ECON 1030 Business Statistics Project: Bitcoin and Market Securities

VerifiedAdded on 2022/12/22

|16

|3103

|68

Report

AI Summary

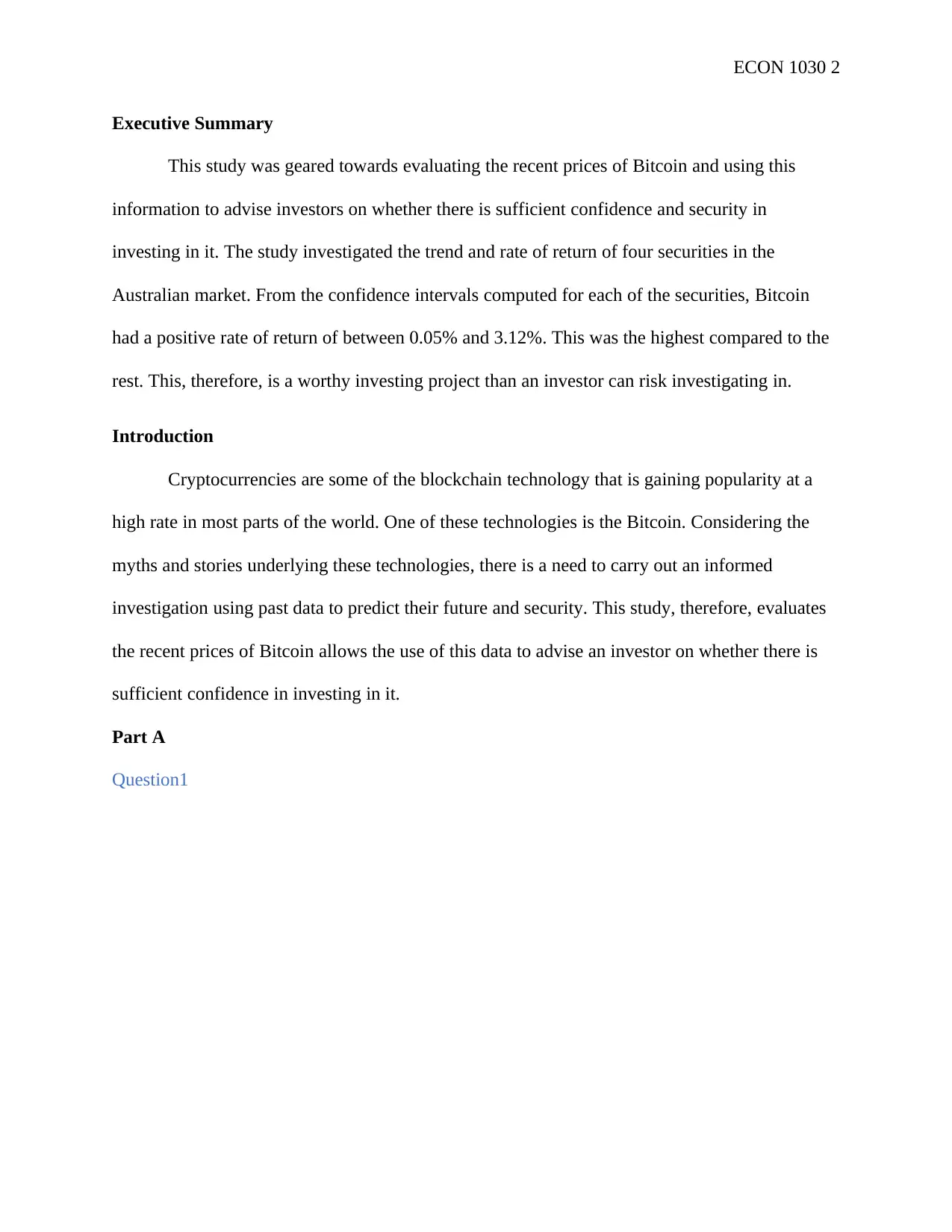

