Microeconomics and Profit Maximization

VerifiedAdded on 2020/03/04

|13

|2040

|45

AI Summary

This assignment delves into microeconomics concepts to analyze a gardening company's profit maximization strategy. It examines their cost structure, including average variable cost, average total cost, and marginal cost. The analysis incorporates the concept of marginal revenue and applies it within the framework of a perfectly competitive market. Students are expected to determine the optimal production level for the company based on these microeconomic principles.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ECONOMIC ASSIGNMENT

Economic Assignment

Name of the Student

Name of the University

Author note

Economic Assignment

Name of the Student

Name of the University

Author note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1ECONOMIC ASSIGNMENT

Table of Contents

Answer 1..........................................................................................................................................2

Answer 2..........................................................................................................................................4

Answer 3..........................................................................................................................................7

Answer 4..........................................................................................................................................8

Answer 5........................................................................................................................................10

References......................................................................................................................................12

Table of Contents

Answer 1..........................................................................................................................................2

Answer 2..........................................................................................................................................4

Answer 3..........................................................................................................................................7

Answer 4..........................................................................................................................................8

Answer 5........................................................................................................................................10

References......................................................................................................................................12

2ECONOMIC ASSIGNMENT

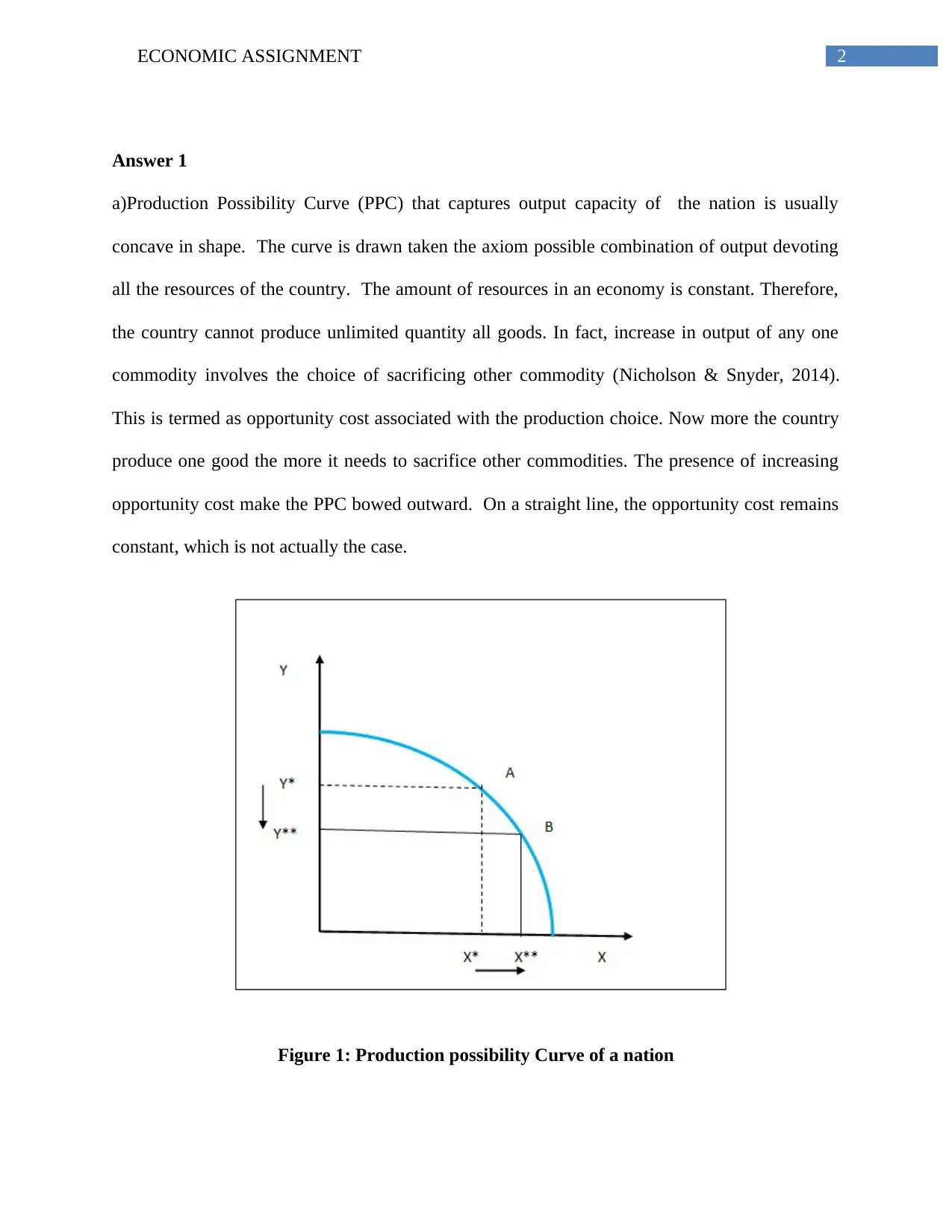

Answer 1

a)Production Possibility Curve (PPC) that captures output capacity of the nation is usually

concave in shape. The curve is drawn taken the axiom possible combination of output devoting

all the resources of the country. The amount of resources in an economy is constant. Therefore,

the country cannot produce unlimited quantity all goods. In fact, increase in output of any one

commodity involves the choice of sacrificing other commodity (Nicholson & Snyder, 2014).

This is termed as opportunity cost associated with the production choice. Now more the country

produce one good the more it needs to sacrifice other commodities. The presence of increasing

opportunity cost make the PPC bowed outward. On a straight line, the opportunity cost remains

constant, which is not actually the case.

Figure 1: Production possibility Curve of a nation

Answer 1

a)Production Possibility Curve (PPC) that captures output capacity of the nation is usually

concave in shape. The curve is drawn taken the axiom possible combination of output devoting

all the resources of the country. The amount of resources in an economy is constant. Therefore,

the country cannot produce unlimited quantity all goods. In fact, increase in output of any one

commodity involves the choice of sacrificing other commodity (Nicholson & Snyder, 2014).

This is termed as opportunity cost associated with the production choice. Now more the country

produce one good the more it needs to sacrifice other commodities. The presence of increasing

opportunity cost make the PPC bowed outward. On a straight line, the opportunity cost remains

constant, which is not actually the case.

