

study of a Vietnamese seafood processing company. In Accounting for Sustainability:

Asia Pacific Perspectives (pp. 237-258). Springer, Cham.

Persson, M.E., 2019. Special Characteristics of Accounting in Great Britain. In Harold Cecil

Edey: A Collection of Unpublished Material from a 20th Century Accounting Reformer.

Emerald Publishing Limited. Persson, M.E., 2019. Special Characteristics of

Accounting in Great Britain. In Harold Cecil Edey: A Collection of Unpublished

Material from a 20th Century Accounting Reformer. Emerald Publishing Limited.

Scerri, C., 2021. The applicability of management accounting techniques when launching a new

product (Master's thesis, University of Malta).

Zakieva, L.B. and Sokolov, A.Y., 2019. JIT philosophy in modern management cost accounting

and performance management systems. Administrative Consulting.

Zhaolei, W. and Lei, Z., 2021, February. Manufacturing Cost Accounting Method under

Accounting Informationization. In 2021 International Conference on Public

Management and Intelligent Society (PMIS) (pp. 111-114). IEEE.

Zhu, X. and Jiang, Y., 2021. RETRACTED ARTICLE: Coastal biometric recognition based on

virtual sensor network and accounting cost accounting of logistics companies. Arabian

Journal of Geosciences, 14(17), pp.1-17.

Books and Journals

Anghelache, C. and et.al., 2019. Target Costing and Its Impact on Business Strategy: Computer

Program for Cost Accounting and Administration. In Network Security and Its Impact

on Business Strategy (pp. 20-43). IGI Global.

Feyaerts, D. and Demarsin, S., 2020. Development of a management cost accounting tool for the

benelux market leader in the door manufacturing industry.

Flaah, H.J., 2020. A suggested model for the application of resource consumption accounting

approach in the oil refining industry Applied study in south refineries

company. Managerial Studies Journal, 13(27).

Hilorme, T. and et.al., 2019. Human capital cost accounting in the company management

system. Academy of Accounting and Financial Studies Journal, 23, pp.1-6.

Mazahrih, B., 2019. Integration of environmental costs into accounting information

system. Academy of Accounting and Financial Studies Journal, 23(4), pp.1-20.

Nguyen, D.T.T., 2018. Is Japanese Material Flow Cost Accounting useful to Vietnam? A case

study of a Vietnamese seafood processing company. In Accounting for Sustainability:

Asia Pacific Perspectives (pp. 237-258). Springer, Cham.

Persson, M.E., 2019. Special Characteristics of Accounting in Great Britain. In Harold Cecil

Edey: A Collection of Unpublished Material from a 20th Century Accounting Reformer.

Emerald Publishing Limited. Persson, M.E., 2019. Special Characteristics of

Accounting in Great Britain. In Harold Cecil Edey: A Collection of Unpublished

Material from a 20th Century Accounting Reformer. Emerald Publishing Limited.

Scerri, C., 2021. The applicability of management accounting techniques when launching a new

product (Master's thesis, University of Malta).

Zakieva, L.B. and Sokolov, A.Y., 2019. JIT philosophy in modern management cost accounting

and performance management systems. Administrative Consulting.

Zhaolei, W. and Lei, Z., 2021, February. Manufacturing Cost Accounting Method under

Accounting Informationization. In 2021 International Conference on Public

Management and Intelligent Society (PMIS) (pp. 111-114). IEEE.

Zhu, X. and Jiang, Y., 2021. RETRACTED ARTICLE: Coastal biometric recognition based on

virtual sensor network and accounting cost accounting of logistics companies. Arabian

Journal of Geosciences, 14(17), pp.1-17.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.