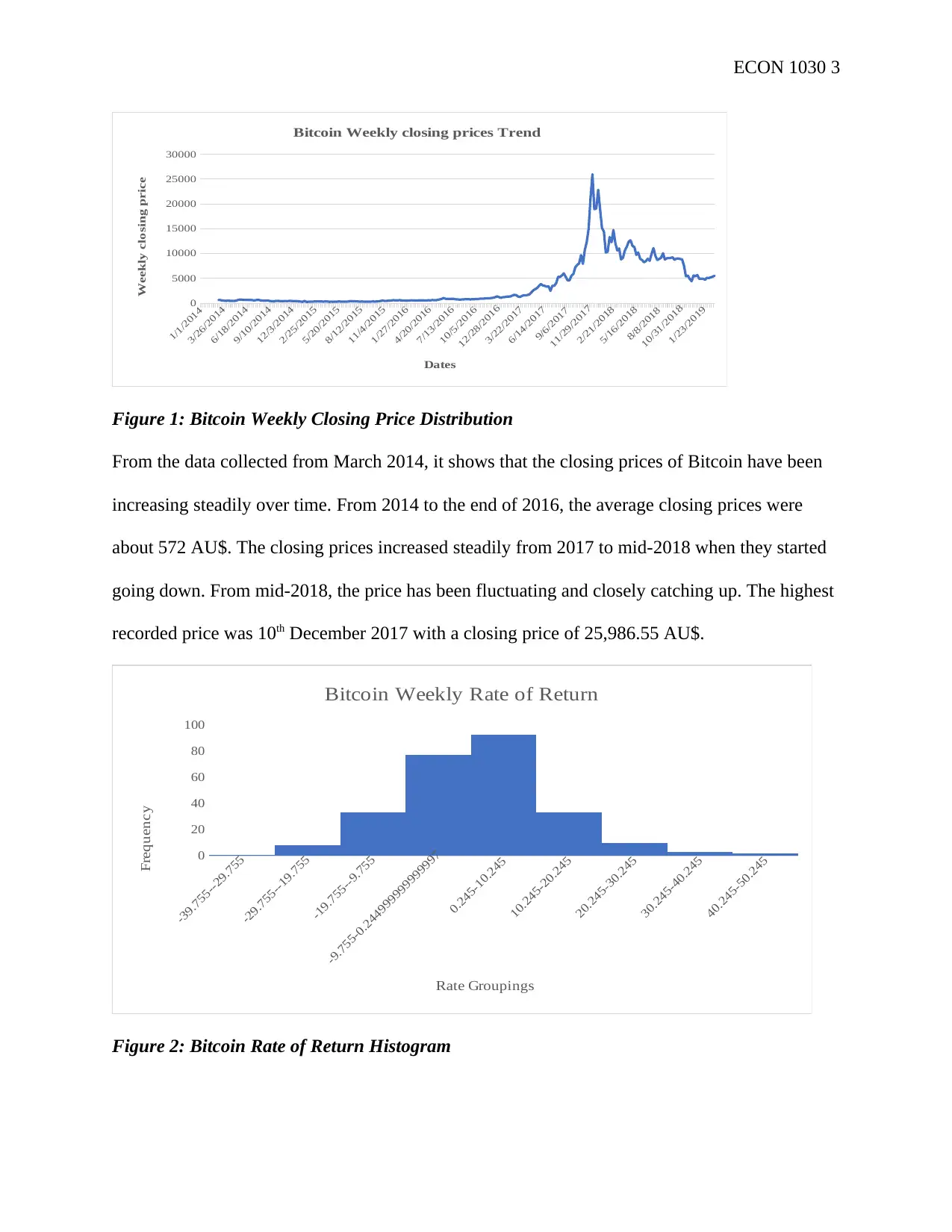

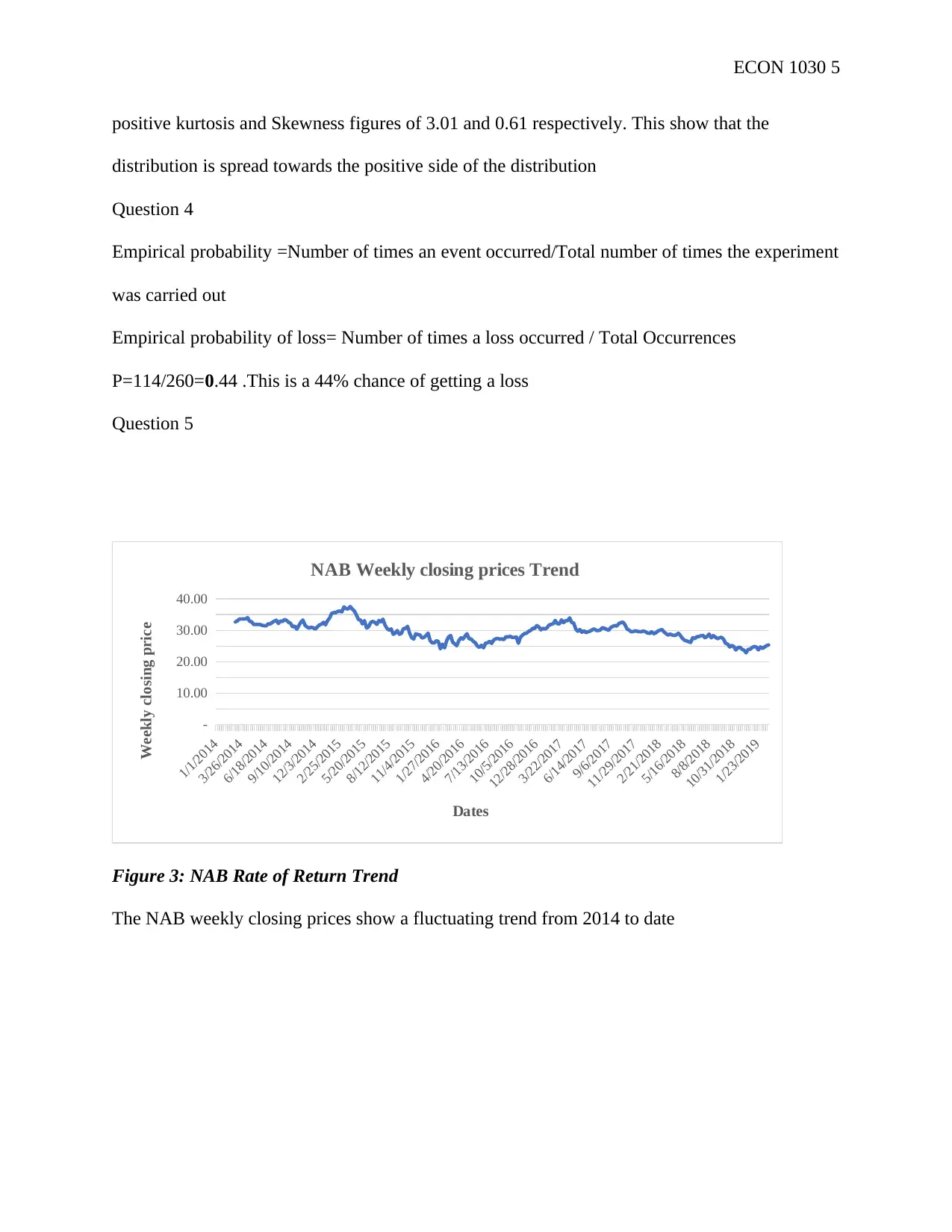

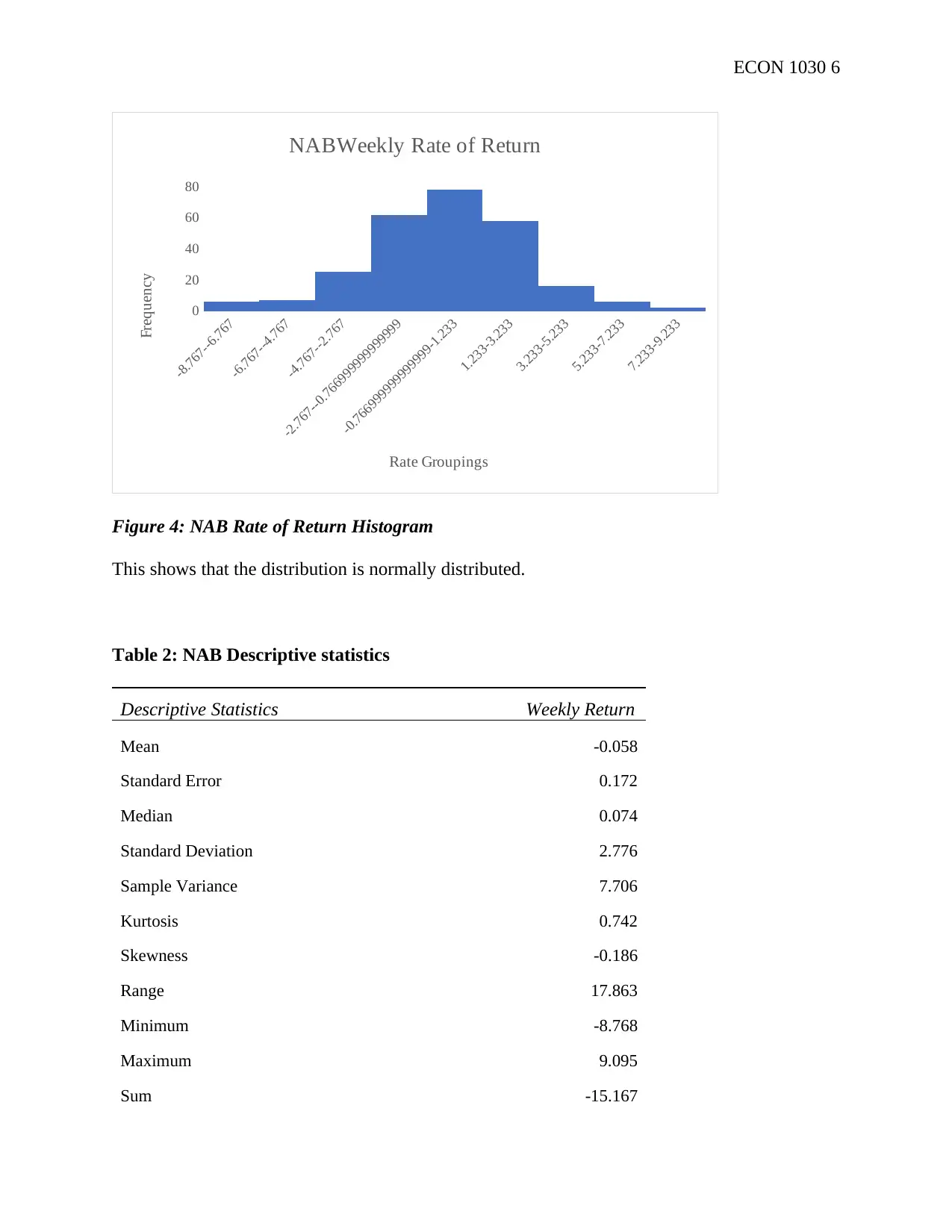

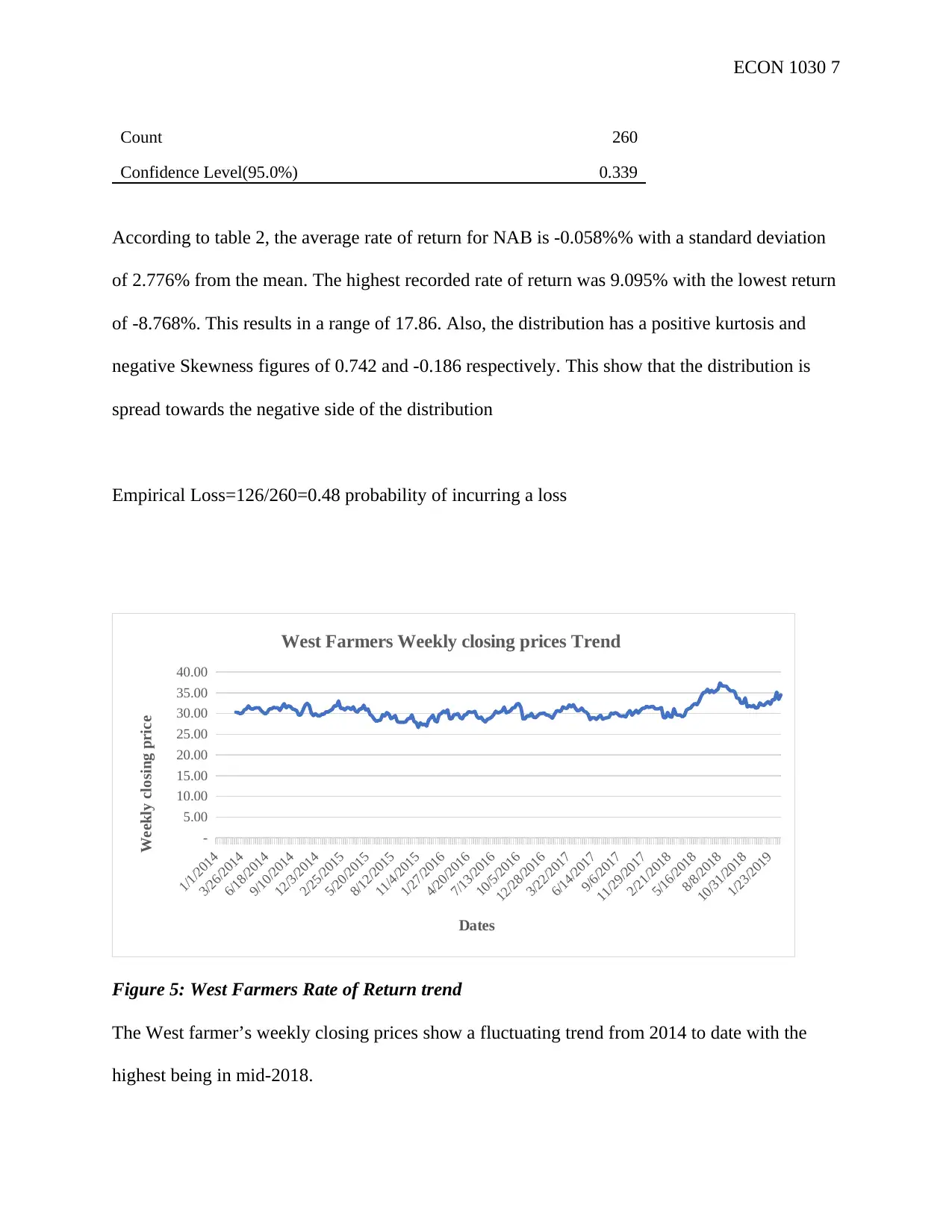

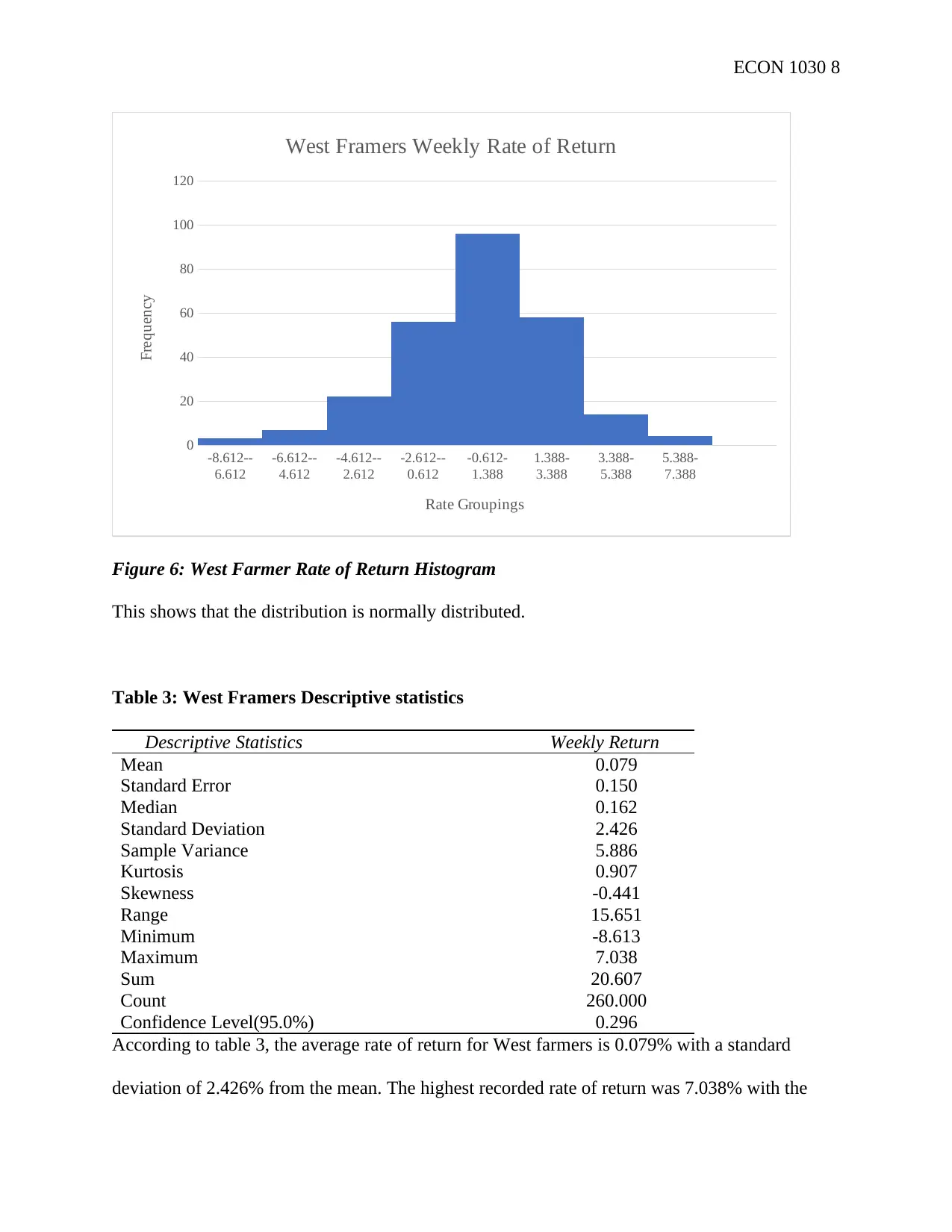