Figure 1: Production possibility Curve of a nation

3ECONOMIC ASSIGNMENT

(Source: as created by Author)

The above figure describes the production possibility frontier of a nation assuming the

economy produces only two goods X and Y. Increase in production of X from X* to X**

involves decrease in consumption of Y from Y* to Y**.

b) The basic problem of the economy is limited means and unlimited wants. This creates scarcity

problem in the economy (Krosch & Amodio, 2014). People always have to sacrifice some

choice to opt some their choice. It is not about the problem of a single economic agent. Rather it

is the problem of the whole economy. Jane who was unemployed for nearly a year may suffer

from the problem of monetary scarcity. When Jane gets a high paying job it may solve his

monetary problem but cannot solve the choice problem. Thus, he never gets rid off the problem

of economic scarcity.

c) Every economy operates in a way such that is can minimize the scarcity problem. The

economy tries to optimum decision that will lead to efficient allocation its scarce resources. In

some economy the economic decision is taken by a central power while in some other it is left on

free market economy (Koo & Perkins, 2016). The economy where the central power exists and

takes decision on behalf of economic agents is known as socialist economy. In economy where

different economic agents as consumers and producers take independent decision to maximize,

their welfare is called capitalist or free market economy. In addition, there can be a combination

of these two types of economy known as mixed economy.

Economic system refers to the management of production, consumption and distribution

of goods and services in the economy. The economy in the United States is an example of mixed

economy. In US, there are both public and privately owned enterprises (Sutton, 2017). The

(Source: as created by Author)

The above figure describes the production possibility frontier of a nation assuming the

economy produces only two goods X and Y. Increase in production of X from X* to X**

involves decrease in consumption of Y from Y* to Y**.

b) The basic problem of the economy is limited means and unlimited wants. This creates scarcity

problem in the economy (Krosch & Amodio, 2014). People always have to sacrifice some

choice to opt some their choice. It is not about the problem of a single economic agent. Rather it

is the problem of the whole economy. Jane who was unemployed for nearly a year may suffer

from the problem of monetary scarcity. When Jane gets a high paying job it may solve his

monetary problem but cannot solve the choice problem. Thus, he never gets rid off the problem

of economic scarcity.

c) Every economy operates in a way such that is can minimize the scarcity problem. The

economy tries to optimum decision that will lead to efficient allocation its scarce resources. In

some economy the economic decision is taken by a central power while in some other it is left on

free market economy (Koo & Perkins, 2016). The economy where the central power exists and

takes decision on behalf of economic agents is known as socialist economy. In economy where

different economic agents as consumers and producers take independent decision to maximize,

their welfare is called capitalist or free market economy. In addition, there can be a combination

of these two types of economy known as mixed economy.

Economic system refers to the management of production, consumption and distribution

of goods and services in the economy. The economy in the United States is an example of mixed

economy. In US, there are both public and privately owned enterprises (Sutton, 2017). The

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4ECONOMIC ASSIGNMENT

government controls resource allocation in public sectors and controls the necessary production

of the economy. Food stamps are provided people to meet their need for food demand. In order

to fulfill the basic needs of the people with scarce resources government grants aid for house,

health and other benefits. For other sector, the economy relies on free market economy for

efficient resource allocation.

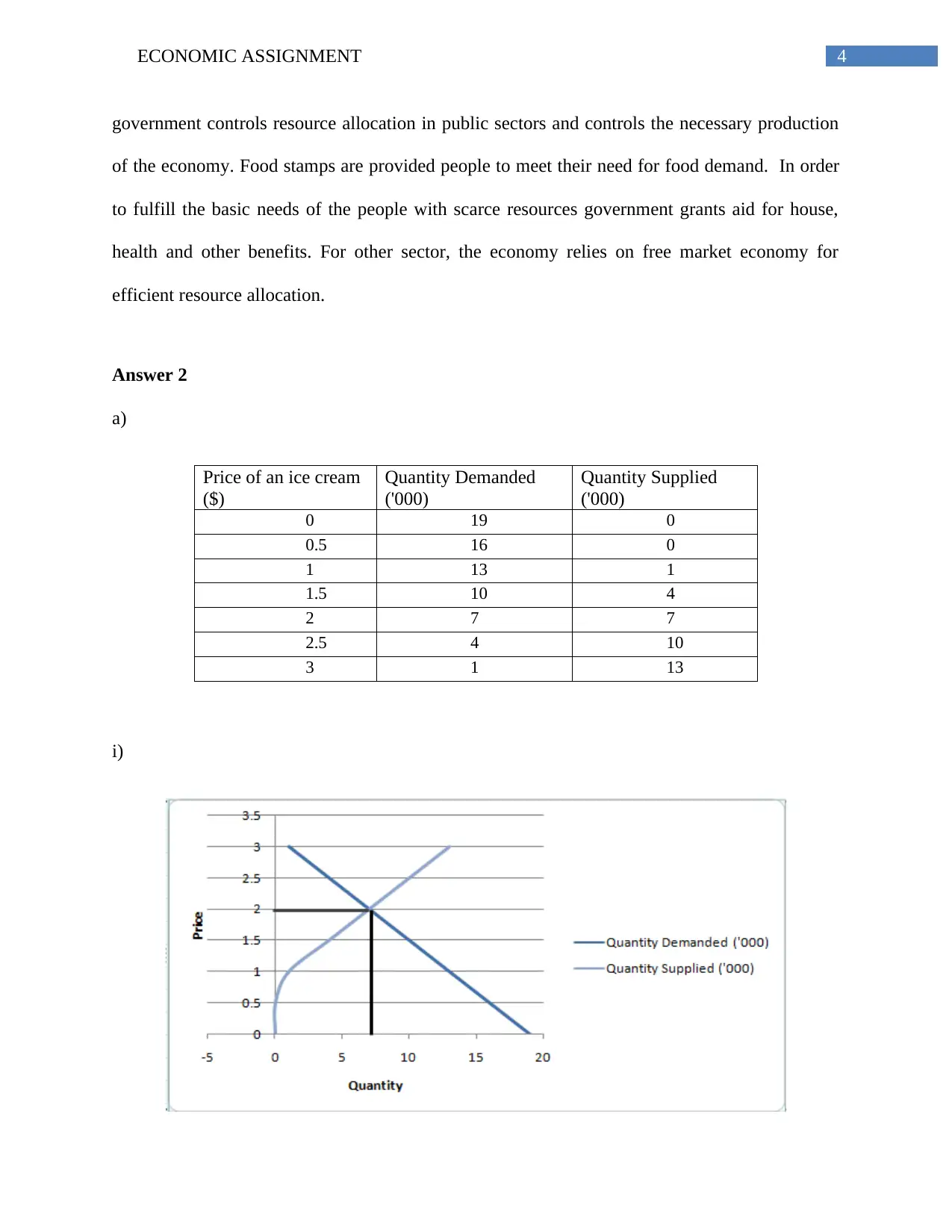

Answer 2

a)

Price of an ice cream

($)

Quantity Demanded

('000)

Quantity Supplied

('000)

0 19 0

0.5 16 0

1 13 1

1.5 10 4

2 7 7

2.5 4 10

3 1 13

i)

government controls resource allocation in public sectors and controls the necessary production

of the economy. Food stamps are provided people to meet their need for food demand. In order

to fulfill the basic needs of the people with scarce resources government grants aid for house,

health and other benefits. For other sector, the economy relies on free market economy for

efficient resource allocation.

Answer 2

a)

Price of an ice cream

($)

Quantity Demanded

('000)

Quantity Supplied

('000)

0 19 0

0.5 16 0

1 13 1

1.5 10 4

2 7 7

2.5 4 10

3 1 13

i)

5ECONOMIC ASSIGNMENT

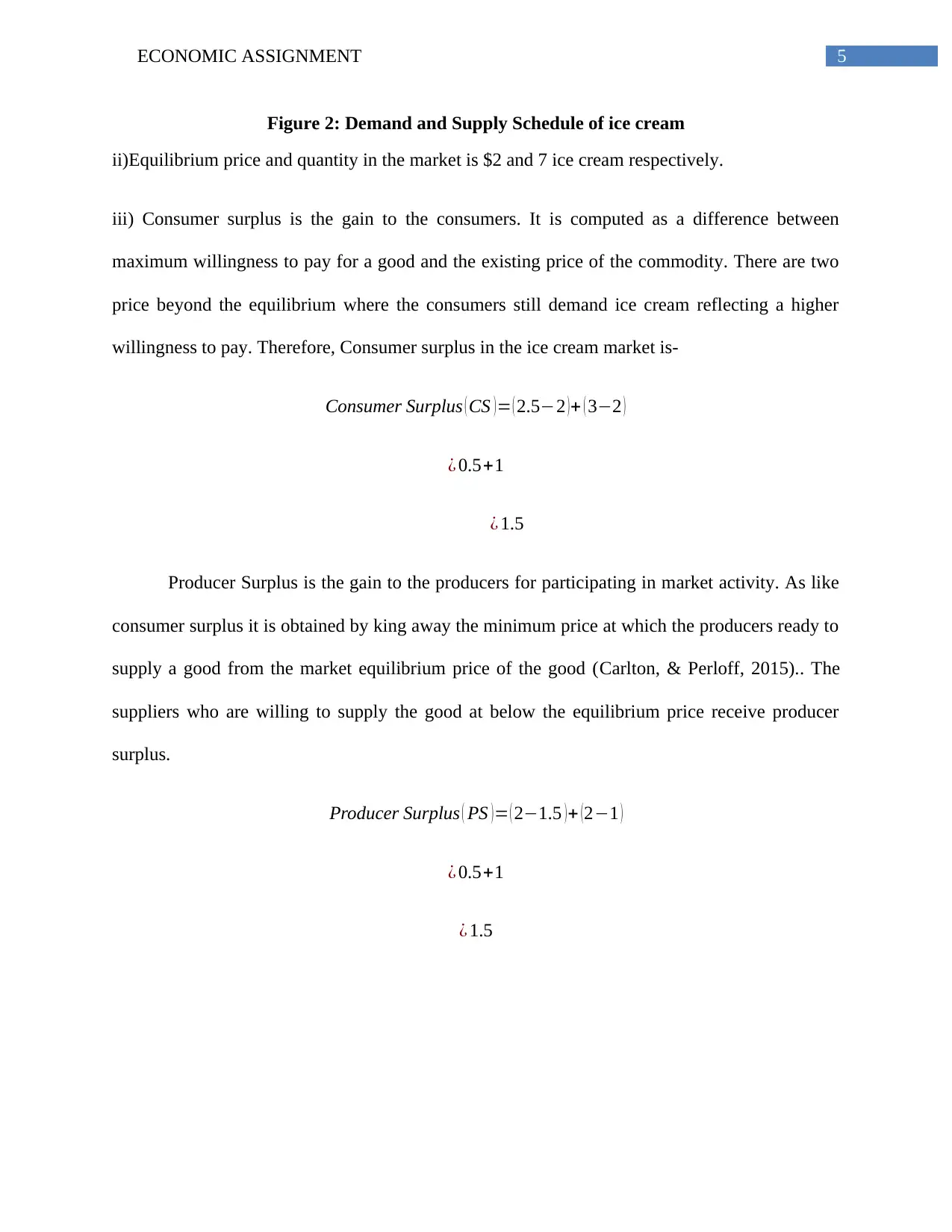

Figure 2: Demand and Supply Schedule of ice cream

ii)Equilibrium price and quantity in the market is $2 and 7 ice cream respectively.

iii) Consumer surplus is the gain to the consumers. It is computed as a difference between

maximum willingness to pay for a good and the existing price of the commodity. There are two

price beyond the equilibrium where the consumers still demand ice cream reflecting a higher

willingness to pay. Therefore, Consumer surplus in the ice cream market is-

Consumer Surplus ( CS )= ( 2.5−2 )+ ( 3−2 )

¿ 0.5+1

¿ 1.5

Producer Surplus is the gain to the producers for participating in market activity. As like

consumer surplus it is obtained by king away the minimum price at which the producers ready to

supply a good from the market equilibrium price of the good (Carlton, & Perloff, 2015).. The

suppliers who are willing to supply the good at below the equilibrium price receive producer

surplus.

Producer Surplus ( PS )= ( 2−1.5 )+ (2−1 )

¿ 0.5+1

¿ 1.5

Figure 2: Demand and Supply Schedule of ice cream

ii)Equilibrium price and quantity in the market is $2 and 7 ice cream respectively.

iii) Consumer surplus is the gain to the consumers. It is computed as a difference between

maximum willingness to pay for a good and the existing price of the commodity. There are two

price beyond the equilibrium where the consumers still demand ice cream reflecting a higher

willingness to pay. Therefore, Consumer surplus in the ice cream market is-

Consumer Surplus ( CS )= ( 2.5−2 )+ ( 3−2 )

¿ 0.5+1

¿ 1.5

Producer Surplus is the gain to the producers for participating in market activity. As like

consumer surplus it is obtained by king away the minimum price at which the producers ready to

supply a good from the market equilibrium price of the good (Carlton, & Perloff, 2015).. The

suppliers who are willing to supply the good at below the equilibrium price receive producer

surplus.