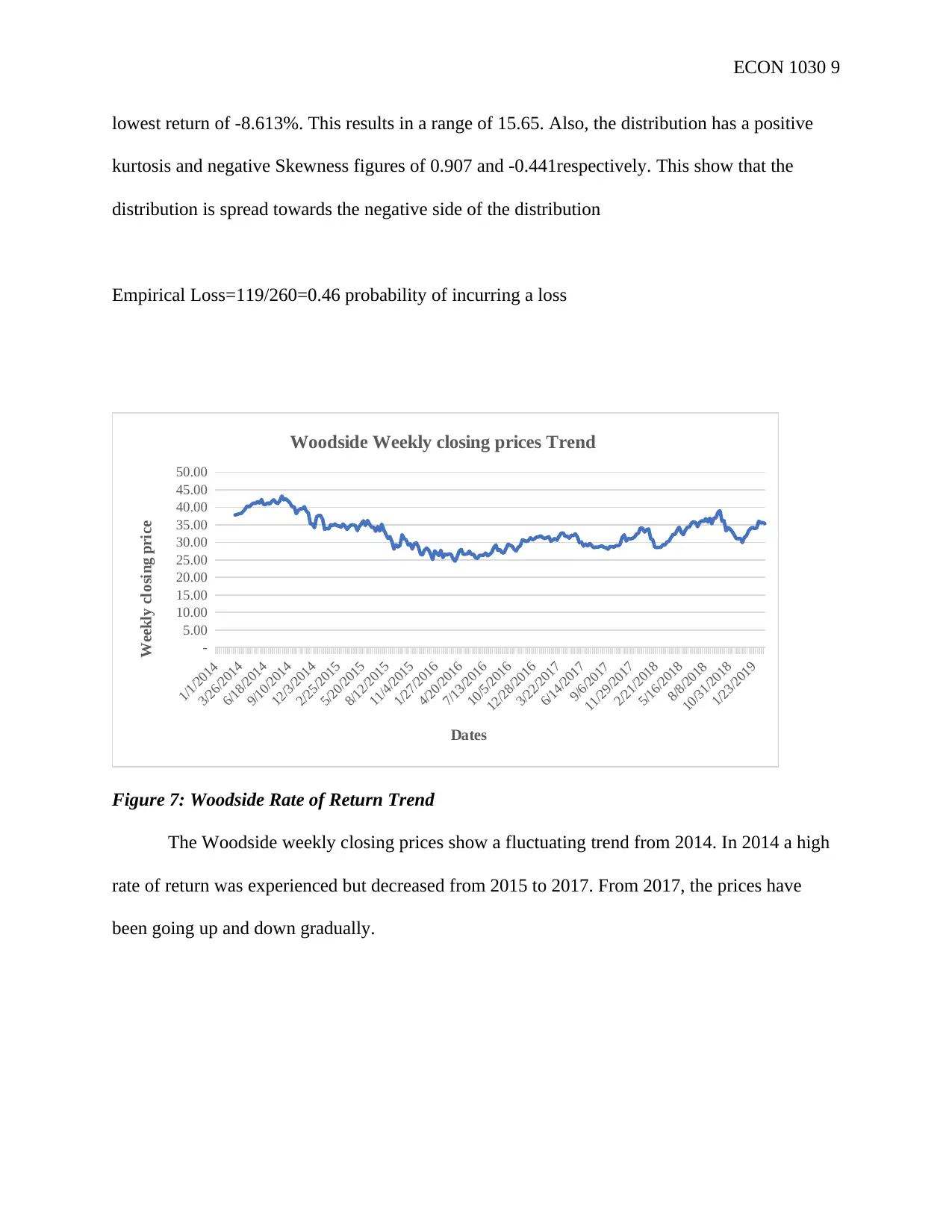

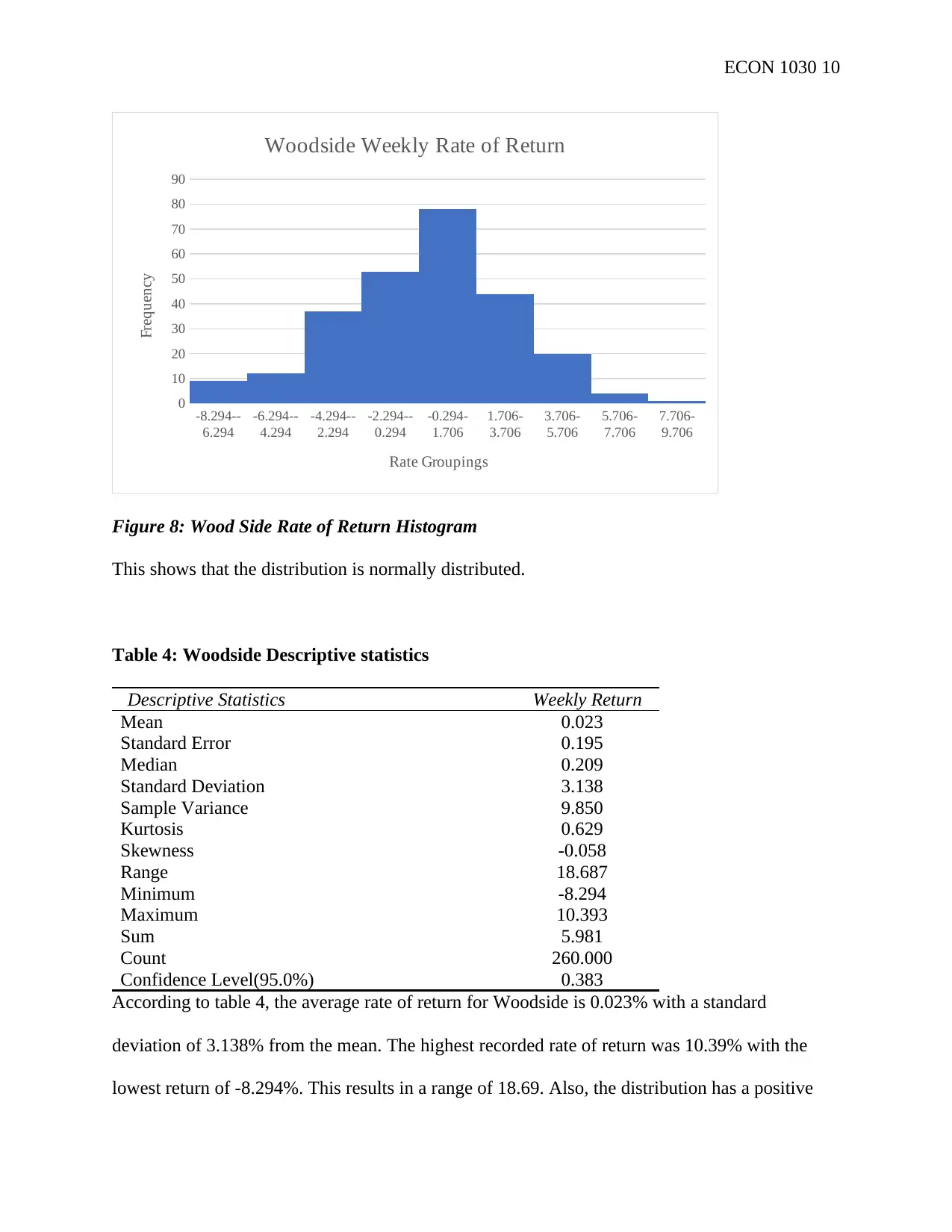

This ECON 1030 Business Statistics project evaluates the recent prices of Bitcoin to advise investors on its investment potential, analyzing data from the Australian market. The report includes a trend analysis of Bitcoin's weekly closing prices from 2014, demonstrating its fluctuating but generally increasing value, with a focus on its rate of return and descriptive statistics like mean, standard deviation, and empirical probability of loss. The project also compares Bitcoin's performance with other securities, such as NAB, West Farmers, and Woodside, examining their weekly closing prices, rate of return, and descriptive statistics. The study calculates confidence intervals for Bitcoin, revealing a positive rate of return, and concludes that Bitcoin is a worthy investment compared to the other securities. The project includes a ministerial brief summarizing the findings and providing recommendations based on the statistical analysis, including the results of the Micro-credential on cross-cultural communication.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.