Producer Surplus ( PS )= ( 2−1.5 )+ (2−1 )

¿ 0.5+1

¿ 1.5

6ECONOMIC ASSIGNMENT

iv)

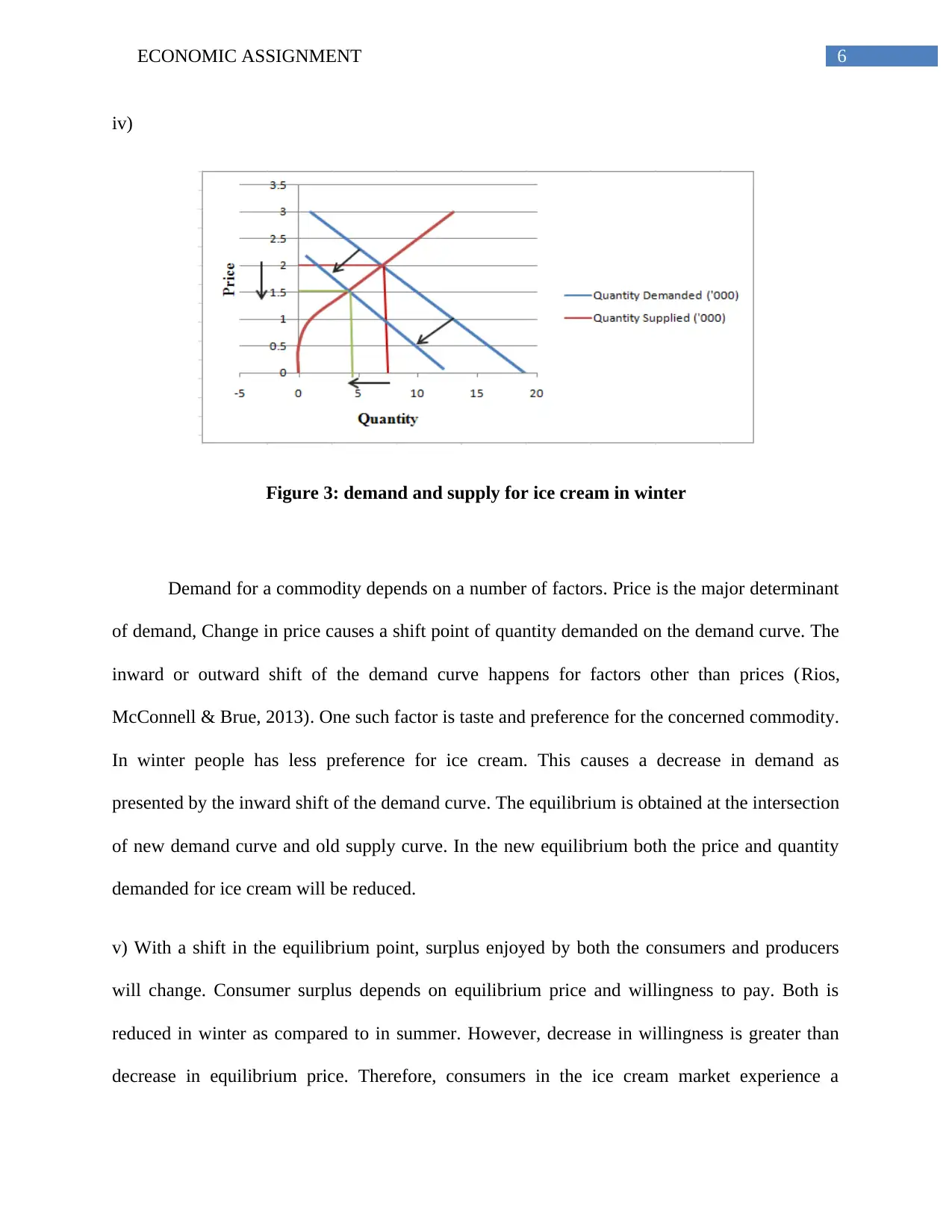

Figure 3: demand and supply for ice cream in winter

Demand for a commodity depends on a number of factors. Price is the major determinant

of demand, Change in price causes a shift point of quantity demanded on the demand curve. The

inward or outward shift of the demand curve happens for factors other than prices (Rios,

McConnell & Brue, 2013). One such factor is taste and preference for the concerned commodity.

In winter people has less preference for ice cream. This causes a decrease in demand as

presented by the inward shift of the demand curve. The equilibrium is obtained at the intersection

of new demand curve and old supply curve. In the new equilibrium both the price and quantity

demanded for ice cream will be reduced.

v) With a shift in the equilibrium point, surplus enjoyed by both the consumers and producers

will change. Consumer surplus depends on equilibrium price and willingness to pay. Both is

reduced in winter as compared to in summer. However, decrease in willingness is greater than

decrease in equilibrium price. Therefore, consumers in the ice cream market experience a

iv)

Figure 3: demand and supply for ice cream in winter

Demand for a commodity depends on a number of factors. Price is the major determinant

of demand, Change in price causes a shift point of quantity demanded on the demand curve. The

inward or outward shift of the demand curve happens for factors other than prices (Rios,

McConnell & Brue, 2013). One such factor is taste and preference for the concerned commodity.

In winter people has less preference for ice cream. This causes a decrease in demand as

presented by the inward shift of the demand curve. The equilibrium is obtained at the intersection

of new demand curve and old supply curve. In the new equilibrium both the price and quantity

demanded for ice cream will be reduced.

v) With a shift in the equilibrium point, surplus enjoyed by both the consumers and producers

will change. Consumer surplus depends on equilibrium price and willingness to pay. Both is

reduced in winter as compared to in summer. However, decrease in willingness is greater than

decrease in equilibrium price. Therefore, consumers in the ice cream market experience a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ECONOMIC ASSIGNMENT

reduction in consumer surplus. A reduction in equilibrium price along with change in the

willingness to supply reduces producer surplus as well.

Answer 3

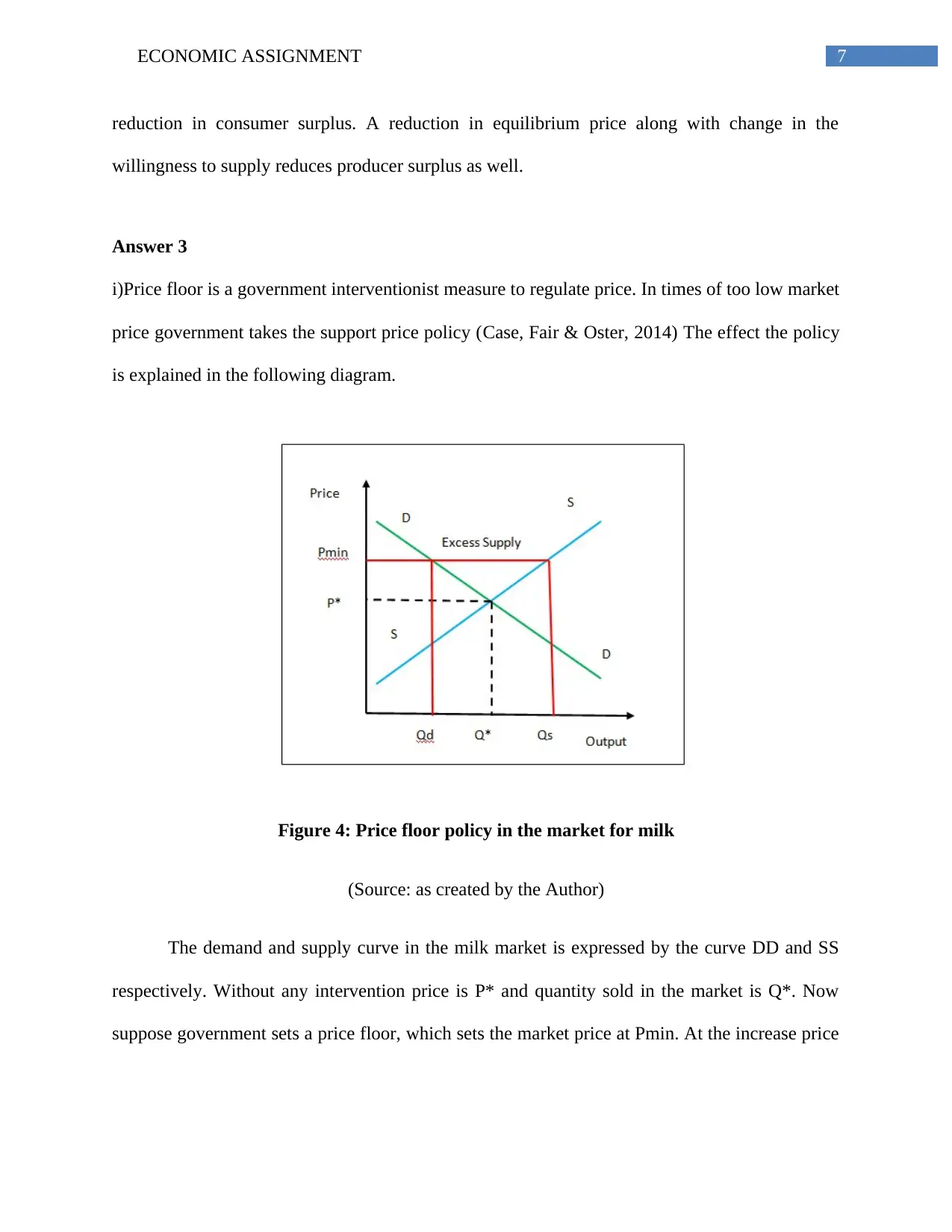

i)Price floor is a government interventionist measure to regulate price. In times of too low market

price government takes the support price policy (Case, Fair & Oster, 2014) The effect the policy

is explained in the following diagram.

Figure 4: Price floor policy in the market for milk

(Source: as created by the Author)

The demand and supply curve in the milk market is expressed by the curve DD and SS

respectively. Without any intervention price is P* and quantity sold in the market is Q*. Now

suppose government sets a price floor, which sets the market price at Pmin. At the increase price

reduction in consumer surplus. A reduction in equilibrium price along with change in the

willingness to supply reduces producer surplus as well.

Answer 3

i)Price floor is a government interventionist measure to regulate price. In times of too low market

price government takes the support price policy (Case, Fair & Oster, 2014) The effect the policy

is explained in the following diagram.

Figure 4: Price floor policy in the market for milk

(Source: as created by the Author)

The demand and supply curve in the milk market is expressed by the curve DD and SS

respectively. Without any intervention price is P* and quantity sold in the market is Q*. Now

suppose government sets a price floor, which sets the market price at Pmin. At the increase price

8ECONOMIC ASSIGNMENT

consumes decreases their demand whereas suppliers increase their supply. Consumers demanded

Qd amount of milk whereas in the market thee available supply is Qs.

ii)Price floor increase the price in the market. A higher price for the product increases revenue

earn from per unit of the product. This is likely to increase their income f it is possible to sell all

their product at the prevailing market price. Consumers in response to high price by shrinking

their demand as much as possible. Thus, fulfilling only the existing demand cannot assure the

farmers with an increased income.

iii) In order to assure the dairy farmers an increased income, government should purchase the

excess supplied quantity from the farmers. This costs heavily to the government. Government

can store this to the buffer stock. However, for non-durable goods like milk it is nit possible to

store for a long time. Thus, the government has to destroy it or sell it at a low price to elsewhere.

This ultimately causes a huge loss to the government. Therefore, it may not be a good decision to

purchase the entire surplus product. However, it increases income of the dairy farmers but

ultimately is results in a deadweight loss as net cost exceeds net benefit.

Answer 4

a)

Price(

P)

Quantity

(Q)

d

P

(P1+P2

)/2

% change in

price

d

Q

(Q1+Q2

)/2

% change in

quantity

Elastici

ty

2 10

3 8 1 2.5 40.00 2 9 22.22 0.56

4 6 1 3.5 28.57 2 7 28.57 1

5 4 1 4.5 22.22 2 5 40 1.80

consumes decreases their demand whereas suppliers increase their supply. Consumers demanded

Qd amount of milk whereas in the market thee available supply is Qs.

ii)Price floor increase the price in the market. A higher price for the product increases revenue

earn from per unit of the product. This is likely to increase their income f it is possible to sell all

their product at the prevailing market price. Consumers in response to high price by shrinking

their demand as much as possible. Thus, fulfilling only the existing demand cannot assure the

farmers with an increased income.

iii) In order to assure the dairy farmers an increased income, government should purchase the

excess supplied quantity from the farmers. This costs heavily to the government. Government

can store this to the buffer stock. However, for non-durable goods like milk it is nit possible to

store for a long time. Thus, the government has to destroy it or sell it at a low price to elsewhere.

This ultimately causes a huge loss to the government. Therefore, it may not be a good decision to

purchase the entire surplus product. However, it increases income of the dairy farmers but

ultimately is results in a deadweight loss as net cost exceeds net benefit.

Answer 4

a)

Price(

P)

Quantity

(Q)

d

P

(P1+P2

)/2

% change in

price

d

Q

(Q1+Q2

)/2

% change in

quantity

Elastici

ty

2 10

3 8 1 2.5 40.00 2 9 22.22 0.56

4 6 1 3.5 28.57 2 7 28.57 1

5 4 1 4.5 22.22 2 5 40 1.80

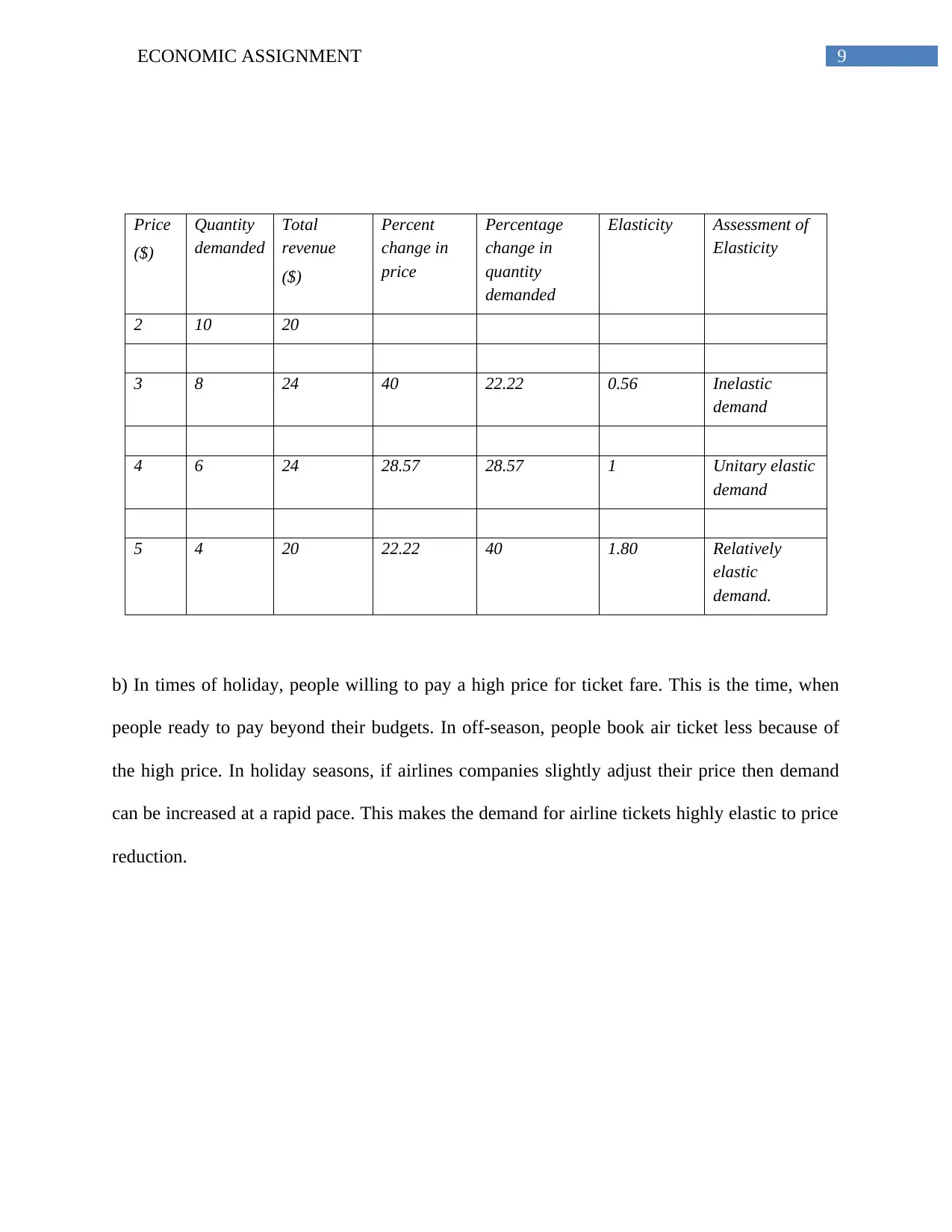

9ECONOMIC ASSIGNMENT

Price

($)

Quantity

demanded

Total

revenue

($)

Percent

change in

price

Percentage

change in

quantity

demanded

Elasticity Assessment of

Elasticity

2 10 20

3 8 24 40 22.22 0.56 Inelastic

demand

4 6 24 28.57 28.57 1 Unitary elastic

demand

5 4 20 22.22 40 1.80 Relatively

elastic

demand.

b) In times of holiday, people willing to pay a high price for ticket fare. This is the time, when

people ready to pay beyond their budgets. In off-season, people book air ticket less because of

the high price. In holiday seasons, if airlines companies slightly adjust their price then demand

can be increased at a rapid pace. This makes the demand for airline tickets highly elastic to price

reduction.

Price

($)

Quantity

demanded

Total

revenue

($)

Percent

change in

price

Percentage

change in

quantity

demanded

Elasticity Assessment of

Elasticity

2 10 20

3 8 24 40 22.22 0.56 Inelastic

demand

4 6 24 28.57 28.57 1 Unitary elastic

demand

5 4 20 22.22 40 1.80 Relatively

elastic

demand.

b) In times of holiday, people willing to pay a high price for ticket fare. This is the time, when

people ready to pay beyond their budgets. In off-season, people book air ticket less because of

the high price. In holiday seasons, if airlines companies slightly adjust their price then demand

can be increased at a rapid pace. This makes the demand for airline tickets highly elastic to price

reduction.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10ECONOMIC ASSIGNMENT

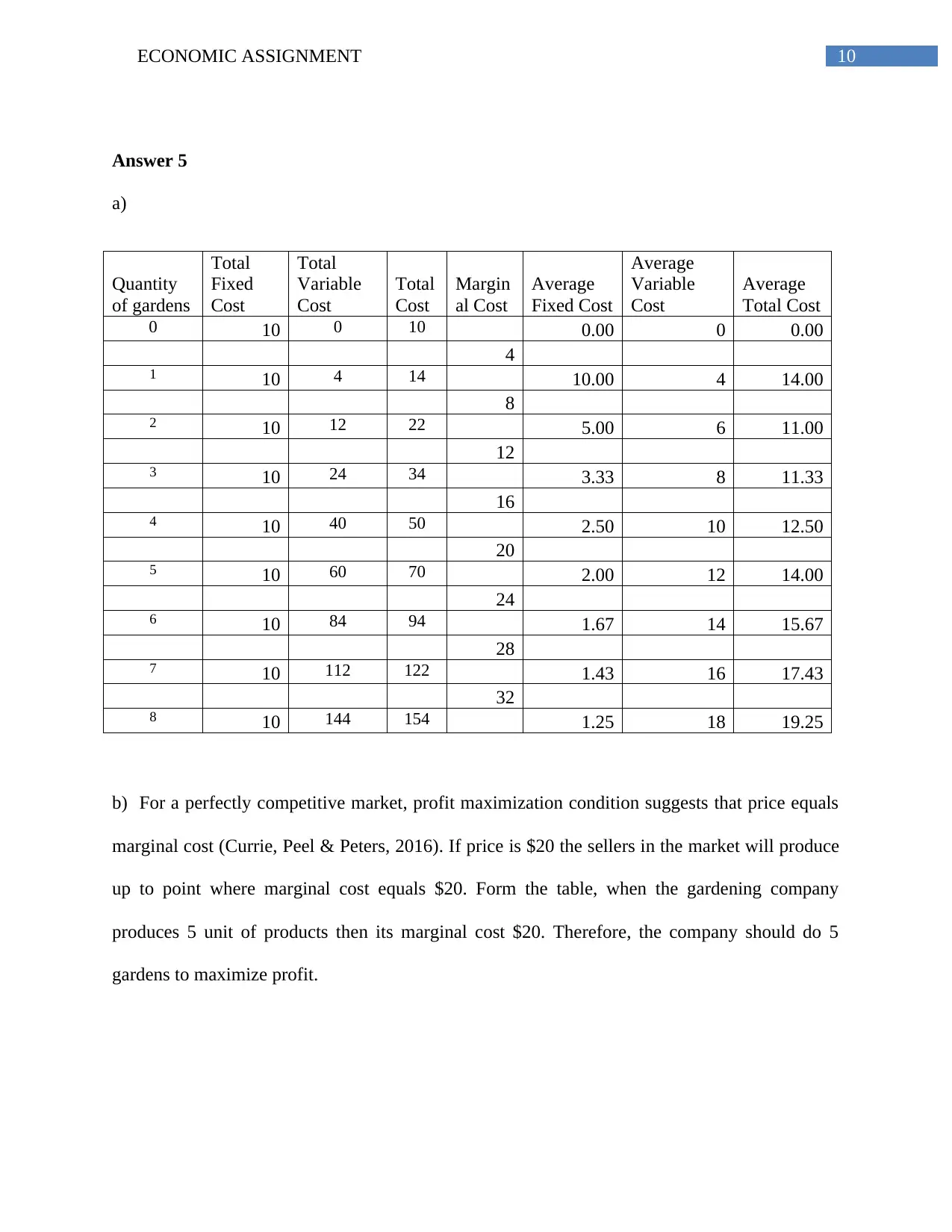

Answer 5

a)

Quantity

of gardens

Total

Fixed

Cost

Total

Variable

Cost

Total

Cost

Margin

al Cost

Average

Fixed Cost

Average

Variable

Cost

Average

Total Cost

0 10 0 10 0.00 0 0.00

4

1 10 4 14 10.00 4 14.00

8

2 10 12 22 5.00 6 11.00

12

3 10 24 34 3.33 8 11.33

16

4 10 40 50 2.50 10 12.50

20

5 10 60 70 2.00 12 14.00

24

6 10 84 94 1.67 14 15.67

28

7 10 112 122 1.43 16 17.43

32

8 10 144 154 1.25 18 19.25

b) For a perfectly competitive market, profit maximization condition suggests that price equals

marginal cost (Currie, Peel & Peters, 2016). If price is $20 the sellers in the market will produce

up to point where marginal cost equals $20. Form the table, when the gardening company

produces 5 unit of products then its marginal cost $20. Therefore, the company should do 5

gardens to maximize profit.

Answer 5

a)

Quantity

of gardens

Total

Fixed

Cost

Total

Variable

Cost

Total

Cost

Margin

al Cost

Average

Fixed Cost

Average

Variable

Cost

Average

Total Cost

0 10 0 10 0.00 0 0.00

4

1 10 4 14 10.00 4 14.00

8

2 10 12 22 5.00 6 11.00

12

3 10 24 34 3.33 8 11.33

16

4 10 40 50 2.50 10 12.50

20

5 10 60 70 2.00 12 14.00

24

6 10 84 94 1.67 14 15.67

28

7 10 112 122 1.43 16 17.43

32

8 10 144 154 1.25 18 19.25

b) For a perfectly competitive market, profit maximization condition suggests that price equals

marginal cost (Currie, Peel & Peters, 2016). If price is $20 the sellers in the market will produce

up to point where marginal cost equals $20. Form the table, when the gardening company

produces 5 unit of products then its marginal cost $20. Therefore, the company should do 5

gardens to maximize profit.

11ECONOMIC ASSIGNMENT

0 1 2 3 4 5 6 7 8 9

0

5

10

15

20

25

30

35

average variable cost

Average toital cost

Marginal cost

Output

Cost

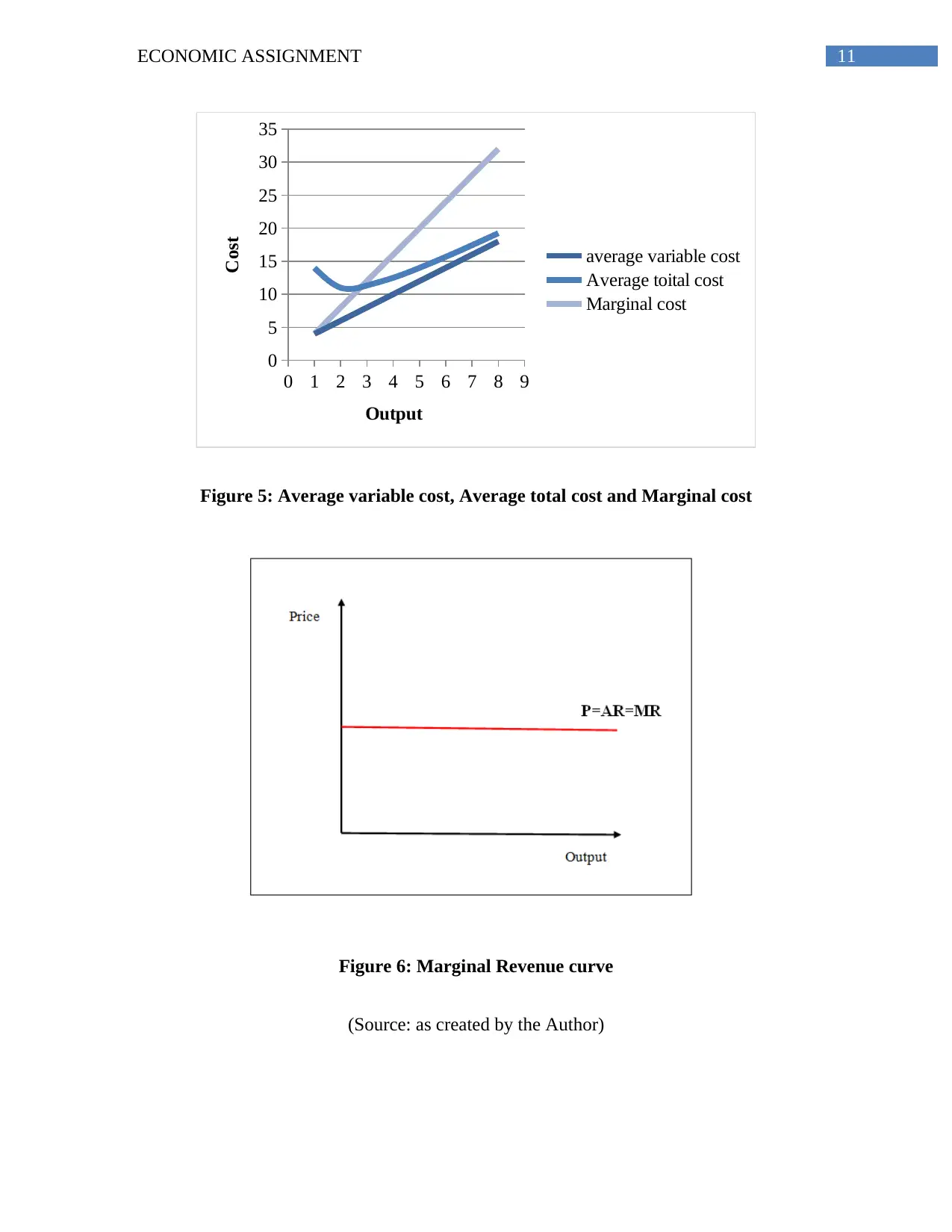

Figure 5: Average variable cost, Average total cost and Marginal cost

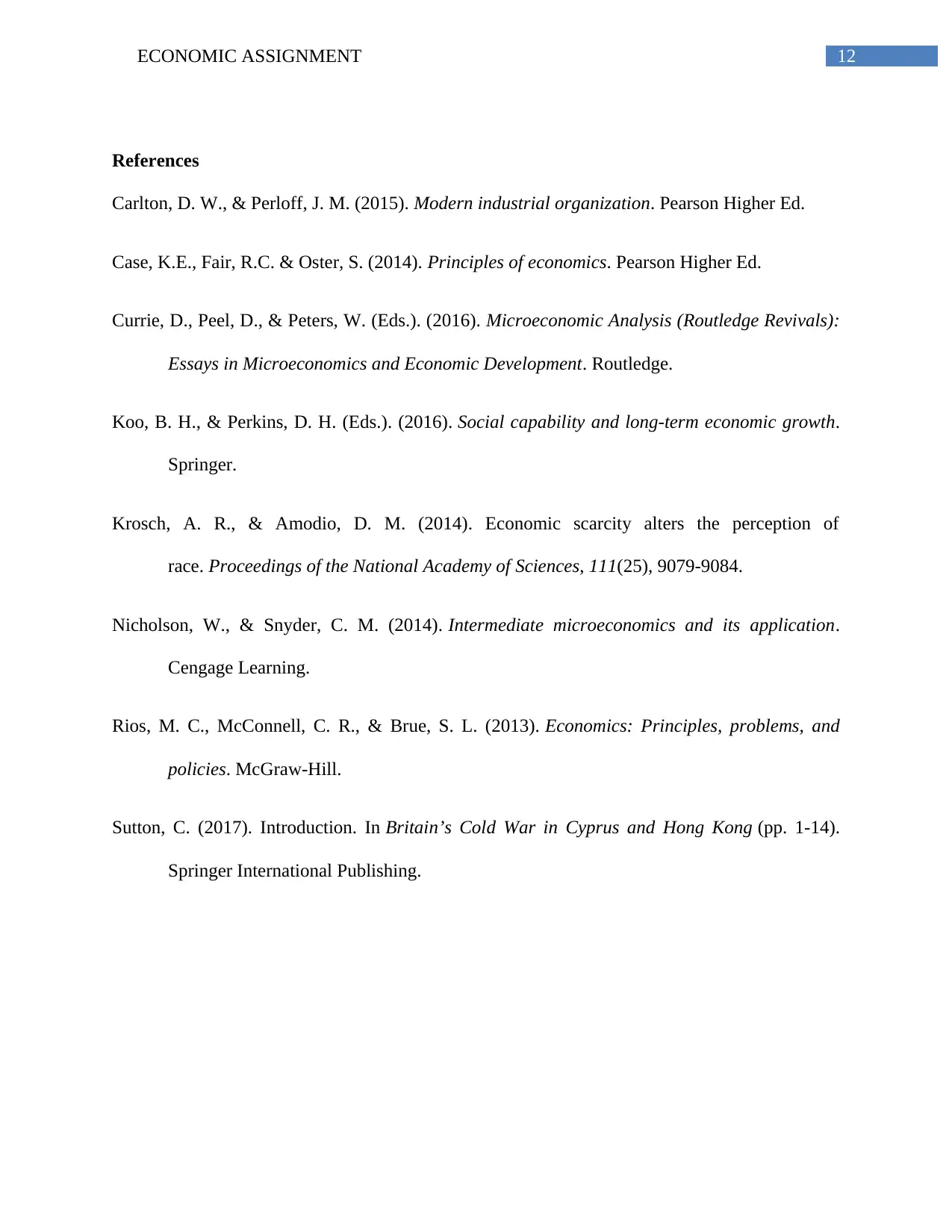

Figure 6: Marginal Revenue curve

(Source: as created by the Author)

0 1 2 3 4 5 6 7 8 9

0

5

10

15

20

25

30

35

average variable cost

Average toital cost

Marginal cost

Output

Cost

Figure 5: Average variable cost, Average total cost and Marginal cost

Figure 6: Marginal Revenue curve

(Source: as created by the Author)

12ECONOMIC ASSIGNMENT

References

Carlton, D. W., & Perloff, J. M. (2015). Modern industrial organization. Pearson Higher Ed.

Case, K.E., Fair, R.C. & Oster, S. (2014). Principles of economics. Pearson Higher Ed.

Currie, D., Peel, D., & Peters, W. (Eds.). (2016). Microeconomic Analysis (Routledge Revivals):

Essays in Microeconomics and Economic Development. Routledge.

Koo, B. H., & Perkins, D. H. (Eds.). (2016). Social capability and long-term economic growth.

Springer.

Krosch, A. R., & Amodio, D. M. (2014). Economic scarcity alters the perception of

race. Proceedings of the National Academy of Sciences, 111(25), 9079-9084.

Nicholson, W., & Snyder, C. M. (2014). Intermediate microeconomics and its application.

Cengage Learning.

Rios, M. C., McConnell, C. R., & Brue, S. L. (2013). Economics: Principles, problems, and

policies. McGraw-Hill.

Sutton, C. (2017). Introduction. In Britain’s Cold War in Cyprus and Hong Kong (pp. 1-14).

Springer International Publishing.

References

Carlton, D. W., & Perloff, J. M. (2015). Modern industrial organization. Pearson Higher Ed.

Case, K.E., Fair, R.C. & Oster, S. (2014). Principles of economics. Pearson Higher Ed.

Currie, D., Peel, D., & Peters, W. (Eds.). (2016). Microeconomic Analysis (Routledge Revivals):

Essays in Microeconomics and Economic Development. Routledge.

Koo, B. H., & Perkins, D. H. (Eds.). (2016). Social capability and long-term economic growth.

Springer.

Krosch, A. R., & Amodio, D. M. (2014). Economic scarcity alters the perception of

race. Proceedings of the National Academy of Sciences, 111(25), 9079-9084.

Nicholson, W., & Snyder, C. M. (2014). Intermediate microeconomics and its application.

Cengage Learning.

Rios, M. C., McConnell, C. R., & Brue, S. L. (2013). Economics: Principles, problems, and

policies. McGraw-Hill.

Sutton, C. (2017). Introduction. In Britain’s Cold War in Cyprus and Hong Kong (pp. 1-14).

Springer International Publishing.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.